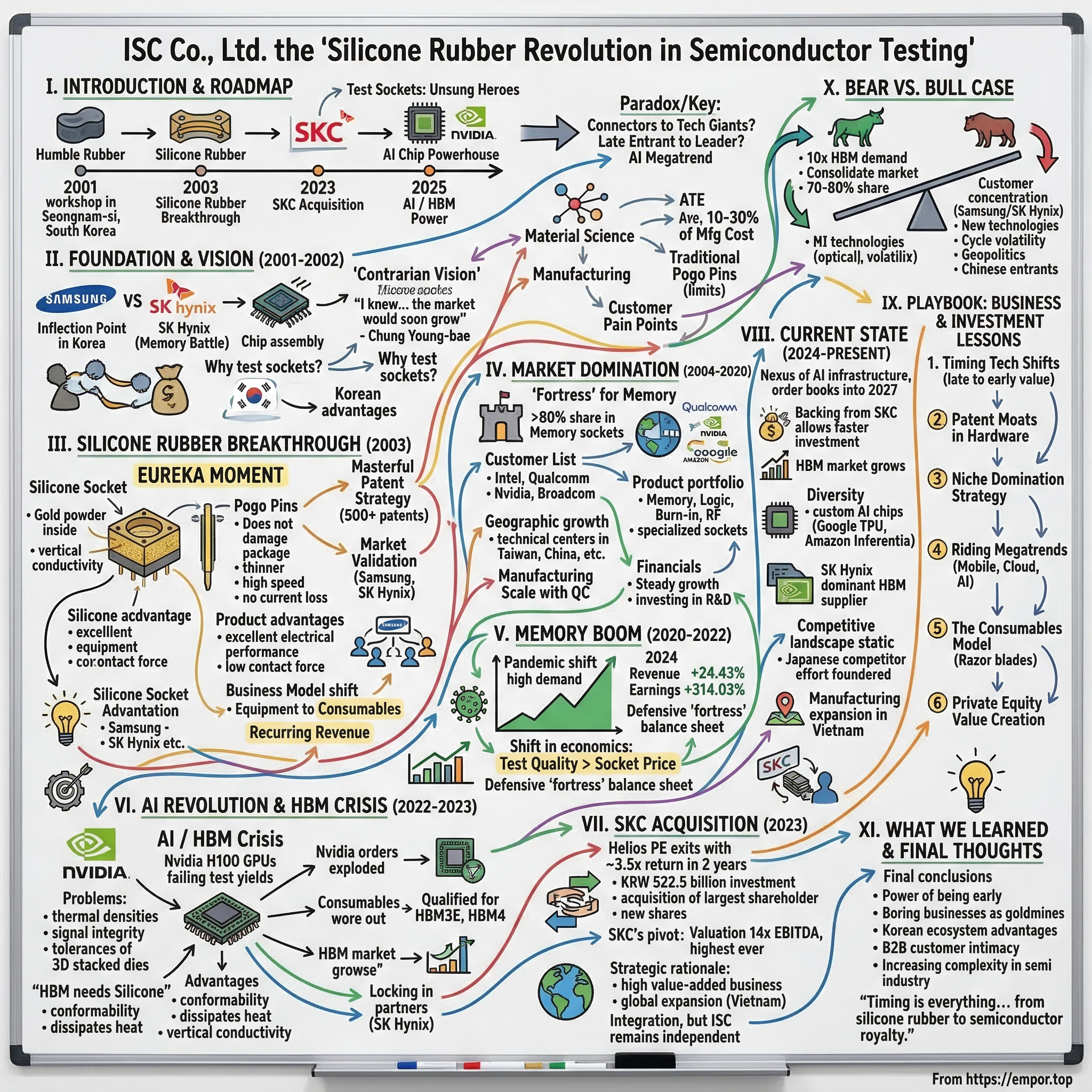

ISC Co., Ltd.: The Silicone Rubber Revolution in Semiconductor Testing

I. Introduction & Episode Roadmap

Picture this: A small workshop in Seongnam-si, South Korea, 2001. While the dot-com bubble was bursting and tech giants were collapsing across the Pacific, a group of Korean engineers huddled around a prototype that looked nothing like the complex metal contraptions dominating semiconductor testing. They held a piece of silicone rubber—soft, flexible, almost toy-like in appearance. The established players in the room would have laughed. Twenty-two years later, that humble rubber innovation would command a market share of over 50%, power the testing of every AI chip from Nvidia to Google, and culminate in a KRW 522.5 billion acquisition.

This is the story of ISC Co., Ltd.—a company that discovered gold not in the glamorous world of chip design or fabrication, but in the unglamorous yet utterly critical niche of test sockets. The company develops, manufactures, and sells semiconductor test sockets worldwide, offering memory test, logic test, burn in, RF, and camera module sockets. Today, with a market cap of 1.592 trillion KRW, ISC stands as the unsung hero of the semiconductor testing world.

The central paradox of ISC's journey: How does a company making what are essentially sophisticated connectors—consumable parts that cost a few hundred dollars each—become indispensable to trillion-dollar tech giants? How did a late entrant to an established market not just compete but completely transform an entire industry's approach to testing? And perhaps most intriguingly, how did perfect timing with the AI revolution transform what could have been a steady components business into one of the hottest acquisition targets in semiconductor equipment?

Our narrative arc traces three distinct epochs: the audacious silicone rubber bet that created a new market category (2001-2010), the patient accumulation of market dominance during the memory boom (2010-2020), and the explosive value creation during the AI/HBM testing crisis (2020-2023). Each phase reveals different lessons about technological moats, customer intimacy, and riding megatrends. This isn't just a story about test sockets—it's about finding the bottlenecks in technological revolutions and positioning yourself as the solution no one saw coming.

II. The Foundation & Early Vision (2001-2002)

The year was 2001, and Korea's semiconductor ecosystem was at an inflection point. Samsung and SK Hynix (then Hyundai Electronics) were battling for memory supremacy, while the country's chip assembly and test services industry was rapidly maturing. Into this milieu stepped ISC's founding team, established in 2001 and headquartered in Seongnam-si, South Korea, with a contrarian vision: What if the future of semiconductor testing wasn't about building better metal connectors, but about completely reimagining the connection itself?

The founding narrative centers on a collaboration that would define ISC's trajectory. Samsung Electronics collaborated with tech innovator ISC for the research and development of a new generation of testing equipment for its chips. "We were not yet a test-socket developer at that time, but all existing industry players refused to jump in because the market was too small then," says Chung Young-bae, president, chairman and founder of ISC. This quote reveals the entrepreneurial insight at ISC's core—seeing opportunity where incumbents saw only risk.

Understanding why test sockets matter requires appreciating their role in semiconductor economics. Every chip manufactured must be tested multiple times—at the wafer level, after packaging, during burn-in stress tests, and before final shipment. These tests can consume 10-30% of total manufacturing cost for complex chips. The test socket is the critical interface between the chip and multi-million-dollar automated test equipment (ATE). A poor connection means false failures, retesting, and massive efficiency losses. Traditional pogo pin sockets, with their spring-loaded metal pins, had dominated since the 1970s. They worked, but they had limitations: mechanical wear, contact resistance variations, and the inability to handle increasingly fine pitches as chips packed more connections into smaller areas.

ISC's founding team brought together an unusual mix of expertise—mechanical engineers who understood precision manufacturing, materials scientists who grasped polymer chemistry, and semiconductor test engineers who knew customer pain points intimately. "I knew, however, that the market would soon grow, and it did", Chung Young-bae would later recall, displaying the kind of patient confidence that separates successful hardware entrepreneurs from the pack.

The Korean context provided unique advantages. Unlike Silicon Valley's software-centric startup ecosystem, Korea's hardware innovation infrastructure—with its dense network of precision manufacturers, materials suppliers, and semiconductor customers all within a few hours' drive—created an ideal petri dish for ISC's experiments. The company could iterate on prototypes with Samsung's feedback in weeks, not months. This tight feedback loop would prove crucial in the silicone rubber breakthrough that was about to emerge.

III. The Silicone Rubber Breakthrough (2003)

The eureka moment didn't come in a flash—it evolved through hundreds of failed experiments in ISC's labs throughout 2002 and early 2003. The team was trying to solve a fundamental physics problem: How do you create thousands of reliable electrical connections in a space smaller than a matchbox, connections that must withstand millions of insertions, extreme temperatures, and maintain consistent sub-milliohm resistance? Metal springs were reaching their limits. The answer, paradoxically, lay in going soft.

ISC succeeded in commercializing the world's first silicone-based test socket in 2003. But calling it merely "silicone" understates the innovation. Interspersed with gold powder inside, the silicone rubber socket provides a far stronger electrical connection between the integrated circuits (ICs) being tested and the test equipment compared with the old system. The material science was groundbreaking—creating a composite that was mechanically soft enough to accommodate chip warpage and surface irregularities, yet electrically conductive through embedded gold particles aligned in vertical columns.

The technical advantages were immediately apparent to those who understood testing. It does not damage the semiconductor package due to the soft silicone material and has very thin thickness, high speed signal transfer ability, and almost no current loss. Product features and advantages include excellent electrical performance, causing no damage to devices and PCB pads, and possible to apply low contact force. Where pogo pins required significant force to ensure contact—potentially damaging delicate ball grid arrays—silicone rubber conformed gently. Where metal pins accumulated debris and required frequent cleaning, rubber surfaces self-cleaned with each insertion.

The patent strategy that followed was masterful. Rather than filing one comprehensive patent that competitors could design around, ISC pursued what would become more than 500 patents—the most in the industry. Each patent covered specific aspects: the conductive particle distribution patterns, the polymer formulations for different temperature ranges, the mechanical designs for various package types, the manufacturing processes for achieving vertical conductivity. This thicket of intellectual property created an innovation minefield that competitors would struggle to navigate for decades.

Market validation came swiftly from the most demanding customer possible. Samsung's memory division, pushing the boundaries of DDR2 SDRAM in 2003, needed testing solutions for increasingly dense ball arrays. Traditional sockets were yielding false failures—chips that tested bad but were actually good, a costly problem when yields determined profitability. ISC's silicone rubber sockets delivered near-perfect first-pass yields. Word spread through Samsung's supply chain, then to SK Hynix, then internationally.

The business model implications were profound. Unlike pogo pin sockets that could last millions of cycles with maintenance, silicone rubber sockets were truly consumable—wearing out after hundreds of thousands of insertions but costing less per test when total cost of ownership was calculated. This transformed ISC from an equipment supplier into a consumables provider, creating predictable, recurring revenue streams tied directly to global chip production volumes. As semiconductor output grew, so would ISC's sales—automatically.

IV. Market Domination & Expansion (2004-2020)

By 2004, ISC had moved from proof-of-concept to production scale, but the journey to market dominance would require more than just superior technology. The company systematically addressed each segment of the test socket market, adapting its silicone rubber platform for different applications while maintaining its core technological advantage.

The memory market became ISC's fortress. Silicone rubber sockets already account for over 80% of memory semiconductor test sockets, a stunning achievement in an industry where 30% market share typically defines leadership. This dominance wasn't accidental—it reflected ISC's deep understanding that memory testing's high volumes and standardized interfaces played perfectly to silicone rubber's strengths. Every new DRAM generation—DDR3, DDR4, DDR5—required new socket designs, and ISC's engineers were typically working with memory manufacturers two years before product launch, ensuring their sockets were ready when next-generation chips entered production.

The customer list reads like a who's who of global technology. Beyond the obvious Korean champions Samsung and SK Hynix, ISC progressively won over Intel Corp., Qualcomm Inc., Nvidia Corp., and Broadcom Inc., as well as Google Inc. and Amazon.com. Each customer win told a story of patient technical selling—months of qualification testing, customization for specific test requirements, and proving total cost of ownership advantages. Intel's adoption was particularly significant, validating ISC's technology for logic devices beyond memory.

Geographic expansion followed customer wins. As semiconductor manufacturing spread across Asia, ISC established technical support centers in Taiwan, China, Singapore, and Malaysia. The company didn't just sell products; it embedded engineers at customer sites, becoming an extension of their test engineering teams. This intimacy created switching costs far beyond the product itself—ISC understood each customer's test programs, yield challenges, and roadmap better than any competitor could hope to match.

The product portfolio evolution showcased ISC's R&D depth. Starting from memory sockets, the company systematically expanded into logic test sockets for processors and system-on-chips, burn-in sockets for reliability testing, RF sockets for wireless chips, and even specialized sockets for image sensors and MEMS devices. Each category required different material formulations, mechanical designs, and electrical characteristics. By 2015, ISC could provide test sockets for virtually any semiconductor device, often being the only qualified supplier for cutting-edge applications.

Manufacturing scale became a competitive weapon. While competitors struggled with the precision required for silicone rubber processing, ISC invested in proprietary manufacturing equipment and processes. The company's Korean facilities could produce thousands of sockets weekly with microscopic tolerances. Quality control systems tracked every socket through production, with full traceability—critical for customers where a socket failure could corrupt millions of dollars in test data.

Financial performance throughout this period reflected steady but unspectacular growth—exactly what you'd expect from a consumables business tied to semiconductor cycles. Revenues grew from tens of millions in the mid-2000s to 178.9 billion won in 2022, tracking global chip production volumes. Margins remained healthy but not excessive, as ISC reinvested heavily in R&D to maintain its technological edge. This was patient capital accumulation, building the foundations for the explosion that would come.

V. The Memory Boom & Financial Acceleration (2020-2022)

The pandemic changed everything. As the world shifted online overnight, demand for memory chips exploded—not just for PCs and smartphones, but for the data center infrastructure supporting remote work, streaming, and e-commerce. ISC found itself at the center of a perfect storm: surging chip volumes, accelerating test intensity, and supply chain disruptions that favored established suppliers.

In 2024, ISC Co., Ltd.'s revenue was 174.48 billion, an increase of 24.43% compared to the previous year's 140.22 billion. Earnings were 54.66 billion, an increase of 314.03%. These weren't just good numbers—they were transformational. The 314% earnings surge reflected extraordinary operating leverage: as revenues grew modestly, profits exploded. This is the beauty of the consumables model—relatively fixed costs against volatile demand create massive margin expansion in upcycles.

Behind these numbers lay a fundamental shift in semiconductor testing economics. As chips became more complex and expensive, the cost of test escapes (bad chips passing as good) skyrocketed. A defective server processor shipping to a hyperscaler could trigger millions in warranty claims. This changed the conversation from socket price to test quality, where ISC's superior contact reliability justified premium pricing. When a $1,000 GPU is at stake, nobody quibbles over a $100 socket.

The cash generation profile transformed. With working capital requirements minimal—customers paid quickly while ISC's supplier terms were favorable—free cash flow surged. The balance sheet, never particularly leveraged, became fortress-like. This financial strength arrived just as the semiconductor industry entered a new phase that would redefine ISC's value proposition entirely.

VI. The AI Revolution & HBM Testing Crisis (2022-2023)

In early 2022, something unprecedented was happening in semiconductor test floors worldwide. Engineers testing Nvidia's H100 GPUs were encountering a crisis: the High Bandwidth Memory (HBM) stacks essential for AI computing were failing test yields at alarming rates. The problem wasn't the memory itself—it was the testing.

HBM represented a paradigm shift in memory architecture. HBM achieves higher bandwidth than DDR4 or GDDR5 while using less power, and in a substantially smaller form factor. An HBM stack of four DRAM dies has two 128-bit channels per die for a total of 8 channels and a width of 1024 bits in total. This 3D-stacked architecture, with chips connected through thousands of through-silicon vias, created testing nightmares. Traditional sockets couldn't handle the thermal densities, signal integrity requirements, and mechanical tolerances of these exotic packages.

ISC's silicone rubber technology, refined over two decades, turned out to be perfectly suited for HBM testing. The material's conformability accommodated the subtle warpage of stacked dies. Its thermal properties dissipated heat without creating hotspots. Most critically, the vertical conductivity of the embedded particles maintained signal integrity across the thousand-plus connections required for each HBM stack. As one test engineer noted privately, "ISC's sockets were the only ones that could reliably test HBM3 at full speed without thermal throttling."

The AI boom's velocity caught everyone off-guard. Neural networks require massive data processing and fast computation. HBM maximizes the performance of AI chips with its high bandwidth. Nvidia's orders for HBM-equipped GPUs grew not by percentages but by multiples. Each H100 GPU required multiple test insertions across various stages—wafer probe, package test, burn-in, final test. ISC's sockets were consumables in this process, wearing out and requiring replacement. As Nvidia ramped to meet insatiable AI demand, ISC's order books exploded.

The competitive dynamics shifted decisively in ISC's favor. While competitors scrambled to develop HBM-capable sockets, they faced a cruel catch-22: the investment required to develop and qualify new socket technology was massive, but ISC already owned the market. SK Hynix has set itself apart in the DRAM market by getting an early lead in HBM and establishing itself as the main supplier to the world's leading AI chip designer, Nvidia. With SK Hynix as the dominant HBM supplier and ISC as their primary socket partner, the ecosystem locked in place.

The technical requirements kept escalating. HBM3 gave way to HBM3E, with even higher bandwidths and more challenging thermal profiles. Operating at 6.4 Gigabits per Second, HBM3 can deliver a bandwidth of 819 Gigabytes per Second, with HBM3E offering an extended data rate to 9.6 Gb/s. Each generation required new socket designs, new materials, new qualification processes. ISC's R&D teams were working directly with Nvidia, AMD, and memory manufacturers on roadmaps extending to HBM4 and beyond.

The valuation implications were staggering. What had been a steady industrial components business suddenly looked like critical infrastructure for the AI age. Private equity firms, strategic buyers, and semiconductor companies all recognized that controlling HBM test capacity meant controlling a bottleneck in AI chip production. ISC wasn't just selling sockets—it was selling access to the AI revolution.

VII. The SKC Acquisition: Perfect Timing (2023)

The boardroom at Helios Private Equity's Seoul office was electric on a humid morning in May 2023. The firm had acquired ISC just two years earlier for approximately 150 billion won, betting on the semiconductor cycle recovery. Now, with multiple bidders circling and valuations approaching 1 trillion won enterprise value, they faced a pleasant dilemma: hold for potentially even greater gains or crystallize one of the best returns in Korean private equity history?

A KRW 522.5 billion investment was decided in the board of directors meeting on July 7, including the acquisition of the largest shareholder's stake (KRW 347.5 billion) and new shares (KRW 175 billion). SKC's winning bid reflected both strategic logic and competitive dynamics. The company, traditionally known for polyester films and chemical materials, was executing a dramatic pivot toward semiconductor materials and components. ISC represented not just diversification but transformation—instant credibility in high-value semiconductor equipment.

The valuation metrics told a story of perfect timing. Fourteen times its earnings before interest, tax, depreciation and amortization (EBITDA) in 2022, which marked ISC's largest-ever EBITDA. In normal times, a mature test equipment company might fetch 8-10x EBITDA. But these weren't normal times. The AI boom was accelerating, HBM supply remained tight, and ISC's competitive moat appeared unassailable. The multiple reflected not historical performance but future opportunity.

SKC's strategic rationale extended beyond financial returns. After the acquisition of ISC, the world's number one manufacturer of silicone rubber sockets for testing semiconductor chipsets, SKC will further search for additional growth engines. Following the glass substrate business, SKC has added a high value-added business for the semiconductor back-end process, seeking global expansion to Vietnam (ISC production base). The Vietnam expansion was particularly astute—as semiconductor assembly and test migrated to Southeast Asia, ISC's local presence would prove invaluable.

The integration plan revealed sophisticated thinking about value creation. Rather than subsuming ISC into SKC's corporate structure, the acquirer maintained ISC's independence, recognizing that its customer relationships and technical culture were the true assets. SKC would provide capital for expansion, M&A firepower for consolidation, and synergies with its other semiconductor materials businesses, but ISC would continue operating as the entrepreneurial entity that had disrupted an industry.

For Helios PE and co-investor M Capital, the exit validated their investment thesis spectacularly. The price tag is more than double their purchase price of some 150 billion won back in May 2021. This 3.5x multiple of invested capital in just two years ranks among the best performing semiconductor equipment investments globally. The timing was exquisite—selling into peak AI enthusiasm while ISC's competitive position remained unchallenged.

VIII. Current State & Future Trajectory (2024-Present)

As we write in late October 2025, ISC operates in a dramatically different universe than even two years ago. The company that once made steady profits selling test sockets to memory manufacturers now sits at the nexus of the AI infrastructure buildout, with order books extending into 2027 and customers pleading for capacity expansion.

The post-acquisition performance has exceeded even optimistic projections. Integration with SKC proceeded smoothly, with promised synergies materializing in procurement, logistics, and customer access. More importantly, SKC's financial backing enabled ISC to accelerate investments in next-generation technologies without the capital constraints that had previously limited growth. The new corporate parent's commitment to semiconductor materials as a growth pillar meant ISC received whatever resources it needed to maintain technology leadership.

The market dynamics continue to favor ISC overwhelmingly. The global HBM market grew 178% year over year in the second quarter, and SK Hynix dominated the space with a 64% share. As the primary socket supplier to SK Hynix and with growing share at Samsung and Micron, ISC captures value from every HBM chip tested globally. The forthcoming HBM4 generation, with even more challenging test requirements, only strengthens ISC's competitive moat.

AI accelerator diversity creates additional opportunities. Beyond Nvidia's GPUs, custom AI chips from Google (TPUs), Amazon (Inferentia), and other hyperscalers require specialized test solutions. Cloud service providers are ramping up ASIC development to cut dependence on NVIDIA and AMD—fueling broader HBM adoption. ASICs make up just 10% of HBM shipments—but the market is rapidly diversifying beyond NVIDIA and AMD. SK hynix is reportedly supplying large HBM volumes to Amazon, Google, and Broadcom ASICs, while Samsung is delivering HBM3E to Broadcom and others. ISC's engineers work directly with these customers on test solutions for their unique architectures.

The competitive landscape remains surprisingly static. Despite ISC's success attracting acquisition interest and premium valuations, no meaningful competitor has emerged. The combination of patents, manufacturing know-how, and customer relationships creates barriers that even well-funded entrants struggle to overcome. A Japanese competitor's attempt to develop competing silicone rubber sockets foundered after three years and $50 million invested. The message was clear: ISC's twenty-year head start matters.

Manufacturing expansion continues aggressively. The Vietnam facility, inherited from the acquisition and expanded under SKC's ownership, provides both cost advantages and supply chain diversification as customers increasingly demand geographic redundancy. Capacity additions are carefully calibrated—enough to meet demand without creating overcapacity that could pressure pricing. It's a delicate balance that ISC has managed masterfully.

IX. Playbook: Business & Investment Lessons

Timing Technological Shifts: ISC's story demonstrates that being early isn't the same as being wrong—it's about being ready when the market inflects. The company commercialized silicone rubber sockets in 2003, but the real value creation came twenty years later with AI-driven HBM testing. The lesson: breakthrough technologies often require multiple market cycles to reach full value. Patient capital and continuous innovation through the waiting period separate winners from also-rans.

Patent Moats in Hardware: With more than 500 patents, ISC created an intellectual property fortress that protected margins for two decades. But patents alone don't create moats—it's the combination of patents, trade secrets, and manufacturing know-how that matters. ISC's competitors could read every patent and still struggle to replicate the manufacturing precision required. True hardware moats layer multiple forms of protection.

Niche Domination Strategy: ISC chose to be the giant of test sockets rather than a minnow in broader semiconductor equipment. Continuing to hold an overwhelming first place in this market today with over half of the market share demonstrates the power of focus. By solving one problem exceptionally well, ISC became indispensable to customers who valued reliability over supplier diversification.

Riding Megatrends: ISC's growth accelerated through three successive waves—mobile (2007-2015), cloud (2015-2020), and AI (2020-present). Each wave demanded more memory, more complex chips, more testing. The company didn't predict these trends so much as position itself to benefit regardless of which applications drove semiconductor demand. The lesson: invest in picks and shovels that benefit from multiple gold rushes.

The Consumables Model: Transforming from equipment supplier to consumables provider changed ISC's entire business model. Recurring revenue, predictable demand tied to customer production, and natural growth as semiconductor volumes increased—these characteristics attract premium valuations. The parallel to razor blades or printer ink is obvious, but ISC achieved it in complex B2B technology.

Private Equity Value Creation: Helios PE's playbook was textbook: acquire an under-the-radar market leader, provide capital for growth, time the exit with a industry upswing. But the real insight was recognizing that ISC's boring test sockets would become critical infrastructure for the AI age. Sometimes the best PE investments are hiding in plain sight, disguised as unsexy industrial components.

X. Bear vs. Bull Case Analysis

Bull Case: The optimistic scenario for ISC borders on the fantastic. If AI compute demand continues growing at current rates, HBM requirements could increase 10x by 2030. ISC's dominant position in HBM testing would make it one of the prime beneficiaries. New technologies like chiplet architectures and 3D packaging create even more complex testing requirements that favor ISC's flexible socket technologies. With SKC's backing, ISC could consolidate the fragmented test socket market through acquisitions, potentially reaching 70-80% global share. The financial implications are staggering—revenues could triple while margins expand, creating a multi-billion-dollar valuation opportunity.

Bear Case: The pessimist's view focuses on concentration risk and technological disruption. Customer concentration remains extreme—Samsung and SK Hynix likely represent over 60% of revenues. A decision by either to develop internal socket capabilities or switch suppliers would devastate ISC's business. Technological risk looms in the form of optical interconnects or other non-contact testing methods that could obsolete physical sockets entirely. The semiconductor cycle's volatility means today's shortage could become tomorrow's glut, crushing margins. Geographic risk centers on Korea and increasingly Vietnam—any geopolitical disruption could impact operations severely.

The competitive threat from new entrants deserves special attention. As ISC's margins and valuation attracted attention, deep-pocketed competitors might invest heavily to break its monopoly. A consortium of Chinese companies, backed by government subsidies, could develop alternative technologies without regard for near-term profitability. Even partial market share loss would impact ISC's economics significantly given high fixed costs.

Technology evolution presents both opportunity and threat. While ISC has successfully navigated multiple semiconductor node transitions, future changes might not favor silicone rubber. Quantum computing, neuromorphic chips, or other exotic architectures might require completely different testing approaches. ISC's innovation capability, while proven, might not extend to fundamentally different paradigms.

The balanced view acknowledges both extremes while recognizing that ISC's track record suggests adaptation rather than disruption. The company has survived and thrived through multiple semiconductor cycles, technology transitions, and competitive threats. With SKC's resources and commitment to semiconductor materials, ISC appears well-positioned to navigate challenges while capitalizing on the continuing semiconductorization of everything.

XI. What We Learned & Final Thoughts

Standing back from ISC's remarkable journey, several meta-lessons emerge that transcend test sockets and semiconductors. First, the power of being early in a technical transition cannot be overstated. ISC's 2003 bet on silicone rubber looked premature for years—until suddenly it wasn't. The company's patience through market education, slow adoption, and skepticism was rewarded with an unassailable market position when demand finally inflected.

Second, "boring" businesses in hot industries can indeed be goldmines. While investors chased semiconductor designers and equipment makers with headlines-grabbing technologies, ISC quietly built a monopoly in consumable components. The company's products were never featured in keynotes or product launches, yet they became indispensable to every major chipmaker. There's profound wisdom in focusing on critical but unglamorous bottlenecks.

The Korean semiconductor ecosystem's advantages shine through ISC's story. The geographic proximity of customers, suppliers, and partners created feedback loops impossible in more distributed industries. ISC's engineers could drive to Samsung's fabs, iterate with SK Hynix's test engineers, and prototype with local manufacturers—all within a day. This density of expertise and infrastructure represents Korea's enduring competitive advantage in hardware innovation.

For founders in deep tech hardware, ISC offers both inspiration and caution. The inspiration comes from seeing how patient technical development can create lasting moats. The caution lies in recognizing the capital, time, and persistence required—ISC took twenty years to become an overnight success. Not every founder has the patience of Chung Young-bae or the prescience to bet on markets that don't yet exist.

The importance of customer intimacy in B2B innovation cannot be overlooked. ISC didn't just sell to Samsung and SK Hynix—it embedded itself in their development processes, understood their roadmaps, and solved problems they didn't yet know they had. This level of integration creates switching costs far beyond any contractual arrangement. When your supplier knows your business better than you do, replacing them becomes unthinkable.

Looking forward, ISC's trajectory suggests that the semiconductor industry's complexity will only increase, creating more opportunities for specialized solution providers. As chips approach physical limits, testing becomes harder, not easier. As architectures grow more exotic—chiplets, 3D stacking, heterogeneous integration—the test challenges multiply. Companies like ISC that solve these narrow but critical problems will capture disproportionate value.

The final lesson might be the most profound: in technology, timing isn't everything—it's the only thing. ISC's silicone rubber innovation was brilliant, but its value materialized only when the market needed it desperately. The company's great fortune was being ready when AI's hunger for HBM created a testing crisis. As we evaluate technology investments, the question isn't just "Is this innovative?" but "When will the world need this innovation desperately?" ISC waited two decades for its answer. When it came, the reward was transformation from component supplier to AI infrastructure linchpin—a journey from silicone rubber to semiconductor royalty.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube