Aramark: The Invisible Empire Feeding America

I. Introduction & Episode Roadmap

Picture this: It's game day at Lincoln Financial Field in Philadelphia. A father hands his daughter an overflowing tub of nachos, their faces bathed in stadium lights as the Eagles take the field. Across town, a surgeon at Jefferson Hospital grabs a quick coffee between procedures. A few miles away, inmates at a state correctional facility shuffle into a cafeteria line. And at the University of Pennsylvania, thousands of students swipe into dining halls for breakfast.

These four scenes—separated by socioeconomics, circumstances, and purpose—share one invisible thread. The same company prepared all of that food: Aramark.

Aramark (NYSE: ARMK) proudly serves the world's leading educational institutions, Fortune 500 companies, world champion sports teams, prominent healthcare providers, iconic destinations and cultural attractions, and numerous municipalities in 15 countries around the world with food and facilities management.

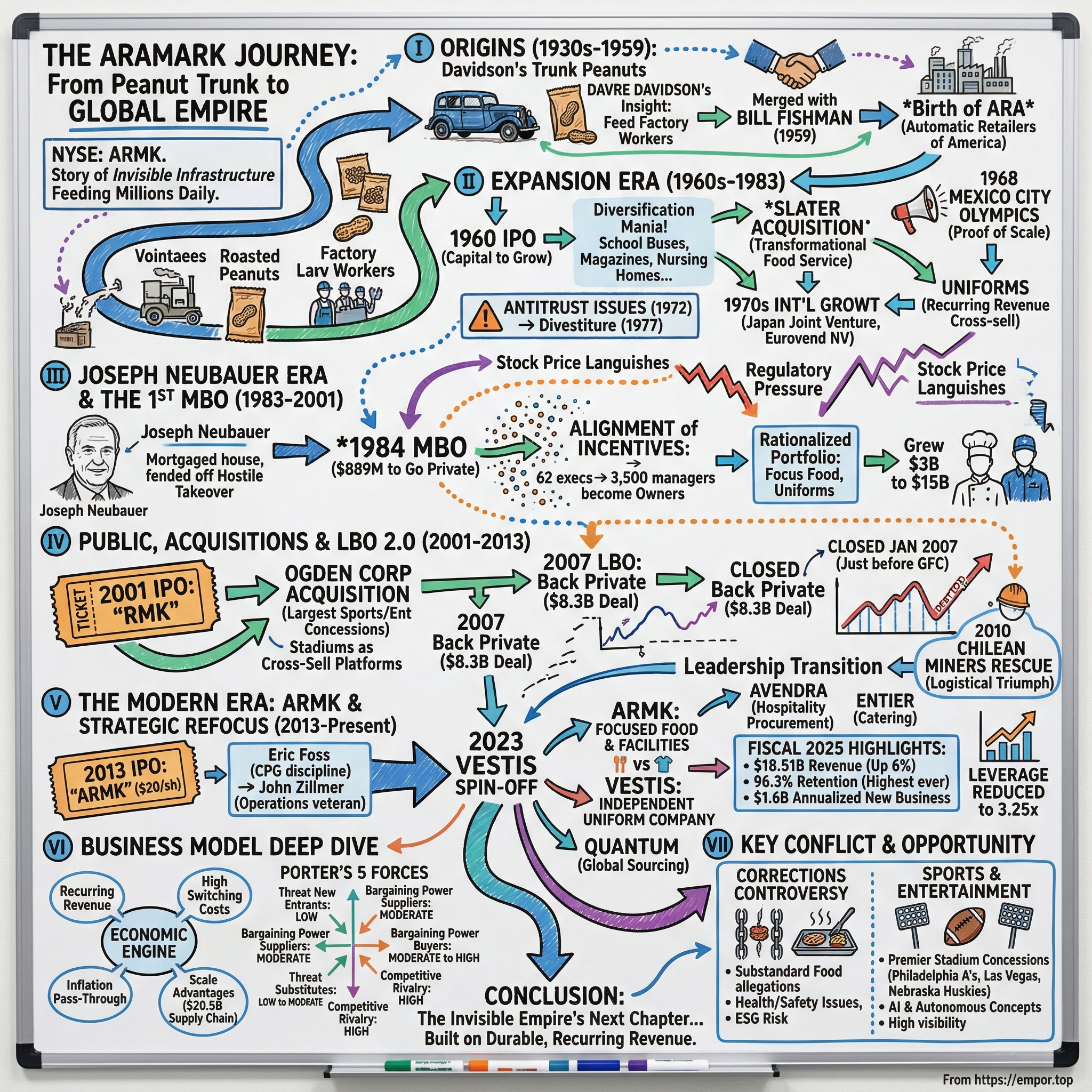

Here's the fascinating hook that makes Aramark one of the most extraordinary stories in American business: Aramark went public on December 12, 2013, at $20 per share. This was the third time the company had gone public, with the first two IPOs taking place in 1960 and 2001. That makes Aramark one of only four companies in U.S. market history to publicly list three times. How does a company stage three separate IPOs, go private twice through leveraged buyouts, and emerge each time larger than before?

The story begins not in gleaming corporate boardrooms but in the dusty parking lots of 1930s Los Angeles, with a man selling peanuts from the trunk of his car. That humble origin evolved into an $18.5 billion enterprise that feeds more people than you've ever stopped to consider. Aramark serves meals at Olympic Games and prison facilities, at Fortune 500 headquarters and elementary school cafeterias. It dresses workers in uniforms from oil rigs to hotel lobbies. It cleans facilities from hospitals to convention centers.

The company posted full-year revenue of $18.51 billion in fiscal 2025, up 6% from the prior year, supported by $1.6 billion in annualized gross new business and a retention rate of 96.3%, the highest in Aramark's history.

The numbers are staggering. Aramark ranks among the 21st-largest employers on the Fortune 500 list. It operates across 15 countries with over 270,000 employees. And yet, despite touching millions of lives daily, most Americans couldn't name the company behind their stadium hot dog or college dining hall salad bar.

This is the story of how peanuts became an empire—and what the journey tells us about American capitalism, the power of recurring revenue, the magic of management buyouts, and the strategic choices that separate good businesses from great ones. From peanuts to prison food, from Olympics to office cafeterias, this is Aramark.

II. Origins: The Peanut Vendor & The Birth of Vending (1936–1959)

Los Angeles, 1936. The Great Depression still gripped America, but Southern California's aviation industry was booming. Douglas Aircraft, Lockheed, and North American Aviation were hiring thousands of workers who needed something to eat during grueling factory shifts. And a scrappy entrepreneur named Davre Davidson spotted an opportunity most would have overlooked.

Davidson didn't have capital for a restaurant or connections to land a food service contract. What he had was a Dodge sedan, a supplier willing to sell him peanuts on credit, and the audacity to drive onto factory parking lots during shift changes. He sold roasted peanuts to hungry workers—five cents a bag—from the trunk of his car.

The business model was elegantly simple: go where the workers are, sell what they'll buy, and keep overhead near zero. Davidson quickly expanded his operation, bringing his brother Henry into what became Davidson Brothers, a vending service focused on the booming aviation industry's workforce.

By the early 1940s, the operation had evolved beyond peanuts. Davidson renamed it Davidson Automatic Merchandising Company and began installing vending machines for snacks, cigarettes, and beverages across Southern California workplaces. The key insight was that factory workers couldn't leave their stations for lunch, but they still needed sustenance. Vending machines—that marvel of automated retail—solved the access problem while requiring minimal labor.

The story could have ended there: a successful regional vending operation, perhaps eventually acquired by a larger player. But seven hundred miles northeast, an almost identical story was unfolding.

In Chicago, a man named Bill Fishman was building his own peanut vending empire, working the industrial plants of the Midwest with the same scrappy determination Davidson had shown in California. Aramark was founded as Davidson Brothers in 1936 by Davre and Henry Davidson. In September 1959, Davidson and Fishman merged their operations into one, and the combined company became known as Automatic Retailers of America, or ARA for short.

The 1959 merger represented something more than two vending companies combining scale. Davidson and Fishman shared a vision that the vending business was merely a wedge into something much larger: the entire business of feeding people who couldn't cook for themselves at work. Vending machines were profitable, but the real opportunity was managed food service—taking over entire cafeterias, kitchens, and dining operations for companies that didn't want to run them.

The timing was fortuitous. Post-war corporate America was expanding rapidly, and large employers increasingly viewed food service as a distraction from their core missions. Why should an aerospace company worry about running a cafeteria when it could focus on building planes? The outsourcing trend that would reshape American business was beginning, and ARA was perfectly positioned to ride it.

In 1960 they took ARA public to infuse the enterprise with new capital and expand the business. In 1961, Automatic Retailers of America merged with Slater Corporation, doing approximately 65 million dollars in manual service sales, and the company was renamed ARA Services, Inc.

The Slater acquisition was transformational. Slater was the largest food service company in the United States at the time, and the merger catapulted ARA from a vending-focused operation into a comprehensive food service provider. The combined entity now had the scale to pursue major contracts and the operational expertise to deliver on them.

In 1963, ARA was listed on the New York Stock Exchange. By 1964, ARA operated 95,000 vending machines, offering freshly brewed coffee, hot soup, sandwiches, and other items.

For investors, the key insight from this origin period is the power of adjacent expansion. Davidson and Fishman didn't try to revolutionize food—they simply went where existing food infrastructure was inadequate and filled the gap. Vending led to food service contracts, which led to facilities management, which led to uniforms. Each expansion leveraged existing client relationships and operational capabilities.

The founders had also stumbled upon a business model with remarkable characteristics: recurring revenue from multi-year contracts, high switching costs (it's painful to change your entire cafeteria operation), and inflation pass-through clauses that protected margins. These would prove to be the foundation of Aramark's durability through economic cycles, management transitions, and multiple trips through public and private markets.

III. The IPO & Diversification Era (1960–1983)

The 1960s marked ARA's transformation from a successful food service company into a sprawling conglomerate. The IPO provided capital, but more importantly, it gave ARA currency—publicly traded stock—to make acquisitions. Management deployed that currency aggressively.

The company's diversification strategy was audacious. Beyond food service, ARA expanded into school bus transportation, magazine distribution, nursing homes, childcare centers, and even emergency rooms. The logic was "managed services"—any operation that institutions didn't want to run themselves represented a potential market for ARA.

In 1968, ARA was awarded the food service contract for the first of many Olympic Games and served over 10,000 athletes, fans and officials in Mexico City, Mexico. Back at home, stadiums, national parks and convention centers across the U.S. hungered for a solution to their food service needs.

The Mexico City Olympics contract represented something more significant than revenue. It was a proof point that ARA could execute at scale under extraordinary circumstances—feeding athletes specific diets, accommodating diverse cuisines, operating under intense scrutiny. The Olympics became a calling card, and ARA would eventually serve 16 Olympic Games, including Athens in 2004 and Beijing in 2008.

International expansion accelerated through the 1970s. A joint venture with Mitsui & Co. Ltd. positioned the company in Japan. That same year, it entered the work uniform rental and career apparel industry. It broke into the European market by acquiring Eurovend NV, giving it food service capabilities in the UK, France, Germany and Belgium.

The uniform business deserves special attention. While seemingly unrelated to food service, uniforms shared the same fundamental economics: recurring revenue, high switching costs, and operational leverage from scale. A company that already had relationships with corporate cafeteria directors could easily sell uniform services to the same clients. The cross-selling opportunity was obvious and lucrative.

But the diversification strategy had a dark side. By the early 1980s, ARA had become unwieldy. The magazine distribution business had antitrust problems. School bus operations required massive capital investments. The childcare business was operationally complex. Management's attention was spread across too many disparate businesses.

In 1972, ARA faced FTC charges due to its monopolistic control of the vending machine market. In 1977, the company divested nearly all of its vending machine operations. In 1981, a federal grand jury began investigating the company's student transport division; sales began to drop off.

The regulatory pressure and operational challenges created an opening for corporate raiders. ARA's stock price languished, trading at a significant discount to the value of its parts. To sophisticated investors, the company looked like a prime target for a leveraged buyout—strip out the underperforming divisions, sell off non-core assets, and unlock trapped value.

That's exactly what happened in 1984. But the twist was that the buyout came from within.

IV. The Joseph Neubauer Era & First MBO (1983–2001)

Joseph Neubauer's biography reads like a novel about the American Dream. Joseph Neubauer's parents fled Nazi Germany in 1938 to start over again in what is now Israel, where Neubauer was born three years later. Neubauer was not yet 15 when his parents put him on a boat for the United States in the hope that he would have more opportunities for education and a career. He did not know when he would see his parents again. The only English he spoke had been learned from watching John Wayne movies. "I was alone but very excited about this new country," he says.

Sent to Massachusetts from Israel at 14 to live with an aunt and uncle, Neubauer majored in chemical engineering at Tufts, where he worked his way through college waiting tables at his fraternity. An economics professor helped him win a full scholarship to the business school at the University of Chicago, where he graduated in 1965.

Neubauer joined ARA in 1979 as Chief Financial Officer and was elevated to CEO in 1983. Almost immediately, the company faced an existential threat.

In July 1984, early in Joseph Neubauer's tenure as chief executive of ARA Services, now Aramark, a former executive of the Philadelphia company dropped a bombshell on Neubauer after a friendly lunch in New York. The executive told Neubauer that he wanted to take ARA private, with Neubauer staying as CEO. Neubauer immediately rebuffed the offer, and the hostile-takeover attempt fizzled quickly. But Neubauer knew it wouldn't be the last, given the company's lagging stock price. That spurred him into action. "I figured if they can do it, we can do it ourselves," Neubauer said.

What followed was one of the most consequential management buyouts in American corporate history. Neubauer turned him down flat. Instead, he mortgaged his house, took out a personal loan, and helped lead a management buyout with 70 other executives to fend off the raiders. "I felt an obligation to the people who worked with me," he says.

Neubauer is credited with fending off a hostile takeover bid in 1984 by coordinating a management buyout that resulted in management ownership of 40 percent of the company. In 1994, the company changed its name to Aramark.

The first time Joseph Neubauer took Aramark Corp. private in 1984, the deal was worth $889 million.

The 1984 MBO fundamentally changed ARA's culture. The 62 core executives contributed $17 million, much of it borrowed. The rest came from Wall Street firms, suppliers, smaller institutional investors, and others. Neubauer kept outsiders from having a large stake. "I didn't want anybody to have more than I had, frankly," said Neubauer, who had options that gave him the largest position. The buyout led to impressive investment returns for any executives who bought shares in 1984 and kept them through all of the firm's iterations. They are sitting on a 23 percent annual return—not counting dividends. That blows away the 11 percent annual return in the Standard & Poor's 500-stock index, including reinvested dividends, over roughly the same period. Starting from a base of 62 executives in 1984, ownership expanded to more than 3,500 managers, who collectively owned 70 percent of Aramark when it went public in 2001.

The private ownership structure gave Neubauer the freedom to make long-term investments without quarterly earnings pressure. He used that freedom to rationalize the portfolio—exiting marginal businesses and doubling down on food service, facilities management, and uniforms. The company also invested heavily in "customized service" capabilities that allowed it to tailor offerings for specific clients rather than offering one-size-fits-all solutions.

The gutsy 1984 buyout set the stage for Neubauer's long tenure at the helm of one of the world's largest food- and support-services firms. Aramark, which got that name in 1994, grew from $3 billion to $15 billion in annual revenue when he was CEO and then chairman, until he retired at the end of 2014. Neubauer had a twofold focus as CEO. He thought not just about having the right mix of services but also having the right set of owners. "In a service business, you don't have monopolies, you don't have patents, you don't have street corners," Neubauer said.

That last quote reveals Neubauer's sophisticated understanding of service business economics. In a world without structural moats, execution and culture become the competitive advantage. By making thousands of managers into owners, Neubauer aligned incentives across the organization. Every cafeteria manager who owned shares had a direct stake in customer satisfaction, operational efficiency, and long-term growth.

The results were extraordinary. By 1997, Aramark recorded $6 billion in sales. Its food service and leisure divisions had expanded throughout Europe and into Japan. At the 1992 Barcelona Olympics, Aramark served athletes their native foods—a logistical triumph that required preparing thousands of culturally specific meals simultaneously.

By the late 1990s, the management ownership structure had created its own challenges. Outside investors who held minority stakes wanted liquidity. The company needed capital for acquisitions. And frankly, the private equity returns had been so spectacular that both management and financial sponsors were ready to crystallize gains.

V. Return to Public Markets & The Acquisition Spree (2001–2006)

In 2001, Aramark returned to the New York Stock Exchange as a public company under the RMK ticker.

The 2001 IPO represented a vindication of the 1984 management buyout thesis. Executives who had risked their mortgages seventeen years earlier were rewarded handsomely. But more importantly, the public listing provided capital and currency for the next phase of growth.

Aramark's acquisition strategy in the early 2000s focused on two themes: vertical integration in sports and entertainment, and portfolio rationalization to focus on core competencies.

In March 2000, the firm acquired the food and concession services of the Ogden Corp., which would make it the largest sports and entertainment concessions provider in the United States.

Aramark purchased the concessions arm of the Ogden Corporation for $225 million in cash and $11 million in assumed debt, expanding its business to locations that included several major sports league venues.

The Ogden acquisition was strategic genius. Sports venues represent captive audiences with high willingness to pay—few food service environments enjoy the same pricing power as a baseball stadium. More importantly, winning stadium contracts creates decades-long relationships with franchise owners who also need food service at their corporate offices, training facilities, and hospitality suites. Each contract became a platform for cross-selling.

Simultaneously, Aramark pruned its portfolio. The company sold its childcare division in 2003 to focus on growth opportunities in core food, facilities, and uniform businesses. The message was clear: Aramark would compete in markets where it had competitive advantages, not peripheral businesses that diluted management attention.

But even as Aramark executed its public company strategy, Neubauer was thinking about ownership structure again. The quarterly earnings treadmill constrained long-term investments. Activist investors were pushing for short-term results. And the private equity market was awash in capital looking for exactly the kind of stable, cash-generative business that Aramark represented.

By 2006, conditions were ripe for another trip through the private-public revolving door.

VI. The 2007 LBO: Going Private Again

The 2006-2007 leveraged buyout boom produced some of the largest private equity deals in history: TXU Energy, Hilton Hotels, First Data Corporation. And Aramark joined the list.

Aramark's CEO, Joseph Neubauer, and investment funds managed by GS Capital Partners, CCMP Capital Advisors and J.P. Morgan Partners, Thomas H. Lee Partners and Warburg Pincus LLC signed an agreement on August 8 to acquire Aramark in an acquisition valued at approximately $8.3 billion.

Aramark has been acquired by an investor group led by Joseph Neubauer, Chairman and Chief Executive Officer of ARAMARK, and investment funds managed by GS Capital Partners, CCMP Capital Advisors and J.P. Morgan Partners, Thomas H. Lee Partners and Warburg Pincus LLC. Approximately 250 ARAMARK senior managers will also invest in the transaction.

Under the terms of the agreement, ARAMARK shareholders are entitled to receive $33.80 in cash for each share of ARAMARK common stock held. ARAMARK common stock will cease trading on the New York Stock Exchange at market close on Friday, January 26, 2007, and will no longer be listed.

The deal structure reflected lessons learned from the 1984 buyout. After initially offering $32 per share, they bumped the payout to $33.80 per share in cash, enough to win over shareholders. This leaves all the potential upside to Neubauer, his partners and 250 Aramark managers, who are on the hook for almost $2 billion in existing debt and an additional $4.5 billion in buyout debt.

Neubauer and his family's holdings soared in value to almost $1 billion. That puts Neubauer, 65, who came to the United States from Israel alone at the age of 14 and said he learned English from John Wayne movies, near the top of the list of beneficiaries from a wave of LBOs that have swept corporate America in the last year.

The timing was both fortunate and challenging. The deal closed in January 2007—just before the global financial crisis began unfolding. The debt load consequences would prove significant. By 2008, Aramark carried $7.3 billion in total debt following the buyout. While this was eventually reduced, the leverage constrained flexibility during the worst economic downturn since the Great Depression.

The strategic rationale made sense: take the company private, make long-term operational improvements without quarterly earnings pressure, then return to public markets when conditions were favorable. But navigating that strategy through 2008-2009 required extraordinary management skill.

VII. The Private Years & Leadership Transition (2007–2013)

The 2008-2009 financial crisis tested every assumption behind the Aramark LBO. Corporate clients cut back on food service spending. Sporting events saw reduced attendance. Hospitals faced budget pressures. And Aramark's debt load limited financial flexibility.

Yet the company's diversification proved its worth. While business dining suffered, healthcare food service remained stable—people still needed to eat in hospitals regardless of economic conditions. College dining halls continued serving students. Correctional facilities maintained contracts. The portfolio's breadth created natural hedges.

We completed the purchase of FilterFresh, an office coffee service, from Green Mountain Coffee Roasters and expanded our healthcare capabilities with the purchase of Masterplan, a clinical technology management and medical equipment maintenance company. For 68 days, we delivered a constant supply of nutritional vacuum-sealed meals through a narrow tube 1/2 mile into the earth until the 33 miners were rescued.

The Chilean miners rescue in 2010 provided an unexpected brand moment. When 33 miners were trapped half a mile underground, Aramark's team figured out how to deliver nutritionally optimized meals through narrow tubes for 68 days until rescue. It was a vivid demonstration of operational capability under the most challenging circumstances imaginable.

Aramark additionally gained traction in the press for its innovations starting in 2009. In July of that year, Aramark and the Colorado Rockies opened what is believed to be the first gluten-free concession stand in major league baseball. By 2010, Aramark made gluten-free foods available at all 12 of its major league baseball accounts.

As the economy recovered, attention turned to leadership succession. Our board of directors elected Eric J. Foss—an accomplished global business leader and world-class operator with a long tenure at Pepsi Beverages Company—as CEO, president and member of our board. Eric succeeded Joseph Neubauer, who served as our CEO for 29 years.

In May 2012, Eric Foss became the new CEO and President of our company. Previously, Mr. Foss was the CEO of Pepsi Beverages Company and was Chairman and CEO of the publicly-traded Pepsi Bottling Group. Under Mr. Foss' leadership at our company, we have introduced a number of initiatives designed to accelerate revenue and profit growth and expand margins.

Foss brought consumer packaged goods discipline to a service business. His initiatives focused on standardizing operations, improving procurement leverage, and building brand recognition for Aramark's various service lines. The company was being prepared for its third trip to public markets.

VIII. Third IPO & The Modern Era (2013–2023)

Philadelphia, PA-based Aramark, a leading global provider of food, facilities and uniform services, opened for trading on December 12, 2013 on the New York Stock Exchange (NYSE) under the ticker symbol "ARMK" after its initial public offering.

Company Name: Aramark Holdings. Stock Symbol: ARMK. Exchange: NYSE. Status: Priced. IPO Date: 12/12/2013. IPO Price: 20.00.

ARAMARK Holdings, which is a leading global provider of food and facilities management and uniform services, raised $725 million by offering 36.3 million shares at $20, the low end of its $20 to $23 range.

The IPO pricing at the low end of the range suggested some market skepticism about the food service sector's growth prospects. But the stock quickly rewarded early believers. Since the initial public offering, the price of the common stock, as reported by the NYSE, ranged from a low of $20.10 on December 12, 2013 to a high of $30.96 on November 28, 2014.

Aramark has been public a year now. Since its IPO debut in December of 2013 at $20 per share, the stock has enjoyed a post-IPO trading range of $20.10 to $30.96—and shares were right at $30 on last look.

The private equity sponsors had generated substantial returns and were exiting in an orderly fashion. The company itself had emerged from private ownership with a cleaner balance sheet and improved operational metrics.

Post-IPO acquisitions continued the strategic pattern of vertical integration and capability building. Aramark announced it completed the previously announced acquisition of Avendra for approximately $1.35 billion, or a net purchase price of $1.05 billion after adjusting for the value of the anticipated tax benefits. Avendra International is the leading hospitality procurement services provider in North America, managing nearly $5 billion in annual purchasing spend for over 650 companies at more than 8,500 locations, including over half of the Top 30 hotel chains.

The Avendra acquisition was strategically brilliant. By acquiring the procurement consortium founded by Marriott, Hyatt, and other major hotel chains, Aramark gained both purchasing scale and sticky client relationships. As part of the agreement, Marriott, Hyatt, Accor and ClubCorp have agreed to commit to a 5-year procurement agreement with Aramark and Avendra.

In December 2014, Joseph Neubauer announced his retirement and Foss was elected as the company's next chairman. Foss remained as CEO until his retirement in August 2019; he was succeeded by John Zillmer in October that same year.

Between the tenure of Foss and Zillmer, Aramark created a position of "Office of the Chairman" consisting of Lauren Harrington, Stephen Sadove, Lynn McKee and Bramlage Stephen to handle day-to-day operations, until a new CEO was found.

The leadership transition reflected activist investor influence. A longtime veteran of Aramark's foodservice operations, John Zillmer, is returning to the contract-services company as CEO at a time of increased activism by one of its major stockholders. He succeeds Eric Foss, who retired from the post in late August after activist investor Mantle Ridge increased its stake in the company to 20% of shares outstanding. Simultaneous with hiring Zillmer, Aramark announced that it will reconstitute its board with five new independent directors, including Mantle Ridge CEO and founder Paul Hilal.

IX. The Vestis Spin-Off & Strategic Refocus (2022–Present)

Aramark (NYSE: ARMK), today announced that it has completed the spin-off of Vestis Corporation ("Vestis"), which holds Aramark's uniform and workplace supplies business. Vestis is now an independent public company.

The spin-off was completed through a distribution to Aramark stockholders of one share of Vestis common stock for every two shares of Aramark common stock held as of the close of business on September 20, 2023, the record date for the distribution.

CEO John Zillmer stated: "The successful spin-off of Vestis is a tremendous opportunity for both Aramark and Vestis to independently build long-term value through a focused commitment to serve customers and deliver on strategic priorities that leverage our core strengths and expertise."

The Vestis spin-off represented the most significant strategic shift since the 1984 management buyout. After decades of building a diversified services conglomerate, Aramark was returning to its roots as a focused food and facilities management company.

Vestis is the second largest provider in the industry and launches with over 300,000 customer locations and approximately 20,000 employees across North America. The Company's comprehensive service offering includes uniforms and workwear, floor care (mats), towels, aprons, linen services, managed restroom supply services, and first aid and safety products.

The logic was straightforward: uniforms and food service, while both recurring-revenue businesses, require different operational capabilities, face different competitors, and deserve different capital allocation decisions. Cintas dominates the uniform industry with 20x EBITDA multiples; food service trades at more modest valuations. Separating the businesses allows each to pursue its optimal strategy without internal capital competition.

Post-spin-off, Aramark has accelerated "tuck-in" acquisitions to strengthen its core business. Aramark's most recent acquisition—Entier—is a provider of contract catering services, founded in 2008 and located in Aberdeen City. Aramark acquired it in February 2025.

MaetaData was acquired by Aramark in February 2025, igniting a new era of sourcing transparency. This long-term technology partner provides innovative AI-driven technology that elevates ingredients and source transparency, engages and empowers local, small suppliers and optimizes the company's responsible sourcing purchasing analytics and reporting practices.

The Quantum acquisition further enhances the company's position as a leading global professional procurement and supply chain services provider. Quantum has customer spend of nearly half a billion dollars (converted to US currency). Autumn Bayles, Aramark's Senior Vice President of Global Supply Chain, noted: "Both companies share a similar vision and culture and adding Quantum positions us to better globally serve not only the hotel category, but several other hospitality markets."

Current Performance:

Aramark (NYSE: ARMK) today reported results for the fourth quarter and full year of fiscal 2025. "Fiscal 2025 represented many consequential milestones for the Company, contributing to the strong growth trajectory ahead," said John Zillmer, Aramark CEO. "In addition to being awarded one of the most prestigious medical systems in the world, we delivered almost $1 billion in Annualized Net New business, added more than $1 billion of new purchasing spend in our Global Supply Chain network for a second consecutive year, and achieved a leverage ratio of 3.25x, a number we haven't seen since prior to when Aramark went private in 2007."

Operating income increased 12% year-over-year to $792 million and AOI grew 12% to $981 million, which represented an operating margin increase of 20 basis points and AOI margin expansion of nearly 25 basis points year-over-year. Profitability growth resulted from higher revenue levels, expanded supply chain capabilities, and disciplined above-unit cost management.

Aramark's earnings per share in fiscal 2025 was $1.22, compared to $0.99 in fiscal 2024. Adjusted earnings per share increased 19% to $1.82.

Net cash provided by operating activities increased 27% to $921 million in fiscal 2025 and Free Cash Flow grew 41% to $454 million. The year-over-year increase was led by stronger cash from operations and favorable working capital.

X. Business Model Deep Dive & Competitive Dynamics

The Economic Engine

Aramark operates what might be called the "invisible infrastructure" of institutional life. Its business model combines several powerful characteristics:

Recurring Revenue: Multi-year contracts with automatic renewal provisions create predictable cash flows. A typical food service contract runs 3-7 years with extension options.

High Switching Costs: Changing food service providers requires retraining staff, transitioning equipment, disrupting operations, and risking employee and customer satisfaction. Most clients renew rather than switch.

Inflation Pass-Through: Contracts typically include provisions to pass through food cost inflation, protecting margins during inflationary periods.

Scale Advantages: Aramark's Global Supply Chain commands $20.5 billion in procurement power and combines supply chain resources backed by Aramark's global footprint across 15 countries. That purchasing scale translates directly into cost advantages versus smaller competitors.

Labor Leverage: Food service is labor-intensive, but Aramark's scale allows better training programs, career paths, and operational systems that improve productivity.

The Competitive Landscape

While the goal of the Top 50 is to provide the most accurate comparison of the largest foodservice contractors, some companies—particularly the top three of Compass, Aramark and Sodexo—do some of their business in areas other than foodservice.

The contract food service industry is dominated by three global giants:

Compass Group (UK-listed): Compass Group plc is a British multinational contract foodservice company headquartered in Chertsey, England. It is the largest contract foodservice company in Europe, employing over 580,000 people as of July 2025. The U.S. represented 65% of Compass Group's fiscal year 2024 revenue and organically grew 10.5% year-over-year to $28.58 billion.

Sodexo (France-listed): The France-based food services and facilities management firm also had a successful fiscal year, reaching about $24.9 billion in revenue—an organic growth of 7.9%, according to its 2024 earnings presentation. North America revenue grew 8.7% organically year over year to roughly $11.65 billion.

Aramark (US-listed): In fiscal year 2024, Aramark grew organic revenue about 10% year over year to $17.4 billion, enjoying a 7.3% spike in U.S. revenue.

With an employee count of 478,070 people, Compass Group outnumbers Aramark which has an employee count totaling 273,900 people. Compass Group generates greater annual revenue than Aramark. Aramark's annual revenue is $17.7B while Compass Group generates a total annual revenue of $111.5B.

The revenue comparison requires context: Compass Group's figures include substantial international operations where Aramark has less presence. In North America, the competitive positions are closer, though Compass still leads.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The contract food service industry has significant barriers to entry. New competitors need operational track records, references from major clients, scale to achieve competitive procurement costs, and capital for equipment and working capital. Regional operators exist but rarely threaten national players.

Bargaining Power of Suppliers: MODERATE Food suppliers range from large commodity producers to specialized vendors. Aramark's $20.5 billion purchasing spend provides leverage, but food costs ultimately flow through to clients via contract terms.

Bargaining Power of Buyers: MODERATE TO HIGH Large clients—hospital systems, university consortiums, major corporations—can negotiate aggressively. But switching costs and the limited number of qualified providers create some pricing power for incumbents.

Threat of Substitutes: LOW TO MODERATE Companies can bring food service in-house, but most conclude outsourcing is more efficient. The real substitute is companies eliminating food service entirely (e.g., work-from-home trends), which became a concern during COVID.

Competitive Rivalry: HIGH Competition among Compass, Aramark, and Sodexo is intense, particularly for marquee contracts. Major contract renewals attract significant attention and often require substantial investments to retain.

Hamilton Helmer's Seven Powers Analysis

Scale Economies: Present. Procurement leverage and operational systems provide cost advantages that smaller competitors cannot match.

Network Effects: Limited. Each client operates independently; there's no direct network benefit from scale.

Counter-Positioning: Limited. All major players offer similar services with similar approaches.

Switching Costs: Strong. The operational disruption from changing providers creates meaningful retention even when competitors offer modest price advantages.

Branding: Moderate. Aramark's brand recognition helps in pitching new clients but isn't determinative. Most end consumers don't know who provides their institutional food.

Cornered Resource: Limited. Aramark has strong relationships and operational expertise but nothing truly proprietary.

Process Power: Moderate. Decades of operational refinement create execution advantages, but these can be replicated over time.

The Corrections Controversy

Any honest analysis must address Aramark's prison food service business, which generates approximately $1.5 billion in annual revenue—about 8% of the total.

Through its subsidiary Aramark Correctional Services, Aramark provides food services to some 450 U.S. prisons and jails. As of 2024, the company has contracted with prison and jail agencies in at least 35 states.

Aramark holds around 35% of the prison food service market.

The business has faced significant controversy. Aramark has a long history of providing substandard food in prisons. The company reduces quantities and serves lower-quality, less nutritious food. It has been accused of severe violations, tainted food, food substitutions, and other health and safety issues. For example, in 2023, people incarcerated in West Virginia sued Aramark, alleging they were routinely served spoiled and undercooked food.

In 2015, the Michigan Department of Corrections ended its $145 million contract with Aramark because of employee misconduct and food contamination.

This represents a genuine ESG risk. Prison food service contracts are awarded based on cost, creating inherent pressure to minimize quality. The incarcerated population has limited ability to complain or switch providers. And reputational damage from prison controversies could theoretically affect other business lines, though evidence of such spillover is limited.

For investors, the question is whether corrections exposure represents acceptable risk for the returns it generates. Some ESG-focused investors exclude Aramark specifically because of its prison business; others view it as acceptable if operations meet regulatory requirements.

XI. The Sports & Entertainment Franchise

Aramark Sports + Entertainment (Aramark, NYSE: ARMK), the award-winning food and beverage provider at more than 60 premier stadiums, arenas, and sports facilities across North America, continues to solidify its position as the industry leader across its extensive portfolio of 21 NCAA sports venues and power conference schools.

Aramark Sports + Entertainment serves more than 150 award-winning food and beverage, retail, and facility service programs in premier stadiums, arenas, convention centers, cultural attractions, performance venues, and unique entertainment destinations across North America. The company has received accolades for industry innovations including autonomous markets, dining concepts powered by artificial intelligence, and high-profile events like the MLB World Series, MLB at Rickwood Field, and NBA All-Star.

The Sports + Entertainment division represents Aramark's highest-visibility business segment. When fans eat at NFL stadiums, MLB ballparks, and NCAA venues operated by Aramark, they experience the company's capabilities firsthand.

The Athletics announced Aramark Sports + Entertainment as their first Las Vegas ballpark investor, while also naming the company concessionaire for the team's Strip stadium and a minority owner of the club. Philadelphia-based Aramark, which served as the concessionaire for the A's former home, the Oakland Coliseum, will oversee hospitality offerings at the Las Vegas stadium, from general concessions to premium dining. Aramark has operated professional sports venues for decades, including the home fields of the Philadelphia Phillies, Boston Red Sox, New York Mets, Colorado Rockies and the San Francisco Giants.

Nebraska Athletics and Aramark Sports + Entertainment today announced a new multi-year partnership to manage all gameday food and beverage services, including concessions and premium spaces, at the University of Nebraska's Memorial Stadium. Aramark, the award-winning food and beverage provider at more than 60 premier stadiums, arenas, and sports facilities across North America, is expanding its portfolio by adding the University of Nebraska as its fourth Big Ten Conference client alongside the University of Iowa, University of Minnesota, and University of Washington.

The athletics partnership with Nebraska—one of college football's most passionate fan bases—exemplifies Aramark's strategy of landing prestigious accounts that serve as references for future contracts.

XII. Leadership & Management Assessment

John J. Zillmer has been our Chief Executive Officer ("CEO") since October 2019. Prior to joining us, Mr. Zillmer served as Chief Executive Officer and Executive Chairman of Univar from 2009 until 2012. Prior to that, Mr. Zillmer served as Chairman and Chief Executive Officer of Allied Waste Industries from 2005 to 2008 and various positions at Aramark, including Vice President of Operating Systems, Regional Vice President, Area Vice President, Executive Vice President Business Dining Services, President of Business Services Group, President of International and President of Global Food and Support Services, from 1986 to 2005.

John Zillmer is a highly effective and successful business leader with deep experience and expertise in the food services and related businesses, corporate culture, logistics and corporate governance. Zillmer is also an expert in strategies for business optimization and process improvement, having previously served Aramark for nearly two decades with a focus on clients and consumers. During his time at the Company, Zillmer progressed through the ranks. Under his leadership, Aramark Food & Support Services was a best-in-class company and the largest food management provider in North America. After leaving Aramark, Zillmer became Chairman and CEO of Allied Waste Industries.

Zillmer represents a return to Aramark's operational roots. Unlike his predecessor Eric Foss (a consumer packaged goods executive), Zillmer grew up in the food service industry. His nearly two decades at Aramark, followed by turnaround experience at Allied Waste and distribution expertise at Univar, provide relevant operational background.

Through his family foundation, Zillmer focuses his philanthropic efforts on the needs of children and families in Tanzania and Haiti. The foundation built the Inspiration Center, a multi-purpose facility for doctors, nurses and patients at the Machame Hospital in the Kilimanjaro district in Tanzania.

The current management team's execution metrics are strong: record client retention (96.3%+), $1 billion+ in net new business annually, and leverage reduction to levels not seen since before the 2007 LBO.

XIII. Investment Considerations: Bull & Bear Cases

The Bull Case

1. Stable, Recurring Revenue Model Multi-year contracts with high renewal rates create predictable cash flows through economic cycles. Even during COVID's worst impacts, Aramark maintained substantial revenue because healthcare, corrections, and essential facilities continued operating.

2. Scale Advantages Compounding Aramark's Global Supply Chain spend now exceeds $20.5 billion—and it's growing through acquisitions like Avendra and Quantum. Each incremental dollar of purchasing scale improves margins across the entire portfolio.

3. Favorable Industry Dynamics The outsourcing trend continues as institutions seek operational efficiency. The global food and support services market is approximately $900 billion. As only approximately 50% of this opportunity is outsourced, there is substantial potential for growth by winning business with institutions that currently provide these services in-house.

4. Post-Vestis Focus The uniform spin-off allows management to concentrate entirely on food and facilities, eliminating internal capital competition and strategic distraction.

5. Valuation Reset Potential If Aramark can demonstrate consistent organic growth and margin expansion, the market may re-rate the stock closer to Compass Group multiples. Even modest multiple expansion on $18+ billion in revenue creates significant value.

The Bear Case

1. Labor Intensity and Inflation Risk Food service is fundamentally a people business. Labor cost inflation, unionization pressure, and staffing challenges create margin headwinds that are difficult to fully offset. Aramark workers at Citizens Bank Park, Lincoln Financial Field and the Wells Fargo Center reached a tentative agreement on a new labor contract that will include raises up to $6 an hour and health care benefits. Pending ratification, the deal is poised to end more than two years of negotiations that led to three strikes.

2. Competitive Pressure Compass Group's superior scale ($42B vs. $18.5B revenue) provides advantages in procurement and operational investment that Aramark cannot fully match.

3. Corrections Exposure The prison food business (~8% of revenue) creates ESG risk and reputational concerns. Continued controversies could affect contract renewals in other segments where institutional clients face pressure from stakeholders.

4. Work-From-Home Structural Shift While return-to-office trends have helped, permanent remote work for some portion of the workforce reduces the addressable market for business dining services.

5. Debt Load While leverage has improved to 3.25x, the company still carries substantial debt that limits strategic flexibility and creates refinancing risk if credit markets tighten.

XIV. Key Performance Indicators

For investors monitoring Aramark's ongoing performance, three KPIs deserve particular attention:

1. Client Retention Rate

This is the most important metric. Aramark achieved a retention rate of 96.3%, the highest in Aramark's history. Each percentage point of retention represents hundreds of millions in recurring revenue. Declining retention would signal competitive or service quality problems. Target: 95%+ annually.

2. Net New Business as % of Prior Year Revenue

This measures the company's ability to grow beyond existing contracts. Combined, this represented unprecedented annualized Net New business for the Company at 5.6% of prior year revenue. Management targets 4-5% annually; outperformance suggests strong competitive positioning.

3. Adjusted Operating Income Margin

This shows pricing power and operational efficiency. Margin expansion (or maintenance during inflationary periods) indicates successful cost pass-through and scale leverage. Track AOI margin progression across quarters to assess execution.

XV. Myth vs. Reality

Myth: "Aramark is just a cafeteria company." Reality: Food service is the largest segment, but the company's procurement operations (Avendra, Quantum), facilities management, and supply chain services represent meaningful and growing portions of the business. The global supply chain business alone manages $20.5+ billion in purchasing spend.

Myth: "The company has no competitive moats." Reality: While not as defensible as software businesses, Aramark possesses meaningful switching costs (contracts average 3-7 years, transition costs are significant), scale advantages (procurement leverage compounds with size), and relationship depth (multi-decade relationships with many clients). These aren't impregnable moats, but they're not nothing.

Myth: "Private equity extraction damaged the business." Reality: Both LBO cycles actually strengthened operations. The 1984 buyout created an ownership culture that persists today. The 2007 buyout, while adding leverage, forced operational discipline that improved margins. The current leverage ratio (3.25x) is the lowest since before the 2007 transaction.

XVI. Conclusion: The Invisible Empire's Next Chapter

Aramark's 89-year journey from peanut vending to global food service empire illuminates several enduring business truths:

Adjacent expansion beats pivot strategies. Davidson didn't abandon vending for food service—he used vending relationships to win food service contracts. Aramark didn't abandon food service for facilities management—it sold facilities services to existing food service clients. Incremental expansion into related markets compounds capabilities while managing risk.

Ownership structure matters. The 1984 management buyout created an ownership culture that aligned thousands of managers with long-term value creation. The 2007 LBO, while controversial, allowed investments that improved operations. The 2023 Vestis spin-off sharpened focus on core competencies. Each ownership transition served a strategic purpose.

Scale advantages compound in services businesses. Aramark's $20.5 billion in purchasing spend isn't just a cost advantage—it's a barrier to entry that strengthens over time. Smaller competitors cannot match Aramark's procurement leverage, training infrastructure, or operational systems.

Recurring revenue creates durability. Multi-year contracts with high renewal rates allowed Aramark to survive two financial crises, multiple leadership transitions, and enormous changes in its operating environment. That durability is the foundation of the investment case.

The current chapter finds Aramark executing on a focused strategy: food and facilities services, powered by an expanding global supply chain operation, with selective "tuck-in" acquisitions building capabilities. CEO John Zillmer stated that Fiscal 2025 represented "many consequential milestones for the Company, contributing to the strong growth trajectory ahead."

Whether that trajectory continues depends on execution in competitive markets, navigation of labor cost pressures, and the ability to win new business while retaining existing clients at industry-leading rates.

The invisible empire that started with peanuts sold from a car trunk now feeds millions daily across every conceivable institutional setting. Most people who eat Aramark's food have no idea who prepared it. But for nearly nine decades, that anonymity has been just fine with a company built on operational excellence rather than consumer brand recognition.

From peanuts to prison food, from Olympic athletes to office workers, Aramark's story continues to be written—one meal at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube