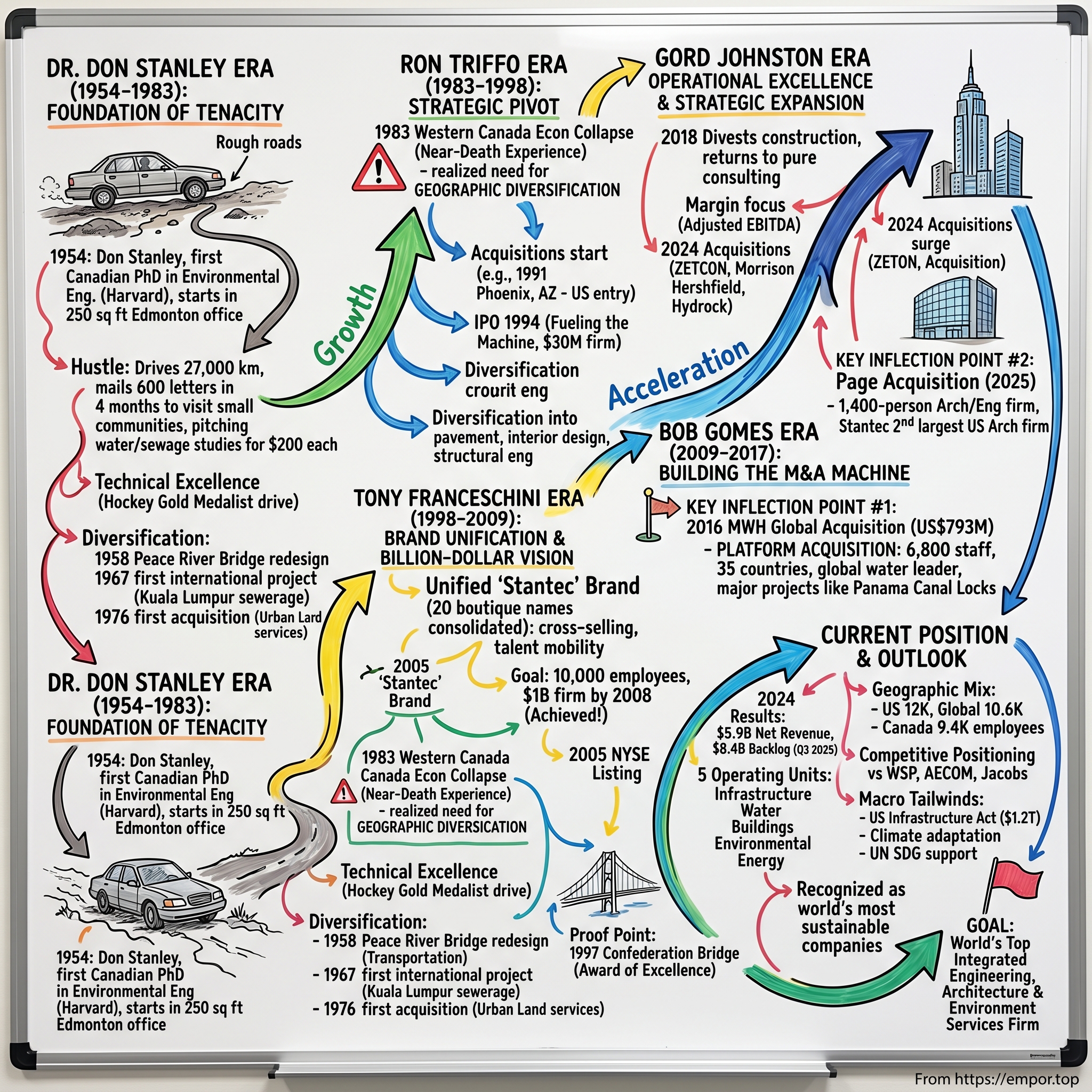

Stantec: From Edmonton Engineer to Global Infrastructure Powerhouse

The Dr. Don Stanley Era: Foundation of Tenacity (1954–1983)

The Founder's Hustle

Don Stanley was the first Canadian to earn a Ph.D. in environmental engineering. Attending Harvard University on a Rockefeller Foundation scholarship, he earned his doctorate in 1952 and two years later founded D.R. Stanley & Associates, working as the sole proprietor out of a 250-square-foot office in Edmonton, Alberta.

What makes Stanley's origin story remarkable isn't just his credentials—it's his willingness to get his hands dirty. This wasn't an academic retreating to a consulting tower; this was a man who understood that in the early days of any professional services firm, the founder must be the rainmaker, the doer, and the administrator all at once. In search of work, Dr. Stanley sent out 600 letters and drove 27,000 kilometres (17,000 miles) in four months visiting small communities in western Canada.

There's a revealing detail buried in the company's archives: "I waited for the business to come in, and it didn't," Stantec's 50th anniversary book quotes Stanley saying. "Then I went out and visited these people. Several times I put on 700 miles in a day." His tenacity started earning actual returns when initial clients agreed to pay $200 for water and sewage feasibility studies. He developed innovative, low-cost solutions that smaller communities could afford. The strategy worked.

Stanley's background is worth lingering on because it established the cultural DNA that persists today. Here was a man who had won a gold medal at the 1950 World Ice Hockey Championships as a member of the Edmonton Mercurys—he was even offered a contract with the Boston Bruins, but turned the team down to pursue his engineering career. That same competitive drive, the willingness to sacrifice easier paths for a harder but more meaningful pursuit, defined the firm's early character.

Building Beyond Water and Sewage

The first decade saw steady but deliberate expansion. Stanley's initial expertise was in water and sewerage—the essential infrastructure that small rural municipalities desperately needed in postwar Canada. But from the beginning, he showed an appetite for diversification that would become the firm's hallmark.

By 1958, the firm gained prominence through redesigning the Peace River Bridge on the Alaska Highway, which enhanced its reputation in bridge and transportation engineering. Operations expanded geographically, with projects extending from Alberta into British Columbia, and the workforce grew to nearly 30 employees by 1963.

In 1967, with close to 50 employees, the Company obtained its first international project—a sewerage system for Kuala Lumpur, Malaysia. Other international projects soon followed, including the installation and rehabilitation of water systems in Jamaica.

This early international work is significant. While the firm remained predominantly Western Canadian in focus, Stanley was already demonstrating that the company's technical capabilities could translate across borders. The Malaysia project, in particular, showed that Stantec's approach to solving water infrastructure problems was portable—a crucial insight that would pay dividends decades later.

In the 1970s, Stantec continued organic growth and completed its first acquisition in 1976, targeting urban land services, while adding five regional branch offices across Western Canada to extend its municipal engineering footprint.

That 1976 acquisition—the first of over 130 to follow—was a modest transaction by any measure. But it established an important principle: growth could come not just from organic expansion but from absorbing complementary capabilities. Stanley was building a playbook that his successors would execute at dramatically larger scale.

By the end of the 1970s, the firm had grown to approximately 400 employees, had worked on ambitious development projects, including the transformation of Fort McMurray from sleepy frontier town to bustling petropolis.

For Investors: The Foundation Matters

The Stanley era established three critical elements that continue to drive value creation today:

-

Technical excellence as competitive moat: Stanley's Harvard credentials and pioneering work in environmental engineering gave the firm credibility that attracted both clients and talent.

-

The diversification imperative: From water to bridges to transportation to land development, the firm consistently expanded its service lines—reducing dependence on any single sector.

-

Acquisition as growth lever: The 1976 acquisition planted a seed that would grow into one of the industry's most prolific M&A machines.

The 1983 Crisis & Ron Triffo's Strategic Pivot (1983–1998)

The Near-Death Experience

Every great company has at least one near-death experience that shapes its character. For Stantec, that moment came in 1983, when Western Canada's economy collapsed.

When the economy in western Canada took a downturn in 1983, staff reductions were necessary, and the Company implemented a major strategic redirection. The Company survived because of geographic and practice diversification. This was also a time of organizational transition. In 1983, Ron Triffo was appointed president, and Dr. Don Stanley became chairman and chief executive officer.

The 1983 crisis revealed a fundamental vulnerability: despite all the service line expansion, Stantec remained dangerously concentrated in a single regional economy. When Alberta's oil-dependent economy cratered, the firm's revenue followed. Staff cuts ensued—painful decisions for a firm that prided itself on its people-centric culture.

But crisis creates clarity. The lesson was unmistakable: geographic diversification wasn't optional; it was existential.

Ron Triffo: The Diversification Architect

Ron Triffo joined the firm in the 1970s and became Don Stanley's second-in-command, taking on the role of President and Chief Operating Officer in 1983. He championed diversification at a time when over-reliance on the Western Canadian market made the company vulnerable. Under his guidance, Stantec broadened its service lines beyond civil engineering and initiated its long-running practice of growth through acquisition. Triffo's strategic vision laid the groundwork for Stantec to become a multidisciplinary, geographically diversified firm.

Triffo understood something critical: in professional services, scale matters not just for efficiency but for resilience. A larger, more diversified firm could weather regional downturns by shifting resources to healthier markets. It could pursue larger, more complex projects that demanded multidisciplinary expertise. And it could attract and retain top talent by offering more varied career paths.

The decade of 1984 to 1993 saw the continued diversification of the Company's services and geographic locations. For example, it added pavement management, interior design, and structural engineering to develop bridges and sports facilities, thereby creating work with new clients and offering an increased number of services to existing clients. The Company also completed its first US acquisition in Phoenix, Arizona, in 1991.

That 1991 Phoenix acquisition marked a watershed moment. For the first time, Stantec had a permanent presence south of the border—establishing a beachhead in what would eventually become its largest market. The US expansion wasn't just about pursuing larger clients; it was about accessing a more diverse economic base that wouldn't correlate perfectly with Canadian cycles.

Going Public: Fueling the Machine

In 1994, the Company was listed on the Toronto Stock Exchange. The Company began the decade with more than 800 employees.

The IPO provided two crucial resources: capital for acquisitions and currency (in the form of publicly traded shares) for deals. It also imposed a discipline of public reporting and governance that forced management to articulate strategy clearly and execute consistently.

After almost 30 years of building the business, Don Stanley handed the reins to Ron Triffo, who diversified it and took it public, a $30-million firm in 1994.

A $30 million firm going public might seem modest by today's standards. But it set the stage for everything that followed—providing the platform for an acquisition engine that would drive a 200x revenue increase over the next three decades.

For Investors: The Diversification Imperative

The Triffo era established the strategic framework that guides Stantec to this day:

- Geographic diversification as insurance: Never again would the firm be held hostage to a single regional economy.

- Service diversification as growth driver: Each new capability created cross-selling opportunities and attracted different client segments.

- The US as growth market: The 1991 Phoenix acquisition proved that Stantec's model could translate across the border.

- Public markets as accelerant: Access to equity capital and publicly traded shares enabled larger, more transformative acquisitions.

The Tony Franceschini Era: Brand Unification & Billion-Dollar Vision (1998–2009)

A Bold New Vision

In 1998, Triffo stepped into the role of board chair, where he remained until retiring in 2011. Tony Franceschini, then vice president of the Commercial/Institutional sector and a board member, became president and CEO. Franceschini began his career with a consulting engineering firm in Toronto, Ontario in 1975 after graduating from the University of Waterloo with a degree in civil engineering, where he worked with Triffo. The year Franceschini became president and CEO, Stantec had 2,000 employees in 40 offices and reported $185.5 million in gross revenue. "Our vision is to grow the company into a 10,000 employee, billion-dollar firm by 2008," Franceschini said.

Let that sink in: Franceschini was committing to 5x growth in a decade. In professional services—where growth is constrained by talent acquisition and integration challenges—this was an audacious target. And yet, by 2008, Stantec had achieved Franceschini's vision of becoming a billion-dollar company with over 10,000 employees worldwide.

How did he do it? Through two transformative moves: brand unification and aggressive US expansion.

The Stantec Brand Revolution

When Franceschini took the helm, the company operated as a loose confederation of boutique firms. Following the success of various acquisitions, Stanley Associates' various practices operated under boutique names, with as many as 20 different companies. By the early 1990s, the companies were placed under the umbrella of Stanley Technology Group, and most subsidiaries featured the name Stanley in their name.

This fragmented structure had served the company well during its regional phase—local brands had local credibility. But it was a liability for a firm aspiring to compete nationally and internationally.

Franceschini was instrumental in launching the new global, single-brand identity, Stantec, which enabled the company's services to be delivered through an integrated approach. "The move was a major achievement –– in a two-month period, we sought and received shareholder approval to change the name of over 30 companies."

Before 1998, Stantec operated under various boutique names like Stanley Technology Group. Adopting the single, global 'Stantec' brand, championed by then-CEO Tony Franceschini, was a huge move. It allowed the company to present its diverse services—from engineering to architecture—as an integrated offering, which is a key competitive advantage today.

The rebranding accomplished several things simultaneously:

-

Unified client experience: A hospital system in Houston could now engage "Stantec" for engineering, architecture, and environmental services—not three different firms with confusing relationships.

-

Cross-selling enabled: With a single brand, staff could more easily refer work across service lines. The architect who landed a hospital project could bring in Stantec's transportation engineers to design the parking infrastructure.

-

Talent mobility: Employees could now move between offices and service lines while maintaining a consistent professional identity.

-

M&A integration accelerated: New acquisitions would be rebranded as Stantec, eliminating the fragmentation that plagued many serial acquirers.

US Expansion & NYSE Listing

Stantec was listed on the New York Stock Exchange in 2005.

The NYSE listing wasn't just about accessing US capital markets—though that mattered. It was a signal to US clients and potential acquisition targets that Stantec was a serious, permanent player in the American market. For a professional services firm competing against giants like AECOM and Jacobs, credibility matters enormously.

The addition of Keith Cos. would create a combined company with $658-million in revenue, within striking distance of top-10 status. The deal would also give Stantec a solid base in the United States.

The Confederation Bridge: A Proof Point

In 1997, the Company made history with the completion of the Confederation Bridge.

The multi-award-winning 12.9 km bridge, which saw 6,000 employees and sub-contractors cross the gates during the four-year construction period, was designed by a consortium headed by a joint venture of J. Mueller International and Stantec (then SLG Consulting).

"The main challenge facing the design team was to demonstrate that the design could meet the requirement that it last 100 years, or twice the average bridge life span," said Eric Tromposch, vice-president at Stantec and one of the design engineers on the project. "Our concept was to prefabricate the components on land using high-strength concrete and put them in place with a crane."

The Confederation Bridge—at 13 kilometres, the world's longest bridge over ice-covered waters, completed in 1997, with Stantec in joint venture providing civil and structural engineering services—represented exactly the kind of marquee project that Franceschini wanted Stantec to win. The bridge was later recognized by the International Federation of Consulting Engineers (FIDIC) with an Award of Excellence for a major civil engineering project of the last 100 years.

For Investors: Brand as Competitive Moat

The Franceschini era delivered several strategic insights:

- Brand unification creates operating leverage: A single brand enables cross-selling, talent mobility, and faster acquisition integration—all of which drive margin expansion.

- Public market visibility matters: The NYSE listing wasn't just about capital access; it signaled permanence and credibility to US stakeholders.

- Marquee projects build reputation: The Confederation Bridge demonstrated capabilities that attracted increasingly complex and valuable work.

- Audacious targets can be achieved: Franceschini's billion-dollar vision seemed impossible in 1998—and became reality in 2008.

The Bob Gomes Era: Building the M&A Machine (2009–2017)

Continuity & Acceleration

Franceschini retired in May 2009. Bob Gomes was appointed president and CEO. Like Stantec's previous three presidents, Gomes is a licensed engineer who earned his degree in civil engineering from the University of Alberta and joined Stantec in 1988.

The continuity in leadership is worth noting. Stantec has been led by just five CEOs in seven decades—all engineers, all promoted from within. This consistency has enabled long-term strategic thinking that would be impossible under the revolving-door leadership common at many public companies.

Between 2008 and 2011, gross revenue increased from $1.4 billion to $1.7 billion, the Stantec team grew from 8,000 staff to over 12,000 staff, the company acquired 16 firms, and strengthened its presence in markets across North America and internationally.

The Gomes playbook was straightforward: continue the acquisition engine, but with increasing discipline around integration and returns. The financial crisis of 2008–2009 tested this approach—but also created opportunities as distressed competitors became acquisition targets.

Recognizing the Limits of North American Focus

By the mid-2010s, a challenge emerged: the pipeline of suitable North American acquisition targets was thinning. The firms that fit Stantec's criteria—strong local market positions, complementary capabilities, cultural alignment—were either already acquired or not for sale.

Fourth came Bob Gomes, who got Stantec through the aftermath of the financial crisis and then, in 2015, with growth prospects in North America dimming, thought it was time to take a big leap.

This recognition led to the most transformative decision in Stantec's modern history: the pursuit of MWH Global.

Key Inflection Point #1: The MWH Global Acquisition (2016)

The Deal That Changed Everything

In 2016, 40 years after completing its first acquisition, Stantec completed its largest-ever acquisition: MWH Global, a 6,800-person engineering, consulting, and construction management firm.

Canadian design firm Stantec Inc. acquired engineering, consulting and construction management group MWH Global Inc. for a purchase price of about US$793 million.

Let's put this in context: this wasn't just adding another regional firm—this was acquiring a global platform in one fell swoop. MWH was headquartered in Broomfield, a suburb of the Denver metropolitan area, with operations in 35 countries. As of May 2015, MWH Global had a global staff of approximately 7,000 employees.

Why MWH Mattered

Stantec announced that it had completed the acquisition of Broomfield, Colorado-based MWH Global, Inc., a 6,800-person engineering, consulting and construction management firm focused on water and natural resources for built infrastructure and the environment. With award-winning project work and 187 offices distributed across 26 countries, the Acquisition expands Stantec's position as a global leader in water resources infrastructure while gaining presence in key geographies, including the United Kingdom, Australia, New Zealand, South and Central America, Europe and the Middle East.

The strategic logic was compelling on multiple dimensions:

1. Water as Mega-Trend: This was the moment Stantec truly went global in water infrastructure. The $1.04 billion CAD deal instantly added 6,800 employees and positioned the company as a leader in a business line that is now a critical global focus: water and environmental services.

2. Geographic Diversification: The acquisition was aimed at increasing the global reach of the until-now predominantly North American focused company.

3. Marquee Project Credentials: MWH had supported some of the world's most technically challenging water and natural resource infrastructure projects, including: Serving as the lead designer on the Panama Canal Third Set of Locks Project. Providing asset management, design and construction strategies as part of an alliance of industry-leading organizations for the Thames Water Asset Management Programme 6 in the United Kingdom.

4. Construction Management Capabilities: MWH brings capabilities that are new to Stantec, including its Engineering and Technical Services group, which provides water-related design services to hydropower, oil and gas, mining and industrial clients. MWH further contributes construction management, program management, and management consulting business services related to water infrastructure.

The Integration Challenge

The MWH shareholders voted overwhelmingly in favor of the Acquisition. 97% of the issued and outstanding MWH shares were voted, and the vote was 99.7% in favor of approving the Acquisition.

Executive leaders from Stantec and MWH are working together to develop an integration strategy that identifies and leverages the firms' combined strengths. In combination, Stantec will have approximately 22,000 team members distributed across more than 400 offices located around the world.

The near-unanimous shareholder approval was telling: MWH's employee-owners saw value in joining a larger platform with Stantec's capital resources and operational discipline.

For Investors: Transformational M&A as Value Driver

The MWH deal illustrates several principles for evaluating acquisition-heavy business models:

- Platform acquisitions vs. tuck-ins: MWH wasn't a small tuck-in; it was a platform that enabled an entirely new strategic direction—global water leadership.

- Cultural alignment matters: The 99.7% shareholder approval suggests strong cultural fit and management confidence.

- Integration risk is real: Stantec divested MWH's construction business in 2018, returning to its consulting-focused roots—a reminder that not every acquired capability fits the long-term strategy.

- Water as a thematic bet: The focus on water infrastructure positioned Stantec for the climate-driven investment wave that would accelerate in the 2020s.

The Gord Johnston Era: Operational Excellence & Strategic Expansion (2018–Present)

The Fifth CEO

In January 2018, Gord Johnston became CEO of Stantec. Johnston has 30 years of private and public sector experience in the design and project management of infrastructure projects. Johnston has bachelor of science and master of engineering degrees in civil engineering from the University of Alberta, and is a registered professional engineer, certified project management professional, and Envision Sustainability Professional.

It's rare to be able to say of a company as old as Stantec, and as big—with 34,000 employees in 450 offices flung across dozens of cities in the U.K. and Australia, along with Milan, Brussels, Lima, Taipei, Dubai and more—that it's just now coming into its own. But how else would you put it? Since Gord Johnston took over as CEO at the beginning of 2018, Stantec's market cap has risen from roughly $4 billion to nearly $18 billion. From a low of less than $28 in 2019, its share price has grown a staggering 450%. The company took about six decades to build its annual net revenue to $3.4 billion, and over Johnston's term, that number has almost doubled, to about $6 billion in 2024, while its adjusted EBITDA has nearly tripled, to $980 million.

Continued Acquisition Discipline

In 2018, Gord Johnston became Stantec's fifth president and chief executive officer. That same year, the Company completed the divestiture of its construction business, returning to its consulting roots as a pure design firm. The Company continued to grow its global presence outside North America with acquisitions in Australia, New Zealand, and the United Kingdom.

The divestiture of MWH's construction business is worth highlighting. It would have been easy to justify keeping these higher-revenue but lower-margin operations. Instead, Johnston made the disciplined decision to focus on Stantec's core competency: design and consulting. This improved margins and reduced project execution risk—a tradeoff that has proven wise.

The 2024 Acquisition Surge

We continued to be disciplined in our capital allocation strategy by prioritizing the deployment of capital towards investments in strategic acquisitions, which aggregated to $672 million, and returned capital to shareholders through dividends of $96 million. We completed the acquisitions of ZETCON Engineering (ZETCON), Morrison Hershfield Group Inc. (Morrison Hershfield), and Hydrock Holdings Limited (Hydrock), which added 2,745 employees to our organization and expanded our North America and Global footprints with new and complementary services offerings.

The Page Acquisition: Becoming an Architecture Powerhouse

Stantec, a global leader in sustainable design and engineering, has signed a definitive purchase agreement to acquire Page, a 1,400-person architecture and engineering firm headquartered in Washington, DC.

On August 4, 2025, Stantec closed its previously announced acquisition of Page. With the addition of Page, Stantec's US Buildings practice grows by nearly 35 percent and the Company's overall US employee headcount expands to approximately 13,500 people. The acquisition positions Stantec as the second largest architecture firm in the US and strengthens its place as the largest integrated engineering and architecture firm in North America.

Page was founded in 1898 in Texas. The combination of Stantec's engineering depth with Page's 127-year architectural heritage creates a formidable integrated offering.

The acquisition will deepen Stantec's expertise and resources in key growth areas such as advanced manufacturing, data centers, and healthcare, while adding new capabilities in cleanroom design and fabrication facilities.

For Investors: The Current Strategic Position

Johnston's era has delivered:

- Margin expansion: From roughly 14% adjusted EBITDA margin at the start of his tenure to record 16.7% in 2024.

- Portfolio optimization: Divesting construction while doubling down on design/consulting.

- US market leadership: The Page acquisition positions Stantec as the second-largest architecture firm in the US.

- Continued global expansion: Acquisitions in UK, Germany, Ireland, and Australia.

Key Inflection Point #2: Strategic Plan Evolution & Margin Expansion (2020–2026)

The 2024-2026 Strategic Plan

The current Strategic Plan focuses on unprecedented funding and urgency due to climate change impacts; re-imagining and creating new approaches for communities and infrastructure; and further embracing technology to drive efficiencies. Our marketing and business development growth programs, combined with our strong expertise and exceptional cross collaboration, position us well to take advantage of the organic growth ahead of us.

Record 2024 Results

2024 was another record-setting year for Stantec, as the Company completed the first year of its ambitious 2024-2026 Strategic Plan. Net revenue increased 15.8% to $5.9 billion, driven by 7.4% organic growth and 7.5% acquisition growth.

Net income and diluted EPS achieved record highs in 2024. Net income increased 14.2%, or $45.0 million, to $361.5 million, and diluted EPS increased 11.2%, or $0.32, to $3.17.

The company's backlog reached a record $7.8 billion, representing a 24.1% increase from December 2023, indicating strong demand for its services.

Q3 2025: Momentum Continues

Adjusted EPS increased 17.7% or $0.23, to $1.53. Contract backlog increased to $8.4 billion at September 30, 2025, achieving 14.9% overall growth year over year, which includes 6.8% acquisition growth and 5.6% organic growth.

Adjusted EBITDA increased 17.8% or $48.8 million, to $323.4 million. Adjusted EBITDA margin was 19.0%, an increase of 100 basis points compared to Q3 2024.

2025 Outlook

Stantec expects to achieve net revenue growth of 7% to 10% in 2025, with net revenue organic growth in the mid- to high-single digits.

For 2025, Stantec projects net revenue growth of 7% to 10% and adjusted EBITDA margin between 16.7% and 17.3%. The company expects adjusted EPS growth of 16% to 19%.

Business Model Deep Dive

Operating Segments & Geographic Mix

Stantec offers services through five business operating units (BOUs): Infrastructure, Water, Buildings, Environmental Services, and Energy & Resources.

The Company has three operating and reportable segments for its Consulting Services: Canada, United States, and Global.

As of December 31, 2024, Stantec had approximately 32,000 employees, including professionals, technologists and technicians, and support personnel. The distribution of employees among Stantec's reportable segments was approximately 9,400 employees for Canadian operations, 12,000 for United States operations, and 10,600 for Global operations.

Global operations encompass operations outside of North America. In 2024, Stantec remained active internationally; gross revenue from Global operations was $1,720.9 million. The company performs work and has permanent offices in the United Kingdom, Europe, Australia, New Zealand, India, the Middle East, China, Taiwan, Türkiye, South and Central America, and the Caribbean.

The Design-Focus Advantage

Stantec serves the design phase of infrastructure, water, buildings, and energy & resources projects which offers higher margin opportunities and more controllable risk than integrated engineering and construction.

This is a crucial strategic choice. Many competitors (like AECOM before its restructuring) combined design consulting with construction—a model that generates higher revenues but lower margins and greater project risk. Stantec's 2018 divestiture of MWH's construction business signaled a clear preference for the higher-margin, lower-risk design-focused model.

Revenue Drivers: Macro Tailwinds

Public infrastructure spending and private investment continue to be key growth drivers in 2024, with increased project work in water security and transportation sectors. Another key driver is the urgent challenge to tackle climate change and resource security.

We've entered a golden age of engineering and design. In the United States, the 2021 Infrastructure Investment and Jobs Act alone is pushing over US$1.2 trillion of government funding into water, transportation, broadband and power-grid projects. Added to that are the billions being invested in data centres and new manufacturing facilities by companies coerced by the Trump administration into onshoring their operations.

Stantec generated C$4.63 billion from work supporting UN Sustainable Development Goals (62 percent of 2024 gross revenue).

Sustainability as Differentiator

Stantec Inc (NYSE:STN) was recognized as one of the world's most sustainable companies, ranking 8th overall and 1st among industry peers.

The company generated $4.63 billion in revenue from work supporting UN Sustainable Development Goals, representing 62% of gross revenue. Key milestones include achieving operational carbon neutrality for the third consecutive year, ranking eighth in Corporate Knights' Global 100 most sustainable corporations, and maintaining a CDP A- rating for climate-related progress for the seventh straight year.

Competitive Landscape Analysis

The Major Players

Stantec's revenue in 2024 was approximately $6.1 billion. AECOM's revenue in fiscal year 2024 was around $14.4 billion. Jacobs reported approximately $16.4 billion in revenue for fiscal year 2024. WSP Global had approximately $9.9 billion in revenue in 2024. Arcadis reported revenue of approximately $4.8 billion in 2024.

The top 10 competitors in Stantec's competitive set are WSP, AECOM, Arcadis, Jacobs, Fluor, KBR, Golder, Primoris, Groupe Canam and KEO.

Competitive Positioning

Stantec vs. AECOM/Jacobs: The US giants have significantly larger revenue bases, but Stantec has demonstrated superior margin discipline and organic growth rates. The integrated engineering-architecture model differentiates Stantec from pure engineering competitors.

Stantec vs. WSP: Fellow Canadian WSP Global is perhaps Stantec's closest comparable—similar focus on diversified consulting, aggressive acquisition strategy, and global footprint. The aggressive acquisitions made by WSP and Stantec position these firms with greater international exposure than ever.

Porter's Five Forces Analysis

| Force | Assessment | Implications for Stantec |

|---|---|---|

| Threat of New Entrants | Low | High barriers: reputation, technical expertise, client relationships, regulatory credentials. Regional competitors exist but struggle to compete on complex, multi-disciplinary projects. |

| Bargaining Power of Buyers | Moderate | Large public clients can negotiate; however, specialized expertise creates switching costs. Long-term relationships reduce buyer power. |

| Bargaining Power of Suppliers | Moderate-High | Talent is the key input. Competition for engineers and architects is intense, limiting margin expansion. |

| Threat of Substitutes | Low | Infrastructure must be designed by qualified professionals. AI may automate some tasks but won't replace professional judgment. |

| Competitive Rivalry | High | Numerous large global competitors; however, industry consolidation continues. Project-based competition on complex work favors established players. |

Hamilton Helmer's 7 Powers Framework

| Power | Stantec's Position |

|---|---|

| Scale Economies | ✓ Partial – Larger projects require integrated multi-disciplinary teams; spreading overhead across larger revenue base improves margins. |

| Network Effects | ○ Weak – Limited direct network effects, though reputation compounds with project portfolio. |

| Counter-Positioning | ○ Weak – Competitors could replicate the design-focused, acquisition-led model. |

| Switching Costs | ✓ Moderate – Long-term client relationships, institutional knowledge, and regulatory familiarity create stickiness. |

| Branding | ✓ Strong – Single global brand enables integrated service delivery; 70-year track record. |

| Cornered Resource | ○ Weak – No exclusive access to talent or technology. |

| Process Power | ✓ Strong – Demonstrated excellence in acquisition integration; operational discipline. |

Bull Case & Bear Case

The Bull Case

1. Infrastructure Super-Cycle: Global infrastructure deficits, climate adaptation requirements, and reshoring/nearshoring trends are creating unprecedented demand for design and consulting services. The US IIJA ($1.2 trillion), UK AMP8 water program (£104 billion), and similar initiatives globally provide multi-year visibility.

2. Margin Expansion Runway: Adjusted EBITDA margins have expanded from ~14% to ~17% under Johnston. Real estate optimization, high-value centers (offshore support), and AI-enabled productivity could drive further expansion.

3. M&A Optionality: With net debt/EBITDA at 1.5x and strong free cash flow generation, Stantec has capacity for continued acquisitions. The $8.4 billion backlog provides visibility to digest recent deals while pursuing new targets.

4. Water & Climate Leadership: Water achieved 24% organic backlog growth in Canada and the US. Water infrastructure is a multi-decade growth theme with strong secular tailwinds.

5. Proven Execution: "RBC Dominion Securities analyst Sabahat Khan, who covers Stantec, says these years have been the most transformative in that company's long history."

The Bear Case

1. Valuation Premium: Critics may point to Stantec's forward P/E ratio of 25, above its 10-year average of 18, as a sign of overvaluation. The stock prices in significant execution.

2. Integration Risk: Serial acquirers eventually face integration fatigue or cultural dilution. The Page integration is proceeding well, but each new deal adds complexity.

3. Economic Sensitivity: Despite diversification, Stantec remains exposed to construction and infrastructure spending cycles. A severe recession would pressure both public budgets and private development.

4. Talent Competition: Weaknesses include intense competition and the need for continuous innovation. Engineering talent is scarce; wage inflation could pressure margins.

5. US Market Uncertainty: Management flagged moderated US organic growth due to slower public-sector procurement cycles and private-sector caution for large projects.

Myth vs. Reality

| Consensus Narrative | Reality Check |

|---|---|

| "Stantec is just a rollup" | While acquisitions drive ~50% of growth, organic growth has averaged 6-7% annually—demonstrating genuine operating momentum, not just financial engineering. |

| "Infrastructure spending is temporary" | Climate adaptation, water security, and grid modernization are multi-decade requirements. The UK AMP8 program alone extends to 2030 with unprecedented budgets. |

| "Margins can't expand further" | Real estate optimization (~6% footprint reduction in 2024), AI implementation, and offshore high-value centers provide additional levers. |

Key Metrics to Watch

For long-term investors, two KPIs deserve primary focus:

1. Organic Revenue Growth (Target: Mid-to-High Single Digits)

Organic growth demonstrates the underlying health of client relationships and market positioning. While acquisitions add capabilities and scale, organic growth proves the integrated entity is winning new work. Stantec has consistently delivered 6-8% organic growth; sustained performance above this range would signal accelerating market share gains.

2. Contract Backlog & Book-to-Bill

Contract backlog increased to $8.4 billion at September 30, 2025, representing approximately 13 months of work. Backlog provides forward visibility into revenue; tracking organic backlog growth (excluding acquisitions) reveals underlying demand trends. The water segment's 24% organic backlog growth signals exceptionally strong positioning in a critical growth vertical.

Secondary metrics: Adjusted EBITDA margin (trajectory toward 17%+ target), days sales outstanding (cash conversion efficiency), and net debt/EBITDA (acquisition capacity).

Regulatory & Accounting Considerations

Revenue Recognition: Stantec uses percentage-of-completion accounting for long-term contracts, which requires management judgment on project progress. Investors should monitor DSO and working capital trends for signs of aggressive revenue recognition.

Goodwill: Serial acquisitions create significant goodwill balances. As of late 2024, impairment risk appears low given strong operating performance, but economic downturns could trigger writedowns.

Currency Exposure: Stantec generates over 75% of gross revenue in foreign currencies, primarily in US dollars, British pounds (GBP), and Australian dollars. Exchange rate movements affect reported results though hedging partially mitigates this.

Conclusion: The Long Game

Stantec's story is ultimately about patient capital and disciplined execution across seven decades. From Don Stanley driving 27,000 kilometers to drum up business, to Ron Triffo's post-crisis diversification, to Tony Franceschini's billion-dollar vision, to Bob Gomes' MWH deal, to Gord Johnston's margin-focused transformation—each era built on the last.

Gord Johnston has set a goal for the company: to be the world's top integrated engineering, architecture and environment services firm.

Whether Stantec achieves that ambition depends on continued execution: integrating Page successfully, maintaining organic growth amid economic uncertainty, and expanding margins while investing in talent and capabilities.

What's not in question is the strategic positioning. "Climate change, and the race to get ahead of it, is a critical driver. The work of forestalling disaster is basically an engineering job—or rather, a series of engineering jobs, all interlinked."

In a world that needs to rebuild its infrastructure, adapt to climate change, and modernize its water systems, companies like Stantec aren't just beneficiaries of spending—they're essential partners in solving civilization-scale challenges. That's a powerful position for long-term value creation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube