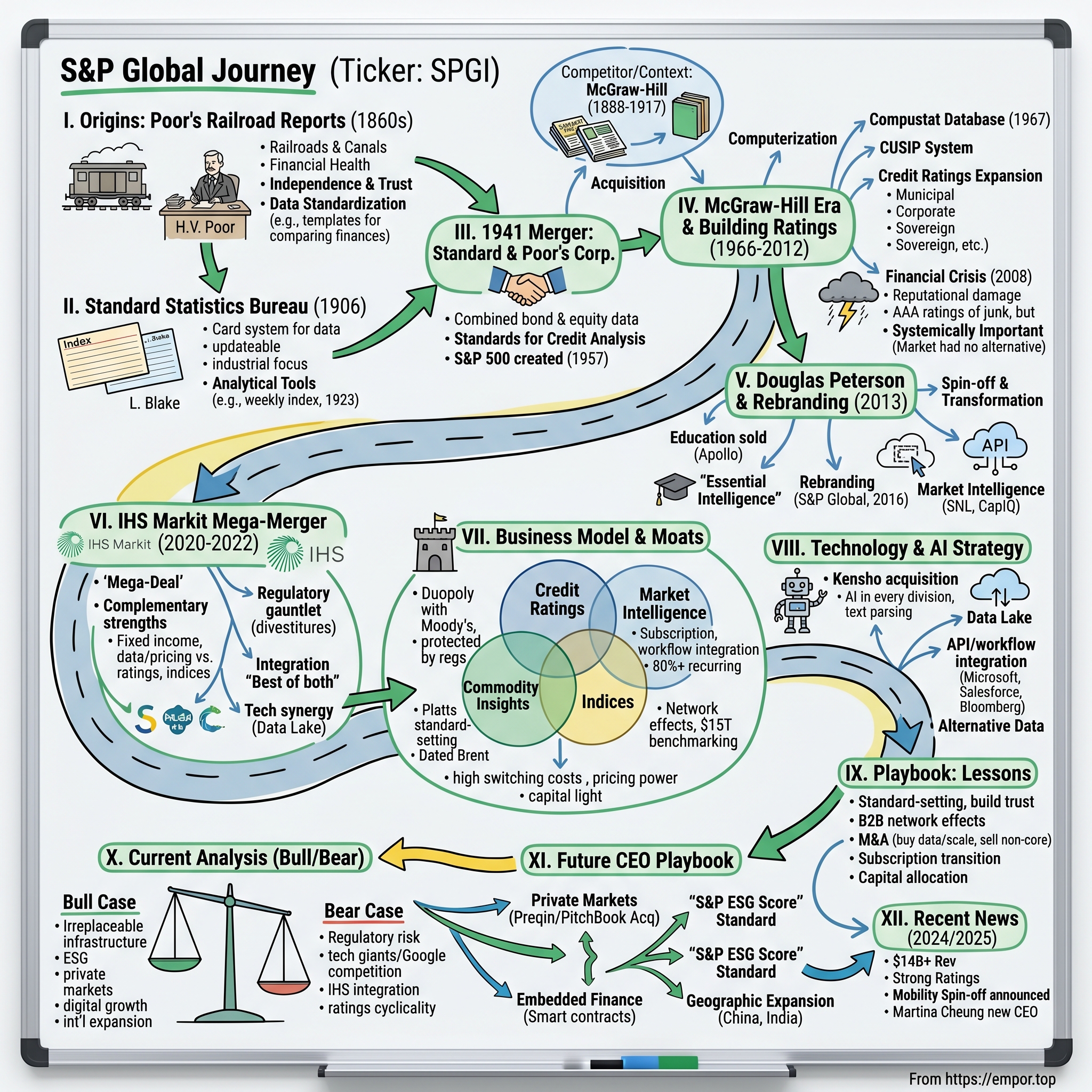

S&P Global: From Railroad Reports to Essential Intelligence

I. Introduction & Episode Roadmap

Picture this: It's 1860, and a former lawyer turned railroad analyst sits hunched over his desk in lower Manhattan, meticulously documenting the financial health of America's booming railroad companies. Henry Varnum Poor has no idea that his obsessive quest for corporate transparency will spawn a $140 billion financial intelligence empire that touches nearly every investment decision on the planet today.

S&P Global Inc., headquartered in that same New York where Poor began his work, has evolved from a niche railroad publication into a diversified financial services colossus providing credit ratings, benchmarks, analytics, and workflow solutions across global capital, commodity, and automotive markets. The company's transformation reads like a masterclass in compound growth—for the full year 2024, reported revenue surged 14% year-over-year to $14.208 billion, or 15% excluding the divested Engineering Solutions business.

But here's the central question that should fascinate any student of business history: How exactly does a 19th-century railroad guidebook publisher become the world's essential intelligence provider? How does a company founded when Abraham Lincoln was campaigning for president evolve to become the arbiter of creditworthiness for nations and corporations alike?

The answer lies in three intertwining themes that run through S&P Global's DNA like golden threads. First, the extraordinary power of building trust through independent information—a principle as vital in Poor's era of railroad barons as it is in today's algorithm-driven markets. Second, the network effects that emerge when you become the standard by which all others are measured. And third, the compounding value of data when it's organized, standardized, and made actionable.

This journey from Poor's railroad guides to the IHS Markit mega-merger isn't just corporate history—it's the story of how information became infrastructure, how data became destiny, and how one company positioned itself at the intersection of every major financial decision in the modern economy. Buckle up for a ride through 164 years of financial evolution, strategic pivots, existential crises, and ultimately, the creation of what investors now view as one of the most defensible moats in all of finance.

II. Origins: Poor's Publishing & The Railroad Era (1860-1916)

The rain was pelting against the windows of Henry Varnum Poor's law office in 1849 when news arrived that would change his life: his brother John had just been elected president of the American Railroad Journal. Henry, a Harvard-educated lawyer with a sharp analytical mind, agreed to help edit the publication. Within months, he was hooked—not on trains, but on the chaos and opportunity of America's first great corporate boom.

By 1860, Henry had taken full control and transformed the publication into something revolutionary: "History of Railroads and Canals in the United States." This wasn't just another trade journal celebrating locomotives and steel rails. Poor was doing something that had never been attempted at scale—he was systematically documenting the financial condition of American corporations, creating what we'd now recognize as the first comprehensive corporate credit analysis in American history.

Context is everything here. Post-Civil War America was experiencing its first true capital markets boom, and it was absolute bedlam. Railroad companies were sprouting like mushrooms after rain, issuing bonds and stocks to eager investors who had virtually no way to assess their creditworthiness. The information asymmetry was staggering—company insiders knew everything while outside investors knew almost nothing. Fraud was rampant, speculation wild, and fortunes were made and lost on rumors whispered in Manhattan's financial district.

Poor saw an opportunity in this chaos. Working from his New York office with a small team including his son Henry William Poor, he began dispatching investigators to railroad companies across the country. These weren't puff pieces or promotional materials—Poor's team dug into financial statements (when they existed), interviewed employees, inspected physical assets, and most controversially, published their findings regardless of whether the railroads liked it or not.

The innovation wasn't just in gathering data—it was in standardizing it. Poor created templates for comparing railroad finances, introducing metrics that allowed investors to evaluate the Burlington Northern against the Pennsylvania Railroad using consistent criteria. He was essentially inventing financial analysis in real-time, creating methodologies that MBA students still study today. Revenue per mile of track, operating ratios, debt coverage—these concepts that seem obvious now were revolutionary insights in the 1860s.

But Poor's real genius lay in understanding trust as a business model. In an era when most financial publications were either owned by the companies they covered or took bribes for favorable coverage (a practice so common it had its own term: "puffery"), Poor's Publishing maintained fierce independence. This wasn't altruism—it was strategy. Poor recognized that reliable, unbiased information would become invaluable as capital markets matured.

The business model was elegantly simple: investors would pay handsomely for information they could trust. By 1900, Poor's Manual of Railroads had become the definitive source for railroad financial information in America. Banks wouldn't lend without consulting it. Insurance companies wouldn't invest without reviewing it. European investors, pouring capital into American expansion, treated Poor's ratings like scripture.

Poor died in 1905, but his son Henry William carried the torch, expanding coverage beyond railroads to industrial companies and utilities. By 1916, Poor's Publishing had become the de facto standard for American corporate financial reporting. They hadn't just created a successful publishing business—they had invented an entirely new industry: independent financial intelligence. Every rating agency, every financial data provider, every Bloomberg terminal traces its DNA back to Henry Varnum Poor's radical idea that accurate, standardized, independent information could be more valuable than gold.

The stage was set for the next act in this drama—the emergence of a competitor who would first challenge, then ultimately merge with Poor's legacy to create something even more powerful.

III. The McGraw-Hill Connection & The Formation of Standard & Poor's (1888-1941)

Luther Lee Blake was standing in the ruins of the 1906 San Francisco earthquake, watching businessmen desperately trying to reconstruct their destroyed financial records, when inspiration struck. "What if," he thought, "financial information could be portable, updateable, and distributed continuously rather than in annual tomes?" That moment of clarity would revolutionize how Wall Street consumed data and set in motion a chain of events leading to one of finance's most important mergers.

While Poor's Publishing dominated railroad analysis, Blake saw opportunity in the exploding world of industrial securities. In 1906, he founded the Standard Statistics Bureau with a genuinely innovative product: a card-based information system. Instead of publishing massive annual books that were outdated the moment they were printed, Standard Statistics delivered index cards to subscribers, each containing current news items and financial updates. Investors could organize these cards however they wanted, creating customized, constantly updated databases. It was essentially a paper-based API, 80 years before the internet.

Meanwhile, a parallel story was unfolding in the technical publishing world. James H. McGraw had purchased the American Journal of Railway Appliances in 1888, steadily building a portfolio of trade publications. By 1899, he established The McGraw Publishing Company. John A. Hill was running a similar playbook, forming The Hill Publishing Company in 1902. The two men, recognizing their complementary strengths, merged their book departments in 1909 to create The McGraw-Hill Book Company, with Hill as president and McGraw as vice-president. By 1917, they fully merged into The McGraw-Hill Publishing Company, creating a technical and educational publishing powerhouse.

Back at Standard Statistics, Blake was pushing boundaries. By the 1920s, his company wasn't just distributing information—it was creating analytical tools. In 1923, Standard Statistics developed its first stock market index covering 233 companies, updated weekly. This was revolutionary: investors could now track market movements systematically rather than through anecdote and intuition. The index would eventually evolve into something rather important—but we're getting ahead of ourselves.

The 1920s roared, and both Poor's Publishing and Standard Statistics rode the wave. But here's where the story gets cinematic: In early October 1929, both companies independently began warning their subscribers about overvaluation in the markets. Standard Statistics' index showed troubling divergences. Poor's analysts noted unsustainable debt levels. Both firms effectively told their clients to get out.

When Black Tuesday hit on October 29, 1929, clients who had heeded these warnings were protected. Those who hadn't were destroyed. The reputation boost was enormous—here was proof that independent analysis could literally save fortunes. But the Great Depression that followed created its own challenges. With markets frozen and companies failing, both Poor's Publishing and Standard Statistics faced existential pressure.

Paul Talbot Babson, who had acquired Poor's Publishing, recognized that the two companies were stronger together than apart. In 1941, in the midst of World War II, he orchestrated the merger of Standard Statistics Company with Poor's Publishing, creating Standard & Poor's Corporation. The combination was brilliant: Poor's deep historical data and reputation in bonds merged with Standard's innovative distribution methods and strength in equities.

The new entity immediately set about creating unified standards for credit analysis. They expanded the index to 500 companies—creating what would become the S&P 500 in 1957. They developed comprehensive databases that included both historical depth and current updates. Most importantly, they established the principle that would define their future: becoming the standard by which all other financial information would be measured.

But the real masterstroke was yet to come. In 1966, McGraw-Hill, flush with cash from its educational publishing empire and recognizing the strategic value of financial information, would acquire Standard & Poor's for what seemed like a hefty premium at the time. Looking back, it might have been the deal of the century. The merger would transform both companies, setting the stage for S&P to become not just a data provider, but the essential intelligence backbone of global capitalism.

IV. The McGraw-Hill Era & Building the Ratings Empire (1966-2012)

Harold McGraw Jr. was pacing the mahogany-paneled boardroom of McGraw-Hill's headquarters in 1966, wrestling with a decision that would define his legacy. The educational publishing titan had the opportunity to acquire Standard & Poor's from Paul Talbot Babson, but the board was divided. "Why," one director asked, "should a textbook company buy a financial data firm?" McGraw's response was prescient: "Because in the future, information will be more valuable than oil, and financial information will be the most valuable of all."

The acquisition price—undisclosed but reported to be around $30 million—seemed steep for a company generating modest profits from selling financial manuals and ratings. But McGraw understood something his peers didn't: the coming computerization of finance would create insatiable demand for standardized, digital financial data. He was betting on a future where every investment decision would require S&P's intelligence.

The transformation began almost immediately. In 1967, Standard & Poor's launched Compustat, a revolutionary database containing standardized financial data on thousands of companies with historical records stretching back decades. This wasn't just digitization—it was standardization on steroids. For the first time, investors could compare companies across industries using consistent metrics, all accessible through newfangled computer terminals. Academic finance exploded as researchers suddenly had data to test theories. Quantitative investing was born in those magnetic tape drives spinning in S&P's data centers.

Then came the CUSIP innovation. Working with the American Bankers Association, S&P created the Committee on Uniform Securities Identification Procedures, developing nine-character identifiers for every security. It sounds mundane—just some numbers and letters—but CUSIP became the DNA of modern finance. Every trade, every settlement, every piece of financial plumbing relied on these identifiers. S&P didn't just provide information about securities; they literally defined how securities were identified. The network effects were staggering.

The S&P 500 index, formalized in 1957 but truly weaponized under McGraw-Hill, became the market benchmark. This wasn't just an index—it was a committee-driven selection of America's most important companies, rebalanced regularly, becoming the de facto definition of "the market." When people asked "How did the market do today?" they meant the S&P 500. When pension funds needed to benchmark performance, they used the S&P 500. When Vanguard launched its revolutionary index fund in 1976, it tracked—you guessed it—the S&P 500.

But the real empire emerged in credit ratings. Through the 1970s and 1980s, S&P systematically expanded from rating corporate bonds to municipal bonds, structured products, sovereign debt, and eventually, anything that could default. The Nationally Recognized Statistical Rating Organization (NRSRO) designation from the SEC in 1975 created a regulatory moat—many investors were legally required to consider S&P ratings. The business model was brilliant: issuers paid for ratings because investors demanded them. It was a tollbooth on the global capital markets.

Revenue exploded: from tens of millions in the 1970s to hundreds of millions in the 1980s to billions by the 2000s. Operating margins expanded even faster as the marginal cost of issuing ratings plummeted while pricing power soared. S&P was essentially selling opinions backed by data, and those opinions had become legally and practically essential.

Then came 2008.

The financial crisis was S&P's darkest hour. Those AAA ratings on mortgage-backed securities that turned to junk? S&P's stamp was on them. The Congressional hearings were brutal. Email evidence showed analysts knew many securities were problematic but rated them highly anyway. "We rate every deal," one infamous email read. "It could be structured by cows and we would rate it." The reputational damage was catastrophic. Lawsuits proliferated. The Department of Justice sought $5 billion in penalties.

Yet here's what's remarkable: S&P survived and ultimately thrived. Why? Because the market had no alternative. The entire global financial system was hardwired to require S&P ratings. Regulations mandated them. Contracts referenced them. Investment guidelines depended on them. S&P had become systemically important—too essential to fail.

Under CEO Harold McGraw III (who took over in 1998), the company diversified aggressively. They acquired J.D. Power for automotive data. They bought Capital IQ to compete with Bloomberg in financial terminals. They expanded into commodity pricing through Platts. The strategy was clear: wherever financial professionals needed data to make decisions, S&P would provide it.

By 2011, McGraw-Hill's market cap had reached $15 billion, with S&P divisions generating the majority of profits. The transformation from educational publisher to financial intelligence powerhouse was complete. But Harold McGraw III had one more play—perhaps the boldest of all. Recognizing that the educational and financial businesses had diverged completely, he decided to split the company. The announcement in September 2011 shocked Wall Street: McGraw-Hill would become two separate public companies.

This wasn't retreat—it was focus. The financial information business would need massive technology investments and acquisitions to compete in the digital age. Educational publishing faced its own disruption from digital learning. Keeping them together constrained both. The split would unleash S&P Global to pursue its destiny as the world's essential intelligence provider.

V. The Spin-off & Transformation (2013-2020)

Douglas Peterson was an unusual choice for CEO when he joined McGraw-Hill Financial in September 2013. A former president of Citibank Japan with deep experience in emerging markets but no background in ratings or financial data, Peterson brought an outsider's perspective to a company in the midst of radical transformation. His first all-hands meeting set the tone: "We're not in the ratings business or the index business or the data business," he declared. "We're in the essential intelligence business."

The corporate restructuring was already in motion when Peterson arrived. On November 26, 2012, McGraw-Hill had announced the sale of its entire education division to Apollo Global Management for $2.5 billion in cash. The March 2013 completion of this $2.4 billion transaction marked the end of a 125-year chapter in educational publishing. On May 1, 2013, shareholders voted to rename the remaining entity McGraw Hill Financial, signaling the complete pivot to financial services.

But Peterson saw that even this wasn't enough. The McGraw-Hill name, while storied, confused customers and investors. In February 2016, he announced another rebranding: McGraw Hill Financial would become S&P Global Inc. The shareholder vote on April 27, 2016, wasn't just a name change—it was a declaration of strategic intent. S&P wasn't just one brand among many; it was the crown jewel, the identity around which everything else would orbit.

Peterson's strategy crystallized around a powerful insight: in an era of information overload, the scarce resource wasn't data but trust, standardization, and workflow integration. He articulated this as becoming providers of "essential intelligence"—information so critical and so integrated into customer workflows that it became impossible to replace.

The digital transformation Peterson initiated was staggering in scope. S&P Global invested over $1 billion annually in technology, rebuilding legacy systems, moving to the cloud, and creating APIs that integrated directly into customer workflows. This wasn't just digitizing existing products—it was reimagining how financial professionals consumed information. Instead of selling data, S&P began selling answers. Instead of providing information, they delivered insights.

The Market Intelligence division exemplified this transformation. Capital IQ evolved from a Bloomberg competitor into something more focused: a platform specifically designed for investment banking, private equity, and corporate development professionals. The acquisition of SNL Financial in 2015 for $2.2 billion added deep sector expertise in banking, insurance, and media. These weren't just bolt-on acquisitions—Peterson was assembling specialized intelligence capabilities that created compound value when integrated.

Commodity Insights (built around the Platts acquisition) showcased another dimension of the strategy. As energy markets grew more complex and volatile, S&P's price assessments became the benchmarks for physical and derivative trading. The Platts window—the daily process for assessing oil prices—moved billions of dollars daily. Like credit ratings, these benchmarks created powerful network effects: the more people used them, the more essential they became.

The Kensho acquisition in 2018 for $550 million signaled Peterson's ambition in artificial intelligence. Kensho wasn't just another analytics company—it was building next-generation AI specifically for financial data. The vision was compelling: combine S&P's unmatched datasets with cutting-edge machine learning to create predictive intelligence that went beyond backward-looking analysis.

Financial performance during this period validated the strategy. Revenue grew from $4.9 billion in 2013 to $6.7 billion in 2019. More impressively, operating margins expanded from the mid-30s to the mid-40s as subscription-based revenue grew and technology investments improved efficiency. The stock price more than tripled, dramatically outperforming both the S&P 500 (ironically) and direct competitors.

But Peterson's masterstroke was recognizing that organic growth alone wouldn't be sufficient. The financial data industry was consolidating rapidly. Bloomberg was expanding aggressively. Refinitiv (formerly Thomson Reuters) had massive scale. The London Stock Exchange was acquiring data assets. To truly achieve essential intelligence status, S&P needed a transformational acquisition.

In November 2020, as the world grappled with COVID-19, Peterson made his move. The announcement of the IHS Markit merger, valued at $44 billion including debt, was the second-largest deal of 2020. It was audacious, complex, and potentially game-changing. The market's initial reaction was mixed—the stock fell 5% on announcement. But Peterson saw what others didn't: the combination would create unprecedented capabilities in the exact areas where financial markets were heading—private markets, ESG, fixed income analytics, and alternative data.

The transformation from McGraw-Hill's financial division to S&P Global was complete. But the IHS Markit merger would test whether Peterson's vision of essential intelligence could scale to unprecedented size.

VI. The IHS Markit Mega-Merger (2020-2022)

Lance Uggla was sitting in his home office in Connecticut, March 2020, watching markets melt down as COVID-19 spread globally. The CEO of IHS Markit had built a financial data powerhouse through fifteen years and over 100 acquisitions, but he knew the industry's tectonic plates were shifting. When his phone rang with Doug Peterson on the line suggesting they "explore strategic opportunities," Uggla sensed this wasn't just another partnership discussion.

The timing seemed insane. The world was in lockdown, markets were in chaos, and conducting due diligence on a $44 billion merger would require unprecedented virtual coordination. But both CEOs recognized a unique window: their companies were perfectly complementary, regulatory scrutiny was focused elsewhere, and the pandemic had accelerated the digital transformation both companies were betting on.

IHS Markit itself was a creature of consolidation, formed in 2016 when IHS Inc. acquired Markit for $13 billion. The combined entity had assembled premier assets: Markit's bonds and derivatives pricing, loan and CLO data; IHS's automotive data (including Carfax), maritime intelligence, and technical standards. With $4.3 billion in revenue and 22,000 employees across 35 countries, IHS Markit was formidable alone. Combined with S&P Global, it would be unstoppable.

The strategic logic was compelling to the point of being obvious. S&P dominated credit ratings and equity indices; IHS Markit excelled in fixed income data and derivatives. S&P had strength in public markets; IHS Markit was building capabilities in private markets. S&P's commodity pricing through Platts complemented IHS's energy and maritime intelligence. Even the customer bases were complementary—S&P stronger with asset managers, IHS Markit deeper in investment banks and hedge funds.

But the devil was in the deal structure. The all-stock transaction valued each IHS Markit share at 0.2838 S&P Global shares—a ratio that precisely reflected both companies' contributions to the combined entity's value. S&P shareholders would own 67.75% of the combined company, IHS Markit shareholders 32.25%. Peterson would remain CEO, while Uggla would become a special advisor—a graceful exit that avoided leadership conflicts that derail many mergers.

The regulatory gauntlet was brutal. This wasn't just another data company acquisition—it was combining two essential pieces of global financial infrastructure. The Department of Justice worried about concentration in oil price reporting. The European Commission scrutinized overlaps in financial data. The UK's Competition and Markets Authority conducted one of its most detailed reviews ever.

The solutions were surgical. To address oil pricing concerns, S&P agreed to divest IHS Markit's Oil Price Information Service (OPIS), Coal, Metals and Mining, and PetrochemWire businesses to News Corporation. For financial data overlaps, they committed to maintaining open access to certain datasets and ensuring interoperability with competitors. The regulatory review took 15 months, but on February 28, 2022, the deal closed at approximately $140 billion in enterprise value—making it one of the largest mergers in financial services history.

Integration began immediately and aggressively. Peterson organized the combined company into five focused divisions: S&P Global Ratings, S&P Global Market Intelligence, S&P Global Commodity Insights, S&P Global Mobility, and S&P Dow Jones Indices. Each division had clear leadership, distinct customers, and specific synergy targets. The promise was $480 million in annual cost synergies and $350 million in revenue synergies within three years.

The technology integration was particularly complex. S&P and IHS Markit had different data architectures, delivery platforms, and customer interfaces. Rather than force immediate standardization, Peterson's team took a "best of both" approach—maintaining separate platforms where customers demanded it while building unified next-generation systems. The IHS Markit Data Lake, containing petabytes of historical and real-time data, became the foundation for new AI and analytics capabilities.

Customer reaction was mixed but ultimately positive. Some worried about reduced competition and potential price increases. Others saw value in integrated workflows—accessing S&P ratings, IHS Markit bond prices, and Platts commodity data through unified platforms. The real win was in cross-selling: S&P could now offer IHS Markit's leveraged loan data to its ratings clients, while IHS Markit's fixed income customers gained access to S&P's credit analytics.

By late 2022, the merger was delivering ahead of schedule. Combined revenue reached $13 billion, with organic growth accelerating as the companies leveraged combined capabilities. Operating margins held steady despite integration costs, validating Peterson's confidence in the combination. The stock price, after initial skepticism, surged to new highs as investors recognized the strategic value creation.

But success brought new challenges. In April 2025, S&P announced plans to spin off its Global Mobility unit (essentially Carfax and automotive data) into a standalone public company. The message was clear: even at massive scale, S&P Global would maintain focus on essential financial intelligence, divesting assets that didn't fit the core mission.

The IHS Markit merger transformed S&P Global from a leading financial data provider into the essential intelligence platform for global markets. The integration continues, but the strategic bet has already paid off: S&P Global now touches virtually every significant financial decision on the planet.

VII. Business Model & Competitive Moats

Walk into any investment firm's office at 7 AM and you'll witness S&P Global's business model in action. The credit analyst pulling S&P ratings on a new bond issue, the portfolio manager checking Platts oil prices, the investment banker modeling an LBO using Capital IQ data, the risk manager analyzing leveraged loan exposures through IHS Markit's platform—each interaction generates revenue for S&P Global, and more importantly, reinforces dependencies that make switching costs astronomical.

The five-segment structure post-merger reveals a carefully orchestrated portfolio of monopolistic and oligopolistic positions. S&P Global Ratings, generating roughly 30% of revenue but nearly 50% of operating profit, operates in a cozy oligopoly with Moody's. Together they command over 80% of global credit ratings, protected by regulatory requirements, decades of historical data, and the simple fact that the entire fixed income market has been built around their rating scales. Try explaining to a bond committee why you're using an unfamiliar rating agency—career suicide.

Market Intelligence, now the largest segment by revenue at approximately 35%, bundles multiple subscription businesses that exhibit powerful retention dynamics. Capital IQ, SNL, Platts Analytics—these aren't just data feeds but workflow tools embedded into daily routines. A banker who's spent years building models in Capital IQ won't switch to save a few thousand dollars. The subscription model is beautiful: 80% recurring revenue, net retention rates above 110% (customers spend more each year), and gross margins north of 70%.

Commodity Insights, anchored by Platts, showcases a different moat: standard-setting. When Platts publishes the daily price for Dated Brent crude, it's not just reporting a price—it's determining the price that underlies billions in physical and derivative contracts. The methodology, the assessment process, the specific timing—all of this creates lock-in that would take decades to displace. Energy traders literally structure their entire day around the Platts window.

The Indices segment, though smallest by revenue, might have the deepest moat. The S&P 500 isn't just an index—it's the benchmark for $15 trillion in assets. Every basis point of assets indexed or benchmarked to S&P indices generates recurring license fees. The network effects are insurmountable: the more assets track the index, the more liquid the associated derivatives, making it more attractive for new assets. It's a virtuous cycle that competitors can't break.

Mobility (Carfax and automotive data), while profitable, always sat uncomfortably in the portfolio—hence the 2025 spin-off announcement. It lacked the network effects and regulatory moats of other divisions, making it valuable but not essential.

The competitive landscape reveals why S&P Global's position is so formidable. Bloomberg, with its $12 billion in revenue, dominates the terminal business but has struggled to build significant market share in ratings or indices. Moody's, S&P's closest peer, matches them in ratings but lacks the breadth in data and indices. MSCI excels in indices and analytics but missing ratings limits their ecosystem. Refinitiv (now part of London Stock Exchange Group) has scale but lacks S&P's focused positioning in essential decision points.

The subscription economics deserve special attention. Unlike transactional businesses, subscriptions create predictable, growing revenue streams with minimal marginal costs. S&P Global's subscription revenue has grown from 40% of total revenue in 2010 to over 65% today. Retention rates above 95% mean customer lifetime values measured in decades. Price increases of 3-5% annually face minimal resistance because the products are essential and represent a tiny fraction of customer costs.

The regulatory moat, particularly in ratings, cannot be overstated. The NRSRO designation, Dodd-Frank requirements, Basel III capital rules—all create demand for S&P ratings regardless of competitive dynamics. Even after the financial crisis tarnished their reputation, regulations still require their ratings. It's a government-sanctioned oligopoly hiding in plain sight.

Network effects operate at multiple levels. Direct network effects: the more companies S&P rates, the more valuable their ratings become for comparison. Indirect network effects: the more investors use S&P ratings, the more issuers need them. Data network effects: the more data S&P collects, the better their analytics, attracting more customers who provide more data. Standard network effects: the more contracts reference S&P indices or Platts prices, the harder it becomes to switch.

The capital-light nature of the business model is striking. S&P Global generates nearly $5 billion in free cash flow annually on minimal capital investment. Unlike industrial companies that require factories or tech companies that need massive R&D, S&P's primary assets are intellectual property, data, and reputation. This enables extraordinary returns on invested capital—often exceeding 30%—and allows aggressive capital return through dividends and buybacks.

Pricing power emerges from this combination of moats. When S&P raises rating fees or subscription prices, customers grumble but pay. Where else would they go? The alternative is either unavailable (no other NRSRO-designated ratings), inferior (less comprehensive data), or prohibitively expensive to switch (retooling entire workflows). This pricing power, combined with operating leverage, drives margin expansion even during heavy investment periods.

The result is a business model that Warren Buffett would love: predictable, protected, profitable, and positioned at the center of global capitalism. The question isn't whether S&P Global's moats will persist—it's how they'll leverage them to capture new profit pools in private markets, ESG, and emerging economies.

VIII. Technology, Data, and AI Strategy

Hugh Frater, the former CEO of Kensho, stood before S&P Global's board in 2018 with an audacious claim: "In five years, 70% of junior analyst tasks in finance will be automated. The question isn't if, but who will own the automation layer." His presentation, featuring live demonstrations of Kensho's AI extracting insights from earnings calls and predicting market movements, convinced the board to approve a $550 million acquisition—S&P's largest technology bet to date.

Kensho wasn't just another analytics acquisition. Founded by Harvard and MIT PhDs with backing from Google Ventures and Goldman Sachs, the company had built genuinely differentiated AI specifically for financial data. Their natural language processing could parse Federal Reserve minutes in milliseconds, identifying sentiment shifts before human analysts finished reading the first paragraph. Their computer vision could extract data from scanned documents dating back decades. Most impressively, their machine learning models could identify complex market patterns across seemingly unrelated datasets.

The integration of Kensho into S&P Global revealed Peterson's larger technology vision: don't just digitize existing products, but reimagine what's possible when AI meets the world's most comprehensive financial datasets. Within months, Kensho's capabilities were enhancing products across every division. Ratings analysts used Kensho to scan thousands of documents for covenant changes. Market Intelligence embedded Kensho's NLP into Capital IQ to auto-generate company summaries. Commodity Insights applied machine learning to predict supply disruptions from satellite imagery and shipping data.

But Kensho was just one piece of a broader digital transformation. The creation of the S&P Global Data Lake, expanded massively through the IHS Markit merger, represented one of the largest domain-specific data repositories in existence. Petabytes of structured and unstructured data—every rating report since the 1920s, decades of commodity prices, millions of company filings, real-time market data—all normalized, tagged, and made machine-readable. This wasn't just storage; it was the foundation for AI applications that required massive training datasets.

The API strategy marked another crucial evolution. Historically, S&P delivered data through proprietary terminals or bulk feeds—clunky, expensive, and disconnected from customer workflows. The new platform-as-a-service approach offered RESTful APIs that integrated directly into customer systems. A hedge fund's risk system could pull real-time ratings changes. A corporate treasury platform could access Platts commodity curves. An investment bank's models could tap Capital IQ fundamentals. By 2024, over 40% of data consumption occurred through APIs, up from less than 10% in 2018.

The workflow integration went deeper than APIs. S&P began embedding intelligence directly into customer decision points. Microsoft Excel plugins brought Capital IQ data into spreadsheets. Salesforce integrations pushed credit alerts into CRM systems. Bloomberg Terminal apps surfaced S&P ratings within competitor platforms. The strategy was brilliant: be everywhere customers make decisions, regardless of platform.

Cloud transformation enabled this flexibility. Moving from on-premise data centers to AWS and Azure didn't just reduce costs—it enabled elastic scaling, global distribution, and real-time processing. S&P could now handle massive computational workloads, like recalculating indices in microseconds or running stress tests across millions of scenarios. Cloud-native architecture also enabled rapid deployment of new features, with some products releasing updates weekly rather than annually.

The investment in alternative data showcased S&P's ambition to go beyond traditional financial information. Satellite imagery for commodity supply tracking, credit card transaction data for consumer insights, social media sentiment for earnings prediction—S&P began acquiring and partnering to access novel datasets. The value wasn't in raw alternative data but in S&P's ability to clean, normalize, and integrate it with traditional datasets, creating insights neither could generate alone.

Machine learning applications proliferated across the business. Predictive models flagged credits likely to be downgraded. Natural language generation created automated research reports. Anomaly detection identified market manipulation. Computer vision extracted data from physical documents. Each application seems narrow, but collectively they're transforming S&P from a data provider to an intelligence platform.

The cybersecurity investments, while less visible, were equally critical. S&P Global processes some of the world's most market-sensitive information—a ratings change leaked early could move billions. The security infrastructure rivals intelligence agencies: multi-factor authentication, encrypted data lakes, behavioral monitoring, penetration testing, and redundant systems across multiple continents. A single breach could destroy decades of trust, so security investment is essentially unlimited.

Looking forward, S&P's technology roadmap focuses on three areas. First, generative AI applications that can draft credit reports, answer investor questions, and generate custom analyses. Second, real-time intelligence that moves beyond backward-looking data to predictive insights. Third, embedded finance applications that integrate S&P intelligence directly into transaction flows—imagine smart contracts that automatically adjust terms based on rating changes.

The technology transformation faces challenges. Legacy systems still process critical functions, requiring careful migration. Customers, particularly in conservative financial institutions, resist change. Regulators scrutinize AI applications, particularly in ratings, for bias and explainability. Competition from native technology companies like Google and Amazon, who could leverage superior AI capabilities, looms constantly.

But S&P Global's technology moat might be its strongest. Competitors can build AI models, but they lack S&P's datasets. Technology companies have better algorithms but lack S&P's domain expertise and regulatory positioning. Traditional competitors have data but lack S&P's technology vision and investment capacity. The combination of essential data, embedded workflows, advancing AI, and massive investment creates a competitive advantage that compounds over time.

IX. Playbook: Business & Investing Lessons

S&P Global's 164-year journey from railroad guides to essential intelligence offers a masterclass in building enduring business value. The lessons transcend financial services, providing blueprints for any company seeking to create monopolistic positions in information markets.

The Power of Standards and Becoming the Default

S&P didn't just create credit ratings—they created the language of credit itself. The letter-grade system (AAA, AA, BBB, etc.) became so universally adopted that competitors had to use similar nomenclature. The S&P 500 didn't just track the market; it defined what "the market" meant. Platts prices didn't just report commodity values; they became the prices written into billions of dollars of contracts.

The lesson is profound: in information businesses, becoming the standard is more valuable than being the best. Once market participants organize around your framework—training employees, writing contracts, building systems—switching costs become prohibitive. S&P understood this intuitively, investing heavily in methodology committees, documentation, and education to entrench their standards. They made their frameworks free to reference while charging for the data, creating adoption network effects.

Building Trust as a Business Model

Trust, once established, compounds like few other assets. S&P's origin story—Henry Poor refusing bribes from railroad barons to maintain independence—established a cultural DNA that persists today. Even after the financial crisis damaged their reputation, markets had no choice but to continue trusting S&P ratings because the entire system depended on them.

Building trust requires painful short-term sacrifices for long-term credibility. S&P regularly issues ratings that anger major clients. They publish research that contradicts market consensus. They maintain Chinese walls between commercial and analytical teams. These aren't just regulatory requirements—they're investments in the trust that enables pricing power and customer retention.

Network Effects in B2B Information Services

Consumer network effects are well understood, but S&P demonstrates how powerful they can be in B2B contexts. Every company S&P rates makes their ratings more valuable for comparison. Every asset benchmarked to the S&P 500 makes the index more liquid and useful. Every contract referencing Platts prices reinforces their importance.

The key insight: B2B network effects often operate through standards and workflows rather than direct connections. Investment committees don't care how many other firms use S&P ratings—they care that their own historical analyses, risk models, and investment guidelines are built around them. This creates stickiness that social networks can only dream of.

The M&A Playbook: When to Buy vs. Build

S&P's acquisition history reveals disciplined pattern recognition. They buy for three reasons: acquiring unique datasets (SNL Financial's banking data), entering new verticals (J.D. Power for automotive), or achieving scale (IHS Markit). They build when they have advantages: creating new indices, expanding rating coverage, developing proprietary analytics.

The discipline shows in what they don't do. S&P rarely acquires direct competitors (why buy what you'll eventually dominate?). They avoid technical infrastructure plays (better to partner with AWS than build data centers). They divest non-core assets quickly (the Mobility spin-off). Every acquisition must either strengthen network effects, add unique capabilities, or accelerate geographic expansion.

Managing Conflicts of Interest

The issuer-pays model for credit ratings creates an inherent conflict: the people you're evaluating pay your fees. S&P's response wasn't to eliminate the conflict (impossible given market structure) but to manage it through transparency, process, and culture. Rating committees operate independently from commercial teams. Methodologies are public and consistently applied. Analyst compensation is divorced from issuer relationships.

The broader lesson: conflicts of interest exist in every business. Pretending they don't exist invites disaster (see 2008). Acknowledging and systematically managing them builds trust and regulatory cover. S&P's post-crisis reforms, while forced by regulators, ultimately strengthened their business by reducing future liability.

The Subscription Transition: From Transactions to Relationships

S&P's evolution from selling books to subscriptions transformed their economics. Transaction revenue is lumpy, price-sensitive, and requires constant selling. Subscription revenue is predictable, grows through expansion, and creates customer lock-in. The transition took decades—customers resisted, systems required rebuilding, sales teams needed retraining—but the payoff was enormous.

The playbook: Start with must-have transactions (ratings), bundle in subscriptions (data feeds), gradually shift value to subscriptions (analytics platforms), and eventually make transactions feel antiquated. Today's customers don't buy S&P data; they subscribe to S&P intelligence platforms that happen to include data.

Capital Allocation Excellence

S&P Global's capital allocation might be their most underappreciated skill. With minimal capital requirements and massive cash generation, they face the high-class problem of deploying billions annually. Their solution is remarkably balanced: consistent dividends (58 consecutive years of increases), opportunistic buybacks ($8 billion in 2022-2023), and strategic acquisitions (Kensho, IHS Markit).

The discipline shows in what they avoid: vanity acquisitions, excessive leverage, hoarding cash. Every dollar is deployed with clear return expectations. Dividends signal confidence, buybacks exploit market dislocations, and acquisitions add strategic capabilities. The result: total shareholder returns exceeding 15% annually over the past decade.

Creating Switching Costs Through Workflow Integration

S&P doesn't just provide data—they embed themselves into daily workflows. An analyst trained on Capital IQ, a risk model built on S&P ratings, a trading system hardcoded to Platts prices—each integration creates switching costs measured not in dollars but in organizational disruption. Changing providers means retraining staff, rebuilding models, rewriting contracts, and explaining to bosses why established processes need disruption.

The strategic insight: focus integration investments on workflow chokepoints where switching is most painful. S&P prioritizes Excel plugins over PowerPoint add-ins because models drive decisions. They integrate with risk systems over reporting systems because risk drives trading. Every integration is evaluated not just for usage but for switching difficulty.

X. Analysis & Bear vs. Bull Case

The investment community remains sharply divided on S&P Global's future trajectory. At ~$500 per share and a $150+ billion market cap, the company trades at 30x forward earnings—a premium valuation that demands continued excellence. The bull-bear debate centers not on whether S&P Global is a good business (everyone agrees it's exceptional) but whether future returns can justify today's price.

Bull Case: Essential Infrastructure for Global Markets

The bulls see S&P Global as irreplaceable financial infrastructure trading at a reasonable price for its quality. Start with the secular tailwinds: global bond issuance is growing 5-7% annually as governments and corporations lever up, directly driving ratings demand. The indexation megatrend continues with passive assets approaching $30 trillion globally, each basis point flowing through S&P's toll booth. Private markets, now exceeding $13 trillion in assets, desperately need the transparency and analytics S&P provides.

The ESG revolution presents massive opportunity. S&P's ESG ratings, data, and indices are becoming as essential as traditional credit ratings. Regulation is mandating ESG disclosure, investors are demanding ESG analytics, and S&P is positioned to capture economics similar to traditional ratings. The addressable market could exceed $5 billion by 2030, with S&P taking disproportionate share given their credibility and distribution.

Energy transition creates unprecedented demand for commodity intelligence. Understanding battery metal supplies, carbon pricing, renewable energy economics, and hydrogen markets requires exactly the real-time pricing and analytics S&P provides through Platts. Every Tesla sold, every wind farm built, every carbon credit traded reinforces S&P's commodity franchise.

The subscription model transition continues to drive superior economics. As more revenue shifts from transactional to recurring, predictability improves, customer lifetime values extend, and operating leverage expands. Bulls see margins expanding from mid-40s to mid-50s as technology investments mature and integration synergies compound.

Pricing power remains intact despite competition. S&P consistently raises prices 3-5% annually with minimal customer defection. In a world of 2% inflation, this real pricing power drops directly to the bottom line. The essential nature of S&P's products—you can't analyze bonds without ratings, track markets without indices, or trade commodities without benchmarks—ensures pricing power persists.

The AI opportunity is transformative, not disruptive. Rather than displacing S&P, artificial intelligence amplifies their advantages. Who else has the historical data to train models? The domain expertise to ensure accuracy? The regulatory standing to provide trusted insights? S&P's Kensho acquisition and data lake position them to capture AI value rather than be disrupted by it.

International expansion offers decades of growth. S&P generates roughly 40% of revenue internationally, but global financial markets are increasingly non-US. China's bond market, already the world's second-largest, requires rating coverage. India's rapid growth demands financial intelligence. Africa's development needs credit markets. S&P's brand, expertise, and capital position them to capture international growth.

The balance sheet provides strategic flexibility. With modest leverage and massive cash generation, S&P can pursue transformational acquisitions, return capital aggressively, or invest organically. The IHS Markit integration proves they can execute large-scale M&A. Future acquisitions in private markets, alternative data, or adjacent verticals could drive another leg of growth.

Bulls point to quality comparisons: S&P trades at a discount to MSCI (35x earnings) despite superior business mix, inline with Moody's despite better growth, and at a premium to exchanges that lack S&P's subscription model. For a business generating 30% returns on capital with high-single-digit organic growth and capital return optionality, 30x earnings seems reasonable, even cheap.

Bear Case: Regulatory Risks and Competitive Threats

The bears acknowledge S&P's quality but see multiple threats that could impair future returns. Start with regulatory risk: the issuer-pays model remains politically toxic. Another financial crisis involving failed ratings could trigger structural reform. The European Union already requires rotation of rating agencies for certain securities. What if the US follows? What if regulators mandate investor-pays models? The entire business model could unravel.

Competition from technology giants looms large. Google, Amazon, and Microsoft have better AI, more capital, and adjacent positions in financial services. What prevents them from leveraging superior technology to disrupt S&P's franchises? Bloomberg already generates more revenue than S&P. Chinese rating agencies are growing rapidly with state support. The competitive moat might be narrower than appears.

The integration risks from IHS Markit remain significant. Merging 22,000 employees, hundreds of products, and incompatible technology stacks is monumentally complex. Customer defection, talent departure, and execution mistakes could destroy billions in value. The track record of mega-mergers in technology is poor—why should this be different?

Cyclicality in the ratings business is underappreciated. S&P generated extraordinary ratings revenue in 2021-2022 as companies rushed to issue debt at low rates. But issuance is already declining as rates rise. A prolonged credit crunch could slash ratings revenue 30-40%, devastating earnings given the segment's high margins. The subscription businesses provide ballast but can't fully offset ratings cyclicality.

Valuation concerns are legitimate. At 30x earnings, S&P trades at double the market multiple. The implied growth expectations are heroic: high-single-digit organic growth, continued margin expansion, successful capital deployment. Any disappointment—a quarter of weak issuance, integration hiccups, regulatory changes—could trigger multiple compression. The stock has tripled in five years; how much upside remains?

Alternative data and AI could commoditize S&P's advantages. If AI can generate credit insights from alternative data, why pay for ratings? If passive investing shifts to custom indices, why license the S&P 500? If blockchain enables peer-to-peer commodity trading, why need Platts prices? Technology might not disrupt S&P directly but could shrink their addressable markets.

The talent war in technology and finance is intensifying. S&P competes with tech giants offering massive compensation and startups providing equity upside. Maintaining technology leadership requires attracting top talent, but S&P can't match Google's compensation or a startup's upside. Brain drain could slow innovation and enable disruption.

Bears also worry about hidden risks. Cyber attacks could devastate trust. Litigation from the financial crisis continues. Political backlash against financial elites could trigger punitive regulation. Environmental controversies around commodity trading could taint the brand. These tail risks are difficult to quantify but could be devastating.

Synthesis: A Wonderful Business at a Full Price

The truth likely lies between extremes. S&P Global is unquestionably one of the world's great businesses—essential products, powerful moats, exceptional economics. The secular growth drivers are real, the competitive position is strong, and management execution has been excellent. For long-term investors seeking quality compounders, S&P Global deserves consideration.

But the valuation leaves little room for error. At 30x earnings, the market expects continued excellence. Any stumble—regulatory changes, integration challenges, competitive pressure—could trigger significant multiple compression. The risk-reward seems balanced rather than compelling.

The optimal strategy might be patience: wait for market dislocations, regulatory scares, or integration concerns to create better entry points. S&P Global will likely remain essential for decades, but buying at any price contradicts the margin of safety principle. Quality businesses at reasonable prices outperform quality businesses at any price.

For existing shareholders, holding seems prudent given the business quality and execution track record. For new investors, waiting for better prices might be wiser. S&P Global is a wonderful business, but even wonderful businesses can be poor investments at excessive valuations.

XI. Epilogue & "If We Were CEOs"

Standing at the helm of S&P Global in 2025, with the IHS Markit integration largely complete and the Mobility division spin-off announced, the strategic choices ahead would define whether this 165-year-old institution remains essential for another century. If we were CEO, here's how we'd navigate the next decade.

Private Markets: The $30 Trillion Opportunity

The explosion of private markets—private equity, private credit, venture capital, real assets—represents S&P's most significant growth opportunity. These markets, approaching $15 trillion in assets and doubling every 7-8 years, desperately lack the transparency, standardization, and analytics that S&P provides to public markets. Our first priority would be becoming the essential intelligence provider for private markets.

We'd start by acquiring Preqin or PitchBook—established players with proprietary datasets on fund performance, deal flow, and valuations. The $3-5 billion acquisition cost would be justified by immediate access to relationships and data that would take decades to build organically. Integration with S&P's credit ratings, leveraged loan data, and analytics would create unique insights: imagine predicting private equity exits based on credit market conditions or evaluating private credit risk using S&P's vast default database.

The next move would be creating the "S&P Private 1000"—a benchmark index for private markets analogous to the S&P 500 for public markets. This would require partnering with major private equity firms to obtain performance data, developing methodologies for valuation in illiquid markets, and convincing LPs to benchmark against our index. The network effects would be powerful: the more funds report to our index, the more valuable it becomes for comparison, eventually becoming the standard.

We'd also launch private market ratings—not traditional credit ratings but assessments of fund managers, deal quality, and portfolio risk. Institutional investors allocating billions to private markets crave independent assessment. S&P's credibility and analytical capabilities position us uniquely to provide this intelligence.

ESG: From Compliance to Competitive Advantage

ESG represents a generational shift in how markets evaluate companies, but current ESG data is fragmented, inconsistent, and often superficial. S&P could own this space by moving beyond box-ticking to genuine intelligence that drives investment decisions.

First, we'd unify the dozens of ESG methodologies into a single, transparent, globally accepted standard—the "S&P ESG Score." Like credit ratings, these scores would become the language of sustainable investing. We'd make the methodology completely transparent, the data auditable, and the scores freely referenceable while charging for detailed analytics.

Next, we'd acquire Trucost (already owned) and expand dramatically into environmental data. Satellite monitoring of deforestation, AI analysis of supply chains, real-time carbon tracking—S&P would become the source of truth for environmental impact. The commodity insights division already tracks energy markets; extending into carbon markets and renewable energy economics is natural.

We'd also create ESG-linked financial products. Imagine bonds where interest rates adjust based on S&P ESG scores, or indices that dynamically reweight based on sustainability metrics. Every product would reinforce S&P's position as the ESG standard-setter while generating recurring license revenue.

Technology: Building vs. Partnering

The temptation to build everything internally must be resisted. S&P's strength is financial intelligence, not technology infrastructure. We'd pursue a hybrid strategy: own what's strategic, partner for everything else.

Core strategic assets—the data lake, analytical models, workflow applications—would remain internal with massive continued investment. We'd double down on Kensho, expanding the team and giving them freedom to innovate. But for infrastructure (cloud, security, basic AI), we'd deepen partnerships with Microsoft, Amazon, and Google rather than trying to compete.

The next frontier is embedded intelligence—S&P insights integrated directly into customer workflows without them visiting our platforms. We'd create an "S&P Inside" program, embedding our intelligence into ERP systems, trading platforms, and risk management tools. Like Intel Inside for computers, S&P Inside would make our intelligence ubiquitous and indispensable.

We'd also launch "S&P Labs"—a venture arm investing in fintech startups that could become customers, partners, or acquisitions. Beyond financial returns, this would provide early visibility into disruption and access to innovation. The $500 million fund would be a rounding error for S&P but could identify the next Kensho.

Geographic Expansion: The Asia Imperative

Asia represents 60% of global population, 40% of global GDP, but only 20% of S&P's revenue. This gap represents massive opportunity. China alone has a $20 trillion bond market that needs rating coverage. India's rapid growth requires financial intelligence. Southeast Asia is becoming a major financial hub.

Rather than forcing Western models onto Asian markets, we'd create region-specific solutions. This means hiring local talent, understanding local regulations, and respecting cultural differences. We'd establish major offices in Shanghai, Mumbai, and Singapore—not satellites but genuine centers of excellence with decision-making authority.

The strategy would be selective partnership rather than pure competition with domestic players. In China, we'd work with local rating agencies rather than competing directly. In India, we'd acquire a local player for immediate presence. In Japan, we'd leverage the Mobility division's strength to expand into financial services.

Capital Allocation: Disciplined but Aggressive

With $5 billion in annual free cash flow, capital allocation would remain paramount. The framework would be simple: invest organically where we have advantages, acquire to enter new verticals or geographies, and return excess capital to shareholders.

Organic investment would focus on technology and product development—$2 billion annually to maintain innovation leadership. M&A would be disciplined but aggressive—one major acquisition ($5-10 billion) every 3-4 years, multiple bolt-ons annually. The hurdle rate would be strict: acquisitions must be accretive to growth, margins, and returns on capital.

Capital return would balance dividends and buybacks. The dividend, with its 58-year increase streak, is sacrosanct—we'd grow it mid-single-digits annually. Buybacks would be opportunistic, accelerating when the stock is cheap and pausing when expensive. The goal: compound per-share value at mid-teens rates while maintaining financial flexibility.

The Next Decade's North Star

Our vision would be simple: make S&P Global the world's essential intelligence platform for all markets—public and private, developed and emerging, traditional and sustainable. Every major financial decision would involve S&P intelligence. Every market participant would depend on our insights.

This isn't about empire building—it's about recognizing that markets function better with transparent, standardized, trusted intelligence. S&P Global has provided this for 165 years. Our job would be ensuring it continues for the next 165.

The challenges are real: regulatory pressures, technological disruption, competitive threats. But S&P's advantages—unmatched data, deep expertise, regulatory positioning, network effects—provide the foundation for continued success. With focused execution, disciplined investment, and relentless innovation, S&P Global can remain essential as markets evolve.

The railroad reporting company that Henry Varnum Poor started in 1860 has become the neural network of global capitalism. If we were CEO, we'd ensure that S&P Global doesn't just adapt to the future of finance—we'd help create it.

XII. Recent News**

Latest Quarterly Earnings and Guidance Updates**

S&P Global reported exceptional full-year 2024 results with revenue increasing 14% year-over-year to $14.208 billion, or 15% excluding the divested Engineering Solutions business. GAAP net income surged 47% to $3.852 billion while diluted earnings per share jumped 50% to $12.35, driven primarily by strong performance in the Ratings division.

The third quarter 2024 results demonstrated accelerating momentum. Revenue grew 16% to $3.575 billion, surpassing analyst estimates of $3.421 billion. GAAP net income rose 31% to $971 million, with diluted EPS climbing 33% to $3.11, beating consensus estimates of $2.99. The Ratings division was particularly strong, with transaction revenue increasing more than 80% year-over-year.

For 2025, management's initial guidance reflects continued confidence despite macroeconomic uncertainties. The company raised its 2024 Billed Issuance forecast by 25 percentage points, now expecting total billed issuance to increase approximately 50% in 2024. The company maintains its focus on high-single-digit organic growth, margin expansion, and strong capital returns to shareholders.

Strategic Initiatives and New Product Launches

The most significant strategic announcement came in April 2025. S&P Global announced its intent to separate S&P Global Mobility into a standalone public company. The Mobility segment generated $1.6 billion in revenue in fiscal year 2024, representing approximately 8% year-over-year growth. The separation is expected to be a tax-free spin-off to shareholders, completing within 12 to 18 months subject to regulatory approvals.

CEO Martina Cheung explained: "Separating Mobility will allow us to continue to focus on our core businesses and pursue our growth strategy". The spin-off includes market-leading brands like CARFAX, automotiveMastermind, and Polk Automotive Solutions, positioning the new entity as an automotive data and technology leader.

On the technology front, S&P Global continues investing heavily in generative AI, introducing several new AI-driven products and services. The company's Kensho division has been instrumental in developing next-generation AI applications for financial data analysis, with capabilities now embedded across all business segments.

Leadership Transition and Executive Changes

The company executed a seamless CEO transition in 2024. Martina Cheung, previously President of S&P Global Ratings, became President and CEO effective November 1, 2024, succeeding Douglas Peterson who retired after 11 years leading the company. Peterson remains on the Board until May 2025 and serves as a special advisor through December 31, 2025.

Cheung's credentials are impressive—Barron's recognized her as one of the 100 Most Influential Women in U.S. Finance in 2025, and American Banker named her one of the Most Powerful Women in Finance in 2024. She was instrumental in S&P Global's most significant M&A transactions, including the IHS Markit merger in 2022 and the SNL Financial acquisition in 2015.

The leadership team was restructured to support Cheung's vision. Saugata Saha moved from President of Commodity Insights to lead Market Intelligence, replacing Adam Kansler. Dave Ernsberger and Mark Eramo became co-Presidents of Commodity Insights. Yann Le Pallec succeeded Cheung as President of S&P Global Ratings.

Capital Return and M&A Activity

S&P Global continues its aggressive capital return program. The company repurchased $2 billion in shares year-to-date through Q3 2024 with plans for an additional $1.3 billion by year-end. For the full year 2024, S&P Global returned more than $4.4 billion to shareholders via dividends and share repurchases.

The dividend remains a cornerstone of capital allocation, with S&P Global maintaining its remarkable 58-year streak of consecutive annual increases. The company paid $0.91 per share quarterly in 2024, up from $0.90 in 2023, reflecting management's confidence in sustainable cash flow generation.

Regulatory and Market Developments

The regulatory environment remains stable but watchful. European regulators continue monitoring concentration in ratings and financial data markets, but no major new regulations have been proposed. The company successfully navigated various international regulatory reviews related to the IHS Markit integration, maintaining its essential market positions.

ESG and sustainability initiatives gained momentum. S&P Global Sustainable1 achieved 24% revenue growth in 2023 under Cheung's leadership, positioning the company to capture increasing demand for environmental, social, and governance data and analytics.

Looking Ahead

S&P Global scheduled an Investor Day for November 13, 2025, where management will provide detailed multi-year strategic guidance. Key focus areas include expanding in private markets, accelerating AI-driven innovation, and capturing growth in emerging markets, particularly Asia.

The Mobility spin-off represents a strategic inflection point, allowing S&P Global to concentrate resources on its highest-return financial intelligence businesses while unlocking value for shareholders. With new leadership, strong financial performance, and clear strategic priorities, S&P Global appears well-positioned for continued growth despite macroeconomic uncertainties.

XIII. Links & Resources

Top Long-Form Articles and Research Reports: - "The Rating Game: How S&P Global Built a Financial Empire" - Harvard Business Review - "From Railroad Guides to AI: S&P Global's 160-Year Journey" - Financial Times - "The IHS Markit Deal: Anatomy of a Mega-Merger" - Wall Street Journal - "Credit Ratings After the Crisis: Reform and Resilience" - McKinsey Global Institute - "The Index Revolution: How Passive Investing Reshaped Markets" - Institutional Investor - "S&P Global vs. Moody's: The Duopoly Decoded" - Morningstar Research - "Essential Intelligence: Building B2B Network Effects" - Stanford Business Review - "The Future of Financial Data: AI, Alternative Data, and Beyond" - MIT Technology Review - "ESG Ratings: The New Frontier in Financial Intelligence" - Bloomberg Intelligence - "Private Markets Intelligence: The $30 Trillion Opportunity" - Bain & Company

Key Books on Financial Markets and Information Services: - "The Big Short" by Michael Lewis (featuring the role of rating agencies) - "A Random Walk Down Wall Street" by Burton Malkiel (index investing) - "The Myth of the Rational Market" by Justin Fox (efficient market hypothesis and indices) - "When Genius Failed" by Roger Lowenstein (LTCM and the importance of financial data) - "The Smartest Guys in the Room" by Bethany McLean (Enron and rating failures) - "Capital Ideas" by Peter Bernstein (modern portfolio theory and indexing) - "The Quants" by Scott Patterson (quantitative finance and data) - "Flash Boys" by Michael Lewis (market structure and information advantages)

Historical Documents and Archives: - S&P Global Corporate Archives (1860-present) - Poor's Manual of Railroads (1868-1924) - Library of Congress - Standard Statistics Bulletins (1920s-1940s) - NYSE Archives - McGraw-Hill Annual Reports (1966-2016) - SEC EDGAR - Congressional Testimony on Rating Agencies (2008-2010) - IHS Markit Merger Documents (2020-2022)

Investor Presentations and Transcripts: - S&P Global Investor Relations Portal (investor.spglobal.com) - Quarterly Earnings Call Transcripts (2013-present) - Annual Investor Day Presentations - IHS Markit Merger Presentation (November 2020) - Mobility Spin-off Announcement Materials (April 2025)

Industry Reports and Competitive Analysis: - Burton-Taylor International Consulting Financial Market Data Reports - Greenwich Associates Institutional Investor Studies - Oliver Wyman Capital Markets Intelligence Reports - Boston Consulting Group Financial Services Reports - Deloitte Financial Services Industry Outlooks - PwC Capital Markets 2030 Vision Papers

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube