Team, Inc.: The Rise, Fall, and Struggle for Survival of an Industrial Services Empire

I. Introduction: From Market Darling to Delisting Danger

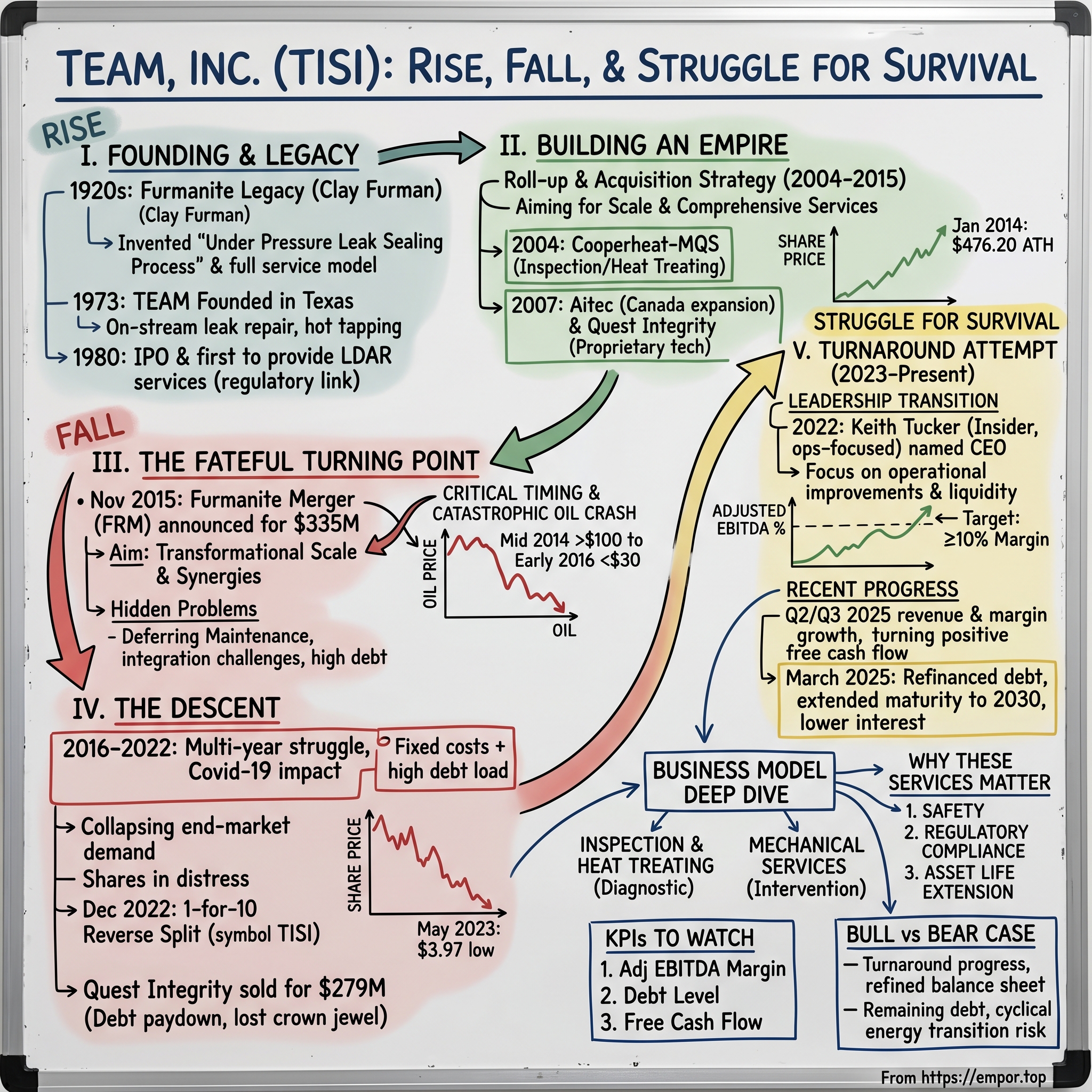

Picture this: It's January 10, 2014, and somewhere in a refinery control room along the Texas Gulf Coast, a Team, Inc. technician is sealing a high-pressure leak while the plant runs at full capacity. The stock closes that day at $476.20 per share—its all-time high. Fast forward to May 16, 2023, and that same share trades at $3.97, a 99% collapse that nearly cost the company its NYSE listing.

The stock reached its highest end of day price of $476.20 on January 10, 2014, and its lowest at $3.97 on May 16, 2023. What happened in between tells a story of acquisition ambition run amok, catastrophic timing, and the brutal economics of servicing cyclical industries with a leveraged balance sheet.

Team, Inc., headquartered in Sugar Land, Texas, is a global, leading provider of specialty industrial services offering customers access to a full suite of conventional, specialized, and proprietary mechanical, heat-treating, and inspection services. The company deploys conventional to highly specialized inspection, condition assessment, maintenance, and repair services that result in greater safety, reliability, and operational efficiency for customers' most critical assets.

The company operates in a world most investors never see—the dangerous interiors of refineries, petrochemical plants, pipelines, and power generation facilities. When a valve leaks toxic chemicals under extreme pressure, or a critical pipe needs heat treatment to maintain structural integrity, Team's technicians are the ones who respond. It's mission-critical work: failure doesn't just mean lost revenue—it means explosions, environmental disasters, and loss of life.

The central question of this story is uncomfortable but essential: How did a company providing these indispensable services, with over a century of combined heritage through its Furmanite acquisition, destroy so much shareholder value? In 2024, Team, Inc.'s revenue was $852.27 million, a decrease of -1.20% compared to the previous year's $862.62 million. Losses were -$38.27 million, -49.47% less than in 2023.

The answer involves a classic roll-up strategy that worked brilliantly until it didn't, a transformational merger closed at precisely the wrong moment in the commodity cycle, and a multi-year struggle to survive under crushing debt. It's a cautionary tale for any investor seduced by acquisition-driven growth stories in cyclical industries.

Yet there's also a turnaround narrative emerging. Keith Tucker was appointed as TEAM's Interim Chief Executive Officer in March 2022 and Chief Executive Officer in November 2022. Tucker joined TEAM in 2005 and has served TEAM as President, Inspection & Heat Treating Group, Executive Vice President – North Division, Executive Vice President – Mid Continent Division and Vice President of the Great Lakes Region. Tucker has 32 years of industry experience, including various positions with Citgo and BP Amoco supporting the process safety management and inspection functions.

For investors, Team represents a fascinating case study in the limits of scale economics in services businesses, the perils of leverage in cyclical industries, and the operational mechanics of corporate turnarounds.

II. The Furmanite Legacy: A Century of Leak Sealing (1920s–1972)

Before there was Team, there was Furmanite—and before there was Furmanite, there was Clay Furman's simple yet revolutionary idea.

TEAM, Inc. has a long legacy of delivering innovative industrial services, safety solutions, and technical expertise. Its heritage is built on more than a century of pioneering advancements in inspection, repair, and maintenance technologies, starting in the 1920's when the Leak Sealing process was developed under the company name, FURMANITE.

The story begins in the early 1920s when Eugene Clay Furman developed a solution to one of industry's most costly problems: leaks in operating equipment. In an era before sophisticated materials science, industrial facilities faced a brutal choice when pipes, valves, or vessels began leaking—shut down the entire process for repairs, or continue operating while risking catastrophic failure.

The first do-it-yourself Leak Sealing kits were developed and marketed by Clay Furman and while they worked as advertised, he struggled to find an audience that would listen to his revolutionary achievement. Furman's kits did not gain wide acknowledgement and acceptance until the US Navy reviewed their performance favorably in the "Bulletin of Engineering Information" November, 1926 edition following a series of practical evaluations on the USS Melville and the USS Memphis.

This Navy endorsement proved transformational. The US customer reference list that includes individual warships in the US Navy, US steel companies and other US industrial operations using the Furmanite Corporation Leak Sealing Kits. Several of these companies still exist, though as with Standard Oil under a different name, and remain customers of TEAM to this day.

The leak sealing process patent filed in 1927 was the first such patent for this process and established Furmanite as the inventor and originator of the "Under Pressure Leak Sealing Process."

The company didn't just pioneer the technology—it pioneered an entirely new service model. In 1929, Furmanite Engineering Company Limited moved from selling "kits" to a full leak sealing service company employing its own engineers and leak-sealing technicians.

The transformation from product company to service company was driven by a visionary consultant. Alan Forsyth, acting as a consultant to Furmanite Engineering (1929) advised the Board to move from selling low pressure leak sealing kits into providing a leak sealing service as well as introduce other mechanical add-on service lines. Alan Forsyth can be regarded as the pioneer of today's modern leak sealing industry. It was Alan that moved the company to "service" from selling a kit product, that drove the move to ever higher pressures and temperatures, that identified complimentary technologies such as on-site machining and controlled bolting, which expanded the service offering and allowed clients to entrust larger packages of work to a specialist company.

This shift from selling kits to providing comprehensive services established the business model that would define the industrial services industry for the next century. Instead of teaching customers to fix their own problems, Furmanite positioned itself as the specialist—the experts you called when something critical was leaking and shutting down wasn't an option.

Furman sold the business to a United Kingdom-based licensee in the early 1950s. Furmanite remained a British-based company until 1991, when Kaneb bought it and moved the headquarters to the United States.

Understanding why this business model works requires understanding its customers' economics. For a refinery processing hundreds of thousands of barrels of crude per day, every hour of unplanned downtime represents millions in lost revenue. A specialized leak-sealing service that costs tens of thousands of dollars but saves millions in avoided shutdowns represents extraordinary value—if it actually works under the extreme conditions of industrial operations.

This value proposition explains why customers couldn't simply do these services themselves. While refineries employ massive maintenance staffs, the specialized expertise required for on-stream leak repair, advanced non-destructive testing, or precision heat treatment justifies outsourcing to specialists. It's the same logic that drives hospitals to outsource specialized imaging to radiology groups or manufacturers to outsource precision machining to specialty shops.

III. The Founding of TEAM & Early Growth (1973–2003)

While Furmanite was becoming a global force in leak sealing, a parallel story was unfolding in Texas that would eventually merge with it decades later.

TEAM was founded as an on stream leak repair and hot tapping company. The Company began with five locations, 60 people and three service lines.

The company was founded in 1973 and is headquartered in Sugar Land, TX. The timing was hardly accidental. The 1973 oil embargo and resulting energy crisis was transforming the American industrial landscape, dramatically increasing the value of keeping refineries and petrochemical plants running at maximum capacity. The demand for specialized maintenance services that could work on operating equipment—without costly shutdowns—was surging.

TEAM was traded on the NYSE stock exchange (Symbol: TISI). The company went public in 1980—remarkably early for a specialty services firm of its size, suggesting both the growth trajectory and the capital needs of the business.

In 1980, TEAM became the first company to provide LDAR (Leak Detection and Repair) services. TEAM provides LDAR services for hundreds of customers and maintains millions of records to document compliance.

The LDAR innovation deserves special attention because it illustrates how regulatory changes create market opportunities. The Clean Air Act and subsequent EPA regulations required industrial facilities to systematically identify and repair equipment leaks of volatile organic compounds. Rather than develop these capabilities internally, most facilities outsourced to specialists like Team who could maintain the complex documentation required for regulatory compliance.

This created a recurring revenue stream fundamentally different from emergency leak repairs. LDAR contracts provided predictable income while building deep relationships with facility operators who would naturally turn to Team for other services when problems arose.

The company's trajectory through the 1990s and early 2000s reflected the broader growth of the industrial services sector. As refineries and chemical plants aged, maintenance requirements increased. As environmental and safety regulations tightened, the need for specialized inspection and testing services grew. And as facilities sought to minimize downtime, demand for on-stream repair capabilities expanded.

By the early 2000s, Team had established itself as a significant player in specialty industrial services, with a focus on the Gulf Coast petrochemical and refining complex—the heart of American industrial infrastructure. The stage was set for the acquisition-driven expansion that would define the company's next decade.

IV. The Acquisition Machine: Building Scale (2004–2015)

The transformation of Team from a regional specialty services provider into an international industrial services conglomerate began in earnest in 2004 with a deal that would reshape the company's capabilities.

On August 11, 2004, TEAM purchased substantially all of the assets of Cooperheat-MQS Inc. and its parent company, International Industrial Services Inc. Cooperheat-MQS was a leading provider of non-destructive testing (NDT) inspection and field heat treating services throughout the U.S. and Canada.

This acquisition deserves attention because it fundamentally expanded Team's service capabilities. Non-destructive testing—using techniques like ultrasonic waves, X-rays, and magnetic particles to identify defects without damaging equipment—was complementary to Team's existing leak repair and hot tapping services. Heat treating, which involves precisely controlled heating and cooling of metal components to achieve desired properties, added another specialized capability.

The strategic logic was compelling: customers who needed leak repairs often also needed NDT inspection. By offering both, Team could capture more spending from existing customers while providing more comprehensive solutions. This "single-source" provider model would become central to Team's value proposition.

The geographic expansion continued. On June 1, 2007, TEAM acquired Aitec, Inc and related companies, an NDT inspection services company that was headquartered near Toronto with 13 service locations across Canada, including large operations in Alberta and Ontario. This acquisition expanded TEAM's inspection services into Canada.

The Canadian expansion was strategically important given the growth of the Alberta oil sands and associated petrochemical development. It also established Team's international capabilities—critical for serving major oil companies with global operations who preferred working with vendors who could support them across geographies.

TEAM purchased Leak Repairs Specam ("LRS") from the GTI Group in the Netherlands. GTI was an affiliate of the Suez Group. LRS, which is headquartered in Vlissingen, The Netherlands, provided a range of services including on-stream leak sealing, hot tapping, fugitive emissions monitoring, field machining, and bolting services. This purchase provided TEAM with its initial operating presence in Europe.

The Quest Integrity Acquisition

Team's largest and most significant acquisition during this period targeted advanced technology capabilities. Team effectively purchased 95% of Quest Integrity for a total consideration of $42.6 million, consisting of a cash payment of $39.1 million and the issuance of $3.5 million in TISI restricted common stock (approximately 186 thousand shares).

Headquartered near Seattle, Washington, Quest Integrity has leading technical capabilities related to the measurement and assessment of facility and pipeline mechanical integrity. It has developed several proprietary tools for advanced tube and pipeline inspection and measurement. Supporting and augmenting these proprietary inspection tools, Quest Integrity has an advanced technical team that provides specialized engineering assessments of facility conditions and serviceability. The company maintains operations in Seattle, Boulder, and New Zealand, and has service locations in Houston, Calgary, Australia, The Netherlands, and the Middle East.

Quest Integrity represented an important strategic shift. While Team's traditional services were labor-intensive, Quest brought proprietary technology—specialized inspection tools that provided differentiated capabilities. For calendar year 2010, Quest Integrity Group revenues and EBITDA are estimated to be approximately $22 million and $5 million, respectively.

Additional Tuck-In Acquisitions

The acquisition pace continued through 2015 with a series of smaller deals:

On July 6, 2015, TEAM strengthened its existing inspection and heat treating business with the acquisition of Qualspec Group.

By mid-2015, Team had assembled an impressive portfolio of capabilities through aggressive M&A. The company could offer customers NDT inspection, heat treating, leak repair, hot tapping, field machining, emissions monitoring, and advanced pipeline integrity assessment—a comprehensive suite of services for maintaining critical industrial infrastructure.

The strategy appeared to be working. The stock had appreciated dramatically, reaching that January 2014 peak of over $476 per share. But the very success of the acquisition strategy was creating the conditions for what would come next: the fateful decision to pursue an even larger, transformational deal.

V. The Transformational Furmanite Merger: A Fateful Decision (2015–2016)

In boardrooms across corporate America, there's a moment in every acquisition-driven growth story when executives face a fateful choice: consolidate gains and integrate recent acquisitions, or push forward with an even bigger deal that promises transformational scale. In November 2015, Team's leadership chose the latter.

Team, Inc. (NYSE:TISI) and Furmanite Corporation (NYSE:FRM) announced that the Boards of Directors of both companies have unanimously approved a definitive merger agreement under which Team will acquire all of the outstanding shares of Furmanite in a stock-for-stock transaction valued at approximately $335 million, including the assumption of debt, which is intended to be tax-free to Furmanite stockholders for U.S. federal income tax purposes.

The strategic rationale seemed compelling on paper. Furmanite Corporation (NYSE:FRM), founded in 1920, is one of the world's largest specialty industrial services companies, providing world class solutions to customer needs through more than 80 offices on six continents. The Company delivers a wide portfolio of inspection and mechanical services which help monitor, maintain and renew the global energy, industrial and municipal infrastructures. World Headquarters and Global Support Operations are located in Melbourne, Australia.

Under the terms of the proposed merger, Furmanite stockholders will receive 0.215 shares of Team common stock for each share of Furmanite common stock they own, representing an 8% premium to Furmanite's stock price based on the closing prices of Team and Furmanite's shares on October 30, 2015, the last trading day prior to announcement of the transaction, and an implied value of $7.53 per Furmanite share. The implied $7.53 per share value represents a 15% premium to the average Furmanite closing stock price over last 60 days prior to announcement.

The Synergy Case

The combined company expected to realize an estimated $20-$25 million in annual cost synergies within two years of closing. Synergies are primarily associated with the elimination of duplicative public company costs and back-office support functions.

Before synergies, Team expects the transaction to contribute ~$400M/year in revenue and $38M in annual adjusted EBITDA.

Merger Completion

Team, Inc. (NYSE:TISI) completed the acquisition of Furmanite Corporation (NYSE:FRM) on February 29, 2016.

As a result of the merger transaction, Team issued approximately 8.3 million shares of its common stock. With the completion of this merger, Team fortifies its foundation as a premier NDT inspection and specialty mechanical services company with a strong presence in North America, with more than 8,300 employees and 220 locations in 22 countries. The merger approximately doubles the size of Team's mechanical services capabilities.

As a result of the Merger, Furmanite shareholders own approximately 27% of the combined company.

Ted W. Owen, Team's President and Chief Executive Officer at the time, proclaimed the deal's virtues: "Finalizing the merger of Team and Furmanite is great news for our employees and customers. Team and Furmanite both have long-term, successful histories and together, are expected to have an even brighter future."

The Hidden Problems

But the timing couldn't have been worse. Oil prices, which had been above $100 per barrel in mid-2014, had crashed below $30 by early 2016. The 2014-16 collapse in oil prices was driven by a growing supply glut, but failed to deliver the boost to global growth that many had expected.

For Team's customers—refineries, petrochemical plants, and pipeline operators—the oil crash meant slashing capital expenditures and deferring maintenance wherever possible. The very services Team was positioning itself to dominate were seeing demand collapse just as the company was taking on integration challenges and debt from the merger.

Since TEAM's acquisition of FURMANITE our dedication to excellence, customer-focused solutions, and industry leadership has earned us a strong reputation globally, supporting critical industries such as refining, petrochemical, and power generation.

The combination of integration complexity and collapsing end-market demand would set the stage for years of struggle. What looked like a transformational combination would instead become a case study in the perils of cyclical M&A timing.

VI. The Descent: From $476 to Penny Stock (2016–2022)

The years following the Furmanite merger read like a slow-motion corporate disaster. What had been presented as a transformational combination instead became a weight that would drag Team toward insolvency.

The Oil Price Impact

When your primary customers are oil refineries and petrochemical plants, an oil price crash doesn't just hurt revenue—it fundamentally changes customer behavior. Refining margins compress. Capital budgets get slashed. And maintenance spending—which is easier to defer than essential production spending—becomes the first target for cuts.

For Team, this meant that the very scale advantages the Furmanite merger was supposed to create became liabilities. Fixed costs that made sense at peak utilization became crushing burdens as revenue declined. The debt taken on to finance acquisitions required servicing regardless of business conditions.

The Integration Challenges

Roll-up strategies in services businesses always face integration challenges, but the Furmanite combination was particularly complex. The company had grown through numerous acquisitions into a sprawling global operation that defied easy management.

The numbers tell the story. At its peak, Team had grown to over $1 billion in revenue and more than 7,000 employees across more than 200 locations in over 20 countries. Managing that complexity required sophisticated systems—but the acquisition pace had outrun the company's ability to standardize operations.

COVID-19 and the Breaking Point

If the oil crash of 2014-2016 was a severe blow, the COVID-19 pandemic in 2020 was nearly fatal. Industrial activity collapsed globally. Refineries operated at reduced capacity. Capital projects were postponed or cancelled. And Team's technicians—who needed to be physically present at customer sites—faced all the disruptions of pandemic restrictions.

The company's stock, which had already fallen precipitously from its 2014 highs, entered true distress territory. By late 2022, shares were trading below $1—the minimum price threshold for NYSE listing compliance.

The Reverse Stock Split

On December 21, 2022, Team, Inc. announced that it has completed the previously announced reverse stock split of the outstanding shares of the Company's common stock, par value $0.30 per share, at a ratio of one-for-ten, effective at 5:00 p.m. Eastern Time.

The Common Stock began trading on a split-adjusted basis at market open on December 22, 2022. Trading in the Common Stock continued on the New York Stock Exchange under the symbol "TISI," with a new CUSIP number.

The Reverse Stock Split also effected a proportionate reduction in the Company's authorized shares of Common Stock from 120,000,000 shares to 12,000,000 shares.

The reverse split served its immediate purpose—keeping the stock above the NYSE's minimum price threshold—but it was a stark symbol of how far the company had fallen. A shareholder who had bought at the 2014 peak and held through the reverse split would have seen their position decline by over 97% in value.

The Quest Integrity Sale

In a desperate move to shore up the balance sheet, Team sold its crown jewel. The company announced the closing of the previously disclosed sale of its Quest Integrity business to Baker Hughes, an energy technology company that provides solutions to energy and industrial customers worldwide, for approximately $279 million, reflecting certain estimated post-closing adjustments. The net proceeds to the Company (after payment of transaction related expenses and certain other fees) was approximately $270 million. The Company intended to use approximately $238 million of the proceeds to pay down term debt and to pay certain fees associated with that repayment and related accrued interest, with the remainder reserved for general corporate purposes.

Keith Tucker, TEAM's Interim Chief Executive Officer, stated, "We are pleased to close the Quest Integrity transaction, which represents an important step in our plan to refocus TEAM on its core Inspection and Heat Treating and Mechanical Services businesses. The cash proceeds provide for a substantial debt paydown that significantly strengthens our balance sheet and improves our financial flexibility while we continue to execute on our strategic initiatives designed to improve profitability and cash flow."

The Quest sale was bittersweet. The business Team had acquired for $43 million in 2010 sold for $279 million twelve years later—a spectacular return on that single investment. But selling it meant giving up the most technologically differentiated part of the portfolio to a major competitor, Baker Hughes, which could now offer Quest's proprietary inspection capabilities to its own customers.

VII. The Turnaround Attempt: Survival Mode (2023–Present)

The year 2023 marked the beginning of a new chapter for Team, Inc.—not a triumphant turnaround story, but a grinding struggle to rebuild from the wreckage of the previous decade.

Leadership Transition

Team, Inc. announced a leadership transition, effective March 21, 2022, including the departure of Amerino Gatti from his positions as Chairman and Chief Executive Officer. In connection with the leadership transition, the Board of Directors appointed Keith Tucker, currently the President of TEAM's Inspection and Heat Treating group, to the role of Interim Chief Executive Officer. Simultaneous with Keith Tucker's appointment, the Board also appointed Michael Caliel as non-executive Chairman of the Board.

Tucker had been serving as interim Chief Executive Officer since March 2022. "We are pleased to announce Keith's appointment as Chief Executive Officer. With his strong operational background and extensive knowledge of our client base, Keith is the right person to lead Team," said Michael Caliel, non-executive Chairman of Team, Inc.'s Board of Directors. "Over the last eight months as Interim CEO, Keith has taken decisive actions to improve financial results and enhance liquidity while establishing the groundwork for further performance improvement."

Tucker's profile is notably different from his predecessors. Decades of experience learning all facets of an organization and trusting those within have worked out well for Keith Tucker, CEO of TEAM Inc. Since its founding in 1973, TEAM has set the standard for asset performance optimization and integrity assurance across a wide range of industries and applications. Tucker has been with the company for 18 years.

Financial Reality Check

The current financial situation remains challenging. The Company's total debt as of December 31, 2024 was $325.1 million as compared to $311.4 million as of fiscal year end 2023. The Company's net debt (total debt less cash and cash equivalents), a non-GAAP financial measure, was $289.6 million at December 31, 2024.

Recent Progress

The operational improvements are real, even if the overall financial picture remains difficult. Team Inc (NYSE: TISI) reported its Q4 and full-year 2024 financial results, showing significant improvements in profitability despite flat revenues. The company generated Q4 revenues of $213.3 million and full-year revenues of $852.3 million.

The gross margin rose to $57.3 million, or 26.9% of revenues, representing a 330-basis-point expansion and a $6.9-million increase from the prior year. Operating income was $2.2 million against an $8.9-million loss in the fourth quarter of 2023.

Free cash flow for the fourth quarter reached $19.6 million from $8.1 million a year earlier. For the year, free cash flow totaled $13.3 million, a turnaround from a negative $21.4 million in 2023.

Net loss narrowed to $38.3 million from $75.7 million in 2023.

Debt Restructuring

As previously announced, the company successfully closed on a refinancing transaction in March 2025 that extended term maturities out to 2030 and lowered the Company's blended interest rate by more than 100 basis points.

On March 13, 2025, TEAM announced that it had successfully closed on a refinancing transaction that lowers the Company's cost of capital and terms out its capital structure. The Transaction consists of a First Lien Term Loan Facility provided by HPS Investment Partners, LLC that matures in March 2030 and is comprised of a funded $175.0 million Term Loan and a $50.0 million Delayed Draw Term Loan available to the Company subject to satisfying certain conditions.

2025 Performance

The momentum has continued into 2025. In Q2 2025, the company generated revenue of $248.0 million, up $19.4 million, or 8.5% over the second quarter of 2024, and grew gross margin to $68.1 million, a $4.5 million, or 7.1% increase over the second quarter of 2024.

For Q3 2025, the company generated revenue of $225.0 million, up $14.2 million, or 6.7% over the third quarter of 2024, grew gross margin to $58.0 million, a $4.5 million, or 8.4% increase over the third quarter of 2024, reported net loss of $11.4 million, and increased consolidated Adjusted EBITDA by 28.6% to $14.5 million (6.5% of consolidated revenue) up from $11.3 million (5.4% of consolidated revenue) for the third quarter of 2024.

In September 2025, the company completed the private placement of preferred stock with Stellix Capital Management, which strengthened our balance sheet and enhanced financial flexibility. This $75 million investment recognizes the impactful progress made to date in our ongoing program to improve margins and lower our cost structure, as well as reinforces the significant opportunities that remain for further improvements in margins and top-line growth.

"We have line of sight to full year 2025 revenue growth of approximately 5% and adjusted EBITDA growth of approximately 13%" according to CEO Keith Tucker.

VIII. Business Model Deep Dive

Understanding Team's current business requires understanding the two distinct segments that make up the company today.

Inspection and Heat Treating (IHT)

The IHT segment offers non-destructive evaluation and testing, radiographic testing, ultrasonic testing, magnetic particle inspection, liquid penetrant inspection, positive material identification, electromagnetic testing, alternating current field measurement, and eddy current testing services. This segment also provides long-range guided ultrasonic, phased array ultrasonic testing, terminals and storage inspection and management program, rope access, mechanical and pipeline integrity, and heat treating services.

Think of IHT as the company's diagnostic capabilities. When a refinery needs to know whether a critical pipe wall is thinning from corrosion, or whether a weld contains hidden defects, IHT technicians deploy sophisticated testing equipment to provide answers without damaging the equipment being tested.

Heat treating adds a different dimension—the ability to precisely control the thermal properties of metal components. Post-weld heat treatment, for example, relieves stresses in welded joints that could otherwise lead to premature failure.

Mechanical Services (MS)

The MS segment offers leak repair, engineered composite repair, emissions control/compliance, hot tapping, valve insertion, field machining, bolted joint integrity, vapor barrier plug and weld testing, and valve management services.

MS is the intervention side of the business. When diagnostics reveal a problem, MS technicians can often fix it—frequently while the equipment remains in service. Hot tapping allows new connections to be made to pressurized pipelines. Leak sealing stops escaping fluids without shutting down operations. Composite repairs can restore structural integrity to damaged components.

Geographic Footprint

Geographically, the company derives its key revenue from the United States, followed by other countries, and Canada.

Headquartered in Sugar Land, Texas, Team, Inc. is a global, leading provider of specialty industrial services offering customers access to a full suite of conventional, specialized, and proprietary mechanical, heat-treating, and inspection services. The company deploys conventional to highly specialized inspection, condition assessment, maintenance, and repair services that result in greater safety, reliability, and operational efficiency for customers' most critical assets. Through locations in 13 countries, they unite the delivery of technological innovation with over a century of progressive, yet proven integrity and reliability management expertise.

End Markets

Team Inc. is a leading provider of specialty industrial services, including inspection and assessment, required in maintaining and installing high-temperature and high-pressure piping systems and vessels that are utilized extensively in the refining, petrochemical, power, pipeline and other heavy industries.

Why These Services Matter

The value proposition comes down to three factors:

-

Safety: When pressurized systems containing hazardous materials fail, people die. The Deepwater Horizon disaster, which killed 11 workers and created an environmental catastrophe, began with failed seals and pressure control equipment. The Bhopal disaster killed thousands when toxic gases escaped from a chemical plant. Rigorous inspection and maintenance prevents these catastrophes.

-

Regulatory Compliance: The EPA, OSHA, and industry-specific regulators mandate regular inspection and testing of critical equipment. Non-compliance can result in fines, forced shutdowns, and personal liability for executives. Outsourcing to specialists like Team helps ensure compliance while documenting that required procedures were followed.

-

Asset Life Extension: Properly maintained equipment lasts longer. Rather than replacing a $10 million vessel, a combination of inspection, repair, and heat treatment can often extend its useful life by decades—at a fraction of the replacement cost.

IX. Porter's Five Forces Analysis

Threat of New Entrants: MODERATE

The industrial services industry presents a mixed picture for potential new entrants. On one hand, many services are labor-intensive with relatively modest capital requirements—a trained technician with appropriate equipment can start providing NDT services without massive investment.

On the other hand, significant barriers protect established players. Safety certifications take years to build. Customer relationships in mission-critical services depend heavily on trust and track record. Large industrial customers often maintain approved vendor lists that new entrants must qualify for—a process that can take years and requires demonstrated performance.

MISTRAS Group (NYSE:MG) is a leading, global provider of asset protection solutions, serving customers in the oil & gas, aerospace, manufacturing, infrastructure, and power generation industries. MISTRAS Services is dedicated to delivering the right set of solutions to its clients, offering multi-disciplined teams to perform multiple asset protection services. Combining inspection, maintenance, engineering, and data management services, MISTRAS Services helps to maximize clients' safety and operational uptime.

MISTRAS represents the type of well-capitalized competitor that makes new entry challenging. With established operations, recognized brand, and comprehensive service offerings, companies like MISTRAS make it difficult for new entrants to compete for major contracts.

Bargaining Power of Suppliers: LOW

Team's primary input is skilled labor—certified technicians who can perform specialized services. While qualified technicians command premium wages, no single supplier has leverage over Team. Equipment is generally available from multiple suppliers. Consumables (testing materials, sealants, etc.) are commoditized.

The constraint is labor availability rather than supplier power. Finding and retaining qualified technicians is an ongoing challenge, but this affects the industry broadly rather than giving any particular supplier leverage.

Bargaining Power of Buyers: HIGH

MISTRAS is a leading "one source" global provider of technology-enabled asset protection solutions used to evaluate the structural integrity of critical energy, industrial and public infrastructure. Mission critical services and solutions are delivered globally and provide customers with asset life extension, improved productivity and profitability, compliance with government safety and environmental regulations, and enhanced risk management operational decisions.

Large industrial customers—refineries, chemical plants, power generators—have substantial purchasing power. They can play vendors against each other, demand competitive pricing, and credibly threaten to bring services in-house. During industry downturns, this buyer power intensifies as customers aggressively cut costs.

The saving grace is that switching costs exist once services are being delivered. A vendor with deep knowledge of a facility's equipment, access credentials, and established relationships is difficult to displace. But this protection is incomplete—customers regularly rebid contracts and evaluate alternatives.

Threat of Substitutes: LOW-MODERATE

Some substitutes exist but generally don't threaten the core business. Customers can bring basic inspection services in-house, and some do. Advanced monitoring technology (remote sensors, predictive maintenance algorithms) may reduce the need for some periodic inspection.

But specialized repairs—on-stream leak sealing, hot tapping, precision heat treatment—have few substitutes. When a valve is leaking under 2,000 PSI of pressure, there's no remote monitoring solution that fixes the problem. Someone has to seal the leak.

Competitive Rivalry: HIGH

The industrial services industry is fragmented, with many regional and specialty players competing alongside larger national operators. Well-known competitors of MISTRAS Group include X-Ray Industries, Inc., Acuren, Aerotech Inspection & NDT (India) Private Limited and Oryx Midstream Services, LLC.

Price competition is intense, particularly during industry downturns when excess capacity leads vendors to cut prices to maintain utilization. The cyclical nature of end markets creates feast-or-famine dynamics that put constant pressure on margins.

X. Hamilton's 7 Powers Analysis

Scale Economies: MODERATE

Team offers these services in over 140 locations throughout the world.

Geographic density provides some scale benefits—a location serving multiple nearby customers achieves better utilization than one serving isolated facilities. Equipment can be shared across jobs. Overhead costs are spread over more revenue.

But services businesses have inherent limits to scale economies. Every job requires people on site. Unlike manufacturing, you can't produce inspection services in a central factory and ship them to customers. Labor costs scale roughly linearly with revenue.

Network Economies: WEAK

No significant network effects exist. Team's services don't improve as they add more customers. A refinery in Louisiana doesn't benefit from Team also serving a power plant in California.

Counter-Positioning: WEAK

Team's business model is well-understood and easily replicable by competitors. There's no differentiated approach that incumbents can't copy. The roll-up acquisition strategy that built Team's scale was simultaneously being pursued by competitors.

Switching Costs: MODERATE

Several of these companies still exist, though as with Standard Oil under a different name, and remain customers of TEAM to this day.

Long-term customer relationships provide some protection. Vendors who know a facility's equipment history, have established safety records, and maintain good relationships with operations personnel are difficult to displace. But services are often competitively bid, and customers can and do switch vendors.

Branding: MODERATE

For half a century, TEAM has been at the forefront of ensuring safety, reliability, and the longevity of industrial assets across numerous sectors including aerospace, pipeline, and the petrochemical industries. From its inception in 1973 to its current position as a global leader, TEAM's journey has been characterized by innovation, expertise, and an enduring dedication to excellence.

The Furmanite heritage provides credibility in leak sealing—the company literally invented the industry. But brand doesn't command a significant pricing premium. Customers choose vendors based on capabilities, track record, and price rather than brand loyalty.

Cornered Resource: WEAK

TEAM's digital platform launched in 2018, providing quantifiable digitally-driven asset integrity insights. Through the platform, users obtain increased operational efficiency and reliability with less rework and greater confidence in results through real-time reporting.

Team has some proprietary technology, but nothing that competitors can't replicate. The sale of Quest Integrity to Baker Hughes removed what was arguably the company's most differentiated technical capability. Current technology investments are focused on operational efficiency rather than creating unique customer-facing capabilities.

Process Power: MODERATE

"Over the years, one thing that has become profoundly clear to me is the value of employees and clients and the deep appreciation I have for the importance of building a positive culture within the organization," Tucker said.

Decades of accumulated expertise in specialized services provide some process advantage. Safety culture, operating procedures, and institutional knowledge are difficult for new entrants to replicate quickly. As of Oct 27, 2025, the company has 5.4K employees.

Overall Assessment

Team has WEAK overall competitive moats. The company competes primarily on reputation, geographic reach, and comprehensive service offering rather than structural advantages that would protect margins long-term. This reality helps explain why the company struggled so much when end markets turned down—without strong moats, there was nothing to protect against the full force of cyclical pressure.

XI. Playbook: Business & Investing Lessons

Lesson 1: The Perils of Acquisition-Driven Growth

Team's trajectory illustrates the inherent risks in roll-up strategies. Acquisitions can create scale, but they also:

- Add integration complexity that distracts management

- Create cultural conflicts between legacy organizations

- Accumulate debt that becomes crushing in downturns

- Risk buying at cycle peaks when valuations are highest

The Furmanite merger exemplifies all of these. Closed just as oil prices collapsed, it doubled the company's complexity while adding debt at precisely the wrong moment in the cycle.

Lesson 2: Timing Matters Enormously

The November 2015 Furmanite announcement came after oil had already fallen from $107 (June 2014) to around $45. By the February 2016 close, prices had dropped below $30. Counter-cyclical M&A requires fortress balance sheets—the ability to absorb integration challenges while revenues decline. Team didn't have that luxury.

Lesson 3: Cyclical Industries Require Financial Discipline

Team's business model features high operating leverage—substantial fixed costs (equipment, facilities, trained workforce) that don't decline proportionally with revenue. Combining high operating leverage with high financial leverage (debt) creates a toxic combination when revenues decline.

Net loss narrowed to $38.3 million from $75.7 million in 2023.

The improvement is real, but it's taken years of grinding work to get from the depths of 2022-2023 to even this level.

Lesson 4: The Debt Trap

Acquisition debt becomes crushing when revenues decline because: - Interest payments continue regardless of business conditions - Covenants can restrict operational flexibility just when flexibility is most needed - Refinancing becomes expensive or impossible when lenders see distress - Required debt service can force fire sales of assets (like Quest Integrity)

Lesson 5: Turnarounds Are Hard

For the year, free cash flow totaled $13.3 million, a turnaround from a negative $21.4 million in 2023.

Progress is being made, but from a deep hole. The stock remains far below historical highs even after the operational improvements of 2024-2025.

XII. Bear vs. Bull Case

The Bear Case

The bearish argument for Team rests on several structural concerns:

Balance Sheet Weakness

The Company's total debt as of September 30, 2025, was $302.8 million as compared to $325.1 million as of fiscal year end 2024.

While debt has declined, it remains substantial relative to the company's size and profitability. The company continues to operate at a net loss even as operational metrics improve.

Cyclical Vulnerability

Team's primary customers—refineries, petrochemical plants, and pipelines—face long-term questions about energy transition. If traditional hydrocarbon infrastructure declines faster than new opportunities (LNG, hydrogen, carbon capture) develop, demand for Team's services could follow.

Competitive Position

As analyzed above, Team lacks strong competitive moats. In a fragmented industry with many capable competitors, maintaining pricing power is challenging. MISTRAS operates as a leading provider in the public safety and asset integrity market with a comprehensive suite of inspection, testing, and data management services. This positions the company well to expand its reach into energy, industrial, and public infrastructure sectors.

History of Value Destruction

The track record from 2014 to 2023 destroyed enormous shareholder value. While management has changed and operational improvements are evident, institutional investors may be reluctant to trust a company with such a troubled history.

The Bull Case

The bullish argument focuses on the turnaround progress and potential for continued improvement:

Operational Momentum

The growth in adjusted EBITDA outpaced top-line growth, which is a testament to the solid progress being made on ongoing cost and margin improvement initiatives.

Looking ahead, the company expects to continue seeing strong operational and financial results in 2025 with year-over-year growth in the top line, continued improved performance from Canadian and other international operations, and further meaningful progress towards adjusted EBITDA target margin of at least 10%, all of which we believe will enhance shareholder value.

Management Alignment

The CEO's total yearly compensation is $1.66M, comprised of 45.2% salary and 54.8% bonuses, including company stock and options, and directly owns 1.16% of the company's shares, worth $795.44K.

Keith Tucker is an operations-focused insider who rose through Team's ranks over nearly two decades. His compensation is heavily weighted toward stock-based incentives, aligning his interests with shareholders.

Refinanced Balance Sheet

The remaining senior secured term loan was rolled into a $97.4-million Second Lien Term Loan maturing in 2030. Management highlighted that the refinancing extended maturities, lowered the blended interest rate by more than 100 basis points and improved liquidity.

Market Position

Management projects mid-single-digit top-line growth for 2025, driven by expanding higher-margin service offerings and market penetration into adjacent sectors such as midstream, aerospace and industrial lab testing.

Diversifying beyond traditional refining and petrochemical customers could provide more stable demand and potentially higher margins.

Depressed Valuation

As of the Nov 28, 2025, the market capitalization of Team Inc is 65.035M.

A market cap of ~$65-85 million for a company generating $850+ million in annual revenue represents extreme valuation compression. If the turnaround succeeds and the company returns to even modest profitability, the equity could appreciate substantially from current levels.

XIII. Key Performance Indicators to Watch

For investors monitoring Team's progress, three metrics deserve closest attention:

1. Adjusted EBITDA Margin

The ≥10% Adjusted EBITDA margin target remains the strategic North Star, with actions underway; continued SG&A leverage and mix shift to higher-margin markets (power, aerospace, LNG) are the levers.

This single metric captures both revenue quality and cost discipline. The company currently operates around 6-7% margins; reaching the 10%+ target would transform the equity value proposition.

2. Net Debt / Total Debt Level

At September 30, 2025, the Company's net debt (total debt less cash and cash equivalents), a non-GAAP financial measure, was $288.0 million.

Reducing absolute debt levels is essential to creating shareholder value. Every dollar of debt reduction directly increases equity value in a leveraged situation like this.

3. Free Cash Flow

Cash flow remains a focus given year-to-date working capital headwinds; Q3 CFO noted negative YTD FCF from refinancing and AR/AP dynamics expected to reverse in Q4 to support FCF.

Sustainable positive free cash flow would enable debt reduction without additional dilutive equity raises or asset sales.

XIV. Conclusion: A Century-Old Business Fighting for Its Future

The Team, Inc. story is ultimately a tale of two eras. The first era—from the 1920s founding of Furmanite through Team's 2014 peak—demonstrated how specialized industrial services could create substantial value. Clay Furman's leak-sealing innovation, Alan Forsyth's transformation from product to service company, and Team's aggressive acquisition strategy all built a substantial enterprise serving critical infrastructure.

The second era—from the Furmanite merger through the near-insolvency of 2022—demonstrated how quickly that value could be destroyed. Ill-timed M&A, excessive leverage, and the brutal economics of cyclical industries combined to evaporate over 95% of shareholder value.

Now the company stands at a crossroads. Tucker says the biggest lesson learned along the arc of his career is that leadership is not about title or position. "Rather, it's about influence and humility. Leadership is about others and not about yourself. Leaders give credit and take blame."

The operational turnaround is real. Margins are improving. Revenue is growing. Cash flow has turned positive. The balance sheet has been restructured. These are the necessary conditions for a successful turnaround—but they're not yet sufficient.

What remains is execution: continuing margin expansion, reducing debt, and navigating an uncertain energy landscape. If successful, the current depressed valuation could provide substantial upside. If unsuccessful—if another downturn hits before the balance sheet is fully repaired, or if operational improvements stall—the equity could face renewed existential pressure.

In the past six months, Tucker said the evolving culture within the organization — alongside improvements TEAM is making in its organizational structure — is setting up the company to reach new heights of success. "I believe our employees are seeing the momentum and are feeling proud to be a part of TEAM, as we continue to improve our business in a dynamic fashion," Tucker said.

For investors, Team represents a bet on operational execution in a challenging industry. The heritage is impressive—a century of industrial services innovation. The recent track record is sobering—massive value destruction over the past decade. The current trajectory is promising—real operational improvements from a focused management team.

Myth vs. Reality Check

| Consensus Narrative | Reality |

|---|---|

| "Roll-ups create value through synergies" | Integration complexity and debt accumulation can destroy more value than synergies create, especially in cyclical industries |

| "Scale provides competitive advantage in services" | Labor-intensive services have inherent limits to scale benefits; every job still requires people on site |

| "Turnarounds are quick once the right management is in place" | Team's turnaround has taken 3+ years and remains incomplete; patience is essential |

| "Depressed valuations mean obvious buying opportunities" | Depressed valuations can reflect genuine structural problems, not just temporary dislocations |

Material Risks and Regulatory Considerations

- Going Concern Risk: While improved, the company has operated at net losses for multiple consecutive years. Continued losses could stress the balance sheet.

- Customer Concentration: Heavy dependence on refining and petrochemical industries exposes the company to sector-specific risks.

- Energy Transition: Long-term shift away from fossil fuels could reduce demand for traditional industrial services.

- Regulatory Requirements: Services must comply with EPA, OSHA, and industry-specific regulations; violations could result in significant liability.

- Accounting Note: Adjusted EBITDA and other non-GAAP measures exclude items management considers non-representative; investors should review GAAP reconciliations carefully.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube