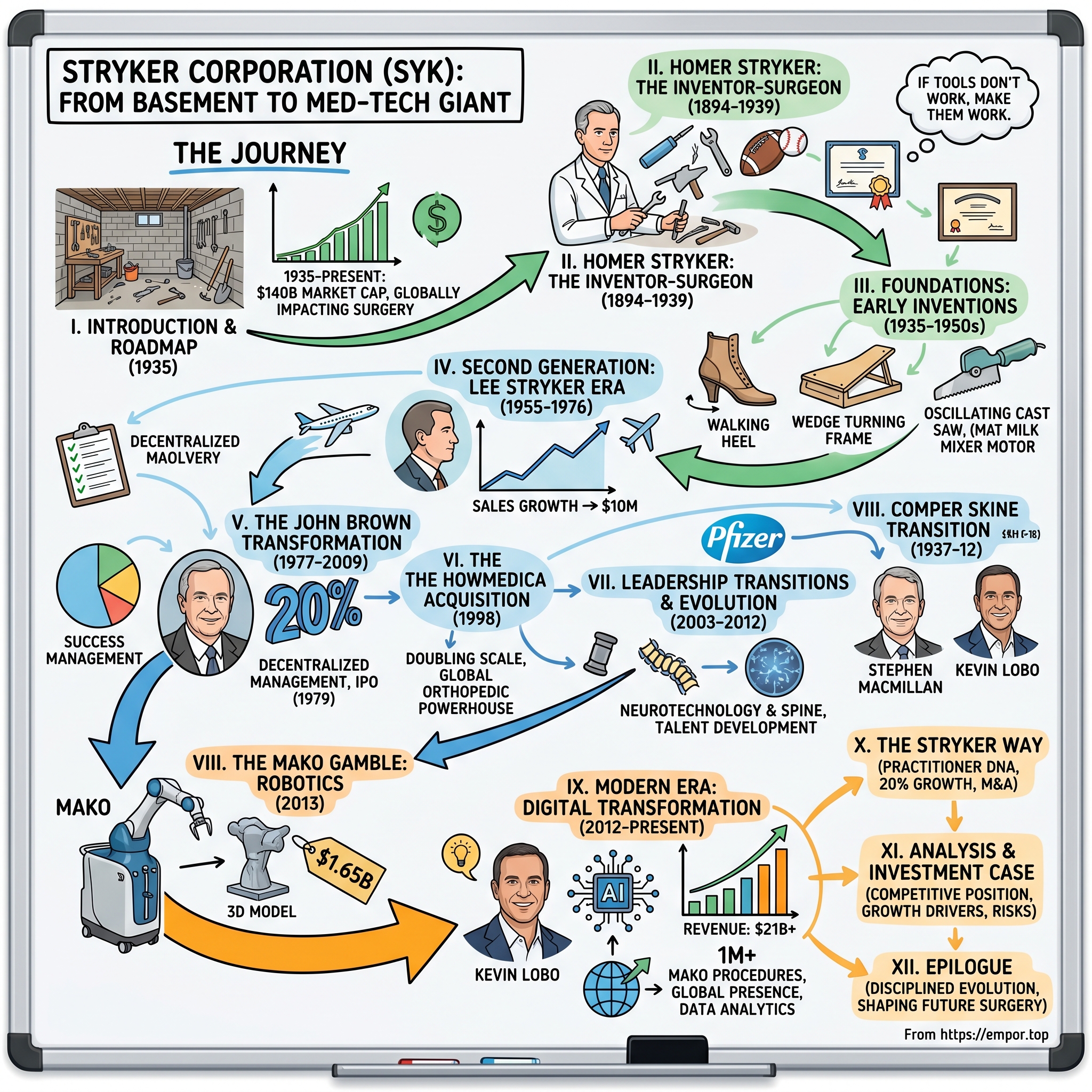

Stryker Corporation: From Doctor's Workshop to Medical Technology Giant

I. Introduction & Episode Roadmap

Picture this: It's 1935 in Kalamazoo, Michigan. A young orthopedic surgeon descends into the basement of Borgess Hospital after a frustrating day in the operating room. Not to decompress, but to tinker. Dr. Homer Stryker had just watched another patient struggle with a plaster cast, witnessed another bedridden patient develop painful bedsores, and felt the familiar ache in his hands from using inadequate surgical tools. While other doctors might have simply accepted these as occupational hazards, Homer saw engineering problems begging for solutions.

That basement workshop would become the birthplace of Stryker Corporation—today a $140 billion medical technology colossus that touches millions of surgeries annually. From those humble beginnings of a doctor solving his own problems with hand tools and ingenuity, Stryker has evolved into one of the "Big Three" orthopedic device makers globally, pioneering everything from the oscillating cast saw to AI-powered surgical robots.

The Stryker story isn't just another corporate success tale. It's a masterclass in how practitioner-innovators create enduring value, how operational discipline can become a competitive moat, and how strategic bets on emerging technologies—even when Wall Street howls in protest—can define industries. This is the story of three generations of leadership, each navigating their era's unique challenges: Homer's inventive genius, Lee's modernization efforts cut tragically short, John Brown's legendary 20% growth mandate that defied gravity for decades, and today's leaders betting billions that the future of surgery is robotic.

We'll trace how a company built on mechanical innovations for broken bones became a digital surgery powerhouse. We'll examine the acquisition playbook that turned regional players into global platforms. And we'll explore why, in an era of software eating the world, a hardware-heavy medical device company remains one of the market's most consistent performers.

The themes that emerge—innovation from the frontlines, operational excellence as strategy, and the courage to make transformational bets—offer lessons far beyond healthcare. Because at its core, this is a story about solving real problems for real people, and building a machine that can do it at scale for generations.

II. The Inventor-Surgeon: Homer Stryker's Origins

The path to becoming a medical device pioneer rarely starts in a township of 300 people, yet Homer Hartman Stryker's journey began exactly there. Born on November 4, 1894, in Wakeshma Township, Michigan, Homer grew up in rural America at the dawn of the 20th century—a time when a medical emergency often meant a day's journey by horse and buggy to the nearest doctor.

His early years showed little hint of the innovator to come. After graduating from Athens High School in 1913, Homer enrolled at Western State Normal College (now Western Michigan University), planning to become a teacher. He graduated in 1916, equipped with the credentials to educate but not yet the calling that would define his life. The real drama begins with Homer's quest for medical education. To afford medical school tuition, Stryker taught at a school in Grand Ledge, Michigan, coached football, basketball and baseball, worked as a barber, and pitched for the Grand Ledge semi-professional baseball team. Picture the future medical device mogul moonlighting as a barber between baseball games, saving every penny for a dream that seemed impossibly distant. This wasn't just financial hustle—it was character formation. The man who would later insist on solving problems himself was already demonstrating that ethos, refusing to let circumstances dictate his future.

The medical school required passing a foreign language exam before full admittance, which Stryker failed. Rather than surrender, Homer found a creative solution: He got tutoring in French from a fellow student, and was later able to begin his medical studies in 1921 after earning enough for the tuition and passing the foreign language exam. That French tutor, Mary Jane Underwood, would become his wife in 1924—a partnership that would sustain him through the challenging years ahead.

Once admitted to medical school, Homer didn't just study medicine—he dominated athletics too. Homer was the starting pitcher for the University of Michigan baseball team, leading them to a Big Ten Conference title. This dual excellence—intellectual rigor combined with physical mastery—would define his approach to surgical innovation. He understood the body both as a biological system and as a mechanical challenge.

He earned his Doctor of Medicine degree from the University of Michigan Medical School in 1925 and interned at the University Hospital in Ann Arbor for three years. After moving to Alma, Michigan, and working briefly at a small private hospital, they moved to Kalamazoo in 1928. He opened a general practice on the second floor of the State Theater building in downtown Kalamazoo.

The transformation from general practitioner to orthopedic specialist came later. After serving as Kalamazoo County physician from 1929 to 1930, Homer realized his true calling lay in fixing broken bones and damaged joints. He returned to University Hospital in 1936 for a residency in orthopedic surgery, bringing his wife and young son Lee along. During his residency, he began working on ways to improve traditional procedures for moving immobile patients and to make patients more comfortable.

When he returned to Kalamazoo in 1939, he established offices in Borgess Hospital, where he was the only orthopedic surgeon in the region. He had an office on the second floor and a workshop in the basement. That basement workshop would become the birthplace of an empire.

Homer embodied a philosophy he would later articulate in a 1963 speech: "It's a poor workman that blames his tools. If they don't work, make them work. If you can't make them work, make some that do work". This wasn't just a motto—it was a manifesto that would guide three generations of innovation at Stryker Corporation.

III. From Frustration to Foundation: The Early Inventions (1935–1950s)

The basement of Borgess Hospital in 1935 looked nothing like a corporate R&D facility. Workbenches cluttered with metal scraps, rubber samples, and hand tools. The smell of machine oil mixing with hospital antiseptic wafting down from the floors above. This was where Dr. Homer Stryker retreated after long days in surgery, not to rest but to wrestle with the inadequacies he encountered upstairs.

In 1935, Stryker began tinkering in his workshop with medical devices, developing a rubber heel for walking casts as well as an innovative hospital bed that reduced the incidence of bedsores in bed-ridden patients. The rubber heel seems simple in retrospect, but consider the alternative: The Walking Heel for walking casts was made of rubber, and thus was much lighter than the cast iron heels of the time, so the patient's mobility was better. Patients who previously limped under the weight of iron could now walk more naturally. Small innovation, massive impact.

But it was the hospital bed problem that truly consumed Homer. He watched immobilized patients develop painful bedsores, blood clots, and muscle atrophy—complications that often proved more dangerous than the original injuries. The standard protocol required multiple nurses to manually turn patients every few hours, a process that was labor-intensive, often painful for patients, and sometimes resulted in further injury.

The Wedge Turning Frame was an important medical breakthrough used to treat patients who were immobilized during extended hospital stays and often developed blood clots and skin problems. It allowed medical personnel to quickly and easily turn their patients to help prevent some of those complications. The device used a sandwich-like design where the patient lay between two frames that could be rotated, allowing a single nurse to safely turn even the heaviest patient with minimal effort.

World War II transformed everything. During World War II, his Wedge Turning Frame was sought after by the U.S. Army, so orders increased. Dr. Stryker hired two part-time workers and began producing Wedge Turning Frames and Walking Heels. The military's demand validated what Homer already knew: these weren't just clever gadgets but essential medical infrastructure. Battlefield hospitals desperately needed ways to manage wounded soldiers who couldn't move themselves.

It was in this workshop that he began to manufacture and sell some of his inventions, transforming from inventor to entrepreneur almost by accident. As word spread through the medical community, orders arrived from hospitals across the Midwest. Homer found himself running a small manufacturing operation between surgeries, filling orders in the evening, and delivering products personally on weekends.

The formal incorporation came in 1946 when Homer founded the Orthopedic Frame Company Inc. to properly manufacture and sell his inventions. This wasn't a Silicon Valley-style startup with venture funding and growth hackers. It was a doctor solving problems for other doctors, one device at a time. Perhaps Homer's most ingenious creation emerged in 1943. He created his most important invention, an oscillating electric saw "such that the cutter is actuated with a relatively short oscillating stroke of the order of one-eighth of an inch", that cuts and removes casts but would not cut skin. The engineering brilliance lay in the physics: The design enables the saw to cut rigid materials such as plaster or fiberglass. In contrast, soft tissues such as skin move back and forth with the blade, dissipating the shear forces, and preventing injury.

Originally named The Cast Cutter, the Stryker saw was designed with an oscillating blade that was originally powered by a motor from a malted milk mixer. Think about that for a moment—a surgeon borrowing a motor from a kitchen appliance to solve a medical problem that had plagued physicians for decades. Modern cast saws date back to the plaster cast cutting saw which was submitted for a patent on April 2, 1945, by Homer H. Stryker, an orthopedic surgeon from Kalamazoo, Michigan. He received a patent in 1947 and the principle is used today in the "Stryker Saw", the standard surgical tool for bone and plaster casts.

The company's growth accelerated through the 1950s. During this decade, Homer developed what many consider his masterpiece: the Circ-O-Lectric Hospital Bed. During the 1950s, Dr. Stryker worked on what was arguably his most famous invention — the Circ-O-Lectric Hospital Bed. An electric motor turned a bed, suspended between two wheels, to a vertical or horizontal position, as well as many positions in between. The device could be operated by the patient or a nurse. Like the Wedge Turning Frame, this reduced the amount of time and effort required by staff to physically move patients. Patients liked the bed because it was more comfortable, and they could operate it themselves.

By 1955, a crucial transition began. In 1955, Dr. Stryker's son Lee joined the company as general manager and, in 1958, sales hit $1 million. This marked the shift from inventor's workshop to genuine business—a transformation that would accelerate dramatically under Lee's leadership.

IV. The Second Generation: Lee Stryker Era (1955–1976)

Lee Stryker entered the family business carrying the weight of being the founder's son but also the promise of a new generation's perspective. Where Homer was the tinkerer-surgeon, Lee was the modernizer—a man who understood that great inventions needed great organizations to reach their potential.

The contrast between father and son was immediately apparent. Homer still showed up to work in surgical scrubs, often disappearing to the workshop between patient appointments. Lee arrived in business attire, armed with organizational charts and growth projections. Yet rather than clash, their styles complemented perfectly during the transition years.

Lee's first major contribution was systematizing what had been an artisanal operation. He established proper manufacturing processes, quality control standards, and distribution networks. The company that had relied on Homer personally demonstrating products at medical conferences now had a professional sales force calling on hospitals nationwide.

Under Lee's operational leadership, the company expanded beyond Homer's original inventions. They developed powered surgical instruments—drills, saws, and reamers that gave surgeons unprecedented precision and control. These weren't just incremental improvements but fundamental reimaginings of how surgery could be performed. The powered instruments reduced surgeon fatigue, shortened procedure times, and improved patient outcomes.

In 1964, Dr. Stryker retired from his medical practice and changed the name of the company to Stryker Corporation. This wasn't just a rebranding—it signaled the transformation from a medical practice with a side business to a corporation with global ambitions. In 1969, Lee became president and chief operating officer.

By the mid-1970s, Lee had transformed his father's workshop into a sophisticated medical device company. The company boasted 280 employees and approached $10 million in annual sales—a far cry from the basement operation of three decades earlier. Lee had professionalized every aspect of the business while maintaining the innovative spirit that Homer had instilled.

Then tragedy struck. He served in that position until 1976, when he died in a plane crash while on vacation in Wyoming. Lee was just 45 years old, in the prime of his leadership, with plans for international expansion and new product lines. The company he'd spent two decades building suddenly faced an existential crisis.

The loss reverberated through Kalamazoo's business community and the broader medical device industry. Stryker Corporation had lost not just its CEO but its bridge between the founding generation and the future. The board faced an impossible question: Who could fill the shoes of both Homer the innovator and Lee the operator?

For months, the company drifted. Sales teams continued selling, factories continued producing, but without clear leadership, strategic decisions stalled. Competitors sensed vulnerability. Employees worried about their futures. The Stryker family, still reeling from personal loss, had to make decisions about the company's ownership and direction.

What happened next would define Stryker for the next three decades and transform it from a regional player into a global powerhouse. The board's choice would prove to be one of the most consequential CEO selections in American business history.

V. The John Brown Transformation: Going Public & 20% Growth (1977–2009)

The boardroom at Stryker headquarters in January 1977 was thick with tension. Six months had passed since Lee's death, and the company needed direction. Then walked in John W. Brown—a chemical engineer from rural Tennessee who'd never worked in medical devices but had something more valuable: a track record of operational excellence and an almost religious belief in disciplined growth.

In 1976 Brown got a call from a recruiter, who was helping Stryker after the loss of its President and CEO. Lee Stryker, the son of the founder, was killed in a tragic plane crash. The company needed a new leader, but Brown had his doubts initially. Lee had close friends on the Board, and he didn't want them to think he was trying to replace him—he knew that wasn't possible. But one of the directors was assigned the task, 'Get John Brown.' He sent Brown's wife flowers, wrote him notes, and finally said, 'What would it take to get you to come to Stryker?'

Brown initially turned them down. They thought it was a negotiating strategy, but it was just he was very concerned because Lee Stryker, the owner, deceased owner, had commingled the business in social activities. Brown worried he couldn't replicate Lee's style of mixing business with personal relationships. But the board persisted, ultimately convincing him he could run the company his own way.

Brown arrived at a company doing $17 million in revenue with about 400 employees. The product line was modest: primarily stretchers – emergency room stretchers and powered instruments and [a] cast cutter. Pretty mundane products. What Brown saw, however, was potential—a strong foundation of innovation that needed operational discipline to scale.

The defining moment came during the IPO roadshow in 1979. Brown had an agreement with the company that he would take it public. In the spring of 1979 the market opened up, and the venture capitalists on the board recommended that we take the leap. One of the investment bankers asked, 'Where are you taking this company?' Brown replied, 'We're going to be a growth company.' He then explained that to do this Brown would have to grow earnings at a rate of 20%.

With 20% seared in his brain, Brown returned to Stryker headquarters and set the stage for the remaining 26 years of his tenure. This became our mantra, and probably had more to do with defining Stryker than anything else. Each year everyone knew the goal. And we did it without violating any rules.

The 20% rule wasn't just a financial target—it became Stryker's operating system. Every division, every product line, every manager was measured against this single, uncompromising standard. Miss it once, you got coaching. Miss it twice, you got replaced. The clarity was brutal but effective.

Brown steadfastly expanded the company's product lines and introduced an effective decentralized management structure as the company grew. This decentralization was key. Rather than micromanage from Kalamazoo, Brown pushed decision-making down to division presidents who ran their units like independent businesses. They had autonomy to innovate, acquire, and expand—as long as they hit 20%.

The first major strategic move came immediately after going public. Stryker went public in 1979 and entered the orthopedic implant market in 1979 by purchasing Osteonics, a New Jersey-based company. This acquisition marked Stryker's transformation from a medical equipment company to an orthopedic powerhouse. Osteonics brought hip and knee implant technology that complemented Stryker's surgical instruments perfectly.

Brown's acquisition philosophy was distinctive: buy companies with strong technology and distribution, then supercharge them with Stryker's operational discipline. He wasn't interested in turnarounds or fixer-uppers. He wanted winners that could become super-winners under Stryker's system.

The results were staggering. Revenues increased from $23 million in 1977 to $4 billion by 2004, and the number of employees increased from 325 to 15,000 during the same time period. By the time Brown retired as chairman in 2009, the company had grown from 400 employees and $17 million in annual sales to 17,000 employees worldwide and more than $6.7 billion in sales.

Jim Collins, in his book "Great by Choice," held up Brown as the exemplar of what he called the "20 Mile March"—the discipline to maintain consistent performance regardless of conditions. John Brown understood that if you want to achieve consistent performance, you need both parts of a 20 Mile March – a lower bound and an upper bound – a hurdle that you jump over, and a ceiling that you will not rise above. The ambition to achieve and the self-control to hold back.

This meant saying no to acquisitions that might juice short-term growth but compromise long-term consistency. It meant investing in R&D during downturns. It meant maintaining pricing discipline even when competitors slashed prices. The 20% rule wasn't just about growth—it was about sustainable, profitable, predictable growth.

Early on, Brown was insistent on making all of the decisions on everything, and then it struck him about three or four years down the road that he was the obstacle. This self-awareness led to his management philosophy: hire great people, give them clear targets, then get out of their way. Brown observed a lot of CEOs over the years, and the smart ones realize that the best way to achieve success is to be a servant of the organization.

Under Brown's leadership, Stryker became a case study in operational excellence. The company maintained its 20% earnings growth for 21 consecutive years—a streak that defied industry cycles, regulatory changes, and economic downturns. When the streak finally ended with the Howmedica acquisition in 1998, it wasn't seen as failure but as strategic evolution. Brown had traded one year of earnings growth for a transformational acquisition that would position Stryker for decades of future success.

VI. The Howmedica Acquisition: Doubling Down on Scale (1998)

The August 1998 boardroom presentation at Stryker headquarters carried unusual tension. John Brown, who'd delivered 21 consecutive years of 20% earnings growth, was about to propose breaking his own sacred rule. The target: Howmedica, Pfizer's orthopedic division. The price: $1.9 billion in cash—nearly double Stryker's entire revenue the previous year.

The healthcare landscape of the late 1990s looked nothing like the fragmented market Stryker had thrived in for decades. Hospital systems were consolidating. Group purchasing organizations wielded unprecedented power. Medicare reimbursements were tightening. Stryker, who had built its sales approach on personal relationships with individual decision-makers, realized that it could not compete effectively as a small company any longer. "Larger institutions and buying groups are demanding ever-higher quality at ever-lower cost, and they prefer to deal with clearly identified market leaders," Brown wrote in his 1998 letter to shareholders, adding, "In this environment, only companies that offer scale and superior efficiency will succeed."

In 1998, Stryker purchased Howmedica, the orthopaedic division of Pfizer, for $1.65 billion. Howmedica became Stryker Orthopaedics. The acquisition wasn't just about size—it was about completeness. Howmedica's products include hip and knee implants for primary and revision surgery, bone cement, trauma systems used in bone repair, craniomaxillofacial fixation devices and specialty surgical equipment used in neurosurgery.

The strategic logic was compelling. Stryker Corp. will buy Pfizer Inc.'s Howmedica unit for $1.9 billion in cash, combining the world's fifth and third largest makers of orthopedic implants, respectively. Upon completion of the deal, Stryker said it will hold approximately 15% of the roughly $10-billion world orthopedic market. This would vault Stryker from a strong regional player to a global orthopedic powerhouse overnight.

But the financial implications were stark. Stryker, now the fifth-largest maker of orthopedic implants, had sales of more than $980 million last year, with $740 million of that coming from orthopedic products. The acquisition will almost double the company's size. But cost of the acquisition will dampen Stryker's growth next year, slowing it to 5 percent, company executives told analysts.

Wall Street's reaction was brutal. Though the company said it expects to return to 20 percent growth by 2000, investors viewed the purchase as somewhat risky, and its shares fell $5.75, to $36. For a company that had trained the market to expect clockwork consistency, even a temporary stumble was heresy.

The integration challenge was massive. Howmedica wasn't just a product line—it was an entire culture, with its own sales force, manufacturing facilities, and ways of doing business. Stryker had to merge two organizations while maintaining operational continuity in a market where surgeons despised disruption to their familiar tools and suppliers.

Brown's team executed with surgical precision. They retained Howmedica's strongest product lines while eliminating redundancies. They cross-trained sales forces to sell the expanded portfolio. Most critically, they applied Stryker's operational discipline to Howmedica's manufacturing, squeezing out inefficiencies and improving margins.

The financial engineering was equally sophisticated. Stryker Corporation's net sales increased 91% in 1999 to $2,103.7 million from $1,103.2 million in 1998. Net sales increased $854.5 million, or 77%, as a result of the Howmedica acquisition. Net sales also grew by 9% as a result of increased unit volume; 3% related to higher selling prices from the conversion of distributors to direct sales; 2% as a result of other acquired businesses; and 1% due to changes in foreign currency exchange rates.

Although the purchase of Howmedica broke its 21-year streak of 20 percent net earnings increases, the company expected to return to its historical growth rate as early as the year 2000. This wasn't just optimism—it was a calculated bet that scale would become the new competitive advantage in orthopedics.

The Howmedica acquisition marked a fundamental shift in Stryker's strategy. No longer could the company rely solely on organic innovation and small tuck-in acquisitions. In the consolidating healthcare market, size mattered. Distribution reach mattered. The ability to offer complete solutions to large hospital systems mattered.

Looking back, the Howmedica deal stands as one of the defining moments in medical device industry consolidation. It triggered a wave of mega-mergers as competitors scrambled to match Stryker's scale. Johnson & Johnson acquired DePuy. Zimmer merged with Biomet. The orthopedic industry's structure was permanently altered.

For Stryker, the gamble paid off spectacularly. By 2004, revenues had reached $4.3 billion—more than double the combined revenues of Stryker and Howmedica at the time of the merger. The company had successfully transformed from a growth story to a growth-at-scale story, proving that operational excellence could work just as well at $4 billion as it had at $400 million.

VII. Leadership Transitions & Strategic Evolution (2003–2012)

The year 2003 marked the beginning of a new chapter as John Brown began planning his succession after 26 years at the helm. MacMillan joined Stryker Corporation in 2003 as president and chief operating officer, and was promoted to chief executive officer in 2005. Stephen P. MacMillan arrived with impressive credentials—11 years at Johnson & Johnson in various senior roles and experience at Pharmacia Corporation. He represented a new generation of medical device leadership: polished, strategic, and comfortable navigating the increasingly complex healthcare landscape.

MacMillan inherited a company that had successfully digested the Howmedica acquisition and returned to its growth trajectory. At the end of 2012, Stryker had approximately 22,000 global employees and annual sales of $8.7 billion. But he also faced new challenges: increasing pricing pressure from hospitals, more stringent regulatory requirements, and the need to expand beyond traditional orthopedics.

Under MacMillan's leadership, Stryker accelerated its push into adjacent markets. The company systematically built positions in neurotechnology, spine, and medical/surgical equipment. Each move was calculated to leverage Stryker's core competencies—direct sales relationships with surgeons, operational excellence, and innovation—into new growth vectors.

In August 2011, Stryker signed a definitive agreement to acquire privately held Concentric Medical, Inc. in an all-cash transaction for $135 million. Concentric's products include devices for the removal of thrombus in patients experiencing acute ischemic stroke along with a broad range of AIS access products. This acquisition exemplified MacMillan's strategy: find innovative technologies in high-growth markets adjacent to Stryker's core.

The transformational move came in January 2011. Lobo came in as the president of a new neurotechnology unit, comprised of the company's own neurovascular and spine divisions and the assets from its $1.5 billion acquisition of Boston Scientific (NYSE:BSX) stroke-treatment business. This acquisition of Boston Scientific's Neurovascular Division marked Stryker's aggressive entry into the rapidly growing stroke treatment market.

MacMillan also began the critical work of talent development. MacMillan recruited Lobo from healthcare giant Johnson & Johnson (NYSE:JNJ), where Lobo was president of Ethicon Endo-Surgery. Lobo was one of MacMillan's recruits, joining the company in early 2011. Kevin Lobo's arrival as Group President would prove more significant than anyone realized at the time.

Then came the shock. He resigned from the position in February 2012, with the company citing "family reasons." Chief Financial Officer Curt Hartman stepped in as interim CEO. The sudden departure after just seven years rattled investors and employees alike. Unlike the planned transition from Brown to MacMillan, this was abrupt and unexpected.

Hartman's resignation was announced alongside Lobo's appointment, although he will stay on in an advisory role for the time being. "Hartman, who has served as Stryker's interim CEO since February of this year, has decided to pursue opportunities outside of Stryker," the device maker announced, "but has agreed to stay on as an advisor to the CEO to assure a smooth transition as the company conducts a search for a permanent CFO."

The board faced a critical decision: go outside for a proven CEO or promote from within. They chose the insider with outside experience. On October 1, 2012, Mr. Kevin A. Lobo was appointed as president and chief executive officer. Lobo was named CEO on Oct. 1, 2012 after the sudden resignation of Stephen MacMillan in February of 2012.

Former CEO MacMillan himself endorsed the choice. "He's by far the best choice. I'm frankly happy to have him carry on our legacy," MacMillan told us. "They made a great choice in Kevin." "Kevin has a lot of outside experience and he clearly understands the company," he added. "He's a natural choice and it's the best of both worlds."

Lobo brought a unique combination of experiences. Prior to Stryker, Lobo held executive positions with Rhone-Poulenc, where he was based in England and France, before moving to Johnson & Johnson. He was eventually named president of Johnson & Johnson Medical Products in Canada in 2005. He became President of Ethicon Endo-Surgery, Inc. in 2006.

His approach was methodical yet bold. "The first step is always to listen. You listen, learn, engage the teams, be transparent and open, identify areas of opportunity, align the team and focus on winning," said Lobo. This wasn't just corporate speak—it was a philosophy that would guide Stryker's next phase of growth.

The transition period from 2003 to 2012 had transformed Stryker from a primarily orthopedic company to a diversified medical technology leader. The company now operated across three distinct segments, each with its own growth dynamics and competitive challenges. The stage was set for the next big bet—one that would either secure Stryker's future or become an expensive mistake.

VIII. The MAKO Gamble: Betting Big on Robotics (2013)

The September 25, 2013 announcement sent shockwaves through Wall Street and the medical device industry. Stryker Corporation (NYSE:SYK) announced today a definitive agreement to acquire MAKO Surgical Corp. (MAKO) for $30.00 per share with an aggregate purchase price of approximately $1.65 billion. The deal, which values MAKO at $30 per share, represents a whopping acquisition premium of 87.5% over the previous day's closing price.

Kevin Lobo, barely a year into his CEO tenure, was making his boldest move yet. This wasn't a tuck-in acquisition or a geographic expansion—it was a bet that the future of orthopedic surgery would be robotic. And he was willing to pay a price that made even seasoned analysts gasp.

Founded in 2004, MAKO has pioneered the advancement of robotic assisted surgery in orthopedics. MAKO currently markets the RIO® Robotic Arm Interactive Orthopedic System and RESTORIS® family of implants to enable its flagship MAKOplasty Partial Knee Resurfacing procedure for the treatment of early to mid stage osteoarthritis. More recently, MAKO expanded its product offering to include the MAKOplasty Total Hip Arthroplasty, a new robotic arm application for patients in need of a total hip replacement.

The strategic rationale was compelling but controversial. The RIO offered surgeons an interactive platform that incorporated a robotic surgical arm and a patient-specific visualization technology. The combination was designed to perform minimally invasive procedures that were more exact and repeatable. The RIO system assists surgeons by creating a 3-D model of the patients' anatomy, enabling surgeons to develop a pre-surgical plan that customizes implant size, positioning and alignment specifically for each patient.

But the price tag drew immediate criticism. According to Needham & Company analyst Mike Matson, represents a 2013E EV/sales multiple of 10.6x. "This is well above the average orthopedics acquisition multiple of 3.1x but perhaps not shocking given MAKO's leadership position, growth rate, and patent portfolio," added Matson. Still, paying over 10 times sales for a company generating just $103 million in 2012 revenue seemed audacious.

Glenn Novarro at RBC Capital Markets acknowledged in a research note that the announcement had caught him off guard, but sounded a less positive note. Even while conceding that the move "will essentially expand SYK's recon offering," he cautioned about the high price that Stryker was paying - at $30 per share, Stryker was paying nearly double the company's closing price of $16.17 on Tuesday.

The skepticism was understandable. Only 2% of worldwide surgeries last year were performed with robot-assisted procedures. MAKO's RIO Robotic Arm, by comparison, costs nearly $1 million. Hospitals were already squeezed on capital budgets. Would they really invest in expensive robotic systems when traditional surgery worked just fine?

Lobo saw what the skeptics missed. "MAKO has established a compelling technology platform in robotic assisted surgery which we believe has considerable long term potential in joint reconstruction," said Lobo. "The acquisition of MAKO combined with Stryker's strong history in joint reconstruction, capital equipment (operating room integration and surgical navigation) and surgical instruments will help further advance the growth of robotic assisted surgery. Our combined expertise offers the potential to simplify joint reconstruction procedures, reduce variability and enhance the surgeon and patient experience."

The integration proved challenging. "Introducing a disruptive technology to an industry that has historically relied on incremental improvements to implants and procedures has had its challenges. We will continue to integrate our robotic-arm assisted technology into our existing reconstructive business," said Stuart Simpson, VP and GM of Stryker Reconstructive Business. While 2014 sales figures of MAKO fell below the company's conservative forecasts, "We worked through integration issues early last year, [and] by Q4 we had gained considerable momentum, which resulted in the sale of 20 MAKO robots – the highest level of quarterly-unit sales ever," Simpson said.

The long-term vision began paying dividends. Stryker's 2013 acquisition of MAKO Surgical for $1.65B was criticized at the time as too expensive, but by 2019 Stryker felt justified in its purchase. In 2019, Stryker had about 860 Mako robots installed globally. By the end of 2020, about 44% of all its total knee replacement procedures were done with the Mako robot.

The MAKO acquisition represented more than just a product addition—it was a philosophical shift. Stryker was no longer content to be a fast follower in technology. Under Lobo's leadership, the company would make bold bets on transformational technologies, even if Wall Street didn't immediately understand the vision.

BMO Capital Markets analyst Joanne Wuensch wrote that this signifies the start of industry consolidation. "For Stryker, the company takes a step forward into robotic surgery, consolidates its orthopedic silo, and continues its M&A strategy that it has been on for several years." She was right—the MAKO deal would trigger a robotics arms race in orthopedics that continues to this day.

IX. Modern Era: Kevin Lobo's Leadership & Digital Transformation (2012–Present)

Kevin Lobo's tenure as CEO has transformed Stryker from a $8.7 billion company in 2012 to a medical technology powerhouse approaching $21 billion in revenue. Under his leadership, the company has completed more than 60 acquisitions and advanced innovation and global market presence. But the true validation of his strategy has come through the spectacular success of the Mako platform.

The numbers tell a compelling story of patient adoption and market dominance. In 2019, Stryker had about 860 Mako robots installed globally. By 2023, Mako Systems were installed in 35 countries with over 1 million Mako global procedures completed to date. In the U.S., Stryker saw 60% of its knee replacements and 34% of its hips performed using Mako at the end of the year.

The transformation hasn't been merely about selling robots—it's been about changing the entire paradigm of joint replacement surgery. The RIO system assists surgeons by creating a 3-D model of the patients' anatomy, enabling surgeons to develop a pre-surgical plan that customizes implant size, positioning and alignment specifically for each patient. During the procedure, real-time visual, tactile, and auditory feedback enforces a safety-zone and facilitates ideal implant positioning and placement, which reduces potential for complications.

Lobo's strategy has evolved beyond the original Mako platform. The company is systematically expanding robotic capabilities across specialties. Mako for spine surgery is coming in the third quarter of 2024, with Mako shoulder coming near the end of the year. This isn't just feature creep—it's building a comprehensive robotic surgery ecosystem that touches every major orthopedic procedure.

The financial performance under Lobo has been remarkable. In 2023, Stryker saw sales increase 11.1% to $20.5 billion, with adjusted EPS of $10.60. This year, Stryker expects sales to grow another 7.5–9.0%, with adjusted EPS of $11.70–12.00. This consistent growth in a mature market demonstrates the power of innovation-driven market share gains.

But Lobo's vision extends beyond robotics. He's positioning Stryker for the digital transformation of healthcare. Stryker segregates their reporting into three reportable business segments: Orthopedics, Medical and Surgical (MedSurg), and Neurotechnology and Spine. Each segment is being infused with digital capabilities, from AI-powered surgical planning to connected hospital beds that predict patient falls.

The company's approach to acquisitions under Lobo has been strategic and disciplined. Rather than chasing growth at any price, Stryker has focused on technologies that enhance its core platforms. Stryker's move into robotics that began with its MAKO Surgical acquisition has developed further with the 2021 acquisition of OrthoSensor, adding an intraoperative sensor technology to enhance Stryker's Mako robots.

The market validation has been overwhelming. Stryker ended 2019 with its best quarterly sales of Mako robotic systems since launching the joint surgery platform in 2017. The company sold 89 of the robots during the fourth quarter, compared to 51 in the prior quarter and 54 a year before. By 2024, record installations had become routine, with management noting record-breaking quarters repeatedly.

Lobo's leadership philosophy combines technological vision with operational discipline. "We continue to be a high-growth company with a focus on our mission to deliver for our patients and customers," Stryker CEO Kevin Lobo said during the company's earnings call. This isn't just corporate speak—it's reflected in the company's consistent outperformance.

The expansion into ambulatory surgery centers (ASCs) represents another strategic masterstroke. "Close to half of the deals that we win includes a Mako in these orthopedic ASCs. We've now crossed sort of the 10% mark of large joints that are done in ASCs," Lobo noted. As procedures migrate from hospitals to lower-cost settings, Stryker is positioned to capture this shift.

Looking forward, Lobo is positioning Stryker for the next wave of innovation. "It's an area that we like as a space," Lobo said about soft tissue robotic surgery, currently dominated by Intuitive Surgical. "It's complicated, and there is room for more than one big player." This hints at Stryker's ambitions beyond orthopedics into general surgery robotics.

The digital transformation under Lobo extends to data analytics and artificial intelligence. With 1 million+ patient records and 105 million actionable data points in Mako Insightful Data Analytics database, Stryker is building a competitive moat based on surgical outcomes data that competitors can't replicate.

X. Playbook: The Stryker Way

After eight decades of evolution, Stryker has developed a distinctive playbook that separates it from competitors. This isn't just operational excellence or innovation—it's a systematic approach to building and scaling medical technology businesses that has proven remarkably resilient across market cycles, leadership transitions, and technological disruptions.

The Practitioner-Innovator DNA

The founding insight—that the best medical innovations come from those who use them—remains central to Stryker's culture. Homer Stryker wasn't trying to build a company; he was trying to solve problems he encountered daily. This practitioner-first mentality permeates product development even today. Engineers don't just design in labs; they observe surgeries, talk to nurses, and understand the frustrations of healthcare delivery firsthand.

This approach creates a fundamental advantage: Stryker's innovations solve real problems rather than searching for applications. When a Stryker sales representative demonstrates a new product, they're not selling features—they're addressing pain points the surgeon has likely complained about for years.

The 20% Growth Discipline

John Brown's 20% rule did more than set financial targets—it created a culture of relentless improvement. Every division, every product line, every regional manager knows the expectation. This clarity eliminates excuses and creates accountability. You either hit the target or you don't. There's no middle ground.

But the genius of the 20% rule isn't the number itself—it's what achieving it requires. You can't grow 20% annually through price increases alone. You can't do it through cost-cutting. You must innovate, gain market share, enter new markets, or make smart acquisitions. The target forces strategic thinking and operational excellence simultaneously.

Even after the streak ended, the discipline remained. Stryker still targets industry-leading growth, just with more flexibility to make transformational moves like the MAKO acquisition that might temporarily disrupt the trajectory.

Decentralized Entrepreneurship

Stryker operates like a confederation of entrepreneurs rather than a monolithic corporation. Division presidents run their businesses with remarkable autonomy. They control their R&D budgets, sales strategies, and operational decisions. Corporate provides capital, shared services, and strategic direction, but execution happens at the division level.

This structure enables speed and accountability. A division president can't blame corporate for missing targets—they own their results. It also allows different businesses to operate optimally for their specific markets. The dynamics of selling hospital beds differ vastly from selling robotic systems, and Stryker's structure acknowledges this reality.

M&A as a Core Competency

Stryker's acquisition strategy follows clear principles: buy market leaders or transformational technologies, pay fair prices for quality assets, and integrate systematically. The company doesn't do turnarounds or distressed acquisitions. It buys strength and makes it stronger.

The integration playbook is equally disciplined. Stryker typically maintains the acquired company's product development and customer relationships while implementing its operational systems and sales processes. This preserves value while improving execution. The MAKO integration exemplifies this—the technology remained intact while Stryker's sales force and operational discipline accelerated adoption.

Building Platforms vs. Point Solutions

Stryker thinks in platforms, not products. The Mako robot isn't just a surgical tool—it's a platform for multiple procedures, data collection, and continuous improvement. Hospital beds aren't just furniture—they're part of an integrated patient monitoring and safety system.

This platform thinking creates competitive moats. Once a hospital invests in Mako, switching costs are high—not just financially but in terms of surgeon training, workflow integration, and patient marketing. Each additional application (knee, hip, spine, shoulder) increases the platform's value and stickiness.

Direct Sales Relationships

While many medical device companies rely on distributors, Stryker maintains direct sales forces in major markets. This requires significant investment but provides invaluable benefits: direct customer feedback, better service, stronger relationships, and higher margins.

Stryker sales representatives aren't just order-takers—they're clinical consultants who attend surgeries, provide training, and become trusted advisors. This relationship-based selling creates barriers to competition that product features alone cannot provide.

Innovation Cycles Management

Medical technology follows predictable innovation cycles—mechanical to electronic to digital to AI-enhanced. Stryker has successfully navigated each transition by investing ahead of the curve while maintaining strong positions in mature technologies.

The company doesn't abandon profitable legacy businesses to chase the latest technology. Instead, it manages a portfolio across the innovation spectrum. Basic surgical instruments still generate cash that funds robotic development. Manual hospital beds coexist with AI-powered models. This portfolio approach provides stability while enabling transformation.

Operational Excellence as Strategy

Stryker's operational discipline turns execution into competitive advantage. Inventory turns, manufacturing efficiency, quality metrics—these aren't just operational details but strategic differentiators. When you can deliver products faster, more reliably, and with better quality than competitors, you win deals regardless of product superiority.

This operational excellence extends to financial management. Stryker maintains strong balance sheets, generates consistent cash flow, and allocates capital efficiently. This financial strength enables opportunistic acquisitions and sustained R&D investment even during downturns.

Cultural Consistency Across Transitions

Despite multiple CEO transitions and massive growth, Stryker's culture remains remarkably consistent. The emphasis on customer focus, innovation, accountability, and performance persists across generations of leadership. This isn't accident—it's systematic culture building through hiring, training, incentive systems, and leadership development.

New employees quickly learn the Stryker way: customer problems drive innovation, quality is non-negotiable, growth is expected, and results matter. This cultural consistency enables the company to scale while maintaining its entrepreneurial spirit.

XI. Analysis & Investment Case

Competitive Positioning

Stryker occupies an enviable position in the global medical device oligopoly. Against Johnson & Johnson's DePuy Synthes, Stryker wins on focus—while J&J manages a conglomerate, Stryker lives and breathes orthopedics. Against Zimmer Biomet, Stryker wins on execution and innovation—particularly in robotics where Mako's 5-year head start has created a commanding lead. Against Medtronic, Stryker's orthopedic specialization provides deeper expertise despite Medtronic's larger scale.

The competitive dynamics increasingly favor scale players. Hospital consolidation creates larger customers demanding comprehensive solutions. Value-based care shifts focus from products to outcomes. Regulatory requirements raise barriers to entry. In this environment, Stryker's position as one of the "Big Three" in orthopedics provides structural advantages that grow stronger over time.

The Robotics Moat

Mako represents more than a product—it's a platform creating multiple competitive moats. The data moat grows with every procedure, now exceeding 1 million surgeries. This surgical outcome data enables continuous algorithm improvement that competitors starting today cannot replicate. The training moat means thousands of surgeons trained on Mako are unlikely to switch systems. The workflow integration moat makes Mako part of hospital operations, not just a surgical tool.

The economic moat may be most powerful. With systems costing nearly $1 million and requiring significant training investment, hospitals typically choose one robotic platform. Stryker's installed base of over 860 systems globally creates recurring revenue from disposables, service contracts, and upgrade paths that provide predictable cash flow and customer lock-in.

Growth Drivers

Demographics provide a powerful tailwind. The global population over 65 will double by 2050, driving demand for joint replacements, spine surgeries, and other orthopedic procedures. Rising obesity rates accelerate joint degeneration. Active aging means more seniors demanding mobility solutions rather than accepting limitations.

Emerging markets offer massive expansion potential. As healthcare infrastructure develops in China, India, and other growth markets, demand for advanced orthopedic care explodes. Stryker's acquisition of Trauson in China provides a platform for capturing this growth while navigating local market dynamics.

Technology adoption remains early. Despite Mako's success, robotic penetration in orthopedics remains under 20% in most procedures. The expansion to spine and shoulder procedures opens entirely new markets. The potential move into soft tissue robotics could double the addressable market.

Risk Factors

Reimbursement pressure remains the industry's sword of Damocles. Government healthcare programs and private insurers continuously push for lower prices. While robotic surgery's better outcomes support premium pricing today, this could change if budget pressures intensify.

Competitive threats are intensifying. Zimmer Biomet's Rosa robot is gaining traction. Smaller players like Globus Medical are innovating aggressively. Tech giants like Google and Apple circle healthcare, potentially disrupting traditional business models.

Technology disruption could obsolete current approaches. Regenerative medicine might reduce the need for joint replacements. 3D-printed custom implants could commoditize standard products. AI might enable non-specialists to perform complex procedures, reducing the value of specialized tools.

Capital Allocation Track Record

Management's capital allocation deserves high marks. The company generates strong returns on invested capital, consistently exceeding 20%. Dividend growth has been reliable, with increases every year since going public. Share buybacks supplement dividends without compromising growth investment.

The acquisition track record shows discipline. While the MAKO price seemed high, the strategic value has proven worth the premium. Smaller acquisitions consistently add capabilities without diluting returns. The company walks away from overpriced deals, showing discipline rare in growth-focused management teams.

Valuation Considerations

Stryker typically trades at premium multiples reflecting its quality and growth. The premium is justified by consistent execution, strong competitive position, and secular growth drivers. However, investors must consider whether current multiples adequately reflect risks from healthcare reform, competition, and technology disruption.

The key isn't whether Stryker deserves a premium—it clearly does—but whether the current premium adequately balances growth potential against emerging risks. Long-term investors should focus less on multiple expansion and more on the company's ability to compound earnings through market share gains and new market entry.

XII. Epilogue & Looking Forward

Standing in Stryker's headquarters today, you can still feel Homer's presence—not in memorabilia or portraits, but in the engineering labs where problems become products, in the training centers where surgeons master new techniques, and in the manufacturing floors where precision is measured in microns. The boy who lost two fingers to a farming accident and became a surgeon never stopped solving problems. That DNA persists.

The evolution from mechanical to digital to AI-powered devices isn't just technological progress—it's the continuation of Homer's original insight: healthcare providers need better tools. Today's Mako robot, with its haptic feedback and 3D modeling, would seem like magic to Homer. Yet he'd immediately recognize the driving force: a surgeon's frustration with imprecise outcomes transformed into engineering solutions.

The next decade promises even more dramatic transformation. Artificial intelligence will move from surgical planning to real-time surgical guidance. Robots will gain greater autonomy, handling routine tasks while surgeons focus on critical decisions. Digital twins will enable surgeons to practice procedures on patient-specific virtual models before touching real tissue.

But technology alone won't determine winners. The lessons from Stryker's history—solving real problems, operational excellence, strategic M&A, and cultural consistency—matter more than any specific innovation. Companies that combine technological capability with these fundamentals will thrive. Those chasing technology without operational discipline will struggle.

The competitive landscape will reshape dramatically. Tech giants will enter healthcare more aggressively, bringing AI expertise and capital resources that dwarf traditional medical device companies. Chinese competitors will challenge Western incumbents globally, not just in emerging markets. Startups will exploit regulatory changes and new technologies to attack incumbent positions.

Yet Stryker's position appears strong. The company's combination of clinical expertise, customer relationships, and operational excellence creates barriers that pure technology players struggle to overcome. The installed base of Mako robots and the data they generate provide competitive advantages that compound over time. The culture of innovation and accountability that began with Homer continues to drive performance.

For investors, Stryker represents a fascinating case study in long-term value creation. From Homer's basement workshop to today's $140 billion market capitalization, the company has compounded wealth through multiple generations, technologies, and market cycles. The next chapter—AI, robotics, and digital health—offers similar potential for those patient enough to let the story unfold.

The enduring lesson from Homer Stryker's tinkering mindset isn't about medical devices or robotics or even healthcare. It's about the power of solving problems you understand deeply, the value of operational excellence, and the importance of building organizations that outlast their founders. In a world obsessed with disruption, Stryker's eight-decade journey reminds us that sometimes the most powerful force is disciplined evolution.

From that basement in Borgess Hospital to operating rooms worldwide, from mechanical frames to AI-powered robots, from a doctor's frustration to a global enterprise—the Stryker story demonstrates that the best businesses don't just adapt to the future. They create it, one solved problem at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube