Supermicro (SMCI): The AI Infrastructure Gold Rush Story

I. Introduction & Cold Open

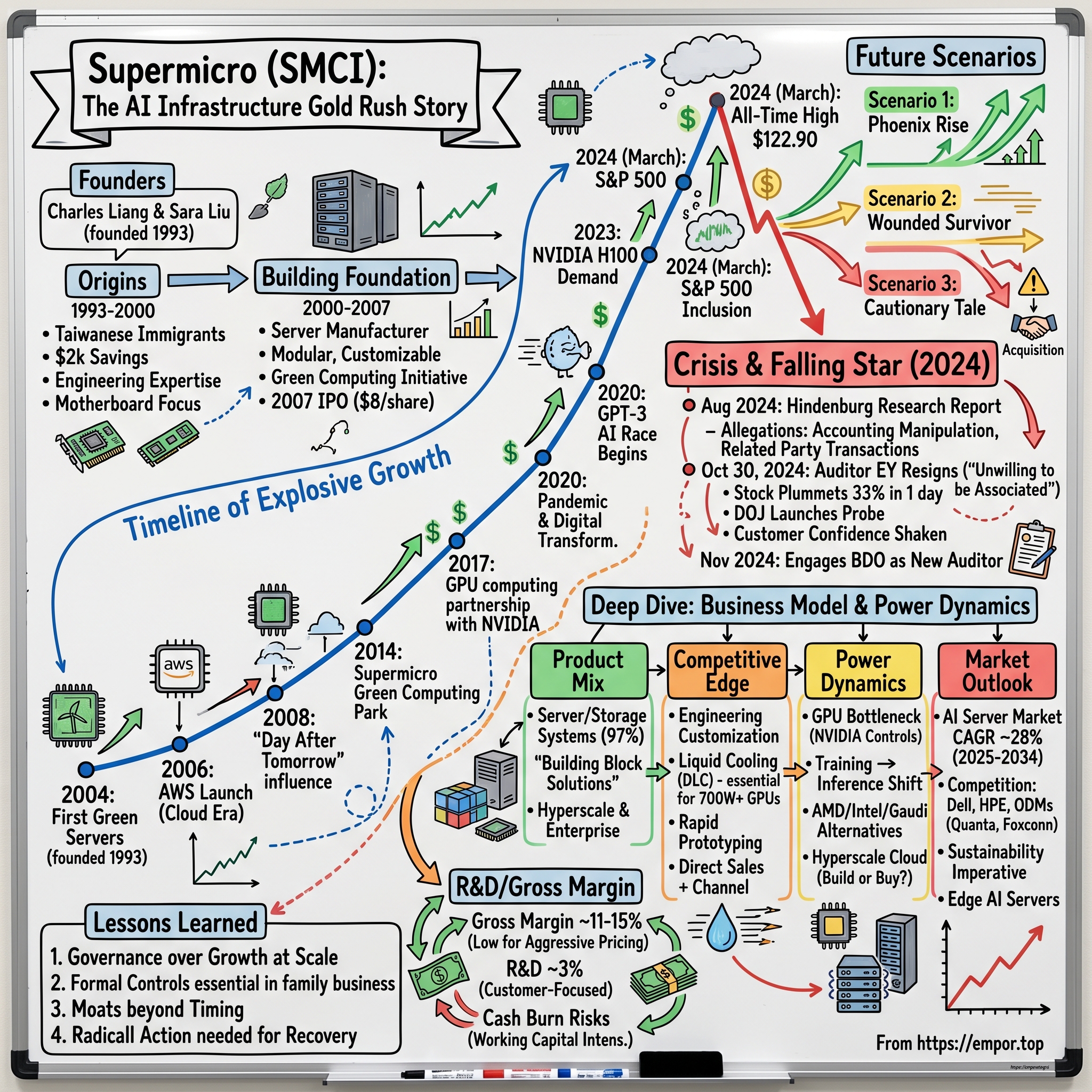

Picture this: A small motherboard company tucked away in a San Jose industrial park, founded by a Taiwanese immigrant couple with $2,000 in savings. Fast forward three decades, and that same company's market value would briefly eclipse Ford Motor Company. In April 2023, Supermicro's stock traded around $100. By February 2024, it shattered $1,000—a breathtaking 10-fold surge in less than a year. Fortune magazine would call it "the best-performing stock in the S&P 500." Then, just as dramatically, it all came crashing down.

This is the story of Super Micro Computer Inc.—SMCI to Wall Street—a company that built the invisible backbone of the AI revolution, only to watch its triumph turn to turmoil when its auditor walked away, declaring itself "unwilling to be associated" with the company's financial statements. It's a tale of engineering brilliance and accounting disasters, of family loyalty and corporate governance failures, of riding the most explosive technology wave in history while navigating the treacherous waters of public markets. The numbers tell only part of the story. SMCI reached its all-time high on March 8, 2024 with the price of $122.90, representing not just financial success but validation of a three-decade bet on server infrastructure. Yet within months, the stock would lose over 80% of its value, making it one of the most spectacular rises and falls in modern tech history.

What makes Supermicro fascinating isn't just the volatility—it's what the company represents in the broader technology ecosystem. While NVIDIA gets the glory for powering AI with its GPUs, and OpenAI captures imaginations with ChatGPT, Supermicro builds the unglamorous but essential infrastructure that makes it all work. They're the arms dealers in the AI gold rush, selling the picks and shovels—or more accurately, the server racks and liquid cooling systems—that every AI company desperately needs.

This is a story about timing, technology transitions, and the thin line between triumph and disaster in public markets. It's about a company that perfectly positioned itself for the AI boom, only to stumble on the basics of financial reporting. Most importantly, it's a case study in what happens when exponential growth meets existential governance challenges—a cautionary tale wrapped inside one of the greatest technology opportunities of our time.

II. Origins: Charles Liang's American Dream (1993-2000)

The year was 1993. Bill Clinton had just become president, the internet was still something you dialed into, and in a modest office in San Jose, California, Charles Liang Chien-Hou, born in 1956 or 1957 in Chiayi, Taiwan, was about to launch what would become a Taiwanese billionaire businessman's empire alongside his wife Sara Liu. They had little more than engineering expertise, immigrant determination, and a conviction that the future of computing would need better motherboards.

Liang's journey to Silicon Valley followed a familiar arc for talented Taiwanese engineers: a bachelor's degree in electrical engineering from the National Taiwan University of Science and Technology, then a master's degree in electrical engineering from the University of Texas at Arlington. But what set him apart was his early fascination with the intersection of computing and real-world applications. As a student, Liang was interested in medical technologies and worked on "developing computerized systems to help diagnose illnesses"—a prescient interest given how AI would later transform healthcare computing.

After graduating, he worked on a chip design for a healthcare company that utilized artificial intelligence, which he called an "AI Processor". Think about that timing: Liang was working on AI chips in the 1980s, three decades before the current AI boom. From July 1991 to August 1993, Liang served as president and chief design engineer of Micro Center Computer, a motherboard design and manufacturing company, where he honed the skills that would define Supermicro's engineering culture.

On November 1, 1993, Liang co-founded Supermicro alongside his wife and company treasurer, Chiu-Chu Liu (known as Sara), beginning as a five-person operation. The founding capital? Industry lore suggests it was around $2,000—pocket change even by 1993 standards. Remarkably, Liang stated that the company was able to turn a profit after six months of operation.

The Silicon Valley of 1993 was experiencing a unique moment. The Cold War had ended, defense spending was down, but the commercial technology sector was exploding. The x86 architecture—Intel's bet on standardized computing—was winning the processor wars. Companies needed servers, and servers needed motherboards. Liang saw an opportunity not in building complete systems like Dell or Compaq, but in becoming the supplier to the suppliers—the picks and shovels strategy that would later prove genius.

By 1996, the company opened a manufacturing subsidiary, Ablecom, in Taiwan, run by Charles's brothers, Steve Liang and Bill Liang. This wasn't just cost arbitrage—it was family business strategy at its finest. Charles and his wife own close to 31 percent of Ablecom, while Steve Liang and other members of the family own close to 50 percent. The Liang family was building a vertically integrated empire, with trusted family members controlling each critical node.

The late 1990s brought the dot-com boom, and Supermicro rode the wave by focusing on what others overlooked: engineering excellence and customization. While competitors chased volume with standardized products, Supermicro would build whatever customers needed. A telecom startup needed a weird form factor? Supermicro would design it. A financial services firm needed ultra-low latency? Supermicro would optimize for it.

When the dot-com crash arrived in 2000, destroying countless Silicon Valley dreams, Supermicro survived through a combination of diversification and engineering culture. They hadn't overextended, hadn't taken venture capital, hadn't hired thousands of employees they couldn't afford. The Liang family's conservative, profit-focused approach—so unfashionable during the go-go years—proved prescient. As competitors collapsed or consolidated, Supermicro quietly picked up their customers, their talent, and their market share.

III. Building the Foundation: From Components to Systems (2000-2007)

The rubble of the dot-com crash created opportunity for those with patience and capital. While Silicon Valley licked its wounds, Charles Liang made a strategic decision that would transform Supermicro: they would stop being just a motherboard supplier and become a complete server manufacturer. It was risky—competing directly with giants like Dell and HP—but Liang saw something others missed. The big vendors were optimizing for volume and standardization. Supermicro would optimize for customization and time-to-market.

The early 2000s saw Supermicro developing what would become their signature approach: modular, customizable server architectures that could be rapidly configured for specific customer needs. While Dell might take six months to design a custom server, Supermicro could do it in six weeks. This speed came from vertical integration—with manufacturing in both San Jose and Taiwan, they controlled their entire supply chain.

A pivotal moment came in 2004 when Supermicro began to develop energy-saving servers, partially influenced by Liang watching the movie "The Day After Tomorrow" with his family. It sounds almost quaint now—a CEO watching a disaster movie and deciding to make servers more efficient—but this was prescient. Data center power consumption was becoming a crisis, and Supermicro's "Green Computing" initiative would become a major differentiator.

The decision to go public wasn't easy for the Liang family. They had built Supermicro as a private company, maintaining control and focusing on long-term engineering excellence rather than quarterly earnings. But growth required capital, and the public markets were recovering. On March 8, 2007, Supermicro raised $64 million in an initial public offering, selling 8 million shares at $8 a share.

The IPO timing was both brilliant and concerning. The markets were frothy again—this was just months before the financial crisis would begin. But Supermicro wasn't a speculative play; they had real revenue, real profits, and real customers. The $64 million would fund expansion just as the world was about to discover cloud computing.

Throughout this period, Supermicro cultivated a unique position with chip manufacturers. They became the "Switzerland" of servers—neutral territory where both Intel and AMD could showcase their latest technologies. When Intel launched a new Xeon processor, Supermicro would have servers ready on day one. When AMD needed to prove their Opteron chips could compete, Supermicro built the demonstration systems. This relationship would prove invaluable when another chip company—NVIDIA—needed server partners decades later.

The family dynamics remained central to operations. Steve and Bill Liang ran the Taiwan operations with the efficiency and cost discipline that Taiwanese manufacturing was famous for. Charles focused on customer relationships and technology vision from San Jose. Sara Liu managed the finances with the conservative approach that had kept them profitable through the dot-com crash. It was a family business, but one operating at the cutting edge of technology.

IV. The Data Center Revolution (2008-2019)

The 2008 financial crisis should have been a disaster for Supermicro. Credit markets froze, IT spending collapsed, and server demand plummeted. Yet something remarkable was happening in parallel: Amazon Web Services, launched quietly in 2006, was gaining traction. Google was building massive data centers. Facebook was scaling beyond anyone's imagination. The cloud computing revolution had begun, and Supermicro was perfectly positioned to capitalize.

In 2004, Supermicro began to develop energy-saving servers, which was partially influenced by Liang watching the movie The Day After Tomorrow with his family. By 2008, this Green Computing initiative became their calling card. Data centers were consuming 2% of global electricity—a crisis in the making. Supermicro's energy-efficient designs could reduce power consumption by 30-40%, translating to millions in savings for hyperscale customers.

The company's approach to the cloud giants was unique. While Dell and HP pushed standardized products with long development cycles, Supermicro offered something different: complete customization with rapid turnaround. A cloud provider needed a specific configuration for their AI workloads? Supermicro would design, prototype, and deliver in weeks, not months. This agility came from their unusual structure—with manufacturing in both San Jose and Taiwan, they could iterate quickly while maintaining cost competitiveness.

But beneath this success story, problems were brewing. The Securities and Exchange Commission found that Super Micro executives, including CFO Howard Hideshima, pushed employees to maximize end-of-quarter revenue, yet failed to devise and maintain sufficient internal accounting controls to accurately record revenue. As a result, Super Micro improperly and prematurely recognized revenue, including by recognizing revenue on goods sent to warehouses but not yet delivered to customers, shipping goods to customers prior to customer authorization, and shipping misassembled goods to customers.

The accounting issues weren't abstract violations—they reflected a culture of growth at any cost. Sales teams were pressured to hit quarterly targets. Manufacturing was pushed to ship products before customers were ready. The Taiwan operations, run by Charles's brothers, operated with an independence that made oversight difficult. Super Micro's CEO, Charles Liang, while not charged with misconduct, was required to reimburse the company $2.1 million in stock profits that he received while the accounting errors were occurring, pursuant to the clawback provision of the Sarbanes-Oxley Act.

In September 2014, Supermicro moved its corporate headquarters to the former Mercury News headquarters in North San Jose, California, along Interstate 880, naming the campus Supermicro Green Computing Park. The symbolism was perfect: a traditional media company's headquarters transformed into a hub for the digital revolution. The campus would eventually expand to include multiple manufacturing facilities, all focused on rapid prototyping and customization.

Throughout this period, Supermicro maintained its Switzerland strategy with chip vendors. They were early adopters of every new Intel Xeon generation, every AMD EPYC processor, and crucially, they began working with a graphics card company that was pivoting to data center compute: NVIDIA. While others saw NVIDIA as a gaming company, Supermicro recognized the potential for GPU computing in AI and machine learning applications.

The numbers tell the story of transformation: from around $720 million in revenue in 2009 to multiple billions by the late 2010s. But the accounting issues culminated in a crisis. Under the terms of the consent settlement, the Company paid a $17.5 million civil penalty to the SEC in 2020. The company had survived, but trust was damaged. Little did anyone know that the biggest opportunity in Supermicro's history was about to emerge.

V. The AI Explosion: Riding the NVIDIA Wave (2020-2023)

The pandemic changed everything. March 2020 brought global lockdowns, but also an unprecedented digital transformation. Zoom went from verb to lifeline. Cloud computing shifted from IT strategy to survival necessity. And quietly, in a San Jose industrial park, Supermicro was about to experience the most explosive growth in its 27-year history.

The catalyst wasn't just digital transformation—it was artificial intelligence. OpenAI's GPT-3, released in June 2020, sparked an AI arms race. Every tech company, from startups to hyperscalers, suddenly needed massive compute infrastructure. And that compute required NVIDIA GPUs, which needed specialized servers, which Supermicro had been perfecting for years.

Supermicro's revenue and earnings rose 37% and 115%, respectively, in fiscal 2023 as AI infrastructure demand exploded. But that was just the warm-up. "Supermicro continues to experience record demand of new AI infrastructures propelling fiscal 2024 revenue up 110% year over year to $14.9 billion and non-GAAP earnings per share up 87% to $22.09," said Charles Liang.

The numbers defy conventional business physics. The stock was up by 246% in 2023 and again bounced back with a 278% rise in 2024. For context, a 10% annual return is considered good in public markets. Supermicro was delivering 20x that.

What drove this insane growth? Three converging factors created a perfect storm. First, NVIDIA's H100 GPU became the most sought-after silicon in history, with months-long waiting lists. Second, Supermicro had spent years developing liquid cooling technology—essential for managing the heat generated by these power-hungry chips. Third, and most importantly, Supermicro could deliver custom AI server configurations faster than anyone else.

The liquid cooling revolution deserves special attention. Traditional air-cooled data centers were hitting physical limits. NVIDIA's latest GPUs consumed 700 watts each—multiply that by thousands of GPUs, and you have a thermal crisis. Supermicro's liquid-cooled AI SuperClusters offer energy-efficient products for reducing data center power consumption by up to 40%. This wasn't just about efficiency; it was about physics. Without liquid cooling, the AI revolution would literally melt down.

Super Micro is now a component of the S&P 500 index, joining in March 2024—a remarkable achievement for a company that had faced delisting just years earlier. The inclusion triggered mandatory buying from index funds, further accelerating the stock's moonshot trajectory.

The company's relationship with NVIDIA evolved from partnership to symbiosis. While NVIDIA designed the chips, Supermicro built the infrastructure that made them usable at scale. Major companies such as Meta and Amazon depend on Supermicro hardware for their AI and data center tasks. Supermicro works closely with these tech leaders and supplies tailored, high-performance servers. Supermicro partners with NVIDIA to deliver robust AI infrastructure for companies like Meta and Amazon.

But the most staggering metric was the forward guidance. Super Micro Computer expects to earn between $26 billion and $30 billion in revenue in its fiscal year 2025. For context, this is about the same revenue that NVIDIA earned in 2022. Think about that: Supermicro was projecting revenues equal to what NVIDIA—the darling of the AI boom—had earned just three years prior.

The transformation was complete. Supermicro had evolved from a motherboard manufacturer to the arms dealer of the AI revolution, providing the critical infrastructure that every AI company desperately needed. The stock price reflected this reality, creating wealth that would have seemed impossible just years earlier. But as 2024 progressed, storm clouds were gathering.

VI. Peak and Crisis: The Accounting Scandal (2024)

October 30, 2024. The date will be remembered as one of the most dramatic in Supermicro's history. That Wednesday morning, investors woke up to news that would send the stock plummeting 33%—its worst single-day decline in six years. Ernst & Young LLP resigned as the auditor to troubled server maker Super Micro Computer Inc., citing concerns about the company's governance and transparency. The shares plummeted the most in six years.

The resignation letter was devastating in its simplicity. "We are resigning due to information that has recently come to our attention which has led us to no longer be able to rely on management's and the Audit Committee's representations," Ernst & Young wrote. More damning still, EY said in its resignation letter it was "unwilling to be associated" with management's financial statements.

For a Big Four accounting firm to resign mid-audit is extraordinary. It's the corporate equivalent of a pilot parachuting out of a plane mid-flight. EY resigned while conducting the audit for the Company's fiscal year ended June 30, 2024, EY's first audit on the Company's behalf. They had replaced Deloitte & Touche in March 2023, brought in presumably to provide a fresh start after the previous accounting issues.

The timeline reveals a company in crisis. In late July 2024, EY communicated to the Audit Committee concerns about several matters relating to governance, transparency and completeness of communications to EY, and other matters pertaining to the Company's internal control over financial reporting, and that the timely filing of the Company's annual report was at significant risk.

But the problems had been building before EY's concerns. In August 2024, Hindenburg Research—the short-selling firm that had previously targeted companies like Nikola—released a scathing report on Supermicro. The report alleged "accounting manipulation" and claimed to have found "glaring accounting red flags, evidence of undisclosed related party transactions, sanctions and export control failures."

The Hindenburg report wasn't just another short-seller hit piece. It detailed specific allegations about channel stuffing—the practice of shipping products to distributors before they're actually sold to end customers, artificially inflating revenues. They claimed Supermicro was recognizing revenue on partial orders and defective products, echoing the same issues that had led to the 2020 SEC settlement.

The resignation comes after news broke last month that the US Department of Justice had launched a probe into an ex-employee's claims that Super Micro violated accounting rules. A DOJ investigation is orders of magnitude more serious than an SEC inquiry. While the SEC can impose civil penalties, the DOJ can bring criminal charges.

The board's response revealed a company scrambling to contain the damage. In response, the Board appointed an independent special committee of the Board (the "Special Committee") to review the matters and certain of the Company's internal controls and certain governance procedures (the "Review"). The Special Committee engaged Cooley LLP, and forensic accounting firm Secretariat Advisors, LLC to perform an investigation on behalf of and at the direction of the Special Committee.

The accountancy also raised concerns about the board's independence from CEO Charles Liang and "other members of management." This struck at the heart of Supermicro's family-controlled structure. The same tight-knit management that had built the company was now being questioned for its independence and oversight.

The market reaction was brutal but predictable. A stock that had touched $122.90 in March 2024 was suddenly trading below $30. Billions in market value evaporated. The S&P 500 inclusion that had been such a triumph now meant index funds were forced sellers, accelerating the decline.

The Company does not currently expect that resolution of any of the matters raised by EY, or under consideration by the Special Committee, as noted below, will result in any restatements of its quarterly reports for the fiscal year 2024 ending June 30, 2024, or for prior fiscal years. But this reassurance rang hollow. Ernst & Young said it agreed only with portions of Super Micro's regulatory filing. The auditor didn't co-sign Super Micro's statements that the company doesn't expect changes to previously issued financial results.

The crisis represented more than just accounting irregularities—it was an existential threat to a company at the heart of the AI infrastructure boom. Customers began questioning whether they could rely on Supermicro for critical infrastructure. Competitors circled, ready to poach clients and talent. The company that had ridden the AI wave to unprecedented heights was now fighting for its credibility, its future, and perhaps its very survival.

VII. Business Model Deep Dive

To understand Supermicro's crisis and potential recovery, one must first grasp the intricate business model that enabled both its meteoric rise and dramatic fall. At its core, Supermicro isn't just a server company—it's an engineering-first, vertically integrated manufacturer operating at the intersection of customization and scale.

The revenue breakdown tells the story. Server and Storage Systems account for approximately 97% of revenue, with subsystems making up the remainder. But this simple categorization masks extraordinary complexity. Supermicro doesn't just assemble servers; they design and manufacture everything from the motherboard up, creating what they call "Building Block Solutions"—modular, interchangeable components that can be rapidly configured into thousands of different SKUs.

The customization capability is Supermicro's superpower. While Dell or HP might offer dozens of server configurations, Supermicro offers thousands. Need a server with 24 NVMe drives, four GPUs, and redundant 10GbE networking? They'll build it and ship it in two weeks. This isn't just assembly—it's rapid engineering at scale.

Manufacturing strategy reveals another layer of sophistication. The company operates facilities in San Jose (California), Taiwan, and Malaysia, but this isn't simple labor arbitrage. San Jose handles rapid prototyping and high-value, low-volume products for U.S. customers requiring domestic manufacturing. Taiwan, run by Charles Liang's brothers through Ablecom, manages high-volume production with Asian supply chain proximity. Malaysia provides additional capacity and geographic diversification.

The direct liquid cooling (DLC) technology deserves special attention. Traditional air cooling becomes inefficient above 400 watts per chip. Modern AI accelerators consume 700+ watts. Supermicro's liquid cooling can handle 1,500+ watts per chip while reducing overall data center power consumption by 40%. This isn't incremental improvement—it's physics-based differentiation that competitors struggle to match.

Go-to-market strategy combines direct sales to hyperscalers with a vast channel partner network. The direct relationships with companies like Meta and Amazon provide volume and technical feedback. The channel—thousands of VARs and system integrators—provides reach into enterprise and mid-market segments. This dual approach creates resilience: when hyperscaler spending slows, enterprise picks up, and vice versa.

Gross margin dynamics reveal both opportunity and challenge. Supermicro typically operates at 11-15% gross margins, significantly below Dell's 23% or HP's 35%. This isn't incompetence—it's strategy. Lower margins enable aggressive pricing that wins deals, particularly in the price-sensitive hyperscaler segment. The bet is that volume and operational efficiency will drive acceptable returns on capital.

The working capital intensity is brutal. Supermicro must purchase components—CPUs, GPUs, memory, drives—weeks or months before shipping finished systems. With quarterly revenues exceeding $5 billion, this means billions in inventory and receivables. Any hiccup in collections or demand can create cash crunches, explaining why the company burned $635 million in cash in a recent quarter despite strong revenues.

Research and development spending, while modest as a percentage of revenue (around 3%), is laser-focused on customer needs. Rather than pursuing moonshot technologies, Supermicro's engineers work directly with customers to solve specific problems. This customer-intimate innovation model creates deep relationships but limits breakthrough innovation potential.

The supply chain relationships are critical and complex. Supermicro sources from hundreds of suppliers but depends heavily on a few critical ones. Intel and AMD for CPUs, NVIDIA for GPUs, Samsung and SK Hynix for memory. One supplier can account for over 25% of purchases. This concentration creates both bargaining power challenges and allocation advantages—suppliers prioritize partners who can move volume.

Quality control operates differently than traditional manufacturers. Rather than extensive incoming inspection, Supermicro relies on supplier quality and rapid testing of integrated systems. This lean approach reduces costs but requires exceptional supplier relationships and can create quality issues if not carefully managed.

The November 2024 announcement that the Audit Committee of its Board of Directors has engaged BDO USA, P.C. ("BDO") as its independent auditor, effective immediately provided crucial breathing room. BDO is a member firm of BDO International, one of the world's top five accounting firms network with over 115,000 professionals across its global network and a recognized leader in audit and assurance. While BDO is respected, they're not Ernst & Young—signaling both Supermicro's reduced options and BDO's willingness to take on complex, high-risk engagements.

The business model's greatest strength—rapid customization and engineering agility—becomes weakness without proper controls. The same flexibility that enables two-week turnaround on custom designs can enable premature revenue recognition. The same family relationships that ensure trust and speed can compromise independence and oversight. The same aggressive growth culture that wins deals can pressure employees to cut corners.

Understanding this business model is essential for evaluating Supermicro's future. The operational capabilities are real and differentiated. The market opportunity in AI infrastructure is massive and growing. But the financial and governance challenges threaten to destroy value faster than operations can create it. The question isn't whether Supermicro has a good business—it's whether that business can survive its own success.

VIII. The AI Infrastructure Market Landscape

The AI infrastructure market isn't just growing—it's exploding at rates rarely seen in mature technology sectors. The AI server market was valued at USD 128 billion in 2024 and is expected to grow at a CAGR of 28.2% between 2025 and 2034, with some analysts projecting even more aggressive growth. The global AI server market was valued at US$12.34 billion in 2023, and is expected to be worth US$50.65 billion in 2029. The AI server market is expected to grow at a CAGR of 26.54% over the years 2024-2029.

Understanding this market requires grasping its unprecedented velocity. Traditional server markets grew at 5-10% annually. The AI server market is growing at 3-5x that rate, creating both massive opportunity and brutal competition. Every percentage point of market share represents billions in revenue—explaining why companies fight so fiercely for position.

The competitive landscape resembles a three-tier pyramid. At the apex sit the hyperscale cloud providers—Amazon, Microsoft, Google, Meta—who both consume and compete in AI infrastructure. They buy from vendors like Supermicro while simultaneously designing their own custom silicon and systems. This dual role creates complex dynamics where today's customer becomes tomorrow's competitor.

The second tier contains traditional server vendors pivoting to AI. Dell Technologies and Hewlett Packard Enterprise bring massive sales forces, enterprise relationships, and financial resources. They lack Supermicro's engineering agility but compensate with brand trust and support infrastructure. HPE's November 2024 announcement of new AI supercomputers configured for machine learning training signals their aggressive push into Supermicro's territory.

The third tier—and perhaps most threatening to Supermicro—consists of Original Design Manufacturers (ODMs) like Quanta, Wistron, and Foxconn. These Taiwanese giants have historically operated in the shadows, building servers for others to brand and sell. But AI's margin opportunity has drawn them into direct competition. They offer hyperscalers even lower costs than Supermicro, though with less customization and support.

NVIDIA's role transcends typical supplier relationships. They effectively control the AI infrastructure market through GPU allocation. The GPU segment held a 39% market share in 2024. The air-cooled segment dominated the market with a 68.4% share in 2024 and is set to expand at a CAGR of over 27% between 2025 and 2034. When NVIDIA GPUs are scarce, server vendors with strong NVIDIA relationships—like Supermicro—gain enormous advantage. But this dependency creates vulnerability. NVIDIA could integrate forward into complete systems, or shift allocations to favor other partners.

Market share dynamics reveal fascinating patterns. Bank of America estimates Supermicro's market share could increase from 10% in 2023 to 17% by 2026, while KeyBanc projects 23% of the AI server market this year. But these projections preceded the accounting crisis. Customer confidence, once shattered, takes years to rebuild. Reports suggest some hyperscale customers have already begun shifting orders to competitors.

The technology transition from Hopper to Blackwell GPUs represents both opportunity and risk. Blackwell promises 5x the performance of Hopper, potentially obsoleting billions in existing infrastructure. Server vendors must manage this transition carefully—selling current-generation systems while preparing for next-generation disruption. Supermicro claims to have secured 25% of NVIDIA's GB200 supply (~10,000 server racks), but supply chain dynamics remain fluid.

Geographic patterns matter enormously. North America dominates the global AI server market due to its advanced technology landscape, significant investments, and the presence of leading tech companies. The US, particularly Silicon Valley, plays a crucial role in influencing AI server development and adoption. But growth is shifting. The demand for the AI server market in the Asia Pacific is expected to be the fastest-growing region with a CAGR of 40.6% from 2025 to 2030. This geographic shift favors Asian manufacturers with local presence and relationships.

The shift from training to inference represents another crucial dynamic. It is expected that the market size of inference servers would surpass that of training servers for the first time in 2026 and the gap between these two kinds of servers will continue to widen. Training servers require maximum performance regardless of cost. Inference servers need efficiency and cost-effectiveness at scale. This shift favors vendors who can optimize for total cost of ownership, not just peak performance.

Liquid cooling has emerged as a critical differentiator. Air cooling's physical limits create an opportunity for vendors with advanced thermal management. Supermicro's early investment in liquid cooling provides genuine differentiation, but competitors are rapidly closing the gap. The question is whether Supermicro can maintain its lead while navigating its corporate crisis.

Edge computing adds another dimension. Growing need for edge computing is driving market growth, with a trend towards using ai for server workload optimization. Edge AI servers require different optimizations than data center systems—ruggedization, power efficiency, remote management. This creates opportunities for specialized vendors but also fragments the market.

The sustainability imperative cannot be ignored. Data centers consume 1-2% of global electricity, projected to reach 3-4% by 2030. Customers increasingly demand not just performance but efficiency. Supermicro's "Green Computing" positioning resonates, but substance must match marketing. Real efficiency gains require fundamental architecture innovations, not incremental improvements.

Competition in AI infrastructure isn't just about products—it's about ecosystems. Successful vendors must navigate relationships with chip suppliers, cloud providers, software vendors, and end customers. They must balance standardization with customization, scale with agility, innovation with reliability. The market rewards those who can manage this complexity while maintaining trust.

For Supermicro, the competitive landscape presents both existential threat and unprecedented opportunity. The market's explosive growth could enable recovery from current troubles—if they can restore trust. But competition is intensifying just as Supermicro is most vulnerable. The next 12-18 months will determine whether Supermicro emerges stronger or becomes a cautionary tale of operational excellence undermined by governance failure.

IX. Corporate Governance & Family Dynamics

The Liang family's control of Supermicro represents both its greatest strength and most critical vulnerability. Understanding this duality requires examining not just ownership percentages but the cultural and operational dynamics that shape decision-making at the highest levels.

Charles Liang and his wife Sara Liu maintain approximately 15-20% direct ownership, but their control extends far beyond shareholding. Brothers Steve and Bill Liang run the crucial Taiwan operations through Ablecom, creating a web of family relationships that span the Pacific. This structure enabled rapid decision-making and trust-based operations for decades—until auditors began questioning whether trust had replaced controls.

The board composition tells a revealing story. As of May 2025, Supermicro's board of directors consists of co-founder Charles Liang, co-founder Sara Liu, Wally Liaw (another founding member of the company), Daniel W. Fairfax, Tally Liu, Sherman Tuan, Judy Lin, Robert Blair, Susie Giordano, and Scott Angel. The presence of both founders plus early employee Wally Liaw means management effectively controls three board seats. Family members and long-time associates occupy positions throughout the organization, creating what governance experts call "entrenchment risk."

Ernst & Young's resignation letter specifically cited concerns about board independence from CEO Charles Liang and "other members of management." This isn't abstract governance theory—it's about whether directors can provide genuine oversight when their economic interests and personal relationships align with management. Can Sara Liu objectively evaluate her husband's performance? Can board members who've worked with Charles for decades challenge his decisions?

The Taiwan connection adds complexity. Ablecom, the manufacturing subsidiary run by Charles's brothers, operates with significant autonomy. Charles and his wife own close to 31 percent of Ablecom, while Steve Liang and other members of the family own close to 50 percent. This structure creates potential for related-party transactions that may not be at arm's length. When Supermicro buys from Ablecom, is it getting market pricing? When capacity is constrained, who gets priority? These questions become critical when billions flow between entities.

Cultural factors cannot be ignored. Taiwanese business culture often emphasizes family loyalty, long-term relationships, and informal communication—values that built Supermicro but clash with U.S. public market expectations. What seems like normal business practice in Taiwan—hiring relatives, informal agreements, relationship-based deals—appears as nepotism and weak controls to U.S. regulators and investors.

The accounting issues reflect these cultural tensions. The SEC's findings about premature revenue recognition often stemmed from aggressive interpretation of rules rather than outright fraud. Sales teams pushed to meet quarterly targets—a very American practice—but without the formal controls American companies typically implement. The result was a hybrid worst-of-both-worlds: aggressive growth culture without corresponding governance infrastructure.

Giordano joined the board in August 2024 and served as the only member of Supermicro's special committee to oversee an internal audit of concerns raised by EY. The appointment of a single-person special committee raised eyebrows among governance experts. Typically, special committees have multiple independent members to ensure thorough investigation. The structure suggests either board dysfunction or lack of truly independent directors.

Comparison to other family-controlled tech companies reveals patterns. Successful examples like NVIDIA (controlled by founder Jensen Huang) or Meta (controlled by Mark Zuckerberg) maintain family/founder control while implementing robust governance structures. They have genuinely independent directors, professional CFOs from outside the company, and clear separation between family and business interests. Supermicro attempted to follow this model but implementation fell short.

The failed examples are equally instructive. Theranos, though not family-controlled, showed how founder dominance could override governance. WeWork demonstrated how charismatic leadership without proper oversight destroys value. Luckin Coffee—another company with accounting issues—illustrated how cultural differences in business practices can collide with U.S. market requirements.

Institutional investors face a dilemma. The Liang family's technical expertise and customer relationships built Supermicro's success. Their rapid decision-making and engineering focus created competitive advantages. But the same concentration of power that enabled agility also enabled accounting issues. Can you have one without the other?

The governance reforms required for recovery are clear but painful. Supermicro needs genuinely independent directors—not family friends or long-time associates. They need a CFO from outside the organization with credibility to stand up to the CEO. They need formal controls on related-party transactions and clear separation between U.S. and Taiwan operations. Most difficult, they need Charles Liang to cede some control—something founder-CEOs rarely do voluntarily.

The cultural transformation may be even harder than structural changes. Supermicro must shift from relationship-based to process-based decision-making, from informal to formal communication, from trust to verification. This isn't just about satisfying regulators—it's about building an organization that can handle $30+ billion in revenue without breaking.

The irony is striking: the family dynamics that enabled Supermicro to build the AI infrastructure for companies creating the future may prevent it from participating in that future. The same tight control that enabled rapid innovation may cause institutional investors to flee. The trust-based culture that customers valued may be precisely what auditors cannot accept.

Reform is possible—other companies have successfully transitioned from family to professional management. But it requires acknowledgment that what worked at $1 billion in revenue breaks at $15 billion. It requires accepting that public markets demand transparency and independence that family businesses resist. Most fundamentally, it requires the Liang family to choose: maintain control of a smaller, possibly private company, or cede control to participate in the AI infrastructure boom.

The special committee's investigation and BDO's audit will reveal whether Supermicro can thread this needle—maintaining family involvement while implementing professional governance. The outcome will determine not just Supermicro's fate but provide lessons for other family-controlled tech companies navigating hypergrowth. Can you preserve entrepreneurial culture while accepting institutional constraints? Supermicro's answer will resonate far beyond San Jose.

X. Investment Analysis & Valuation

The investment case for Supermicro presents one of the most complex risk-reward equations in public markets today. A company trading at forward P/E near 22x with projected FY2025 revenue of $22 billion (47% YoY increase) would typically screen as attractive. But traditional metrics fail to capture the binary nature of Supermicro's situation.

Start with the bull case, which remains compelling despite recent turmoil. The AI infrastructure market's explosive growth—28% CAGR through 2029—provides massive tailwind. Supermicro's claimed 25% share of NVIDIA's GB200 supply represents approximately 10,000 server racks, potentially $5-10 billion in high-margin revenue. If management can execute and governance issues resolve, the stock could easily double or triple from current depressed levels.

The operational metrics support optimism. Despite the chaos, the company continues shipping products and winning customers. The liquid cooling technology provides genuine differentiation in a market where thermal management increasingly determines data center viability. The Building Block Solutions approach enables customization that pure contract manufacturers cannot match. These are real competitive advantages, not financial engineering.

But the bear case is equally powerful. Ernst & Young's resignation—stating they were "unwilling to be associated" with management's financials—represents a corporate death sentence unless reversed. The DOJ investigation could result in criminal charges, executive bans, or massive fines. Customer defections to Dell and HPE may be irreversible. The company could face delisting, bankruptcy, or forced sale at distressed prices.

The financial analysis reveals troubling patterns. Gross margins compressed from 17% to 11% over recent quarters—partly due to competition but possibly masking deeper issues. The company burned $635 million in cash despite strong revenues, suggesting working capital problems or collection issues. Days sales outstanding have stretched, indicating customers may be delaying payments due to uncertainty.

Consider the range of outcomes. In the optimistic scenario, BDO completes its audit finding no material misstatements, the DOJ investigation closes without charges, and customers return. The stock could reach $100-150, representing 150-275% upside. In the pessimistic scenario, BDO finds material issues requiring restatement, the DOJ brings charges, and major customers defect permanently. The stock could fall below $10, representing 75% downside.

The probability distribution is highly skewed. There's perhaps a 30% chance of the optimistic scenario, 40% chance of a muddle-through middle case (stock ranges $30-60), and 30% chance of disaster. This isn't a normal bell curve—it's a barbell with little middle ground. Either governance issues resolve and the company thrives, or they don't and it collapses.

Cash flow analysis adds complexity. The company's cash conversion cycle has deteriorated—they're paying suppliers faster while collecting from customers slower. This could reflect negotiating weakness as suppliers demand better terms while customers delay payment. Or it could indicate channel stuffing, with inventory building at distributors who haven't actually sold products to end users.

The capital structure provides some cushion but not much. The company has approximately $2 billion in cash and equivalents, but also significant working capital needs. The recent $2.3 billion convertible note offering in November 2024 provided breathing room but added dilution risk. If the stock recovers, conversion will dilute existing shareholders. If it doesn't, debt service will pressure cash flow.

Valuation requires scenario analysis rather than point estimates. At 22x forward P/E, the stock appears cheap relative to AI beneficiaries like NVIDIA (44x) or cloud providers (30-40x). But Supermicro deserves a discount for governance issues, customer concentration, and margin pressure. The question is whether current prices reflect appropriate discount or overcorrection.

Competitive dynamics affect valuation. Every day Supermicro remains in crisis, competitors gain ground. Dell and HPE are aggressively courting Supermicro customers with stability pitches. ODMs are offering lower prices to hyperscalers. NVIDIA may diversify its partner ecosystem to reduce Supermicro dependence. Time is not neutral—delay means permanent market share loss.

The institutional ownership changes tell a story. Many growth funds have exited, replaced by value investors and special situation funds. This changing shareholder base reflects the shift from growth story to turnaround situation. The investors now buying have different expectations and time horizons than those who rode the AI wave up.

Technical analysis suggests a potential bottom around $25-30, with resistance at $50-60. But technical levels matter less than fundamental catalysts. The stock will move on audit results, DOJ developments, and customer announcements, not chart patterns. This is an event-driven situation where news flow dominates price action.

Risk management becomes paramount. This isn't a position for retirement accounts or risk-averse investors. It's suitable only for those who can afford total loss and understand the binary nature of outcomes. Position sizing should reflect the possibility of zero, not the dream of tripling.

For existing shareholders, the decision is agonizing. Selling locks in massive losses but preserves remaining capital. Holding risks further decline but maintains upside optionality. Averaging down could be brilliant or foolish depending on unknowable audit results. There's no clear answer—only risk tolerance and conviction matter.

The investment decision ultimately depends on answering three questions: Can management restore trust with stakeholders? Will the business model's strengths overcome governance weaknesses? Is the risk-reward favorable at current prices? Reasonable people can disagree on all three, explaining the massive volatility and divergent analyst opinions.

The parallel to historical situations provides context but not answers. Companies have recovered from accounting scandals (Waste Management, Computer Associates) but others haven't (Enron, WorldCom). The difference often comes down to whether the underlying business was real. Supermicro's products are real, customers are real, and market opportunity is real. But that may not be enough if trust cannot be restored.

XI. Playbook: Lessons for Founders & Investors

The Supermicro saga offers a masterclass in how spectacular success can transform into existential crisis when growth outpaces governance. The lessons extend far beyond one company's struggles, providing a playbook for founders navigating hypergrowth and investors evaluating high-flying stocks.

Lesson 1: Corporate governance isn't optional at scale. Supermicro could operate informally when revenue was $1 billion. At $15 billion, informal became illegal. The transition from startup to public company requires fundamental changes in how decisions are made, documented, and overseen. Founders who resist this transition risk destroying everything they've built.

The practical implications are clear: hire a CFO from outside the company before going public. Recruit genuinely independent directors, not friends or family associates. Implement formal controls even if they slow decision-making. Document everything. What seems like bureaucracy is actually infrastructure for scale.

Lesson 2: Family businesses face unique challenges in public markets. The same trust and loyalty that enable family businesses to thrive can become liability under public scrutiny. Related-party transactions that seem normal in private companies appear corrupt in public ones. The solution isn't eliminating family involvement but creating clear boundaries and oversight mechanisms.

Best practice suggests separating family members across reporting lines, implementing mandatory recusal from related-party decisions, and hiring professional managers for key roles. The family can maintain control through shareholding while ceding operational control to professionals. This balance is delicate but essential.

Lesson 3: Riding technology waves requires different skills than building sustainable moats. Supermicro perfectly timed the AI wave, but timing isn't a sustainable competitive advantage. When everyone sees the same opportunity, competition intensifies and margins compress. The companies that survive waves build differentiation beyond being early.

The implication for founders: identify what remains valuable after the gold rush ends. For Supermicro, it might be liquid cooling expertise or customer relationships. For other companies, it could be data, network effects, or switching costs. The time to build moats is during the boom, not after.

Lesson 4: Financial engineering cannot substitute for operational excellence. The temptation during hypergrowth is to juice numbers through aggressive accounting. Pull forward revenue, delay expenses, optimize for headlines. This works until it doesn't. When music stops, companies with real operations survive while financial engineers collapse.

The warning signs are identifiable: deteriorating cash conversion, growing gap between earnings and cash flow, increasing days sales outstanding, channel stuffing accusations. Investors who see these flags should exit regardless of growth rates. Founders who create these conditions are mortgaging their future for temporary stock gains.

Lesson 5: When to take chips off the table matters enormously. Charles Liang's net worth peaked above $10 billion and has since collapsed. Early employees who exercised options at the peak lost fortunes. The psychological difficulty of selling during success is real, but diversification isn't betrayal—it's prudence.

The framework for decision-making: sell enough to be financially secure regardless of outcome. For founders, this might mean selling 10-20% at liquidity events. For employees, it means exercising and selling regularly rather than waiting for the perfect moment. The goal isn't maximization but resilience.

Lesson 6: Recovery from scandal requires radical action, not incremental change. Companies that successfully recover from accounting scandals typically replace entire management teams, implement completely new control systems, and accept years of elevated scrutiny. Half-measures fail. Supermicro's challenge is that the same people who created the problem are trying to fix it.

The recovery playbook is proven: bring in crisis management experts, cooperate fully with investigators, over-communicate with stakeholders, and accept short-term pain for long-term credibility. Most importantly, demonstrate through actions—not words—that culture has changed.

Lesson 7: The danger of customer concentration in commodity businesses. When a few customers drive majority of revenue and switching costs are low, company power is illusory. Supermicro's dependence on hyperscalers for volume and NVIDIA for components created double vulnerability. When confidence wavered, customers could easily shift orders to competitors.

The strategic imperative: diversify before you need to. Build switching costs through software, services, or integration. Create direct relationships that transcend procurement departments. Most importantly, recognize that customer concentration is debt that must eventually be repaid.

Lesson 8: Culture eats strategy for breakfast, but compliance eats everything. Supermicro had brilliant strategy—first to liquid cooling, close to NVIDIA, customization at scale. But strategy means nothing if you can't file financial statements. In regulated public markets, compliance isn't a cost center—it's existential.

This requires cultural change from engineering-first to process-first mindset. It means celebrating the person who catches errors, not just the person who closes deals. It means accepting that some opportunities must be declined if they can't be properly documented. This cultural shift is painful but necessary.

Lesson 9: The institutional imperative will assert itself. As companies grow, they inevitably become more like their peers. The same institutional investors, board members, and executives circulate among companies, bringing similar practices and expectations. Fighting this tendency requires enormous energy and usually fails.

The implication: plan for institutionalization rather than resisting it. Build unique advantages that survive standardization. Accept that the company at $30 billion revenue will be fundamentally different from the company at $3 billion. The goal is managed evolution, not prevented change.

Lesson 10: Timing matters more than most admit. Supermicro's success came from being perfectly positioned for the AI boom. Their crisis came from governance failures exposed during scrutiny that success brought. Had AI emerged five years later, they might have fixed governance first. Had it emerged five years earlier, they might have been too small to capture opportunity.

This isn't an argument for luck but for preparation. The companies that successfully ride waves are those prepared when waves arrive. This means maintaining flexibility, building capabilities before they're needed, and accepting that timing—while crucial—cannot be perfectly controlled.

For current founders, the message is clear: build governance infrastructure before you need it. For investors, the lesson is equally clear: growth without governance is a ticking time bomb. For Supermicro itself, the path forward requires acknowledging that what got them here won't get them there—fundamental change is required for survival.

XII. Power & Future Outlook

Where does power truly lie in the AI infrastructure stack? This question determines not just Supermicro's fate but the entire industry's evolution. The answer reveals why Supermicro's position is both stronger and weaker than it appears.

Power in technology markets flows to whoever controls the scarce resource. In AI infrastructure, that resource isn't servers—it's GPUs. NVIDIA controls GPU supply, making them the true power broker. Server vendors like Supermicro are essentially systems integrators, adding value through engineering and customization but ultimately dependent on NVIDIA's allocation decisions. This dependency explains both Supermicro's spectacular rise (favored partner status) and vulnerability (what NVIDIA gives, NVIDIA can take away).

But power dynamics are shifting. As AI moves from training to inference, as edge computing proliferates, as alternative architectures emerge, the GPU bottleneck loosens. AMD's MI300 series, Intel's Gaudi, Google's TPUs, and startup accelerators provide options. Supermicro's value proposition—integrating diverse components into optimized systems—becomes more valuable as complexity increases.

The question of commodity versus differentiation cuts to Supermicro's existential challenge. Bears argue servers are commoditizing—standardized components assembled by whoever offers lowest price. Bulls counter that AI infrastructure requires sophisticated thermal management, power delivery, and system optimization that few can provide. Reality lies between: some aspects commoditize while others differentiate.

Liquid cooling represents genuine differentiation today but may not tomorrow. Every major vendor is developing liquid cooling capabilities. The question is whether Supermicro can maintain its lead through continuous innovation or whether competitors will close the gap. History suggests technology advantages erode without persistent investment—something difficult during corporate crisis.

The next computing paradigm offers both hope and threat. Quantum computing, neuromorphic chips, optical interconnects—each could obsolete current infrastructure. But transitions take decades, not years. Supermicro has time to evolve if it survives current challenges. The company's engineering culture and customization capabilities could prove valuable regardless of underlying technology.

Three scenarios define Supermicro's potential futures:

Scenario 1: The Phoenix Rise (30% probability) BDO's audit finds no material misstatements. The DOJ investigation closes without charges. Customer confidence returns. Supermicro implements world-class governance while maintaining engineering excellence. The company captures 20%+ of the AI server market, reaching $40+ billion in revenue by 2027. Stock price exceeds previous highs.

This requires threading an extremely narrow needle: reforming governance without destroying culture, maintaining NVIDIA relationship while diversifying, growing rapidly while improving margins. Possible but difficult.

Scenario 2: The Wounded Survivor (45% probability) Accounting issues prove manageable but require restatements. Some customers return but others permanently lost. Growth continues but at reduced rate. Supermicro becomes solid but unspectacular player in AI infrastructure—profitable but not dominant. Stock stabilizes at $40-70, below previous highs but above crisis lows.

This middle path might be most likely. Companies rarely fully recover from accounting scandals but can build respectable businesses. Supermicro would join the ranks of reformed but forever-tainted companies that trade at permanent discount to peers.

Scenario 3: The Cautionary Tale (25% probability) Material accounting fraud discovered. Criminal charges filed. Major customers permanently defect. NVIDIA shifts allocation to other partners. Supermicro either enters bankruptcy, gets acquired at distressed price, or shrinks to niche player. Stock falls below $10, potentially to zero.

This disaster scenario remains real possibility. The combination of DOJ investigation, auditor resignation, and customer defection creates downward spiral that could prove irreversible. Many accounting scandals end this way.

What needs to happen for recovery? Five critical milestones:

First, complete BDO audit without material restatements. This validates that underlying business is real and accounting issues were control failures, not fraud. Timeline: 3-6 months.

Second, resolve DOJ investigation without criminal charges. Civil settlements are survivable; criminal charges are not. Timeline: 6-12 months.

Third, retain major customers through the crisis. Every hyperscaler that maintains orders provides vote of confidence. Customer defection rate determines recovery possibility. Timeline: ongoing.

Fourth, implement governance reforms that satisfy regulators and investors. New independent directors, outside CFO, enhanced controls. Must be substantial, not cosmetic. Timeline: 3-9 months.

Fifth, maintain technological competitiveness during crisis. Continue product development, particularly for Blackwell generation. Technology markets are unforgiving to those who fall behind. Timeline: continuous.

The broader implications extend beyond Supermicro. The AI infrastructure boom created many instant winners—companies whose valuations exploded based on proximity to AI rather than fundamental strength. Supermicro's crisis reminds markets that execution matters, governance matters, sustainability matters. The shakeout has begun.

For the industry, Supermicro's struggles create opportunity and warning. Competitors gain market share but see consequences of growth without governance. Customers diversify suppliers but lose customization capabilities. Investors learn to scrutinize operations, not just narratives.

The final verdict depends on unknowable factors. Will prosecutors show leniency? Will customers show loyalty? Will the Liang family accept necessary changes? Will AI infrastructure demand continue growing? These questions lack definitive answers, explaining why Supermicro remains among the most controversial stocks in markets.

What's certain is that Supermicro stands at an inflection point. The next twelve months will determine whether it emerges as strengthened survivor or cautionary tale. The company that pioneered AI infrastructure may not survive to see AI's full flowering. Or it may emerge from crisis with hard-won wisdom that enables next phase of growth.

The story continues to unfold, lesson by lesson, revelation by revelation. Whatever the outcome, Supermicro's journey from immigrant startup to AI giant to governance crisis provides enduring lessons about ambition, innovation, and the price of success in modern technology markets. The final chapter remains unwritten, but the implications already resonate across Silicon Valley and beyond.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube