JASH Engineering: From Family Workshop to Global Water Infrastructure Leader

I. Introduction & Episode Teaser

Picture this: It's 1948 in the small town of Dewas, 35 kilometers from Indore. India has just gained independence, and the air is thick with both hope and uncertainty. In a modest workshop, a mechanical engineer named Jashbhai Patel is tinkering with machine tools—lathes, drilling machines, slotting machines. He has no idea that his small enterprise will one day become a global water infrastructure powerhouse with operations spanning four continents.

Fast forward to today: Jash Engineering derives over 60% of its revenue from supply of equipment to projects outside India. The company boasts a market capitalization of 3,242 Crore, revenues of 748 Cr, and profits of 81.5 Cr. It's a story that nobody talks about, yet everyone needs—because water infrastructure isn't sexy, but it's absolutely essential.

Think about it: every time you turn on a tap, flush a toilet, or watch stormwater drain away during monsoons, there's infrastructure working silently in the background. And increasingly, that infrastructure might just have been made by a company that started in a small Indian town over 75 years ago.

What makes this story particularly fascinating is how Jash transformed from a general engineering workshop into India's No.1 manufacturer of water control gates with over 70% market share and for Bed plates with over 80% market share. It's a tale of strategic pivots, calculated risks, international acquisitions, and the kind of patient capital building that would make Warren Buffett smile.

But here's the kicker: while everyone's talking about sexy tech startups and AI unicorns, Jash has quietly built a moat so wide that it's the largest supplier of water control gates to PUB Singapore and with presence on 4 continents through its wholly owned subsidiaries and cumulative experience of over 350 years with its subsidiaries, is considered preferred supplier for critical applications to over 45 countries worldwide.

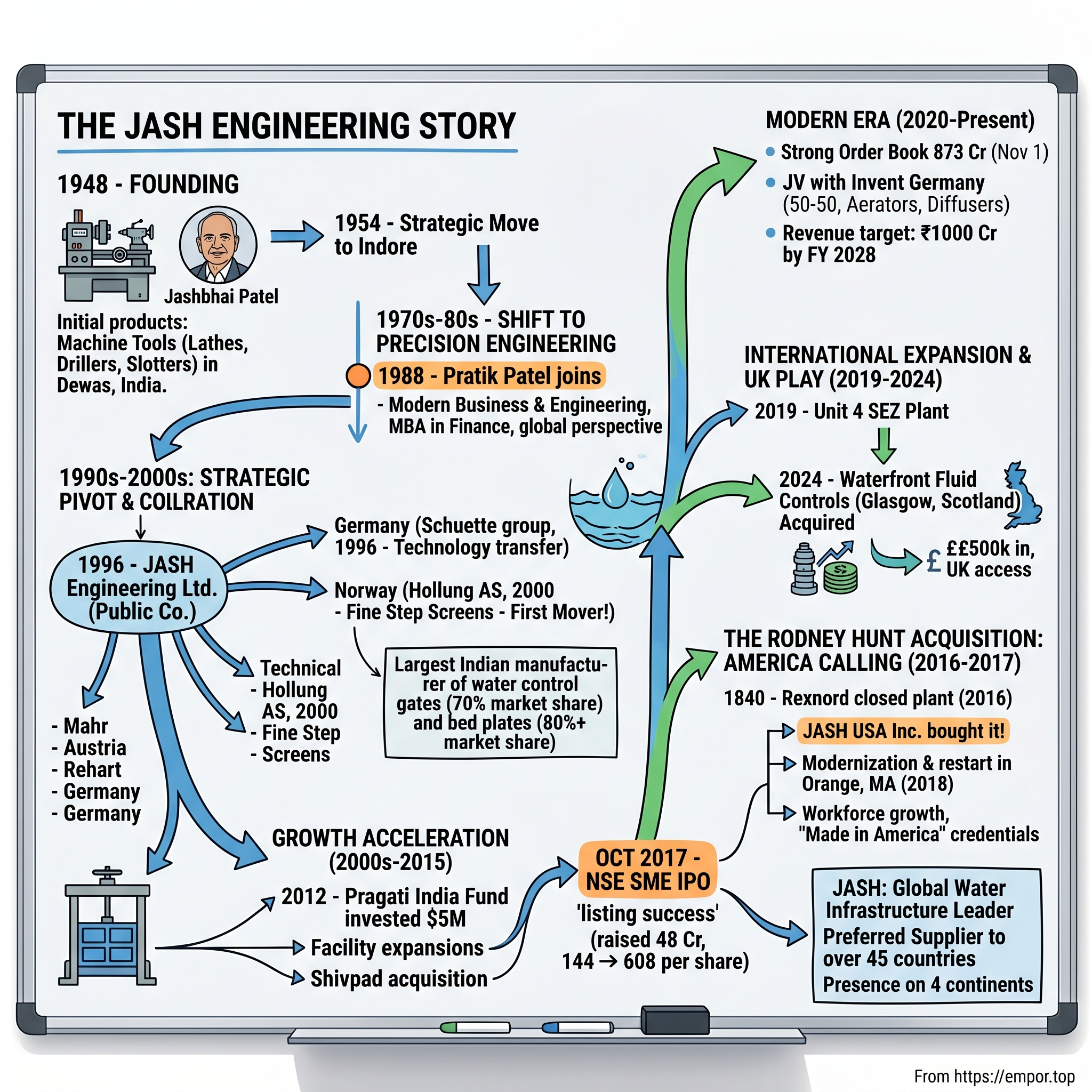

II. Founding Story & Early Years (1948-1990s)

The year is 1948. India is barely a year old as an independent nation. Infrastructure? Practically non-existent. Manufacturing? In its infancy. Into this landscape steps Jashbhai Patel, a Mechanical Engineer, establishing his business in the town of Dewas located 35 kms from Indore. Initial products were machine tools like lathe drilling and slotting machines.

This wasn't some grand vision to build a water infrastructure empire. No, Jashbhai was simply a skilled engineer trying to make a living in newly independent India, building the basic tools that other businesses needed to function. But even then, there were signs of the ambition that would define the company's trajectory.

By 1954, the manufacturing plant shifted to the city of Indore—a strategic move that would position the company at the heart of central India's industrial growth. Indore wasn't Delhi or Mumbai, but that was precisely the point. Lower costs, room to grow, and proximity to both raw materials and emerging markets.

The company's formal incorporation tells an interesting story of evolution. The company was incorporated as a Private Limited Company with the name 'Jash Engineering Industries Private Limited' on September 29, 1973. But here's where it gets interesting: Company name was changed to Jash Engineering Private Limited on January 29, 1976. Even the name change—dropping "Industries"—signaled a shift from being just another industrial company to something more focused, more specialized.

Through the 1970s and 1980s, Jash was building capabilities that would later prove crucial. The company wasn't just manufacturing; it was learning the art of precision engineering, understanding metallurgy, mastering fabrication techniques. The company commenced manufacturing of water control gates, precision surface equipment, and bed plates/T-slotted plates during this period.

Then came 1988, a pivotal year that doesn't get enough attention. Entry of third generation of family in the business Mr. Pratik Patel a Product Engineer with Masters in Business Administration in finance joins the business. This wasn't just another family member joining the firm—this was the injection of modern business thinking into a traditional engineering company. Pratik Patel brought something his grandfather's generation couldn't: formal business education combined with engineering knowledge, and most importantly, a global perspective.

The family business dynamics here are worth unpacking. In many Indian family businesses, the third generation is where things either professionalize or fall apart. The founder builds it, the second generation maintains it, but the third generation? They either destroy it through complacency or transform it through ambition. Pratik Patel chose transformation.

III. The Strategic Pivot: Water Infrastructure (1990s-2000s)

The 1990s marked India's economic liberalization, and Jash was ready. In 1996, the company converted into a closely held Public Limited Company under name Jash Engineering Limited. But this wasn't just a routine corporate restructuring. This was the company preparing for something bigger.

The real game-changer came with the company's first major international collaboration. Entered into Technical & Financial Collaboration with Schuette group, Germany. 20% equity given to Mr. Axel Schuette, who joins the board as a director.

Think about what this meant: a family-owned Indian engineering company was giving up 20% equity to a German partner. This wasn't desperation; this was strategic brilliance. The Schuette collaboration brought world-class technology to India at a time when the country was desperately modernizing its infrastructure.

The late 1990s saw rapid expansion. Between 1997-1999, expansion of facilities and addition of new line of bulk solids handling valves in product range. But the real masterstroke came in 2000.

In 2000, the company entered into Technical Collaboration with Hollung AS, Norway for manufacture of Fine Step Screens. Jash become the first company to introduce fine screening equipments in India. First mover advantage in a market of 1.3 billion people? That's the kind of moat Warren Buffett dreams about.

The company didn't stop there. In 2002, it entered into Technical Collaboration with Hollung AS, Norway for manufacture of Coarse bar screens. By 2005, expansion in manufacturing facilities for screens made it the largest manufacturer of Fine screens in India.

But here's what's fascinating about this period: while everyone else in India was chasing IT and software—the "new economy"—Jash was quietly dominating the decidedly unsexy but absolutely essential water infrastructure space. No venture capitalists were writing blog posts about water control gates. No one was calling them a unicorn. They were just methodically building market share, one technical collaboration at a time.

Then came a critical acquisition that would reshape the company's trajectory. Acquisition of Shivpad Engineers Private Limited, Chennai, leaders in manufacturing mechanical processing equipment like Clariflocculators, Digesters, Clarifiers, Aerators, Classifiers, Detritors etc, required in water and waste water treatment plants. This wasn't just buying a competitor; this was vertical integration at its finest.

The technical collaborations continued to accelerate. Entered into technical collaboration with Rehart, Germany to manufacture Archimedes screw pumps and Hydro-power generators. Each partnership wasn't random—it was carefully chosen to fill a specific gap in Jash's product portfolio or to bring a new technology to the Indian market.

IV. The Growth Acceleration Era (2000s-2015)

The 2000s marked Jash's transformation from a regional player to a company with serious global ambitions. The infrastructure expansion during this period was staggering. Establishment of new plant (Unit 2: Fabricated Products Plant) comprising of 65,000 sq feet built up area for Stainless steel products and 85,000 sq feet for Carbon steel products.

Let's put this in perspective: 150,000 square feet of manufacturing space dedicated to specialized water infrastructure products. This wasn't speculative capacity building—this was responding to real demand from India's rapidly modernizing cities and industries.

The financial validation came in 2012 with a significant development. Pragati India Fund invests 5 million Dollars into Jash equity with a commitment to invest 4 million Dollars more, if required. When private equity comes knocking at your door in the water infrastructure business, you know you're doing something right. This wasn't some fly-by-night VC looking for a quick flip—Pragati was betting on India's long-term infrastructure story, and Jash was their vehicle.

The technical collaboration strategy continued to evolve. Entered into technical collaboration with Mahr Maschinenbau GmbH, Austria for manufacturing of "MM2MM" Multi Raking Bar Screens, Travelling band screens, Perforated screens & screening conveying equipment. Each partnership added another layer to Jash's competitive moat.

What's remarkable about this period is the patience. While the Indian startup ecosystem was beginning to heat up with companies racing to raise rounds every 12-18 months, Jash was playing a different game entirely. They were building manufacturing capabilities that would take years to replicate, establishing relationships that couldn't be bought, and creating technical know-how that couldn't be easily copied.

The company's market position by the mid-2010s was formidable. They weren't just participating in India's water infrastructure boom—they were enabling it. Every new water treatment plant, every sewage facility, every industrial water system needed their products. And with their technical collaborations, they could offer solutions that their purely domestic competitors simply couldn't match.

V. Going Public & The SME IPO (2017)

October 2017. The Indian stock market is buzzing with tech IPOs and new-age businesses. And then there's Jash, choosing to list not on the main board, but on the NSE SME exchange. The Jash Engineering IPO opens on September 28, 2017 and closes on October 3, 2017.

The numbers tell an interesting story. The IPO is a SME IPO of 40,00,800 equity shares of the face value of ₹10 aggregating up to ₹48.01 Crores. The issue is priced at ₹120 per share. The fresh issue of 22,61,198 equity shares aggregating to Rs. 27.13 crores and an offer for sale of 17,39,602 equity shares aggregating up to Rs. 20.88 Crores by Pragati India Fund Limited.

Notice what's happening here: Pragati India Fund, which invested in 2012, is taking some money off the table five years later. That's patient capital by Indian standards, and they're not even fully exiting—just partial monetization.

The market reception was telling. The shares of Jash Engineering Limited were listed at 144.00 per share and are currently trading at 608.60 per share. That's a 20% pop on listing day—not bad for a company making water control gates when everyone's obsessed with e-commerce and fintech.

But why the SME exchange? This is where it gets strategic. The SME platform had less stringent requirements, lower costs, and honestly, less scrutiny. For a company like Jash, which was profitable and growing but not yet at the scale of main board companies, it was perfect. They could access capital markets, provide liquidity to early investors, and use the IPO as a stepping stone for bigger things.

The IPO proceeds weren't earmarked for some moonshot project. This was about boring but essential stuff: working capital and gradual expansion. No fancy investor deck promising to "revolutionize water infrastructure with AI and blockchain." Just solid, steady growth.

The Jash Engineering IPO listing date is on Wednesday, October 11, 2017, and with it, the company entered a new phase. Public market scrutiny would bring discipline, quarterly reporting would bring transparency, and the equity currency would enable future acquisitions.

VI. The Rodney Hunt Acquisition: America Calling (2016-2017)

Now here's where the story gets really interesting. While preparing for their IPO, Jash pulled off what might be their most audacious move yet.

JASH USA Inc. bought the company and its intellectual property on Sept. 21, 2016. But this wasn't buying some hot startup or growing business. No, they were buying a piece of American industrial history. Rodney Hunt was founded in 1840 by Mr. Rodney Hunt, and the company pioneered the use of stainless steel as a common material of construction in the 1930's.

Think about that timeline: Rodney Hunt was founded before the American Civil War. It had survived a Civil War, two World Wars, The Great Depression, two devastating floods, and a fire. And then came 2016. Rexnord, which formerly owned Rodney Hunt, closed the plant in 2016 and moved its 200 jobs to Pittsburgh.

This is where Jash saw opportunity where others saw a dying business. An American company with 176 years of history, pioneering technology, and established relationships was available because its corporate parent didn't want to deal with it anymore. The brand alone was worth something, but the real value was in the intellectual property, the customer relationships, and the Made-in-America credentials that would open doors Jash could never access as a purely Indian company.

The turnaround story is remarkable. Since the acquisition, Jash has invested more than $12 million in Rodney Hunt to help it become the number one gate company. Under Jash, Rodney Hunt has grown exponentially and expanded our workforce to close to 50 employees in Orange, MA.

The company didn't just restart operations; they modernized them. Starting of Rodney Hunt manufacturing facility covering 60,000 sq feet at Orange, Massachusetts, USA in 2018. This wasn't financial engineering or asset stripping—this was genuine industrial revitalization.

But here's what's brilliant about this acquisition: it gave Jash something money couldn't easily buy—American credentials. In the water infrastructure business, especially for municipal projects in developed countries, being able to say "Made in America since 1840" opens doors that "Made in India since 1948" simply cannot.

The acquisition also came with surprises. Also included in the transaction are the SCUBA, BASCULE, and PELICAN products and the hydraulic product line. These weren't just random products; they were specialized solutions for specific water control applications that Jash could now offer globally.

By 2024, the transformation was complete. Mr. Patel also plans to invest another $10 million in the next few years to improve the overall infrastructure. From a shuttered plant that had lost 200 jobs to a growing facility with expansion plans—that's value creation.

VII. International Expansion & The UK Play (2019-2024)

While Rodney Hunt was being revitalized in America, Jash wasn't standing still in other markets. The company continued its infrastructure expansion with establishment of new plant (Unit 4 : SEZ Fabricated Products Plant) of 50,000 sq feet built up area at Special Economic Zone (SEZ), Pithampur, District – Dhar, MP in 2019.

The SEZ facility was strategic for multiple reasons. First, it provided tax benefits for exports. Second, it allowed for easier import of raw materials and equipment. Third, it signaled to international customers that Jash was serious about serving global markets with world-class facilities.

But the real coup came in 2024 with another strategic acquisition. The Company acquired 80% shares of Waterfront Fluid Controls Limited, Glasgow, Scotland, UK, on 30 April, 2024. Jash has purchased an 80% stake in Waterfront, which has seen a 25% increase in export sales over the last 12 months.

The Waterfront acquisition is fascinating for several reasons. First, the company wasn't in distress like Rodney Hunt. Waterfront Fluid Controls was founded by Neil Betteridge in 2006, following the expansion of his former business, Waterfront Engineering Services, which he set up 10 years earlier. This was an entrepreneur who had built something valuable and was looking for the right partner to take it to the next level.

The acquisition cost was GBP 2 million according to the initial agreement in May 2023. But the real investment came after. As a result of the acquisition, there has been a £500,000 investment in the new UK arm of the business, which will see the factory expanded and a full office refurbishment.

What's brilliant about this deal structure is that Neil, Director of Sales and Marketing, and Liz Niven, Director of Operations, will continue in their positions and retain shares in the business. This isn't a case of Indian company comes in, fires everyone, and moves production to India. No, this is about preserving what works while providing capital and scale.

Neil Betteridge's own words are telling: "I've been speaking to Jash for many years about shared equity. They approached us and it was the perfect time". This wasn't a desperate seller or an opportunistic buyer—this was a meeting of minds.

The strategic importance cannot be overstated. "Jash is already well established and this is an avenue into the UK and markets they've not had before. It's a really good fit between the two companies". With Rodney Hunt providing U.S. access and Waterfront providing UK/European access, Jash now had manufacturing and market presence on three continents.

VIII. Modern Era & Future Bets (2020-Present)

The 2020s have seen Jash accelerate rather than slow down. The company has been executing on multiple fronts simultaneously, each move calculated to strengthen its position in the global water infrastructure market.

The Shivpad integration represents a significant consolidation. Shivpad Engineers Pvt Ltd has been merged with the Company as Unit-5 effective 1st April, 2024. This wasn't just paper shuffling—this was about operational efficiency and unified go-to-market strategy. According to the company's regulatory filing under SEBI (LODR) Regulations, the production at the facility began on August 1, 2025 at a new facility, showing the company's commitment to expanding Shivpad's capabilities post-merger.

But perhaps the most interesting development is the joint venture with German technology. In 2023, INVENT Umwelt‐ und Verfahrenstechnik AG has joined forces with Jash Engineering Ltd. to establish a joint venture. This strategic collaboration aims to combine their respective strengths and expertise to deliver innovative solutions to the water industry in India.

This JV, JASH Invent India Pvt Ltd, was created as a joint venture between JASH and Invent Umwelt Und Verfahrenstechnik AG, Germany with a 50-50 partnership. Jash Engineering will manufacture a range of aerators, diffusers, mixing and aeration equipment, decanting equipment, and turbo blowers and the JV will market these products.

The timing is impeccable. The joint venture seizes this opportunity, strategically positioning INVENT for incremental growth in a market forecasted to expand its water and wastewater treatment market from approximately USD 1.5 billion in 2023 to over USD 2.3 billion by 2028, growing annually by over 9%.

Infrastructure expansion continues aggressively. Construction of a new SS Products assembly plant of approx. 28,000 square feet at Unit 2 have been completed and this plant was commissioned in Sept'23. Every new facility isn't just capacity—it's capability. Stainless steel fabrication requires different skills and equipment than cast iron or carbon steel. By expanding into specialized facilities, Jash can serve increasingly sophisticated customer requirements.

The financial performance reflects these strategic moves. Jash Engineering Ltd (NSE:JASH) reported a significant revenue growth of 61% compared to the same period last year. Profit after tax grew by 212%, indicating strong financial performance in Q2 FY25.

The order book tells the real story. The company has a strong order book position, standing at 873 crore as of November 1st. In a business where projects can take years from order to completion, a strong order book is like having years of revenue already locked in.

Looking ahead, management's ambitions are clear. They're targeting ₹1000 crore revenue by FY 2028. Given they're at ₹748 crore now, that's about 33% growth needed—aggressive but achievable given their track record and market position.

IX. Playbook: Building a Water Infrastructure Empire

Let's step back and decode what Jash actually did here. This wasn't luck or being in the right place at the right time. This was methodical empire building, and there's a playbook worth understanding.

Technical Collaboration as Growth Strategy: Rather than trying to develop everything in-house, Jash systematically partnered with global technology leaders. Each collaboration brought not just technology but credibility. When you're selling to Singapore's water authority or a U.S. municipality, saying "we use German technology" or "Norwegian design" matters.

Buy vs. Build: The company showed remarkable discipline in knowing when to build organically versus when to acquire. Rodney Hunt and Waterfront weren't random acquisitions—they were strategic moves to acquire geography, heritage, and customer relationships that would take decades to build organically.

Geographic Diversification: With presence on 4 continents through its wholly owned subsidiaries, Jash is a global company deriving over 60% of its revenue from supply of equipment to projects outside India. This isn't just about reducing India risk—it's about being close to customers, understanding local requirements, and being seen as a local player rather than an Indian exporter.

Product Portfolio Expansion: From water control gates to screening equipment to treatment systems, each addition to the portfolio made Jash more valuable to customers. Water authorities don't want to deal with dozens of suppliers—they want integrated solutions from credible partners.

Family Business Professionalization: The transition from founder to third generation could have been a disaster. Instead, it became a strength. Professional management with family commitment—that's a powerful combination when executed well.

Capital Efficiency: Despite all this expansion, the company has remained remarkably capital efficient. They haven't raised massive rounds or taken on crushing debt. The IPO raised just ₹48 crores—that's roughly $6 million. Companies in Silicon Valley raise that in a pre-seed round.

X. Analysis & Investment Case

Bull Case:

The macro story is compelling. The expenditure on industrial water and wastewater infrastructure in India was $2.87 billion in 2024 and will increase to $4.65 billion by 2030. That's a 62% increase in just six years. And that's just India—globally, the numbers are even more staggering.

The company's competitive position is formidable. With over 70% market share in water control gates and over 80% market share in bed plates in India, Jash has the kind of market dominance that's extremely difficult to displace.

International growth prospects remain robust. Revenue growth within India should be approximately 10% in FY 2024-25 and 15% beyond FY25. Outside India, the growth rate should be 30% given the acquisition of Waterfront Fluid Controls in April 2024 and healthy demand in the Rodney Hunt business.

The business model has attractive characteristics. Water infrastructure is essential, not discretionary. Municipalities and industries can defer upgrades but can't eliminate them. When water systems fail, they fail catastrophically—remember Flint, Michigan. This creates steady, long-term demand.

Operating leverage is kicking in. With revenue growth of 61% and profit after tax growth of 212%, profits are growing much faster than revenues. This is what happens when you've built the infrastructure and just need to run more volume through it.

Bear Case:

Project-based revenues create lumpiness. Unlike software companies with predictable monthly recurring revenue, Jash's revenues depend on project completion timing. A delayed project can shift millions from one quarter to another.

Working capital intensity remains high. Manufacturing physical products, especially large custom equipment, requires significant working capital. Cash conversion cycles are long, and growth consumes cash before it generates it.

Competition from Chinese manufacturers is intensifying. While Jash has technology and quality advantages, Chinese companies are moving upmarket and competing aggressively on price, especially in developing markets.

Currency and geopolitical risks are real. With 60% of revenue from exports and operations in multiple countries, currency fluctuations can significantly impact profitability. A strong rupee helps with imports but hurts export competitiveness.

Dependence on government spending creates vulnerability. Much of water infrastructure spending comes from government budgets. Political changes, fiscal constraints, or shifting priorities can impact demand.

The U.S. regulatory environment is challenging. The company faces challenges in the US market due to the 'Build America, Buy America' Act, which requires a significant portion of products to be manufactured domestically. This could limit Rodney Hunt's ability to leverage Jash's Indian manufacturing.

XI. Key Inflection Points

Looking back, several moments stand out as crucial turning points:

1994-1996: Public Conversion & Professionalization The Company got converted into a Public Limited Company and the name of the Company was changed to "Jash Engineering Limited" on September 21, 1994. This set the stage for external partnerships and eventual public listing.

2000s: Technical Collaborations The systematic partnering with Norwegian, German, and Austrian companies transformed Jash from a local player to one with global technology. Each partnership was a building block for the next level of growth.

2012: PE Investment Pragati India Fund's investment provided not just capital but validation. It signaled that professional investors saw value in water infrastructure, legitimizing the sector for future investors.

2016-17: Rodney Hunt Acquisition Buying a 176-year-old American company was audacious. It could have been a disaster—instead, it became a transformation catalyst, providing U.S. market access and global credibility.

2017: IPO Going public brought discipline, transparency, and currency for acquisitions. The SME listing was a clever stepping stone rather than a destination.

2024: Waterfront Acquisition Adding UK/European presence completed the geographic triangle. With manufacturing in India, the U.S., and the UK, Jash became a truly global player.

XII. Epilogue & Future Outlook

Water scarcity isn't a future problem—it's a current crisis. By 2030, the world is projected to face a 40% shortfall in freshwater supply. Climate change is making wet places wetter and dry places drier. Aging infrastructure in developed countries needs replacement. Developing countries need new infrastructure. It's a perfect storm of demand.

India alone needs massive infrastructure investment. The government has approved 56 new Watershed Development Projects across 10 high-performing states, with a budget of Rs. 700 crore (US$ 80.9 million). Multiply this across states, across countries, and you begin to see the opportunity.

The company's target of ₹1000 crore revenue by FY 2028 seems conservative given the market opportunity. But that's the Jash way—under-promise and over-deliver rather than the Silicon Valley model of over-promise and under-deliver.

M&A will likely continue. With established platforms in India, the U.S., and the UK, bolt-on acquisitions make sense. Small specialized companies in areas like smart water management or IoT-enabled infrastructure could be targets.

Technology evolution will be crucial. The water industry is slowly digitizing. Smart water meters, IoT sensors, AI-driven predictive maintenance—these aren't Jash's core competencies today, but they'll need to be part of the solution tomorrow.

The big question is succession. Pratik Patel has built something remarkable, but he won't run it forever. Whether the fourth generation of the family steps up or professional management takes over will determine whether Jash becomes a century-old company or gets acquired by a larger player.

But here's what's certain: water infrastructure isn't going away. If anything, it's becoming more critical. And companies that can deliver reliable, high-quality solutions at scale will win. Jash has spent 75 years building the capabilities to be one of those winners.

From Jashbhai Patel's workshop in 1948 to a global water infrastructure leader in 2024—it's been quite a journey. But in many ways, the story is just beginning. Because while software might eat the world, the world still needs water. And increasingly, that water needs Jash.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube