CSX Corporation: The Epic Tale of America's Eastern Railroad Giant

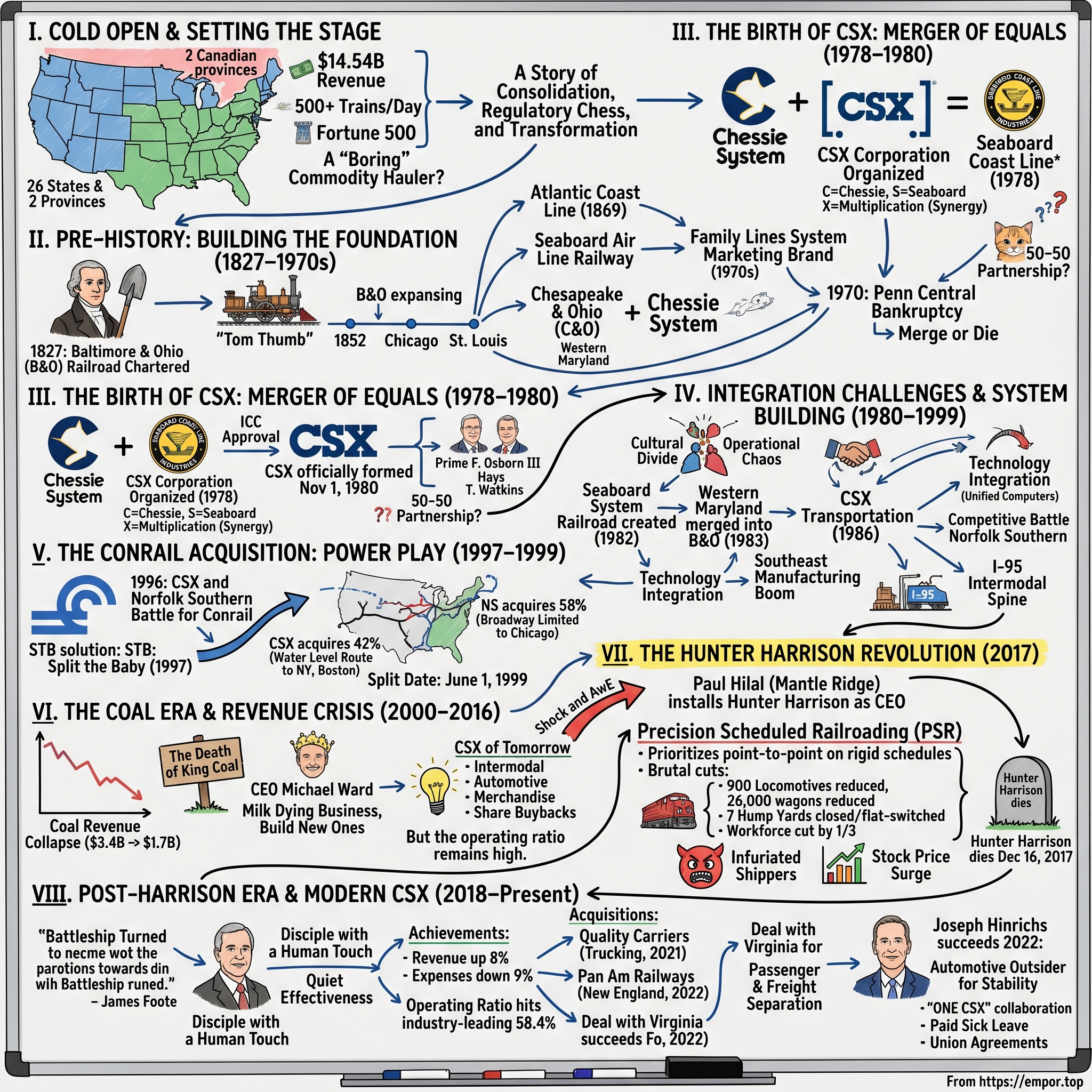

I. Cold Open & Setting the Stage

Picture this: Every single day, across 26 states and two Canadian provinces, a fleet of locomotives pulls 500 trains carrying everything from automobiles fresh off assembly lines to grain destined for export terminals. This vast network generates $14.54 billion in annual revenue, serves two-thirds of Americans living within its territory, and operates with the kind of margins that would make Silicon Valley jealous—39.1% operating margin in recent quarters. This is CSX Corporation, and if you've never heard of it, you're not alone. While tech giants dominate headlines, this 200-year-old business quietly moves the physical economy of the Eastern United States.

The paradox of CSX is striking. Here's a Fortune 500 company headquartered in Jacksonville, Florida, operating approximately 21,000 route miles of track—enough to circle the Earth nearly once—yet it trades at valuations that suggest the market views it as a boring, cyclical commodity hauler. The reality is far more nuanced. CSX is an infrastructure monopoly with network effects Warren Buffett would admire, operating in markets where the alternative—trucking—becomes less competitive every year due to driver shortages, emissions regulations, and highway congestion.

But the most fascinating aspect isn't the business model—it's the journey. How did a company formed through a 1978 merger experiment, widely predicted to fail due to cultural clashes and operational complexity, become the dominant force in Eastern U.S. rail freight? How did it survive the collapse of coal, its largest revenue source? And perhaps most intriguingly, how did a 73-year-old Canadian railroad executive named Hunter Harrison walk through the door in 2017 and completely transform a 40,000-person organization in less than a year before his sudden death?

This is a story of industrial consolidation on a massive scale, of regulatory chess matches that reshaped American commerce, and of operational transformations so radical they redefined an entire industry. It's also a story about timing—about being in the right place when manufacturing reshored to the Southeast, when intermodal shipping revolutionized logistics, and when environmental concerns made rail's fuel efficiency a competitive superpower.

What we're about to explore isn't just corporate history—it's the hidden infrastructure of American capitalism, the rails that literally and figuratively connect producers to consumers, ports to factories, farms to tables. Along the way, we'll uncover how a series of bold bets, near-death experiences, and one extremely controversial management philosophy created one of the most efficient transportation networks on the planet.

II. The Pre-History: Building the Foundation (1827–1970s)

The July 4, 1828 ceremony was more theater than transportation. Charles Carroll, at 91 years old and the last surviving signer of the Declaration of Independence, lifted the ceremonial spade to break ground for America's railroad age. The symbolism was unmistakable—the man who helped birth the nation was now launching its industrial transformation. The first stone for the line was laid on July 4, 1828, by Charles Carroll, the American Revolutionary leader and last surviving signer of the Declaration of Independence. But this wasn't just ceremony. The Baltimore merchants who gathered that day were fighting for their city's survival.

Baltimore in 1827 faced an existential crisis. New York's Erie Canal, completed in 1825, had diverted western trade northward, threatening Baltimore's position as America's second-largest city. Philadelphia was planning its own canal system. Without a competitive transportation link to the western territories, Baltimore risked economic irrelevance. The B&O Railroad Company was established by Baltimore, Maryland, merchants to compete with New York merchants and their newly opened Erie Canal for trade to the west. The solution came from an unlikely source: two Baltimore businessmen who had traveled to England in 1826 to study an experimental new technology—railroads.

Chapter 123 of the 1826 Session Laws of Maryland, passed February 28, 1827, and the Commonwealth of Virginia on March 8, 1827, chartered the Baltimore and Ohio Rail Road Company, with the task of building a railroad from the port of Baltimore west to a suitable point on the Ohio River. This wasn't just America's first common carrier railroad—it was a $3 million gamble (roughly $83 million in today's dollars) on unproven technology. The remaining private equity was purchased by around 22,000 people, equivalent to one-quarter of the city's population at the time. Think about that: one in four Baltimore residents bought stock in this experimental venture. This wasn't Wall Street speculation—it was civic survival.

The early years were equal parts innovation and improvisation. The first 13-mile stretch to Ellicott's Mills opened in 1830, initially using horses to pull carriages on wooden rails. Then came Peter Cooper's "Tom Thumb," a tiny steam locomotive that looked more like a vertical boiler on wheels than a transportation revolution. Peter Cooper's steam locomotive, the Tom Thumb, ran over this line and demonstrated to doubters that steam traction was feasible on the steep, winding grades. When the Tom Thumb famously lost a race to a horse-drawn car due to a mechanical failure, skeptics declared steam power dead. They were spectacularly wrong.

What followed was seven decades of relentless expansion westward, each mile of track a small victory against geography, politics, and physics. The B&O reached Cumberland, Maryland, in 1842, requiring the construction of the Kingwood Tunnel through the Allegheny Mountains. It finally reached its namesake destination—the Ohio River at Wheeling—in 1852, twenty-four years after breaking ground. By the 1870s, the railroad had extended to Chicago and St. Louis, transforming from a regional carrier into a transcontinental force.

But the B&O was just one piece of the puzzle. Down south, two other railroad empires were taking shape. The Atlantic Coast Line, incorporated in 1869, stitched together a network of smaller railroads along the Eastern seaboard from Richmond to Florida. Its rival-turned-partner, the Seaboard Air Line Railway, despite its name having nothing to do with aviation (the term meant the shortest distance between two points), built a parallel network serving many of the same markets. These weren't just transportation companies—they were the arteries of the post-Civil War South's economic reconstruction. The corporate chess game intensified in 1969. Seaboard Coast Line Industries, Inc., incorporated in Delaware on May 9, 1969, was a railroad holding company that owned the Seaboard Coast Line Railroad, its subsidiary Louisville and Nashville Railroad, and several smaller carriers. The genius of this structure was its flexibility—The Seaboard Coast Line Railroad had already held some of L&N's stock, but the new holding company began buying up as much as it could find and held nearly total control of shares by 1971. They also gained control of the Clinchfield Railroad and Georgia Railroad, creating what became known as the "Family Lines System"—a marketing masterstroke that unified these railroads under a common brand while maintaining their separate corporate identities. Meanwhile, up north, the pieces were aligning differently. Chessie System was incorporated in Virginia on February 26, 1973, and it acquired the railroads on June 15, becoming the parent company of an unlikely triumvirate: the venerable Baltimore & Ohio, the coal-hauling powerhouse Chesapeake & Ohio, and the scrappy Western Maryland Railway. Headquartered in Cleveland, Ohio, the Chessie System was the creation of Cyrus S. Eaton and his protégé Hays T. Watkins, then president and chief executive officer of the C&O.

The Chessie name itself carried marketing genius. "Chessie" had been a popular nickname for the C&O since the 1930s, cemented with an advertising campaign that featured a sleeping kitten named Chessie. By 1973, that sleeping kitten logo—overlaid in a circle to form a rough letter "C"—became the symbol of a railroad empire that controlled critical coal routes from West Virginia to the Great Lakes and automobile parts corridors to Detroit.

These weren't random corporate maneuvers. They were responses to a fundamental shift in American railroading. The Interstate Commerce Commission, which had blocked railroad mergers for decades, was finally allowing consolidation in response to the bankruptcy of Penn Central in 1970—the largest corporate failure in American history at that time. The message was clear: merge or die.

By the mid-1970s, two railroad superpowers dominated the Eastern United States. The Family Lines System controlled the Southeast with its network stretching from Louisville to Florida. The Chessie System commanded the mid-Atlantic and Midwest, hauling Appalachian coal and Detroit automobiles. They eyed each other warily, knowing that eventually, one would have to make a move. That moment was about to arrive, setting the stage for the birth of CSX.

III. The Birth of CSX: Merger of Equals (1978–1980)

The boardroom at Cleveland's Terminal Tower on November 14, 1978, witnessed corporate history being written with a placeholder. CSX Corporation was organized on November 14, 1978, as a future vehicle for such a merger between Chessie System and Seaboard Coast Line Industries. The name itself was supposed to be temporary—a corporate Band-Aid until marketing executives could devise something more elegant. "CSC" was chosen but belonged to a trucking company in Virginia. "CSM" (for "Chessie-Seaboard Merger") was also taken. Needing some sort of identifier for the new railroad, the lawyers decided to use "CSX", and the name stuck, despite only being intended as a placeholder.

The architects of this merger were two railroad titans with contrasting styles. Prime F. Osborn III of Seaboard Coast Line Industries brought Southern gentility and a deep understanding of Florida's booming markets. Hays T. Watkins of Chessie System, a no-nonsense operator who had once fired a president for spending $2 million on tennis courts at the company's Greenbrier resort, brought coal expertise and Midwestern industrial connections. Prime Osborn of SCL and Hays Watkins of Chessie announced that the merger into CSX would be a 50-50 partnership—a claim that would soon be tested. When January 1979 arrived, Chessie and SCL Industries formally applied for ICC approval of their merger plans in January 1979, causing a rapid reaction from the region's other railroads. The application triggered immediate panic at competing railroads. By April, the Norfolk and Western Railway and Southern Railway unveiled their own plans for a merger, creating what would become Norfolk Southern. The Eastern railroad map was being redrawn in real-time, and everyone scrambled for position.

The drama over the name continued right up to the announcement. According to insiders, it was never intended that CSX would be the permanent name of the new corporation. Employee suggestion boxes overflowed with creative combinations of "C" and "S"—everything from "Coastal Systems" to "Chessie-Seaboard United." Marketing executives agonized over finding something that captured the grandeur of this $3.3 billion combination. But facing regulatory deadlines and with all the good alternatives taken, they stuck with their legal placeholder.

The public relations team, desperate to make lemonade from lemons, crafted an explanation that would become railroad lore: In the public announcement, it was said that "CSX is singularly appropriate. C can stand for Chessie, S for Seaboard and X, the multiplication symbol, means that together we are so much more." It was corporate spin at its finest—transforming an administrative accident into a mathematical metaphor for synergy.

The shareholders of both companies approved the merger in 1979, with SCL shareholders getting 1.35 shares of CSX stock for every share of SCL stock, while Chessie shareholders would get one share of CSX for one share of Chessie. This exchange ratio reflected the relative market values but also hinted at which company held more leverage—despite claims of a 50-50 partnership, Chessie shareholders got the better deal.

On November 1, 1980, following Interstate Commerce Commission (ICC) approval, CSX Corporation officially came into being as the successor of Chessie System and Seaboard Coast Line Industries. The first board meeting brought together 24 directors—12 from each side—in a carefully choreographed display of equality. Prime Osborn was named chairman, Hays Watkins president and CEO. But anyone watching closely could see where the real power lay. Watkins controlled operations, and when Osborn retired in 1982, Watkins added the chairman title to his collection.

What had been created wasn't just another railroad—it was the largest rail system in the United States, with 27,000 miles of track, 70,000 employees, and annual revenues exceeding $5 billion. The geography was staggering: from the Great Lakes to the Gulf of Mexico, from the Atlantic Coast to St. Louis. Coal from Appalachia, automobiles from Detroit, chemicals from the Gulf Coast, and intermodal containers from every major Eastern port—it all moved on CSX rails.

But the real genius of the combination wouldn't become apparent for years. While competitors focused on the overlapping routes and potential cost savings, the strategic thinkers at CSX saw something else: complementary networks that, when combined, created a transportation machine perfectly aligned with America's economic future. The Chessie brought industrial muscle and coal expertise. The Seaboard brought Sun Belt growth and port access. Together—and here the multiplication metaphor actually worked—they were indeed more than the sum of their parts.

IV. Integration Challenges & System Building (1980–1999)

The morning of November 2, 1980, should have been a celebration. CSX Corporation had officially begun operations as America's largest railroad. Instead, chaos reigned. In Jacksonville, Seaboard dispatchers couldn't communicate with Chessie crews in Cumberland. Computer systems spoke different languages—literally. The Seaboard's IBM mainframes couldn't process Chessie's billing codes. Customer service representatives in Baltimore had no idea what rates to quote for shipments originating in Florida. This wasn't a merger; it was a collision.

Despite the merger in 1980, CSX was a paper railroad (meaning no CSX painted locomotives or rolling stock) until 1986. The company existed more in boardrooms and legal documents than on actual rails. Locomotives still wore their heritage paint—Chessie's blue and yellow here, Seaboard's black and yellow there. Engineers refused to operate "foreign" equipment. The Baltimore & Ohio brotherhood, with roots stretching back 150 years, viewed the Seaboard newcomers with suspicion bordering on contempt.

The cultural divide ran deeper than paint schemes. The Chessie System epitomized old-school railroading—hierarchical, tradition-bound, focused on heavy industry and coal. The Seaboard culture reflected its Southern and merger-heavy heritage—more flexible, entrepreneurial, comfortable with change. When executives tried to standardize operating procedures, they discovered that something as basic as a train order meant different things in different territories. The companies didn't just use different forms; they thought about railroading differently.

Hays Watkins, now firmly in control after Osborn's 1982 retirement, chose a gradual approach that frustrated Wall Street but probably saved the company. Rather than force rapid integration, he allowed the subsidiaries to maintain separate identities while slowly harmonizing back-office functions. Initially only a holding company, the subsidiaries that made up CSX Corporation completed merging in 1987. CSX Transportation formally came into existence in 1986, as the successor of Seaboard System Railroad.

The integration proceeded in stages, each one a careful dance of corporate politics and operational necessity. First came the Southern roads: Seaboard System Railroad was created on December 29, 1982, by the merger of Louisville & Nashville and Seaboard Coast Line. This consolidation brought together the entire Family Lines System under one corporate umbrella, simplifying the Southern network while maintaining the Chessie System as a separate entity.

Meanwhile, the Chessie roads underwent their own consolidation. The Western Maryland, always the smallest and most vulnerable of the three, was the first casualty. Despite having some of the best-engineered routes through the Appalachians—its grades were superior to the parallel B&O lines—it was deemed redundant. The WM was merged into the B&O on May 1, 1983, erasing a proud railroad that had served as a critical competitor and innovator for decades.

The human cost was staggering. Thousands of jobs disappeared as duplicate facilities closed. The Western Maryland's shops in Hagerstown shut down. Redundant yards in Cincinnati consolidated. The Seaboard's Jacksonville headquarters absorbed functions from Louisville, Baltimore, and Richmond. Each closure meant not just lost jobs but broken traditions—railroad towns that had defined themselves by their backhops and yards suddenly had neither.

In 1986 CSX Corp. eliminated its Seaboard and Chessie systems as separate components and reorganized itself into 3 separate firms: CSX Transport, headquartered in Jacksonville, FL, and CSX Distribution Service and CSX Equipment, both headquartered in Baltimore. This reorganization finally created a unified railroad from the hodgepodge of predecessors, though the scars of forced integration would last for years.

Competition with the newly formed Norfolk Southern added urgency to the integration efforts. In 1982, N&W and the Southern completed their merger and formed Norfolk Southern Railway, creating a competitor to CSX. The NS combination had proceeded more smoothly—both roads shared similar cultures and operating philosophies. They mocked CSX's integration struggles in sales presentations, positioning themselves as the stable alternative to CSX's chaos.

The competitive dynamics were fascinating. In many markets, CSX and NS were the only games in town, creating a duopoly that would define Eastern railroading for decades. But in the crucial Chicago gateway, they faced the Western giants—Burlington Northern, Union Pacific, Santa Fe. The battle for transcontinental traffic became a chess match of rates, service, and strategic alliances.

By the late 1980s, patterns emerged that would define CSX's network strategy. The I-95 corridor from Boston to Miami became the spine of the intermodal network. The Appalachian coal fields, despite beginning their long decline, still generated massive revenues. The Chicago–East Coast lanes competed fiercely with truckers and Norfolk Southern. The chemical complexes along the Gulf Coast provided steady, high-margin traffic.

But the real transformation was happening in the Southeast. As manufacturing fled the Rust Belt for right-to-work states, CSX found itself perfectly positioned. Auto plants sprouted in Alabama and South Carolina. Distribution centers clustered around Atlanta. Ports like Jacksonville and Savannah exploded with Asian imports. The old Seaboard routes, once considered secondary to the industrial arteries up north, suddenly became gold mines.

Technology finally began to stitch the system together. A unified computer system—implemented at enormous cost and with countless glitches—replaced the babel of incompatible platforms. Centralized dispatching centers replaced local towers. Radio systems were standardized. By 1990, a CSX conductor in Syracuse could communicate with dispatchers in Jacksonville as easily as one in Savannah.

The operational improvements were real but incremental. Train speeds increased marginally. On-time performance improved from abysmal to merely poor. But the fundamental problem remained: CSX was trying to operate a 20th-century railroad with 19th-century infrastructure and thinking. The company moved freight, generated profits, and paid dividends, but it wasn't transforming transportation.

As the 1990s dawned, CSX faced a strategic crossroads. The easy synergies from merger had been captured. The coal business that had sustained the Chessie System was beginning its structural decline. Trucks continued to eat into merchandise traffic. And most ominously, whispers emerged that Conrail—the government-created giant that controlled the Northeast—might be for sale. The next phase of consolidation was about to begin, and CSX needed to be ready. The integration struggles of the 1980s had been painful but necessary preparation. The company that emerged was leaner, unified, and battle-tested. It would need all those qualities for what came next.

V. The Conrail Acquisition: Power Play of the Century (1997–1999)

The June 21, 1970, bankruptcy of Penn Central Transportation Company wasn't just corporate failure—it was economic catastrophe. At the time, this was the largest bankruptcy in American history, a $7 billion collapse that threatened to take down the entire Northeastern economy. The railroad that had carried a third of the nation's freight was suddenly unable to pay its bills. Freight cars sat idle. Shippers scrambled for alternatives. Wall Street panicked.

The backstory reads like Greek tragedy. The Pennsylvania Railroad and New York Central, bitter rivals since the 1800s, had merged in 1968 out of desperation rather than strength. They were hemorrhaging money from passenger operations, losing freight to trucks, and watching their industrial customers flee to the Sun Belt. The merger, rather than solving these problems, magnified them. Incompatible computer systems, clashing corporate cultures, and redundant routes created operational chaos. By 1970, Penn Central was losing nearly $1 million per day.

The federal government, faced with the prospect of economic collapse in the Northeast, created an unprecedented solution. After the failure of Penn Central in 1970, the government formed the United States Railway Association in 1973 to develop a plan to save railroading in the Northeast. The result was Conrail—Consolidated Rail Corporation—which began operations on April 1, 1976, absorbing Penn Central and six other bankrupt railroads into a government-owned entity. Against all expectations, Conrail turned itself around. Through the 1980s, freed from passenger obligations and with new flexibility under the Staggers Act deregulation, the government-owned railroad became profitable. By 1987, it was privatized through an initial public offering, emerging as a lean, efficient operator with the best routes in the Northeast. Suddenly, everyone wanted Conrail.

The opening shot came on October 15, 1996. CSX announced it would acquire Conrail for $8.4 billion in a friendly merger blessed by both boards. John Snow, CSX's CEO, and David LeVan, Conrail's chairman, painted a vision of an integrated Eastern system stretching from Boston to Miami, Chicago to New Orleans. The deal seemed done. Then Norfolk Southern crashed the party.

David Goode, Norfolk Southern's CEO, understood what was at stake. A CSX-Conrail combination would create a railroad behemoth controlling virtually all rail traffic north of Washington and east of Ohio. NS would be boxed into the Southeast, cut off from the industrial heartland. On October 23, just eight days after the CSX announcement, Norfolk Southern launched a hostile bid for Conrail at $100 per share, topping CSX's $92.50 offer.

What followed was the most vicious takeover battle in railroad history. Norfolk Southern raised its bid repeatedly, eventually reaching $115 per share. CSX countered with poison pills and lockup provisions. Conrail's board, loyal to the CSX deal, rejected NS offer after offer. But Conrail shareholders, smelling profit, revolted. In January 1997, they voted down the CSX merger, forcing all parties back to the negotiating table.

The Surface Transportation Board made it clear that neither CSX nor NS would be allowed to acquire Conrail whole—competition in the East had to be preserved. The solution, hammered out in smoke-filled rooms over marathon negotiating sessions, was Solomon-like in its simplicity: split the baby.

On June 23, 1997, CSX and Norfolk Southern Railway filed a joint application with the Surface Transportation Board for authority to purchase, divide, and operate the assets of the 11,000-mile Conrail. The final agreement was surgical in its precision: Under the final agreement approved by the Surface Transportation Board, Norfolk Southern acquired 58 percent of Conrail's assets, including roughly 6,000 Conrail route miles, and CSX received 42 percent of Conrail's assets, including about 3,600 route miles.

The division followed historical logic. NS got the old Pennsylvania Railroad main line from New York to Chicago via Philadelphia and Pittsburgh—the legendary "Broadway Limited" route. CSX acquired the former New York Central "Water Level Route" from New York to Chicago via Albany and Cleveland, plus the Big Four line to St. Louis. The Conrail "X" was neatly split in two, CSX getting one diagonal from Boston to St. Louis and Norfolk Southern the other from New York to Chicago.

The complexity of the split was staggering. Every yard, every customer, every piece of rolling stock had to be allocated. In three areas—North Jersey, Philadelphia, and Detroit—neither railroad could operate efficiently without the other's cooperation. The solution was Conrail Shared Assets Operations, a jointly owned terminal company that would serve customers in these dense markets on behalf of both owners. The preparation for "Split Date"—June 1, 1999—was military in scope. CSX began operating its trains on its portion of the Conrail network on June 1, 1999, bringing Conrail's 23-year existence to an end. Over 11,000 locomotives had to be repainted. Hundreds of thousands of freight cars needed new reporting marks. Computer systems that had taken decades to integrate had to be surgically separated. Employees woke up working for different companies, sometimes literally across the street from former colleagues now wearing competitor's uniforms.

The financial impact was immediate and massive. CSX paid approximately $4.3 billion for its 42% share, adding 3,800 miles of prime Northeastern trackage to its network. The company gained direct access to New York, Boston, and Montreal—markets it had only dreamed of serving. The stock market loved it. CSX shares surged as analysts calculated the synergies from single-line service to major Northeast ports and the elimination of costly interchange delays.

But the real strategic value went beyond route miles or market access. CSX had broken Norfolk Southern's stranglehold on certain markets while preventing NS from dominating the entire East. The duopoly that emerged—CSX and NS roughly equal in size and scope—created a competitive dynamic that benefited shippers while allowing both railroads to generate substantial returns. It was corporate chess at its finest.

The Conrail acquisition also marked the end of major Eastern railroad consolidation. With only two major players left, further mergers would create a monopoly the regulators would never allow. CSX and Norfolk Southern settled into an uneasy equilibrium, competing fiercely in some markets while cooperating in others through the Shared Assets areas. The great Eastern railroad wars were over. The peace, however profitable, would prove temporary.

VI. The Coal Era & Revenue Crisis (2000–2016)

The charts on Michael Ward's wall told a story of slow-motion catastrophe. In 2011, coal generated $3.4 billion in revenue for CSX—nearly 30% of the company's total. By 2016, that number had collapsed to $1.7 billion. The black rock that had built American railroads, that had justified the Chessie System merger, that had sustained CSX through every recession, was dying. Not declining. Not struggling. Dying.

Ward, who had become CEO in 2003, understood the implications better than anyone. CSX moved more coal than any other railroad—roughly 35% of all coal transported in the United States. The company's network was literally built for coal: loading facilities in Appalachia, massive yards for assembling unit trains, direct routes to power plants and export terminals. Billions in infrastructure investment, all predicated on coal remaining America's primary electricity source.

The first warning signs had appeared in the early 2000s. Natural gas, once expensive and scarce, began flowing from shale formations. The fracking revolution made gas competitive with coal for power generation. Then came the environmental regulations—mercury standards, sulfur limits, carbon restrictions. Power plants that had burned coal for decades suddenly switched to gas. Others simply shut down rather than invest in pollution controls.

Ward's response was textbook strategic management. If you can't save a dying business, milk it while building new ones. CSX implemented efficiency improvements that wrung every possible dollar from declining coal volumes. Longer trains, better asset utilization, premium pricing for export coal. Meanwhile, the company poured resources into intermodal, automotive, and merchandise traffic. The strategy had a name: "CSX of Tomorrow."

The transformation required painful choices. Hundreds of miles of coal branch lines were abandoned or sold. Locomotive shops in Cumberland and Huntington, built to service coal operations, closed. Thousands of coal hoppers were scrapped or stored. Communities that had depended on coal traffic for a century watched their economic lifeline disappear.

Yet even as coal collapsed, CSX discovered unexpected opportunities. The same shale revolution killing coal was creating new traffic—sand for fracking, crude oil from North Dakota, natural gas liquids from Pennsylvania. Intermodal volume exploded as online shopping drove demand for container movements. The automotive industry, resurgent after the 2008 crisis, built new plants across the Southeast—all served by CSX.

The financial engineering was equally creative. Ward initiated massive share buyback programs, retiring nearly 30% of CSX's outstanding stock between 2005 and 2015. Dividends increased every year. The company refinanced debt at historically low interest rates. Even as revenues stagnated, earnings per share grew through financial discipline and operational improvements.

But operational improvements had limits. CSX's operating ratio—operating expenses as a percentage of revenue—stubbornly remained in the high 60s to low 70s. Competitors like Canadian National were achieving ratios in the 50s. The company tried everything: technology investments, management reorganizations, consultant studies. Nothing moved the needle significantly.

Labor relations deteriorated as the company pushed for productivity improvements. The unions, watching jobs disappear to technology and efficiency initiatives, fought back with work rules and grievances. Service suffered. Customers complained about inconsistent delivery times and poor communication. CSX seemed stuck—profitable but uninspiring, surviving but not thriving.

By 2016, the situation was becoming critical. Coal revenue continued its death spiral. Intermodal growth was slowing. The stock price languished. Institutional investors were losing patience. Ward, now 66, announced his retirement plans. The board began searching for his successor, expecting a smooth transition to another railroad lifer.

They hadn't counted on Paul Hilal. The activist investor had been quietly accumulating CSX shares through his hedge fund, Mantle Ridge. Hilal had studied the railroad industry for years and reached a controversial conclusion: American railroads were badly managed, operating with 19th-century thinking in a 21st-century economy. He believed one man could fix CSX—if he could be convinced to take the job.

That man was E. Hunter Harrison, and he was about to turn CSX upside down.

VII. The Hunter Harrison Revolution (2017)

The scene at CSX headquarters on January 18, 2017, was surreal. On January 18, 2017, Harrison resigned as CEO of CP Ltd. to join Paul Hilal—the same day Canadian Pacific announced his departure. At 72 years old, walking with assistance and occasionally using oxygen, Harrison hardly looked like a corporate savior. Yet Recruited by activist investor company Mantle Ridge, which had recently taken a stake in CSX, he was about to unleash a revolution that would either transform or destroy one of America's largest railroads.

Paul Hilal, the force behind Harrison's hiring, wasn't your typical activist investor. A protégé of Bill Ackman at Pershing Square, Hilal had orchestrated Harrison's installation at Canadian Pacific in 2012, watching the stock price triple. Now, through his new fund Mantle Ridge, he controlled less than 5% of CSX but wielded influence like he owned half the company. His pitch to the board was simple: give Harrison total control or watch your stock price languish while competitors pull ahead.

The negotiations were brutal. Harrison's demands were extraordinary: Mr. Harrison's terms of employment at a total cost which CSX estimates to exceed $300 million, including $84 million just to reimburse him for compensation forfeited at Canadian Pacific. He wanted complete operational control, his hand-picked team, and no medical examination despite obvious health concerns. The board, facing a proxy fight they would likely lose, capitulated. On March 7, 2017, Harrison was named CEO of CSX.What Harrison unleashed wasn't management consulting—it was corporate warfare. Precision scheduled railroading (PSR) is a concept in freight railroad operations pioneered by American railroad executive E. Hunter Harrison in 1993. It shifts the focus from older practices, such as unit trains, hub and spoke operations, and individual car switching at hump yards to emphasizing point-to-point freight car movements on simplified routing networks.

The numbers were staggering in their brutality. Under CSX's PSR strategy the fleet was reduced by 900 locomotives and 26,000 wagons by the end of the second quarter of 2017 and Harrison aimed to cut the railway's 31,000-strong workforce by nearly a third. Seven of CSX's twelve hump yards—massive facilities where trains were broken apart and reassembled—were shuttered or converted to flat switching yards. Hundreds of miles of secondary track were abandoned. The company went from running trains when they had enough cars to fill them to running on rigid schedules whether full or not.

The human carnage was immediate. Entire departments were eliminated with hours' notice. Managers who had worked at CSX for decades were escorted from the building. Train crews showed up for work to find their runs canceled permanently. The town of Hamlet, North Carolina, which had hosted a major CSX yard for a century, watched it close almost overnight. Avon Yard in Indianapolis, Tilford Yard in Atlanta—one by one, they fell silent.

Customers erupted in fury. From day one, Harrison unleashed shock and awe to transform CSX from a hub-and-spoke network into a lean, point-to-point system. The program infuriated shippers, who were forced to scrap their schedules. Chemical plants that had received five deliveries a week were told they would now get seven smaller ones. Automotive factories accustomed to dedicated unit trains found their cars mixed with lumber and grain. The Surface Transportation Board was flooded with complaints about service failures, missed switches, and cars lost in the system for weeks.

Harrison's response was characteristic: deal with it or find another railroad. Since CSX was often the only railroad serving these customers, they had no choice. When the Rail Customer Coalition complained to regulators about "chronic service failures," Harrison dismissed their concerns as "unfounded and exaggerated." He knew that by the time regulators could act, if they ever did, the transformation would be complete.

The financial markets loved it. CSX's stock price surged from $45 when Harrison arrived to over $55 by summer. The operating ratio, which had been stuck in the high 60s under Ward, plummeted toward 60 and below. Wall Street analysts who had written off American railroads as mature, slow-growth businesses suddenly saw them as cash machines capable of Silicon Valley-style margins.

But Harrison was racing against time in more ways than one. Those close to him noticed the oxygen tank appearing more frequently. The long days took their toll—he would arrive at 5 AM and leave after dark, seven days a week. He missed meetings due to exhaustion. His appearance became increasingly gaunt. Yet he pushed harder, knowing that PSR needed to be irreversibly embedded in CSX's DNA before his time ran out.

The internal alarm bells started ringing in November. On December 14, 2017, CSX announced that Hunter Harrison was on medical leave, sending shockwaves through Wall Street. The impact was immediate—on December 15 the CSX stock plunged 12% before trading opened, and finished the day with a 7.3% loss, making it one of the day's biggest losers on the S&P 500. What investors didn't know was that Harrison's time had already run out.

On December 16, 2017, CSX announced that Hunter Harrison, President and Chief Executive Officer of CSX, died today in Wellington, Fla., due to unexpectedly severe complications from a recent illness. He died two days after taking medical leave from CSX. The transformation architect who had promised to reinvent American railroading was gone, leaving behind a company half-transformed, a workforce in turmoil, and a board scrambling to salvage the revolution he had started.

VIII. Post-Harrison Era & Modern CSX (2018–Present)

The conference call on December 15, 2017, was supposed to calm the markets. Instead, James Foote found himself conducting a corporate séance, channeling the ghost of Hunter Harrison to jittery analysts. "I believe that the battleship here has turned," Foote declared during the conference call. The metaphor was apt—CSX was indeed a battleship, half through a dangerous turn, with its captain dead at the helm.

The Board of Directors of CSX Corporation announced on December 22, 2017 that it had unanimously named James M. Foote as the company's president and chief executive officer, effective immediately. Mr. Foote was named acting CEO on December 14, 2017 after E. Hunter Harrison was placed on medical leave. Mr. Foote also joined the Company's Board of Directors.

Foote brought unique credentials to the role. In 1995, Foote joined the Canadian National Railway and was named Executive Vice President of Sales and Marketing in 1999. He was in that position in 2003 when CN named Mr. Harrison as CEO and began its implementation of Scheduled Railroading. Foote worked closely with Mr. Harrison throughout the CN's transformation that turned a $2 billion company into one worth more than $24 billion. He wasn't just Harrison's successor—he was his disciple.

But Foote understood something Harrison hadn't: you couldn't treat an American railroad like a Canadian one, and you couldn't treat employees like obstacles to efficiency. "Atlanta hump yard today is flat," Foote said on the railroad's January 2018 earnings call. "There is no turning back." The message was clear—PSR would continue, but with a human touch Harrison had never possessed.

The transformation under Foote was remarkable in its quiet effectiveness. Under Foote's leadership CSX would go on to become the best performing Class I railroad, based on its financial and operational statistics. By the end of 2019 revenue was up 8%, expenses fell 9%, and the operating ratio leapfrogged from a back-of-the-pack 69.4% in 2016 to an industry leading 58.4%. Net profit nearly doubled compared to the pre-PSR CSX, and earnings per share grew 130%.

Where Harrison had wielded a sledgehammer, Foote used a scalpel. Service metrics improved gradually rather than collapsing then recovering. Customer relationships were rebuilt through consistent communication rather than ultimatums. The workforce, while still reduced, was engaged rather than terrorized. In a major accomplishment during Foote's tenure, CSX was able to halt and reverse the decline of its merchandise network.

The strategic moves during Foote's tenure were equally significant. To extend the reach of its lucrative chemical business, CSX in 2021 purchased bulk trucking company Quality Carriers. CSX acquired New England regional Pan Am Railways in 2022, cementing the railroad's dominance in the region. These weren't just acquisitions—they were strategic expansions that filled network gaps and created new service opportunities.

In a landmark $525 million deal with Virginia, CSX agreed in 2021 to an easement that will enable the separation of passenger and freight operations in the busy Washington, D.C., to Petersburg, Va., corridor. The deal also included the sale of CSX line segments from Petersburg to Ridgeway, N.C., and from Doswell to Clifton Forge. This wasn't just selling track—it was monetizing infrastructure while improving network fluidity.

Then came the pandemic. Foote guided the railroad through the pandemic, related huge swings in freight volume, and the crew shortages that led to widespread service problems at the big four U.S. railroads. While competitors struggled with labor shortages and service meltdowns, CSX maintained relative stability. The PSR model, for all its brutality, had created operational flexibility that proved invaluable during the chaos of 2020-2021.

By 2022, Foote was ready to pass the torch. CSX Corp. announced Sept. 15 that James Foote would retire as president and CEO on Sept. 26 and be succeeded by former Ford Motor Co. executive Joseph Hinrichs. Jacksonville-based CSX said the change in leadership was part of a planned succession process. The choice was unconventional—an automotive executive with no railroad experience taking over one of America's largest railroads.

Joseph R. Hinrichs, a leader with more than 30 years of experience in the global automotive, manufacturing, and energy sectors, was named President and Chief Executive Officer of CSX in September 2022. Hinrichs brings to CSX a commitment to operational excellence, experience building global businesses through investment in people and culture, and a deep understanding of balancing safety and efficiency in a complex industry. Hinrichs previously served as President of Ford Motor Company's global automotive business. In that role, he led the company's $160-billion automotive operations, overseeing Ford's global business units and the Ford and Lincoln brands.

The Hinrichs era represented something new for CSX: stability. No activist investors, no revolutionary operating models, no mass firings. Instead, Hinrichs focused on what he called "ONE CSX"—an initiative which emphasizes collaboration, inclusion, and mutual respect among employees. After years of upheaval, the railroad was finally settling into sustainable operations.

At CSX, he gained a reputation for bringing paid sick leave to employees and forging preliminary agreements with unions prior to negotiating. This wasn't weakness—it was recognition that sustainable efficiency required workforce buy-in. The adversarial relationship Harrison had cultivated was replaced with cautious cooperation.

The financial results under Hinrichs have been mixed but solid. In 2024, the company posted revenue of $14.54 billion, a 0.8% decline from 2023. Operating income fell 5% to $5.25 billion, while net income declined to $3.47 billion ($1.79 per share) from $3.67 billion ($1.82 per share) the previous year. Not spectacular, but in an industry facing headwinds from economic uncertainty and shifting freight patterns, stability itself was an achievement.

The challenges have been real. Hinrichs has faced major infrastructure disruptions, including over $400 million in reconstruction costs in eastern Tennessee following Hurricane Helene, as well as impacts from the Baltimore Key Bridge collapse and other severe weather events. Climate change wasn't just an environmental issue—it was becoming an operational nightmare, destroying infrastructure faster than it could be maintained.

IX. Business Model & Operating Playbook

The economics of rail freight are beautifully simple and maddeningly complex. Simple because the physics haven't changed since 1827—steel wheels on steel rails remain the most efficient way to move heavy loads over land. Complex because orchestrating 500 daily trains across 20,000 miles of track while competing with subsidized highways requires operational precision that would challenge a Swiss watchmaker.

CSX's business model rests on three pillars, each generating roughly a third of revenue. Merchandise—everything from chemicals to automobiles—provides the highest margins but requires the most operational complexity. Intermodal—containers moving between ships, trains, and trucks—offers growth potential but faces fierce competition. Coal, the dying king, still generates cash but shrinks every quarter.

The network effect is CSX's moat. Its network connects every major metropolitan area in the eastern United States, where nearly two-thirds of the nation's population resides. It also links more than 240 short-line railroads and more than 70 ocean, river and lake ports with major population centers and farming towns alike. Every additional customer makes the network more valuable to every existing customer. Every new connection point increases the possible routing combinations exponentially.

The precision scheduled railroading transformation fundamentally rewired this network. Before PSR, trains operated like buses—waiting until they had enough passengers (freight cars) to justify the trip. PSR turned them into subways—running on fixed schedules regardless of load. This seems inefficient until you realize that predictability has value. Customers will pay premium prices for certainty.

The operational metrics tell the story. Train velocity—the average speed of trains across the network—improved from 18 mph pre-PSR to over 20 mph today. That might seem marginal, but at scale it means each locomotive and crew can handle 11% more freight. Dwell time—how long cars sit in yards—dropped from 30 hours to under 24. Terminal processing time fell by 40%. These aren't just statistics; they're compound interest on billions in assets.

The capital allocation strategy reflects this operational leverage. CSX spends roughly $2 billion annually on capital expenditures, mostly on maintaining existing infrastructure rather than expansion. Why build new track when you can extract more capacity from existing rails through operational improvements? The company returns most of its free cash flow to shareholders through dividends and buybacks, a strategy that only works because the network requires minimal growth investment.

But the real genius of the model is pricing power. In most markets, CSX faces only one competitor—Norfolk Southern—or none at all. Trucking provides theoretical competition, but at distances over 500 miles, rail's cost advantage becomes insurmountable. As highway congestion worsens and driver shortages intensify, this advantage only grows.

The environmental angle adds another dimension. A single train can move one ton of freight 500 miles on a single gallon of fuel. Achieving the same efficiency by truck would require three to four times the fuel. As carbon regulations tighten, this efficiency transforms from operational advantage to existential necessity for shippers needing to meet emissions targets.

X. Analysis & Investment Case

The bull case for CSX writes itself. Here's a company with a legal oligopoly, irreplaceable infrastructure, and improving operations trading at a reasonable valuation. CSX's operating margin was 31.3% for the quarter, and adjusted operating margin was 34.3%—margins that would make most businesses weep with envy. The network would cost hundreds of billions to replicate, assuming you could even acquire the land rights, which you couldn't.

The secular trends all favor rail. E-commerce drives intermodal growth as containers move from ports to distribution centers. Manufacturing reshoring benefits CSX's Southeast network. Environmental regulations make rail's fuel efficiency increasingly valuable. Highway congestion and truck driver shortages eliminate rail's primary competition. Demographics concentrate population in CSX's service territory.

The recent financial performance, while mixed, shows resilience. For the full year 2024, CSX operating income of $5.25 billion was down 5% from the previous year. Net income for the year was $3.47 billion, or $1.79 per share, compared to $3.67 billion, or $1.82 per share, in 2023. In a challenging economic environment, maintaining near-record profitability demonstrates the model's durability.

The bear case requires equally serious consideration. Economic sensitivity remains CSX's Achilles heel—when industrial production slows, freight volumes collapse. The stock acts like a leveraged bet on GDP growth, amplifying both upturns and downturns. A recession would savage earnings regardless of operational improvements.

Regulatory risk looms larger than investors appreciate. The Surface Transportation Board has grown increasingly aggressive about service standards and rate regulation. Political pressure to reduce shipping costs could cap pricing power. Environmental regulations, while favoring rail over trucking, impose massive costs for track maintenance and equipment upgrades.

Labor relations present ongoing challenges. While Hinrichs has improved the dynamic, the fundamental tension remains: PSR's efficiency comes from employing fewer people to move more freight. The unions understand this math and fight accordingly. According to Comparably, he ranks in the bottom 5% of CEOs at companies with more than 10,000 employees, with only 43% of CSX employees saying they would recommend the company to a friend. Some critics have described his employee engagement efforts as limited or primarily focused on public relations.

The technology wildcard cuts both ways. Autonomous trucks could theoretically compete with rail for long-haul freight, though the timeline remains uncertain. Conversely, autonomous trains could dramatically reduce CSX's largest operating cost—labor. The company investing wisely in technology could create insurmountable advantages; the one that doesn't could become obsolete.

Competition from Norfolk Southern remains intense in overlapping markets. While the duopoly generally maintains pricing discipline, periodic price wars erupt, particularly for high-value intermodal traffic. The Shared Assets Areas from the Conrail split create operational complexity and potential conflict points.

The valuation question depends on your time horizon. At current levels, CSX trades at approximately 20 times earnings—neither cheap nor expensive for a business of its quality. The dividend yield around 1.3% won't excite income investors but leaves room for growth. The company's share buyback program, having retired roughly 35% of shares outstanding over the past decade, continues to boost per-share metrics.

XI. Looking Forward: The Next Chapter

The railroad industry stands at an inflection point more significant than any since dieselization. Climate change is destroying infrastructure faster than companies budgeted to maintain it. Labor shortages are forcing automation decisions that unions have successfully resisted for decades. Environmental regulations are making rail's efficiency advantage existential for heavy industry. The companies that navigate these transitions successfully will dominate for generations; those that don't will become historical footnotes.

For CSX specifically, the path forward requires threading multiple needles simultaneously. The company must maintain operational excellence while rebuilding workforce morale. It must invest in technology while returning cash to shareholders. It must serve customers reliably while adapting to climate disruption. It must grow revenue while coal continues its terminal decline.

The infrastructure bill passed in 2021 provides both opportunity and challenge. Billions in funding for rail improvements could enhance CSX's network, but strings attached to government money often reduce returns. Passenger rail expansion, while politically popular, complicates freight operations on shared tracks. The company must navigate these political currents while maintaining operational independence.

The technology investments CSX makes today will determine its relevance in 2040. Distributed power systems that allow longer trains with fewer crews. Predictive maintenance using sensors and artificial intelligence. Automated terminals that process cars without human intervention. These aren't futuristic concepts—they're being tested today. The question is implementation speed and union acceptance.

The competitive landscape could shift dramatically. A merger between CSX and Norfolk Southern, while currently unthinkable from a regulatory perspective, might eventually become necessary to compete with trucking's technological advances. Alternatively, a transcontinental merger—CSX with Union Pacific or BNSF—could create new single-line services that transform logistics patterns.

Climate adaptation will require massive capital investment. Tracks that have lasted a century now wash away in single storms. Bridges designed for historical flood levels face unprecedented water flows. The company that masters resilient infrastructure design while controlling costs will have an enormous competitive advantage.

XII. Recent News

The fourth quarter 2024 results released on January 23, 2025, painted a picture of operational challenges and financial resilience. CSX Corp. today announced fourth quarter 2024 operating income of $1.11 billion compared to $1.32 billion in the prior year period. Net income was $733 million, or $0.38 per diluted share, compared to $882 million, or $0.45 per diluted share, in the same period last year. The results included a painful reminder of past decisions: Results for the fourth quarter include a pre-tax, non-cash goodwill impairment charge of $108 million.

Despite the headline disappointment, operational trends showed promise. Total volume of 1.58 million units for the quarter was 1% higher compared to fourth quarter 2023, suggesting demand stabilization after years of coal-driven decline. Management's commentary emphasized continued investment in network capabilities and safety improvements, signaling confidence in long-term growth prospects despite near-term headwinds.

The broader context reveals the challenges facing all North American railroads. Supply chain disruptions, inflation, and economic uncertainty create an operating environment unlike any in recent memory. CSX's ability to maintain profitability while navigating these challenges demonstrates the resilience of the business model, even as it highlights the limitations of operational improvements alone to drive growth.

Conclusion: The Acquired Perspective

Standing back from the minutiae of operating ratios and regulatory filings, CSX represents something profound: the physical manifestation of American industrial capitalism. Every ton of steel produced, every car manufactured, every container imported touches CSX's network. The company isn't just moving freight; it's moving the economy itself.

The transformation from a collection of 19th-century railroads to a 21st-century logistics network required corporate brutality that would make private equity blush. Thousands lost their jobs. Entire communities built around rail yards watched them close. A way of life that sustained families for generations vanished in quarterly earnings calls. Hunter Harrison didn't create this reality—he simply had the audacity to execute it without apology.

Yet the efficiency gained wasn't just financial engineering. Those shuttered hump yards were genuinely inefficient. Those eliminated jobs often involved dangerous, backbreaking work. The PSR transformation, for all its human costs, created a railroad that moves more freight with less equipment, less fuel, and yes, fewer people. In a world facing climate catastrophe, that efficiency isn't just profitable—it's necessary.

The investment case ultimately depends on your view of America's economic future. If you believe manufacturing will continue reshoring, ports will continue growing, and businesses will continue needing physical goods moved efficiently, then CSX offers exposure to these trends with limited downside protection from its oligopoly position. If you believe autonomous trucks will revolutionize logistics, environmental regulations will cripple heavy industry, or economic growth will stagnate, then CSX becomes a value trap—profitable today but irrelevant tomorrow.

What would Ben and David do if they were running CSX? They'd probably accelerate technology investment, even at the cost of near-term earnings. They'd pursue strategic acquisitions that extend the network's reach or add complementary capabilities. They'd prepare for a future where moving data about freight becomes as important as moving freight itself. Most importantly, they'd recognize that CSX's greatest asset isn't its track or locomotives—it's the network effect created by connecting every major Eastern economy with reliable, efficient transportation.

The CSX story isn't finished. The company that emerged from the 1978 merger barely resembles today's precision railroad, and today's CSX will likely be unrecognizable in 2050. Whether that transformation creates or destroys value depends on decisions being made in Jacksonville boardrooms and Washington hearing rooms today. For investors, customers, and the communities CSX serves, those decisions will echo for generations.

The rails that Charles Carroll ceremonially began in 1828 still carry freight today, upgraded and maintained but fundamentally unchanged. That permanence in an era of disruption is both CSX's greatest strength and its ultimate challenge. The company must innovate while preserving, transform while maintaining, advance while remembering that sometimes the old ways—steel wheels on steel rails—remain the best ways.

In the end, CSX is a bet on the physical economy's continued relevance in an increasingly digital world. It's a wager that things will still need to move from place to place, that geography still matters, that the elegant efficiency of rail transport will outlive its critics and competitors. For nearly 200 years, that bet has paid off. Whether it continues to do so will depend on CSX's ability to evolve while remaining true to its fundamental purpose: connecting American commerce, one train at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube