IndusInd Bank: From NRI Dreams to India's Banking Powerhouse

I. Introduction & Episode Roadmap

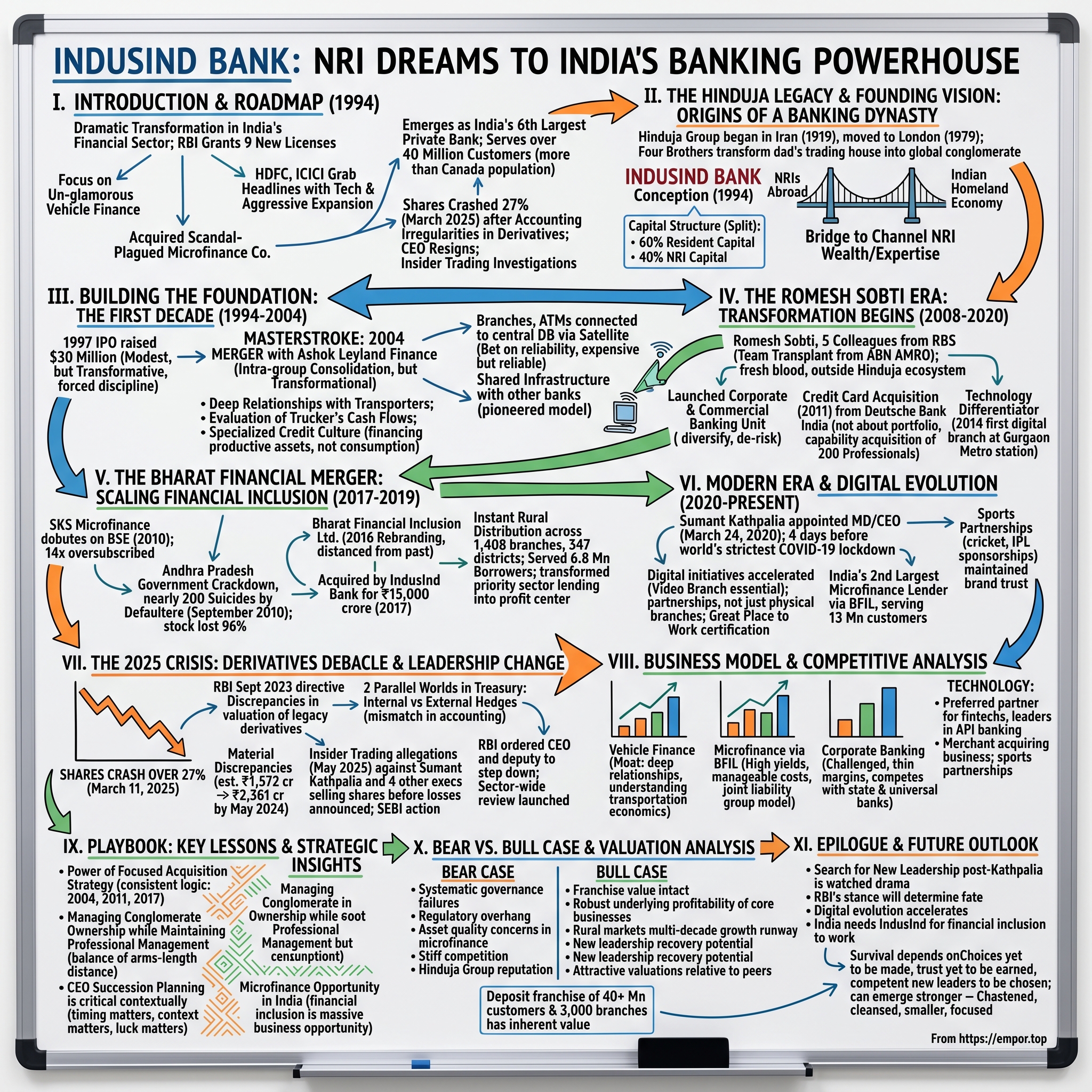

The year is 1994. India's financial sector is experiencing its most dramatic transformation since independence. The Reserve Bank of India has just granted nine new banking licenses—the first in over two decades. Among the recipients is a bank with an unusual name and an even more unusual mission: IndusInd Bank, conceived by one of India's most prominent business dynasties living abroad, aiming to channel the wealth and expertise of Non-Resident Indians back into their homeland.

The name itself tells a story. "IndusInd"—inspired by the Indus Valley Civilization, one of history's earliest examples of sophisticated commerce and urban planning. The founders saw themselves as inheritors of this 5,000-year-old tradition of Indian enterprise, now ready to build a modern financial institution that could bridge the old India with the new.

But here's what makes this story remarkable: While HDFC Bank and ICICI Bank grabbed headlines with their aggressive expansion and tech-forward strategies, IndusInd Bank took a different path. It built its empire on the unglamorous foundation of vehicle finance, acquired a scandal-plagued microfinance company at the height of regulatory scrutiny, and somehow emerged as India's sixth-largest private bank by market capitalization. Today, it serves over 40 million customers—more than the population of Canada—with a unique model that combines haute finance in Mumbai's business districts with microloans in Bihar's villages.

The journey hasn't been smooth. In March 2025, the bank's shares crashed 27% in a single day after revealing accounting irregularities in its derivatives portfolio. The CEO resigned. Executives were investigated for insider trading. The very survival of the institution seemed in question. Yet the bank continues to operate, its 3,000+ branches opening every morning, its ATMs dispensing cash, its loan officers visiting villages.

This is a story about ambition and hubris, about the promise and peril of financial innovation, about what happens when a family-controlled conglomerate tries to build a professional banking institution in the world's most populous democracy. It's about three transformative CEOs, each bringing their own vision and leaving their own scars. It's about the collision between global banking sophistication and Indian ground realities.

Most fundamentally, it's about a question that every emerging market faces: Can you build world-class financial institutions while serving the unbanked masses? Can you maintain pristine corporate governance while navigating family ownership? Can you grow fast without growing reckless?

Over the next several hours, we'll explore how IndusInd Bank attempted to answer these questions, where it succeeded brilliantly, and where it failed spectacularly. We'll meet the characters who built this institution, understand the deals that shaped it, and examine the crisis that nearly destroyed it.

Let's begin where all great Indian business stories begin: with a family, a vision, and perfect timing.

The Hinduja Legacy & Founding Vision: Origins of a Banking Dynasty

Picture this: Mumbai in 1914. A young Sindhi entrepreneur named Parmanand Deepchand Hinduja arrives from Shikarpur (in what is now Pakistan), carrying little more than ambition and an eye for opportunity. In the trade and financial capital of Bombay, he quickly learns the ropes of business. Within five years, he would establish the company's first international operation in Iran in 1919, beginning a century-long saga of global expansion that would eventually birth one of India's most distinctive banks.

The Hindujas built their fortune on a simple principle that Parmanand often expressed: "My dharma (duty) is to work, so that I can give". This wasn't mere rhetoric. Merchant Banking and Trade were the twin pillars of the Group's business, and for sixty years—from 1919 to 1979—the headquarters of the group remained in Iran. The Islamic Revolution forced them to relocate to London, but by then, the four Hinduja brothers—Srichand, Gopichand, Prakash, and Ashok—had transformed their father's trading house into a global conglomerate.

Fast forward to 1991. India is undergoing its most dramatic economic transformation since independence. Finance Minister Manmohan Singh is dismantling the License Raj, opening sectors that had been closed for decades. The Reserve Bank of India, for the first time in over twenty years, is preparing to issue new banking licenses to private players. The timing couldn't be more perfect for the Hindujas.

IndusInd Bank was among nine 'new-generation' banks that obtained a banking license in 1994; it was started by S. P. Hinduja along with hundreds of NRI and other shareholders. But this wasn't just another bank. Srichand P. Hinduja, the eldest of the brothers and head of the Hinduja Group, conceived it as something unique: a bridge between the vast wealth of the Non-Resident Indian community and the capital-starved Indian economy.

The choice of name was deliberate and symbolic. The name 'IndusInd Bank' was inspired by the Indus Valley Civilization - one of the greatest cultural examples of a combination of innovation with sound business and trade practices. The founders weren't just starting a bank; they were positioning themselves as heirs to a 5,000-year tradition of subcontinental commerce.

On April 17, 1994, in a ceremony that brought together India's political and business elite, the bank began its operations after being inaugurated by the then Union Finance Minister Manmohan Singh. The symbolism was powerful: the architect of India's economic liberalization blessing a bank founded by one of India's most successful diaspora families. The Bank began its operations with USD 35 million with the first branch being opened at Opera House, Mumbai.

The capital structure itself told a story about the bank's ambitions. The operations of IndusInd Bank were started with a capital base of Rs. 1,000 million. Of the total 1,000 million, Rs. 600 million was raised through private placements by Indian Residents and Rs. 400 million was contributed by Non-Resident Indians (NRIs). This 60-40 split between resident and non-resident capital wasn't just about funding—it was about creating a institution that could serve as a conduit between global Indian wealth and domestic opportunity.

What set IndusInd apart from its peers—HDFC Bank, ICICI Bank, and the other new entrants—was its DNA. While HDFC came from housing finance and ICICI from project finance, IndusInd carried the Hinduja Group's century-old trading instincts and their deep understanding of cross-border flows. The Group, which by then employed over 200,000 people globally and operated everything from Ashok Leyland trucks to Gulf Oil lubricants, understood something fundamental: India's growth would require not just capital, but the right kind of capital deployed in the right ways.

The Hinduja philosophy—built on Vedic principles of "service with devotion" and collective interest—would shape the bank's approach. But there was also a hard-nosed commercial logic. The Group had been in Iran when the Shah fell. They'd navigated the treacherous waters of the Bofors scandal in the 1980s. They understood risk, both political and financial, in ways that few Indian business houses did.

As 1994 turned to 1995, and the first branches began opening across Mumbai and beyond, the question wasn't whether IndusInd Bank would survive—the Hinduja backing ensured that. The question was whether it could carve out a distinctive position in a market that was about to become extraordinarily competitive. The answer would come from an unexpected source: the humble business of vehicle finance, inherited from another Hinduja company that would soon merge with the bank.

III. Building the Foundation: The First Decade (1994-2004)

The story of IndusInd Bank's first decade reads like a case study in contrarian strategy. While competitors rushed to build retail empires in India's metros, IndusInd quietly assembled the building blocks of what would become a formidable franchise through technology, standards, and a series of prescient acquisitions.

By 2000, the bank became the first new-generation private bank in India to receive the ISO 9001:2000 certification—a distinction that seems quaint today but signaled something important then. In an era when Indian banking was still associated with creaky manual processes and indifferent service, IndusInd was signaling it would compete on operational excellence. It also claims the distinction of being the first bank in India that received ISO 9001:2000 certification for its Corporate Office and its entire network of branches.

The real story, though, begins with a number: $30 million. The Bank issued an Initial Public Offering in November 1997 and raised USD 30 million—modest by today's standards but transformative for a three-year-old bank. The IPO wasn't just about capital; it was about legitimacy. Going public forced discipline, demanded transparency, and most importantly, began the slow process of establishing IndusInd as an institution independent of its promoters.

But the masterstroke came in 2004. In 2004, IndusInd Bank completed its merger with Ashok Leyland Finance, a vehicle financing company which was also part of the Hinduja Group. On paper, this looked like a routine intra-group consolidation—a captive finance company being folded into the group's bank. In reality, it was transformational.

Ashok Leyland Finance wasn't just any vehicle financier. In June 2004, IndusInd Bank was merged with Ashok Leyland Finance Ltd, which was one of the largest leasing finance and hire purchase companies in India, at that time. It brought with it deep relationships with transporters, an understanding of commercial vehicle economics, and most crucially, a credit culture built on financing productive assets rather than consumption.

Think about what this meant: While HDFC Bank and ICICI Bank were fighting over salaried professionals in Mumbai and Delhi, IndusInd suddenly had access to every truck operator from Ludhiana to Coimbatore. While others were figuring out how to assess creditworthiness using salary slips, IndusInd's inherited teams could evaluate a trucker's cash flows by looking at route permits and freight contracts.

The technology infrastructure tells another part of the story. All the branches as well as ATMs of IndusInd Bank are connected to its central database, via a satellite that operates on the latest version of IBM's AS400-720 hardware & Midas Kapiti (now Misys) software. In an era before reliable terrestrial connectivity, IndusInd bet on satellite links—expensive but reliable. The message was clear: we'll spend what it takes to ensure that a customer in Chandigarh has the same experience as one in Chennai.

By 2006, the expansion was accelerating. By 2006, it had expanded its branch network, from 61 in 2004, to 137. But the more interesting number was this: Apart from setting up 150 ATM centers of its own, the bank also concluded multilateral arrangements with other banks, taking the total number of authorized ATM outlets to 15,000. While competitors built their own expensive ATM networks, IndusInd pioneered shared infrastructure—a model that would become standard a decade later.

The product portfolio during this period reveals the bank's evolving ambitions. The Bank widened its product portfolio by introducing services like FAST Forex, Indus Home, Indus Estate, and Indus Auto among many others. Each product name tells a story: FAST Forex for the NRI remittance market, Indus Auto leveraging the Ashok Leyland connection, Indus Estate targeting the emerging real estate boom.

Successfully launched the concept of 'Anywhere Banking' by growing its network to 18 branches and 11 ATMs. Today, "anywhere banking" is table stakes. In the late 1990s, it was revolutionary. Most Indian banks still operated on a branch-specific model—your account belonged to a particular branch, and accessing it elsewhere involved paperwork and delays. IndusInd's satellite-linked network made this obsolete.

The numbers from this period seem modest now but represented geometric growth then. Starting with that single Opera House branch in 1994, by 2004 the bank had built a foundation that would support explosive growth in the next phase. The branch count had crossed 60, the ATM network was expanding, and most importantly, the bank had found its niche: vehicle finance, particularly commercial vehicles, would be its beachhead into the broader market.

But there was a problem. The bank was still subscale, still searching for an identity beyond being "the Hinduja bank." It needed leadership that could think beyond the constraints of a promoter-driven institution. It needed someone who understood global banking but could navigate Indian realities. It needed someone willing to bet big.

In 2008, that someone walked through the door, bringing with him five colleagues from the Royal Bank of Scotland. His name was Romesh Sobti, and he would transform IndusInd from a niche player into a universal bank.

IV. The Romesh Sobti Era: Transformation Begins (2008-2020)

The transformation of IndusInd Bank began not in a boardroom but in a crisis. In early 2008, the global financial system was beginning to crack, and IndusInd Bank—still a niche player with around 180 branches—was struggling to define itself beyond vehicle finance. The board made a decision that would reshape the institution: they needed fresh blood, someone from outside the Hinduja ecosystem who could think like a global banker but execute in the Indian context.

Mr. Romesh Sobti joined the Bank as its Managing Director and CEO, along with five of his colleagues, from RBS Bank. This wasn't just a CEO change; it was a team transplant. He was the CEO and MD of IndusInd Bank from 2008 to 2020, and of ABN AMRO Bank for the previous 12 years. Sobti brought with him the playbook from running one of India's most sophisticated foreign banks, but more importantly, he brought a vision: IndusInd could be more than a vehicle financier with a banking license.

Soon after, the Corporate and Commercial Banking Unit was commissioned with the aim of providing financial and banking solutions to small, mid and large sized corporates. This was the first signal of intent. While the bank's DNA was in retail vehicle finance, Sobti understood that sustainable growth required diversification. Corporate banking wasn't just about adding another revenue stream—it was about de-risking the franchise.

The numbers tell the story of transformation. When Sobti took over, the bank had around 180 branches. By 2012, As at the end of the year, the Bank had a total of 400 branches spread across 270 geographical locations and 692 ATMs inclusive of 345 off-site ATMs. But growth wasn't just about planting flags. Each expansion decision was strategic, each product launch calculated.

Take the Deutsche Bank credit card acquisition in 2011. In 2011, IndusInd Bank acquired Deutsche Bank India's loss-making credit cards division. On paper, this looked puzzling—why buy a loss-making business? But Sobti saw what others missed. The portfolio size of the credit card business with nearly 2,50,000 cardholders is about Rs 225 crore, and more importantly, As part of the deal, IndusInd Bank would also get the services of around 200 professionals from the German bank's credit card division.

This wasn't about the portfolio; it was about capability acquisition. Credit cards are one of the most complex retail banking products—requiring sophisticated risk management, technology infrastructure, and operational excellence. By acquiring Deutsche Bank's platform wholesale, IndusInd leapfrogged years of development. The fact that Prior to joining IndusInd Bank, Ramachandran was heading Deutsche Bank's credit card business in India—whom IndusInd had already hired as head of cards—meant they knew exactly what they were buying.

The strategy extended beyond acquisitions. The Bank launched a host of Savings and Current Account products with a focus on growing the Consumer Banking portfolio. But unlike competitors who chased mass market deposits with high interest rates, IndusInd focused on relationship banking. There was a focused effort on strengthening our Product Delivery capabilities across all product groups - Global Markets, Transaction Banking and Investment Banking.

Technology became a differentiator during this period. On 29 September 2014, IndusInd Bank inaugurated its first digital branch at IndusInd Cybercity Rapid Metro station, Gurgaon. This wasn't just India's first digital branch at a metro station—it was a statement about the bank's ambitions. While others were still figuring out internet banking, IndusInd was experimenting with fully automated branches.

The Diamond & Jewellery financing acquisition from RBS in 2015 followed a similar pattern. On 10 April 2015, IndusInd Bank announced that it has entered into an agreement with Royal Bank of Scotland N.V. to acquire its diamond and jewellery financing business in India and related deposits portfolio. On 27 July 2015, IndusInd Bank announced that it had completed the acquisition of Royal Bank of Scotlands diamond and jewellery financi[ng] Again, this was about acquiring specialized expertise in a high-margin niche that larger banks found too complex to manage.

The cultural transformation under Sobti was equally important. He was also named Business Standard's Banker of the Year for 2013-14. The same year, he was named EY Entrepreneurial CEO of the Year. These weren't just personal accolades—they signaled that IndusInd had arrived as a serious player in Indian banking.

By 2017, the bank was ready for its biggest bet yet. The announcement of the Bharat Financial merger would test everything Sobti had built—the risk management systems, the technology platform, the organizational culture. It would either establish IndusInd as a universal bank or destroy the careful balance he had created.

The foundation was set. The transformation from a vehicle finance company with a banking license to a full-service bank was nearly complete. But the next chapter would involve venturing into India's most challenging and controversial banking segment: microfinance.

V. The Bharat Financial Merger: Scaling Financial Inclusion (2017-2019)

The microfinance story in India cannot be told without understanding its original sin. And that story begins with a Fulbright scholar from Yale named Vikram Akula, who in 1997 returned to India with a vision borrowed from Muhammad Yunus's Grameen Bank but with a uniquely American twist: microfinance could be scaled through capital markets.

As a Ph.D. student, he created a business plan for a for-profit microfinance company and in December 1997, Akula returned to India to set up Swayam Krishi Sangam (SKS) as a vehicle to implement the plan. Initially set up as a non-profit, SKS converted to the for-profit SKS Microfinance in 2005. The transformation from non-profit to for-profit would set the stage for both spectacular growth and devastating controversy.

By 2010, SKS had become the poster child for Indian microfinance's promise and peril. On 28 July 2010, SKS Microfinance debuted on the Bombay Stock Exchange with an IPO that was oversubscribed 14 times and which raised $350 million. This was India's first microfinance IPO, and it made Akula and his investors spectacularly wealthy. But within months, the industry would face its darkest hour.

In September 2010, reports surfaced in the media of nearly 200 suicides by defaulters of a number of micro finance institutions, including SKS finance. The Andhra Pradesh government cracked down, effectively shutting down microfinance operations in the state. SKS's stock price collapsed. The company's shares meanwhile lost 96% of their value from a high of Rs. 1491.50 in 2010. Akula resigned. The dream seemed dead.

But from the ashes emerged a different entity. In 2016, SKS Microfinance was renamed to Bharat Financial Inclusion Ltd. The rebranding was more than cosmetic—it was an attempt to distance the company from its controversial past while signaling a broader mission. By 2017, under new management and with cleaned-up operations, Bharat Financial had quietly rebuilt itself into one of India's largest microfinance institutions.

Enter Romesh Sobti's IndusInd Bank, looking for the next big leap. In October 2017, IndusInd Bank announced its acquisition of Bharat Financial Inclusion Limited (BFIL) for ₹15,000 crore (US$2.3 billion). To understand the audacity of this move, consider the context: microfinance was still toxic in banking circles, the Andhra Pradesh crisis memories were fresh, and no major bank had attempted such a large microfinance acquisition.

Bharat Financial Inclusion Limited fits with the Rural Banking and Microfinance theme of IndusInd's Planning Cycle-4 strategy, and will provide IndusInd access to best in class micro-lending capabilities and domain expertise in microfinance. The strategic logic was compelling. Bharat Financial Inclusion Limited has 1,408 branches across 347 districts—instant rural distribution that would take decades to build organically.

The numbers were staggering. IndusInd Bank's 10 million strong customer base will stand enhanced through the addition of Bharat Financial Inclusion Limited's 6.8 million borrowers. But this wasn't just about adding customers; it was about accessing an entirely different India—the India of villages and small towns, of women's self-help groups and weekly repayment meetings.

The integration strategy was novel. Rather than fully absorbing Bharat Financial, IndusInd chose to maintain it as a subsidiary. This served multiple purposes: it preserved the specialized microfinance expertise, maintained the separate brand identity crucial for rural customers, and critically, kept the regulatory treatment distinct. Microfinance loans have different priority sector classifications and capital requirements—maintaining the subsidiary structure allowed IndusInd to optimize both.

The merger was officially completed in July 2019. The two-year gap between announcement and completion tells its own story—of regulatory negotiations, of careful integration planning, of transforming a crisis-scarred institution into a crown jewel.

The cultural integration was perhaps the biggest challenge. IndusInd's bankers, trained in corporate finance and urban retail banking, suddenly had colleagues whose expertise was in lending ₹20,000 to women who had never held a bank account. The technology stacks were different—IndusInd's sophisticated core banking system versus Bharat Financial's field-force management apps. The risk models were worlds apart—how do you reconcile corporate credit ratings with joint liability groups?

But Sobti and his team pulled it off. By maintaining operational independence while integrating treasury and risk management functions, they created a model that others would later copy. The subsidiary structure allowed Bharat Financial to continue its field operations unchanged while benefiting from IndusInd's lower cost of funds and superior technology infrastructure.

The impact on priority sector lending was immediate and dramatic. Indian banks are required to lend 40% of their adjusted net bank credit to priority sectors—agriculture, small enterprises, and weaker sections. For most banks, meeting these targets is a compliance burden. For IndusInd, Bharat Financial turned it into a profit center. The microfinance portfolio, with its high yields and surprisingly low default rates (when properly managed), became a key earnings driver.

By early 2020, as Sobti prepared to hand over the reins after twelve transformative years, IndusInd Bank had become something unprecedented in Indian banking: a universal bank with genuine rural reach, a corporate franchise with a microfinance heart, a Hinduja Group company that had transcended its promoter identity. The integration of Bharat Financial was complete, successful beyond most expectations.

But beneath this success lurked risks that few understood. The aggressive growth had created operational complexities. The multiple acquisitions had layered different cultures and systems. And in the treasury department, creative solutions to manage the bank's growing foreign currency exposure were creating hidden vulnerabilities that would soon explode into crisis.

VI. Modern Era & Digital Evolution (2020-Present)

The timing could not have been worse—or perhaps, in hindsight, better. Sumant Kathpalia was appointed the next managing director (MD) and chief executive officer (CEO) from March 24, 2020, for a three-year term. Four days after taking charge, India went into the world's strictest COVID-19 lockdown. The new CEO of a bank with 3,000 branches and 40 million customers suddenly had to manage from his Mumbai apartment.

Kathpalia wasn't an outsider. Having been a part of the core leadership team at IndusInd since its early days, joining along with Sobti in 2008, he understood the bank's DNA. He has been pivotal in turning the bank around. But stepping into Sobti's shoes during a global pandemic while managing a complex universal bank was a different challenge entirely.

Where Sobti had been the charismatic dealmaker, Kathpalia was the operations expert. With over 30 years in the banking industry, having worked with Citibank, Bank of America, and ABN AMRO, his expertise lay in building scalable systems and digital infrastructure. This would prove prescient.

The pandemic accelerated India's digital transformation by years, and IndusInd was ready. The bank's digital initiatives weren't pandemic reactions but strategic bets placed years earlier. The Video Branch service, launched pre-COVID with much fanfare featuring Bollywood star Farhan Akhtar, suddenly became essential infrastructure. Customers could open accounts, apply for loans, and even get financial advice without stepping into a branch.

The numbers tell the story of transformation. As of December 2024, the bank has 42 million customers, 3,063 branches, and 2,993 ATMs in India. But the real growth was in digital channels. Mobile banking transactions grew 300% in the first two years of Kathpalia's tenure. The bank's app wasn't just for balance checks anymore—it became a full-service financial platform.

India's 2nd largest microfinance lender, operating through its subsidiary Bharat Financial Inclusion Limited (BFIL), serving over 13 Mn customers—this positioning became even more critical during the pandemic. While urban India moved online, rural India still needed physical touchpoints. The Bharat Financial field force, trained to conduct meetings in village squares, adapted to social distancing norms while maintaining the personal touch essential to microfinance.

The sports partnerships that seemed frivolous to some analysts proved their worth during this period. The bank's association with cricket—India's religion—kept the brand visible even during lockdowns. When sports resumed, IndusInd was everywhere, from IPL team sponsorships to grassroots cricket programs. These weren't just marketing expenses; they were investments in brand trust at a time when digital-only interactions could feel impersonal.

Kathpalia's strategic priorities differed from Sobti's. While his predecessor focused on acquisitions and expansion, Kathpalia emphasized consolidation and digitization. Throughout his stint as the MD&CEO of the bank, Kathpalia has put a thrust on strengthening balance sheet, fortifying liability franchise with retailization of deposits, diversifying and building new domain expertise areas. The shift from wholesale to retail deposits reduced concentration risk. The focus on casa (current account and savings account) improved margins.

The technology investments were substantial but targeted. IndusInd didn't try to outspend HDFC Bank or ICICI Bank on technology. Instead, it picked its battles. The bank became a leader in API banking, allowing fintechs to integrate IndusInd services into their apps. The merchant acquiring business exploded as India's UPI revolution took off. The credit card business, acquired from Deutsche Bank a decade earlier, was reimagined for the digital age with contactless cards and instant issuance.

But the most significant achievement of the Kathpalia era might be something that didn't happen: there were no major acquisitions. After years of growth through M&A, IndusInd focused on organic growth and integration. The Bharat Financial subsidiary was fully integrated into the bank's risk and treasury systems. The various businesses acquired over the years—vehicle finance, credit cards, microfinance—were finally working as one cohesive unit.

The cultural transformation was subtle but important. The bank launched initiatives for employee wellness, diversity, and inclusion. The "Great Place to Work" certification wasn't just a trophy—it represented a fundamental shift in how the bank viewed its human capital. In a industry notorious for burnout and turnover, IndusInd was building a sustainable workforce.

By 2023, Kathpalia's transformation seemed complete. The bank had successfully navigated the pandemic, digital adoption was soaring, asset quality had improved post-COVID, and the stock price had recovered to pre-pandemic highs. The RBI had initially approved only a two-year extension for Kathpalia in March 2023 while the bank's board had approved his re-appointment for three years—a minor concern that seemed like regulatory conservatism.

The bank's representative offices in London, Dubai and Abu Dhabi, its clearing bank status for both major stock exchanges - BSE and NSE - and major commodity exchanges in the country including MCX, NCDEX, and NMCE, positioned it as a truly international Indian bank. Everything seemed to be going according to plan.

But beneath this success, problems were brewing in an unexpected corner of the bank: the treasury department's derivative book, where complex hedging strategies designed years earlier were about to explode into the biggest crisis in the bank's history.

VII. The 2025 Crisis: Derivatives Debacle & Leadership Change

The unraveling began with what seemed like routine regulatory compliance. The matter arose after a September 2023 directive from the Reserve Bank of India (RBI) mandating banks to adopt mark-to-market valuation for derivatives. An internal review conducted later that month revealed discrepancies in the valuation of certain legacy derivative contracts over multiple years.

But this wasn't routine at all. For years, IndusInd Bank had been running two parallel worlds in its treasury operations—one internal, one external—with different accounting treatments for each. Over the last five to seven years, the bank's asset-liability desk hedged the foreign currency deposits that it swapped into rupees internally with the treasury desk to mitigate the interest rate risk, while the latter hedged the foreign currency risk with an external counterparty. The external trades were marked-to-market, meaning they reflected real-time market movements and were mostly profitable for the bank, adding to its trading gains. But the internal trades were not being marked-to-market and that caused losses to remain concealed and not be reflected on the bank's profit and loss statement until matters came to a head in March.

The complexity of this arrangement cannot be overstated. When an NRI deposited dollars with IndusInd, the bank would convert these to rupees for lending. To protect against currency fluctuations, it would enter into internal swaps with its trading desk. The trading desk would then hedge externally. But here's where it gets problematic: the external hedges were marked to market daily, showing profits when the rupee weakened. The internal swaps, however, were kept at historical rates. This created a massive accounting mismatch that grew larger as currency volatility increased.

Initial estimates in December 2023 placed the potential financial impact at ₹1,572 crore, which was later revised upward to ₹2,361 crore by May 2024. The numbers kept growing as the bank dug deeper. Independent audits by PwC and Grant Thornton confirmed the material nature of these discrepancies, with Grant Thornton estimating a cumulative impact of approximately ₹1,960 crore.

Then came March 11, 2025—a date that will live in infamy for IndusInd shareholders. On 11 March 2025, IndusInd Bank's shares crashed over 27% after it disclosed discrepancies in its forex derivatives portfolio, with analysts raising questions on the bank's internal controls. On Tuesday, IndusInd Bank share crashed 27.17 per cent on the BSE, recording its biggest one-day fall since listing. The stock ended at Rs 655.95 per share, its lowest level since November 2020.

The market reaction was brutal but perhaps not surprising. The lender, on Monday, informed its shareholders that an internal review of forex derivative transactions has unearthed an accounting mismatch worth Rs 1,577 crore (post-tax), which is about 2.35 per cent of the bank's net worth at the end of December 2024. For a bank, a 2.35% hit to net worth isn't just a number—it's a massive breach of trust.

But the derivatives issue was only part of the problem. The leadership situation added fuel to the fire. The RBI had earlier given Kathpalia only a one-year extension instead of the three years the board had requested. This shorter-than-expected tenure raised immediate questions about succession planning and regulatory confidence in the current management.

The human drama unfolded quickly. In response to the discrepancies, IndusInd Bank's Managing Director and CEO, Sumant Kathpalia, resigned in April 2025, taking moral responsibility for accounting irregularities in the bank's derivatives portfolio. His resignation followed that of Deputy CEO Arun Khurana, who stepped down a day earlier.

But then came the most damaging revelation. In May 2025, SEBI took action against five former top executives of IndusInd Bank, including the CEO Sumant Kathpalia. SEBI accused them of selling shares before the bank publicly announced the losses, avoiding about ₹20 crore in losses. SEBI froze their accounts and barred them from trading while the investigation continues.

The insider trading allegations transformed what might have been seen as an accounting error into a potential criminal matter. The optics were devastating: executives who knew about the problems selling their shares while ordinary investors remained in the dark.

The regulatory response was swift and severe. In the aftermath, the country's central bank, the Reserve Bank of India (RBI), has asked the CEO of the bank and his deputy to step down as soon as replacements are found and approved by it. The RBI also launched a sector-wide review. The Reserve Bank of India (RBI) has launched a sector-wide review of derivative positions across banks after Indusind bank ₹1,500 crore loss.

The technical details that emerged painted a picture of systematic failure. The derivative accounting practices escaped regulatory checks as the complexities of the trades and the valuation models made it difficult for regulators and [auditors to detect] How could auditors, internal and external, miss such large discrepancies for years? How could the board, with its multiple committees, not catch this?

The answer lies partly in the complexity of the instruments and partly in what appears to be a culture of aggressive profit pursuit. IndusInd Bank ignored established Indian derivative accounting practices for years as it chased profit growth, resulting in a $175 million balance-sheet hole and the biggest crisis for the lender in its three-decade history.

The crisis revealed deeper issues about corporate governance at IndusInd. The Hinduja family, while the largest shareholder, had maintained a relatively hands-off approach, trusting professional management. This trust now seemed misplaced. The board, packed with distinguished names, had failed in its primary duty of oversight.

In April 2025, the bank reported a reduction in net worth of ₹1,979 crore, or 2.27%, following revaluation adjustments. The final number was slightly better than initial fears, but the damage to reputation was incalculable.

For employees, customers, and shareholders, the crisis was a betrayal. The bank that had positioned itself as technologically advanced and professionally managed had been hiding losses through accounting sleight of hand. The institution that Sobti had built over twelve years, that Kathpalia was supposed to take to the next level, lay in tatters.

As 2025 progressed, IndusInd Bank found itself fighting on multiple fronts: regulatory investigations, potential lawsuits from shareholders, a leadership vacuum, and most critically, a complete loss of market confidence. The question was no longer about growth or market share—it was about survival.

VIII. Business Model & Competitive Analysis

Even in crisis, IndusInd Bank's fundamental business model remains distinctive in Indian banking. Understanding this model—its strengths, vulnerabilities, and competitive positioning—is crucial to evaluating whether the bank can recover from its current predicament.

As of December 2024, the bank has 42 million customers, 3,063 branches, and 2,993 ATMs in India. These numbers place IndusInd as a mid-sized player by physical presence but with outsized influence in specific niches. The customer base of over 41 mn with a market capitalization of $6.40 Bn (as of April 2, 2025) tells a story of value destruction—the market cap should be much higher given the customer base.

The three-pillar strategy that emerged from the Sobti era remains intact: vehicle finance, microfinance, and corporate banking. Each pillar has its own economics, risks, and competitive dynamics.

Vehicle finance, the original DNA inherited from Ashok Leyland Finance, remains the crown jewel. In a country adding millions of vehicles annually, IndusInd's deep relationships with manufacturers, dealers, and fleet operators create a moat. The bank doesn't just lend against vehicles; it understands transportation economics, route profitability, and operator cash flows in ways that universal banks never will. This expertise allows for better underwriting, lower defaults, and premium pricing.

The microfinance arm, through Bharat Financial, serves over 13 million customers—making IndusInd India's 2nd largest microfinance lender. The economics here are compelling: interest rates of 18-24% (down from 26%+ pre-crisis), operating costs managed through technology and scale, and surprisingly low default rates when properly managed. The joint liability group model, where peer pressure substitutes for collateral, works because of India's social structures.

Corporate banking was Sobti's addition and remains the most challenged. Here, IndusInd competes directly with State Bank of India's relationships, HDFC Bank's balance sheet, and ICICI Bank's product sophistication. The bank has found niches—mid-corporates ignored by large banks, sectors like textiles and diamonds where specialized knowledge matters—but margins are thin and competition fierce.

The Bank has representative offices in London, Dubai and Abu Dhabi and enjoys clearing bank status for both major stock exchanges - BSE and NSE - and major commodity exchanges in the country including MCX, NCDEX, and NMCE. This infrastructure positions IndusInd uniquely for cross-border flows and commodity financing, areas where many private banks lack expertise.

The competitive landscape has evolved dramatically since 1994. HDFC Bank, with its recent merger with HDFC Ltd, has become a behemoth with over ₹20 trillion in assets. ICICI Bank has successfully transformed from a corporate lender to a retail powerhouse. Kotak Mahindra Bank has built a premium franchise focusing on wealth management. Axis Bank has become the digital innovation leader.

Against these giants, IndusInd's positioning is precarious but not hopeless. It cannot match HDFC's scale, ICICI's retail reach, Kotak's premium brand, or Axis's digital capabilities. But it doesn't need to. The combination of vehicle finance expertise, microfinance reach, and selective corporate relationships creates a unique franchise.

The technology strategy reflects this positioning. IndusInd doesn't try to out-innovate the leaders but focuses on specific areas. The bank's APIs are among the best in India, making it a preferred partner for fintechs. The merchant acquiring business leverages the vehicle finance network—fuel stations, spare parts dealers, insurance agents—creating a ecosystem play that others struggle to replicate.

IndusInd Bank is the only Indian bank and one of the 55 banks globally to be included in the S&P DJSI Sustainability Yearbook. This ESG positioning, while seemingly cosmetic, matters increasingly to international investors and corporate clients. In a world where sustainability is becoming a lending criterion, IndusInd's early positioning could become a differentiator.

The priority sector lending strategy showcases the model's elegance. RBI mandates that 40% of adjusted net bank credit go to priority sectors. For most banks, this is a drag on profitability—forced lending to agriculture and small enterprises at controlled rates. For IndusInd, with Bharat Financial's microfinance portfolio and vehicle finance to small transporters, priority sector lending is a profit center. The bank regularly sells priority sector lending certificates to other banks, turning a regulatory requirement into a revenue stream.

But the model has vulnerabilities, now painfully exposed. The dependence on wholesale funding—NRI deposits, corporate deposits, market borrowings—makes the bank vulnerable to confidence crises. The complexity of managing three distinct businesses creates operational risks. The Hinduja Group connection, while providing stability, raises questions about related-party transactions and governance.

The fintech challenge is particularly acute. New-age players like Paytm Payments Bank, PhonePe, and Google Pay are attacking the payments business. Digital lenders like Slice and Jupiter target the young customers IndusInd needs for future growth. The bank's response—partnerships rather than competition—may be pragmatic but cedes ground to nimbler players.

International expansion remains limited despite the representative offices. Unlike ICICI or Axis, which have built significant international franchises, IndusInd remains India-focused. This concentration has benefits—no exposure to international crises—but limits growth options and diversification.

The derivatives crisis has exposed the most fundamental vulnerability: complexity without adequate controls. The bank's attempt to optimize every basis point of profit through elaborate hedging strategies created risks that even senior management didn't fully understand. This isn't unique to IndusInd—the 2008 financial crisis showed that complexity itself is a risk—but the bank learned this lesson the hard way.

Post-crisis, the business model needs recalibration rather than revolution. The vehicle finance and microfinance franchises remain strong. Corporate banking needs to be more selective. Treasury operations require complete overhaul. Digital investments must accelerate. Most critically, the bank needs to simplify—fewer products, clearer strategies, better controls.

The question isn't whether IndusInd's business model is viable—it clearly is. The question is whether the bank can execute this model with the operational excellence required in modern banking. The ingredients are there; what's missing is the recipe and perhaps the chef.

IX. Playbook: Key Lessons & Strategic Insights

The IndusInd story offers a masterclass in both value creation and value destruction. For investors, bankers, and business students, the lessons are profound and sometimes contradictory.

The Power of Focused Acquisition Strategy

IndusInd's acquisition track record is remarkable for its consistency and strategic logic. Ashok Leyland Finance (2004) brought vehicle finance DNA. Deutsche Bank's credit cards (2011) added consumer lending capability. Bharat Financial (2017-2019) delivered microfinance scale. Each acquisition filled a specific gap, brought specialized expertise, and was integrated thoughtfully.

Compare this to peers' scattershot approaches—random branch purchases, unsuccessful bancassurance ventures, failed international expansions. IndusInd's acquisitions were transformative because they were strategic, not opportunistic. The lesson: in banking, where integration is complex and culture matters, fewer, larger, more strategic acquisitions beat multiple small deals.

Building a Universal Bank from Specialized Roots

Most universal banks evolved from universal ambitions. IndusInd did the opposite—it became universal by combining specialized franchises. This "portfolio of niches" approach has advantages: deep expertise in each area, better risk assessment, premium pricing power, and natural hedges across business cycles.

But it also creates challenges: complexity in management, difficulty in cross-selling, cultural conflicts between businesses, and operational risks from running multiple distinct operations. The derivative crisis exemplifies this—the treasury tried to optimize across businesses but created risks nobody fully understood.

Managing Conglomerate Ownership While Maintaining Professional Management

The Hinduja paradox is fascinating. They're the largest shareholders but maintained arms-length distance. They provided stability during crises but didn't interfere in operations. They enabled the bank to leverage group relationships but avoided related-party transactions.

This balance is rare in Indian business. Compare with other promoter-driven banks that struggled with governance issues. The Hindujas' approach—ownership without interference—enabled professional management to flourish. Until it didn't. The derivatives crisis raises questions about whether more active oversight might have prevented problems.

The Importance of CEO Succession Planning

The Sobti-to-Kathpalia transition seemed textbook perfect. An insider who understood the culture, had been part of the transformation, and brought complementary skills. The timing during COVID was unfortunate but manageable. What went wrong?

The derivative issues predated Kathpalia but exploded on his watch. The RBI's reluctance to give him a full term suggests concerns about oversight. The insider trading allegations, even if unproven, destroyed credibility. The lesson: succession planning isn't just about capability; it's about timing, context, and sometimes luck.

Risk Management Failures and Recovery Strategies

The derivative debacle is a classic risk management failure: complex instruments, inadequate controls, aggressive accounting, regulatory arbitrage, and ultimately, catastrophic discovery. But every bank has hidden risks. What matters is how they're managed when exposed.

IndusInd's response has been textbook crisis management: immediate disclosure (though forced), external audits, leadership accountability, and capital adequacy assurance. But the reputational damage is severe. Recovery requires not just fixing problems but rebuilding trust—a much longer journey.

Balancing Growth with Regulatory Compliance

IndusInd's growth under Sobti was spectacular—from 180 to 2,500+ branches, from niche player to universal bank. But growth creates complexity, and complexity creates risks. The bank pushed boundaries—in products, geographies, customer segments—faster than it built control systems.

The regulatory response to the crisis—forced leadership changes, sectoral reviews, potential penalties—shows the cost of prioritizing growth over compliance. In Indian banking, with its history of failures and frauds, regulatory conservatism isn't optional.

The Microfinance Opportunity in India

Despite the SKS crisis and Andhra Pradesh debacle, IndusInd's bet on microfinance through Bharat Financial looks prescient. Financial inclusion isn't just a social goal; it's a massive business opportunity. With 13 million microfinance customers generating high yields with manageable defaults, this is becoming a core profit driver.

The key insights: maintain microfinance as a separate subsidiary to preserve specialized skills; use technology to reduce costs while maintaining high-touch service; and leverage the distribution network for other products. The microfinance acquisition may be IndusInd's most important strategic move.

Strategic Insights for Investors

First, beware complexity in financial institutions. When you don't understand how a bank makes money, danger lurks. IndusInd's derivative strategies were too complex for most analysts to evaluate—a red flag in hindsight.

Second, watch for governance gaps in professionally-managed, promoter-owned companies. The combination can work brilliantly but requires constant vigilance. When professional managers have too much autonomy, or when promoters are too distant, problems can fester.

Third, in banking, culture eats strategy for breakfast. IndusInd built a growth culture under Sobti but perhaps didn't build an equally strong risk culture. The emphasis on profits and market share came at the cost of controls and compliance.

Fourth, regulatory relationships matter more than financial metrics. The RBI's decision to give Kathpalia only one year extension was a warning signal months before the derivative crisis. Regulatory body language often precedes formal action.

Fifth, recovery from reputational damage takes years, not quarters. IndusInd's fundamentals—the franchise businesses, customer base, distribution network—remain strong. But rebuilding trust with depositors, investors, and regulators will take sustained effort and probably new leadership.

The IndusInd playbook, despite recent failures, contains valuable lessons. The focused acquisition strategy works. Building from niches to universal can succeed. Professional management in promoter-owned companies is possible. But execution excellence, risk management, and regulatory compliance aren't optional—they're existential.

X. Bear vs. Bull Case & Valuation Analysis

The IndusInd Bank investment thesis has never been more polarized. Bears see a broken institution with hidden risks and destroyed credibility. Bulls see a fundamentally strong franchise trading at distressed valuations. Both have compelling arguments.

Bear Case: The Structural Pessimist's View

The corporate governance failures revealed by the derivatives crisis aren't isolated incidents but symptoms of deeper problems. When senior executives are accused of insider trading, when accounting discrepancies hide for years, when auditors miss billion-rupee holes, the rot runs deep. These aren't mistakes; they're systematic failures that take years to fix.

The regulatory overhang is just beginning. The RBI forced leadership changes are the start, not the end. Expect heavy penalties, business restrictions, enhanced supervision, and possible criminal prosecutions. Indian regulators, burned by past banking failures, will make an example of IndusInd. The stock could remain under pressure for years.

Asset quality concerns in the microfinance portfolio are understated. Bharat Financial operates in the riskiest segment of lending—unsecured loans to the poorest borrowers. The next economic downturn, drought, or political populism (loan waivers) could trigger massive defaults. The 2010 Andhra Pradesh crisis showed how quickly microfinance can implode. IndusInd is sitting on a powder keg.

Competition from larger private banks and fintechs will intensify. HDFC Bank, post-merger, has unlimited firepower. ICICI and Axis have cleaned up their balance sheets and are aggressive. Fintechs are cherry-picking the best customers with superior digital experiences. IndusInd, distracted by internal issues, will lose market share.

The execution risks in digital transformation are mounting. While peers invested heavily in technology, IndusInd focused on acquisitions. The bank's core systems are aging, digital capabilities lag, and customer experience suffers. Catching up requires massive investments precisely when the bank needs to conserve capital.

The Hinduja Group's reputation, tainted by various controversies over decades, adds another layer of risk. While they've maintained distance from operations, any group-level scandal could trigger deposit flight. In banking, perception is reality, and the perception is damaged.

Valuation might be a trap. Yes, the stock trades at historic lows, but for good reason. Until there's clarity on leadership, regulatory penalties, and hidden risks, the stock is uninvestable for institutions. Retail investors believing in "buying when there's blood on the streets" might find more blood coming.

Bull Case: The Contrarian's Opportunity

The franchise value remains intact despite recent troubles. Vehicle finance, microfinance, and the branch network have real, sustainable competitive advantages. Customers haven't fled, loans are being repaid, branches remain profitable. The operational business, distinct from treasury misadventures, continues performing.

IndusInd Bank's recognition in the S&P DJSI Sustainability Yearbook reflects genuine ESG strengths that matter increasingly to global investors. The bank's sustainability initiatives, rural focus, and financial inclusion efforts position it well for ESG-focused capital flows once governance issues are resolved.

The underlying profitability of the franchise businesses is robust. Vehicle finance generates 15%+ ROEs, microfinance yields 20%+ with manageable credit costs, and the fee businesses grow steadily. Strip away the one-time hits and corporate governance issues, and you have a highly profitable bank.

Under-penetrated rural markets offer massive growth potential. With Bharat Financial's infrastructure and IndusInd's products, the bank can capture the financial inclusion opportunity better than peers. Rural India's formalization, digitization, and prosperity create a multi-decade growth runway.

Recovery potential post-crisis with new leadership could surprise markets. History shows that banks recovering from crises often deliver spectacular returns. New management, freed from past baggage, could unlock value through better execution, simplified operations, and restored credibility.

Attractive valuations relative to peers create asymmetric risk-reward. Trading at a significant discount to book value while peers trade at premiums, the downside is limited while upside potential is substantial. For patient investors willing to wait through the crisis, current prices offer a once-in-a-decade opportunity.

Valuation Analysis: Finding Fair Value in Chaos

Traditional valuation metrics break down during crises. Price-to-book, the banking standard, is complicated by questions about book value itself—how many more derivative losses lurk? P/E ratios are meaningless when earnings are negative or artificially depressed by one-time charges.

The sum-of-parts valuation might be more relevant. Value the vehicle finance business like a specialized NBFC, the microfinance subsidiary at peer multiples, the branch network as a distribution franchise, and the corporate book at a discount. This approach suggests significant value even after haircuts for governance issues.

Scenario analysis provides another framework. In the worst case—more hidden losses, heavy penalties, prolonged leadership vacuum, deposit flight—the stock could fall another 30-40%. In the base case—contained losses, moderate penalties, new leadership by 2026, gradual recovery—fair value is 50% above current levels. In the best case—no more surprises, strong new CEO, regulatory clarity, market share gains—the stock could double.

The deposit franchise value shouldn't be ignored. Even with reputational damage, 40+ million customers and 3,000 branches have inherent value. In a consolidating industry, IndusInd could be an acquisition target for foreign banks entering India or domestic banks seeking scale.

The Verdict: Time Horizon Determines Truth

For short-term investors, IndusInd is toxic. More negative news is likely, regulatory actions pending, leadership uncertainty persists. The stock could remain volatile and underperform for quarters.

For long-term investors, it's a different calculation. The franchise has real value, the business model works, and India's growth story remains intact. If you believe IndusInd survives this crisis—and history suggests it will—current valuations offer compelling risk-reward for patient capital.

The key variables to monitor: regulatory penalties (size and scope), new leadership (quality and credibility), quarterly results (core business performance), and deposit trends (flight or stability). These will determine whether IndusInd is a value trap or opportunity of a decade.

XI. Epilogue & Future Outlook

As monsoon clouds gather over Mumbai in mid-2025, IndusInd Bank finds itself at the most critical juncture in its 31-year history. The institution that began as a bridge between NRI wealth and Indian opportunity now fights for its credibility, perhaps its very survival.

The search for new leadership post-Kathpalia has become Indian banking's most watched drama. The ideal candidate must possess an impossible combination: unimpeachable integrity to restore trust, operational expertise to fix broken systems, strategic vision to compete with larger rivals, and political skills to manage promoters, regulators, and stakeholders. Names circulate—retired deputy governors, foreign bank veterans, successful entrepreneurs—but none seem perfect.

The RBI's stance will ultimately determine IndusInd's fate. If regulators view this as an isolated incident requiring surgical intervention, the bank recovers. If they see systematic failures requiring fundamental restructuring, the path becomes treacherous. Early signals suggest measured response—the RBI wants lessons learned, not banks destroyed—but regulatory patience has limits.

Digital banking evolution accelerates while IndusInd struggles internally. Every day spent fighting fires is a day lost to digital transformation. New-age banks like Jupiter and Fi, backed by patient venture capital, are building what IndusInd should have built. The window to establish digital leadership is closing rapidly.

The neo-bank competition represents an existential challenge traditional banks underestimate. These aren't just apps but fundamentally different business models—zero marginal cost customer acquisition, AI-driven underwriting, platform economics. IndusInd's response—partnering rather than competing—may be pragmatic but cedes the future to new entrants.

Can IndusInd Bank recover its reputation and growth trajectory? History suggests yes, but with caveats. Banks are resilient institutions—they survive crises that would destroy other businesses because society needs them to survive. IndusInd's core franchises remain valuable, its customer relationships intact, its licenses irreplaceable.

Recovery requires three things: competent new leadership that markets trust, clean resolution of all legacy issues without more surprises, and strategic focus on core strengths rather than growth for growth's sake. The first depends on the board and RBI, the second on forensic audits, the third on discipline—all achievable but not guaranteed.

The future of financial inclusion in India provides context for IndusInd's importance. With 13 million microfinance customers through Bharat Financial, the bank serves people no other private bank reaches effectively. This isn't just business; it's social infrastructure. The government and RBI need IndusInd to succeed for financial inclusion to work.

Final reflections on building a bank in liberalized India reveal sobering truths. The original nine new-generation banks of 1994 have had varied fates—some merged, some struggled, few thrived. Success required more than licenses and capital; it demanded execution excellence, regulatory navigation, and occasional luck.

IndusInd's journey from NRI dream to universal bank to crisis-struck institution encapsulates Indian banking's post-liberalization story—spectacular growth, aggressive innovation, inadequate controls, and periodic crises. The bank isn't unique in facing troubles but is unique in how publicly and dramatically they've unfolded.

The broader implications extend beyond one bank. If IndusInd, with its professional management and sophisticated systems, could hide derivative losses for years, what lurks in other banks? The RBI's sector-wide review might uncover more surprises. Indian banking's next chapter might involve painful but necessary cleansing.

For the Hinduja family, this crisis tests their philosophy of "dharma" in business. Do they intervene more actively, risking regulatory scrutiny but potentially accelerating recovery? Or maintain distance, preserving governance standards but accepting slower resolution? Their choice will influence not just IndusInd but perceptions of promoter-owned banks.

For employees, the crisis is personal. Thousands of careers built on IndusInd's growth now face uncertainty. The best talent might leave for stabler institutions, creating a vicious cycle of capability loss. But crises also create opportunities—young managers can step up, new ideas get heard, transformations become possible.

For customers, especially those 13 million microfinance borrowers, IndusInd's survival matters viscerally. These aren't customers with multiple banking relationships; IndusInd might be their only formal financial connection. The bank's failure would push millions back to moneylenders—a social catastrophe regulators won't allow.

For investors, IndusInd becomes a test case for crisis investing in India. Can you make money buying distressed banks? History says yes—those who bought ICICI Bank during its 2015-16 NPA crisis made fortunes. But timing matters, and catching falling knives is dangerous.

The next twelve months will determine IndusInd's trajectory for the decade. New leadership must be appointed and accepted by markets. Regulatory penalties must be absorbed without crippling capital. Customer confidence must be rebuilt through consistent execution. The derivative mess must be fully resolved without more surprises.

If IndusInd navigates this crisis successfully, it emerges stronger—chastened but cleansed, smaller but focused, humbled but hungrier. The bank that emerges won't be the aggressive growth machine of the Sobti era or the ambitious universal bank Kathpalia envisioned. It will be something different—perhaps better.

The IndusInd story isn't ending; it's transforming. From promotion by NRIs to professional management, from vehicle finance to universal banking, from growth to crisis—each chapter led naturally to the next. The current crisis, painful as it is, might catalyze the next transformation: from universal bank to focused financial institution, from growth obsession to sustainable excellence, from complexity to simplicity.

As this is written, IndusInd Bank continues operating—branches open, ATMs dispense cash, loans get disbursed, deposits get collected. The mundane machinery of banking grinds on despite boardroom drama and regulatory scrutiny. In this resilience lies hope. Banks are harder to kill than most imagine.

The question isn't whether IndusInd Bank survives—it almost certainly will. The question is what it becomes: a cautionary tale of hubris and failed governance, or an inspiring story of redemption and transformation? The answer lies not in spreadsheets or strategy documents but in the character and competence of leaders yet to be chosen, decisions yet to be made, and trust yet to be earned.

The Indus Valley Civilization, after which the bank is named, thrived for over 1,000 years before mysteriously declining. IndusInd Bank has existed for just 31 years. Whether it builds a similar legacy of longevity or becomes another archaeological curiosity in Indian banking's history depends on choices being made in boardrooms and regulatory offices across Mumbai today.

The story continues, and its ending remains unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube