ASE Technology Holding: The Hidden Giant Behind Every Chip

Introduction: The Invisible Empire

In the labyrinthine world of semiconductors, where NVIDIA and TSMC command headlines and trillion-dollar valuations, there exists a company that touches virtually every electronic device on the planet yet remains almost entirely unknown to the general public. ASE Technology Holding Co., Ltd. operates in what the semiconductor industry calls the "backend"—a term that belies its increasingly critical role in the age of artificial intelligence.

With a 44.6% market share in the OSAT industry in 2024 and $18.54 billion in revenue, ASE has quietly built an empire that would make most conglomerates envious. Over 90% of electronics companies worldwide utilize their services, yet if you asked a hundred people on the street to name the company, you'd likely draw blank stares.

The hook here is compelling: when Jensen Huang, NVIDIA's CEO, visited ASE subsidiary SPIL's new factory in early 2025, he noted that the two companies have been cooperating for 27 years, revealing that sales had increased twofold over the past year. In an industry where relationships are measured in decades and trust is earned through billions of flawlessly packaged chips, ASE's position as the bridge between silicon and system has never been more valuable.

Why does this story matter now? Because the AI revolution has fundamentally rewritten the rules of semiconductor economics. "CoWoS, short for Chips-on-Wafer-on-Substrate and invented by TSMC, is arguably the best known [advanced packaging technology] that was thrown under the limelight since the debut of OpenAI's ChatGPT, which sparked the AI frenzy." Advanced packaging has become "indispensable to producing AI processors, such as the GPUs produced by Nvidia and AMD that are used in AI servers or data centers."

As Jensen Huang noted during a visit to Taiwan in January 2025, the amount of advanced packaging capacity currently available was "probably four times" what it was less than two years ago. "The technology of packaging is very important to the future of computing," he said.

This is a story about two brothers from Wenzhou who bet on an unsexy business in a city most semiconductor tourists had never visited. It's about a hostile takeover that became Taiwan's most dramatic M&A battle. And it's about how a company that once dumped toxic wastewater into a river transformed itself into a sustainability leader and AI kingmaker. The journey from Kaohsiung to global dominance is one of capitalism's most underappreciated tales.

The Brothers Chang and the Kaohsiung Bet (1984-1990s)

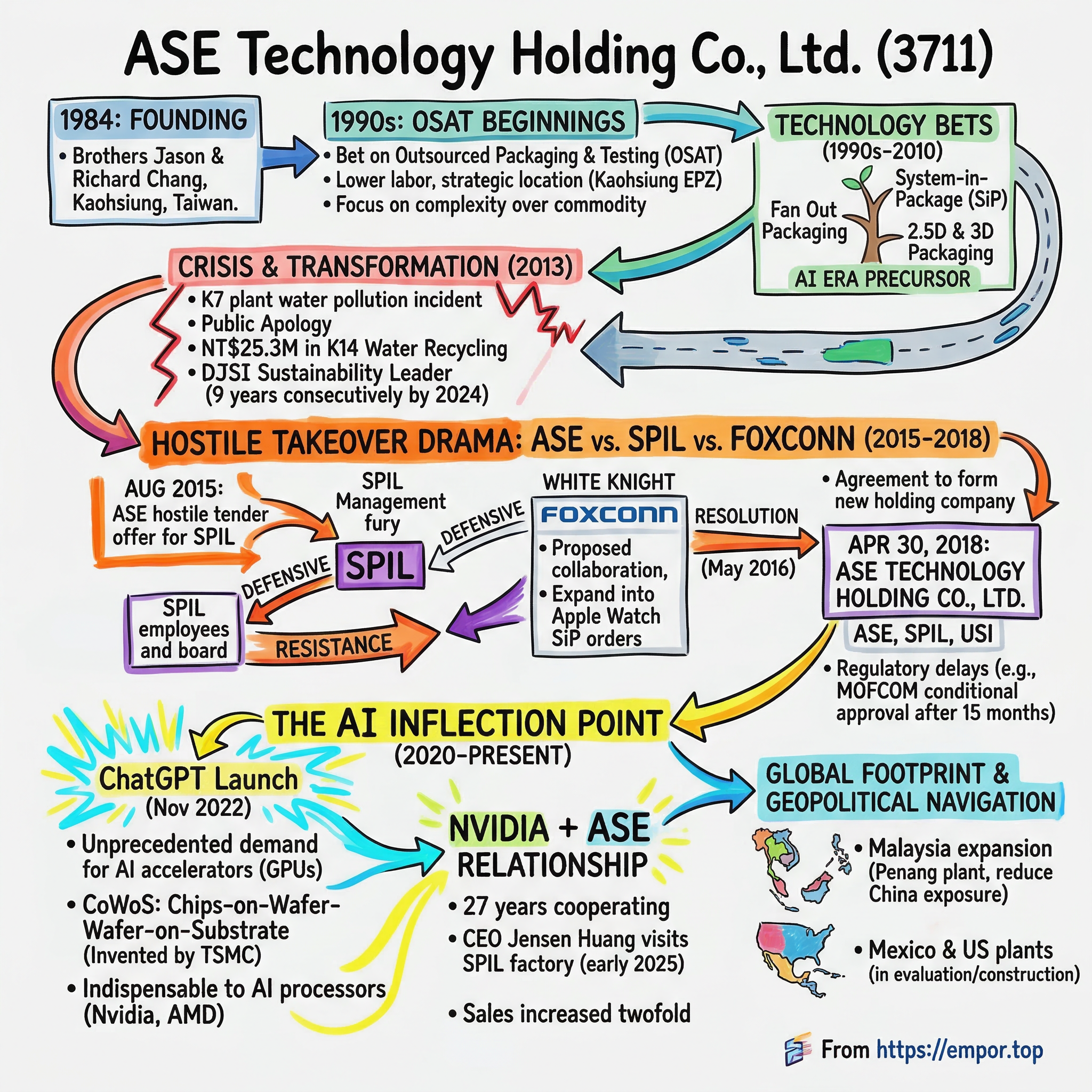

In 1984, while Silicon Valley was captivated by Apple's Macintosh launch and the promise of personal computing, two brothers in southern Taiwan made a bet that would take decades to pay off. Jason Chang and Richard Chang founded Advanced Semiconductor Engineering in Kaohsiung, Taiwan—a city known more for its steel mills and shipyards than for high technology.

Jason Chang was born on May 18, 1944, in Shanghai, China. As the chairman of Advanced Semiconductor Engineering, he would play "a pivotal role in shaping the global electronics landscape." The family relocated to Taiwan during his formative years. He pursued a bachelor's degree in electronic engineering at National Taiwan University before obtaining a master's degree from the Illinois Institute of Technology, equipping him with "a global perspective and advanced technical knowledge."

Richard Chang, his brother, would serve as vice chairman and president. He holds a bachelor's degree in Industrial Engineering from Chung Yuan Christian University in Taiwan. While Jason provided the strategic vision, Richard handled operational execution—a partnership that would prove remarkably durable across four decades.

Why Kaohsiung? The question seems obvious in retrospect but was genuinely contrarian at the time. Northern Taiwan, particularly Hsinchu, was emerging as the island's semiconductor hub. TSMC would be founded there three years later, in 1987. But the Changs planted their flag in Kaohsiung, where main operations remain to this day, with additional plants in China, South Korea, Japan, Malaysia, and Singapore.

The location choice reflected several strategic calculations. Labor costs in southern Taiwan were lower. The Kaohsiung Export Processing Zone offered favorable tax treatment. And perhaps most importantly, the Changs sensed that the OSAT (Outsourced Semiconductor Assembly and Test) business required different capabilities than chip fabrication—less about cutting-edge cleanrooms and more about operational excellence at scale.

The business model the Changs pursued required explanation. In the semiconductor value chain, "front-end" manufacturing (fabrication of chips on silicon wafers) gets most of the glory. Companies like TSMC and Intel operate massive fabs requiring billions in investment. But those wafers aren't finished products. They need to be diced into individual chips, packaged to protect the delicate silicon, tested for defects, and prepared for integration into electronic devices. This "back-end" work was increasingly outsourced as the industry specialized.

The economics were compelling. Packaging and testing offered reasonable margins without requiring the astronomical capital expenditure of leading-edge fabs. A fab might cost $20 billion; a packaging facility could be built for hundreds of millions. The tradeoff was thinner margins and less differentiation—or so the conventional wisdom held.

The Changs saw something different. They recognized that as chips grew more complex, packaging would transition from commodity service to strategic capability. The semiconductor industry's relentless march toward smaller, faster, more powerful chips would eventually hit physical limits—and when it did, packaging would become the new frontier for performance gains.

Their early customer wins created a virtuous cycle. Reliable execution earned repeat business. Repeat business funded capacity expansion. Expanded capacity attracted new customers seeking diversified supplier bases. By the early 1990s, ASE had established itself as a credible alternative to in-house packaging operations, particularly for fabless chip designers who had no manufacturing infrastructure of their own.

The timing proved fortuitous. Taiwan's government was actively promoting semiconductor industry development, offering incentives and infrastructure support. The island's geographic position facilitated trade with both Asian electronics manufacturers and American chip designers. And the culture of precision manufacturing that permeated Taiwanese industry aligned perfectly with the quality demands of semiconductor packaging.

By the mid-1990s, ASE had grown from a startup in an industrial park to a publicly traded company with ambitions far beyond Taiwan's shores. The foundation was laid for what would become the world's largest independent semiconductor packaging and testing operation.

Building the OSAT Empire: The Scale Game (1990s-2010)

If the founding decade established ASE's viability, the next two decades would demonstrate something far more important: that scale and technology leadership could transform a supposedly commodity business into an unassailable market position.

The technology bets came fast and early. ASE developed advanced packaging technologies including Fan Out Packaging, System-in-Package, 2.5D & 3D packaging—capabilities that seemed exotic at the time but would prove essential in the AI era.

The System-in-Package (SiP) investment deserves particular attention. Traditional packaging put one chip in one package. SiP technology allows multiple chips—potentially from different manufacturers, using different process technologies—to be integrated into a single package. Apple's S1 chip in the original Apple Watch was a showcase application, cramming an entire computer's worth of components into a tiny, waterproof module.

The acquisition strategy complemented organic investment. In May 2015, ASE Group established a joint venture named ASE Embedded Electronics Inc. with TDK, focusing on IC embedded substrates utilizing TDK's SESUB technology. These partnerships and acquisitions filled capability gaps and extended geographic reach.

In 2018, Advanced Semiconductor Engineering Inc became a part of the ASE Technology Holding Company Ltd and is listed both on NYSE and Taiwan Stock Exchange. Before the company went into a joint venture with SPIL, ASE Group's market capitalization summed up to $8.77 billion.

But growth wasn't without crisis. In October 2013, a water pollution incident at ASE's K7 facility in Kaohsiung triggered what would become a defining challenge for the company.

The K7 plant was fined NT$600,000 (US$20,300) and ordered to suspend operations for contravening the Water Pollution Control Act. The K7 plant discharges wastewater 24 hours a day, making it the ninth-biggest discharger in the city, and the level of nickel in discharged water was about the same as the wastewater found in the plant, indicating the plant was not treating the water before discharging it. Bureau Director-General Derek Chen said that the plant's management showed "malicious intent by trying to use tap water to dilute the highly acid wastewater when the inspectors arrived to conduct tests."

In December 2013, Jason Chang issued a public apology for water pollution caused by untreated wastewater issuing from an ASE plant in southern Taiwan. The crisis exposed operational weaknesses and raised questions about corporate culture.

The response would prove pivotal. From 2010 to 2013, ASE invested US$13.2 million in treating industrial water. In addition, ASE invested $25.3 million to build a water recycling plant, K14 in Kaohsiung, Taiwan. The water recycling plant began trials in January 2015.

The water recycling plant handles up to 20,000 metric tons of wastewater per day, recycling half for internal use and discharging the rest into city drains, meeting local regulations.

The environmental crisis forced a transformation that extended beyond pollution control. ASE Group has 18 smart factories and one of them became the world's first semiconductor packaging plant to get a certification of low carbon building. Five times in a row, ASE became the industry leader in the Dow Jones Sustainability Indices.

ASE aims to reduce energy consumption by 20% by 2030 and achieve net-zero emissions by 2050 through partnerships with 19 equipment suppliers. The company now evaluates suppliers using ESG criteria. These efforts earned ASE inclusion in the Dow Jones Sustainability Indices (DJSI) for the ninth consecutive year in 2024.

The sustainability transformation illustrates a broader truth about ASE's culture: the company treats challenges as opportunities for systematic improvement rather than problems to be managed away. This operational discipline—born of necessity during the environmental crisis—would serve it well in the competitive battles to come.

The Hostile Takeover Drama: ASE vs. SPIL vs. Foxconn (2015-2018)

The most dramatic chapter in ASE's history began on August 21, 2015, when Taiwan's stock market was in free fall and most investors were focused on survival. "On August 21, 2015, there was a merger and acquisition (M&A) case in Taiwan's semiconductor industry. When TAIEX index took a nosedive even fell below the lowest record of the past decade, Advanced Semiconductor Engineering (ASE), the world-leading packaging and testing industry firm launched an offer to acquire nearly 25 percent stake of competitor Siliconware Precision Industries Co. Ltd. (SPIL) whose annual output value is the third-ranked in the world."

ASE "plans to acquire a 25 percent share of its main local rival, Siliconware Precision Industries Co Ltd (SPIL), for up to NT$35 billion (US$1.06 billion) in an effort to fend off growing competition from China. The hostile takeover bid came as a bombshell to SPIL's board, as it was not approached for a deal and the companies have been in a long-term race for industry leadership."

"Far from being common, in Taiwan has been few cases of hostile takeovers. However, the most famous one is happening currently and is being a complex issue."

The industry context matters. Chinese competition was intensifying: "Jiangsu Changjiang Electronics Technology Co (江蘇長電) has made a US$780 million offer to buy its Singapore rival, STATS ChipPAC Ltd, as China is stepping up its efforts to expand its presence in the world's semiconductor industry. The merger is to create an entity with scale equal to SPIL."

Jason Chang's calculation was straightforward: the OSAT industry needed consolidation to survive Chinese scale. Better to consolidate among Taiwanese players than lose market share to state-subsidized competitors.

ASE "made a tender offer to acquire 5% to 25% of SPIL shares at NT$45 per share. By the end of the tender offer period in September, ASE held 36.83% of SPIL shares."

SPIL's management reacted with fury. "Since SPIL claimed they knew nothing about the M&A plan beforehand, they issued a statement accusing ASE of conducting a 'hostile takeover.'"

Enter Foxconn—the white knight SPIL sought to fend off ASE's advances. "By late August, though, SPIL had announced a deal to collaborate with Foxconn, the terms of which included a share swap giving Foxconn a bigger stake and more voting influence than ASE."

The strategic logic for Foxconn was compelling. "Foxconn has stated that it wants to use SPIL as a way of expanding into areas that may win more orders from Apple—in particular, system-in-package (SiP) chips like the S1 in the Apple Watch."

The battle now involved three of Taiwan's most powerful tech companies, all competing for Apple's favor. "ASE assembles chips used in the Apple Watch, while SPIL last year started supplying chips for iPhones. ASE had planned to take a controlling interest in SPIL in order to protect its market-leading position and remain one jump ahead of competitors."

The legal warfare escalated. "Advanced Semiconductor Engineering (ASE) is seeking an injunction from a Taiwan court to prevent Siliconware Precision Industries (SPIL) from holding a provisional shareholders meeting."

SPIL employees protested in the streets. Shareholder advisory firms weighed in. "Shareholder advisers Institutional Shareholder Services Inc. weighed in on ASE's side. 'The company fails to make a compelling case regarding necessity of the share swap for SPIL's strategic alliance with Hon Hai,' ISS wrote in a report."

The Foxconn deal collapsed when shareholders rejected the share swap. "Passage of both amendments would have meant that Foxconn could proceed with plans to take 21.2 percent of SPIL through the issuance of new shares. ASE's ownership would drop below 20 percent. To make the Foxconn deal happen, SPIL's board needed approval to issue 39 percent more shares to accommodate the new stock to be sold to Hon Hai."

With the Foxconn option foreclosed, negotiations resumed. "The hostile takeover by ASE was unsuccessful and it eventually had to acquire SPIL by negotiated merger."

The resolution came on May 26, 2016. "ASE and Siliconware Precision Industries (SPIL) announced that they signed an agreement to form a new holding company, as part of the consolidation in the global semiconductor industry."

The regulatory marathon that followed tested everyone's patience. "On 24 November 2017 the Ministry of Commerce of the People's Republic of China (MOFCOM) conditionally cleared the proposed acquisition. Due to MOFCOM's concerns that the proposed deal may have the impact of eliminating or restricting competition in the market for original equipment manufacturer (OEM) services for semiconductor assembly and testing, the parties had to withdraw and refile the notification, such that MOFCOM's conditional approval was eventually obtained 15 months after the notification was initially submitted to MOFCOM."

To address concerns, "the parties offered, amongst other commitments, to hold the businesses separate for 24 months. This rather exceptional remedy requires ASE and SPIL to operate independently, for 24 months post-merger, in relation to management, finance, personnel, pricing, sales, production capacity, and procurement."

Finally, on April 30, 2018, ASE Technology Holding Co., Ltd. was formed, fully integrating ASE, SPIL, and Universal Scientific Industrial Co., Ltd. (USI) under a unified structure. The company listed on both the Taiwan Stock Exchange and NYSE.

The three-year battle had transformed Taiwan's semiconductor packaging landscape. The combined entity controlled roughly 30% of the global OSAT market—a dominant position that would prove invaluable when AI demand exploded.

The AI Inflection Point: From Backend Player to Strategic Enabler (2020-Present)

The AI revolution arrived at precisely the right moment for ASE. After years of consolidation and capability building, the company found itself positioned at the center of the industry's most transformative shift since the smartphone revolution.

The catalyst was ChatGPT's November 2022 launch, which triggered an unprecedented surge in demand for AI accelerators. NVIDIA's GPUs became the most sought-after components in technology, and they shared a common requirement: advanced packaging.

"CoWoS is indispensable to producing AI processors, such as the GPUs produced by Nvidia and AMD that are used in AI servers or data centers. 'You could call it the Nvidia packaging process if you want to. Almost anyone making AI chips is using the CoWoS process.'"

The physics are straightforward but the engineering is not. Modern AI chips need to communicate with high-bandwidth memory (HBM) at extraordinary speeds. Traditional packaging can't deliver the necessary interconnect density. CoWoS technology places chips on a silicon interposer—essentially a thin slice of silicon patterned with incredibly fine wiring—that enables thousands of connections between processor and memory.

TSMC invented CoWoS and dominates high-end production. But demand has so far outstripped supply that even TSMC needed help. "NVIDIA's surging demand for AI chips has caused a significant shortage in TSMC's CoWoS advanced packaging capacity. Reports suggest that TSMC has urgently sought support from ASE Technology Holding Co., Ltd. (ASE), marking the first time it has outsourced crucial front-end CoW (Chip-on-Wafer) processes. ASE's subsidiary, SPIL (Siliconware Precision Industries Co., Ltd.), has been awarded these outsourcing orders."

"Industry experts in South Korea point out that after over 30 years of collaboration between TSMC and ASE, Taiwan's packaging ecosystem stands to benefit further from the large volume of AI chip orders secured by TSMC."

The financial impact has been substantial. "ASE's 47% revenue contribution from advanced packaging technologies in Q2 2025 (including bumping, flip chip, wafer-level packaging, and SiP) highlights its growing expertise in this high-margin segment. By 2025, revenue from advanced packaging is projected to surge from $600 million in 2024 to $1.6 billion, a 560% increase over three years."

"We are on track to reach the $1.6 billion mark as planned" for leading-edge revenue, the company stated. "Altogether, we expect ATM 2025 full-year revenue to exceed our target and grow over 20% year over year in US dollar terms."

The capacity expansion to meet this demand has been aggressive. "On January 16, Siliconware Precision Industries (SPIL), a subsidiary of ASE Technology Holding, officially inaugurated its new advanced packaging facility at the Tanzi Science Park. SPIL also announced that three additional advanced packaging facilities are set to expand production capacity by 2025."

"Construction of the K28 plant, expected to be completed in 2026, will expand ASE's CoWoS (Chip-on-Wafer-on-Substrate) advanced packaging capacity. The new plant is the second phase of a plan to build two factories on a two-hectare plot in Kaohsiung's Dashe District in response to growing demand for CoWoS advanced packaging and final testing services."

"The company will maintain its $2.5 billion capital spending plan for 2025, up 32% from last year. A large share will support advanced chip packaging and testing capacity."

The NVIDIA relationship has become particularly important. "SPIL is a key supplier of chip-on-wafer-on-substrate (CoWoS) packaging technology for Nvidia's AI chips. 'We will proactively plan for capacity expansions in line with the Nvidia project,' said ASE COO Tien Wu."

"Nvidia has also enlisted non-TSMC suppliers, including Amkor and ASE, for the remaining 80,000 wafers, demonstrating a multi-faceted sourcing strategy." For AMD, "105,000 CoWoS wafers" are forecast, with "25,000" from "ASE/SPIL for its Venice CPU, which employs CoWoS-L technology."

The technology investments extend beyond CoWoS. "A cornerstone of ASE's 2025 strategy is its $690 million investment in co-packaged optics (CPO) and systems-in-package (SiP). CPO, which integrates optical engines directly onto substrates, offers AI data centers unprecedented bandwidth (3.2 Tb/s) and energy efficiency (<5 pJ/bit)."

"TSMC's partners Siliconware Precision Industries and the ASE Group are also ramping up production throughout Taiwan. Over the past two years, ASE's total expenditure neared NT$200 billion, a historic high."

The relationship with TSMC—sometimes cooperative, sometimes competitive—remains central. "ASE is one of the major beneficiaries from the AI boom as Taiwan Semiconductor Manufacturing Co (TSMC) is outsourcing production of advanced chip packaging technology, or chip-on-wafer-on-substrate (CoWoS), to local outsourced semiconductor assembly and test service providers such as ASE in efforts to solve prolonged capacity constraints." As ASE's CFO noted, "TSMC's aggressive expansion of their back-end leading technology capacity is really a statement of a very, very strong demand coming in the next few years."

Global Footprint and Geopolitical Navigation

ASE's geographic diversification represents one of the semiconductor industry's most sophisticated hedging strategies against geopolitical risk.

As of September 30, 2025, the company employed 103,844 people globally. The manufacturing footprint spans Taiwan, China, South Korea, Japan, Singapore, Malaysia, Vietnam, Mexico, the United States, and multiple European locations.

The Malaysia expansion exemplifies the strategic calculus. "ASE has officially launched its fifth plant in Penang, which will significantly build on the company's strong packaging and testing capabilities in the Bayan Lepas Free Industrial Zone."

"The new plant is part of a strategic expansion plan that will expand the floor space of ASE's Malaysia facility from its current area of 1 million square feet to approximately 3.4 million square feet."

"The geopolitical calculus here is clear: ASE is reducing exposure to U.S.-imposed export restrictions on China by bolstering capacity in Malaysia. These rules, which limit TSMC from shipping chips to China without BIS-approved packaging partners, have created a regulatory advantage for ASE. By serving as a neutral, geographically diversified partner, ASE is becoming a critical link in the global supply chain."

The expansion continues. "ASE Technology Holding Co., Ltd. and Analog Devices, Inc. today announced strategic joint efforts in Penang, Malaysia with the signing of a binding Memorandum of Understanding. Subject to the execution of the definitive transaction documents, ASE intends to purchase 100% of the equity of Analog Devices Sdn. Bhd. and consequently its manufacturing facility in Penang. In addition, ADI and ASE intend to enter into a long-term supply agreement for ASE to provide manufacturing services for ADI."

The U.S. expansion question looms large. "'US production is feasible, but it depends on customer support and skilled local labor,' Wu said. 'Beyond that, we've received more customer requests to build 'Made-in-America' packaging capacity, which we're currently evaluating.'"

"TSMC is expanding its advanced packaging (CoWoS) capacity by selecting a site in the southern region, while ASE also announced the construction of a second packaging and testing factory in California, USA, and plans to build another in Mexico."

The challenge is significant. Semiconductor packaging requires skilled technicians, established supply chains, and cultural expertise that took decades to develop in Taiwan. Replicating that ecosystem in Arizona or Texas is neither quick nor cheap.

Yet the pressure is real. The CHIPS Act has created powerful incentives for domestic U.S. production. Major customers increasingly demand supply chain diversification. And the risk of cross-strait conflict—however remote—has focused minds on concentration risk.

ASE's response has been characteristically pragmatic: expand in multiple directions simultaneously, let customer demand guide capacity allocation, and maintain flexibility to pivot as geopolitical winds shift. It's a strategy that sacrifices theoretical optimization for real-world resilience.

Business Model Deep Dive: The Three Pillars of ASEH

Understanding ASE requires grasping its three-pillar business structure, each with distinct economics, growth trajectories, and strategic importance.

Packaging Operations represent the traditional core. Net revenues from packaging operations represented approximately 47% of total net revenues in Q3 2025. This segment takes fabricated wafers and transforms them into packaged integrated circuits ready for system integration.

The technology portfolio spans the complexity spectrum. "ASE specializes in semiconductor assembly, packaging, and testing services, offering a wide range of packaging technologies such as fan-out wafer-level packaging (FO-WLP), wafer-level chip-scale packaging (WL-CSP), flip chip, 2.5D and 3D packaging, and system in package (SiP)."

The margin profile varies dramatically by technology tier. Traditional wire-bond packages are essentially commodities—high volume, low margin, differentiated mainly by cost and reliability. Advanced packaging, particularly 2.5D/3D integration for AI chips, commands premium pricing and delivers margin expansion.

Testing Operations contributed approximately 11% of Q3 2025 revenue. This segment provides front-end engineering testing, wafer probing, and final testing services. The testing business has become increasingly important as chip complexity rises and AI processors require ever-more-sophisticated validation.

Electronic Manufacturing Services (EMS) operations represented roughly 41% of revenue, primarily through subsidiary Universal Scientific Industrial (USI). This segment provides contract manufacturing for computing, peripherals, communications, industrial, automotive, and server applications.

The EMS business operates differently from ATM (Assembly, Test, and Manufacturing). It's higher volume, lower margin, and more exposed to consumer electronics cycles. Yet it provides diversification and customer relationship depth that would be difficult to replicate.

Financial Strength

"For the full year of 2024, the Company reported unaudited net revenues of NT$595,410 million and net income attributable to shareholders of the parent of NT$32,483 million."

"With $77.1 billion in cash reserves as of Q2 2025 and a net debt-to-equity ratio of 0.41, the company has the flexibility to fund aggressive CapEx without overleveraging. Its 11.6% YoY revenue growth in Q1 2025 and 16.8% gross margin demonstrate robust pricing power and operational efficiency."

The capital allocation philosophy balances growth investment with shareholder returns. The company has maintained dividend payments while simultaneously ramping CapEx to historic levels. The $2.5 billion planned for 2025—a 32% increase from 2024—signals confidence in demand visibility.

"For the third quarter of 2025, we had record revenues for our ATM business of TWD 100.3 billion, up TWD 7.7 billion from the previous quarter and up TWD 14.5 billion from the same period last year."

Competitive Dynamics: Porter's Five Forces Analysis

Understanding ASE's competitive position requires systematic analysis of industry structure.

Threat of New Entrants: LOW

The barriers to entry in OSAT are formidable and rising. Capital requirements have escalated as advanced packaging demands cleanroom facilities rivaling foundries in sophistication. "Taiwanese companies have actively developed advanced semiconductor packaging and commercializing CoWoS at an earlier time, while South Korean packaging companies lag in accumulated technologies."

The knowledge barrier may be even more significant. Packaging isn't just about equipment; it's about process know-how accumulated over millions of production hours. ASE has 40 years of learning curve advantages that can't be purchased.

Customer relationships compound the advantage. Qualifying a new packaging supplier takes years. Customers are reluctant to add risk to complex supply chains. The stickiness of relationships creates high switching costs even when pricing differs.

Bargaining Power of Suppliers: MODERATE

ASE depends on specialized equipment suppliers (ASML, Applied Materials, Tokyo Electron) for packaging tools and on materials suppliers for substrates, lead frames, and bonding wire. These suppliers serve multiple OSATs, creating some balance in negotiations.

However, specialized materials for advanced packaging can create chokepoints. Supply constraints in certain components—like the advanced substrates required for CoWoS—can limit ASE's ability to ramp capacity even when customer demand exists.

Bargaining Power of Buyers: MODERATE TO HIGH

"Our five largest customers together accounted for approximately 41% of our total net revenues in 3Q25. One customer accounted for more than 10% of our total net revenues in 3Q25."

Customer concentration creates meaningful negotiating leverage. NVIDIA, Apple, AMD, Qualcomm, and other major customers can credibly threaten to shift volume. However, the limited alternatives for advanced packaging at scale—essentially ASE, Amkor, and TSMC's internal capacity—provides counterbalancing power.

The balance shifts toward ASE during capacity constraints. When CoWoS capacity is short, customers compete for allocation rather than negotiating price. The AI demand surge has temporarily shifted this dynamic in ASE's favor.

Threat of Substitutes: MODERATE

The most significant substitute threat comes from vertical integration. "TSMC 3DFabric® offers 3D silicon stacking and advanced packaging technologies, such as TSMC-SoIC® (System on Integrated Chips), CoWoS® (Chip on Wafer on Substrate), and InFO (Integrated Fan-Out), to enable homogeneous and heterogeneous chip integration."

"Competition is intensifying as foundries integrate backend offerings. TSMC's 3DFabric positioned the firm as a one-stop advanced-packaging supplier, challenging OSAT pricing power."

Intel and Samsung also maintain significant internal packaging capabilities. For certain high-volume products, these integrated players can offer advantages in cycle time and yield optimization.

However, the OSAT model offers flexibility that vertical integration cannot match. Fabless companies prefer working with independent packaging providers who serve multiple customers and can aggregate demand for better economics.

Industry Rivalry: HIGH

"Amkor was in second place in the OSAT rankings with a 15.2% share in 2024, followed in order by JCET (12%), Tongfu Microelectronics (8%), Powertech Technology (5.5%), HT-Tech (4.8%)."

"JCET, ranking third globally, saw its sales increase by 19.3% in 2024, reaching $5 billion. HT-Tech achieved the highest annual growth among the top ten OSATs, with a 26% revenue increase in 2024."

Chinese competitors are gaining ground, supported by domestic demand and government subsidies. The technological gap is narrowing in some segments, though Taiwanese companies maintain leadership in the most advanced packaging technologies.

The rivalry intensifies during demand downturns, when excess capacity triggers price competition. The semiconductor industry's cyclicality creates periodic margin compression that challenges all players.

Hamilton Helmer's 7 Powers: Where Does ASE's Moat Come From?

Analyzing ASE through Hamilton Helmer's strategic framework reveals multiple sources of durable competitive advantage:

Scale Economies: ASE's massive production volume enables capital efficiency unavailable to smaller competitors. A packaging line running at high utilization delivers dramatically better returns than one operating below capacity. The fixed costs of cleanrooms, equipment, and engineering can be spread across more units, creating cost advantages that compound over time.

Network Effects: Limited direct network effects exist in packaging itself. However, the ecosystem relationships around advanced packaging—with EDA vendors, substrate suppliers, test equipment makers—create something analogous. ASE's scale makes it a priority development partner, giving it early access to enabling technologies.

Counter-Positioning: Interestingly, ASE's independent OSAT model benefits from counter-positioning against integrated players. TSMC expanding into packaging creates potential conflicts with customers who also compete with TSMC. ASE's neutrality—it doesn't design chips or manufacture wafers—makes it a "Switzerland" that customers can trust with sensitive production.

Switching Costs: Qualifying a new packaging supplier requires extensive testing, reliability validation, and process optimization. Once a customer's chip design is qualified on ASE's process, switching creates technical risk and delays time-to-market. These switching costs create revenue durability even when competitors offer lower prices.

Cornered Resource: ASE's four decades of process knowledge represent an intellectual resource that can't be easily replicated. The tacit knowledge embedded in its engineering teams—knowing how to handle subtle process variations, troubleshoot yield issues, optimize new package designs—takes years to develop and can't be purchased.

Process Power: Manufacturing excellence is perhaps ASE's most fundamental advantage. The discipline developed through millions of production lots, the quality systems refined through environmental crisis, the operational metrics tracked obsessively—these create sustainable advantages in yield, reliability, and customer satisfaction.

Brand: In B2B semiconductor services, "brand" means reputation for execution. ASE's track record with the world's most demanding customers—Apple, NVIDIA, Qualcomm—signals capabilities to prospective customers. The willingness of Jensen Huang to personally visit ASE facilities speaks volumes about the relationship quality.

The Bull Case

The optimistic scenario for ASE rests on several powerful tailwinds:

AI Demand Persistence: If AI infrastructure spending continues at current rates—or accelerates—ASE sits at a critical chokepoint. Every GPU, TPU, and custom AI accelerator requires advanced packaging. "The OSAT market was valued at USD 44.1 billion in 2024 and is projected to reach USD 102.5 billion by 2034." ASE would capture a disproportionate share of this growth given its market position.

Technology Leadership: The investments in CoWoS, co-packaged optics, and panel-level packaging could position ASE to capture next-generation demand. If these technologies prove essential for AI chip evolution, first-mover advantages could translate to sustained premium pricing.

Geographic Diversification: The Malaysia, Mexico, and potential U.S. expansions could prove prescient if geopolitical tensions further fragment supply chains. Customers increasingly value suppliers who can manufacture in multiple jurisdictions.

Partnership Deepening: The TSMC relationship continues strengthening as both companies invest in adjacent capabilities. If TSMC continues outsourcing backend work rather than fully verticalizing, ASE benefits from the industry structure.

Margin Expansion: As advanced packaging grows from 10% to 20%+ of revenue, the higher-margin mix could drive consolidated margin improvement even without pricing power increases.

The Bear Case

The cautionary scenario centers on several meaningful risks:

TSMC Vertical Integration: TSMC's 3DFabric initiative represents an existential question. "TSMC 3DFabric® is the Company's comprehensive family of 3D silicon stacking and advanced packaging technologies. 3DFabric complements TSMC's advanced semiconductor technologies that unleashes customer innovation." If TSMC decides to bring more packaging in-house, ASE loses its most important partner and faces a formidable competitor.

Chinese Competition: "China's JCET saw its sales grow by 19.3% in 2024." Chinese OSATs are improving rapidly, often with government support that enables aggressive pricing. Market share erosion in mainstream packaging could pressure margins even as advanced packaging grows.

Customer Concentration: Dependence on a handful of major customers creates vulnerability. If any major customer shifts strategy—bringing packaging in-house, shifting to competitors, or reducing overall volume—the impact would be significant.

Cyclicality: The semiconductor industry remains cyclical despite AI-driven optimism. When the inevitable downturn arrives, ASE's high fixed-cost structure magnifies margin compression. The company has navigated cycles before, but each one tests operational discipline.

Geopolitical Risk: Despite diversification efforts, significant operations remain in Taiwan. Any escalation in cross-strait tensions would create severe disruption regardless of capacity elsewhere.

Technology Transition Risk: Packaging technology continues evolving rapidly. If a new paradigm emerges that disadvantages ASE's existing capabilities—perhaps chiplet standards that favor different integration approaches—the company's investments could become stranded.

Key Performance Indicators to Track

For investors following ASE, several metrics deserve ongoing attention:

1. Advanced Packaging Revenue Percentage: The most critical metric is the share of revenue from advanced packaging (CoWoS, SiP, 2.5D/3D). "The strong growth momentum would elevate the revenue contribution from ASE's advanced packaging and testing technology segment to 12 percent or 13 percent of the company's total ATM revenue next year." Expansion of this percentage indicates successful positioning for the AI era. Stagnation would signal competitive challenges.

2. Gross Margin Trajectory: "The company's operations showed mixed performance, with ATM segment's gross margin improving to 23.1%." Margin trends reveal pricing power and operational efficiency. If advanced packaging growth fails to improve margins, the AI opportunity may be less valuable than anticipated.

3. CapEx to Revenue Ratio: The intensity of capital investment relative to revenue indicates management's confidence in demand visibility and willingness to bet on growth. The 2025 plan of $2.5 billion represents roughly 13% of expected revenue—aggressive by historical standards.

Myth vs. Reality

Myth: ASE is a low-margin commodity packaging business.

Reality: While traditional packaging has commodity characteristics, ASE has systematically built capabilities in high-value segments. Advanced packaging margins exceed traditional packaging by significant multiples, and this mix shift is accelerating.

Myth: TSMC will eventually do all packaging in-house.

Reality: The economics and customer dynamics argue against full verticalization. TSMC's customers often compete with each other and value independent packaging options. TSMC also benefits from capacity flexibility—outsourcing during peaks and pulling work in-house during troughs.

Myth: Chinese competitors will commoditize advanced packaging.

Reality: "Taiwanese companies have actively developed advanced semiconductor packaging and commercializing CoWoS at an earlier time, while South Korean packaging companies lag in accumulated technologies." The technology gap in leading-edge packaging remains substantial and may take years to close.

Conclusion: The Essential Enabler

Jason and Richard Chang's 1984 bet on Kaohsiung has grown into something extraordinary: a company that enables virtually every semiconductor manufacturer to bring products to market, that touches devices in every pocket and data center, that sits at the intersection of the industry's most powerful trends.

ASE Technology Holding isn't glamorous. It doesn't launch products that consumers queue for or generate the headlines that foundries and chip designers attract. But it may be the most essential company in the semiconductor supply chain that most people have never heard of.

The AI revolution has elevated packaging from afterthought to strategic imperative. The company that spent decades building capabilities for this moment now finds itself at the center of technology's most important supply chains. Whether it can sustain this position through cycles, competition, and geopolitical turbulence remains the critical question.

Jason Chang's current net worth of $7.08 billion reflects four decades of patient capital allocation and operational excellence. "On the Forbes 2024 list of the world's billionaires, he was ranked #417 with a net worth of US$6.6 billion."

For investors, ASE presents a classic crossroads: a market leader benefiting from secular trends, yet facing legitimate competitive and geopolitical concerns. The company's history suggests resilience—it has navigated environmental crises, hostile takeovers, and industry cycles. The next chapter will test whether that resilience extends to an era of AI-driven transformation and great power competition.

The hidden giant behind every chip has emerged from the shadows. What happens next depends on choices made in Kaohsiung, decisions rendered in Washington and Beijing, and the relentless physics of Moore's Law finally meeting its match.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube