AGI Greenpac: From Sanitaryware Pioneer to India's Glass Packaging Powerhouse

I. Introduction & Episode Setup

Picture this: A modest collaboration in 1960 between an Indian industrialist family and a British sanitaryware company would eventually transform into India's second-largest glass packaging empire, commanding 17-20% market share of the organized glass packaging industry. This is the story of AGI Greenpac—a company that pivoted from toilets to bottles, survived multiple economic cycles, executed complex demergers, and emerged as a focused packaging powerhouse serving over 500 global clients.

The journey from Hindustan Twyfords to AGI Greenpac reads like a masterclass in corporate transformation. It's a saga of ambitious acquisitions of distressed assets, bold strategic pivots, and sometimes controversial decisions that would make or break shareholder value. The company manufactures and sells Container Glass bottles, PET bottles and Security Caps and Closures under Packaging Products segment, holding a 17%-20% market share.

But here's the fundamental question that drives this entire narrative: How did a British collaboration sanitaryware company, founded to bring modern bathroom fixtures to newly independent India, become the country's leading sustainable glass packaging player? And more importantly, what can investors learn from its six-decade journey of reinvention, demergers, and strategic U-turns?

The answer lies in understanding the Somany family's unique ability to spot opportunities in distress, their willingness to completely reimagine their business model multiple times, and their sometimes controversial corporate restructuring decisions that continue to divide market opinion even today.

II. Origins: The Somany Family & Twyfords Collaboration (1960-1980)

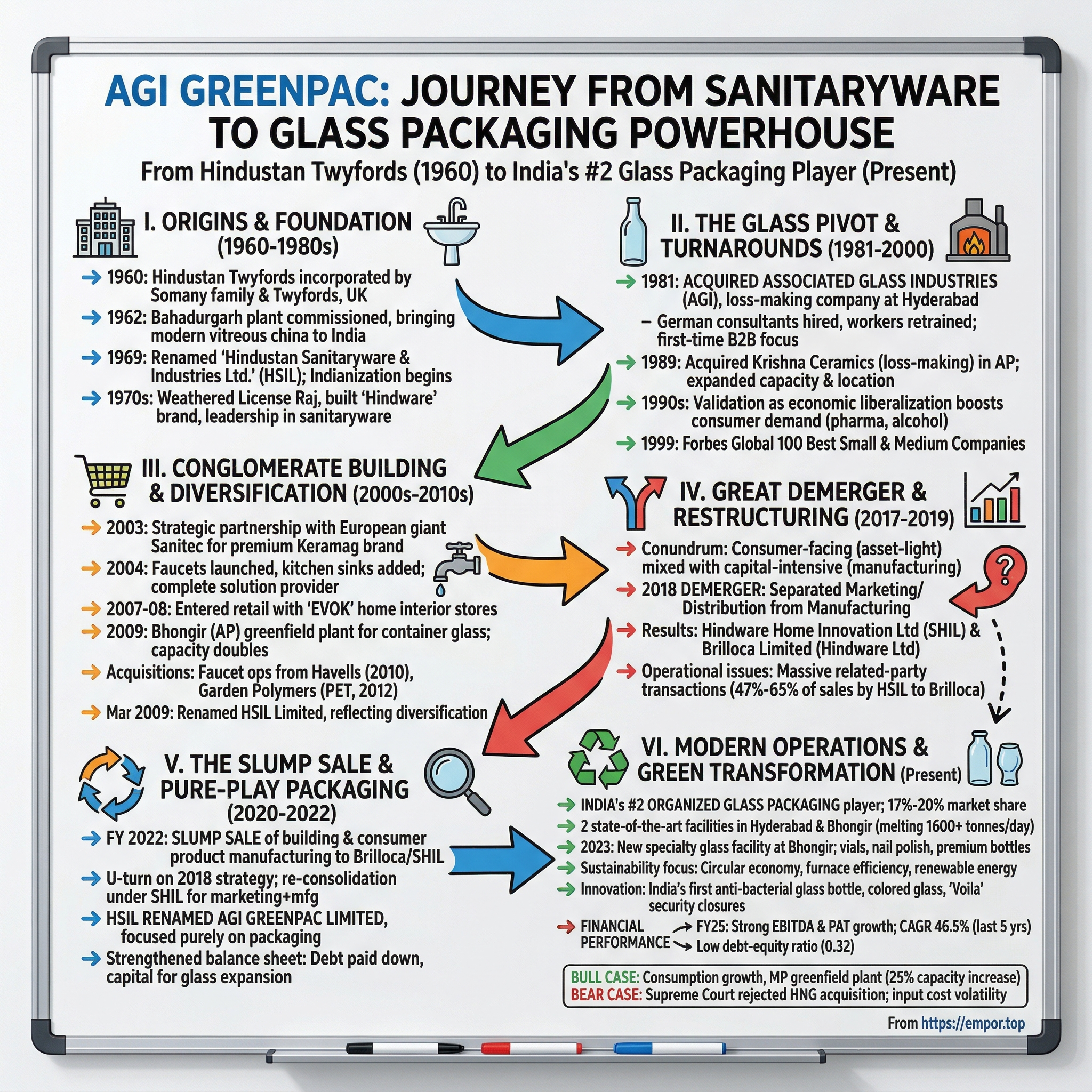

The monsoon rains had just begun sweeping across North India in 1960 when the Somany family signed papers that would launch one of India's most enduring industrial stories. AGI Greenpac was incorporated as Hindustan Twyfords in 1960 by the Somany family (promoter group) in collaboration with Twyfords, UK, to introduce vitreous china ceramic sanitaryware in India.

This wasn't just another foreign collaboration—it was a bet on modernizing India's bathroom habits. The Somanys recognized that post-independence India, with its ambitious nation-building projects and emerging middle class, would need modern sanitaryware. The timing was prescient. India was transitioning from traditional Indian-style toilets to Western-style fixtures, driven by urbanization and changing lifestyles.

In 1962, the sanitaryware plant was commissioned at Bahadurgarh and the plant was inaugurated by the then Chief Minister of Punjab Sardar Kairon. The choice of Bahadurgarh, then a small town in Haryana (previously part of Punjab), was strategic—close enough to Delhi for market access, yet far enough to secure land at reasonable prices. The inauguration by the Chief Minister wasn't mere ceremony; it signaled government backing for industrial modernization.

The early years tested the Somanys' resolve. Selling vitreous china sanitaryware in a price-conscious market dominated by traditional methods required not just manufacturing prowess but market education. They had to convince architects, builders, and ultimately consumers that modern sanitaryware was worth the premium. The company persevered, gradually building the Hindware brand that would become synonymous with quality bathroom fixtures.

By 1969, the partnership dynamics had shifted. The company changed their name from Hindustan Twyfords Limited to Hindustan Sanitary ware & Industries Limited. This wasn't merely cosmetic—it signaled the Indianization of the venture and the Somany family's increasing control. The dropping of "Twyfords" from the name reflected growing confidence in indigenous capabilities and perhaps tensions in the foreign collaboration, common in that era of license raj.

The 1970s proved challenging yet formative. India's socialist policies, foreign exchange crises, and limited consumer purchasing power constrained growth. Yet HSIL (as it became known) steadily expanded its product range and distribution network. The company learned to navigate India's complex regulatory environment, manage working capital in a cash-constrained economy, and build relationships with architects and contractors—skills that would prove invaluable in future pivots.

By 1980, HSIL had established itself as India's sanitaryware leader. The Hindware brand commanded premium positioning. The company had weathered the turbulent 1970s and built manufacturing expertise, distribution networks, and brand equity. But the Somanys were about to make a decision that would fundamentally alter the company's trajectory—venturing into an entirely different industry.

III. The Glass Container Pivot: AGI Acquisition (1981-2000)

The year 1981 marked a defining moment in HSIL's evolution. HSIL acquired Associated Glass Industries Limited (AGI), a loss making and closed company at Hyderabad. On paper, this looked irrational—why would a successful sanitaryware company acquire a failed glass manufacturer in a completely unrelated business? The answer reveals the Somany family's contrarian investment philosophy.

Associated Glass Industries wasn't just distressed; it was dead. The plant had been shut, workers had dispersed, and creditors had written off hopes of recovery. But where others saw industrial wreckage, the Somanys saw opportunity. Glass container manufacturing, they recognized, had structural similarities to sanitaryware—both involved kilns, high-temperature processes, and silica-based raw materials. More importantly, India's packaged goods industry was nascent but growing.

The turnaround wasn't immediate. Restarting a shuttered glass plant required technical expertise HSIL didn't possess. They hired German consultants, retrained workers, and essentially rebuilt the furnaces. The first few years hemorrhaged cash. Board members questioned the wisdom of subsidizing a loss-making venture with sanitaryware profits. But the Somanys persisted, viewing it as patient capital investment in India's consumption story.

The strategic rationale gradually became clearer. India's pharmaceutical industry was beginning its global ascent. The alcohol industry was modernizing beyond country liquor. Food processing was shifting from loose to packaged goods. All needed glass containers—a packaging material that was chemically inert, infinitely recyclable, and premium in perception. HSIL had stumbled into supplying the packaging for India's consumption boom.

In 1989, HSIL acquired Krishna Ceramics Ltd, manufacturers of Sanitaryware at Bibinagar (AP), a loss making company. This acquisition followed the same playbook—acquire distressed assets, inject capital and expertise, achieve turnaround. The Bibinagar acquisition served dual purposes: expanding sanitaryware capacity while gaining another manufacturing location in South India, important for logistics in glass distribution.

The 1990s brought validation of the glass strategy. Economic liberalization unleashed consumer demand. Multinational FMCG companies entered India, demanding quality packaging. The beer industry exploded with brands like Kingfisher. Pharmaceutical exports required international-standard glass vials. AGI, once a failed venture, became HSIL's growth engine.

In 1999, HSIL was rated one of Forbes Global 100 Best Small & Medium Companies (Revenues less than U.S.$500 million per annum). This international recognition was remarkable for an Indian company in that era. It validated the Somany family's strategy of acquiring and turning around distressed assets. The Forbes recognition also helped in international partnerships and technology acquisitions that would fuel future growth.

The glass container business fundamentally changed HSIL's DNA. The company learned to serve institutional clients rather than retail consumers. It mastered B2B relationship management, technical customization, and just-in-time delivery. These capabilities would prove crucial as HSIL evolved from a sanitaryware company with a glass division to something entirely different—a diversified conglomerate.

IV. Building a Conglomerate: Diversification & Brand Building (2000-2010)

The new millennium found HSIL at a crossroads. The company had two successful but distinct businesses—consumer-facing sanitaryware and B2B glass containers. Rather than choosing between them, the Somanys decided to double down on both while adding new verticals. This era would see HSIL transform into a sprawling conglomerate.

In 2003, HSIL signed a strategic partnership with European sanitaryware giant Sanitec, bringing the brand Keramag to Indian consumers. This partnership was more than just brand licensing. Sanitec brought European designs, quality standards, and technical know-how. For HSIL, it meant premiumization—moving beyond basic sanitaryware to designer bathrooms. The Keramag brand targeted India's emerging affluent class, willing to pay premiums for European aesthetics.

2004 saw the launch of Hindware faucets and entry into the kitchen segment with stainless steel sinks. This expansion followed consumer logic—customers renovating bathrooms often redid kitchens simultaneously. By offering complete solutions, HSIL could capture larger wallet share and improve dealer economics. The faucets launch particularly was strategic, as it moved HSIL from ceramics into metal working, requiring new manufacturing capabilities.

But the most significant expansion came in glass containers. In the year 2009, the company set up second green field container glass factory at Bhongir, Andhra Pradesh with a production capacity of 425 tonnes per day. This wasn't just capacity addition—it was a statement of intent. The Bhongir plant incorporated state-of-the-art technology, including furnaces from SORG Germany. The location in Andhra Pradesh provided access to South Indian markets and raw materials.

The retail ambition emerged in 2007-08 when the company through their subsidiary, Hindware Home Retail Pvt. Ltd., forayed into the retail sector. They launched Home Interior Fashion Mega stores providing speciality home interior solutions under the EVOK Brand. They opened their first EVOK store Faridabad, Haryana. EVOK represented HSIL's boldest diversification—from manufacturing to retail. The vision was to create India's answer to IKEA, offering complete home solutions.

Subsequent acquisitions, like the faucet operations from Havells India in 2010 and the merging of Garden Polymers Private Ltd in 2012, diversified AGI's product offerings. The Havells faucet acquisition was particularly strategic. Havells, primarily an electrical company, had struggled with faucets. For HSIL, it meant instant market share, established dealers, and manufacturing facilities. The Garden Polymers merger brought PET bottle capabilities, diversifying beyond glass.

The transformation of HSIL in this decade was remarkable. The name was changed from Hindustan Sanitaryware & Industries Limited to HSIL Limited in March, 2009. The abbreviated name reflected the company's evolution beyond just sanitaryware. HSIL was now a building products company (sanitaryware, faucets), a consumer products company (water heaters, kitchen appliances), a packaging products company (glass, PET), and a retail company (EVOK).

Each business had different economics, customer bases, and competitive dynamics. Sanitaryware was mature with steady margins. Glass containers grew rapidly but required constant capital investment. Consumer products offered brand extension opportunities. Retail promised direct consumer connect but bled cash. Managing this complexity required sophisticated corporate structure—setting the stage for the dramatic restructuring ahead.

V. The Great Demerger: Strategic Restructuring (2017-2019)

In the boardrooms of Gurugram in 2017, the Somany family faced a conundrum that had been brewing for years. HSIL had become a complex conglomerate where consumer businesses requiring brand investment were bundled with capital-intensive manufacturing operations. The market couldn't properly value this hybrid, and investors complained about the lack of focus.

In 2018, pursuant to the composite scheme of arrangement, HSIL Limited demerged marketing & distribution of Consumer Products and Retail Divisions to Somany Home Innovation Limited (SHIL) now known as Hindware Home Innovation Limited. Further, marketing and distribution of Building Products of HSIL Limited was demerged into Brilloca Limited now known as Hindware Limited, a wholly owned subsidiary of SHIL.

The demerger architecture was complex but strategic. The idea was to separate asset-light, consumer-facing businesses from asset-heavy manufacturing. SHIL would house marketing and distribution for consumer products and retail. Brilloca, as SHIL's subsidiary, would handle building products distribution. HSIL would retain all manufacturing assets and the packaging business.

The rationale seemed compelling. The objective was to separate consumer facing businesses and create an asset-light company. Asset-light businesses typically commanded higher valuations due to superior return ratios. Manufacturing businesses, while cash generative, traded at lower multiples. By separating them, each entity could attract its natural investor base—growth investors for SHIL, value investors for HSIL.

Yet, the execution revealed immediate challenges. HSIL continued to manufacture goods for SHIL. This created massive related-party transactions. Effectively sale to Brilloca accounted for circa 47% & 65% in FY 2021 & FY 2022 respectively of total sales by HSIL. Around 70% of the raw material of Brilloca was sourced from HSIL. The supposedly independent entities were operationally intertwined.

The market reaction was tepid. Instead of unlocking value, the demerger created confusion. Investors struggled to understand the web of inter-company transactions. Analysts questioned whether genuine value creation occurred or if it was merely financial engineering. The promoter holdings told an interesting story—on the record date of demerger (2019), the promoter holding 49.34% in HSIL got mirrored in SHIL on the listing. The promoters increased their holding in SHIL to 51.2% while in HSIL, the promoter holding jumped to 60.24%.

The operational complexities became apparent quickly. Coordinating production (at HSIL) with marketing (at SHIL) across corporate boundaries proved challenging. Transfer pricing became contentious. Working capital management grew complex with inter-company receivables. The grand vision of focused, nimble entities was getting lost in operational friction.

Meanwhile, minority shareholders questioned the fairness. Were transfer prices between entities at arm's length? Was value being shifted between listed entities? The regulatory scrutiny increased. Related party transaction approvals became routine board agenda items. What was meant to simplify had complicated everything.

VI. The Slump Sale & Pure-Play Pivot (2020-2022)

Just as the market was digesting the demerger, HSIL's board dropped a bombshell that shocked investors and validated skeptics' worst fears about the 2018 restructuring.

In a complete U-turn of the strategy based on which demerger was done, in FY 2022, manufacturing facilities for building products and consumer products were sold on slump sale basis to the resulting company. The slump sale saw the building products manufacturing business transferred to Hindware Limited (formerly Brilloca), SHIL's subsidiary, for Rs 630 crores.

The reversal was stunning in its admission of strategic failure. The separation of manufacturing from marketing, implemented just three years earlier, was being undone. The BPD Undertaking was transferred to, and vested in, Brilloca Limited (now known as Hindware Limited) as on the Effective Date. The proceeds from this slump sale will be utilised towards the pre-payment of existing bank borrowings which will further strengthen the Company's balance sheet and create capital to further expand its packaging business.

The management offered a new narrative. Rather than the conglomerate structure being the problem, it was the split between manufacturing and marketing that hadn't worked. The future lay in focus—HSIL would become a pure-play packaging company. The building products and consumer products businesses would be consolidated under SHIL. Clean, simple, focused.

To signal this transformation, Somany Home Innovations Limited was renamed as Hindware Home Innovation Limited while its key subsidiary Brilloca Limited changed its name to Hindware Limited. HSIL Limited also changed its name to AGI Greenpac Limited. The AGI Greenpac name harked back to the 1981 acquisition that had started the glass journey. "Greenpac" emphasized sustainability, increasingly important in packaging.

Mr. Sandip Somany, Vice-Chairman & Managing Director, AGI Greenpac, said: "The company's corporate rebranding is a strategic step, and the new name AGI Greenpac reflects the company's renewed market positioning post the completion of the divestment of Building Products Division. This new name and brand perfectly illustrate our commitment to expand the sustainable packaging business and remain one of the most profitable packaging companies in India."

The slump sale proceeds strengthened AGI Greenpac's balance sheet significantly. Debt was paid down, improving credit metrics. The company could now focus entirely on glass containers, PET bottles, and security caps—businesses with different dynamics than sanitaryware. The market began warming to the story of a focused packaging player riding India's consumption boom.

But questions lingered about corporate governance. Had the 2018 demerger been a mistake, or was it designed to fail? Why did it take just three years to reverse course? The slump sale valued the building products business at Rs 630 crores—was this fair value? Minority shareholders who had suffered through the demerger complexity wondered if their interests had been adequately protected.

Despite controversies, AGI Greenpac emerged from this restructuring as a focused entity. The company was no longer pulled between B2C and B2B businesses, between asset-light and asset-heavy models, between regional and national markets. It was now purely a packaging company, serving institutional clients, with clear metrics and strategy.

VII. The HNG Acquisition Saga & Supreme Court Drama (2022-2025)

The conference rooms at AGI Greenpac's Gurugram headquarters buzzed with anticipation in 2022. The company was pursuing its most ambitious acquisition yet—Hindustan National Glass & Industries Limited (HNG), India's largest container glass manufacturer. Success would transform AGI from challenger to champion. Failure would question management credibility. What unfolded was a three-year corporate drama culminating in Supreme Court intervention.

Hindustan National Glass & Industries Ltd (HNG), India's largest container glass manufacturer, was undergoing insolvency resolution. The proposed acquisition of HNG by AGI Greenpac, the second-largest player in the industry, has triggered concerns among smaller manufacturers. While this acquisition promises to resolve HNG's financial woes, it has sparked fears of creating a monopolistic market structure, potentially driving smaller businesses out of competition.

The opportunity was tantalizing. HNG holds a 60 per cent market share in the glass packaging industry in India and has manufacturing plants located in Bahadurgarh (Haryana), Rishra (West Bengal), Neemrana (Rajasthan), Naidupeta (Andhra Pradesh), Sinnar (Maharashtra), Puducherry, and Rishikesh (Uttarakhand). Combined with AGI's operations, the merged entity would command overwhelming market share, creating India's undisputed glass packaging leader.

Back in 2024, Agi Greenpac was in focus after getting a green light from legal authorities for the acquisition of Hindustan National Glass (HNGL). After a series of delays, Agi received the approval of acquisition in 2024 under the corporate insolvency resolution process (CIRP) under Insolvency and Bankruptcy Code 2016. The Committee of Creditors had approved AGI's resolution plan with overwhelming 98% support, valuing the transaction at Rs 2,210 crores.

However, the acquisition faced an unusual adversary—Independent Sugar Corporation (INSCO), backed by East Africa's Madhvani Group. INSCO had also bid for HNG and secured Competition Commission approval before AGI. The legal battle that ensued would test the intersection of insolvency law and competition law, raising fundamental questions about market concentration.

The Competition Commission of India's role became controversial. The Herfindahl-Hirschman Index (HHI), a key metric for market concentration, already places India's container glass industry at 2,919, indicating significant consolidation (uncompetitive). Further mergers/acquisitions could push the market into uncompetitive territory. Small manufacturers in Firozabad, India's "Glass City," feared extinction if AGI-HNG combine proceeded.

The case escalated through legal hierarchies. The National Company Law Appellate Tribunal upheld CCI's approval, but concerns persisted. The procedural question—whether Committee of Creditors could approve a resolution plan before CCI clearance—became central. This wasn't just about AGI and HNG; it would set precedent for all future insolvency resolutions involving market concentration.

Then came the Supreme Court bombshell. In an interesting turn of events, the Supreme Court recently rejected Agi Greenpac's resolution plan for Hindusthan National Glass. The court stated that fresh resolution plans have to be considered for the insolvency. The judgment was categorical: AGI Greenpac's resolution plan is unsustainable as it failed to secure prior approval from the CCI, as mandated under the proviso to Section 31(4) of the Insolvency and Bankruptcy Code (IBC). Consequently, the approval granted by the Committee of Creditors (CoC) to the resolution plan dated October 28, 2022, without the requisite CCI approval, cannot be sustained and is hereby set aside and quashed.

The market reaction was swift and brutal. AGI Greenpac shares declined as much as 19 per cent on Wednesday following the verdict. The stock had already been under pressure—Agi Greenpac has a 52-week high of Rs 1,300 touched on 20 December 2024 and a 52-week of Rs 610 touched on 4 June 2024. In the past 1 year, shares of the company are down 11%.

The Supreme Court verdict raised profound questions about AGI's strategy. Was the HNG acquisition essential for growth, or was organic expansion sufficient? Had management been overconfident about regulatory approvals? The company's response was measured but revealed contingency planning: if the acquisition didn't proceed, focus would shift to organic expansion including debottlenecking to enhance volumes.

VIII. Modern Operations & Green Transformation (2020-Present)

While the HNG saga captured headlines, AGI Greenpac quietly built one of India's most sophisticated packaging operations. The transformation from a conglomerate's division to a focused packaging leader required operational excellence, technological advancement, and strategic positioning in high-growth segments.

The company's manufacturing footprint tells a story of calculated expansion. With two state of the art manufacturing facilities, one in Hyderabad and the other at Bhongir (Telangana) both strategically located in South – Central India, where key raw materials are available in abundance and the shipping of finish goods by road, rail as well as by sea (through ICD) is extremely cost effective. With Hyderabad and Bhongir facilities put together, AGI melts 1600+ tonnes of glass per day.

The crown jewel of recent expansion was the specialty glass facility. In 2023, it inaugurated a specialty glass facility at Bhongir, with a production capacity of 154 tonnes per day. This wasn't just capacity addition—it was a strategic pivot toward higher-margin products. The plant manufactures clear glass products, such as vials, nail polish bottles, and other specialty glass products which are primarily used in the packaging of cosmetics and perfumery, pharmaceuticals, premium spirits, food & beverages water bottles, and candles jars.

The move into specialty glass reflected deeper market understanding. Mass-market bottles competed on cost, where unorganized players had advantages. Specialty glass demanded precision, customization, and quality—areas where AGI's technical capabilities shone. Perfume bottles with complex shapes, pharmaceutical vials meeting stringent standards, craft spirit bottles telling brand stories—these commanded premiums and customer stickiness.

Sustainability became central to AGI's positioning. The "Greenpac" rebranding wasn't mere marketing. Glass inherently offers environmental advantages—infinitely recyclable, chemically inert, no microplastics. AGI amplified these benefits through operational improvements. Furnace efficiency increased through German technology. Cullet (recycled glass) usage grew. Solar installations reduced carbon footprint.

Innovation distinguished AGI from competitors. The company claimed several firsts: India's first anti-bacterial glass bottle, eco-friendly wellness glass containers, colored glass capabilities including cobalt blue and smoke variants. The coloring forehearth technology at Bhongir enabled quick color changes, allowing customization previously impossible in India. This meant craft breweries could order smaller batches in unique colors, pharmaceutical companies could differentiate through packaging.

The closure and caps business added another dimension. AGI Greenpac continued its legacy of innovation by launching specialized closures under the Voila brand in 2021. The recent addition of products like SuperCap and NipAce has solidified AGI's reputation as a leader in innovative packaging solutions. Security closures addressed counterfeiting concerns in pharmaceuticals and spirits. Tamper-evident features became selling points for brand owners concerned about authenticity.

Customer relationships evolved from transactional to strategic. AGI worked with clients from product conception, designing bottles that enhanced brand identity while optimizing production efficiency. The company's design studio, mold manufacturing, and Applied Ceramic Labeling facilities created an integrated ecosystem. Clients could conceptualize, prototype, and scale production without leaving AGI's orbit.

The operational metrics reflected this transformation. Capacity utilization consistently exceeded 95%, sometimes reaching 103% through debottlenecking. Customer concentration reduced as the base expanded beyond 500 institutional clients. Product mix shifted toward higher-margin specialty products. Working capital cycles improved through better forecasting and inventory management.

IX. Financial Performance & Market Position (2020-2025)

The numbers tell a story of resilience and growth that vindicated AGI Greenpac's strategic focus on packaging. Despite macroeconomic headwinds, pandemic disruptions, and the HNG acquisition uncertainty, the company delivered consistent financial performance that impressed even skeptics.

For the first nine months of this financial year (FY25), Agi Greenpac's total income has increased to Rs 18.6 bn, with EBITDA growing by 15.1% year-on-year (YoY) to Rs 5 bn. The company's net profit for the same period grew by 20.9% YoY to Rs 2.3 bn. These weren't just pandemic recovery numbers—they reflected fundamental business strength.

The full fiscal year 2025 results were even more impressive. AGI achieved a strong EBITDA growth of 17% Y-o-Y to INR 689-crore in FY25, and its revenue from operations reached INR 2529-crore, registering year-over-year growth of 5% compared to INR 2418-crore in FY24. The EBITDA margin of 27% stood out in a capital-intensive industry, reflecting pricing power and operational efficiency.

Profit After Tax (PAT) for the year stood at ₹322 crore, up by 28% compared to ₹251 crore in FY24. The PAT growth outpacing revenue growth indicated improving margins and cost control. This wasn't just volume-driven growth—it was profitable expansion, the kind that creates shareholder value.

The balance sheet transformation was equally impressive. Company has reduced debt. The debt-equity ratio of 0.32 represented the lowest level in recent history, providing financial flexibility for growth investments. This deleveraging occurred despite capacity expansions, indicating strong cash generation.

Quarterly performances showed consistency. The company's EBITDA for the quarter stood at INR 191-crore, up 23% from INR 156-crore from the same period last year, resulting in an EBITDA margin of 27%. Profit After Tax (PAT) reached INR 97-crore, a significant 50% rise from INR 65-crore recorded in Q4 FY24. Such quarter-on-quarter improvements indicated momentum, not just one-off gains.

The market share story provided context for financial performance. AGI holds a 17%-20% market share, making it the second-largest player in the Indian organized glass packaging industry by installed capacity. This position provided pricing discipline while leaving room for market share gains. Unlike monopolistic complacency or cut-throat competition, AGI operated in a sweet spot.

Segment performance revealed strategic success. The specialty glass facility, despite being new, achieved rapid utilization. Higher realization products—cosmetics bottles, pharmaceutical vials, premium spirit bottles—grew faster than commodity segments. The closure business, though smaller, showed promising trajectory with innovative security features commanding premiums.

The stock market's reaction was volatile but ultimately positive. From the 52-week low of Rs 599 to high of Rs 1,307, the stock showed both opportunity and risk. Company has delivered good profit growth of 46.5% CAGR over last 5 years. This long-term performance reflected fundamental value creation beyond short-term market gyrations.

X. Playbook: Business & Strategy Lessons

The AGI Greenpac journey offers a masterclass in several strategic principles that transcend industries and geographies. These aren't theoretical concepts but battle-tested strategies refined over six decades.

The Art of Turnaround Acquisitions

The Somany family's greatest skill might be seeing value where others see disaster. The AGI acquisition in 1981 and Krishna Ceramics in 1989 followed the same template: acquire shut plants at distressed valuations, inject capital and expertise, achieve operational turnaround. This isn't financial engineering—it requires operational excellence, patience, and conviction. The key insight: distressed assets aren't just cheap; they come with established locations, licenses, and sometimes dormant customer relationships that would take years to build organically.

Demerger as Value Creation (or Destruction?)

The 2018 demerger and 2022 reversal provide a cautionary tale about corporate restructuring. The original logic—separating asset-light from asset-heavy businesses—was textbook strategy. The execution revealed that operational realities trump financial theory. When 70% of your revenues come from inter-company transactions, you haven't created independent entities; you've created complexity. The lesson: corporate structure must follow operational logic, not vice versa.

Focus vs. Diversification Timing

AGI Greenpac's evolution shows both strategies can work—if timed correctly. Diversification (2000-2017) made sense when core markets were maturing and India's consumption boom offered multiple opportunities. Focus (2022 onwards) became necessary when complexity costs exceeded diversification benefits and when the packaging market itself became large enough to sustain growth. The key is recognizing when to switch strategies.

Building in Emerging Markets

Operating in India taught AGI Greenpac unique skills. Managing working capital when customers delay payments, maintaining quality when input materials vary, dealing with infrastructure constraints, navigating regulatory complexity—these capabilities become competitive advantages. Emerging market companies that master these challenges often prove more resilient than developed market peers.

Family Ownership Dynamics

The Somany family's continued control—now exceeding 60%—provides both stability and controversy. Long-term thinking enabled patient investments in turnarounds and new facilities. But the same control allowed dramatic strategic reversals that left minority shareholders questioning governance. The lesson: family ownership is neither inherently good nor bad; it amplifies both visionary leadership and governance concerns.

Sustainability as Strategy, Not CSR

AGI Greenpac's pivot to "Greenpac" wasn't greenwashing. Glass packaging inherently aligns with circular economy principles. By emphasizing these advantages—infinite recyclability, no chemical leaching, premium perception—AGI positioned itself favorably against plastic alternatives facing regulatory backlash. Sustainability became competitive advantage, not compliance burden.

XI. Bear vs Bull Case

Bull Case: The Optimist's View

The bulls see AGI Greenpac as a compelling play on India's consumption story with multiple growth drivers. The India Glass Packaging Market is expected to reach USD 9.94 billion in 2025 and grow at a CAGR of 3.98% to reach USD 12.08 billion by 2030. AGI, as the second-largest player, is well-positioned to capture this growth.

The upcoming capacity expansion validates the growth thesis. AGI Greenpac Limited announced setting up of a state-of-the-art greenfield, high-output and high-efficiency manufacturing plant in Madhya Pradesh with capital expenditure outlay of ~₹700 Crore. This 25% capacity increase, operational within 24 months, will capture growing demand without waiting for acquisitions.

Financial metrics support optimism. EBITDA margins at 27% rank among the best globally in glass packaging. The debt-equity ratio of 0.32 provides the balance sheet strength for organic and inorganic growth. Return on capital employed exceeding 17% indicates efficient capital allocation. The management's ability to grow PAT at 46.5% CAGR over five years demonstrates execution capability.

Sustainability tailwinds strengthen the bull case. Single-use plastic bans, Extended Producer Responsibility regulations, and consumer preference for eco-friendly packaging favor glass. AGI's established capabilities in recycling, furnace efficiency, and renewable energy position it as a sustainability leader. Premium brands increasingly choose glass for its environmental credentials—a secular trend benefiting AGI.

Market position provides competitive advantages. As the second-largest player, AGI enjoys economies of scale while avoiding monopolistic scrutiny. The 500+ institutional client base provides revenue stability. Specialty glass capabilities create differentiation from commodity players. The integrated model—from design to manufacturing to closures—creates customer stickiness.

Bear Case: The Skeptic's Concerns

Bears point to the failed HNG acquisition as revealing management overreach. The Supreme Court rejection not only eliminated a growth avenue but raised questions about management judgment. The Rs 2,210 crore that would have gone to HNG might have been better deployed in organic expansion without legal complications. The time and resources spent on a failed acquisition represent opportunity costs.

Competition concerns persist despite market position. The unorganized sector, while lacking sophistication, competes aggressively on price in commodity segments. Chinese imports, though limited currently, could increase if currency dynamics change. New technologies like aluminum cans or sustainable plastics could disrupt glass packaging's advantages. The bear case sees AGI as vulnerable to both low-cost and high-tech competition.

Input cost volatility threatens margins. Natural gas, a key fuel for furnaces, faces both price volatility and supply uncertainty. Soda ash, silica sand, and other raw materials link to commodity cycles. While AGI has pricing power, significant input inflation might not be fully passable, pressuring margins. The capital-intensive nature means operating leverage works both ways.

Corporate governance concerns linger from the demerger-reversal episode. The rapid strategic U-turns, complex related party transactions, and concentrated promoter ownership raise minority shareholder concerns. While legal, these actions create trust deficits that might result in valuation discounts. The bears argue that governance concerns offset operational strengths.

Valuation appears stretched to bears. Agi Greenpac has a 52-week high of Rs 1,300 touched on 20 December 2024 and a 52-week of Rs 610 touched on 4 June 2024. The volatility—stock down 45% in two months—reflects uncertainty about growth trajectory post-HNG rejection. Bears see limited upside from current levels given execution risks.

XII. Epilogue: What's Next for AGI Greenpac?

Standing at this inflection point in late 2025, AGI Greenpac faces a future both promising and uncertain. The failed HNG acquisition forces a recalibration—but perhaps that's beneficial. Organic growth, while slower, avoids integration risks and regulatory complications.

The Madhya Pradesh expansion represents the immediate future. The new plant, set to produce 500 tonnes of commercial glass daily, will serve key sectors such as alcoholic beverages, pharmaceuticals, and food. The company anticipates commencing production within 24 months, demonstrating its commitment to efficient project execution and swift market responsiveness. This expansion alone could drive 25% capacity growth, sufficient for several years of demand growth.

Beyond glass, AGI is eyeing adjacencies. Aluminum cans represent a logical extension—serving similar customers (beverages) with different packaging solutions. The company has hinted at evaluating this opportunity, which could open new growth avenues without straying from core packaging competence. The specialty glass success suggests AGI can premiumize commodity products through innovation and service.

India's packaging transformation is just beginning. E-commerce drives demand for protective packaging. Pharmaceutical exports require international-standard primary packaging. Craft beverages, premium foods, and natural cosmetics seek differentiated packaging. AGI's capabilities align with these trends. The company doesn't need to capture entire market growth—maintaining share in an expanding market ensures growth.

Environmental, Social, and Governance (ESG) considerations will shape AGI's trajectory. The company's inherent advantages in circular economy position it well for ESG-focused investors. Carbon neutrality targets, though challenging for energy-intensive glass manufacturing, could differentiate AGI from competitors. Social initiatives around glass recycling could create shared value—environmental benefit and raw material cost reduction.

The Somany family's stewardship continues evolving. Sandip Somany, as Chairman and Managing Director, brings operational focus different from previous generations' entrepreneurial zeal. The next generation's involvement remains unclear, raising succession planning questions. Professional management depth has increased, reducing key person dependency—critical for institutional investor confidence.

Six decades after that British collaboration brought modern sanitaryware to India, AGI Greenpac has transformed beyond recognition. From toilets to bottles, from family enterprise to listed company, from conglomerate to focused player—each transformation reflected changing India and evolving corporate strategy.

The journey ahead won't be linear. Competition will intensify, technology will disrupt, regulations will evolve. But AGI Greenpac has survived and thrived through India's socialist era, liberalization, globalization, and now digitization. The company that began making toilets now packages India's consumption story—a transformation as remarkable as India's own economic journey.

For investors, AGI Greenpac represents a fascinating study in corporate evolution, strategic pivots, and resilience. Whether the next chapter delivers value creation or destruction remains unwritten. But if history guides, the Somany family will continue finding opportunity in challenge, value in distress, and growth in transformation.

The glass is neither half full nor half empty at AGI Greenpac—it's constantly being reshaped, refined, and renewed. And perhaps that's the most important lesson from this remarkable corporate journey: in business, as in glass making, the ability to withstand heat, pressure, and rapid change determines whether you emerge stronger or shatter completely. AGI Greenpac, through six decades of transformation, has consistently emerged stronger.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube