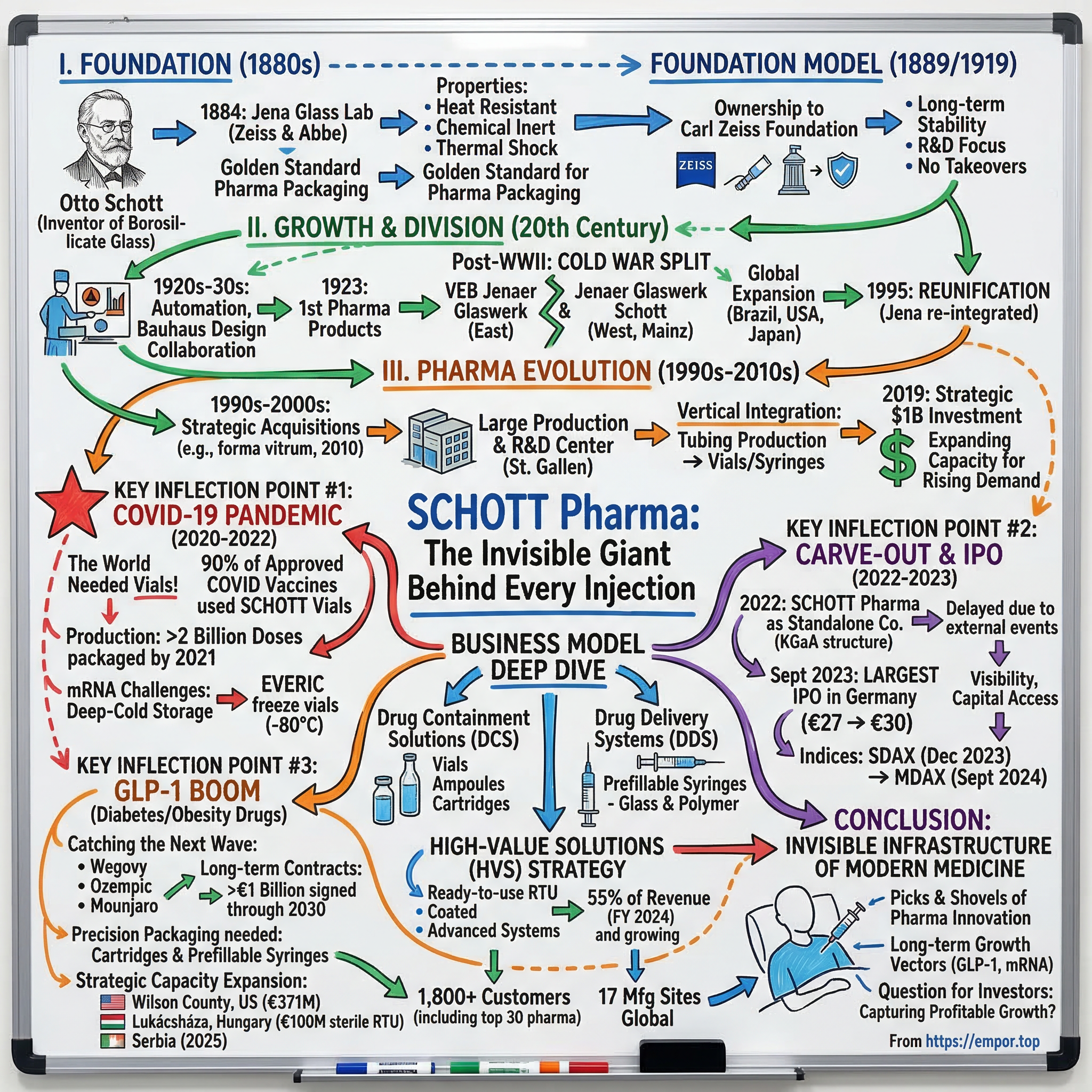

SCHOTT Pharma: The Invisible Giant Behind Every Injection

I. Introduction & Episode Roadmap

Picture a scene playing out somewhere in the world this very second: a pharmacist pulls a vial from refrigerated storage, a nurse draws clear liquid into a syringe, a patient rolls up their sleeve. The moment passes in an instant—routine, unremarkable, forgettable. Yet within that small glass container, invisible to everyone in the room, lies the product of 140 years of scientific innovation, industrial evolution, and strategic positioning that has quietly made one German company indispensable to global healthcare.

"Every minute, more than 30,000 patients safely receive an injection stored in one of our primary packaging products," SCHOTT Pharma declares in its corporate communications. The math is staggering: that's 1.8 million patients per hour, over 43 million per day, roughly 16 billion annually. And here's what makes this truly remarkable—most people have never heard of the company making this possible.

Approximately 90 percent of approved COVID-19 vaccines relied on SCHOTT vials. When the world desperately needed containers to hold humanity's salvation, one company had spent decades quietly positioning itself as the essential supplier. Not Pfizer. Not Moderna. Not even the governments funding Operation Warp Speed. The chokepoint was glass—specifically, borosilicate pharmaceutical glass—and SCHOTT dominated it.

This is the paradox at the heart of SCHOTT Pharma's story: a company almost no one knows, yet one that touches nearly every injectable medication on Earth. From the mRNA vaccines that helped end a pandemic to the GLP-1 weight-loss drugs now reshaping metabolic medicine, the containment and delivery systems that make these breakthroughs possible trace back to a small glass laboratory founded in 1884 in Jena, Germany.

The themes running through this story are classic "Acquired" territory: deep technological moats in so-called "boring" industries, the competitive advantages of foundation ownership, and the art of positioning a company at the intersection of megatrends. SCHOTT Pharma didn't stumble into COVID vaccines or GLP-1 drugs—it systematically built capabilities over generations that made it the obvious choice when these markets exploded. The question for investors is whether this positioning can continue delivering outsized returns, or whether the pandemic-era peak represented a high-water mark.

II. The Origin Story: Otto Schott and the Birth of Specialty Glass (1851-1919)

The Founder's Genius

Friedrich Otto Schott (1851–1935) was a German chemist, glass technologist, and the inventor of borosilicate glass. Schott systematically investigated the relationship between the chemical composition of the glass and its properties. In this way, he solved fundamental problems in glass properties.

To understand how a glassmaker became essential to modern medicine, one must understand the man who transformed glassmaking from craft to science. His work has been described as "a watershed in the history of glass composition." This wasn't hyperbole—before Schott, glass was made by artisans following recipes passed down through generations, often without understanding why they worked.

Schott was the son of a window glass maker, Simon Schott. His mother was Karoline Schott. From 1870 to 1873 Schott studied chemical technology at the technical college in Aachen and at the University of Würzburg and at the University of Leipzig. He earned a doctorate in chemistry at Friedrich Schiller University of Jena, specializing in glass science.

The son of a craftsman who chose to study chemistry rather than simply learn the family trade—this origin story contained the seeds of everything that would follow. Schott didn't want to make glass; he wanted to understand it.

His doctoral thesis was entitled "Contributions to the Theory and Practice of Glass Fabrication" (1875). In 1879, Schott developed a new lithium-based glass that possessed novel optical properties. Schott shared this discovery with Ernst Abbe, a professor of physics at Jena University whose comments on glass had stimulated Schott's interest in the subject.

This letter to Abbe would prove fateful. The deficiencies were particularly acute in scientific instruments for which optical performance of the glass in lenses such as for telescopes and microscopes is paramount. Scientifically, as the magnification power of the lenses were increased, chromatic aberration became large. Chromatic aberration causes the optical quality of the visual image to become dependent on the color of the light, resulting in a significant limitation of the scientific instrument.

The Zeiss-Abbe-Schott Partnership

Otto Schott began researching glass chemistry in the 1870s, driven by a scientific interest in the properties of glass and its potential for technical applications. His work attracted the attention of physicist Ernst Abbe and precision instrument maker Carl Zeiss, who recognized the importance of specialized glass in advancing optical technologies. In 1884, Otto Schott, Ernst Abbe, Carl Zeiss and his son Roderich Zeiss founded the Glastechnische Laboratorium Schott & Genossen (Glass Technical Laboratory Schott & Associates) in Jena, Thuringia, Germany which initially produced optical glasses for microscopes and telescopes.

Consider the cast of characters assembled in that Jena laboratory: a glass chemist who approached his craft as science, a physicist who understood the mathematical principles of optics, and a precision instrument maker who could translate theory into products. This wasn't just a business partnership—it was the Industrial Revolution's version of a startup with a world-class founding team.

They engaged Otto Schott, a chemist, who developed about 100 new kinds of optical glass and numerous types of heat-resistant glass (later called Jena glass) at a glassworks the three founded. One hundred new kinds of glass—from a single chemist. Schott wasn't iterating on existing formulas; he was systematically exploring the relationship between chemical composition and physical properties, creating an entirely new field of materials science.

The Borosilicate Breakthrough

In 1884, in association with Dr. Ernst Abbe and Carl Zeiss, Otto founded Glastechnische Laboratorium Schott & Genossen (Schott & Associates Glass Technology Laboratory) in Jena. It was here, during the period 1887 through to 1893, that Schott developed borosilicate glass. Borosilicate glass is distinguished for its high tolerance to heat and a substantial resistance to thermal shock resulting from sudden temperature changes and resistance to degradation when exposed to corrosive chemicals.

This invention would prove transformative. In 1887, Otto Schott began to develop glasses for technical applications. Using boric acid, he invented borosilicate glass, which had three very special properties: extraordinary resistance to heat, strong resistance to chemicals, and exceptional resistance to abrupt changes in temperature. The first application of borosilicate glass was in technical thermometers (from 1891), which enabled temperature measurements up to 500 ºC for the first time.

For pharmaceutical applications, this trifecta of properties—heat resistance, chemical inertness, and thermal shock resistance—would prove essential. Medicines need containers that don't leach chemicals into the drug, can withstand sterilization processes, and won't shatter during manufacturing or transport. Borosilicate glass would become the gold standard for pharmaceutical packaging, a position it holds to this day.

The Foundation Model: A Radical Corporate Structure

By 1919, the company had grown significantly, employing a workforce of over 1,200 people. In 1919, Otto Schott transferred his shares to the Carl Zeiss Foundation, which had been founded by Ernst Abbe in 1889 and first became a partner in the company in 1891. This made the glass laboratory a foundation company.

This decision—to transfer ownership not to heirs, not to outside investors, but to a perpetual foundation—would shape SCHOTT's destiny for the next century and beyond. The Foundation succeeded in permanently securing the existence of the ZEISS and SCHOTT plants independent of owner interests, as well as giving employees special social rights and promoting scientific and social institutions outside the companies. With the support of Otto Schott, Abbe implemented a unique corporate model that was geared towards sustainability, with SCHOTT's shares transferred to the Foundation in two stages, one in 1891 and the other in 1919. Abbe's Foundation statute of 1896 forms the corporate constitution, which is one of the most important documents in German economic and social history.

The foundation structure creates a distinctive competitive position. The Carl Zeiss Foundation is the sole shareholder of Carl Zeiss AG and SCHOTT AG. The main role of the foundation is to ensure the long-term future of the two foundation companies based on a pioneering spirit and responsible corporate governance as well as the promotion of science. The Foundation is not permitted to sell the shares of its two companies, as specified in the Foundation Statute. Because of this exceptional arrangement, ZEISS and SCHOTT have a unique company model.

No hostile takeovers. No pressure to maximize quarterly earnings at the expense of long-term research. No risk that a private equity firm might strip assets or cut R&D to boost short-term returns. The companies have been under the inalienable sole ownership of the Carl-Zeiss-Stiftung for more than a hundred years. The special feature of our foundation lies in the combination of various foundation purposes, which must be fulfilled by the Foundation itself as well as by the foundation companies.

For investors evaluating SCHOTT Pharma today, this foundation heritage represents both stability and constraint. The parent company won't be sold, ensuring continuity of the technological and cultural DNA that makes SCHOTT valuable. But it also means SCHOTT Pharma must balance its own shareholders' interests against the broader foundation mandate—a nuance that matters when considering governance and capital allocation.

III. Industrial Growth, Division & Reunification (1920s-1995)

Pre-War Expansion

In 1927, Erich Schott, the son of Otto Schott, assumed management of the company. Under his leadership, the company established new business segments, acquired subsidiaries, and modernized its operations, introducing early forms of automated manufacturing processes.

The transition from founder to second-generation leadership went smoothly, with Erich Schott continuing his father's commitment to innovation while scaling the industrial operations. Beginning in 1924, the company designed household glassware with members of the Bauhaus movement, who were active in nearby Weimar. In 1924, Walter Gropius proposed a collaboration to improve the design of household glassware.

This Bauhaus collaboration deserves more than passing mention. The Bauhaus—arguably the most influential design school in modern history—was headquartered just 25 kilometers from Jena. SCHOTT didn't merely sell glass to artists and designers; it invited them into the laboratory to co-create products that would define 20th-century aesthetics. The marriage of scientific innovation and design excellence became embedded in company culture.

For the pharmaceutical business specifically, these pre-war decades established the foundation. Around 1908, the company began manufacturing glass tubing which was used for pharmaceutical packaging. By 1923, SCHOTT produced its first dedicated pharma products, establishing what would eventually become its most strategically important business unit.

The Cold War Split

The aftermath of World War II cleaved Germany—and SCHOTT—in two. In the midst of Germany's political division after World War II, the Jena factory was expropriated and transformed into a Publicly Owned Enterprise (VEB) in 1948. The company was divided in half: VEB Jenaer Glaswerk in Jena in East Germany, later integrated into the VEB Carl Zeiss Jena collective, and Jenaer Glaswerk Schott & Gen in Mainz in West Germany. While VEB Jenaer Glaswerk developed into a specialty glass supplier in the Eastern Bloc, the other half developed into an international group in Mainz with sales offices abroad.

As was the case with Germany as a whole, the glass company founded by Otto Schott was now divided by an "iron curtain." For the next several decades, both companies exploited the Schott name, often to the confusion of consumers.

The Western half rebuilt aggressively. Starting nearly from scratch in Mainz—having left most equipment behind in Jena—the company pivoted toward emerging technologies. The company became a specialist glass manufacturer with products including glass components for television tubes, fiber optics for light and image conductors, mirror substrates for giant telescopes, glass-ceramic cooktop panels (serial production from 1973) and glass tubes for parabolic trough power plants.

Global Expansion & Reunification

The decades between division and reunification saw SCHOTT transform from a regional German company into a truly global operation. Production moved beyond Germany for the first time in 1954 when Vitrofarma, a Brazilian manufacturer of glass tubes for pharmaceutical ampoules, became SCHOTT's first international production site. The 1960s brought expansion across continents: sales offices opened in New York (1963), Tokyo (1966), and Paris (1967). Manufacturing followed: Duryea, Pennsylvania became the first North American production site (1969), and Penang, Malaysia became the first Asian production facility (1975).

The split appeared permanent but with the sudden collapse of the Soviet Union later in the decade and the reunification of Germany in 1990, negotiations commenced to reunite the company founded by Otto Schott as well as the Carl Zeiss Foundation. The transaction was complicated but finally, on January 1, 1995, the Jena operation was fully integrated into the Schott Group. The company, already a major player on the international stage, was now even more formidable.

The reunification brought more than symbolic closure—it restored SCHOTT's birthplace, Jena, to the corporate family and created a larger, more integrated enterprise capable of competing on the global stage that the 21st century would demand.

IV. The Pharma Business Evolution: From Tubes to Critical Infrastructure (1908-2019)

Early Pharma Applications

The pharmaceutical business evolved gradually from SCHOTT's core competency in specialty glass. From 1911, Schott manufactured borosilicate glass tubing for the production of pharmaceutical ampoules and vials. These early products were relatively simple—standardized containers meeting basic pharmaceutical requirements. But they established relationships with drug manufacturers that would deepen over decades.

The vertical integration that defines SCHOTT Pharma today—controlling both the glass tubing production and the conversion of that tubing into finished pharmaceutical containers—began in these early years. SCHOTT is one of the world's leading producers of pharmaceutical containers made from borosilicate glass, the most proven and most widely available material used to store and deliver vaccines and other sensitive medications. SCHOTT's global manufacturing footprint includes five sites dedicated to the manufacture of type-1 borosilicate glass tubes and another 16 plants converting the tubes into vials.

Building the Pharma Empire

The expansion of SCHOTT's pharmaceutical business accelerated in the 1990s and 2000s through strategic acquisitions and joint ventures. In 1992, Schott Corp. formed a joint venture with the West Company to produce packaging products made out of specialty glass for use by the pharmaceutical industry. The enterprise, located in Puerto Rico, was originally the New Jersey-based O'Sullivan Glass Company, founded in 1945. Schott bought out West in 1995 and renamed the operation Schott Pharmaceutical Packaging Incorporated.

The 2010 acquisition of forma vitrum AG in St. Gallen, Switzerland brought 660 employees and what would become SCHOTT Pharma's largest production site—and, critically, its state-of-the-art R&D center. This Swiss facility would prove instrumental in developing the high-value solutions that drive today's growth.

The 2019 Strategic Investment

The decision that positioned SCHOTT to dominate COVID-19 vaccine packaging came well before anyone had heard of SARS-CoV-2. The success of the COVID-19 response is supported by the company's multi-year, $1 billion global investment in pharmaceutical glass and packaging facilities announced early 2019 in response to rising worldwide demand for safer drug packaging. Despite the pandemic, all expansion projects are on track.

This $1 billion investment, announced in early 2019, was motivated by secular trends in pharmaceutical packaging—not pandemic preparedness. Biologics were increasingly replacing small-molecule drugs, and these complex proteins demanded higher-quality containment. Prefillable syringes were gaining share as drug manufacturers sought to improve patient convenience and reduce contamination risks. The investment targeted these trends.

Schott launched a $1.0-billion (840-million-euro) investment programme in 2019 to expand its pharmaceutical business. By the time the COVID-19 vial requests started pouring in, new manufacturing equipment was already up and running. "That puts us in a very good position to ramp up production quickly," Rettig said.

Call it luck or foresight, but when the world needed vaccine vials at unprecedented scale, SCHOTT had just finished expanding capacity. The lesson for investors: companies that invest continuously in capabilities, even when immediate returns are unclear, position themselves to capture unexpected opportunities.

V. KEY INFLECTION POINT #1: The COVID-19 Pandemic (2020-2022)

The World Needed Vials

In March 2020, as governments worldwide scrambled to understand the emerging pandemic, pharmaceutical packaging executives faced a sobering realization: even if scientists developed effective vaccines at record speed, there might not be enough vials to hold them.

SCHOTT's pharmaceutical packaging business unit has delivered enough vials to provide more than 1 billion doses of COVID-19 vaccines, marking a massive contribution to the global fight against COVID-19. The company remains well on track to deliver vials for more than 2 billion vaccine doses through 2021. The vials were delivered to projects around the world, with a focus on the US, Europe, and China.

The numbers are staggering when contextualized. One billion vaccine doses by March 2021—roughly one year into the pandemic—represented an industrial achievement comparable to wartime production mobilizations. Two billion through 2021 meant SCHOTT alone was packaging enough vaccines for approximately one-quarter of the world's population.

Schott says it will produce enough glass vials to hold up to two billion doses of coronavirus vaccine by the end of 2021. As expectations grow that the first COVID-19 jabs will be administered in a matter of weeks, German glassmaker Schott is quietly doing what it has been for months: churning out vials that will hold the vaccine. The 130-year-old company, whose founder Otto Schott invented the high-quality borosilicate glass favoured by the pharma industry, has been working round the clock to meet unprecedented demand. Already it has delivered millions of the little bottles to vaccine makers involved in COVID-19 trials.

Why SCHOTT Dominated

The concentrated nature of pharmaceutical glass packaging became apparent during the pandemic. A relatively small number of major players control the market for Type 1 borosilicate glass—the gold standard for injectable medications. The top 5 players in the global pharmaceutical glass packaging market are Schott AG, Gerresheimer AG, Corning Incorporated, Stevanato Group S.p.A., and Nipro Corporation, collectively accounting for over 26% market share.

SCHOTT's advantages in this oligopolistic market stem from its vertical integration and scale. Unlike competitors who might source glass tubing from external suppliers, SCHOTT produces its own borosilicate glass and converts it into finished pharmaceutical containers. This vertical integration ensures quality control, supply security, and cost efficiency that pure converters cannot match.

It is also chemically inert, meaning there is no chemical interaction between the container and the liquid inside it, preventing any interference that could potentially harm the vaccine. Borosilicate glass is considered "the gold standard" for packaging drugs.

mRNA Innovation: Deep-Cold Storage Requirements

The breakthrough mRNA vaccines from Pfizer/BioNTech and Moderna presented unprecedented packaging challenges. Although vaccines from different manufacturers use LNP as a carrier for mRNA, their storage conditions are different. BioNTech/Pfizer COVID-19 vaccine requires storage at −80 °C with a shelf life up to 6 months, whereas the Moderna COVID-19 vaccine requires storage at −20 °C with the same shelf life.

The mRNA platform allowed rapid development of vaccines, but their global use is limited by ultracold storage requirements. Most resource-poor countries do not have cold chain storage to execute mass vaccination.

These extreme temperature requirements created new demands for pharmaceutical containers. Standard glass can become brittle at ultra-cold temperatures, potentially cracking and compromising sterility. The Cyclic Olefin Copolymer syringe allows for CCI at -180°C. With extremely low sub-visible particles, no ion or heavy metal release and an immobilized cross-linked siliconization, this syringe minimizes drug interaction. With proven CCI, reliable functionality, low particulate at -50°C and with an already established Fill-and-Finish network, syriQ syringes offer suitability for low temperature mRNA applications and the ease for scale up.

In January 2024, SCHOTT Pharma launched EVERIC freeze vials, specifically designed for deep-cold storage of pharmaceuticals, including mRNA vaccines and gene therapies. These vials can withstand storage temperatures as low as -80°C, addressing challenges posed by freezing and thawing processes that often lead to glass breakage in conventional vials. This innovation positions SCHOTT for the next generation of mRNA therapeutics beyond COVID-19—cancer vaccines, personalized medicine, and other applications still in development.

VI. KEY INFLECTION POINT #2: The 2022 Carve-Out & 2023 IPO

Setting Up for Independence

Schott Pharma was established as a standalone company in 2022 under the name Schott Pharma AG & Co. KGaA through an equity carve-out (or spin-off) from Schott AG, a manufacturer of specialty glass and glass-ceramics. In the same year, the company announced their plans to present an IPO, but this was reportedly postponed to 2023 due to the Russian invasion of Ukraine.

The carve-out structure—a KGaA (Kommanditgesellschaft auf Aktien), a German legal form combining elements of a partnership and joint-stock corporation—reflects the complexity of maintaining the foundation relationship while accessing public capital markets. SCHOTT AG remains the controlling shareholder, which itself is wholly owned by the Carl Zeiss Foundation. Public shareholders participate in economic returns but have limited influence over strategic direction.

For the fiscal year 2021, sales for the pharmaceutical unit reached 650 million euros ($666 million). Revenues then jumped 27% to 821 million euros in 2022, driven by COVID-related demand and growing traction in high-value solutions.

The IPO Execution

In June 2023, Schott Pharma announced plans to hold the IPO in September 2023. This plan was enacted in September, with Schott Pharma going public on the Frankfurt Stock Exchange. The IPO was initially priced at 27€ per share, and a potential valuation of up to 4.1 billion euros, but increased the share price to 30€ the following day. The IPO was the largest of the year in Germany.

"For us it is the right moment, the market is stable and we have received very positive feedback from investors," CFO Dr. Almuth Steinkühler was quoted as saying. The IPO enables the company greater entrepreneurial flexibility as well as "visibility - in the market, but also with employees. And it gives us access to the capital market."

The 11% first-day pop from the €27 offer price to €30 suggested strong investor appetite despite challenging market conditions in late 2023. The IPO was the largest of the year in Germany. In December 2023, Schott Pharma was included in the SDAX. In September 2024, Schott Pharma was promoted to the MDAX.

The rapid ascent through German stock indices—SDAX within three months of listing, MDAX within a year—reflects both the company's strong financial profile and investor enthusiasm for pharmaceutical infrastructure plays.

Post-IPO Performance

Successful fiscal year 2023, with a year-on-year increase in revenues of 9% to EUR 899m. Compared to EUR 821m in FY 2022, this represents a strong increase of 9%, taking into account the effects of customers' temporary destocking in the core vials product category during the year. The company's EBITDA increased in line with revenue to EUR 239m (+9% yoy), enabling SCHOTT Pharma to maintain its high EBITDA margin of 26.6%.

The 9% revenue growth in fiscal 2023 came despite meaningful headwinds from vial destocking—customers who had built pandemic-era inventory levels were working through excess stock. That SCHOTT Pharma delivered strong growth despite this drag demonstrated the underlying momentum in higher-margin products.

2024 was another year of both quantitative and qualitative growth for SCHOTT Pharma. Revenue increased by 12% on a constant-currency basis compared with the previous financial year – a new record that falls within the upper half of our guidance.

We are especially proud that this growth was fuelled by high-value solutions, which saw an impressive 22% increase and now account for as much as 55% of our total revenue. On a constant-currency basis, we achieved a record margin of 27.8%.

The fiscal 2024 results reveal the strategic shift underway. High-value solutions now represent over half of revenue, growing at nearly double the rate of the overall business. The margin expansion to 27.8%—despite significant ramp-up costs for new capacity—demonstrates the financial leverage in the business model.

VII. KEY INFLECTION POINT #3: The GLP-1 Obesity/Diabetes Drug Boom

Catching the Next Wave

If COVID-19 vaccines demonstrated SCHOTT Pharma's capability to scale rapidly in response to sudden demand, the GLP-1 drug boom represents something potentially more valuable: a long-duration growth driver with years—perhaps decades—of runway ahead.

Germany's Schott Pharma said on Wednesday it had signed contracts worth about $1 billion to provide glass cartridges and syringes to the top companies selling diabetes and weight-loss drugs from the GLP-1 drug class. The company's CEO Andreas Reisse made the announcement during a news conference on Schott AG's launch of its initial public offering for Schott Pharma, its pharmaceutical bottles and vials unit. "We see GLP-1 drugs as one of the hottest topics in the pharma industry," he said.

"We can't share our customers' names, but, in fact, we have already signed long-term contracts with the leading players. And I'm delighted to share that these contracts add up to a volume of about 1 billion euros ($1.07 billion) until 2030." A spokesperson for the company later told Reuters that the company is also providing other components such as packaging for the pen devices for the injectable GLP-1 drugs.

One billion euros in contracted revenue through 2030 from a single drug class—and one that analysts expect to grow dramatically as treatments expand from diabetes to obesity and potentially cardiovascular disease, liver disease, and other conditions. The GLP-1 market represents exactly the kind of long-cycle growth opportunity that rewards SCHOTT Pharma's investment in high-value solutions.

The GLP-1 drug class is gaining steam, with Novo Nordisk's Wegovy being a notable product that has driven high market demand and contributed to Novo's status as Europe's most valuable listed company.

The major GLP-1 players—Novo Nordisk (Ozempic, Wegovy) and Eli Lilly (Mounjaro, Zepbound)—need reliable suppliers of the glass cartridges and prefillable syringes that deliver their drugs. These are not simple vials; GLP-1 drugs are typically self-administered by patients using pen injectors, requiring precision-manufactured cartridges that maintain drug stability and enable consistent dosing. SCHOTT Pharma's high-value solutions portfolio—particularly its cartriQ and prefillable syringe lines—fits this need precisely.

Strategic Capacity Expansion

SCHOTT Pharma's response to the GLP-1 opportunity exemplifies its strategic approach: commit significant capital to capacity expansion based on contracted customer demand.

The $371 million project in Wilson County will add 401 jobs to the region, with groundbreaking expected by the end of the year and projected operations starting in 2027. The new site will be Schott Pharma's first glass and polymer syringe facility in the U.S., as the company aims to expand the domestic supply chain for syringes used in injectable medicines, vaccines and other fields. It will also allow Schott Pharma to triple its supply of glass and polymer syringes to the U.S. market by 2030. "As drug manufacturers develop and expand the use of mRNA, GLP-1, and other biologic therapies that require precise drug stability and storage properties, SCHOTT Pharma will be able to fill those orders quickly and efficiently here in the U.S.," CEO Andreas Reisse said.

Schott Pharma has broken ground on €100 million production facility for ready-to-use (RTU) glass cartridges at its site in Lukácsháza, Hungary. The €100 million investment will expand the capacity for sterile RTU glass cartridges at the Lukácsháza site. RTU cartridges are used to store biologics, GLP-1 drugs, insulin, or hormone therapies to treat diabetes, obesity, or other immunological diseases.

The geographic distribution of these investments reflects thoughtful supply chain strategy. The U.S. facility addresses the largest pharmaceutical market, reducing lead times and logistics costs while providing supply chain resilience against future disruptions. The Hungarian expansion serves European customers while leveraging lower labor costs. Together with existing facilities in Switzerland, Germany, and elsewhere, SCHOTT Pharma builds redundancy while capturing regional growth.

The projects underscore the company's commitment to meeting the high demand, especially in the Drug Delivery Systems (DDS) segment as well as the RTU cartridges from the Drug Containment Solutions (DCS) segment. In Germany, capacities for prefillable polymer syringes have been increased, which is expected to support the company's short- to mid-term growth trajectory. In Hungary, the production of prefillable glass syringes has started following the inauguration of a new state-of-the-art facility and final customer qualifications. At the new best-cost production site in Serbia, which is expected to go into commercial supply in early 2025, machines are being installed, and product qualifications are underway. At the same time, production capacities for RTU cartridges were expanded in Switzerland and for RTU vials in the U.S. with an additional increase being currently implemented.

VIII. Business Model Deep Dive: What SCHOTT Pharma Actually Does

Product Portfolio

SCHOTT Pharma's product offering spans the full range of pharmaceutical containment and delivery solutions for injectable drugs:

Drug Containment Solutions (DCS): - Vials: Including adaptiQ for injectables, EVERIC pure for drug stability, EVERIC freeze for deep-cold applications. These are the traditional backbone of the business—glass containers ranging from small sample vials to large-volume containers. - Ampoules: Sealed glass containers for single-dose medications, including specialized options for easy opening and anti-counterfeiting. - Cartridges: Glass containers for pen injectors and pump systems, including cartriQ for peptide and protein-based injectables and large-volume cartridges for wearable injection devices.

Drug Delivery Systems (DDS): - Prefillable Glass Syringes: syriQ product line for vaccines and biologics, including silicone-free options for sensitive formulations. - Prefillable Polymer Syringes: SCHOTT TOPPAC line, particularly important for deep-cold applications where polymer's flexibility advantage over glass becomes critical.

It offers syriQ, a glass syringe for vaccines; syriQ BioPure, a glass syringe for biologics; syriQ BioPure silicone-free, a prefillable and silicone-free glass syringe for biologics; SCHOTT TOPPAC, a polymer syringe; SCHOTT TOPPAC cosmetic, a polymer syringe for aesthetic treatments; SCHOTT TOPPAC freeze, a polymer syringe for deep-cold applications. The company also provides pharmaceutical glass cartridge, such as cartriQ for peptide and protein-based injectables; cartriQ Large Volume for large-volume injectables; Cartridges Double Chamber for lyophilized drugs.

High-Value Solutions (HVS) Strategy

The strategic heart of SCHOTT Pharma's growth story is the shift toward high-value solutions—products that command premium pricing due to their technical sophistication, the critical applications they serve, and the switching costs they create.

Our high-margin, high-value solutions (HVS) now account for 55% of our revenue. HVS are tailored to meet even the most specific customer requirements for drug containment and delivery, adding exceptional value for our customers.

HVS includes: - Ready-to-use (RTU) products: Pre-sterilized containers that bypass on-site washing and depyrogenation, reducing customers' clean-room requirements and accelerating fill-finish operations. - Prefillable syringes: Enabling self-administration trends in homecare and reducing healthcare facility burden. - Specialty coated and treated containers: Addressing specific drug-container interaction challenges.

The Alliance for RTU, spearheaded by SCHOTT Pharma, Gerresheimer and Stevanato Group, is accelerating standard protocols for pre-sterilized containers that bypass on-site washing and depyrogenation. RTU formats cut glass-particle risk, reduce clean-room footprint and speed product changeovers. West Pharmaceutical's Ready Pack solution combines pre-sterilized vials, stoppers and seals to further simplify fill-finish operations. Adoption gains momentum as EU GMP Annex 1 revisions tighten particulate thresholds and mandate robust contamination controls. Biologics producers, sensitive to yield loss, are among the earliest RTU adopters, cementing a multiyear growth runway for this subsegment.

The RTU trend benefits established players like SCHOTT Pharma because smaller manufacturers lack the validated sterile processing capabilities required. Regulatory tightening acts as a tailwind by forcing pharmaceutical companies toward suppliers with demonstrated compliance track records.

Scale & Customer Base

Currently, SCHOTT Pharma has over 1,800 customers including the top 30 leading pharma manufacturers for injectable drugs and generated revenue of EUR 957 million in the fiscal year 2024.

Every day, a team of around 4,700 people from over 60 nations works at SCHOTT Pharma to contribute to global healthcare. The company is represented in all main pharmaceutical hubs with 17 manufacturing sites in Europe, North and South America, and Asia. With over 1,000 patents and technologies developed in-house and a state-of-the-art R&D center in Switzerland, the company is focused on developing innovations for the future.

The customer concentration in the top 30 pharmaceutical manufacturers creates both stability and risk. These relationships, built over decades, create significant switching costs—pharmaceutical companies must validate new suppliers through extensive testing before changing packaging for approved drugs. But dependence on major accounts means SCHOTT Pharma's growth trajectory closely tracks its largest customers' fortunes.

IX. Competitive Analysis & Industry Structure

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The pharmaceutical glass packaging industry presents formidable barriers to new entrants:

- Capital intensity: Building a pharmaceutical glass manufacturing facility requires hundreds of millions in investment. The specialized glass melting furnaces, automated forming equipment, clean-room converting facilities, and testing laboratories demand enormous upfront capital.

- Regulatory barriers: Pharmaceutical packaging requires extensive validation and regulatory approval. New suppliers must demonstrate compliance with pharmacopeial standards, undergo facility inspections, and complete stability testing that can take years.

- Customer switching costs: Once a pharmaceutical company validates a container for a drug product, changing suppliers requires new validation studies, regulatory filings, and production line adjustments—costs that can exceed the value of modest price savings.

- Accumulated know-how: With over 1,000 patents and technologies developed in-house and a state-of-the-art R&D center in Switzerland, the company is focused on developing innovations for the future. The IP moat accumulated over 140 years cannot be replicated quickly.

2. Bargaining Power of Suppliers: MODERATE

Specialty glass relies on specific raw materials—silica sand, boron compounds, soda ash—and specialized equipment. SCHOTT's vertical integration into glass tubing production mitigates supplier power for its core input. However, the equipment suppliers for forming, inspection, and packaging represent more concentrated industries where switching costs exist.

3. Bargaining Power of Buyers: MODERATE TO HIGH

The top pharmaceutical companies represent significant purchasing power and can negotiate aggressively on price for commodity products like standard vials. However, for high-value solutions—prefillable syringes, specialty coatings, RTU products—the technical requirements and switching costs limit buyer power. The strategic response is clear: shift mix toward HVS where buyer power is lower.

4. Competitive Rivalry: MODERATE TO HIGH

Market concentration remains moderately fragmented, with Gerresheimer, SCHOTT Pharma and Stevanato Group controlling notable share yet leaving room for regional specialists. These leaders deploy AI-guided camera arrays that flag micro-defects below human visibility, cutting scrap and enhancing consistency.

The leading players compete primarily on quality, reliability, and innovation rather than price for value-added products. July 2025: Gerresheimer revised its 2025 revenue outlook downward for the second time, reflecting ongoing demand normalization. May 2025: Stevanato Group opened a new plant in Cisterna di Latina to produce EZ-fill syringes and cartridges at scale.

5. Threat of Substitutes: LOW

For injectable medications, glass remains the gold standard due to its chemical inertness, barrier properties, and established regulatory acceptance. Polymer syringes represent a viable alternative for some applications, particularly deep-cold storage, but require different manufacturing capabilities—and SCHOTT Pharma participates in both glass and polymer formats, hedging this substitution risk.

Hamilton Helmer's 7 Powers Framework

Counter-Positioning: SCHOTT Pharma's foundation ownership structure and integrated business model represent a form of counter-positioning. Competitors cannot easily replicate the long-term orientation and R&D commitment that foundation ownership enables without restructuring their own corporate governance.

Scale Economies: Manufacturing glass pharmaceutical packaging exhibits meaningful scale economies in glass melting, automated converting, and quality testing. SCHOTT Pharma's 17 manufacturing sites spread fixed costs across substantial volume.

Switching Costs: Validated pharmaceutical suppliers create significant switching costs. Once a drug is approved with a specific container closure system, changing suppliers requires revalidation—an expensive and time-consuming process that pharmaceutical companies avoid unless necessary.

Process Power: The 140 years of accumulated manufacturing know-how, proprietary glass formulations, and refined production processes constitute process power that competitors cannot easily replicate.

Branding: In pharmaceutical packaging, the SCHOTT name carries significant credibility with regulatory agencies and pharmaceutical customers globally, built over more than a century.

X. Leadership & Governance

The Management Team

Andreas Reisse has been with the SCHOTT Group since 1987 and has led the "Pharmaceutical Systems" division since 2010, which has been listed on the Frankfurt Stock Exchange as SCHOTT Pharma AG & Co. KGaA since 2023. "Andreas Reisse has played a key role in developing SCHOTT Pharma into one of the world's leading pioneers in pharmaceutical containment solutions and delivery systems."

Reisse's tenure—nearly four decades at SCHOTT, over fifteen years leading the pharmaceutical business—exemplifies the long-term orientation the foundation structure enables. He graduated from the University of Karlsruhe in 1987 and built his career entirely within SCHOTT, gaining deep expertise in the pharmaceutical packaging business through various international assignments including a directorship at SCHOTT Glass Technologies in Suzhou, China.

The Supervisory Board of SCHOTT Pharma Management AG has appointed Christian Mias as CEO of SCHOTT Pharma. He will take over from Andreas Reisse, who will retire as planned in April 2026. Christian Mias, born in Iserlohn in 1974, will succeed Andreas Reisse starting May 1st. As an industrial engineer with a doctoral degree, he looks back on more than 20 years of management experience, including over 18 years within the SCHOTT group.

The succession plan continues the pattern of promoting from within, maintaining cultural continuity while bringing fresh perspective. Christian Mias gained significant experience in the pharmaceutical industry when joining SCHOTT Tubing, which produces intermediate products for the pharma sector, including SCHOTT Pharma.

The KGaA corporate structure deserves attention for governance purposes. SCHOTT Pharma AG & Co. KGaA is headquartered in Mainz, Germany and listed on the Frankfurt Stock Exchange as part of the SDAX. It is part of SCHOTT AG, which is owned by the Carl Zeiss Foundation.

This structure means SCHOTT AG controls SCHOTT Pharma's strategic direction through its general partner position, while public shareholders participate in economic returns. The foundation cannot sell its controlling stake, providing stability but limiting activist influence or acquisition scenarios.

XI. Financial Analysis & Key Metrics

Revenue Growth and Mix Shift

SCHOTT Pharma's financial trajectory demonstrates the power of its strategic focus on high-value solutions:

| Fiscal Year | Revenue (€m) | Growth | EBITDA Margin | HVS Share |

|---|---|---|---|---|

| FY 2021 | 650 | — | ~26% | ~40% |

| FY 2022 | 821 | +27% | ~26% | ~45% |

| FY 2023 | 899 | +9% | 26.6% | ~48% |

| FY 2024 | 957 | +7% (12% cc) | 27.8% (cc) | 55% |

Revenue: €957.1m (up 6.5% from FY 2023). Net income: €149.7m (down 1.4% from FY 2023). Profit margin: 16% (down from 17% in FY 2023).

The reported revenue growth of 7% in FY 2024 understates underlying momentum—constant-currency growth was 12%, with foreign exchange headwinds compressing reported figures. More importantly, high-value solutions grew 22% and now represent 55% of revenue, approaching management's mid-term target of 60%.

Margin Expansion Despite Investment

In FY 2024, SCHOTT Pharma's high operational cash flow was driven by its profitability and improved working capital performance and led to a strong free cash flow of EUR 79m. The strong cash generation (cash flows from operating activities of EUR 225m) enabled the company to self-fund its investments, mainly its growth investments related to the ongoing expansion of HVS capacities. Total CAPEX amounted to EUR 145m (FY 2023: EUR 176m). The company's net profit after minorities came in at EUR 150m, a slight decline of 1% yoy. SCHOTT Pharma recorded earnings per share of EUR 0.99 (FY 2023: EUR 1.01).

The ability to maintain and expand margins while investing heavily in capacity expansion distinguishes SCHOTT Pharma from competitors facing similar growth opportunities but tighter capital constraints. Free cash flow of €79 million after €145 million in capital expenditures demonstrates healthy cash conversion even during an expansion phase.

Guidance and Outlook

SCHOTT Pharma confirms its fiscal year 2025 targets based on a stronger second half with higher revenues coming from additional production capacities in glass syringes and sterile cartridges to serve exciting contracts. Thus, the company projects strong revenue growth at constant currencies in the high single digits. SCHOTT Pharma forecasts an EBITDA margin approximately at the strong level of FY 2024 (26.9%) at constant currencies.

Based on the good developments in the first half of fiscal year 2025, SCHOTT Pharma is well on track to achieve its full year guidance of revenue growth in the high single digits as well as an EBITDA margin approximately at the high level of FY 2024 (both at constant currencies). Looking ahead, the market demand might experience some short-term volatility due to macro-economic uncertainties. However, the long-term pharma trends remain intact and will drive SCHOTT Pharma's main growth in the long-term.

XII. Key Performance Indicators to Monitor

For investors tracking SCHOTT Pharma's ongoing performance, three KPIs merit particular attention:

1. High-Value Solutions (HVS) Revenue Share

The most important strategic metric. HVS products command higher margins, create stronger customer relationships, and demonstrate SCHOTT Pharma's success in moving up the value chain. Current level: 55%. Mid-term target: 60%. Watch for quarterly progress toward this goal.

Why it matters: HVS growth directly drives margin expansion. A company selling mostly commodity vials operates in a competitive, price-sensitive market. A company where 60%+ of revenue comes from specialized syringes, RTU cartridges, and engineered solutions enjoys pricing power and customer stickiness.

2. Drug Delivery Systems (DDS) Segment Growth

The DDS segment—primarily prefillable syringes—represents SCHOTT Pharma's exposure to the GLP-1 boom, homecare trends, and biologics growth. Revenues were the highest quarterly result ever achieved in this segment with an increase of 39% yoy to EUR 115m at constant currencies. This was driven by the ongoing strong demand for prefillable syringes.

Why it matters: DDS growth validates SCHOTT Pharma's strategic investments and demonstrates capture of secular trends. Sustained 20%+ growth rates in this segment would indicate successful execution on the GLP-1 and biologics opportunity.

3. EBITDA Margin at Constant Currency

Given significant capacity expansion underway, maintaining high-20s EBITDA margins demonstrates operating leverage and pricing discipline. On a constant-currency basis, we achieved a record margin of 27.8%.

Why it matters: Expansion brings ramp-up costs and temporary underutilization as new capacity comes online. If margins compress significantly during this phase, it may indicate pricing pressure or operational challenges. Stable-to-improving margins during growth mode signals healthy competitive positioning.

XIII. Bull and Bear Cases

The Bull Case

GLP-1 Structural Growth: The weight-loss and diabetes drug market appears to be in early innings, with significant expansion into broader indications and geographies ahead. SCHOTT Pharma's contracted €1 billion in GLP-1-related business through 2030 may prove conservative if the market expands as analysts project.

mRNA Platform Expansion: COVID vaccines demonstrated mRNA's potential; applications in cancer vaccines, personalized medicine, and infectious diseases are advancing through clinical trials. SCHOTT Pharma's expertise in deep-cold packaging positions it for this emerging opportunity.

RTU Adoption Accelerating: Tightening regulatory standards (EU GMP Annex 1 revisions) push pharmaceutical companies toward pre-sterilized containers. As a leader in RTU solutions, SCHOTT Pharma benefits from this secular shift.

Foundation Stability: The ownership structure enables long-term investment in R&D and capacity that public market pressure might otherwise discourage, creating sustainable competitive advantages.

Valuation Compression Opportunity: The stock has fluctuated within a day range of 19.60 to 20.20, while its 52-week range spans from 18.50 to 32.74. The average 12-month price target for SCHOTT Pharma is EUR29.58333, with a high estimate of EUR36 and a low estimate of EUR23. 9 analysts recommend buying the stock, while 1 suggest selling, leading to an overall rating of Buy. The stock has an +48.66% Upside potential. Current trading levels represent meaningful compression from 2024 highs, potentially offering an attractive entry point if growth trajectory resumes.

The Bear Case

GLP-1 Concentration Risk: Significant revenue growth depends on continued expansion of a single drug class. Supply normalization, competitive pressures on Novo Nordisk and Eli Lilly, or safety concerns about GLP-1 drugs could materially impact demand for SCHOTT Pharma's products.

Capacity Timing Risk: Major expansion projects in the U.S., Hungary, and Serbia require significant capital and execution over multiple years. Delays, cost overruns, or demand shortfalls during ramp-up could pressure returns.

Vial Destocking Headwinds: The core vials business has faced customer destocking as pandemic-era inventory levels normalize. Extended weakness in this foundation business would offset gains elsewhere.

Competition Intensifying: July 2025: Gerresheimer revised its 2025 revenue outlook downward for the second time, reflecting ongoing demand normalization. Competitors facing demand challenges may become more aggressive on pricing, pressuring the industry's historically attractive margins.

FX Volatility: Significant non-Euro revenue creates currency exposure that can compress reported results, as seen in FY 2024's gap between constant-currency (12%) and reported (7%) growth.

Controlling Shareholder Constraints: The foundation ownership structure limits potential strategic transactions and means minority shareholder interests may not always take priority.

XIV. Regulatory and Accounting Considerations

Regulatory Environment

Pharmaceutical packaging is heavily regulated, which creates both barriers to entry (positive for incumbents) and compliance risk (ongoing investment required). Key regulatory frameworks include:

- USP (United States Pharmacopeia) and EP (European Pharmacopoeia) standards for Type I borosilicate glass

- FDA and EMA requirements for container closure system validation

- EU GMP Annex 1 revisions tightening particulate contamination thresholds

- ISO standards for pre-filled syringe dimensions and functionality

SCHOTT Pharma's 140-year track record of regulatory compliance represents a significant competitive advantage—new entrants cannot purchase this reputation.

Accounting Judgments

Key accounting areas warranting investor attention:

Revenue Recognition: Long-term contracts for high-value solutions may involve milestone-based recognition or continuous delivery. Understanding when contracted GLP-1 revenue translates to reported results requires attention to recognition timing.

Capitalized Development Costs: R&D investments may be capitalized when specific conditions are met, affecting period-to-period comparability.

Related Party Transactions: The relationship with parent SCHOTT AG includes purchasing of glass tubing and shared services. These intercompany transactions should be at arm's length but warrant monitoring.

Goodwill and Intangibles: Acquisitions (including the forma vitrum AG acquisition) create goodwill and intangible assets subject to impairment testing.

XV. Conclusion: The Invisible Infrastructure of Modern Medicine

The story of SCHOTT Pharma encapsulates a particular kind of business success—one that requires patience, technical excellence, and strategic positioning rather than disruptive innovation or viral growth. From Otto Schott's systematic investigation of glass chemistry in the 1880s to today's billion-dollar GLP-1 contracts, the company has consistently invested in capabilities that create value for customers in ways difficult for competitors to replicate.

The COVID-19 pandemic revealed what insiders long understood: pharmaceutical packaging represents critical infrastructure without which breakthrough medicines cannot reach patients. SCHOTT Pharma's position in this infrastructure—90% of approved COVID vaccines relied on its vials—demonstrated both the company's operational excellence and the strategic moat decades of investment created.

Now, with GLP-1 drugs potentially representing the largest pharmaceutical opportunity in decades and mRNA technology opening new frontiers in medicine, SCHOTT Pharma finds itself positioned at the intersection of multiple growth vectors. The question for investors is whether the company can continue translating strategic positioning into profitable growth.

The foundation ownership structure provides unusual stability and long-term orientation, but also limits minority shareholder influence. The capital-intensive expansion program should create competitive advantages but requires successful execution. The shift toward high-value solutions improves margins but increases concentration in specialized product categories.

For long-term fundamental investors, SCHOTT Pharma represents an opportunity to own shares in the "picks and shovels" of pharmaceutical innovation—not betting on which drugs will succeed, but on the certainty that successful injectable medications require world-class containment and delivery solutions. The company's 140-year track record suggests it knows how to maintain that position; the coming years will test whether it can also grow it.

Every minute, more than 30,000 patients receive an injection stored in a SCHOTT Pharma product. As long as injectable medications remain central to modern healthcare, that invisible infrastructure will continue creating value—the question is how much of that value flows to shareholders.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube