Symbotic: The Warehouse Automation Revolution

I. Introduction & Episode Roadmap

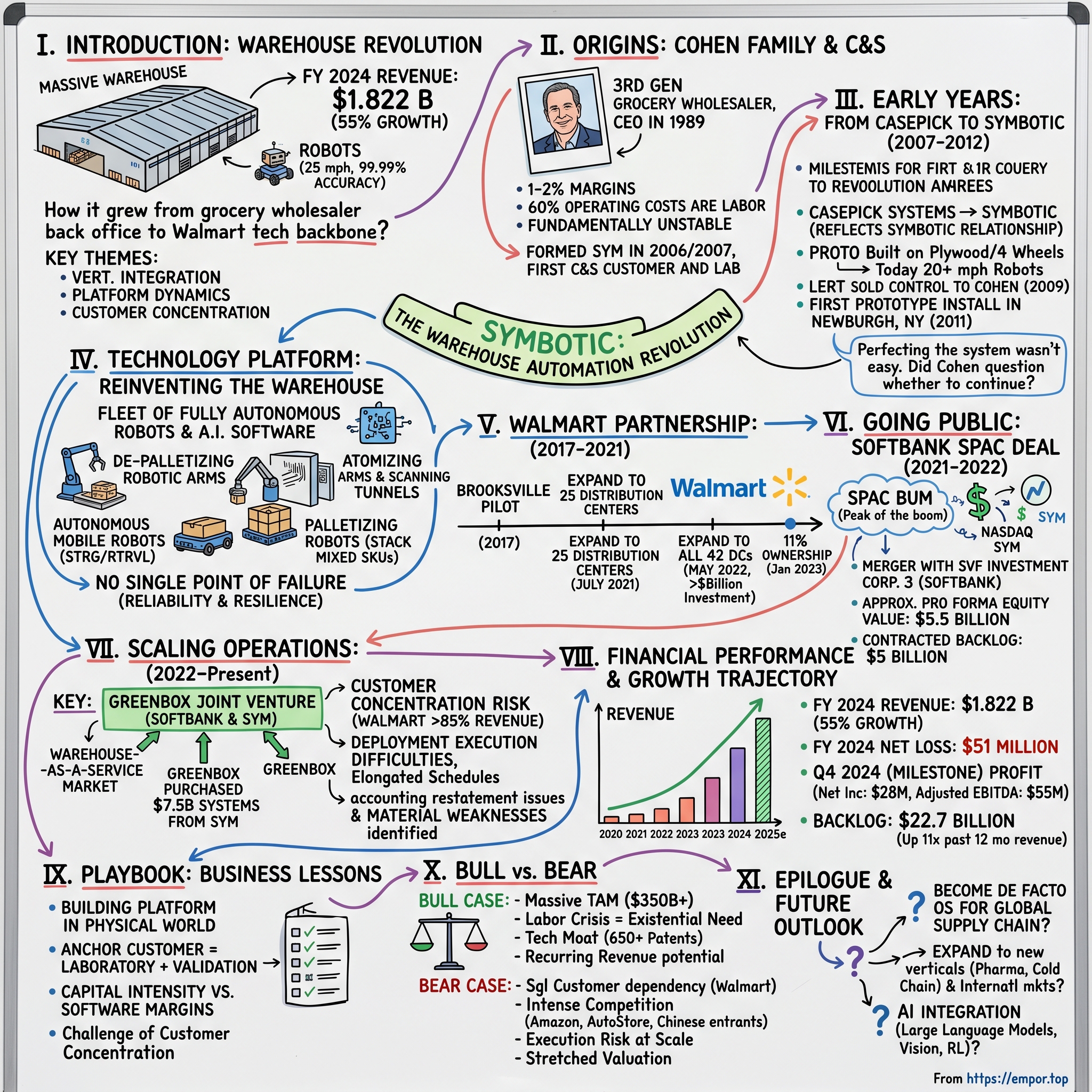

Picture this: Inside a massive warehouse the size of multiple football fields, hundreds of autonomous robots zip through narrow aisles at 25 miles per hour, their movements choreographed by artificial intelligence with balletic precision. No human workers navigate these corridors—the robots handle everything from storage to retrieval, operating 24/7 with 99.99% accuracy. This isn't science fiction or a glimpse into some distant future. This is Symbotic's warehouse automation system, already operational and transforming how consumer goods move through America's supply chain today.

The company behind this revolution posted $1.822 billion in revenue for fiscal 2024, growing 55% year-over-year—remarkable numbers for a business that emerged from the back office of a grocery wholesaler. But here's the question that makes this story fascinating: How did an internal automation project at C&S Wholesale Grocers, born from one man's frustration with razor-thin margins and crushing labor costs, evolve into the technological backbone powering Walmart's ambitious automation strategy?

The answer reveals a quintessentially American business saga—one where family legacy meets technological disruption, where patient capital development collides with the SPAC boom, and where the unglamorous world of warehouse operations becomes the nexus of a multi-billion dollar robotics revolution. This is the story of Rick Cohen, a third-generation grocery wholesaler who looked at his grandfather's business and decided to rebuild it from first principles using robots and AI.

Over the next several hours, we'll trace Symbotic's journey from a prototype built on plywood and four wheels to a public company valued in the billions. We'll explore how they convinced the world's largest retailer to bet its supply chain future on their technology. We'll dissect the engineering breakthroughs that made fully autonomous warehouses possible. And we'll examine the fundamental tension at the heart of this business: Can a hardware-intensive robotics company achieve software-like margins while maintaining the reliability demanded by Fortune 500 supply chains?

The themes we'll encounter—vertical integration, platform dynamics, customer concentration risk, the challenge of scaling complex systems—offer lessons that extend far beyond warehouse automation. Because ultimately, Symbotic's story isn't just about robots replacing humans in distribution centers. It's about the convergence of multiple technological waves—robotics, artificial intelligence, and supply chain digitization—creating opportunities for those bold enough to reimagine entire industries from the ground up.

II. Origins: The Cohen Family & C&S Wholesale Grocers

The year was 1989, and Rick Cohen had just inherited a problem disguised as an opportunity. His grandfather's wholesale grocery business, C&S Wholesale Grocers, had grown from a small New England operation into one of America's largest food distributors. But Cohen, fresh from studying the business with an outsider's eye, saw what industry veterans had long accepted as immutable: the wholesale grocery business was fundamentally broken. In 1974, Cohen began working at the family company, C&S Wholesalers in Worcester, Massachusetts, which was co-founded by his grandfather, Israel Cohen, in 1918. The business had survived the Great Depression, navigated World War II's rationing, and adapted to the supermarket revolution of the 1950s. But by the time Rick took over as CEO from his father, Lester, in 1989, he saw an industry trapped in a vicious cycle.

The numbers told a brutal story. Grocery wholesaling operated on net margins of 1-2%, sometimes less. Labor costs consumed nearly 60% of operating expenses. A single mis-picked case could wipe out the profit from dozens of correctly fulfilled orders. Workers manually handled millions of cases per week, leading to injury rates that ranked among the highest in American industry. The entire business model depended on human muscle moving boxes from Point A to Point B—a fundamentally unscalable proposition in an era of rising labor costs and worker shortages.

Cohen approached the problem with the analytical mindset of his Wharton accounting training. He had graduated from the Wharton School of the University of Pennsylvania with a degree in economics, concentrating in accounting, in 1974, bringing a financial rigor that his grandfather's generation might have viewed as unnecessarily academic. But Cohen understood something crucial: in a business with razor-thin margins, even small efficiency gains could translate to massive competitive advantages. The company was founded in 2006 by Rick Cohen, though technically around 2005, an inventor named John Lert reached out to Cohen about starting an automation company for grocery stores. Cohen provided financing to form the startup in 2007. This wasn't a Silicon Valley startup born from a Stanford dorm room or a venture capital brainstorming session. This was a third-generation grocery wholesaler who understood viscerally that his industry's entire economic model was unsustainable.

"Experiencing firsthand how low margin and inefficient wholesale businesses are due to high labor costs, Cohen came up with the vision to have fully automated warehouses," as company documents would later state. But the vision wasn't born from technological optimism—it emerged from decades of operational pain. Cohen had watched his best warehouse workers develop chronic back problems. He'd seen turnover rates exceed 100% annually. He'd calculated how much profit evaporated every time a forklift operator took a bathroom break.

Not finding a suitable solution in the market, Cohen began with a blank sheet of paper and a vision to create one. This wasn't hubris—it was necessity. The existing automation vendors offered piecemeal solutions: a sortation system here, an automated storage and retrieval system there. But Cohen understood that incremental improvements to a fundamentally broken model wouldn't suffice. The entire warehouse needed to be reimagined from first principles.

Cohen put "hundreds of millions" of his own dollars into the business—a staggering personal bet that would eventually exceed $700 million over Symbotic's history. This wasn't venture capital with its power law returns and portfolio diversification. This was a grocery wholesaler betting his family fortune on robots.

The grocery business, ironically, provided the perfect testing ground for warehouse automation. The combination of high volume, low margins, and labor intensity created both the maximum pain and the maximum potential gain. A typical grocery distribution center handles thousands of SKUs, processes millions of cases per week, and operates on net margins so thin that a 1% efficiency improvement could double profitability. If you could solve automation for grocery, Cohen reasoned, you could solve it for anything.

But perhaps most importantly, Cohen brought something to the automation challenge that Silicon Valley entrepreneurs lacked: he was his own first customer. C&S Wholesale Grocers would serve as both the laboratory and the proving ground for whatever technology emerged. There would be no need to convince skeptical customers to take a chance on unproven technology—Cohen could test, iterate, and perfect the system in his own facilities, where failure meant disappointing himself rather than losing a client.

This vertical integration between customer and developer would prove crucial. While competitors had to negotiate every product change with arms-length customers, Cohen could walk from the boardroom to the warehouse floor and implement modifications in real-time. The feedback loop was measured in hours, not quarters. And the stakes were personal—every operational failure directly impacted the family business that three generations had built.

III. Early Years: From CasePick to Symbotic (2007–2012)

Initially called CasePick Systems, the startup focused on packing and unpacking pallets of boxes at distribution warehouses. The name itself revealed the narrow scope of the original ambition—this wasn't yet about reimagining the entire warehouse, just solving one specific pain point in the case-picking process.

Evolved from an early prototype built on a piece of plywood and four wheels, today A.I.-powered Symbotic robots autonomously navigate a football field size structure at speeds up to 20+ mph. But that evolution took years of false starts, engineering dead ends, and moments where Cohen questioned whether to continue. "There were plenty of times where we said, 'Should we quit? Should we cut our losses?" Cohen would later admit.

The financial crisis of 2008-2009 nearly killed the company before it could prove its concept. After having trouble raising money amid the financial crisis, Lert sold his majority stake to Cohen in 2009. The inventor who had sparked the initial idea was forced to cede control to the businessman with deeper pockets. "We had a complex relationship," Lert said of Cohen in an interview. "I'm very happy for his success and proud of the work we did."

By 2011, the first prototype system was installed at a C&S warehouse in Newburgh, New York—the moment of truth after four years of development. The early system was primitive compared to what would come later, but it demonstrated the core concept: autonomous robots could navigate warehouse aisles, retrieve cases, and build mixed pallets without human intervention. The technology worked, barely, but it worked.

In 2012, Cohen changed the company's name to Symbotic, reflecting the close relationship the robots would have with a warehouse's operations. The company was renamed to Symbotic to indicate the connection to both supply chain and robotics. The new name signaled a broader ambition—this wasn't just about picking cases anymore, but about creating a symbiotic relationship between human workers, robotic systems, and the flow of goods through the supply chain.

But perfecting the system wasn't easy, and Cohen had sharp elbows. Though he was the chairman, not the CEO, Cohen involved himself in everything from hiring to product design to sales, some of his former employees said. This hands-on approach—some would say micromanagement—reflected both Cohen's personal investment in the company and his deep skepticism that anyone else understood the problem as intimately as he did.

The engineering challenges during these early years were staggering. How do you build a robot that can operate reliably in a refrigerated environment? How do you create software sophisticated enough to orchestrate hundreds of robots simultaneously without collisions? How do you design a system modular enough to retrofit into existing warehouses but standardized enough to manufacture at scale?

Each breakthrough created new problems. Making the robots faster increased the complexity of the traffic management software. Adding more SKUs to the system exponentially increased the computational requirements for optimization. Every customer request for customization threatened to fragment the product into unsupportable variants.

Cohen's approach was ruthlessly pragmatic. Unlike Silicon Valley startups that sought elegance and scalability from day one, Symbotic's early systems were held together with industrial-strength duct tape and determination. If a solution worked in the warehouse, it was good enough, even if it offended the sensibilities of the engineers. The only metric that mattered was whether cases moved from point A to point B faster and cheaper than human workers could manage.

The Newburgh installation became a pilgrimage site for potential customers and skeptics alike. Executives from major retailers would tour the facility, watching robots zip through aisles at speeds that seemed impossible given the narrow clearances. Many left impressed but unconvinced—the system worked in Cohen's controlled environment, but could it scale to the chaos of their own operations?

By the end of 2012, Symbotic had spent five years and tens of millions of dollars to build a system that worked in exactly one warehouse. The technology had proven feasible, but the business model remained unproven. The question now was whether any customer beyond C&S would take the leap of faith required to redesign their entire warehouse operations around Symbotic's radical new approach.

IV. The Technology Platform: Reinventing the Warehouse

Symbotic reinvented the traditional warehouse with an end-to-end system leveraging a fleet of fully autonomous robots and A.I.-powered software. To understand the revolutionary nature of this system, consider the traditional warehouse: a massive open space where human workers drive forklifts down wide aisles, manually picking cases from static shelves, building pallets by hand, relying on memory and paper lists to track inventory. It's a system that hasn't fundamentally changed since the invention of the forklift in 1917.

Symbotic's vision was radically different. Imagine instead a dense three-dimensional grid, where every cubic foot of space serves as potential storage, where robots move in perfectly choreographed patterns like a three-dimensional ballet, where artificial intelligence continuously optimizes the placement of every case for maximum efficiency.

Symbotic claims to have the fastest robots in the industry, travelling through the warehouse at speeds of 25 mph. These aren't the slow, deliberate movements of traditional industrial robots. The Symbots—as the company calls them—accelerate like sports cars, navigating aisles with mere inches of clearance on either side. The engineering required to achieve this speed while maintaining safety and reliability pushed the boundaries of what was possible in industrial robotics.

The system's architecture reveals its sophistication. The platform is composed of de-palletizing robotic arms, which pick cases from newly arrived pallets; atomizing robotic arms, which put the cases in scanning tunnels; autonomous mobile robots, which store and retrieve cases; and palletizing robots that stack pallets with the needed SKUs. Each component represents a different engineering challenge solved: computer vision for identifying and grasping cases of varying sizes, path planning for robot navigation, optimization algorithms for storage placement, structural engineering for building stable mixed-SKU pallets.

The overall warehousing structure of Symbotic's system is composed of three feet tall levels stacked on top of each other. Each level contains a series of parallel aisles for the robots to travel to the storage locations. This density is crucial—by building vertically and eliminating the wide aisles required for human workers and forklifts, Symbotic can store the same inventory in 40% less space than a traditional warehouse.

The software system uses AI to determine the cases' optimal location in order to reduce robot travelling times. This isn't simple bin packing or first-in-first-out inventory management. The AI considers factors like SKU velocity (how often an item is ordered), order patterns (which items are frequently ordered together), seasonal variations, and even the weight distribution needed to build stable pallets. The system continuously learns and adapts, moving inventory proactively based on predicted demand.

According to internal metrics, the platform has an accuracy of more than 99.99%—a staggering achievement in an industry where human error rates typically range from 1-3%. This accuracy isn't just about avoiding mistakes; it fundamentally changes the economics of distribution. When errors are virtually eliminated, you don't need quality control checks, you don't need returns processing for mis-picked orders, you don't need customer service representatives handling complaints about wrong shipments.

The system's resilience was perhaps its most innovative feature. Traditional automation fails catastrophically—when a conveyor belt breaks, the entire line stops. Symbotic designed for graceful degradation: The whole system is designed so that there isn't a single point of failure. There are a multitude of robots, lifts and conveyor belts so that any task can always be taken over. Additionally, all equipment has a modular design so that components can easily be swapped on site.

The mobile robots are automatically recharged by charge plates integrated into the floors, allowing them to work continuously. This seemingly minor detail eliminates one of the major constraints of mobile robotics—battery life. The robots charge opportunistically during brief pauses in their routes, maintaining near-constant operation without dedicated charging downtime.

The engineering philosophy behind the platform reflected Cohen's practical background. This wasn't technology for technology's sake—every innovation had to deliver measurable ROI. The robots were fast not because speed was impressive, but because faster robots meant fewer robots were needed. The system was modular not for elegance, but so it could be installed without shutting down existing operations. The AI was sophisticated not to showcase machine learning capabilities, but because better optimization directly translated to labor savings.

Yet for all its sophistication, the system had to be operable by warehouse workers without engineering degrees. The human interface was deliberately simple—tablet-based controls, visual indicators, automated alerts for maintenance needs. Symbotic understood that the most advanced automation in the world was worthless if the customer's existing workforce couldn't maintain and operate it.

The culmination of these technological advances was a system that could handle the full complexity of modern distribution: thousands of SKUs, millions of cases per week, constant changes in inventory and demand patterns, all while maintaining near-perfect accuracy and reliability. It wasn't just an improvement on the traditional warehouse—it was a fundamental reimagining of how goods should flow through the supply chain.

V. Customer Validation & Walmart Partnership (2017–2021)

In 2014, Target adopted Symbotic's technology rather than building a new distribution center in Woodland, California. This early win proved crucial—Target's endorsement signaled to the industry that Symbotic wasn't just Cohen's expensive hobby, but a viable solution for major retailers. Yet it was the relationship with Walmart that would transform Symbotic from an interesting automation vendor into a strategic partner reshaping American retail logistics.

In 2017, Symbotic began working with Walmart at their distribution center in Brooksville, Florida, where the company's automated technology was deployed to sort, store, retrieve and pack freight onto pallets. The retail giant had been testing the technology at one of its Florida distribution centers for more than three years and watched it slowly improve. This wasn't a typical vendor pilot—Walmart's engineers embedded themselves in the facility, studying every aspect of the system's performance, documenting every failure, suggesting hundreds of modifications.

The Brooksville pilot revealed both the promise and the challenges of automation at Walmart scale. The world's largest retailer moves approximately 5 billion cases annually through its distribution network. A system that worked perfectly 99% of the time would still result in 50 million errors per year—unacceptable for a company obsessed with operational excellence. Walmart pushed Symbotic to achieve reliability levels that seemed impossible, forcing innovations that would benefit all future customers. In July 2021, Walmart began introducing Symbotic robots to 25 additional regional distribution centers. The new deal expanded a partnership first piloted in 2017 that's set to bring robotics to 25 regional Walmart distribution centers. This wasn't just another vendor contract—it represented a fundamental bet by America's largest retailer on the future of supply chain automation.

The validation process—proving the technology at scale—had taken four grueling years. Walmart's engineers documented every robot collision, every software glitch, every instance where a human worker had to intervene. They pushed Symbotic to achieve speeds and accuracy levels that seemed physically impossible. The robots had to operate in temperatures ranging from freezing to over 100 degrees Fahrenheit. They had to handle products from fragile eggs to 50-pound bags of dog food. They had to maintain 99.99% uptime during peak holiday seasons when any disruption could leave store shelves empty.

Walmart's strategic decision to bet on Symbotic over alternatives reflected a careful analysis of the competitive landscape. Amazon had acquired Kiva Systems in 2012 for $775 million, effectively removing the leading warehouse robotics company from the market by making it exclusive to Amazon's operations. AutoStore offered impressive density but couldn't handle the case-level picking Walmart required. Other vendors provided point solutions but lacked the end-to-end integration Walmart demanded.

The partnership structure revealed sophisticated deal-making. The two announced today an extension of their relationship that will bring robotics to 25 regional Walmart distribution centers. The company says the rollout will take "several years" to complete. Rather than acquiring Symbotic outright—as Amazon had done with Kiva—Walmart structured a commercial partnership that aligned incentives while preserving optionality.

"The digital transformation happening today, alongside evolving customer habits, is reshaping the retail industry," Walmart's Joe Metzger said in the announcement. But this wasn't just about digital transformation—it was about survival. Walmart understood that without automation, it couldn't compete with Amazon on delivery speed or cost. The math was stark: labor represented 65% of distribution center operating costs, and those costs were rising 5-7% annually while automation costs were falling by similar percentages.

Cohen's ability to land Walmart as a customer reflected more than just superior technology. Supplying groceries taught Cohen about logistics and automation and opened doors to large retailers, including Walmart, which has been a C&S customer. "They remembered me," Cohen said in a 2021 Forbes interview. "It's a very small world." The existing relationship between C&S and Walmart created trust that no amount of venture capital or technical specifications could replicate.

The initial commitment to 25 distribution centers was conservative by Walmart standards—less than 60% of its regional distribution network. This reflected both Walmart's natural caution and the massive operational challenge of retrofitting existing facilities while maintaining operations. Each installation would require months of planning, weeks of physical construction, and months more of testing and optimization.

But behind the scenes, something remarkable was happening. In May 2022, just ten months after the initial announcement, Walmart expanded the partnership dramatically. Symbotic LLC, a revolutionary A.I.-powered supply chain technology company, and Walmart Inc. announced an expanded commercial agreement to implement Symbotic's robotics and software automation platform in all 42 of Walmart's regional distribution centers over the coming years. This is an expansion of Walmart's prior commitment to deploy Symbotic Systems in 25 regional distribution centers.

This expansion from 25 to 42 distribution centers—Walmart's entire regional network—represented one of the largest automation commitments in corporate history. The retrofitting process of all 42 regional distribution centers is expected to be completed over the next 8+ years. The multi-billion dollar investment would transform how Walmart moved products to its 4,700+ U.S. stores.

The strategic implications extended beyond operational efficiency. Walmart will own 9% of the robotics/AI firm. It's not quite the all-in acquisitions of companies like Kiva Systems that have formed the foundation of Amazon Robotics, but it's clear now that Walmart has determined commitments to robotic fulfillment centers to be a necessary step toward its future. As part of the deal, Walmart got a stake in Symbotic and owned 11 percent of the company's shares as of January 2023. Walmart also can have an observer at board meetings and has the right to match outside investment offers, according to Symbotic's annual report.

The partnership validated not just Symbotic's technology but its entire approach to warehouse automation. Where competitors offered incremental improvements, Symbotic had reimagined the warehouse from first principles. Where others sought to augment human workers, Symbotic had designed for full autonomy. Where the industry accepted 95-98% accuracy as excellent, Symbotic had achieved 99.99%.

For Cohen, the Walmart partnership represented vindication of a 15-year journey from prototype to production. But it also created a new challenge: how to scale from a single anchor customer to a broader market, how to maintain innovation while managing explosive growth, and how to navigate the public markets that would soon come calling.

VI. Going Public: The SoftBank SPAC Deal (2021–2022)

In December 2021, the company announced it was going public through a merger with SVF Investment Corp. 3, a special-purpose acquisition company sponsored by an affiliate of SoftBank Investment Advisers. The announcement came at the peak of the SPAC boom, when blank-check companies had become the preferred vehicle for technology companies seeking public market capital without the scrutiny of a traditional IPO.

Combination with SVF Investment Corp. 3 Values Symbotic at an Approximate Pro Forma Equity Value of $5.5 Billion. The valuation represented a stunning achievement for a company that had operated in relative obscurity for most of its existence. The transaction values Symbotic at a pro forma enterprise value of $4.8 billion, representing 4.8x Symbotics forecast 2023 calendar year end estimated revenues—aggressive multiples that reflected both the market's enthusiasm for automation and SoftBank's characteristic optimism about transformative technologies.

The SPAC boom of 2021 had created a feeding frenzy for robotics companies. The list includes Aurora Innovation, Berkshire Grey, Bright Machines, Memic, Sarcos Robotics, and Vicarious Surgical. But Symbotic stood apart from this cohort in crucial ways. Unlike speculative ventures promising future breakthroughs, Symbotic had real customers, proven technology, and perhaps most importantly, Breakthrough Patent-Protected Technology Developed in Multi-Year Partnerships with World's Leading Retailers Boasts an Industry-leading $5 Billion Contracted Backlog.

The decision to choose the SPAC route reflected both opportunity and necessity. Cohen had already invested hundreds of millions of his own capital into Symbotic. The Walmart partnership demanded massive capital investments to fund system deployments. Traditional venture capital would have required giving up too much control, while a conventional IPO would have taken too long and subjected the company to market volatility during a critical expansion phase.

SoftBank's involvement added credibility and deep pockets. "We are highly impressed by how Rick and the team have built Symbotic into the remarkable, growing business and industry leader it is today," said Yanni Pipilis, chairman and CEO of SVF Investment Corp. 3 and managing partner for SBIA. The Japanese conglomerate's Vision Fund had become synonymous with massive bets on transformative technologies, having invested more than $175 billion in companies ranging from Uber to WeWork.

Cohen's perspective on the transaction was characteristically pragmatic: "Now is the time to take Symbotic to the next level. SoftBank has tremendous experience investing in leading-edge artificial intelligence and robotics innovators, and our partnership with them will provide us with new insights, relationships and capital that will help us realize our full potential."

The deal structure revealed sophisticated financial engineering. The transaction is expected to deliver up to $725 million of primary gross proceeds, consisting of $320 million of cash in trust from SVFC, assuming no public shareholders of SVFC exercise their redemption rights, a $205 million common equity PIPE at a $10.00 per share entry price, including a $150 million PIPE participation from Walmart, and a $200 million forward purchase of common equity at $10.00 per share by an affiliate of SoftBank Vision Fund 2.

The ownership structure post-transaction told a story of concentrated control. At closing, assuming no public shareholders of SVFC exercise their redemption rights, existing Symbotic equity holders are expected to own 88% of the combined business, with Mr. Cohen retaining 76% ownership, Walmart retaining 9% and other holders retaining 3%. Cohen would maintain iron-fisted control even as a public company—unusual for a business of this scale but consistent with his hands-on management style.

Symbotic made its debut on the NASDAQ today under ticker symbol "SYM" after completing its business combination with SVF Investment Corp. 3. In 2022, Symbotic became a public company (Nasdaq: SYM), marking the transformation from a private automation vendor to a publicly-traded technology platform company.

The timing proved both fortunate and challenging. Symbotic went public just as the SPAC bubble was beginning to deflate. Many of the robotics companies that had gone public via SPAC in 2021 would see their valuations collapse by 80-90% within a year. The market was beginning to differentiate between companies with real businesses and those with just compelling PowerPoint presentations.

For Symbotic, the public listing represented both an ending and a beginning. The company had achieved Cohen's initial vision of creating a fully automated warehouse system. It had validated the technology with the world's largest retailer. It had secured the capital needed for expansion. But now came the harder challenge: proving to public market investors that a hardware-intensive robotics business could generate software-like returns while managing the complexity of scaling from dozens to hundreds of deployments.

VII. Scaling Operations & Customer Expansion (2022–Present)

The transition from private to public company coincided with Symbotic's most aggressive expansion phase. Symbotic said it has an order backlog of more than $5 billion. Its systems currently service 1,400-plus stores in 16 states and 8 Canadian provinces—numbers that would soon balloon as the company raced to fulfill its commitments to Walmart while simultaneously pursuing new customers. The GreenBox joint venture with SoftBank, announced in July 2023, represented both strategic brilliance and operational complexity. SoftBank Group Corp. and Symbotic Inc. announced the establishment of GreenBox Systems LLC, a new joint venture to address the more than $500 billion annual warehouse-as-a-service market opportunity. Concurrently, Symbotic also announced an approximately $7.5 billion new customer contract with GreenBox. The seemingly matryoshka-doll nature of the deal—where Symbotic's joint venture became its own customer—raised eyebrows among investors and analysts.

The structure was ingenious in its complexity. SoftBank and Symbotic own 65% and 35% of GreenBox, respectively. GreenBox would purchase $7.5 billion worth of Symbotic systems over six years, generating recurring revenue for Symbotic while allowing SoftBank to offer warehouse-as-a-service to companies that couldn't afford the capital expenditure of full automation. It was financial engineering meets operational innovation.

"GreenBox enables Symbotic to bring the benefits of our technology to a broader customer universe, expanding our market opportunity," Cohen explained. But the real genius was deeper: by creating a captive customer, Symbotic could guarantee revenue growth while testing new business models without risking relationships with core customers like Walmart. Yet beneath the surface of ambitious expansion plans lay a fundamental challenge: customer concentration. Symbotic has been unable to attract much meaningful business outside of its principal customer, Walmart, which was responsible for more than 85% of Symbotic's revenue in each of the last two years. In fiscal 2023, ended in late September, Walmart accounted for 88% of its total revenue. This dependency created a sword of Damocles hanging over the company's valuation.

The operational challenges of scaling became increasingly apparent through 2023 and 2024. With the industry's largest contracted order backlog of over $5 billion, the Company already operates systems that service over 1,400 stores in 16 states and 8 Canadian provinces. But deploying systems faster than the company had ever done before exposed weaknesses in project management and execution.

Each new deployment presented unique challenges. Unlike software that could be replicated infinitely at near-zero marginal cost, every Symbotic system required physical construction, robot assembly, software customization, and months of on-site optimization. Construction delays, supply chain disruptions, and the sheer complexity of coordinating hundreds of robots in live warehouse environments created bottlenecks that impacted margins.

The company's customers expanded to include C&S Wholesale Grocers, Albertsons, Giant Tiger, Target, and Walmart, but the revenue concentration remained stark. The GreenBox joint venture, while innovative in structure, essentially created another vehicle for Symbotic to sell to itself and SoftBank rather than diversifying the true customer base.

Deployment execution became the critical constraint on growth. "Our system gross margin fell below expectations due to elongated construction schedules and implementation costs," Cohen acknowledged in a 2024 earnings call. "We are focused on improving our planning, speed of implementation and project management to improve performance." The admission revealed the fundamental tension in the business model: the faster Symbotic tried to grow, the more stress it placed on an organization that had spent 15 years perfecting technology but only a few years learning how to deploy it at scale.

The software side of the business provided some relief. The software is used by 1,400 stores, with customers in the grocery, retail and wholesale industries. Once a system was operational, the recurring software, parts, and services revenue provided predictable cash flow with higher margins than the initial system deployment. Symbotic expects in excess of $500 million in annual recurring software, parts and services revenue from GreenBox once all systems are operational.

But the stock market's patience began wearing thin. Since Symbotic's share price hit its all-time peak in July 2023, it has been on the decline. The combination of customer concentration risk, execution challenges, and the broader tech stock correction created a perfect storm for valuation compression.

The company continued to innovate, developing new robot capabilities and expanding the platform's functionality. "During the quarter, we extended the future capabilities of SymBot by incorporating an enhanced sensor array and we advanced development of our new minibot for BreakPack," Cohen noted. But innovation couldn't mask the fundamental challenge: proving that Symbotic could be more than Walmart's automation vendor.

By late 2024, the narrative had shifted from pure growth to operational excellence. The company needed to demonstrate it could execute on its massive backlog profitably while simultaneously diversifying its customer base. The challenge was existential: without new major customers, Symbotic remained vulnerable to Walmart's whims; but taking on too many new customers too quickly risked operational meltdown.

VIII. Financial Performance & Growth Trajectory

The numbers tell a story of explosive growth colliding with the harsh realities of scaling a hardware business. For the full fiscal year 2024, Symbotic reported revenue of $1,822 million, reflecting 55% growth year over year. This represented a remarkable acceleration from a company that had been essentially pre-revenue just five years earlier. But the headline growth masked underlying complexities that would challenge investor confidence. The path to profitability proved more elusive than the growth trajectory suggested. Despite the impressive top-line growth, the company reported a net loss of $51 million for fiscal 2024. The losses weren't unexpected for a capital-intensive business in expansion mode, but they highlighted the fundamental challenge: building and deploying complex robotic systems required massive upfront investments before recurring software revenue could offset the costs.

Symbotic posted revenue of $577 million, net income of $28 million and adjusted EBITDA of $55 million for the fourth quarter of fiscal 2024. The quarterly profit represented a milestone—proof that the business model could generate positive earnings at scale. In the same quarter of fiscal 2023, Symbotic had revenue of $392 million, a net loss of $45 million and adjusted EBITDA of $13 million. The year-over-year improvement was dramatic, but sustainability remained the question.

The margin structure revealed both the promise and the peril of the business model. System deployments generated gross margins in the 10-15% range—respectable for hardware but far below software industry standards. However, once systems became operational, software and services revenue carried margins exceeding 65%. The challenge was managing the mix: too many new deployments crushed margins; too few stunted growth.

By Q2 fiscal 2025, the narrative had evolved further. Symbotic posted revenue of $550 million, marking a 40% year-over-year increase from $393 million. While posting a net loss of $21 million, this represents a substantial improvement from the $55 million loss in Q2 FY2024. The company was demonstrating operational leverage—growing revenue faster than expenses, a critical milestone for investor confidence.

The accounting restatement issues that emerged in late 2024 added complexity to the financial picture. As Symbotic was reviewing its business processes and preparing its full year financial statements, the company identified occurrences during fiscal year 2024 where goods and services were improperly recognized, resulting in the acceleration of revenue recognition. The company estimates the total impact of correcting these errors will be to lower system revenue, system gross profit, income (loss) before income tax, and adjusted EBITDA by $30 million to $40 million for fiscal year 2024.

These accounting issues, while not suggesting fraud, revealed the complexity of percentage-of-completion accounting for multi-year system deployments. Management has identified in its preliminary assessment of internal control over financial reporting for the fiscal year ended September 28, 2024 certain material weaknesses. The revelation undermined confidence just as the company was trying to establish credibility with public market investors.

The unit economics told a compelling story if one could look past the near-term volatility. A typical Symbotic system deployment cost $50-75 million and took 18-24 months to complete. Once operational, it generated $2-3 million in annual recurring software and services revenue at 65%+ margins. The payback period for Symbotic was attractive—systems became cash flow positive within 3-4 years of completion. For customers, the ROI was even more compelling, with labor savings alone justifying the investment within 2-3 years. The business model evolution continued to unfold through 2025. Backlog: $22.7 billion, up from $22.4 billion last quarter. This massive contracted revenue provided visibility years into the future—unusual for a technology company and crucial for investor confidence. The backlog represented nearly 11 times the revenue the firm generated over the past 12 months, providing a cushion against execution risks.

But the market remained skeptical. The stock's volatility reflected fundamental questions about the business model. Could a company dependent on one customer for the majority of its revenue sustain premium valuations? Could hardware-intensive operations ever generate the margins investors expected from technology companies? Would execution challenges derail growth before the company achieved scale?

The financial trajectory told a story of a company in transition—from startup to scale-up, from technology developer to operational executor, from private company to public market participant. The numbers were impressive: revenue growing 40%+ annually, a backlog worth more than a decade of current revenue, improving operational metrics. But beneath the surface lay the fundamental tension that would define Symbotic's future: the race between growing fast enough to justify its valuation while maintaining the operational excellence required to deliver on its promises.

IX. Playbook: Business & Investing Lessons

The Symbotic story offers a masterclass in building a platform business in the most unlikely of sectors: industrial robotics. Unlike software platforms that scale through network effects and zero marginal costs, Symbotic had to create a platform in the physical world, where every deployment required millions in capital and months of construction.

Building a platform business in hardware/robotics requires a fundamentally different approach than software. Cohen understood this intuitively. Rather than seeking rapid, venture-funded growth, he spent 15 years and $700 million of patient capital perfecting the technology before scaling. The platform wasn't just the robots or the software—it was the entire system architecture, the deployment methodology, the service infrastructure. Every component had to work together seamlessly because, unlike software bugs that could be patched overnight, hardware failures in a distribution center processing millions of cases could cripple a customer's operations.

The power of having an anchor customer (first C&S, then Walmart) cannot be overstated. C&S provided the laboratory; Walmart provided the validation. Without C&S, Symbotic would have been another robotics startup pitching unproven technology to skeptical customers. Without Walmart, it would have remained a niche player. The anchor customer strategy provided not just revenue but credibility, feedback, and most importantly, patience during the long development cycle. But it also created dependency—a double-edged sword that would define both the company's success and its primary risk.

Capital intensity vs. software margins: Finding the balance emerged as the central challenge. The business required massive upfront investments—each system deployment cost $50-75 million—but promised software-like recurring revenues once operational. This hybrid model confused investors accustomed to pure-play categories. The solution wasn't to choose one model over the other but to manage the mix carefully. Too much emphasis on new deployments crushed margins; too little stunted growth. The GreenBox joint venture represented an attempt to solve this dilemma by having someone else fund the capital expenditure while Symbotic captured the technology value.

Network effects in warehouse automation manifested differently than in consumer platforms. Each successful deployment didn't directly make the next one more valuable to customers, but it did create indirect network effects. More deployments meant more data to improve the AI, more credibility with potential customers, more resources to invest in R&D. The real network effect came from standardization—as more warehouses adopted Symbotic's architecture, suppliers and customers adapted their processes to interface with it, creating switching costs and competitive moats.

The challenge of customer concentration loomed over every strategic decision. With Walmart representing 85%+ of revenue, Symbotic was less an independent company than a captive technology provider. The attempts to diversify—Target, Albertsons, GreenBox—hadn't materially changed this dynamic. The lesson: customer concentration might be necessary in the early stages of a B2B platform, but it becomes a liability at scale. The market values optionality, and concentration reduces it.

When to go from internal tool to external product represents one of the most difficult transitions in technology. Too early, and the product isn't ready for the complexity of external customers. Too late, and competitors have captured the market. Symbotic's timing—waiting until 2014 for the first external customer after seven years of internal development—seemed excessively patient by Silicon Valley standards. But for mission-critical infrastructure, this patience proved essential. The product had to work perfectly before risking a customer's entire supply chain on it.

Risk management in complex system deployments emerged as perhaps the most underappreciated aspect of the business. Each deployment represented a potential catastrophic failure point—not just financially but reputationally. Symbotic's approach emphasized redundancy at every level: multiple robots for every task, modular components for easy replacement, gradual rollouts to minimize disruption. This belt-and-suspenders approach increased costs but reduced the tail risk that could destroy the company.

The investment lessons are equally profound. Traditional valuation metrics struggle with businesses like Symbotic that combine elements of hardware, software, and services. The market's wild swings in valuation—from under $10 billion to over $40 billion and back—reflected this confusion. Investors applying software multiples during euphoric periods got burned; those applying industrial multiples during pessimistic periods missed the opportunity.

The key insight for investors: focus on unit economics rather than aggregate metrics. What matters isn't the current margin but the margin trajectory as the mix shifts from deployment to operations. What matters isn't current revenue but the quality and durability of the backlog. What matters isn't the technology alone but the switching costs and competitive moats it creates.

The Symbotic playbook ultimately teaches that building transformative businesses in physical industries requires different rules than digital disruption. It requires patient capital, anchor customers, and the willingness to accept lower margins during the scaling phase. It requires managing the tension between growth and profitability more carefully than pure software businesses. And it requires understanding that the biggest opportunities might lie not in creating entirely new markets but in fundamentally reimagining existing ones.

X. Analysis & Bear vs. Bull Case

Bull Case:

The optimistic view of Symbotic rests on a simple premise: the company sits at the intersection of multiple irreversible trends that virtually guarantee long-term success. Symbotic is at the forefront of a $350 billion addressable market opportunity to reshape the global supply chain—a market that's not just large but also desperately in need of modernization.

The labor shortage crisis in warehousing isn't temporary—it's structural. With unemployment near historic lows and warehouse work ranking among the most physically demanding and injury-prone occupations, the industry faces a permanent labor supply problem. Symbotic doesn't just offer automation; it offers a solution to an existential crisis. The math is compelling: warehouse workers cost $50,000+ annually including benefits and workers' compensation, turnover exceeds 100% in many facilities, and the available workforce continues to shrink. Against this backdrop, Symbotic's robots, which work 24/7 without breaks, injuries, or turnover, become not just attractive but essential.

The technology moat appears insurmountable. With over 650 patents, $1 billion+ invested in R&D, and 15+ years of development, Symbotic has created barriers to entry that would take competitors a decade and similar capital to replicate. But the real moat isn't the technology—it's the installed base. Each operational system creates switching costs measured in tens of millions of dollars and years of disruption. Once a customer commits to Symbotic's architecture, they're essentially locked in for the 20+ year life of the facility.

Strong revenue growth and improving margins tell a story of a business hitting its inflection point. Revenue growing 40%+ annually, gross margins expanding as the mix shifts toward software and services, and a clear path to 30%+ EBITDA margins at maturity. The backlog of $22.4 billion provides unprecedented visibility—the company could sign zero new customers and still grow for years.

The Walmart relationship, rather than being a weakness, represents a competitive advantage that's impossible to replicate. Walmart's commitment to deploy Symbotic across all 42 regional distribution centers isn't just a customer contract—it's a strategic partnership that validates the technology and provides a massive reference customer for other retailers. The recent expansion into micro-fulfillment with the acquisition of Walmart's Advanced Systems and Robotics business opens an entirely new $300 billion market opportunity.

Secular tailwinds—labor shortage, e-commerce growth, same-day delivery expectations, SKU proliferation—all accelerate the need for automation. These aren't cyclical trends that might reverse; they're fundamental shifts in how commerce operates. Every quarter that passes without automation puts retailers further behind Amazon, creating urgency that drives purchasing decisions.

Bear Case:

The skeptical view starts with an uncomfortable truth: Symbotic is essentially a single-customer company masquerading as a platform business. Customer concentration risk (Walmart dependency) isn't just high—it's existential. If Walmart decided to slow deployments, renegotiate terms, or develop internal alternatives, Symbotic's revenue would collapse overnight. The fact that this hasn't happened yet doesn't mean it won't—Walmart has a long history of squeezing suppliers once they become dependent.

Competition from established players and new entrants intensifies daily. Amazon continues to advance its internal robotics capabilities and could enter the third-party market at any time. AutoStore, despite its limitations, has captured significant market share in e-commerce fulfillment. Chinese competitors, backed by government subsidies and lower cost structures, are beginning to enter Western markets. The competitive landscape in 2025 looks nothing like the open field Symbotic enjoyed in 2015.

Execution challenges at scale have already manifested and will likely worsen. Each deployment is essentially a custom construction project with unique challenges. As the company tries to accelerate from 5-10 annual deployments to 20-30, the complexity increases exponentially. The accounting restatements revealed control weaknesses that suggest the company is struggling to manage its current scale, let alone future growth.

Capital intensity of the business model creates a fundamental tension with profitability. Even at scale, Symbotic requires massive ongoing capital investments in R&D, deployment infrastructure, and working capital. Unlike software businesses that can generate 90%+ incremental margins on new revenue, Symbotic must invest heavily for each dollar of growth. The promised software-like margins may never materialize if the company must continuously invest in next-generation technology to stay competitive.

Accounting and control issues, while not suggesting fraud, reveal a company that grew faster than its internal systems could support. Material weaknesses in internal controls, revenue recognition errors, and the need for restatements undermine confidence. These issues often prove to be symptoms of deeper organizational challenges that take years to resolve.

The valuation remains stretched even after recent corrections. At current levels, Symbotic trades at multiples that assume flawless execution, continued rapid growth, and margin expansion—a trifecta that few companies achieve. Any disappointment in quarterly results triggers violent selloffs, suggesting the market has little patience for setbacks.

The Verdict:

The truth likely lies between these extremes. Symbotic has built genuinely transformative technology that addresses real market needs. The warehouse automation market will grow dramatically over the next decade, and Symbotic is well-positioned to capture significant share. The backlog provides unusual visibility and stability for a technology company.

However, the risks are equally real. Customer concentration remains dangerous, competition is intensifying, and execution challenges could derail growth. The company must simultaneously manage rapid scaling, technology innovation, and market expansion—a juggling act that has defeated many promising companies.

For investors, Symbotic represents a high-conviction bet on warehouse automation with asymmetric risk/reward. Bulls who believe in the secular trends and Symbotic's competitive position could see multiple-bagger returns if execution succeeds. Bears who focus on the risks and challenges see significant downside from current levels.

The key variables to watch: customer diversification progress, margin trajectory as mix shifts, execution metrics on deployment speed and quality, competitive dynamics especially from Amazon and Chinese entrants, and most critically, any changes in the Walmart relationship. These factors will determine whether Symbotic becomes the defining platform for warehouse automation or another promising technology company that couldn't scale beyond its anchor customer.

XI. Epilogue & Future Outlook

The future of warehouse automation isn't a question of if but when and how. Every major retailer, distributor, and logistics provider understands that automation is inevitable. The economics are too compelling, the labor challenges too acute, and the competitive pressure from Amazon too intense to maintain status quo operations. In this context, Symbotic's opportunity extends far beyond its current contracts.

The company's technology roadmap reveals ambitious plans that could fundamentally expand its addressable market. The development of systems for cold chain and frozen goods opens the $100+ billion grocery distribution market that has largely resisted automation due to technical challenges. The minibot for break-pack operations addresses the small-item picking that currently requires human workers. Each innovation doesn't just add revenue opportunity—it makes the platform more comprehensive and harder to displace.

Expansion opportunities in new verticals and international markets remain largely untapped. Symbotic has focused almost exclusively on U.S. retail distribution, but the same challenges exist in pharmaceuticals, automotive parts, industrial supplies, and dozens of other verticals. Internationally, Europe and Asia face similar labor shortages and efficiency pressures. The company that wins the U.S. market has a platform to expand globally.

The integration of AI advances promises to accelerate capability development. Large language models could revolutionize how warehouses handle exceptions and interface with other systems. Computer vision improvements could enable handling of previously impossible SKUs. Reinforcement learning could optimize system performance in ways human programmers never imagined. Symbotic's massive installed base provides the data advantage to train these AI systems better than competitors.

What success looks like in 5-10 years: Symbotic becomes the de facto operating system for global supply chains. Just as Windows dominated PCs or iOS dominates premium smartphones, Symbotic's platform becomes the standard that suppliers, retailers, and logistics providers build around. The company evolves from selling systems to selling outcomes—guaranteed fulfillment rates, cost per case handled, inventory optimization as a service.

In this future, the business model transforms. Instead of lumpy system sales, Symbotic generates predictable subscription revenues. Instead of customer concentration, it has hundreds of clients across multiple industries and geographies. Instead of competing on technology features, it leverages network effects and switching costs. The company that started as Rick Cohen's solution to his grandfather's business problems becomes the backbone of global commerce.

But alternative futures are equally plausible. Amazon could open its robotics platform to third parties, instantly becoming the dominant player. Chinese competitors could undercut Symbotic's pricing while offering "good enough" technology. The next recession could freeze capital spending on automation for years. Walmart could acquire Symbotic outright, capturing all the value for itself while limiting the company's broader market opportunity.

The most likely scenario falls between these extremes. Symbotic continues growing rapidly but faces increasing competition. It successfully diversifies beyond Walmart but never fully escapes customer concentration. It achieves attractive margins but not the software-like economics bulls expect. The company becomes a successful, profitable leader in warehouse automation but not the dominant platform that reshapes global supply chains.

For Rick Cohen, now in his seventies, the journey from grocery wholesaler to robotics pioneer represents an American business epic. Whether Symbotic achieves its ultimate vision or settles for more modest success, Cohen has already accomplished something remarkable: proving that patient capital, deep domain expertise, and relentless focus can disrupt even the most entrenched industries.

The final chapter of the Symbotic story remains unwritten. The company stands at an inflection point where the decisions made in the next 2-3 years will determine whether it becomes a transformative platform or a successful but limited automation vendor. The technology works, the market opportunity is massive, and the competitive position is strong. What remains to be proven is whether Symbotic can execute on its vision while navigating the treacherous transition from startup to scale.

For investors, customers, and competitors, Symbotic represents a bellwether for the broader automation revolution. If Symbotic succeeds in transforming warehouse operations, it validates the thesis that robotics and AI can revolutionize traditional industries. If it struggles, it suggests that the physical world's complexity still resists digital disruption. Either way, the attempt itself—to rebuild global supply chains from first principles—represents one of the most ambitious business undertakings of our time.

The warehouse of the future won't look like today's human-centric distribution centers any more than today's factories resemble their pre-automation predecessors. In that transformed landscape, Symbotic aims to be not just a participant but the architect. Whether it achieves that ambition will define not just one company's trajectory but the future of how goods move through the global economy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube