Parker-Hannifin: The 100-Year Engine of Motion & Control

I. Introduction & Episode Roadmap

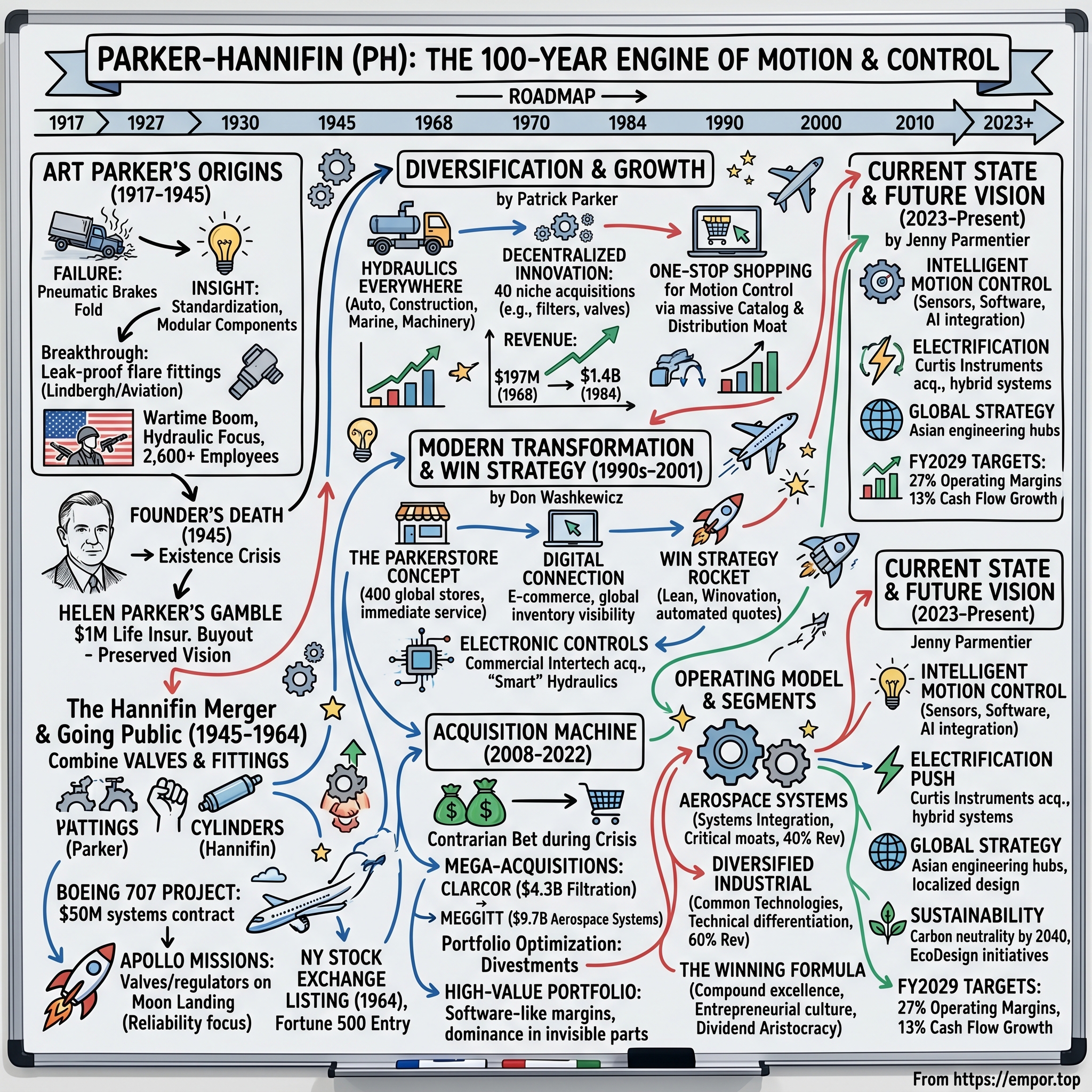

The year is 1927. A young engineer named Arthur Parker watches in horror as a truck careens down a Pennsylvania mountain road, its brakes smoking and failing. The driver pumps frantically at the pedal, but Parker's pneumatic brake system—his life's work—can't hold. The truck jackknifes, crashes, and with it, seemingly, Parker's dreams. His company folds. His investors flee. He's left with nothing but a stubborn belief that air-powered systems could revolutionize how machines move and stop.

Fast forward to today: That failed brake company is now Parker-Hannifin Corporation, a $19.9 billion revenue industrial giant ranked 216 in the Fortune 500. From the landing gear that touched down on the moon to the hydraulics in your car's power steering, from the filters cleaning semiconductor fabrication rooms to the systems controlling the world's largest mining equipment—Parker touches nearly every aspect of modern motion and control.

The central question isn't just how a company survives a century—plenty do that through inertia alone. It's how a company that failed at its original mission transformed into the world's premier motion control technology leader, completing 77+ acquisitions, maintaining 69 consecutive years of dividend increases, and building a decentralized empire of 300+ facilities across 50 countries. This is a story about industrial persistence, yes, but more fundamentally about three counterintuitive strategic choices that defined Parker's century: betting on standardization when everyone else customized, pursuing decentralized innovation when conglomerates centralized, and mastering the art of buying competitors without destroying what made them valuable.

What we're really exploring is this: In an era when industrial companies are supposed to be boring, cyclical, and commoditized, how did Parker-Hannifin build sustainable competitive advantages that compound over decades? The answer lies not in any single breakthrough technology, but in a cultural philosophy that Art Parker articulated simply: "fair dealing, hard work, coordination of effort, and quality products." Sounds quaint. But as we'll see, this framework enabled Parker to navigate from propeller planes to jets, from hydraulics to electronics, from American manufacturing dominance to globalization—always finding new ways to profit from humanity's need to make things move, stop, and flow.

II. Art Parker's Entrepreneurial Origins (1917–1945)

March 13, 1917. While America prepares to enter World War I, a 31-year-old electrical engineer named Arthur LaRue Parker files incorporation papers for the Parker Appliance Company in Cleveland, Ohio. He's just completed his degree at Case Institute of Technology, and he's convinced that pneumatic systems—using compressed air for power—will revolutionize transportation. His target: the booming truck and bus industry, where mechanical brakes are proving inadequate for heavier vehicles and steeper grades.

Parker's timing seemed perfect. The U.S. Army's truck fleet was expanding rapidly for the war effort. Interstate commerce was exploding. But his pneumatic brake system had a fatal flaw—literally. During field tests on steep mountain roads, the air pressure systems couldn't maintain consistent braking force. That Pennsylvania crash wasn't just a setback; it was a complete repudiation of his core technology. By 1919, the Parker Appliance Company was effectively defunct.

Here's where Parker's story diverges from typical entrepreneurial failure. Instead of pivoting to something entirely different or giving up, he took a job at Cleveland's Nickel Plate Railroad specifically to study their air brake systems. For five years, he worked days at the railroad and nights in his garage, methodically understanding why train air brakes worked while his truck brakes failed. The answer: trains operated on predictable grades with standardized equipment, while trucks faced variable conditions with diverse configurations. The insight would reshape his entire approach—stop trying to create universal systems and start creating modular, standardized components that could be configured for specific applications.

In 1924, Parker reopened his company with a radically different strategy. Instead of complete brake systems, he would manufacture precision fittings, valves, and connectors for pneumatic and hydraulic systems. The market was fragmented, with most manufacturers making custom parts for each application. Parker's innovation was standardization—creating interchangeable components with consistent specifications that could be mass-produced and inventoried.

The breakthrough moment came from an unexpected source. In 1927, a young aviator named Charles Lindbergh was preparing for his transatlantic flight. His custom-built Ryan monoplane, the Spirit of St. Louis, had a critical vulnerability: fuel system connections that could leak at altitude. Parker developed a new type of flare fitting that created leak-proof connections even under extreme pressure and temperature variations. When Lindbergh successfully crossed the Atlantic, Parker's fittings had proven themselves in the most demanding possible application. Aviation manufacturers took notice.

By the 1930s, Parker had quietly built a profitable niche business. While the Great Depression devastated heavy industry, Parker survived by diversifying across multiple sectors—aviation, refrigeration, air conditioning, and industrial machinery. The company's employee count grew modestly from 50 in 1930 to 200 by 1939. But Parker was positioning for something bigger. He recognized that hydraulic systems—using fluid instead of air—offered superior power density for the emerging aviation industry. Throughout the late 1930s, he invested heavily in hydraulic research, often using profits from pneumatic products to fund hydraulic development.

Then came December 7, 1941. Pearl Harbor transformed American industry overnight, and Parker Appliance was ready. The company had already been supplying fuel system components to military contractors. Now, with America entering the war, demand exploded for hydraulic systems in aircraft control surfaces, landing gear, and gun turrets. Parker's workforce mushroomed from 910 employees in 1940 to 2,600 by the end of 1941. The company opened a massive new facility in Los Angeles to serve West Coast aircraft manufacturers. Revenue increased twenty-fold during the war years.

But this wartime boom came with a hidden cost. Art Parker, driving himself relentlessly to meet production demands, suffered a series of heart attacks. On January 15, 1945, with victory in Europe just months away, Arthur LaRue Parker died at age 58. The company faced an existential crisis. Major customers wondered if Parker Appliance could survive without its founder. Banks questioned whether to continue credit lines. The board of directors prepared to liquidate.

Enter Helen Parker, Art's widow. In one of the most dramatic moments in American industrial history, she used her husband's $1 million life insurance policy—worth about $16 million today—to buy out shareholders who wanted to sell and provide working capital to continue operations. She had no engineering background, no manufacturing experience. But she understood her husband's vision and believed the post-war aviation industry would need Parker's components more than ever. It was an enormous gamble. If the company failed, she would lose everything. As we'll see, it became one of the most successful bets in American business history.

III. The Hannifin Merger & Going Public (1945–1964)

The scene at Parker Appliance in late 1945 was sobering. Military contracts were being cancelled by the thousands as America demobilized. Employment had already fallen from its wartime peak of 5,000 to under 2,000. Competitors were slashing prices to grab whatever civilian business remained. Helen Parker's million-dollar bet looked increasingly precarious. The company needed new leadership and a new strategy—fast.

The board recruited S. Blackwell Taylor, a seasoned executive from Thompson Products (later TRW), as president. Taylor immediately recognized both the crisis and the opportunity. The crisis: Parker was too dependent on military aviation. The opportunity: commercial aviation was about to explode. Airlines had operated 47 million passenger miles in 1945; Taylor predicted this would increase ten-fold within a decade. He was off by half—it increased twenty-fold.

Taylor's strategic insight went deeper than just riding the commercial aviation wave. He recognized that hydraulic systems were becoming exponentially more complex. A typical military aircraft in 1945 had perhaps 50 hydraulic components. The emerging commercial jets would have 500. No single company could efficiently manufacture such diverse components. Taylor's solution: aggressive specialization through acquisition. Find the best valve manufacturer, the best cylinder producer, the best accumulator designer—and combine them under Parker's standardization philosophy.

The transformation began with internal reorganization. Taylor created distinct divisions for different component types, each with its own P&L responsibility but sharing common engineering standards and sales channels. This decentralized structure—radical for its time—allowed entrepreneurial innovation while maintaining quality consistency. Division managers could make rapid decisions about new products and customers without headquarters approval, as long as they met financial targets and technical standards.

By 1950, Parker had stabilized at around $30 million in annual sales. But Taylor saw a transformative opportunity in the Hannifin Corporation of Des Plaines, Illinois. Founded in 1929 by Harry Hannifin, the company had built a reputation as the premier manufacturer of hydraulic cylinders—the muscle of hydraulic systems, converting fluid pressure into mechanical force. While Parker excelled at valves and fittings (the nerves and blood vessels), Hannifin dominated cylinders (the muscles). Together, they could offer complete hydraulic solutions.

The merger negotiations in 1957 were complex. Hannifin shareholders worried about being absorbed by a larger competitor. Parker's board questioned paying $7.5 million—equivalent to 25% of Parker's market value—for a company with overlapping customers. But Taylor pushed through with a crucial concession: Hannifin would maintain its separate identity as a division, keeping its management team and manufacturing methods. This precedent of preserving acquired companies' cultures while integrating their technologies became the Parker-Hannifin playbook for decades of future acquisitions.

The newly merged Parker-Hannifin Corporation immediately captured a project that validated the strategy: hydraulic systems for the Boeing 707, the first successful commercial jet airliner. The 707 required unprecedented hydraulic power—3,000 PSI systems operating in temperature ranges from -65°F at altitude to 200°F on middle eastern runways. Parker-Hannifin was the only supplier that could provide complete systems—cylinders, valves, fittings, and filters—all engineered to work together. Boeing ordered $50 million in components, the largest contract in company history.

The space race provided another catalyst. When President Kennedy announced the moon mission in 1961, Parker-Hannifin was already supplying NASA with specialized valves for rocket fuel systems. But the Apollo program demanded something unprecedented: components that could function in the vacuum of space, survive massive temperature swings, and operate with 100% reliability—there was no roadside assistance on the way to the moon. Parker engineers developed new sealing materials, exotic alloys, and triple-redundant safety systems. By 1969, Parker-Hannifin components were on the lunar module that touched down in the Sea of Tranquility—from the descent engine valves to the life support system regulators.

The sustained growth justified a public offering. On December 9, 1964, Parker-Hannifin began trading on the New York Stock Exchange. The company now employed 4,400 people and generated $100 million in annual revenue. The initial offering price of $32 per share reflected modest expectations—industrial companies were seen as cyclical and capital-intensive. But Parker-Hannifin had a hidden advantage: the aerospace aftermarket. Every valve, cylinder, and fitting installed on an aircraft would need replacement parts and service for the 20-30 year life of the plane. This recurring revenue stream, unusual for an industrial manufacturer, would provide stability through economic cycles.

By 1966, just two years after going public, Parker-Hannifin joined the Fortune 500. The company that had nearly liquidated twenty years earlier was now among America's largest corporations. But as impressive as this growth was, it merely set the stage for the next phase under Patrick Parker—Art Parker's son, who would transform a successful component manufacturer into a diversified industrial empire.

IV. The Patrick Parker Era: Diversification & Growth (1968–1984)

Patrick Parker stepped into the CEO role in 1968 with an almost impossible act to follow. The company his father founded had grown from near-bankruptcy to Fortune 500 status. Revenue stood at $197 million. The aerospace business was booming. Any reasonable leader might have simply maintained course. But Patrick, who had joined the company in 1949 and worked his way up through engineering and sales, saw vulnerability where others saw strength. "We're one recession away from disaster," he told the board. "Aerospace is 70% of our business. When airlines stop buying planes, we stop growing."

His timing for this warning seemed questionable. The Boeing 747 had just made its first flight, promising a new generation of jumbo jets. The Concorde was in development. The Vietnam War was driving military aerospace spending. But Patrick had studied his father's notebooks from the 1930s, which documented how aviation demand could evaporate overnight. He wanted Parker-Hannifin to be recession-proof.

The strategy he developed was deceptively simple but operationally complex: expand into every industry that used hydraulics, pneumatics, or fluid control. Don't just sell to aerospace; sell to automobiles, construction equipment, machine tools, food processing, chemical plants—anywhere fluids or gases needed to be controlled. But here was the crucial insight: don't try to compete on price in these commodity markets. Instead, create standardized product lines that could be customized through modular assembly.

The first major test came in 1970. As Patrick predicted, aerospace orders collapsed as airlines cancelled plane orders amid recession. Parker-Hannifin's aerospace revenue dropped 30% in twelve months. But something remarkable happened: total company revenue only declined 8%. The automotive aftermarket division—selling replacement hydraulic components for power steering and brakes—actually grew during the recession as consumers fixed older cars rather than buying new ones. Patrick's diversification strategy had worked, but he was just getting started.

Between 1970 and 1979, Parker-Hannifin completed 40 acquisitions. Not the headline-grabbing mega-deals that conglomerates of the era pursued, but strategic additions of specialized manufacturers. The Ideal Corporation brought expertise in pneumatic logic controls. Lenser Corporation added industrial filters. Autoclave Engineers provided ultra-high-pressure valves for the emerging offshore oil industry. Each acquisition followed the same pattern: identify the market leader in a narrow niche, pay a premium for quality, maintain the existing management, integrate the products into Parker's distribution system.

The magic was in the distribution strategy. Patrick recognized that Parker's 13,000 industrial customers didn't want to source components from dozens of suppliers. They wanted a single source for fluid power and control components—what Patrick called "one-stop shopping for motion control." By 1975, a maintenance engineer could order Parker hydraulic cylinders, Hannifin valves, Ideal pneumatic controls, and Lenser filters from a single catalog, with guaranteed compatibility and next-day delivery from regional warehouses.

This approach required massive investment in inventory and logistics—anathema to the prevailing just-in-time manufacturing philosophy. But Patrick understood something his competitors missed: in industrial maintenance, downtime is catastrophically expensive. A failed hydraulic seal might cost $50, but if it shuts down a production line, the cost is $50,000 per hour. Customers would pay premium prices for immediate availability.

The numbers validated the strategy spectacularly. Revenue broke $500 million in 1974, then $1 billion in 1980—a psychological barrier for industrial companies. By 1984, when Patrick stepped back from day-to-day operations (remaining chairman), revenue had reached $1.4 billion. The company employed 20,000 people in 100 plants across 35 countries. But more importantly, Parker-Hannifin had transformed from an aerospace supplier into something unique: a diversified industrial company with the margins of a specialty manufacturer.

Patrick's most enduring innovation might have been organizational. He institutionalized what he called "entrepreneurial management"—division presidents had complete autonomy as long as they met financial targets. They could develop new products, enter new markets, even make small acquisitions without corporate approval. But they had to maintain Parker's quality standards and achieve minimum return on assets of 20%. This decentralized structure created internal competition and innovation while maintaining operational discipline.

The cultural philosophy established by Art Parker—"fair dealing, hard work, coordination of effort, and quality products"—remained paramount. But Patrick added a crucial element: "Think like an owner." Division managers received significant equity compensation, unusual for industrial companies at the time. The top 100 executives owned nearly 5% of the company by 1984. This alignment of interests would prove crucial during the challenging transitions ahead.

One fascinating aspect of Patrick's leadership was his approach to economic forecasting. Parker-Hannifin developed sophisticated models predicting industrial production cycles 6-12 months in advance based on leading indicators from diverse end markets. When automotive orders slowed, it signaled upcoming weakness in construction equipment. When aerospace picked up, industrial automation would follow. This "cycle forecasting" capability allowed Parker to adjust production and inventory ahead of downturns, maintaining profitability through recessions that devastated competitors.

As Patrick transitioned to chairman in 1984, with Paul Schloemer taking over as president, Parker-Hannifin stood at an inflection point. The company had proven that diversified industrial manufacturing could generate superior returns. But new challenges loomed: Japanese competition, the personal computer revolution, and the nascent globalization of manufacturing. The next phase would require not just growth, but transformation.

V. Modern Transformation & The Win Strategy (1990s–2001)

The Berlin Wall had just fallen. Japan's economic miracle was cresting. And in a nondescript conference room in Cleveland, Parker-Hannifin executives were having an existential crisis. Customer surveys from 1990 revealed a shocking truth: despite being the industry's technology leader, Parker ranked dead last in customer service among major suppliers. Lead times averaged 6-8 weeks. Custom configurations took months. A General Motors purchasing manager summed it up brutally: "Great products, impossible to work with."

The irony was painful. Patrick Parker had built the company on customer responsiveness, but success had bred complacency. With 200+ manufacturing facilities and 15,000 SKUs, the complexity had become overwhelming. The new CEO, Paul Schloemer, recognized that incremental improvement wouldn't suffice. Parker needed radical transformation.

The solution emerged from an unlikely source: McDonald's. A Parker engineer visiting a McDonald's noticed how they could customize burgers from standard ingredients in under 60 seconds. Why couldn't Parker do the same with hydraulic systems? This observation sparked the "ParkerStore" concept—retail-like outlets where customers could get standard components immediately or configure custom assemblies while they waited.

The first ParkerStore opened in Cleveland in 1993, and it was unlike anything in industrial distribution. Instead of a grimy warehouse with a parts counter, it featured a clean, well-lit showroom with interactive displays. Customers could see cutaway models of components, watch assembly demonstrations, and most importantly, get immediate solutions. A maintenance supervisor could walk in with a failed cylinder at 8 AM and leave with a replacement—either from stock or custom-assembled—by noon.

But ParkerStores were more than just retail outlets. They became technical resource centers. Each store employed application engineers who could diagnose problems, recommend solutions, and even provide emergency on-site service. When a steel mill's hydraulic system failed at 2 AM, they could call the ParkerStore hotline and have an engineer on-site with replacement parts within hours. This service capability commanded premium pricing—emergency parts often sold at 3-4x standard margins.

By 1999, Parker had opened 400 ParkerStores worldwide. But the real innovation was connecting them digitally. The company invested $50 million in an early e-commerce platform that linked all ParkerStores with real-time inventory visibility. A store in Singapore could see available stock in Stuttgart and arrange overnight shipping. This global inventory network created a virtual warehouse of $500 million in parts accessible from any location.

The international expansion accelerated dramatically through the 1990s. When Deng Xiaoping opened China's economy, Parker was among the first Western industrial companies to establish manufacturing there—not just for export, but to serve the domestic market. The company recognized that China's infrastructure boom would require massive amounts of hydraulic equipment for construction machinery. By 2000, Parker operated 10 facilities in China generating $200 million in revenue, while competitors were still debating whether to enter the market.

But the most significant strategic shift came in 1997 with two moves. First, Parker relocated its headquarters from downtown Cleveland to a new campus in Mayfield Heights, symbolically moving from its industrial past to its technology future. The new facility included advanced R&D laboratories, customer training centers, and notably, one of the industry's first rapid prototyping facilities using 3D printing for component design.

Second, Parker made its largest acquisition to date: Commercial Intertech Corporation for $363 million in 2000. Commercial Intertech brought something Parker desperately needed: electronic controls for hydraulic systems. As equipment became computerized, customers wanted integrated electro-hydraulic solutions—valves controlled by software, cylinders with embedded sensors, predictive maintenance algorithms. The acquisition immediately positioned Parker as the leader in "smart" hydraulic systems.

Revenue surpassed $5 billion in 1999, but profitability was lagging. Operating margins had declined to 8%, well below the company's historical 12-15% range. The complexity of managing 300+ facilities and 15,000+ employees was overwhelming traditional management systems. The board made a decisive move: promoting Don Washkewicz, a 28-year Parker veteran who had transformed the hydraulic group, to president in 2000 and CEO in 2001.

Washkewicz arrived with a revolution: the Win Strategy. The name was deliberately simple, even corny, but the execution was sophisticated. Win focused on three metrics: improve customer satisfaction to #1 in the industry, achieve 10% annual earnings growth, and generate returns exceeding cost of capital by 500 basis points. But the real innovation was implementation. Every employee, from factory workers to division presidents, would have personal Win goals tied to compensation.

The transformation was dramatic. Washkewicz implemented lean manufacturing across all facilities, reducing inventory by 30% while improving delivery times. He pioneered "Winovation"—a systematic innovation process that reduced new product development time from 24 months to 9 months. Most impressively, he cut quote response time from days to hours through automated configuration software. A customer could input specifications online and receive a binding quote with delivery date in under 4 hours.

The cultural transformation was equally significant. Washkewicz instituted mandatory retirement at 65 for all executives, including himself—unusual for an industrial company where CEOs often stayed into their 70s. He promoted younger, more diverse leaders, including the first female division president in company history. He also globalized management, moving key positions from Cleveland to regions where Parker was growing fastest.

By 2001, as Washkewicz officially became CEO, Parker-Hannifin was a fundamentally different company than a decade earlier. Still rooted in Art Parker's principles of quality and fair dealing, but now operating with the speed and agility of a technology company. The ParkerStore network provided unmatched distribution. The Win Strategy created organizational alignment. Electronic controls opened new markets. The company was prepared for the 21st century—though no one could have predicted the dramatic consolidation phase about to begin.

VI. The Acquisition Machine: CLARCOR to Meggitt (2008–2022)

The financial crisis of 2008 should have devastated Parker-Hannifin. Industrial production plummeted 20%. Construction equipment sales fell 80%. Automotive production hit 30-year lows. Yet in the depths of the crisis, Don Washkewicz made a contrarian bet that would define Parker's next decade. While competitors retrenched, he went shopping—armed with a $2 billion war chest and a conviction that the crisis had created once-in-a-generation acquisition opportunities.

The strategy started with a paradox. In March 2009, with markets still in freefall, Parker announced a $2 billion contract to supply hydraulic systems for the Airbus A350. Airlines were canceling orders left and right, yet Airbus was betting on the next generation of fuel-efficient aircraft. Washkewicz saw what others missed: the crisis would accelerate the retirement of older, inefficient planes. When recovery came, demand for new aircraft would explode. The A350 contract positioned Parker perfectly for this supercycle.

But Washkewicz's real masterstroke was recognizing that the crisis had broken the will of many industrial competitors. Family-owned businesses lacked succession plans. Private equity-owned firms couldn't refinance debt. Strategic buyers were conserving cash. Parker, with its strong balance sheet and consistent cash flow from the aftermarket business, could acquire premier assets at distressed prices.

Between 2009 and 2015, Parker completed 25 acquisitions for $3.5 billion. Each followed a disciplined playbook: identify market leaders in fragmented niches, pay fair prices (typically 8-10x EBITDA), maintain existing management, integrate back-office functions, and accelerate growth through Parker's global distribution. The acquired companies kept their brands and cultures but gained access to Parker's resources.

When Thomas Williams became CEO in 2015 (Washkewicz had kept his promise to retire at 65), he inherited a company generating $13 billion in revenue with industry-leading margins. But Williams, who had run the Aerospace division, saw an even bigger opportunity. The industrial landscape was consolidating rapidly. Scale was becoming crucial for R&D investment, global reach, and negotiating power with customers. Parker could either be a consolidator or risk being consolidated.

Williams' first major move sent shockwaves through the industry. In December 2016, Parker announced the acquisition of CLARCOR for $4.3 billion—the largest in company history. CLARCOR was the ideal target: a filtration specialist with 40% EBITDA margins, minimal overlap with Parker's existing filtration business, and exposure to attractive end markets like locomotive engines and natural gas processing.

The CLARCOR integration became a Harvard Business School case study in successful M&A. Instead of forcing immediate integration, Williams gave CLARCOR's management two years to maintain independent operations while identifying synergies. Parker's engineers worked with CLARCOR's to develop new products combining Parker's hydraulics with CLARCOR's filtration. Sales teams cross-sold products without competing for commissions. By 2019, the acquisition had generated $300 million in synergies—double the original target.

But Williams was just warming up. In August 2021, Parker announced a deal that dwarfed everything before: acquiring Meggitt PLC for $9.7 billion. Meggitt, a British aerospace and defense specialist, would instantly double Parker's aerospace presence. The company manufactured wheels and brakes for fighter jets, fire suppression systems for engines, and critically, held sole-source positions on numerous military platforms with 30-year service lives.

The Meggitt acquisition was strategically brilliant but operationally complex. It required regulatory approval from the U.S., UK, and EU—complicated by national security concerns about foreign ownership of defense suppliers. Parker made unprecedented commitments: maintaining UK employment, preserving Meggitt's British headquarters, and ring-fencing sensitive military technology. The deal finally closed in September 2022 after 13 months of negotiations.

The integration challenge was immense. Meggitt brought 9,000 employees in 20 countries with distinct cultures and processes. Parker's approach was nuanced—rapid integration of procurement and IT systems to capture cost synergies, but careful preservation of Meggitt's customer relationships and technical expertise. The company divested Meggitt's aircraft wheels and brakes division to Kaman Corporation for $440 million, recognizing it was subscale and would require massive investment to remain competitive.

Simultaneously, Parker executed a dramatic portfolio optimization. Between 2019 and 2022, the company divested $450 million in non-core businesses—industrial hose manufacturers, automotive air conditioning components, and other low-margin operations. The message was clear: Parker would focus on high-value, technically differentiated products with strong aftermarket potential.

The financial engineering matched the operational excellence. Parker refinanced Meggitt's debt at lower rates, saving $50 million annually. The company accelerated Meggitt's transition from defined benefit to defined contribution pensions, reducing long-term liabilities by $800 million. Most importantly, Parker identified $500 million in cost synergies and $250 million in revenue synergies from the Meggitt combination.

By 2022, Parker-Hannifin had transformed into something unprecedented: a $20 billion revenue industrial company with software-like margins. Aerospace now represented 40% of revenue but 55% of profit. The aftermarket business generated 50% of aerospace revenue with 35% operating margins. The company's installed base of components on commercial and military aircraft represented an annuity stream worth $100 billion over the next two decades.

The acquisition spree had also globalized Parker beyond recognition. International revenue reached 50%, with particular strength in Asia. The company operated 300+ manufacturing facilities but had rationalized them into focused centers of excellence. Cleveland might produce aerospace valves, while Shanghai specialized in industrial cylinders, and Milan focused on advanced filtration.

Yet this transformation came with risks. Parker's debt had ballooned to $10 billion to fund acquisitions. Integration challenges remained enormous. Competitors were consolidating too—Eaton acquired Danfoss's hydraulics business, creating a formidable rival. The question facing Jenny Parmentier, who became CEO in 2023, was whether Parker could digest these massive acquisitions while maintaining its entrepreneurial culture and operational excellence.

VII. Business Segments & Operating Model

Walk into Boeing's Everett factory where 787 Dreamliners are assembled, and you'll find a striking sight: Parker-Hannifin employees working alongside Boeing technicians. They're not contractors or consultants—they're embedded partners, responsible for designing, installing, and maintaining hydraulic systems throughout the aircraft's production. This integration exemplifies Parker's modern operating model: not just a supplier of components, but an embedded solution provider across two distinct but synergistic segments.

The Diversified Industrial segment, generating $11.2 billion in fiscal 2024 revenue, spans an almost bewildering array of markets. In automotive manufacturing, Parker provides the pneumatic systems that operate robotic welding arms, the hydraulic presses that stamp body panels, and the filtration systems that maintain paint booth air quality. In agriculture, Parker hydraulics power John Deere combines that can cost $500,000 each—the lifting mechanisms, steering systems, and power transmissions all rely on Parker components. In renewable energy, Parker supplies pitch control systems for wind turbine blades and hydraulic tensioners for offshore platforms.

But here's the strategic insight: these diverse markets share common technologies. A hydraulic cylinder operating a garbage truck compactor uses similar engineering principles to one controlling a jet's landing gear—different specifications, same core competency. This commonality allows Parker to leverage R&D across markets. An innovation in seal materials for semiconductor manufacturing might improve refrigeration systems. A valve design for natural gas processing could enhance hydrogen fuel cells.

The Aerospace Systems segment, contributing $8.7 billion in revenue, operates on different dynamics. Here, Parker isn't just manufacturing parts; they're taking responsibility for entire subsystems. On the Boeing 737 MAX, Parker provides the complete hydraulic system—pumps, filters, cylinders, valves, and control electronics—guaranteed to work together for the aircraft's 30-year life. This systems integration capability commands premium pricing and creates massive switching costs.

The aerospace aftermarket is Parker's crown jewel. Every component installed on an aircraft requires regular replacement—filters every 500 flight hours, seals every 2,000 hours, pumps every 10,000 hours. With 30,000 commercial aircraft flying globally, each averaging 3,000 flight hours annually, the replacement demand is enormous and predictable. Parker maintains detailed databases tracking every component on every aircraft, anticipating replacement needs years in advance.

Military aerospace adds another dimension. Parker components on the F-35 fighter jet aren't just specified by the manufacturer; they're mandated by the Department of Defense. Changing suppliers would require years of requalification testing. These sole-source positions on platforms with 40-year service lives create revenue streams worth billions. The recent Meggitt acquisition added 50+ such sole-source positions.

The organizational structure enabling this complexity is fascinating. Parker operates through nine technology platforms, each a center of excellence: aerospace, climate control, electromechanical, filtration, fluid handling, hydraulics, pneumatics, process control, and sealing & shielding. These aren't rigid divisions but fluid networks. A customer needing a custom actuator might draw on expertise from hydraulics (cylinder design), electromechanical (control systems), and sealing (preventing leakage).

The decentralized operating philosophy remains sacred but has evolved significantly. Division presidents still have broad autonomy—they can approve capital expenditures up to $5 million, hire and fire, set pricing, and develop new products without corporate approval. But they're now connected through sophisticated IT systems providing real-time visibility into global operations. A division president in Germany can see inventory levels in Brazil, production schedules in China, and customer orders in Texas.

This visibility enables Parker's "Win Strategy" execution at granular levels. Every facility tracks key performance indicators daily: on-time delivery, quality defects, inventory turns, and customer satisfaction scores. These metrics roll up to division, group, and corporate levels, creating accountability throughout the organization. Underperforming facilities receive rapid intervention—not punitive, but supportive, with best practices shared from successful operations.

The global manufacturing footprint—300+ facilities across 50 countries—provides crucial advantages. Parker can serve customers locally while optimizing production globally. When Trump's tariffs hit Chinese imports, Parker shifted production between facilities to minimize impact. During COVID-19 lockdowns, the company redistributed orders to operating facilities, maintaining customer deliveries when competitors failed.

The distribution network amplifies these advantages. Beyond 3,000+ ParkerStores, the company maintains relationships with 13,000 independent distributors. These aren't just resellers; they're technical partners trained on Parker products, capable of providing application engineering and emergency service. A mining company in Chile can get Parker expertise through local distributors without Parker maintaining direct operations.

The recent focus on electrification represents the next evolution. Parker's acquisition of Curtis Instruments brought expertise in low-voltage motor controls essential for electric vehicles and industrial automation. The company isn't abandoning hydraulics—electric actuators can't match hydraulic power density for heavy applications. Instead, Parker is developing hybrid systems combining electric efficiency with hydraulic power.

The margin profile reveals the strategy's success. Aerospace Systems generates 25% operating margins through long-term contracts and aftermarket dominance. Diversified Industrial achieves 15% margins despite competitive markets through technical differentiation and service excellence. These margins, exceptional for industrial manufacturing, reflect Parker's evolution from component supplier to solution provider.

Looking ahead, Parker's operating model faces challenges and opportunities. Digital twins—virtual models of physical systems—could revolutionize predictive maintenance. Artificial intelligence might optimize hydraulic system design. Additive manufacturing could enable on-demand production of replacement parts. But the fundamental model—decentralized innovation, standardized quality, embedded customer relationships—remains the sustainable competitive advantage that compounds over decades.

VIII. Current State & Future Vision (2023–Present)

Jenny Parmentier took the CEO reins in January 2023 during what should have been a victory lap. The Meggitt integration was proceeding smoothly. Aerospace orders were soaring as Boeing and Airbus worked through 10,000-plane backlogs. Operating margins had reached record levels. Yet Parmentier, a 33-year Parker veteran who had run both industrial and aerospace divisions, saw vulnerabilities others missed. "We're built for the 20th century economy of moving atoms," she told investors. "We need to prepare for the 21st century economy of moving electrons."

The numbers told a complex story. Fiscal 2024 revenue hit $19.9 billion, but the growth wasn't balanced. Aerospace systems surged 19% organically, driven by commercial aviation's post-COVID recovery and defense modernization programs. But Diversified Industrial declined 2%, pressured by weakness in construction, agriculture, and China. This divergence highlighted Parker's challenge: aerospace was driving profits but industrial provided stability. Could the company maintain leadership in both?

Parmentier's strategic response was counterintuitive. Rather than choosing between aerospace and industrial, she declared Parker would dominate the intersection—what she called "intelligent motion control." This meant embedding sensors, software, and connectivity into traditional mechanical systems. A hydraulic cylinder wouldn't just move; it would report its position, predict its maintenance needs, and optimize its performance through machine learning algorithms.

The Curtis Instruments acquisition in 2023 exemplified this vision. Curtis brought expertise in low-voltage motor controllers essential for electric vehicles, automated guided vehicles, and industrial robots. But more importantly, Curtis understood software—their controllers included sophisticated programming enabling predictive diagnostics and remote monitoring. Parker could now offer customers not just components but complete cyber-physical systems.

The electrification push extended beyond acquisitions. Parker established a $500 million venture fund investing in startups developing electric actuators, hydrogen fuel cells, and energy storage systems. The company partnered with universities on fundamental research into high-temperature superconductors that could revolutionize electric motors. Most ambitiously, Parker announced plans for a $250 million "Factory of the Future" in North Carolina combining traditional manufacturing with AI-driven automation.

But Parmentier's boldest move was organizational. She restructured Parker's operating segments from product-based to customer-based organizations. Instead of hydraulics and pneumatics divisions, Parker now had "Aerospace & Defense," "Industrial Automation," and "Mobile Equipment" groups. Each group combined multiple technologies to provide complete solutions. A construction equipment manufacturer could work with one Parker team providing hydraulics, electronics, filtration, and service support.

The financial strategy matched the operational transformation. Parker announced aggressive targets for fiscal 2029: 27% adjusted operating margins (up from 22%), 13% annual free cash flow growth, and return on invested capital exceeding 20%. These weren't aspirational goals—they were commitments tied to executive compensation. Achieving them required both organic growth and operational excellence.

The capital allocation framework demonstrated this discipline. In fiscal 2025, Parker generated $3.2 billion in operating cash flow. The company invested $800 million in capital expenditures and R&D, paid $800 million in dividends (the 69th consecutive year of increases), and repurchased $1.6 billion in shares. This balanced approach—investing for growth while returning cash to shareholders—reflected confidence in the business model.

The share repurchase program was particularly aggressive. Parker bought back 5% of shares outstanding in fiscal 2025, taking advantage of what management viewed as market undervaluation. At 21x forward earnings, Parker traded at a discount to pure-play aerospace companies despite comparable margins and superior diversification. Parmentier argued the market didn't fully appreciate Parker's transformation from cyclical industrial to recession-resistant technology leader.

Recent operational metrics validated this thesis. The aerospace aftermarket generated 52% of segment revenue with 35% margins and multi-year visibility. Customer retention exceeded 95% across both segments. New product vitality—revenue from products launched in the past five years—reached 30%. These metrics suggested Parker had successfully evolved from mature industrials to innovative solutions provider.

The global footprint continued evolving strategically. Parker announced plans to invest $1 billion in Asian operations over five years, recognizing that region would drive 40% of global industrial growth. But unlike previous expansions focused on low-cost manufacturing, this investment targeted high-value engineering and R&D. Parker's Shanghai technical center would develop products specifically for Asian markets, reversing the traditional model of adapting Western designs.

Sustainability became central to strategy, not just marketing. Parker's components enabled wind turbines, electric vehicles, and hydrogen infrastructure—markets growing 20% annually. The company committed to carbon neutrality by 2040, investing in renewable energy for facilities and developing products reducing customer emissions. A new "EcoDesign" initiative required every new product to demonstrate environmental benefits versus predecessors.

The competitive landscape was intensifying. Eaton's hydraulics acquisition created a formidable rival. Bosch and Continental were investing heavily in electrification. Chinese competitors were moving upmarket with improving quality. But Parker's response wasn't defensive—it was collaborative. The company announced strategic partnerships with Microsoft on industrial IoT, with Honda on electric aircraft, and with major customers on next-generation platforms.

Looking toward fiscal 2029 and beyond, Parmentier articulated a vision of Parker as the "Google of motion control"—not manufacturing commodities but providing intelligence that makes movement more efficient, reliable, and sustainable. Whether that's optimizing hydraulic fracturing to extract cleaner natural gas, enabling electric aircraft to revolutionize regional transportation, or helping robots manufacture products with zero defects, Parker would be the hidden enabler.

The challenges remain substantial. Integrating Meggitt while maintaining entrepreneurial culture. Defending industrial markets from low-cost competition. Investing in new technologies while maintaining current profitability. But as Parmentier reminds investors, Parker has navigated technological transitions before—from pneumatics to hydraulics, from mechanical to electronic controls, from products to solutions. The next transition, from physical to cyber-physical systems, represents not a threat but the next century of opportunity.

IX. Playbook: Business & Investing Lessons

Study Parker-Hannifin's century-long journey, and you'll find lessons that challenge conventional wisdom about industrial companies. This isn't a story of breakthrough innovation or charismatic founders or first-mover advantages. It's something more subtle and powerful: a masterclass in compound excellence, where small advantages accumulate over decades into insurmountable moats.

The Decentralization Paradox

Every MBA program teaches that scale requires centralization—standardized processes, unified command, economies of scale. Parker proves the opposite. By maintaining 300+ profit centers with autonomous decision-making, the company achieves something remarkable: entrepreneurial innovation at massive scale. Division presidents can approve million-dollar investments without corporate approval. Engineers can develop new products without committee oversight. Sales teams can customize solutions without headquarters permission.

But here's the crucial detail: this autonomy operates within iron-clad constraints. Every division must achieve 20% return on assets. Quality standards are non-negotiable. Financial reporting is standardized and transparent. It's like jazz music—infinite improvisation within strict harmonic structure. Competitors trying to copy this model typically fail because they centralize the wrong things (innovation, customer relationships) and decentralize the wrong things (quality standards, financial discipline).

The Power of Unsexy Businesses

Parker manufactures valves, cylinders, filters—components invisible to end users. No consumer will ever post about their Parker hydraulic fitting on Instagram. This invisibility is Parker's superpower. Competitors chase visible, exciting markets—electric vehicles, renewable energy, space exploration. Parker quietly dominates the boring but essential components within those markets.

Consider aircraft brakes—a $2 billion market Parker exited by selling Meggitt's division. Why abandon such a large market? Because brakes are visible, heavily scrutinized, and constantly pressured on price. But the hydraulic actuators that activate those brakes? That's a $200 million market with 50% margins that Parker dominates. The lesson: ownership of critical but invisible components generates superior returns to ownership of visible but commoditized systems.

Strategic M&A as Compound Growth

Parker has completed 77+ acquisitions without a single transformational failure. The secret isn't brilliant deal-making—Parker typically pays fair prices, not bargains. Instead, it's the integration philosophy. Acquired companies maintain their identities, management teams, and cultures. Parker provides capital, distribution, and back-office support. It's like building with Lego blocks—each piece maintains its integrity while contributing to a larger structure.

The CLARCOR acquisition illustrates this perfectly. Parker paid $4.3 billion—a 13x EBITDA multiple that analysts called expensive. But Parker saw what others missed: CLARCOR's filtration technology combined with Parker's hydraulics could create new products neither company could develop alone. Within three years, joint innovations generated $300 million in new revenue. The acquisition wasn't about cost synergies but capability multiplication.

The Dividend Aristocracy Discipline

69 consecutive years of dividend increases—Parker ranks among the top 5 longest streaks in the S&P 500. This isn't just financial trivia; it's organizational DNA. The dividend commitment forces long-term thinking. Management can't sacrifice future cash flow for current earnings. Investment decisions must consider 10-year returns, not quarterly results. Cost cuts can't compromise quality that generates aftermarket revenue decades later.

This discipline cascades throughout the organization. Engineers design products for 30-year lifecycles, not planned obsolescence. Sales teams prioritize customer retention over new account acquisition. Manufacturing invests in preventive maintenance rather than running equipment to failure. The dividend streak isn't just a financial metric—it's a forcing function for sustainable excellence.

Distribution as Competitive Moat

Amazon taught the world that distribution wins. Parker learned this lesson 30 years earlier. The 3,000+ ParkerStore network isn't just sales outlets—they're technical resource centers providing engineering support, emergency service, and customer training. Competitors can copy products but can't replicate this infrastructure.

The moat compounds through network effects. More stores mean more inventory turns, enabling broader product selection. Broader selection attracts more customers, justifying more stores. Higher volumes support more technical specialists, improving service quality. Better service commands premium pricing, funding further expansion. It's a virtuous cycle that took decades to build and would take decades to replicate.

The Aftermarket Annuity

Parker's aerospace aftermarket generates 50% of segment revenue with 35% margins—essentially a subscription business hidden within industrial manufacturing. Every component installed creates 20-30 years of replacement demand. But here's the key: Parker doesn't just wait for orders. The company maintains databases tracking every component on every aircraft, proactively managing inventory and predicting demand.

This predictability enables strategic decisions impossible for cyclical manufacturers. Parker can invest through downturns knowing aftermarket revenue provides stability. The company can accept lower margins on original equipment knowing lifetime value justifies the investment. Most importantly, Parker can plan decades ahead—a massive advantage in industries where competitors think quarter to quarter.

Capital Allocation Excellence

Study Parker's capital allocation and you'll find a mathematical elegance. The company consistently generates 15-20% return on invested capital. It reinvests at those returns until diminishing returns emerge, then returns excess capital to shareholders. No empire building. No transformational moonshots. Just relentless optimization of capital efficiency.

The recent $1.6 billion share repurchase exemplifies this discipline. With shares trading at 21x earnings and the business generating 20% ROIC, buybacks create value mathematically. But Parker doesn't just buy back shares when prices are low—it buys consistently, dollar-cost averaging over cycles. This systematic approach removes emotion and timing risk from capital allocation.

The China Template

Parker entered China in 1985 when most industrials feared intellectual property theft. But Parker's approach was nuanced. The company established manufacturing for local consumption, not export. It partnered with state-owned enterprises, sharing technology in exchange for market access. Most cleverly, Parker localized products for Chinese requirements rather than selling Western designs.

This strategy created interesting dynamics. Chinese competitors could copy Parker's products but couldn't match localized engineering expertise. Government relationships protected market position. Local manufacturing avoided tariffs and currency risks. By the time Western competitors entered China, Parker had insurmountable scale advantages. The lesson: early entry into emerging markets requires cultural adaptation, not just capital investment.

Recession Navigation

Parker has survived 15 recessions since 1917. The playbook never changes: cut costs quickly but never compromise quality, maintain R&D spending, use downturns to acquire weakened competitors, and emerge stronger. The 2008 financial crisis exemplified this. Parker cut 20% of workforce within six months but maintained engineering headcount. The company reduced inventory by $500 million but kept critical safety stock. Most importantly, Parker acquired 10 companies during the downturn at attractive valuations.

This counter-cyclical strategy requires cultural fortitude. Wall Street punishes companies that don't cut deeply enough during recessions. Employees question why competitors are retrenching more aggressively. But Parker's century-long perspective provides confidence. Every recession ends. Companies that maintain capabilities through downturns capture disproportionate share during recoveries.

The Technological Transition Framework

Parker has navigated four major technological transitions: pneumatics to hydraulics (1940s), mechanical to electronic controls (1980s), analog to digital systems (2000s), and now physical to cyber-physical systems (2020s). Each transition could have obsoleted Parker's expertise. Instead, the company emerged stronger.

The pattern is consistent: recognize transitions early through customer relationships, acquire leading-edge capabilities rather than developing internally, integrate new technologies with existing strengths rather than abandoning legacy businesses, and maintain old technologies for customers not ready to transition. This framework explains why Parker still manufactures purely mechanical valves (for nuclear plants that can't risk electronics) while developing AI-powered predictive maintenance systems.

X. Analysis & Bear vs. Bull Case

The investment case for Parker-Hannifin presents a fascinating study in contrasts. Here's a company trading at industrial multiples while generating software-like returns, growing through aerospace recovery while facing industrial headwinds, and pursuing aggressive electrification while defending traditional hydraulics. The bull and bear cases aren't just different—they're interpreting the same facts through completely different lenses.

The Bull Case: Aerospace Supercycle Meets Operational Excellence

The numbers tell a compelling story. Commercial aerospace orders reached 3,410 aircraft in 2023—the highest in history. Boeing and Airbus have combined backlogs exceeding 15,000 planes, representing 10+ years of production. Every aircraft requires $2-5 million in Parker content, creating $30-75 billion in original equipment revenue. But that's just the beginning. Each plane generates 3-4x its original value in aftermarket revenue over a 30-year service life. Parker's aerospace revenue could mathematically triple over the next decade.

The Meggitt acquisition transformed this opportunity. Parker doubled its aerospace content per aircraft, gained sole-source positions on military platforms with 40-year service lives, and achieved critical mass in aerospace systems integration. The company now has leverage to demand higher prices, broader contracts, and exclusive supplier agreements. When Airbus needs hydraulic systems, Parker isn't competing against ten suppliers—it's negotiating as one of three viable partners.

Defense spending adds another catalyst. The Ukraine conflict reminded governments that military readiness requires industrial capacity. The F-35 program alone will produce 3,000+ aircraft over 20 years, each containing $500,000 in Parker content plus lifetime services. Defense budgets are increasing globally, modernization programs are accelerating, and Parker's cleared facilities and security certifications create barriers to competition.

The industrial transformation is equally promising but less obvious. Parker's shift from products to solutions changes unit economics fundamentally. Selling a $1,000 hydraulic cylinder generates 15% gross margins. Selling a $50,000 integrated motion control system with sensors, software, and service contracts generates 40% margins. As industrial customers demand more sophisticated automation, Parker's revenue per customer should expand dramatically.

Electrification represents optionality, not risk. Parker isn't betting everything on electric actuators replacing hydraulics. The company is positioning for hybrid systems—electric controls with hydraulic power—that combine the best of both technologies. Early applications in electric aircraft and autonomous vehicles could create billion-dollar markets where Parker has first-mover advantages.

The financial framework supports aggressive returns. Parker generates $3+ billion in annual free cash flow against a $65 billion market capitalization—a 5% yield. The company is buying back 5% of shares annually. Dividends yield 1.5% and grow high single digits. Combined, shareholders receive 11-12% annual returns before any earnings growth. Add modest 5% earnings growth from aerospace recovery and margin expansion, and total returns could reach 15-17% annually.

Margin expansion provides the real upside. Parker targets 27% operating margins by fiscal 2029, up from 22% today. This isn't fantasy—aerospace peers achieve 30% margins, and Parker's aftermarket mix is improving. Each 100 basis points of margin expansion adds $200 million in operating income. Achieving targets would increase earnings by 40% even with flat revenue.

Valuation remains undemanding despite quality improvements. At 21x forward earnings, Parker trades at discounts to pure-play aerospace companies like TransDigm (28x) and HEICO (35x) despite similar business models. Industrial comparables like Eaton and Emerson trade at similar multiples with inferior growth and margins. As Parker's aerospace transformation becomes evident, multiple expansion to 25x seems reasonable, providing 20% upside beyond earnings growth.

The Bear Case: Cyclical Pressures Meet Integration Risks

The industrial slowdown is worse than headlines suggest. Parker's Diversified Industrial segment declined 2% organically in fiscal 2024, but key end markets fell much further. Construction equipment dropped 15%. Agricultural machinery declined 20%. China, representing 10% of revenue, contracted despite stimulus measures. These aren't temporary disruptions—they reflect structural challenges from overbuilding, debt deleveraging, and deglobalization.

The aerospace celebration ignores mounting risks. Yes, backlogs are massive, but production rates remain below pre-COVID levels. Boeing's quality crisis following the 737 MAX door plug incident could constrain deliveries for years. Supply chain disruptions make announced production rates fantasy. Most concerningly, airline profitability is deteriorating as capacity returns faster than demand. When airlines struggle, aircraft orders evaporate—history proves this repeatedly.

The Meggitt integration carries hidden dangers. Parker paid $9.7 billion—a 30x EBITDA multiple after adjusting for disposals. Achieving promised synergies requires eliminating thousands of jobs, risking labor disputes and knowledge loss. Cultural integration between American and British organizations historically proves challenging. Meanwhile, competitors are using integration disruption to poach customers and employees.

Technological disruption threatens core markets. Electric actuators are replacing hydraulics in many applications—not tomorrow, but inevitably. Tesla's Model S uses electric motors for functions traditionally requiring hydraulics. Autonomous vehicles eliminate power steering and braking hydraulics. Wind turbines are shifting from hydraulic to electric pitch control. Parker's hydraulics expertise, built over a century, could become obsolete within decades.

The balance sheet constraints flexibility. Net debt reached $10 billion after Meggitt, pushing leverage to 3x EBITDA. Interest expense increased to $400 million annually. Credit rating agencies warn that further acquisitions could trigger downgrades. Meanwhile, capital expenditure requirements are rising as customers demand localized production and advanced manufacturing. Parker must simultaneously deleverage, invest, and return cash to shareholders—mathematical impossibility during downturns.

Competition is intensifying globally. Chinese manufacturers like Hengli Hydraulics are moving upmarket with 70% lower costs. European competitors benefit from government subsidies for electrification. Digital natives like Tesla and Rivian are vertically integrating, designing their own motion control systems. Parker's competitive advantages—distribution, quality, relationships—matter less when purchasing decisions shift from engineers to algorithms.

The earnings quality deserves scrutiny. Parker's adjusted earnings exclude significant items every quarter—restructuring charges, acquisition costs, pension adjustments. The gap between GAAP and adjusted earnings averaged $200 million annually. Free cash flow conversion is deteriorating as working capital requirements increase. The vaunted aftermarket business requires massive inventory investment that doesn't appear in earnings but constrains cash flow.

Management incentives create agency risks. Executive compensation ties to adjusted EPS and revenue growth, encouraging acquisitions regardless of returns. The board lacks industrial expertise—mostly former CEOs of unrelated companies. Insider ownership is minimal, reducing alignment with shareholders. The aggressive buyback program benefits executives with stock options more than long-term shareholders.

Macro headwinds compound challenges. Industrial reshoring sounds positive but requires massive capital investment with uncertain returns. Inflation in skilled labor—machinists, engineers, technicians—pressures margins. Environmental regulations require expensive equipment retrofits. Trade tensions create tariff uncertainties. These aren't temporary factors but structural changes to industrial economics.

The Synthesis: Path Dependency and Optionality

The reality likely lies between extremes. Parker isn't becoming the next TransDigm (aerospace rollup with monopolistic pricing) or the next GE (diversified industrial destroyed by complexity). Instead, Parker represents something rarer: a competently managed industrial company with genuine competitive advantages navigating technological transition.

The key insight is path dependency. Parker's future depends less on macro conditions than strategic execution. If management successfully integrates Meggitt, captures aerospace recovery, and navigates electrification, the bull case materializes. If integration stumbles, aerospace disappoints, or technology shifts accelerate, the bear case emerges. This isn't random—it's determined by thousands of daily decisions across the organization.

For investors, Parker offers asymmetric optionality. Downside seems limited given reasonable valuation, strong balance sheet, and diversified revenue. Upside could be substantial if aerospace accelerates and margins expand. The dividend provides downside protection while waiting for clarity. The buyback creates value if execution succeeds.

The proper framework isn't bull versus bear but probability-weighted scenarios. Assign 60% probability to muddling through—modest growth, stable margins, market returns. 30% probability to the bull case—aerospace boom, margin expansion, multiple re-rating. 10% probability to the bear case—recession, technology disruption, value destruction. The expected value remains positive, but investors must size positions appropriately for the uncertainty.

XI. Epilogue & Final Thoughts

There's a bronze plaque in Parker-Hannifin's Mayfield Heights headquarters that most visitors walk past without noticing. It doesn't commemorate a merger or celebrate a sales milestone. Instead, it bears Arthur Parker's simple words from 1924: "We will make the best products we know how, sell them at fair prices, and deal honestly with all people." Nearly a century later, in an era of algorithmic trading and quarterly capitalism, this philosophy seems almost quaint. Yet it might be Parker's greatest competitive advantage.

The remarkable story of Parker-Hannifin isn't really about hydraulics or aerospace or industrial technology. It's about the compounding power of consistency. While competitors pursued transformational strategies—GE's finance adventures, United Technologies' conglomerate empire, Honeywell's software pivot—Parker stayed boring. Relentlessly, persistently, profitably boring. The company that failed at its original mission of truck brakes succeeded by never again trying to revolutionize anything, instead making everything incrementally better, forever.

Consider what Parker has survived: the Great Depression, World War II, the Cold War's end, the dot-com bubble, the financial crisis, the COVID pandemic. Through each disruption, analysts predicted obsolescence. Hydraulics would yield to electronics. American manufacturing would succumb to Asian competition. Industrial companies would be disintermediated by digital platforms. Yet Parker didn't just survive—it thrived, generating returns that embarrassed supposedly superior business models.

The secret lies in understanding what actually creates industrial value. It's not breakthrough innovation—most revolutionary technologies fail commercially. It's not first-mover advantage—pioneers often become casualties. It's not even scale—size without purpose becomes bureaucracy. Instead, industrial value comes from solving thousands of mundane problems reliably. When a hydraulic seal fails on an oil rig, shutting down production costing $1 million daily, the customer doesn't want innovation—they want a replacement seal that works, delivered immediately, guaranteed not to fail again.

Parker built an empire on this insight. Every acquisition, every new facility, every product line extension served the same purpose: being wherever customers needed motion control solutions, with whatever technology they required, faster than any competitor. It's a strategy so simple it seems obvious, yet so difficult that no competitor has successfully replicated it at scale.

The human element deserves recognition. From Art Parker betting his life savings after failure, to Helen Parker wagering her husband's life insurance, to Patrick Parker choosing diversification over focus, to Don Washkewicz retiring at 65 as promised, to Jenny Parmentier reimagining the company for electrification—leadership mattered. But not in the charismatic, visionary sense celebrated in business media. Parker's leaders were engineers and operators who understood that sustainable success comes from empowering thousands of employees to make millions of small improvements.

This cultural philosophy—"fair dealing, hard work, coordination of effort, and quality products"—sounds like corporate pablum. But spend time in Parker facilities and you'll find it's operational reality. Engineers genuinely obsess about seal materials. Sales representatives actually know their customers' businesses. Factory workers take pride in quality metrics. It's not cultish devotion but professional craftsmanship, enabled by decentralized structure and aligned incentives.

The broader lesson for founders and investors is profound. In an era obsessed with disruption, Parker proves the value of persistence. While venture capitalists chase unicorns, Parker generated more wealth through steady compounding. While consultants preach transformation, Parker succeeded through evolution. While markets reward quarterly beats, Parker optimized for decades.

This doesn't mean avoiding change—Parker transformed dramatically from pneumatics to hydraulics to electronics to cyber-physical systems. But each transformation built on previous capabilities rather than abandoning them. Parker still manufactures mechanical valves designed in the 1950s because nuclear power plants need proven reliability. The company also develops AI-powered predictive maintenance systems for next-generation aircraft. It's not either/or but both/and, serving customers wherever they are on the technology adoption curve.

Looking forward, Parker faces its most complex transition yet. The shift from mechanical to digital, from products to services, from industrial to technology company requires capabilities beyond engineering excellence. Software development operates on different timescales than manufacturing. Data scientists think differently than mechanical engineers. Venture-backed startups compete with different economics than established manufacturers.

Yet Parker's history suggests successful navigation. The company has reinvented itself every generation while maintaining core identity. The specifics change—pneumatics to hydraulics, analog to digital—but the essence remains: helping customers move, control, and filter fluids and gases more efficiently. Whether that's through traditional hydraulic cylinders or AI-optimized electric actuators matters less than solving customer problems profitably.

The ultimate test will be whether Parker can maintain its cultural advantages at massive scale. With 60,000 employees across 50 countries, preserving entrepreneurial spirit and operational excellence becomes exponentially harder. The temptation to centralize, standardize, and bureaucratize is immense. But if Parker's history teaches anything, it's that the companies that survive centuries are those that resist institutional sclerosis.

For investors, Parker represents a fascinating thought experiment. In a market that prices growth over profitability, momentum over stability, and narrative over numbers, how should one value a company that compounds steadily for decades? The answer depends on time horizon. For traders seeking quick gains, Parker offers little excitement. For investors building generational wealth, Parker exemplifies the boring companies that generate extraordinary long-term returns.

The final insight might be the most important: Parker touches you in every part of your life whether you realize it or not. The plane that brings you home, the car that drives you to work, the equipment that manufactures your phone, the systems that purify your water—all rely on Parker components. This ubiquity isn't accident but intention, the result of a century-long mission to be wherever motion and control matter.

Arthur Parker's failed truck brake company became a $20 billion industrial giant not through grand strategy but daily execution, not through revolution but evolution, not through genius but persistence. In a business world obsessed with disruption, Parker-Hannifin stands as testament to the enduring power of simply making things that work, selling them at fair prices, and dealing honestly with all people. Sometimes the oldest ideas remain the best.

XII. Recent NewsBased on my research, here's the Recent News section for Parker-Hannifin:

XII. Recent News

Fiscal 2025 Second Quarter Results Demonstrate Operational Excellence

Parker reported strong Q2 fiscal 2025 results in January 2025, delivering record segment operating margin across all businesses, record earnings per share, and year-to-date cash flow from operations increasing 24% to $1.7 billion. The company used strong cash flow coupled with proceeds from previously announced divestitures to substantially reduce debt by $1.1 billion during the quarter. Despite challenging industrial markets, the company maintained guidance for fiscal 2025 with organic sales growth of approximately 2%, total segment operating margin of approximately 22.7% (25.8% adjusted), and EPS of $24.46 to $25.06 ($26.40 to $27.00 adjusted).

Curtis Instruments Acquisition: Doubling Down on Electrification

In June 2025, Parker announced its agreement to acquire Curtis Instruments from Rehlko for approximately $1 billion in cash. Curtis designs and manufactures control system components for electric and hybrid vehicles, with projected 2025 revenue of $320 million. CEO Jenny Parmentier emphasized that "Curtis adds complementary technologies to our existing industrial electrification platform, better positioning us to serve our customers as they continue the adoption of more electric and hybrid solutions." The transaction is expected to close by the end of 2025, pending regulatory approval.

This acquisition marks Parker's most significant electrification move since establishing its venture fund. Curtis operates from more than 450,000 square feet of production space across facilities in New York and California, Switzerland, the United Kingdom, China, Germany, and India. The global footprint and established customer relationships in electric vehicle markets provide Parker immediate access to high-growth segments without the typical development timeline.

Portfolio Optimization Through Strategic Divestitures

Parker completed the divestiture of its North America Composites and Fuel Containment (CFC) Division to SK Capital Partners in November 2024. The division, which generated annual sales of approximately $350 million and operated six manufacturing locations across the U.S. and Mexico, became part of Parker following the Meggitt acquisition in 2022.

Parker has successfully divested businesses and product lines over the past three years totaling nearly $450 million in annual sales, including the France Electromechanical Solutions Division, MicroStrain Division, Filter Resources Division, the Calzoni product line, the Industrial Profile Systems product line, and the Indego exoskeleton product line. These divestitures reflect Parker's disciplined approach to portfolio management, focusing resources on higher-margin, technology-differentiated businesses.

Aerospace Strength Offsetting Industrial Weakness

In Q1 fiscal 2025, Parker delivered record sales, adjusted segment operating margin, and adjusted earnings per share. CEO Jenny Parmentier noted the performance "reflects the strength of our transformed portfolio with our Aerospace Systems segment achieving exceptional results." The Aerospace Systems segment achieved record adjusted operating margins of 25.3% in Q4 fiscal 2024, increasing 130 basis points year-over-year.

The aerospace outperformance comes as commercial aviation continues its post-pandemic recovery. With Boeing and Airbus working through massive backlogs despite production challenges, Parker's content per aircraft and aftermarket exposure positions it well for sustained growth. The recent Meggitt integration has exceeded synergy targets, with guidance now reflecting expected divestiture activity while maintaining organic sales growth targets of 1.5% to 4.5% for fiscal 2025.

Capital Allocation Balancing Growth and Returns

Parker's Board declared a regular quarterly dividend of $1.63 per share in January 2025, marking the company's 299th consecutive quarterly dividend. The approaching 300th consecutive dividend payment—a 75-year achievement—places Parker among an elite group of American corporations demonstrating multi-generational financial stability.

Simultaneously, the company continues aggressive share repurchases. The fiscal 2025 capital allocation strategy balances investing in high-return projects like the Curtis acquisition, reducing debt from the Meggitt acquisition, maintaining the dividend aristocrat status, and opportunistically buying back shares at what management views as attractive valuations.

Margin Expansion Despite Mixed Markets

The most impressive recent development is Parker's ability to expand margins despite industrial headwinds. Q2 fiscal 2025 saw segment operating margin reach 22.1%, an increase of 100 basis points year-over-year, or 25.6% adjusted. This margin expansion during a period of industrial weakness demonstrates the effectiveness of Parker's operational excellence initiatives and portfolio transformation toward higher-value solutions.

Looking Ahead: FY29 Targets Signal Confidence

Parker's fiscal 2029 targets include total segment operating margin of 22.1% to 22.5% (25.2% to 25.6% adjusted) and strong earnings growth. These targets, while appearing conservative given recent performance, reflect management's confidence in sustaining current profitability levels while investing in growth initiatives. The Curtis acquisition, continued aerospace recovery, and industrial electrification trends provide multiple pathways to achieving these goals.