Expand Energy Corporation: The Story of America's Natural Gas Giant

I. Introduction & Episode Roadmap

The boardroom at One Leadership Square in Oklahoma City was electric with tension on October 1, 2024. After months of integration work, regulatory approvals, and market speculation, the moment had arrived. The company that Aubrey McClendon had named after his beloved Chesapeake Bay—a company that had once commanded a $35 billion market cap, then crashed through bankruptcy, wiping out $7 billion in debt—was about to disappear. In its place: Expand Energy Corporation, instantly America's largest natural gas producer and one of the top producers globally.

The rebrand wasn't just cosmetic. It represented the final chapter in one of American business's most dramatic boom-bust-rebirth sagas. How did two 23-year-old wildcatters with $50,000 between them build an energy empire that would revolutionize American drilling, only to watch it implode spectacularly? How did that same company emerge from the ashes of bankruptcy to swallow its competitors and dominate an industry?

This is a story of geological insight and financial engineering, of corporate excess and boardroom coups, of technological breakthroughs and environmental backlash. It's about the men who saw America's energy independence buried two miles underground and figured out how to extract it—even if it nearly destroyed them in the process.

The narrative arc spans four decades and multiple boom-bust cycles. We'll explore how Aubrey McClendon's vision and salesmanship, combined with Tom Ward's operational discipline, created the template for the shale revolution. We'll examine the corporate governance failures that led to McClendon's dramatic ouster and tragic death. We'll dissect the bankruptcy that should have been the end but instead became a new beginning.

Most importantly, we'll analyze what Expand Energy's journey teaches us about commodity businesses, capital allocation, and corporate governance. Because while the names and faces change, the fundamental tension remains: How do you build lasting value in an industry defined by violent cycles? The answer, as we'll see, isn't always what Wall Street wants to hear.

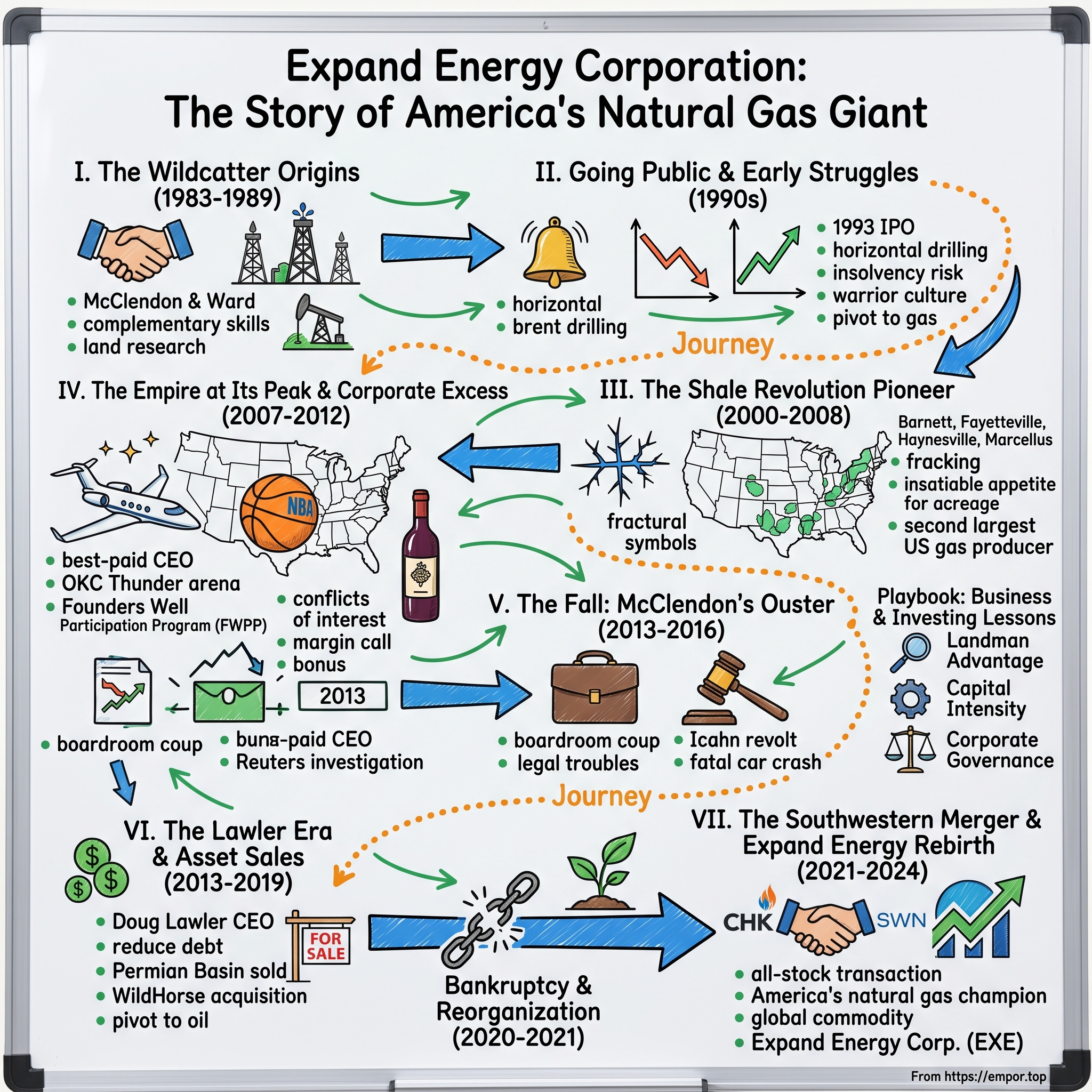

II. The Wildcatter Origins: McClendon & Ward (1983-1989)

The parking lot of a small Oklahoma City diner in 1983 seemed an unlikely birthplace for an energy revolution. Aubrey McClendon and Tom Ward, both 23 and fresh out of college, had been circling each other like prizefighters in the local oil and gas lease market. They kept showing up at the same county courthouses, bidding on the same parcels, driving up each other's costs. Finally, McClendon suggested they meet.

"We were competing against each other, and frankly, neither of us was winning," Ward would later recall. Over coffee, they realized something profound: they had complementary skills. McClendon, a Duke history major with a minor in accounting, possessed an almost supernatural ability to raise capital and paint grand visions. Ward, the son of an Arkansas lumber mill worker, understood operations and had an engineer's mind for efficiency. That day, they decided to "throw in together"—Oklahoma speak for partnership.

McClendon came from oil royalty, though you wouldn't know it from his early struggles. His great-uncle was Robert Kerr, founder of Kerr-McGee and former Oklahoma governor—a titan of the state's energy establishment. But McClendon's path wasn't handed to him. After Duke, he'd returned to Oklahoma as a landman, the unglamorous foot soldiers of the oil business who research mineral rights and negotiate leases. It meant endless hours in dusty courthouse basements, poring over deed records from the 1800s, then driving out to farms to convince skeptical landowners to sign leases.

The work was mind-numbing but educational. McClendon learned to read the land, understand the geology, and most importantly, recognize patterns others missed. He noticed that successful wells often clustered in ways that defied conventional wisdom. While major oil companies focused on proven fields, McClendon saw opportunity in the margins—the unconventional formations that others deemed too difficult or expensive to exploit.

Ward brought different skills. He'd grown up working—really working—in his family's lumber business. He understood machinery, logistics, and the brutal economics of commodity businesses. Where McClendon was vision and charm, Ward was spreadsheets and discipline. Their early partnership involved McClendon securing leases and financing while Ward managed drilling operations.

For six years, they operated as modest wildcatters, drilling conventional vertical wells across Oklahoma. They made money, lost money, and learned the rhythms of the oil patch. By 1989, they'd accumulated enough capital—$50,000 between them—and credibility to think bigger. They needed a corporate structure, a real company.

The naming process revealed their psychology. McClendon wanted something that evoked permanence and geography. He'd fallen in love with Maryland's Chesapeake Bay region during East Coast trips, drawn to its history and sailing culture. Ward preferred something more straightforward, maybe with their names on it. But as McClendon later admitted, "There was some fear that we'd fail, maybe spectacularly, and we thought it would be easier to live with that if our names weren't on the failed enterprise."

Chesapeake Energy Corporation was incorporated in 1989 with a simple strategy: acquire overlooked acreage in Oklahoma, drill vertical wells, and grow steadily. Neither founder imagined they were creating what would become the template for America's shale revolution. They just wanted to survive the next drilling season.

The fear of spectacular failure would prove prescient—though not in the way they imagined. The company they built would indeed fail spectacularly, multiple times, but would also transform American energy independence and make both men billionaires before nearly destroying them. As 1989 turned to 1990, however, they were just two young guys with dirty boots and big dreams, ready to take their company public.

III. Going Public & Early Struggles (1990s)

The bell at the Oklahoma City headquarters of what passed for an investment bank in 1993 didn't ring with quite the fanfare of the New York Stock Exchange. But for McClendon and Ward, taking Chesapeake public at a $25 million valuation felt like conquering Everest. They'd convinced enough investors that two thirty-somethings could find oil and gas where the majors couldn't—or wouldn't look.

The IPO roadshow had been vintage McClendon: part geology lesson, part revival meeting. He'd spread out seismic maps on conference tables from Dallas to Denver, tracing formation lines with his finger while explaining how horizontal drilling—still an exotic technique—could unlock reserves in fields everyone else had written off. "We're not competing with Exxon," he'd tell skeptical fund managers. "We're going where Exxon won't go."

The strategy seemed brilliant. Chesapeake focused on the Golden Trend and the wonderfully named Sholem Alechem fields of South-central Oklahoma. These weren't virgin territories—vertical wells had been pulling oil and gas from them since the 1940s. But McClendon believed horizontal drilling could tap pockets of hydrocarbons that vertical wells missed. Turn the drill bit sideways, extend it through the formation like a straw through a layer cake, and you could access multiple production zones with a single well.

Reality hit hard and fast. The Austin Chalk formation, stretching from Texas through Louisiana, was supposed to be Chesapeake's breakthrough play. Other companies had reported spectacular initial production rates from horizontal wells there. McClendon went all-in, borrowing heavily to lease acreage and drill. The wells came in strong—at first. Then, as if someone had turned off a faucet, production plummeted. The chalk was too tight, too inconsistent. What worked in one spot failed spectacularly a mile away.

By 1997, Chesapeake was effectively insolvent. The company wrote down over $200 million in assets—roughly equal to its entire shareholder equity. The stock, which had peaked around $7, crashed below $1. Board meetings became exercises in triage. Can we make payroll? Which creditors can we stall? Should we just liquidate?

In the conference room where they'd once plotted expansion, McClendon and Ward now strategized survival. They implemented what they called "the warrior culture"—a brutal cost-cutting regime that saw the company shrink from nearly 300 employees to 75. They sold assets at fire-sale prices, renegotiated every contract, and somehow convinced lenders to extend deadlines.

But the real save came from an insight that would define Chesapeake's future: natural gas, not oil, was the play. Gas prices had been depressed through most of the 1990s, making gas wells uneconomical. But McClendon studied demand projections and became convinced prices would rise. More importantly, he recognized that the same horizontal drilling techniques that had failed in the Austin Chalk might work in gas-bearing shale formations—rocks that conventional wisdom said were too dense to produce economically.

The pivot required one more magic trick from McClendon the capital-raiser. Despite Chesapeake's near-death experience, he convinced a group of investors to provide $100 million in fresh financing. His pitch was audacious: forget everything you know about conventional gas drilling. The future is in rocks everyone else considers worthless.

Ward, meanwhile, rebuilt operations from scratch. He instituted fanatical cost discipline, negotiating drilling contracts down to the penny. Every well was analyzed, reanalyzed, and optimized. The company developed proprietary techniques for completing horizontal wells more cheaply. They became students of geology, spending millions on seismic data while competitors relied on outdated surveys.

The transformation showed in the numbers. By 1999, Chesapeake had increased its proved reserves by 300% while reducing finding costs to under $1 per thousand cubic feet—half the industry average. The stock recovered to $5, then $10. The warrior culture had worked, but it had also revealed a fundamental tension between the founders.

McClendon remained the visionary, constantly pushing for bigger acquisitions and bolder bets. Ward had become the operator, focused on efficiency and returns. McClendon would arrive at Monday morning meetings with maps of new plays to pursue; Ward would counter with spreadsheets showing they couldn't afford them. The creative tension drove innovation but also planted seeds of future conflict.

As the 1990s ended, Chesapeake had survived its near-death experience and positioned itself at the forefront of unconventional gas drilling. Natural gas prices were beginning their long-anticipated rise. The company had learned to drill horizontally in challenging formations. Most importantly, McClendon had started studying a geological formation in North Texas called the Barnett Shale—a massive rock formation that conventional wisdom said could never produce commercial quantities of gas.

Conventional wisdom, as Chesapeake was about to prove, was wrong. The stage was set for the shale revolution, and the two wildcatters from Oklahoma were about to become billionaires.

IV. The Shale Revolution Pioneer (2000-2008)

George Mitchell got the credit, but Aubrey McClendon scaled the revolution. In 2000, while Mitchell Energy was still tinkering with hydraulic fracturing in the Barnett Shale, McClendon was already three moves ahead, assembling a land position that would make Chesapeake the undisputed king of unconventional gas.

The eureka moment had come during a 2001 field trip to Mitchell's wells in North Texas. McClendon watched water, sand, and chemicals being pumped at tremendous pressure into the Barnett formation, creating tiny fractures that allowed trapped gas to flow. The wells were producing at rates nobody had thought possible from shale. But McClendon saw what others missed: Mitchell had cracked the code, but hadn't realized the full implications.

"This isn't just about the Barnett," McClendon told his team on the flight back to Oklahoma City. "Every shale formation in America just became a potential gas field. "What followed was the greatest land rush in American energy history. Chesapeake didn't just lease acreage; it hoarded it. McClendon deployed an army of landmen across every shale basin in America. The Barnett in Texas. The Fayetteville in Arkansas. The Haynesville straddling Texas and Louisiana. And most importantly, the Marcellus Formation stretching across Pennsylvania and West Virginia—a geological monster containing more natural gas than Saudi Arabia had oil.

The company's insatiable appetite for shale rock made it one of the biggest leaseholders in the U.S. as commodity prices soared in the years before 2008. The strategy was counterintuitive: pay premium prices for unproven acreage, drill a few wells to prove the concept, then flip portions to major oil companies desperate not to miss the shale revolution. This model netted Chesapeake US$50 billion in asset sales since 2000—a truly staggering figure.

The technological combination of horizontal drilling and hydraulic fracturing—what the industry simply called "fracking"—was transformative. Instead of drilling straight down and hoping to hit a narrow pocket of gas, Chesapeake's wells turned sideways, extending for miles through shale formations. Then came the fracking: millions of gallons of water, sand, and chemicals pumped at extreme pressure, creating a spider web of fractures that released gas trapped for millions of years.

Founded in 1989, it became the world's second-largest natural gas producer in the 2000s, as hydraulic fracturing and horizontal drilling uncovered huge reserves of oil across US states. The numbers were staggering. Wells that would have produced a trickle using conventional methods now gushed gas at rates that defied belief. A single Haynesville well could produce 20 million cubic feet per day—enough to heat 20,000 homes.

The culture at Chesapeake during this period was part Silicon Valley startup, part wildcatter saloon. McClendon installed basketball hoops in the parking garage and held company-wide pep rallies. He recruited top geology graduates with signing bonuses that would make investment banks blush. The company's Oklahoma City campus grew to resemble a university, complete with fitness centers, restaurants, and daycare facilities.

Tom Ward, however, was growing uncomfortable. While McClendon preached the gospel of endless expansion, Ward saw storm clouds. The company was leveraging itself to dangerous levels, borrowing billions to fund land acquisition. Every quarter brought new joint ventures, complex financial structures that allowed Chesapeake to maintain control while offloading costs to partners. Ward worried they were building a house of cards.

The tension exploded in 2006. After 24 years of partnership, Ward abruptly left Chesapeake. The official statement cited "different philosophical approaches." The reality was starker: Ward believed McClendon's grow-at-any-cost strategy would eventually destroy the company. He took his winnings—hundreds of millions in stock—and founded SandRidge Energy, determined to build a more disciplined operator.

McClendon barely paused. With Ward gone, there were no more brakes on the Chesapeake machine. The company announced one massive discovery after another. In 2008, the company announced its discovery of the Haynesville Shale in East Texas and northwestern Louisiana. Each new shale play sent the stock higher.

By summer 2008, Chesapeake's market capitalization exceeded $35 billion. At its peak in 2008, the company was worth more than $35bn. The stock touched $74. McClendon's personal stake was worth over $2 billion, landing him on the Forbes 400. Natural gas prices had spiked above $13 per thousand cubic feet, making even marginal wells wildly profitable.

"Without Chesapeake, there is no shale revolution full-stop," a restructuring adviser would later observe. The statement wasn't hyperbole. Chesapeake had proven that America's shale formations contained enough natural gas to make the country energy independent. The company had fundamentally altered global energy markets.

But McClendon had made a fatal miscalculation. He'd built Chesapeake on the assumption that natural gas prices would remain elevated—above $6 per thousand cubic feet indefinitely. As 2008 drew to a close and the financial crisis erupted, that assumption was about to be violently tested. The empire McClendon built was magnificent, but empires built on leverage and commodity prices have a troubling tendency to collapse.

V. The Empire at Its Peak & Corporate Excess (2007-2012)

The Gulfstream G550 touched down at Teterboro Airport on a humid September morning in 2011. Aubrey McClendon stepped out, immaculate in his custom suit, and into a waiting Mercedes. He had three meetings in Manhattan that day: a breakfast with Carl Icahn, lunch with investment bankers at Goldman Sachs, and an afternoon presentation to pension fund managers. By the time he flew back to Oklahoma City that evening, he'd raised another $1.5 billion.

This was peak McClendon—part CEO, part celebrity, part controversy magnet. At one point the best-paid U.S. CEO with an annual package topping $100 million. Forbes had just named Chesapeake the best-managed oil and gas company in America. The irony of that accolade would become apparent soon enough.

The Oklahoma City headquarters had transformed into McClendon's personal Xanadu. The campus sprawled across 120 acres, featuring Georgian-style brick buildings, pristine lawns, and a 72,000-square-foot fitness center that rivaled professional sports facilities. McClendon had personally overseen every detail, from the antique maps lining executive hallways to the restaurant menus. Employees enjoyed on-site medical care, free meals, and access to a botany center where they could pick fresh vegetables.

But it was McClendon's other investments that raised eyebrows. He'd become Oklahoma City's de facto king, using Chesapeake funds to reshape the city in his image. The company poured millions into restaurants, real estate developments, and most visibly, the NBA's Oklahoma City Thunder. The Chesapeake Energy Arena became the team's home, with McClendon owning a 19.2% stake in the franchise. He sat courtside at games, cementing his image as the energy executive who brought major league sports to Oklahoma. The crown jewel of McClendon's excess was the Founders Well Participation Program (FWPP). Through the Founders Well Participation Program, McClendon was able to purchase a 2.5% interest in every well the company drills. McClendon borrowed as much as $1.1 billion against his 2.5% stake in thousands of company wells from banks that were also lenders to the company. The arrangement was unprecedented in corporate America—a CEO personally investing alongside his company in every single project, using loans from the same banks financing the company itself.

The conflicts of interest were staggering. This created a possible conflict of interest whereby McClendon could act to benefit his personal interests as opposed to those of the company. McClendon could push for wells that benefited his personal portfolio rather than shareholder returns. He negotiated with service providers who worked for both him and Chesapeake. The board, stacked with friends and business partners, rubber-stamped his decisions.

Reuters' explosive April 2012 investigation into the FWPP sent shockwaves through Wall Street. McClendon had received over $1 billion in loans over the last three years, secured by his stake in Chesapeake's oil and gas wells. The loans — some of which came from investment firms that did business with Chesapeake — were not disclosed to the company's shareholders. McClendon reportedly used the loans to finance more personal stakes in the company's wells.

But the FWPP was just one tentacle of McClendon's corporate octopus. He'd hired a company historian at $100,000 per year because he "loved history." The World's Strongest Man was on payroll, also at six figures, to promote employee fitness. Since McClendon was a history major and loved history, he hired a company historian, who was paid a salary of over $100,000 per year. He also hired the World's Strongest Man, who also received a salary of over $100,000 per year, to promote exercise among company staff. The company purchased McClendon's personal map collection for $12.1 million. These weren't rogue transactions—the board approved them all.

The environmental consequences of Chesapeake's drilling frenzy were becoming impossible to ignore. The company faced thousands of lawsuits from landowners claiming underpayment of royalties, water contamination, and earthquake damage. Oklahoma, which had historically experienced one or two earthquakes per year, was suddenly shaking daily. The correlation with injection wells—where Chesapeake pumped fracking wastewater deep underground—was undeniable.

S&P Global Platts named the company Energy Producer of the Year in 2009, even as cracks in the foundation widened. Natural gas prices, which McClendon had bet would stay above $6 forever, crashed below $3. The company's debt load, accumulated during the land grab years, became crushing. Chesapeake was spending $1.50 for every dollar it earned.

The 2008 financial crisis had nearly destroyed McClendon personally. In 2008, at the height of the market panic, McClendon received a margin call from Wall Street that shook his world. He apparently had been buying millions of dollars of Chesapeake stock over the years on margin from various brokers. When Chesapeake's shares unexpectedly dropped, he was left totally exposed. To meet the margin call, McClendon had to sell 94% of his Chesapeake shares, which at one point was estimated to be worth around $3 billion, in a fire sale for around $600 million. Selling such a large chunk of stock into a weak market caused Chesapeake's already distressed shares to fall an additional 40%.

The board's response? Chesapeake awarded McClendon with a $75 million bonus in 2008 for a job well done. They also purchased his wine collection and provided him with a $100 million retention bonus. The corporate governance experts were apoplectic. Institutional investors began agitating for change.

By 2012, the empire McClendon built was magnificent in its scope and troubling in its structure. Chesapeake was simultaneously America's second-largest natural gas producer and a cautionary tale about unchecked CEO power. The reckoning that Tom Ward had predicted six years earlier was about to arrive. The board that had enabled McClendon's excesses would soon turn on him, setting in motion events that would end in tragedy.

VI. The Fall: McClendon's Ouster & Legal Troubles (2013-2016)

The emergency board meeting on April 1, 2013, lasted less than an hour. Aubrey McClendon, who'd built Chesapeake from nothing into a $35 billion empire, walked into the Oklahoma City boardroom as CEO and walked out as a private citizen. No golden parachute, no farewell tour, just a terse press release announcing his resignation "by mutual agreement." The man who'd once commanded a $100 million compensation package left with little more than his personal effects in a cardboard box.

The coup had been brewing since the Reuters revelations about the FWPP a year earlier. Carl Icahn, who'd taken a significant stake in Chesapeake, led the charge. "The board has been derelict in its duties," he'd written in a scathing public letter. Southeastern Asset Management, the company's largest shareholder, joined the revolt. The same directors who'd approved McClendon's excesses suddenly discovered religion about corporate governance.

After this potential conflict was made public, the company terminated the Founders Well Participation Program. The U.S. Securities and Exchange Commission opened an informal inquiry of McClendon's borrowing practices. The board announced it would separate the chairman and CEO roles—a direct rebuke to McClendon's imperial style. By early 2013, even his allies recognized the inevitable. Robert Douglas Lawler, 46, Senior Vice President, International and Deepwater Operations at Anadarko Petroleum, would join Chesapeake as Chief Executive Officer in May 2013. The contrast with McClendon couldn't have been starker. He is a petroleum engineer with 25 years of experience in the upstream Exploration and Production industry who has served in increasingly senior leadership roles at Anadarko, the second-largest independent upstream company in the U.S. with a $45 billion market capitalization. He is a proven oil and gas executive with significant expertise in asset development, operations management and engineering as well as experience in corporate and strategic planning. Where McClendon was flamboyant, Lawler was methodical. Where McClendon spent, Lawler cut.

Yet when Doug Lawler, Chesapeake's president and CEO, joined the company in June 2013, it was a funhouse mirror reflection of its reputation, on the brink of bankruptcy while paying beekeepers and amassing a wine collection. "Despite all your best due diligence, what I found when I got inside the company was much, much worse than I thought," he said at the Houston Producer's Forum luncheon on April 21.

Every day he discovered something that simply blew him away, he said. "Whether it was bee keepers in gardens, wine collections and all kinds of crazy things—we are an E&P company," he said. The corporate excess McClendon had built would take years to unwind.

Meanwhile, McClendon wasn't going quietly. Within weeks of leaving Chesapeake, he launched American Energy Partners, raising billions from private equity to compete directly with his former company. He poached Chesapeake employees, bid on adjacent acreage, and continued preaching the gospel of natural gas. The energy establishment watched nervously—McClendon unbound by public company constraints was potentially even more dangerous.

But federal prosecutors were closing in. The Department of Justice had been investigating potential antitrust violations in Oklahoma land auctions dating back to 2007-2012. Competitors alleged McClendon had orchestrated bid-rigging schemes, dividing territories to avoid competition. The evidence was damning: emails, witness testimony, patterns of suspicious bidding.

On March 1, 2016, McClendon was indicted by a federal grand jury on charges of conspiring "to rig bids for the purchase of oil and natural gas leases in northwest Oklahoma". The indictment alleged he'd masterminded a conspiracy with a competitor to suppress prices, allocating territories between them. Each charge carried up to 10 years in prison.

McClendon released a defiant statement: "The charge that has been filed against me today is wrong and unprecedented. I have been singled out as the only person in the oil and gas industry in over 110 years since the Sherman Act became law to have been accused of this crime." He vowed to fight, assembling a legal dream team.

According to police reports, McClendon died instantly at 9:12 a.m. on March 2, 2016, when his 2013 Chevrolet Tahoe SUV, traveling at 88 miles per hour (142 km/h), crashed into a concrete overpass for the Turner Turnpike on Midwest Boulevard in Oklahoma City in a solo-occupant, single-vehicle crash. The event occurred one day after McClendon's indictment by a federal grand jury accusing him of violating antitrust laws from 2007 to 2012 while the CEO of Chesapeake Energy.

The circumstances raised immediate questions. The crash site showed no skid marks. Police reported McClendon had "plenty of opportunity to correct and get back on the roadway." He wasn't wearing a seatbelt. The bridge abutment he hit was the only obstacle for miles on a straight road. Toxicology reports found traces of medication but nothing that would explain the crash.

The energy world was stunned. Carl Icahn, who'd led the boardroom coup against McClendon, tweeted: "McClendon was one of the brightest men I've ever dealt with. I personally always found him to be a gentleman in our interactions." Even environmental groups that had battled Chesapeake acknowledged McClendon's transformative impact on American energy.

The tragedy left unanswered questions. Was it suicide, as many suspected but police couldn't prove? A moment of distraction at highway speed? An accident by a man under unbearable stress? The only certainty was that one of the most consequential figures in American energy history was gone, his vision for Chesapeake dying with him.

Back in Oklahoma City, Lawler continued dismantling McClendon's empire, selling assets, cutting costs, trying to save a company drowning in debt. The shale revolution McClendon had pioneered continued without him, but Chesapeake—his creation, his obsession—would never be the same. The board that had enabled his excesses and then destroyed him moved on to new battles, but the ghost of Aubrey McClendon haunted every decision.

VII. The Lawler Era & Asset Sales (2013-2019)

Doug Lawler stood before a wall-sized map of Chesapeake's assets in the war room he'd created on the executive floor. Red pins marked properties for sale, yellow for "maybe," green for core holdings. By his count, Chesapeake owned pieces of fields in 15 states—a sprawling, incoherent empire that burned cash faster than it could produce gas. His mandate was simple but brutal: shrink to survive.

Despite all the inherited baggage, the company has solidly increased productivity while lowering spending since Lawler arrived. In 2013, Chesapeake reduced its capex to $6.9 billion, down from $13.4 billion in 2012. But cutting capital spending was just the beginning. Lawler needed to fundamentally restructure a company built for $6 natural gas in a world of $3 gas.

The asset sale marathon began immediately. Properties McClendon had accumulated in his land grab frenzy went on the block. The Permian Basin assets in Texas—once touted as Chesapeake's oil future—sold for $3.3 billion. The Cleveland and Tonkawa plays in Oklahoma fetched $1.9 billion. Each sale was painful, often at prices below what Chesapeake had invested, but necessary to keep creditors at bay. The crown jewel sale came in December 2014. In December 2014, the company sold a large portion of its oil and gas assets in the Marcellus Formation and Utica Shale to Southwestern Energy for net proceeds of $4.975 billion. The transaction included approximately 413,000 net acres and 1,500 wells in northern West Virginia and southern Pennsylvania. Net production of the sold assets was 57,000 barrels of oil equivalent per day in December 2014. The irony wasn't lost on industry observers—Chesapeake was selling the very Marcellus assets that had made it a shale pioneer to a competitor that would later become its merger partner.

The philosophical shift under Lawler was profound. Where McClendon had preached growth at any cost, Lawler instituted "value creation through financial discipline." The company that once employed beekeepers and maintained a wine collection now scrutinized every expense. "Whether it was bee keepers in gardens, wine collections and all kinds of crazy things—we are an E&P company," Lawler told investors, still incredulous at what he'd inherited.

But Lawler made a critical strategic error that would haunt Chesapeake: pivoting to oil just as the market was about to crash. Natural gas, McClendon's obsession, had stayed relatively stable. Oil, which Lawler bet the company's future on, was about to enter a brutal bear market. In February 2019, the company acquired Texas oil producer WildHorse Resource Development for $4 billion in cash and stock. The timing couldn't have been worse.

The WildHorse acquisition was Lawler's attempt to transform Chesapeake from a gas company into an oil company. The $4 billion price tag—paid with precious cash and stock—added prime Eagle Ford acreage and boosted oil production. But it also added debt at exactly the wrong moment. Oil prices, which had been recovering, rolled over. The shale revolution McClendon had started had succeeded too well—America was drowning in oil and gas.

By 2019, Chesapeake's financial statements told a grim story. The company carried over $10 billion in debt against a market capitalization of just $2.4 billion. At the end of the June quarter, Chesapeake Energy Corp.'s principal amount of debt outstanding was $10.16 billion, which is a lot for a company with an equity value of only $2.4 billion. Interest payments alone consumed much of the company's cash flow. Asset sales, which had provided breathing room, were getting harder as buyers recognized Chesapeake's desperation.

Lawler had stabilized the patient but hadn't cured the disease. "Chesapeake is burdened with legacy debt," he said. "We're fighting that challenge every single day. Without having additional cash flow from higher [commodity] prices, it makes it more difficult to offset and improve that debt." The debt McClendon had accumulated during the land grab years remained a millstone around the company's neck.

Employee morale cratered. In September 2015, the company announced layoffs of hundreds of people in Oklahoma City. In January 2018, the company laid off 400 employees. The gleaming campus McClendon had built felt like a mausoleum. The restaurants closed, the fitness center emptied, the Thunder played to crowds that no longer included Chesapeake executives.

As 2019 turned to 2020, Chesapeake's bonds traded at distressed levels, implying imminent default. The company that had once been worth $35 billion was valued at less than the cash on its balance sheet. Lawler had bought time but hadn't changed the fundamental reality: Chesapeake had too much debt for a commodity business in a world of volatile prices.

The COVID-19 pandemic would deliver the final blow, but the company was already mortally wounded. Six years after McClendon's ouster, despite asset sales totaling tens of billions, despite cutting costs to the bone, despite Lawler's disciplined management, Chesapeake remained trapped by the capital structure McClendon had created. The empire was about to fall for the second time.

VIII. Bankruptcy & Restructuring (2020-2021)

The Chesapeake board convened via Zoom on a Sunday morning in June 2020, their faces arranged in a digital grid that would have been unimaginable just months earlier. Outside their home offices, the world had stopped. Oil prices had briefly gone negative—buyers literally paid others to take oil off their hands. Natural gas wasn't much better. The pandemic had crushed energy demand just as Russia and Saudi Arabia flooded the market with supply. For Chesapeake, already teetering on the edge, it was the death blow.

Doug Lawler's prepared remarks were clinical, devoid of emotion. The company had posted an $8.3 billion loss in the first quarter of 2020. Cash was burning fast. The next interest payment was due in August—$192 million the company didn't have. After thirty-one years, countless near-death experiences, and one resurrection, Chesapeake Energy would file for Chapter 11 bankruptcy protection.

Chesapeake Energy, the poster child of the U.S. shale revolution, filed for bankruptcy protection on Sunday. The move comes as the company and industry more broadly has been rocked by a drop in oil and gas prices amid the coronavirus pandemic. The company said that $7 billion in debt will be wiped out through the restructuring.

The filing on June 28, 2020, was both shocking and inevitable. Shocking because this was Chesapeake—the company that had unlocked America's shale resources, that had made natural gas a viable alternative to coal, that had transformed Oklahoma City. Inevitable because the debt load McClendon had accumulated and Lawler had struggled to reduce had finally become unbearable.

But this wasn't a liquidation. Chesapeake had negotiated a prepackaged bankruptcy—Wall Street's version of a controlled demolition. The company had secured $925 million in debtor-in-possession financing to keep operating and agreements for $2.5 billion in exit financing plus $600 million in new equity. The plan would wipe out existing shareholders but preserve the company as a going concern.

The bankruptcy revealed the full extent of Chesapeake's operational bloat. Despite Lawler's cost-cutting, the company still had contracts and commitments dating back to the McClendon era—pipeline agreements, drilling contracts, office leases. The bankruptcy process allowed Chesapeake to reject these "executory contracts," finally freeing it from obligations negotiated when gas was $13 and the future seemed limitless.

Most dramatically, the restructuring would eliminate approximately $7.8 billion of debt. Bondholders would receive equity in the reorganized company—a brutal haircut but better than liquidation. The company's revolving credit facility would be replaced with a new $2.5 billion exit facility. For the first time since the early 2000s, Chesapeake would have a balance sheet sized appropriately for its assets. The strategic reset was dramatic. Chesapeake Energy Corporation announced today that it has successfully concluded its restructuring process and emerged from Chapter 11, satisfying all conditions precedent under its Plan of Reorganization on February 9, 2021. As of February 9, 2021, Chesapeake's principal amount of debt outstanding was approximately $1,271 million, compared to $9,095 million as of June 30, 2020. "We have fundamentally reset our business, and with an improved capital and cost structure, disciplined approach to capital reinvestment, diverse asset base and talented employees, we are poised to deliver sustainable free cash flow for years to come," said Chesapeake president and chief executive Doug Lawler.

But the human cost was severe. U.S. shale oil and gas producer Chesapeake Energy Corp plans to cut 15% of its workforce, an email sent to employees revealed. Most of the 220 layoffs will happen at the Oklahoma City headquarters. Employees who'd survived multiple rounds of cuts found out via email whether they still had jobs. The campus McClendon built, once buzzing with thousands of workers, felt ghostly.

The new board was populated with restructuring specialists and industry veterans, not McClendon cronies. Michael Wichterich, chief executive of private oil explorer Three Rivers Operating Company, became chairman. The mandate was clear: no more empire building, no more debt-fueled expansion, just disciplined operations and cash generation.

The company also made ESG commitments that would have been unthinkable in the McClendon era. Chesapeake committed to achieving net-zero GHG direct emissions by 2035, eliminating routine flaring on all wells. The fracking pioneer was trying to rebrand as an environmental steward—a necessary evolution in a world increasingly concerned about climate change.

Most significantly, the bankruptcy had forced a strategic refocus. The permanent elimination of over $1 billion in annual cash costs from 2019 levels with opportunities for additional reductions. The company would concentrate on its best assets: the Marcellus shale in Pennsylvania, the Haynesville shale in Louisiana, and selected oil properties. The scattershot approach of the McClendon years was dead.

Lawler's comments after emergence were telling: "As we look ahead, maintaining the strength of our balance sheet, our cost leadership position, and our steadfast commitment to delivering consistent returns, while lowering our emissions profile will be paramount to our success." No mention of transforming America's energy landscape or building empires—just returns and discipline.

The bankruptcy had achieved what years of management changes couldn't: finally right-sizing Chesapeake for the reality of commodity markets. The company that emerged was leaner, focused, and financially viable. But it was also diminished—no longer the swashbuckling pioneer that had unlocked America's shale resources but just another disciplined operator in a maturing industry.

As Chesapeake's new shares began trading on NASDAQ under the familiar CHK ticker, opening at $43, the market rendered its verdict. The company was worth something, but not what it once was. The bankruptcy had saved Chesapeake from extinction but at the cost of its identity. The question now was whether this disciplined, restructured company could thrive in a world where natural gas was abundant and cheap—ironically, the very world Chesapeake had helped create.

IX. The Southwestern Merger & Expand Energy Rebirth (2021-2024)

Nick Dell'Osso had watched Chesapeake's rise and fall from the inside. He'd joined in 2008 as an energy investment banker, witnessed McClendon's excesses, survived Lawler's cuts, and navigated the bankruptcy. When the board named him CEO in October 2021, replacing Lawler who'd departed for Continental Resources, Dell'Osso understood both Chesapeake's potential and its limitations. The company needed more than restructuring—it needed transformation.

The post-bankruptcy honeymoon was brief. Natural gas prices spiked in 2021-2022, driven by the Ukraine war and European energy crisis, giving Chesapeake breathing room. But Dell'Osso recognized a fundamental problem: even lean and disciplined, Chesapeake lacked the scale to compete in a consolidating industry. The company that had once dominated through aggressive expansion now found itself subscale in its own pioneering basins. The solution emerged in January 2024. Chesapeake Energy Corporation (NASDAQ: CHK) and Southwestern Energy Company (NYSE: SWN) today announced that they have entered into an agreement to merge in an all-stock transaction valued at $7.4 billion, or $6.69 per share, based on Chesapeake's closing price on January 10, 2024. The deal was transformative in its simplicity: combining two pioneers of the shale revolution who'd taken different paths but ended up in the same place.

Southwestern's story paralleled Chesapeake's in many ways. Founded in 1929, it had reinvented itself as a shale player in the 2000s, cracking the code in Arkansas's Fayetteville Shale. Where Chesapeake had been flamboyant, Southwestern was methodical. Where Chesapeake overspent, Southwestern stayed disciplined. But both companies faced the same fundamental challenge: natural gas prices that stubbornly refused to rise despite growing demand.

Under the terms of the agreement, Southwestern shareholders will receive a fixed exchange ratio of 0.0867 shares of Chesapeake common stock for each share of Southwestern common stock owned at closing. Pro forma for the transaction, Chesapeake shareholders will own approximately 60% and Southwestern shareholders will own approximately 40% of the combined company, on a fully diluted basis. The math was compelling: the combined entity would produce 7.9 billion cubic feet per day, making it America's undisputed natural gas champion.

But Dell'Osso had a bigger vision than just scale. In 2023, in three transactions, the company sold all of its assets in the Eagle Ford shale to Ineos, WildFire Energy (a subsidiary of Warburg Pincus and Kayne Anderson), and SilverBow Resources for a total of $3.5 billion. The divestiture of oil assets—the very properties Lawler had acquired to diversify—signaled a return to Chesapeake's roots: natural gas, pure and simple.

The regulatory scrutiny was intense. The Federal Trade Commission, increasingly skeptical of energy consolidation, demanded extensive documentation. Environmental groups opposed the merger, citing both companies' fracking histories. But Dell'Osso navigated the challenges methodically, agreeing to environmental commitments and market share limitations that satisfied regulators without crippling the combined entity.

The rebranding announcement came in September 2024, just days before the merger closed. The new name—Expand Energy—was both aspirational and strategic. "As America's largest natural gas producer and a top producer globally, Expand Energy is built to disrupt the industry's traditional cost and market delivery model," said Nick Dell'Osso, Expand Energy's President and Chief Executive Officer. No more Chesapeake Bay nostalgia, no more McClendon legacy. This was a new company for a new era.

The irony wasn't lost on industry veterans. The company McClendon founded to unlock America's natural gas had sold those very Marcellus assets to Southwestern in 2014 for $5 billion. Now, a decade later, Chesapeake was buying them back, along with the rest of Southwestern, for $7.4 billion. The assets had come full circle, but the industry had fundamentally changed.

Chesapeake Energy Corporation and Southwestern Energy Company have officially completed their merger, forming a newly rebranded entity, Expand Energy Corp. on October 1, 2024. The combined company's portfolio was formidable: dominant positions in the Marcellus and Haynesville, the two most economic gas basins in America. Production of 7 Bcf/d, roughly 7% of total U.S. output. A cleaned-up balance sheet with manageable debt. Most importantly, the scale to compete globally as American LNG exports reshaped world energy markets.

Dell'Osso's vision extended beyond domestic markets. "The world needs more energy, and our team is committed to sustainably delivering it to consumers," he stated at closing. With Europe desperate for alternatives to Russian gas and Asia's insatiable energy demand, American natural gas—once trapped in oversupplied domestic markets—had become a strategic global commodity.

The cultural integration would be challenging. Chesapeake employees, scarred by years of upheaval, met their Southwestern counterparts warily. The combined workforce would need rightsizing. The headquarters would remain in Oklahoma City, but the swagger of the McClendon era was gone forever. In its place: operational excellence, capital discipline, and sustainable returns.

As October 2024 arrived and the Expand Energy ticker began trading on NASDAQ, the transformation was complete. From wildcatters with $50,000 to bankruptcy to America's natural gas champion—the journey had been brutal, transformative, and ultimately redemptive. The question now wasn't whether Expand Energy could survive, but whether it could thrive in the world it had helped create: abundant, cheap natural gas that had transformed global energy markets forever.

X. Playbook: Business & Investing Lessons

The Chesapeake saga reads like a Harvard Business School case study written by Shakespeare—ambition, betrayal, redemption, and enough financial engineering to make your head spin. But strip away the drama and you're left with timeless lessons about commodity businesses, capital allocation, and corporate governance that every investor should internalize.

The Landman Advantage: First-Mover Economics in Resource Plays

McClendon understood something fundamental that Wall Street missed: in resource extraction, the money is made when you buy the acreage, not when you drill the well. Chesapeake's model netted US$50 billion in asset sales since 2000—a truly staggering figure. The company would lease land at $150 per acre, prove the concept with a few wells, then flip portions to desperate majors at $5,000 per acre. It's the same playbook tech companies use today—grab market share first, monetize later—but applied to rocks two miles underground.

The key insight: information asymmetry is everything. Chesapeake invested millions in proprietary seismic data while competitors relied on outdated government surveys. They hired geology PhDs when others hired roughnecks. They studied title records in courthouse basements to understand mineral rights that had been severed decades earlier. This obsessive focus on information gathering created a sustainable competitive advantage—until everyone copied it.

Capital Intensity and the Funding Treadmill

Here's the dirty secret of unconventional drilling: shale wells are manufacturing operations, not treasure hunts. Unlike conventional wells that might produce for decades, shale wells decline by 70% in their first year. You're not drilling for oil; you're running on a treadmill that gets faster every year. Miss a quarter of drilling and production collapses. It's a capital-intensity trap that destroyed dozens of companies who thought they were in the oil business when they were actually in the capital-raising business.

Chesapeake's mistake wasn't recognizing this reality—it was believing they could outrun it through scale. McClendon thought if he drilled enough wells fast enough, the declining production from old wells would be offset by new drilling. But that required ever-increasing capital, which required ever-increasing debt, which required ever-increasing commodity prices. When any variable in that equation failed, the whole structure collapsed.

Corporate Governance: The $7 Billion Lesson

The Founders Well Participation Program wasn't just a corporate governance failure—it was a masterclass in how perverse incentives destroy companies. McClendon could profit personally from wells that lost money for shareholders. He negotiated with banks that lent to both him and Chesapeake. He bought assets from entities he partially owned. The conflicts of interest weren't hidden; they were disclosed in footnotes nobody read until it was too late.

The lesson isn't just "have independent directors"—it's that governance failures compound geometrically. Bad governance leads to bad capital allocation, which leads to desperate financing, which leads to more governance compromises. By the time shareholders revolt, the damage is irreversible. The board that enabled McClendon's excesses and then fired him ultimately presided over a $7 billion bankruptcy. Sometimes the cure is worse than the disease.

Commodity Cycles and Leverage: The Deadly Combination

Every commodity executive claims to understand cycles, but behavior suggests otherwise. At $13 gas, Chesapeake levered up to buy more acreage. At $3 gas, they couldn't sell assets fast enough to survive. The company consistently planned for the current price environment to persist forever—a psychological bias that destroyed capital across the industry.

The math is brutal: a 50% drop in commodity prices doesn't mean 50% less profit—it often means no profit at all. When your breakeven is $6 gas and spot prices are $3, every molecule you produce loses money. But you can't stop producing because you need cash flow to service debt. So you drill more wells to increase production, which increases supply, which lowers prices further. It's a death spiral that only bankruptcy can break.

The Bankruptcy Reorganization Playbook

Chesapeake's bankruptcy was a $7.8 billion wealth transfer from equity to debt holders, but it also demonstrated how Chapter 11 can save viable businesses from impossible capital structures. The key was speed—a prepackaged bankruptcy with financing lined up, operations continuing uninterrupted, and emergence in just eight months. Compare that to traditional liquidation where assets get sold piecemeal and value evaporates.

The restructuring eliminated approximately $7.8 billion of debt. As of February 9, 2021, Chesapeake's principal amount of debt outstanding was approximately $1,271 million, compared to $9,095 million as of June 30, 2020. The lesson: in commodity businesses with volatile cash flows, the capital structure matters more than the assets. Great rocks two miles underground are worthless if you can't afford to drill them.

Industry Consolidation as Value Creation

The Southwestern merger demonstrated a profound truth: in mature industries with oversupply, consolidation is the only path to value creation. Two subscale players struggling with overhead and lacking negotiating power with service providers became one scaled operator with lower unit costs and pricing power. The synergies weren't theoretical—they showed up immediately in operating metrics.

But timing matters. Chesapeake tried to buy its way to scale during the boom and overpaid massively. The Southwestern deal happened when both companies were beaten down, making the relative valuation fair. In commodity industries, the best deals happen when nobody wants to deal.

Environmental and Social License to Operate

McClendon dismissed environmental concerns as liberal hand-wringing. That arrogance cost Chesapeake billions in lawsuits, regulatory delays, and reputational damage. Expand Energy's commitment to net-zero emissions by 2035 isn't just greenwashing—it's recognition that social license to operate has become a hard asset that needs investment and maintenance.

The lesson extends beyond energy. Every business today faces stakeholders who care about more than profits. Ignore them at your peril. The companies that survive the next decade will be those that recognize externalities eventually become internalities—pollution becomes lawsuits, community opposition becomes permitting delays, regulatory hostility becomes stranded assets.

The Ultimate Lesson: Missionary vs. Mercenary

McClendon was a missionary who believed natural gas would transform America. That conviction let him see opportunities others missed but also blinded him to risks. Lawler was a mercenary focused on returns. He saved the company but lacked vision. Dell'Osso might be the synthesis—someone who understands both the mission (energy abundance) and the constraints (capital discipline).

The best businesses are built by missionaries but run by mercenaries. Vision gets you started; discipline keeps you alive. Chesapeake had 20 years of vision without discipline, then 8 years of discipline without vision. Expand Energy's challenge is maintaining both. History suggests that's harder than drilling two miles underground and turning right.

XI. Analysis & Bear vs. Bull Case

Expand Energy trades at a fraction of its enterprise value from the McClendon era, but is it cheap or a value trap? The answer depends on your view of natural gas markets, capital allocation, and whether leopards—or energy companies—can change their spots.

The Competitive Position: Last Man Standing

Expand Energy Corporation (NASDAQ: EXE) is the largest independent natural gas producer in the United States, powered by dedicated and innovative employees focused on disrupting the industry's traditional cost and delivery model. But "largest" in a fragmented industry still means just 7% market share. The company produces 7 Bcf/d out of total U.S. production of roughly 100 Bcf/d. That's scale, but not dominance.

The asset quality is undeniable. The Marcellus Formation in Pennsylvania and West Virginia contains some of the lowest-cost gas resources globally—breakeven prices under $2.50 per thousand cubic feet. The Haynesville Shale in Louisiana, while more expensive to develop, sits next to the Gulf Coast's massive LNG export infrastructure. These aren't marginal assets that only work at high prices; they're Tier 1 resources that generate returns even in oversupplied markets.

But competitive advantages in commodity extraction are ephemeral. Expand doesn't have proprietary technology—everyone uses the same horizontal drilling and fracking techniques Chesapeake pioneered. They don't have exclusive access to resources—mineral rights trade in competitive markets. What they have is scale, operational excellence, and a clean balance sheet. In commodity businesses, sometimes that's enough.

Natural Gas Demand: The LNG Escape Valve

The bear case for natural gas has been wrong for a decade but right on price. Production keeps growing, efficiency keeps improving, and prices stay stubbornly low. The Marcellus alone could supply the entire Eastern seaboard for decades. Add the Permian's associated gas (produced as a byproduct of oil drilling) and America is drowning in methane.

But the demand picture is transforming. U.S. LNG exports, basically zero in 2015, now exceed 14 Bcf/d and are heading to 25 Bcf/d by 2030. That's equivalent to creating a new South Korea worth of demand every few years. Europe, desperately weaning itself off Russian gas, will pay premium prices for American molecules for decades. Asia's insatiable energy growth requires cleaner fuels than coal. Natural gas is the transition fuel that makes the energy transition possible.

The domestic story is equally compelling. Data centers powering AI require reliable, 24/7 electricity that renewables can't provide. Natural gas plants are getting built at the fastest pace in years. Coal retirements accelerate. Even with renewable growth, gas demand for power generation keeps climbing. The electrification of everything requires electricity from something, and increasingly, that something is natural gas.

Financial Metrics: The Discipline Test

Post-bankruptcy Expand is a different animal. Debt of $1.3 billion against EBITDA of roughly $3 billion yields leverage under 0.5x—investment grade territory. The company generates free cash flow at $2.50 gas, a price that would have meant bankruptcy in the McClendon era. Capital spending at 60-70% of operating cash flow leaves room for dividends and buybacks while maintaining production.

But the history haunts. This is a company that went from IPO to $35 billion to bankruptcy twice (almost). Management talks about discipline, but commodity price spikes test discipline in ways bear markets don't. When gas hits $6 again—and it will—will Expand resist the siren song of growth? Will they return cash to shareholders or convince themselves that this time is different?

ESG Considerations: Feature or Bug?

Expand's commitment to net-zero direct emissions by 2035 is either brilliant positioning or expensive virtue signaling. The optimistic view: natural gas is the essential transition fuel, and the cleanest producer wins. LNG buyers increasingly demand carbon scores. Methane leaks destroy the climate math that makes gas better than coal. Expand's environmental commitments ensure long-term market access.

The skeptical view: these commitments are costs with no corresponding revenue. Monitoring equipment, leak detection, and emission reduction technologies cost millions with no impact on the commodity price. Worse, they could become regulatory floors rather than ceilings, with governments mandating ever-stricter standards that advantage renewables over gas.

The Bear Case: Structural DeclineThe pessimistic case starts with price. The EIA forecast shows inflation-adjusted natural gas prices drop to $12.75 per Mcf in 2024 and $12.00 per Mcf in 2025, a decline of 17% and 22%, respectively, from 2023 prices. The Henry Hub price in this STEO averages around $3.60/MMBtu in 2H25 and $4.30 in 2026, which is 21% and 6% lower than we forecast in April, respectively. Even with growing LNG exports and data center demand, supply keeps overwhelming demand.

The technology curve is relentless. Every year, drillers extract more gas from each well for less money. Drilling times fall, completion techniques improve, artificial intelligence optimizes production. The breakeven price for Marcellus gas has fallen from $4 to under $2 in a decade. There's no reason to think this stops. Expand might be the lowest-cost producer, but in commodity markets, the lowest-cost producer of an oversupplied commodity still struggles.

Renewables plus batteries increasingly compete with gas peakers. Hydrogen hype might be overblown, but industrial users are exploring alternatives. Carbon prices, currently nonexistent in America, could devastate gas economics. Even a modest $50/ton carbon price would double the effective cost of gas-fired electricity. Europe's experience shows gas can be displaced faster than expected when economics shift.

The balance sheet is clean now, but commodity companies always relever in good times. Management incentives push growth. Shareholder memories are short. The next $6 gas spike will bring calls to "capitalize on the opportunity." History suggests discipline fails precisely when it's needed most.

The Bull Case: Energy Realism

The optimistic case starts with physics: renewable intermittency is unsolvable without massive storage, and massive storage is decades away. Every data center, every EV charging station, every electrified industrial process needs baseload power. Wind doesn't blow on demand. Solar doesn't shine at night. Batteries for grid-scale, season-long storage don't exist at any price. Natural gas is the only scalable solution. The LNG buildout is staggering. Between 2025 and 2030, a total of almost 295 bcm/yr of new LNG export capacity is expected to come online from projects that have already reached FID and/or are under construction. This represents the largest capacity wave in any comparable period in the history of LNG markets. Five LNG export projects are currently under construction with a combined export capacity of 9.7 Bcf/d—Plaquemines (Phase I and Phase II), Corpus Christi Stage III, Golden Pass, Rio Grande (Phase I), and Port Arthur (Phase I). That's massive new demand that only American gas can fill.

The AI revolution changes everything. Every ChatGPT query, every autonomous vehicle calculation, every machine learning model requires data centers that consume electricity 24/7/365. These facilities can't run on solar panels and good intentions. They need reliable, dispatchable power, and natural gas is the only solution that scales. The hyperscalers—Amazon, Microsoft, Google—are building data centers at unprecedented rates. Each one is a permanent new source of gas demand.

Expand's asset positioning is nearly perfect for this world. The Marcellus sits next to the Northeast's data center corridor and LNG export terminals. The Haynesville feeds directly into Gulf Coast LNG infrastructure. These aren't stranded assets in North Dakota; they're connected to the highest-value markets globally. Geography is destiny in commodity markets, and Expand owns the right geography.

The capital discipline appears real this time. Management compensation is tied to returns, not production growth. The board includes restructuring specialists who remember bankruptcy. The company is returning cash to shareholders even at $3 gas. The culture has fundamentally shifted from empire-building to value creation. Will it hold at $6 gas? Maybe not perfectly, but the scars from bankruptcy run deep.

The geopolitical reality is that natural gas has become a strategic weapon. Europe learned that depending on Russia for energy was existential folly. China knows depending on Middle Eastern oil passing through the Strait of Malacca is a strategic vulnerability. American LNG offers energy security to allies and leverage over adversaries. This isn't just commodity trading; it's geopolitics, and America's gas resources are a strategic asset that will be monetized.

The Verdict: Cautious Optimism

Expand Energy is neither the transformational investment McClendon promised nor the value trap bears fear. It's a cyclical commodity business with genuine competitive advantages in a structurally growing market. The company will never command tech multiples or generate software margins. But at current valuations, with natural gas trading below marginal cost and LNG demand set to explode, the risk-reward appears favorable.

The key is position sizing and patience. This isn't a core holding for widows and orphans. It's a tactical bet on mean reversion in commodity markets, consolidation in fragmented industries, and the reality that the world needs more energy, not less. Expand owns the resources, has the balance sheet to survive downturns, and finally has management that understands capital allocation.

The ghosts of Chesapeake's past will always haunt Expand Energy. McClendon's vision, ambition, and ultimate destruction left scars that define the company's DNA. But sometimes the best investments come from the ashes of previous failures. The company that emerges from bankruptcy, chastened and disciplined, often creates more value than the high-flying predecessor ever could. Expand Energy might just be that company—if it can resist the siren song of empire building when commodity prices inevitably spike again.

XII. Epilogue & "If We Were CEOs"

The circle is complete. From two wildcatters with $50,000 and a handshake deal in an Oklahoma City parking lot to America's largest natural gas producer with a $24 billion enterprise value. The Chesapeake story—now the Expand Energy story—embodies everything glorious and terrible about American capitalism: the audacity to drill sideways two miles underground, the hubris to leverage that innovation into unsustainable debt, the resilience to emerge from bankruptcy stronger.

Aubrey McClendon's ghost haunts every decision. Would he recognize the company he built? The disciplined capital allocation, the ESG commitments, the focus on returns over growth—it's everything he wasn't. Yet the core insight remains his: America sits atop centuries of natural gas, and technology can unlock it. McClendon saw the future but couldn't navigate the present. His successors navigate the present but struggle to articulate a future beyond "disciplined operations."

If We Were CEOs: The Path Forward

Standing in Dell'Osso's shoes, the strategic priorities would be clear but the execution treacherous.

First, resist the growth trap. When gas hits $5—and it will—Wall Street will demand production growth. Activists will push for acquisitions. The board will get restless. The answer must be no. Return cash to shareholders through variable dividends tied to commodity prices. Let investors decide whether to reinvest in energy or diversify. The company's job is to generate cash, not empire-build.

Second, become the consolidator, not the consolidated. The North American gas industry remains fragmented with dozens of subscale producers burning cash. Expand should be the buyer of last resort, acquiring distressed assets at bankruptcy prices. But only assets that immediately lower unit costs or improve market access. No "strategic" acquisitions that require PowerPoint gymnastics to justify.

Third, vertical integration—but smart vertical integration. Don't buy LNG export capacity (too capital intensive) or power plants (wrong business). Instead, secure long-term contracts with LNG exporters and data center developers. Lock in demand at prices that ensure profitability through the cycle. Let others take the commodity price risk while Expand takes the volume risk it understands.

Fourth, technology leadership. The next breakthrough in extraction technology will create another wave of value creation. Expand should be spending 2-3% of revenue on R&D—AI-optimized drilling, methane detection, water recycling. The company that reduces breakeven costs from $2.50 to $1.50 gas wins the next decade. This isn't sexy, but compound improvements in extraction efficiency create lasting competitive advantages.

Fifth, international optionality without international operations. As American LNG reshapes global markets, opportunities will emerge to partner with importers, particularly in Asia. Joint ventures for dedicated supply, equity stakes in receiving terminals, technical services agreements—ways to capture value from globalization without the operational complexity of foreign assets.

Finally, prepare for the energy transition—realistically. Natural gas isn't forever, but it's the next 30 years. Position Expand as the essential transition fuel company. Partner with renewable developers for gas peaking plants. Invest in carbon capture at the wellhead. Explore hydrogen production from natural gas. These might not generate returns today, but they ensure political and social license to operate tomorrow.

The Fundamental Tension

The challenge facing Expand Energy is existential: How do you create lasting value in a commodity business? The answer isn't to pretend you're not in a commodity business (McClendon's mistake) or to simply cut costs and pray for higher prices (Lawler's limitation). It's to accept the commodity reality while building competitive advantages around it.

Those advantages are scale, operational excellence, capital discipline, and strategic positioning. Expand has achieved the first two and is demonstrating the third. The fourth—strategic positioning for a world where natural gas is both essential and transitional—remains a work in progress.

Final Reflections

The Chesapeake/Expand Energy saga is fundamentally American. Only in America would two kids from Oklahoma bet everything on drilling sideways through rocks older than dinosaurs. Only in America would banks lend them billions based on PowerPoint presentations and charisma. Only in America would the company go bankrupt with some of the world's best energy assets. And only in America would it emerge from bankruptcy to dominate the industry it helped create.

McClendon was right about the big thing: natural gas would transform America's energy landscape. He was wrong about everything else: the permanence of high prices, the sustainability of debt-fueled growth, the acceptability of conflicts of interest. His tragedy was seeing the future but being unable to wait for it.

Expand Energy now has the opposite challenge. It can wait—the balance sheet ensures that. But can it seize the future when it arrives? When the next technology breakthrough emerges, when the next basin opens up, when the next opportunity for transformation appears, will Expand have the courage to act? Or will the scars of Chesapeake's collapse create a paralysis that lets smaller, hungrier competitors steal the next revolution?

The answer will determine whether Expand Energy becomes a lasting institution—the Exxon of natural gas—or just another chapter in the boom-bust history of American energy. The resources are there, the market is growing, the balance sheet is clean. All that's missing is the vision to match the opportunity. McClendon had too much vision and not enough discipline. His successors have plenty of discipline. Time will tell if they have enough vision to build something that lasts.

The story of Chesapeake Energy is complete. The story of Expand Energy has just begun.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube