Service Corporation International: The Roll-Up That Conquered Death

I. Introduction: When Death Became a Business Model

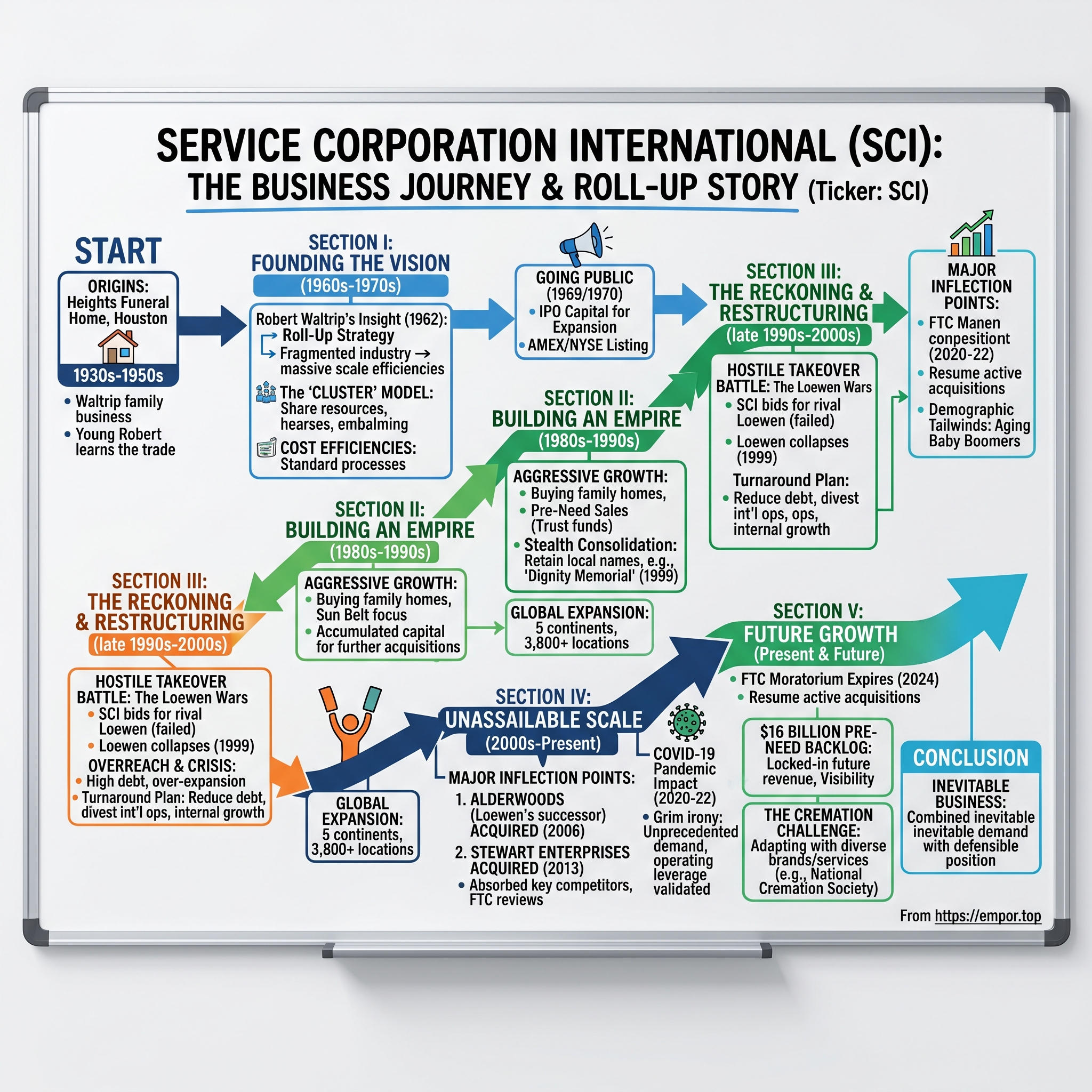

In the quiet suburbs of Houston, Texas, there stands a nondescript corporate tower on Allen Parkway—just a few miles from a modest funeral home on Heights Boulevard where, in the early 1950s, a young man named Robert L. Waltrip learned that death, handled properly, could be a very good business indeed.

Service Corporation International is the largest provider of deathcare products and services in North America. In 2024, the company made a revenue of $4.18 billion USD. Today, SCI serves more than 600,000 families annually through an empire that spans more than 1,900 funeral home, cemetery and crematory locations across North America.

But raw numbers only tell part of the story. What makes SCI remarkable isn't just its size—it's how it got there. This is the tale of perhaps the most successful roll-up in American business history, executed not in a glamorous industry like technology or media, but in the most inevitable sector of all: death.

The central question that makes SCI's story instructive for investors: How did a single Houston funeral home become the largest death care company in the world—and what does that teach us about roll-up strategies, local brand economics, and the peculiar advantages of operating in an industry with guaranteed demand?

The themes we'll explore are universal to great businesses: the power of consolidation in fragmented industries, the financial alchemy of pre-need sales (essentially collecting revenue years before delivering services), the counterintuitive genius of keeping local names while achieving corporate scale, and the discipline required to survive your own overreach and emerge stronger.

One more thing worth noting before we begin: SCI operates in an industry that will never disappear. The crude mortality rate in America runs at roughly 2.8 to 3 million deaths per year, and demographic projections suggest that number will steadily climb as the Baby Boomer generation ages. The 65-and-older population is projected to nearly double during the next three decades—ballooning from 56 million to 94 million by 2060. Unlike nearly every other business you can invest in, SCI's addressable market grows with mathematical certainty.

But guaranteed demand doesn't guarantee success. The funeral industry is riddled with failed consolidators, regulatory landmines, and companies destroyed by their own ambition. SCI survived them all. Understanding how requires going back to a funeral parlor in Houston Heights, where a young football player decided to become an undertaker.

II. Origins & Founding Story (1931–1962): The Making of an Industry Iconoclast

The story of Robert L. Waltrip reads like an American original—part hardscrabble determination, part visionary audacity, and entirely self-made. Born on January 10, 1931, Mr. Waltrip grew up in the family's funeral business. His father owned Heights Funeral Home in Houston, TX, and Mr. Waltrip often rode along in the lead car during funeral processions.

Picture this: a boy growing up literally above a funeral parlor, watching his father and grandmother manage the solemn rituals of death while Houston boomed around them in the oil-drunk 1930s and '40s. When teachers at Reagan High School asked young Robert what he wanted to be when he grew up, the answer—funeral director—drew puzzled looks from classmates dreaming of wildcatting or ranching. "It was strange at school when the teacher would ask you, 'What do you want to be?'" he later remembered.

Mr. Waltrip graduated from Reagan High School in 1949, where he played on the school's football team. He enrolled at Rice University, the elite Houston institution known for its demanding curriculum and technical rigor. But fate intervened with brutal efficiency in 1951.

While he was a student at Rice University, his father died suddenly, and Waltrip had to leave school so he could help manage the business. Robert E. Waltrip was just 48 years old when he died, leaving his 20-year-old son to assume management of Heights Funeral Home alongside his mother. It was a crucible moment—the kind that either breaks a young person or forges them into something stronger.

Young Robert ran the funeral home while completing his degree at the University of Houston. He then attended Rice University and the University of Houston, receiving a bachelor's degree in business administration in 1953. Note the business degree, not mortuary science. From the beginning, Waltrip saw funeral service through the lens of an entrepreneur, not merely a practitioner.

By the late 1950s, something began crystallizing in Waltrip's mind. By 1957 he had come to see the profit potential of buying more funeral homes, and the family acquired two more in Houston. But this wasn't the insight that would change the industry—lots of successful funeral directors owned multiple locations. Waltrip's vision was fundamentally different.

He looked at the funeral industry and saw what Ray Kroc saw in hamburger stands: a fragmented universe of mom-and-pop operators, each running essentially the same business with the same economics, but none achieving the scale efficiencies that could come from consolidation. Just as Ray Kroc, the founder of McDonald's, brought efficiencies of scale to fast food, Robert Waltrip did the same for funeral homes.

By 1962, Waltrip had purchased a funeral operation on Hyde Park Boulevard and built a new building, Waltrip Funeral Home in Spring Branch. It was then that he incorporated as SCI, with the goal of a funerary manifest destiny.

The founding insight was deceptively simple but revolutionary in execution: why should every funeral home maintain its own fleet of hearses, its own preparation facilities, its own accounting staff? Part of his formula for success was the purchase of additional funeral homes starting in the 1960s and the "cluster" concept whereby many facilities pool their resources for cost-efficiency.

He began buying additional funeral homes in the 1960s and achieved significant cost efficiencies through the "cluster" strategy of sharing pooled resources among numerous locations. The cluster model worked like this: Instead of each funeral home in a metropolitan area maintaining its own hearse garage, embalming facility, and back-office functions, SCI would centralize these services for all locations in a geographic cluster. The clusters shared embalming operations and personnel. This eliminated much of the down time in the business, where people had to be kept on the payroll but might have nothing to do between funerals. Under the cluster arrangement, employees worked for whatever SCI funeral home in the area needed them, bringing an efficiency that traditionally family-run businesses could not imitate.

This was operations excellence applied to an industry that had never seen it—McDonald's economics brought to memorial services. A central preparation facility could serve multiple funeral homes. A shared fleet reduced per-unit hearse costs. Centralized purchasing created buying power with casket manufacturers. Standardized processes improved quality while lowering costs.

What made Waltrip different from other ambitious funeral directors wasn't just the idea—others had considered consolidation—it was his willingness to execute at scale and his understanding that the model required capital markets access to achieve its potential.

Mr. Waltrip envisioned a business with streamlined operations and reduced overhead, increasing the quality of service to families. After the plan proved effective in Houston in the early 1960s, Mr. Waltrip and a small group of associates set out to apply this strategy through acquisitions in other markets.

The founder had arrived at a crucial understanding: to consolidate an industry with over 20,000 funeral homes nationwide, you needed more than retained earnings from a few Houston locations. You needed Wall Street.

III. The Roll-Up Playbook: Building an Empire (1962–1990s)

A. Early Expansion & Going Public

The 1960s saw SCI methodically proving its cluster concept across Houston, but the inflection point came in 1969 when he took Service Corporation International public in 1969 and has provided leadership to it for over 40 years. The company began selling shares to the public in 1970, debuting on the American Stock Exchange.

The IPO provided more than just capital—it gave SCI a currency for acquisitions and established credibility with acquisition targets. Family funeral home owners who might have balked at selling to another local competitor were more receptive to partnering with a publicly traded company that could offer liquidity, professional management, and a clear succession path for their life's work.

SCI's operating income rose almost 40 percent to $2.3 million, or 68 cents a share, in 1971. The growth spurt was principally caused by the acquisition of Kinney Services' 28 funeral homes and related businesses in New York City and Miami. This deal demonstrated something crucial: the cluster model could work in entirely different markets from Houston. This gave SCI the ability to service about 15 percent of New York's funeral needs.

Five years later he founded SCI, and by 1974 he owned three hundred funeral homes and the company's stock was trading on the New York Stock Exchange.

During the 1980s, SCI entered the Florida market with characteristic aggression, recognizing that retirement demographics made it the highest-growth death care market in America. The Sun Belt strategy demonstrated SCI's sophistication in targeting markets where both current demand and demographic trends favored funeral service growth.

B. The Pre-Need Innovation

While the cluster model drove operational efficiency, SCI's financial innovation came through mastering pre-need sales—the practice of selling funeral services and cemetery property to people years or even decades before death.

Pre-need contracts represented a genuine win for consumers: lock in today's prices for services that might not be needed for decades, eliminate the emotional burden of funeral planning for grieving survivors, and spread the cost over time. But for SCI, pre-need created something even more valuable: a financial flywheel that generated capital for expansion.

When a consumer signed a pre-need contract, the funds typically went into state-regulated trusts where they earned investment returns while waiting to fund eventual services. SCI didn't just collect future revenue—it accumulated investable capital. Those trust assets could fund further acquisitions, creating a virtuous cycle where growth funded growth.

The pre-need backlog also provided remarkable earnings visibility. Unlike most businesses that struggle to forecast next quarter, SCI could model future revenues with unusual precision because it literally had contracts on the books for services not yet performed. Today, that backlog has grown to extraordinary proportions: "As we think about 2025, we have a $16 billion preneed backlog, and we are poised to capture incremental value for our shareholders as future demographic trends have a very positive impact on our industry."

C. Stealth Consolidation Strategy

Perhaps SCI's most brilliant strategic insight was understanding that in funeral services, corporate ownership worked best when invisible. Although SCI introduced the brand 'Dignity Memorial' in 1999, many of their network of funeral homes still trade under the family names that were acquired. In fact, in some businesses, the original funeral home staff may still be retained and employed by SCI.

This approach flew in the face of conventional M&A wisdom, which typically emphasizes integration and rebranding. But funeral services aren't conventional. Families choosing a funeral home often rely on generations of community trust. The Smith family may have used "Jones Funeral Home" for three generations—why would they change just because the corporate ownership changed? SCI tends to buy successful funeral homes that are firmly settled and already well known in their community. SCI then retains the funeral home's original name, often along with former owners who are kept on as management.

A typical SCI-owned funeral home will not contain adverts or SCI logos. Consequently, most consumers are unfamiliar with the company itself. This stealth strategy meant SCI could achieve massive scale while appearing, to consumers, as thousands of locally-owned businesses.

D. Global Expansion

By the 1990s, SCI's ambitions had outgrown North America. On December 31, 1999, SCI owned and operated 3,823 funeral service locations, 525 cemeteries, 198 crematoria and two insurance operations located in 20 countries on five continents.

The international expansion began notably in 1994 with Britain. In 1994, SCI made a hostile offer for Great Southern Group, one of Britain's largest funeral home chains. The SCI executives had skin as thick as the longhorn hides on Heiligbrodt's parquet office floor. "They said some horrible things over there," Waltrip recalled. "They called us cowboys," Heiligbrodt, the company president, said. In the end, Great Southern agreed to sell.

At its peak, SCI had become something unprecedented: a global death care conglomerate operating on five continents. But as we'll see, global expansion would prove to be one ambition too many.

So what for investors: The 1962-1999 era established SCI's core competitive advantages: cluster economics, pre-need financial engineering, and the preservation of local brand equity at corporate scale. These advantages compound over decades and are extraordinarily difficult for competitors to replicate.

IV. The Loewen Wars: A Hostile Takeover Battle (1995–1999)

A. The Rise of The Loewen Group

SCI wasn't the only company that recognized consolidation opportunity in death care. The Loewen Group Inc., which began consolidating funeral homes in 1969 under Raymond Loewen and went public in 1987, expanding aggressively into the United States with its first acquisition in California that year.

Raymond Loewen was a fascinating counterpoint to Waltrip—a Canadian entrepreneur with a messianic streak and outsized ambitions. The founder, chairman and chief executive of Loewen Group—the world's second-biggest funeral home chain, based in the Vancouver suburbs—boasts that when he took command of his family's mortuary in rural Manitoba 35 years ago, he immediately fired his two brothers.

By the mid-1990s, the rivalry between SCI and Loewen had become industry-defining. By 1995, Loewen owned 1,115 funeral homes and 427 cemeteries, achieving a stock peak of $55.50. As of September, Houston-based SCI owned 2,864 funeral homes and 335 cemeteries worldwide. At the start of 1997, Loewen, of Vancouver, B.C., owned or operated 956 funeral homes and 299 cemeteries across the U.S.

B. The Mississippi Lawsuit That Changed Everything

What brought Loewen Group to its knees wasn't competition from SCI—it was a Mississippi courtroom. The Loewen Group was building along when it came to a disagreement with the Bradford-O'Keefe Funeral Homes in Mississippi over how some business dealings with certain funeral homes and insurance companies would be handled in a sale/purchase agreement.

That lawsuit and pursuant trial comes straight out of a John Grisham southern courtroom novel, all set with a flamboyant attorney, Willie Gary, who had been portrayed on the television show "Lives of the Rich and Famous" and flew in a private jet named "Wings of Justice." In the end, a plaintiff's lawsuit for about $5 million in damages turned into a jury award of about $500 million against the Loewen Group.

After a jury trial in Mississippi, Bradford-O'Keefe was victorious in the verdict and the jury not only awarded the $5 million in damages but upped that amount to $500 million including punitive damages (and it is now known that 8 of the 12 jurors would have preferred a $1 billion punitive damage amount). In 1996, Loewen Group, knowing it can never pay off the $500 million arranges for a $175 million settlement with Bradford-O'Keefe.

C. SCI's Hostile Bid

SCI saw blood in the water. One month later, the Loewen Group's rival consolidator—Service Corporation International (SCI), the largest provider of death services in the US—launched a hostile takeover bid for the Loewen Group valued at $2.8 billion.

Though bitter rivals, Loewen and SCI have competed relatively quietly in Florida—until September, when SCI mounted a hostile takeover bid for Loewen. SCI initially offered $43 a share for Loewen, then upped the bid to $45. Loewen's board of directors rejected both offers from SCI.

Loewen was widely reported to have waged a multi-pronged defensive strategy that included making a slew of acquisitions, granting lucrative severance packages to senior executives and encouraging state and federal regulatory agencies in the U.S. to investigate the proposed transaction's anticompetitive effects.

At stake for Loewen is its independence. At stake for SCI is unchallenged leadership in making the American way of death as coolly efficient as the marketing of fast food.

D. Loewen's Collapse

The hostile bid ultimately failed, but Loewen had mortally wounded itself in the defense. By the late 1990s, the Loewen Group had accumulated over $2.3 billion in debt primarily through an aggressive expansion strategy involving hundreds of acquisitions of funeral homes and cemeteries across North America and the United Kingdom during the mid-1990s. This overextension was compounded by operational challenges, including integration difficulties from the purchases, which strained cash flow and profitability.

1999—Loewen Group, after purchasing Prime Succession—a group of about 200 funeral homes for $320 million in 1996—and fending off a hostile takeover by Service Corporation International in 1997, files for bankruptcy protection.

The Loewen Group filed for Chapter 11 bankruptcy in June 1999 with $3 billion in debt.

The Loewen collapse offered a cautionary tale about roll-up strategies: consolidation economics only work if you maintain discipline on acquisition pricing and integration execution. Loewen paid premium prices to defend against SCI's hostile bid, took on excessive leverage, and lost operational focus. SCI would later face similar pressures and nearly repeat the same mistakes.

V. The Reckoning & Restructuring (1999–2006)

A. SCI's Own Crisis

The irony of Loewen's collapse was that SCI had its own house in disorder. The company that had seemed invincible was stumbling under the weight of its own global ambitions.

The company had accumulated a load of debt because of its acquisitions. SCI discontinued paying dividends to stockholders in 1999. Where it had once been active in 20 countries, it now operated in only eight. Its number of funeral homes had fallen almost by half, to around 2,500.

The late 1990s had seen funeral home acquisition prices become inflated as SCI, Loewen, and Stewart Enterprises bid against each other for targets. Purchase multiples that made sense at reasonable prices became value-destructive at peak-cycle valuations. Corporate debt levels grew, access to financial markets tightened, and it became apparent that the dynamics of the business expansion model had changed.

B. The Turnaround

What followed represents one of the more impressive corporate turnarounds in modern business history. SCI endeavored to weather the hard times, planning future growth to emerge internally, instead of through acquisition. SCI began marketing its Dignity Memorial package as a national corporate brand name, giving its funeral homes a cohesive image they had not hitherto possessed.

Between 2002 and 2006, SCI reduced its net debt (total debt minus cash) by more than US$1.0 billion, increased operating cash flow, and simplified its field management organization to enhance efficiency, performance, and accountability. It also changed business and sales processes, tightened internal controls following the protocols, strengthened corporate governance standards, and established a new training and development system.

The company divested international operations, returned to its North American roots, and focused on extracting value from existing locations rather than adding new ones. By the mid-2000s, SCI had emerged leaner, more focused, and ready for its next chapter.

So what for investors: The restructuring period demonstrates both the risks and opportunities inherent in roll-up strategies. Discipline in acquisition pricing and balance sheet management determines whether consolidation creates or destroys value. SCI's survival—while Loewen did not survive—came down to having slightly better financial cushion and slightly better operational execution during the crisis.

VI. Inflection Point #1: The Alderwoods Acquisition (2006)

The business world occasionally offers moments of poetic justice, and SCI's 2006 acquisition of Alderwoods Group delivered one of the most satisfying in corporate history.

Remember the Loewen Group—the Canadian rival that had fought off SCI's hostile bid in 1996-97, nearly bankrupted itself in the process, and filed for Chapter 11 in 1999? In January 2002, the Loewen Group emerged from bankruptcy as The Alderwoods Group.

Four years later, On April 3, 2006, Service Corporation International (SCI) announced a definitive agreement to acquire Alderwoods Group in an all-cash transaction valued at $856 million for the equity portion, or $20 per share for all outstanding shares, with the total enterprise value reaching $1.23 billion including the assumption of approximately $373 million in net debt.

The deal that SCI couldn't complete for $2.8 billion in 1996 was now being done for $1.23 billion in 2006. Loewen shareholders who had rejected SCI's $43-45 per share offers a decade earlier now saw their successor company sold for $20 per share. The math of resisting a hostile bid rarely looks this damning.

The consent order settled charges that Service Corporation International's (SCI) proposed acquisition of Alderwoods Group Inc. would likely lessen competition in 47 markets for funeral or cemetery services, leaving consumers with fewer choices and the prospect of higher prices or reduced levels of service. Under the settlement, SCI must sell funeral homes in 29 markets and cemeteries in 12 markets across the United States.

To resolve these issues, SCI and Alderwoods entered a consent agreement with the FTC on October 13, 2006, which was accepted for public comment on November 22 and became final on January 5, 2007. The decree mandated divestitures of 40 funeral home facilities across 29 markets and 15 cemetery properties across 12 markets.

In November 2006, The Alderwoods Group was acquired by SCI, which had been The Loewen Group's rival. The circle was complete. SCI had absorbed its most formidable competitor, proving that in business as in funeral services, patience is often rewarded.

VII. Inflection Point #2: The Stewart Enterprises Acquisition (2013)

Seven years after Alderwoods, SCI made its largest acquisition ever: Stewart Enterprises, the New Orleans-based company that had been the third major player in the industry consolidation race of the 1990s.

In May 2013, SCI signed a US$1.4 billion deal to purchase Stewart Enterprises, the second-largest death care company. Stewart is the second-largest funeral and cemetery services provider in the nation, with 217 funeral homes and 141 cemeteries in 24 states and Puerto Rico. For the year ending on October 31, 2013, Stewart's total revenues were approximately $524.1 million.

The acquisition will expand SCI's unparalleled network in the highly fragmented funeral and cemetery industry in North America. The combined company is expected to have pro forma revenue of nearly $3 billion and a pro forma backlog of future preneed revenue exceeding $9 billion. The two companies have 2,168 locations in 48 states, eight Canadian provinces and Puerto Rico. These locations include 1,653 funeral homes and 515 cemeteries.

The FTC scrutinized this merger intensively. Following a public comment period, the Federal Trade Commission has approved a final order settling charges that Service Corporation International's (SCI) acquisition of Stewart Enterprises, Inc. was anticompetitive in 29 local funeral services markets and 30 local cemetery markets throughout the United States. According to the FTC's complaint, first announced in December 2013, SCI's proposed acquisition of Stewart would likely substantially reduce competition in a number of local markets identified by the agency.

The proposed order settling the FTC's charges requires SCI and Stewart to sell the 53 funeral homes and 38 cemeteries to Commission-approved buyers within 180 days. Also, for 10 years, the FTC will be able to review any attempt by SCI to acquire any funeral or cemetery assets in the relevant geographic markets.

Today it has completed its acquisition of Stewart Enterprises, Inc. (Nasdaq GS: STEI). Under the terms of the merger agreement, each outstanding share of Stewarts' common stock has been converted into the right to receive $13.25 in cash.

The Stewart deal transformed SCI from dominant to nearly unassailable. With Loewen/Alderwoods and Stewart absorbed, SCI had consolidated the three largest players from the 1990s consolidation wars into a single entity. The FTC's 10-year prior notice requirement for acquisitions in affected markets was a meaningful constraint, but it would eventually expire—setting the stage for the next growth chapter.

VIII. Inflection Point #3: The COVID-19 Pandemic (2020–2022)

The COVID-19 pandemic presented SCI with a grim irony: the company's core service—managing death—faced unprecedented demand at precisely the moment when many businesses faced existential threat.

Just to give you a little color on the cadence of the quarter, our same-store funeral volumes were up 7% in October, then grew to 13% in November and an unprecedented 31% in December, which is the highest monthly growth rate we experienced all year. And as a result of this surge late in the quarter, we finished the fourth quarter with adjusted earnings per share of $1.13 compared to $0.60 in the prior year, well above the range we provided to you in October. Both funeral and cemetery segments had margin improvement of over 600 basis points, driven by double-digit top line percentage growth applied against a more efficient cost structure.

Revenue from all sources for 1Q 2021 was $1.078 billion as compared to $803 million in 1Q 2020—an increase of over 34% and Operating Income more than doubled for the company over 1Q 2020.

For the year, we grew revenue $632 million, or 18%; and adjusted earnings per share to $4.57, or 57% compared to the prior year. While we saw 4% comparable funeral volume growth, even growing over a COVID-impacted 2020, the primary drivers of our revenue was mid-20% growth in both preneed and atneed cemetery revenues, combined with a strong 7% increase in our funeral sales average.

The pandemic years tested SCI operationally while rewarding it financially. CEO Tom Ryan noted: "If we learn something from this crisis is that people value what we provide. And you can see the cremation average only moved 20 basis points, which is, again, shocking when you think about your immediate reaction to what will people choose to do through this COVID crisis."

What's remarkable is that despite predictions that COVID would accelerate the shift away from traditional funeral services toward minimal cremation, consumer behavior proved remarkably resilient. Families continued to value professional death care services even during the most challenging period in modern memory.

So what for investors: The pandemic demonstrated SCI's operating leverage—when volume increases, a disproportionate share of incremental revenue flows to the bottom line due to the fixed-cost nature of funeral operations. It also validated the pre-need model, as contracted services provided stability during uncertainty.

IX. Inflection Point #4: FTC Moratorium Expiration & Future Growth (2024–Present)

The Stewart Enterprises acquisition came with a significant constraint: the FTC's 10-year review period limiting acquisitions in affected markets. That constraint expired in May 2024, opening a new chapter for SCI's growth strategy.

Back in 2013, SCI was virtually prohibited from acquiring funeral home and cemetery properties in certain markets for the next ten years. Fast-forward, the Earnings Call from SCI's year end results noted that prohibition will be ending come May 2024. In response to a question on the subject, CEO Thomas Ryan responded: "I think it's hard to size it, but it is a significant amount of markets that we've been really precluded from participating in for the last two years by those prior notice agreements, which expire in May. So it's very difficult to predict when or what. But we're excited about it. We do think it kind of allows us to be a little more active as it relates to acquisitions and get back involved in some of those markets. So we're excited about it. We think it will create some momentum."

Our robust cash flow for the year allowed us to invest $181 million into the acquisition of 26 funeral homes and 6 cemeteries in major metropolitan markets and $62 million into real estate transactions to expand our footprint of funeral homes and cemeteries in our existing markets.

SCI has also signaled interest in larger expansion opportunities. Among recent announcements, SCI's interest in a potential expansion into Canada through an acquisition of Arbor Memorial stands out. This move directly supports the company's goal of increasing market share by up to 30 percent, reinforcing its acquisition-led growth strategy.

Consolidation Opportunities: Target acquisition spend of $75-$125 million; acquired $180-$185 million in 2024. Consolidation Goals: Aims to increase market share to 25-30%, with interest in acquiring Arbor Memorial in Canada.

The moratorium expiration arrives at an opportune moment. SCI has a strong balance sheet, proven integration capabilities, and demographic tailwinds from an aging Baby Boomer population. The question is whether attractive acquisition targets remain at reasonable prices in an industry that SCI has already substantially consolidated.

X. The Cremation Challenge: Industry Disruption

Every industry faces disruption, and death care is no exception. The rise of cremation represents the most significant shift in American funeral practices in a century—and forces investors to ask whether SCI's traditional business model remains viable.

The cremation rate has doubled in the last ten years, and the National Funeral Directors Association (NFDA) reports that the cremation rate is expected to reach 82.1% by 2045, highlighting a profound shift in funeral practices.

The U.S. cremation rate is now at just over 60%. Forecasts are for the rate to reach 80% within 20 years.

According to the National Funeral Directors Association (NFDA), cremation rates soared from 3.56% in 1960 to 61.9% in 2024, with projections estimating 82.1% by 2045, while burials have plummeted to 33.2%. Driven by cost, cultural shifts, and environmental considerations, this trend has disrupted the funeral industry's traditional business model, forcing adaptation through revised cost structures, diversified services, and innovative technologies.

The average cost of a traditional funeral is $7,848 (NFDA) without any cemetery costs. If a family now opts for a cremation service, that price is likely to drop to around $3,600. So, it is easy to see that funeral home revenue must decrease as families shift from traditional burial to cremation.

SCI's response has been characteristic pragmatism. SCI's large-scale acquisition led it to operate under different brands to cater to all market segments, from National Cremation as a budget brand, Funeraria Del Angel to capture the U.S. Spanish-speaking population, to LHT Consulting delivering funerals of distinction to the celebrities and politicians. During their major acquisition of small funeral homes, they retained the local funeral home name and just added the Dignity Memorial brand.

Rather than fight the cremation trend, SCI has adapted its business model to capture value across the price spectrum. Budget cremation services through National Cremation Society compete for price-sensitive consumers, while full-service memorial offerings capture families who want professional support regardless of disposition method.

The core cremation rate increased modestly by 50 basis points to 57.3%. SCI's internal cremation rate runs somewhat below the national average, suggesting its customer base skews toward full-service offerings—a favorable positioning given the higher revenue per case for traditional services.

XI. The Pre-Need Backlog: SCI's Secret Weapon

If there's one number that captures SCI's competitive position better than any other, it's the pre-need backlog: The company has established a substantial backlog of $16 billion in future revenue derived from preneed sales, indicating strong future earnings potential and customer commitment.

For 2025, as Tom mentioned on the call last week, we are expecting low single digit declines in our funeral preneed production for 2025 as a result of all that volatility. But as we look forward to 2026, expecting stability there and growth, which to really back to your question, our hope is that growth in that backlog, which today in total for funeral and cemetery sits right at $16 billion. That growth is going to help not only lock in future market share, but hopefully grow some premium or funeral market share going forward as well.

The pre-need model creates multiple competitive advantages. First, it locks in future market share years before services are performed. When someone signs a pre-need contract with an SCI funeral home, that revenue is effectively booked—the family will return to that location when the time comes. Second, pre-need sales generate trust assets that earn investment returns while waiting for fulfillment, creating a financial float similar to insurance companies. Third, the pre-need sales process builds customer relationships and brand preference that extend beyond the original purchaser to their families.

In July 2024, SCI made a strategic shift in how it funds pre-need contracts: Global Atlantic announced a 10-year partnership with Service Corporation International ("SCI"), positioning it to become the preferred provider of preneed insurance for North America's largest provider of funeral, cremation and cemetery services.

Preneed insurance is a type of life insurance policy created to help cover the costs associated with funeral expenses, providing peace of mind for the individual and alleviating the potential financial burden on their family. This preferred partnership provides Global Atlantic the opportunity to significantly grow its preneed business and positions the firm to become the number one provider of preneed insurance in North America.

Back in July, SCI announced its new partnership with Global Atlantic, during which it switched from trust-funded preneed to insurance-funded preneed. That switch cost the company an estimated $30 million in preneed sales as compared to last year as its sales force had to be retrained on all the new products.

The shift from trust-funded to insurance-funded pre-need represents a significant evolution in SCI's capital structure and risk profile. Insurance-funded contracts transfer investment risk to the insurance provider while generating commission revenue for SCI—a more capital-light model that should support returns on equity over time.

XII. Bull Case vs. Bear Case: Evaluating SCI's Investment Thesis

The Bull Case

Demographic Destiny: The 65-and-older population is projected to nearly double during the next three decades—ballooning from 56 million to 94 million by 2060. SCI operates in an industry where demand growth is mathematically certain. The only question is timing and magnitude.

Unassailable Scale: After absorbing Loewen/Alderwoods and Stewart, SCI has no meaningful public company competitor in traditional funeral services. The next largest United States public death care company does less than 1/10th of that financial volume. Scale advantages in purchasing, technology, and talent recruitment compound over time.

$16 Billion Pre-Need Backlog: This backlog represents locked-in future revenue with high visibility. Unlike most businesses scrambling to forecast next quarter, SCI has unusual certainty about its medium-term trajectory.

Proven Management: Tom Ryan has navigated the company through the COVID crisis, the Stewart integration, and the pre-need insurance transition with steady execution. The management team understands their business deeply and has demonstrated capital allocation discipline.

Acquisition Optionality: With the FTC moratorium expired and $1.5 billion in liquidity, SCI can pursue attractive tuck-in acquisitions and potentially larger transactions like Arbor Memorial in Canada.

The Bear Case

Cremation Economics: The shift from traditional burial (average ~$8,000) to cremation (average ~$3,600) structurally reduces revenue per service. Even if SCI captures cremation share, lower average tickets pressure margins.

Private Equity Competition: Foundation Partners Group and other private equity-backed consolidators are actively acquiring funeral homes, potentially bidding up prices and capturing targets that might otherwise have gone to SCI.

Regulatory Risk: The funeral industry faces periodic regulatory scrutiny. FTC enforcement of the Funeral Rule, state-level regulations, and consumer protection litigation create ongoing legal and compliance costs.

Valuation: At roughly 4x revenue and 15-17x forward earnings, SCI trades at a premium to the S&P 500. The premium is justified by predictability and defensive characteristics, but there's less margin of safety than in cyclical businesses trading at trough valuations.

Pre-Need Execution Risk: The transition from trust-funded to insurance-funded pre-need is complex. Near-term disruption to sales production and the learning curve for sales counselors obtaining insurance licenses could create earnings volatility.

Porter's Five Forces Analysis

Threat of New Entrants: LOW. Funeral homes benefit from location economics and community trust built over decades. New entrants struggle to replicate established relationships. Scale advantages in purchasing and technology create barriers.

Bargaining Power of Suppliers: LOW. Casket manufacturers, vault suppliers, and other vendors face a highly concentrated customer base. SCI's purchasing power is unmatched.

Bargaining Power of Buyers: MODERATE. Funeral purchases are emotional and often made under time pressure, limiting price shopping. However, FTC-mandated price disclosure and cremation alternatives give consumers more options than in the past.

Threat of Substitutes: MODERATE. Direct cremation and DIY memorial services represent substitutes for traditional funeral services. Green burials and human composting are emerging alternatives, though still small in scale.

Competitive Rivalry: LOW-MODERATE. SCI faces limited direct competition from public companies. Private equity consolidators compete for acquisitions. Independent funeral homes compete locally but lack scale advantages.

Hamilton Helmer's 7 Powers Framework

Scale Economies: SCI benefits from fixed costs (technology, corporate overhead, training) spread across 1,900+ locations. The cluster model shares operational resources within geographic markets.

Network Effects: Limited. Funeral services don't benefit from traditional network effects.

Counter-Positioning: SCI's scale and pre-need backlog create a business model that independent funeral homes cannot replicate, even if they wanted to.

Switching Costs: MODERATE. Pre-need contracts create switching costs—if you've contracted with an SCI funeral home, you're unlikely to switch. Family tradition and community relationships also create inertia.

Branding: The Dignity Memorial brand provides national recognition, while local funeral home names provide community trust. This dual branding strategy captures both economies.

Cornered Resource: SCI has accumulated premier funeral home locations in major metropolitan areas. These locations—often acquired decades ago—would be impossible to replicate today.

Process Power: The cluster model and standardized operations represent institutionalized process advantages that create cost benefits versus independent operators.

XIII. Key Metrics & Investor Considerations

For investors monitoring SCI's ongoing performance, three KPIs deserve primary attention:

1. Same-Store Funeral Volume Growth

This metric captures whether SCI is gaining or losing market share in its existing markets. Volume trends reflect demographic shifts, competitive dynamics, and the maturation of pre-need contracts. In the funeral segment, we expect volumes to range in the slightly down 1% range to the slightly up 1% range, bringing the 12-month volume for 2025 to slightly below flat. This is 200 basis points better than 2024, and we believe now the pull-forward effect going forward will be negligible.

2. Average Revenue Per Funeral

This metric captures pricing power and mix shift between traditional services and cremation. We're pretty comfortable in that 2.5 to 3% range depending on the cremation rate change. We're really focused on discounts and I think we've done a good job of managing those things. If average revenue per funeral grows faster than cremation rate compression, SCI is successfully navigating the industry transition.

3. Pre-Need Backlog Growth

The $16 billion backlog represents SCI's embedded future growth. Watch for whether new pre-need sales production exceeds contract maturations, growing the backlog over time. Growth Strategies: Focus on expanding the $16 billion preneed backlog and enhancing cemetery sales through tiering strategies.

XIV. Legal, Regulatory & Accounting Considerations

FTC Funeral Rule: The Federal Trade Commission's Funeral Rule requires funeral homes to provide itemized price lists and restricts certain bundling practices. Compliance is ongoing, and rule revisions remain possible.

California Legal Reserve: The current year quarter was favorably impacted by $20.3 million resulting from a reduction in our California legal reserve as the primary claims period expired. SCI has faced legal challenges in California related to pre-paid funeral plans, though recent reserve reductions suggest the primary exposure window has passed.

Trust Fund Accounting: Pre-need trust assets are held for future fulfillment of contracts. Investment returns affect recognized revenue, creating earnings volatility tied to capital market performance. SCI relies on the performance of its trust investments to fund future obligations associated with preneed contracts. For the nine months ended September 30, 2024, recognized trust fund income related to preneed trust investments was $134.3 million, up from $121.3 million in 2023.

Debt Profile: As of September 30, 2024, SCI's total debt stood at approximately $4.83 billion, with a significant portion subject to variable interest rates. Rising interest rates could increase SCI's financing costs, particularly affecting their ability to refinance existing debt or take on new loans for acquisitions or operational expansions. In 2024, interest expenses increased to $194.5 million from $174.9 million in 2023, driven largely by higher rates.

XV. Conclusion: The Inevitable Business

Robert L. Waltrip, the Houston funeral director who built SCI from a single funeral home to an empire spanning 1,900+ locations, started SCI in 1962, and served as chairman of the board for 54 years, between 1962 and 2016. He passed away in March 2023, his legacy secured as perhaps the most consequential figure in modern funeral service.

What he built represents something rare: a business model that combines inevitable demand with defensible competitive position. Everyone dies. Most families want professional help navigating that reality. SCI has positioned itself to serve more of those families than any competitor, with operational advantages that compound over time.

The story of SCI offers lessons that extend beyond funeral services: the power of patient consolidation in fragmented industries, the value of maintaining local brands while achieving corporate scale, and the financial engineering possible when you collect revenue years before delivering services.

CEO Tom Ryan expressed optimism, stating, "We feel very good about our momentum that we will carry into 2026."

For investors, SCI presents a defensive growth story in an unconventional industry. The demographic tailwinds are mathematical certainties. The pre-need backlog provides unusual visibility. The competitive position is nearly unassailable at scale.

The risks—cremation economics, private equity competition, regulatory exposure—are real but manageable. SCI has navigated worse challenges in its history and emerged stronger.

"We want to place our bets on aces, straights, and cinches," Robert Waltrip once said. By betting on death, he found a cinch indeed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube