Charles Schwab Corporation: The Democratization of Wall Street

I. Introduction & Episode Roadmap

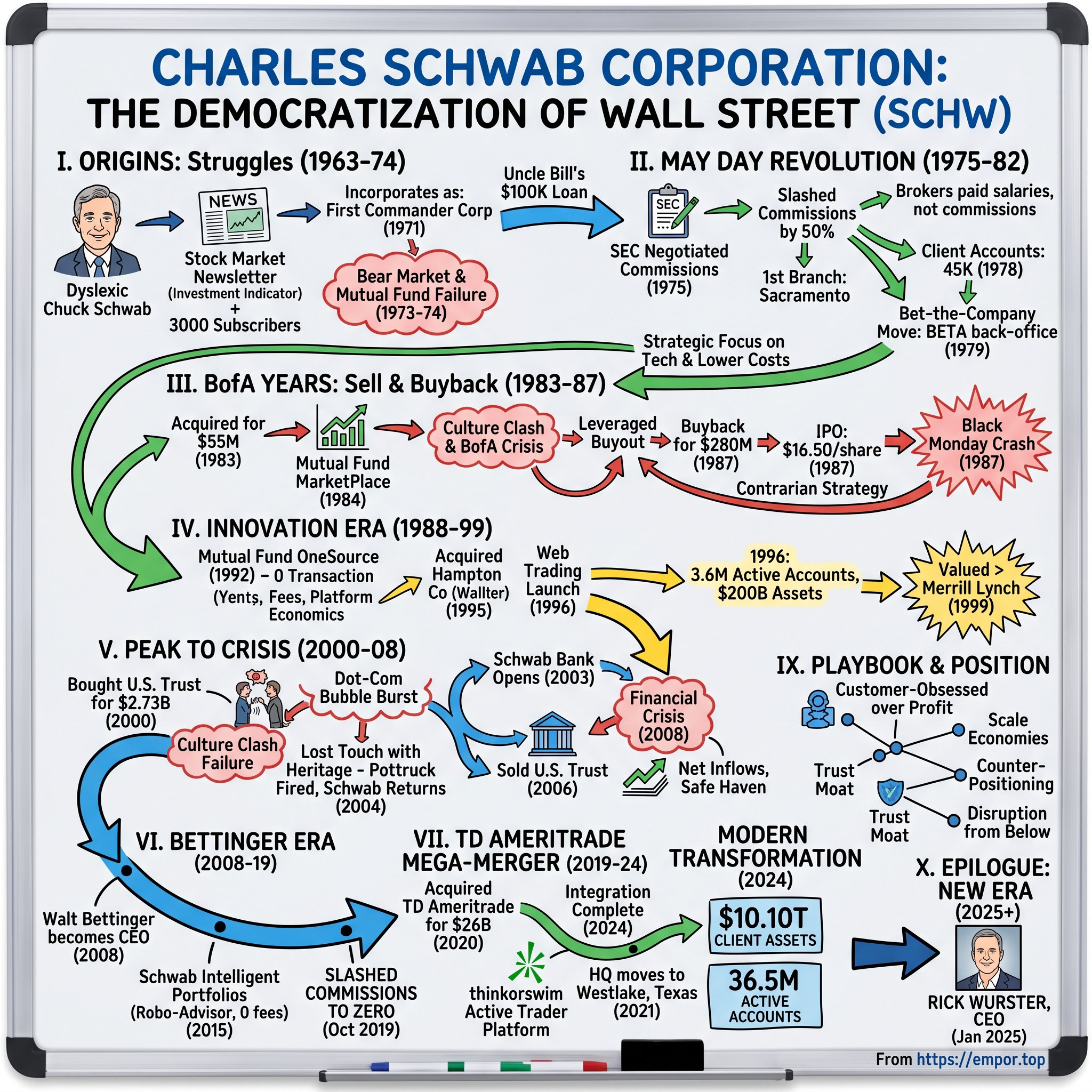

Picture this: It's 1975, and a dyslexic kid from Sacramento walks into a tiny San Francisco office with a radical idea—what if ordinary Americans could buy stocks without paying Wall Street's exorbitant fees? The established brokers laughed. The banks wouldn't lend to him. Landlords refused to rent office space to his fledgling operation. Nearly five decades later, that same company manages $10.10 trillion in client assets across 36.5 million active brokerage accounts, making it one of the largest financial institutions in America.

This is the story of Charles Schwab Corporation—not just a business success story, but a tale of how one company systematically dismantled Wall Street's country club and transformed investing from an exclusive privilege into something approaching a democratic right. It's a narrative filled with near-death experiences, hostile takeovers, buybacks, technological revolutions, and ultimately, the complete restructuring of how Americans interact with their money.

The genius of Chuck Schwab wasn't in creating complex financial products or pioneering new investment strategies. It was simpler and more radical: he looked at the brokerage industry's fat commissions, its conflicts of interest, its country-club exclusivity, and asked, "What if we just... didn't do any of that?" What if brokers were paid salaries instead of commissions? What if we charged half of what everyone else charged? What if we used technology to give small investors the same tools as the wealthy?

These questions launched a revolution that would see Schwab survive the 1987 crash, the dot-com bubble, the 2008 financial crisis, and emerge stronger each time. It's a company that sold itself to Bank of America for $55 million in 1983, bought itself back for $280 million in 1987, and today commands a market capitalization north of $140 billion. Along the way, it forced the entire industry to adopt its innovations—from discount pricing to online trading to zero commissions—often kicking and screaming.

What makes this story particularly compelling for investors is how Schwab repeatedly chose long-term customer value over short-term profits, and how that contrarian strategy ultimately delivered extraordinary shareholder returns. When competitors were maximizing trading commissions, Schwab cut them. When others pushed proprietary products, Schwab created an open marketplace. When the industry resisted the internet, Schwab embraced it. Each time, the short-term pain led to long-term dominance.

II. Origins: The Newsletter Years & Early Struggles (1963-1974)

The Charles Schwab story doesn't begin with discount brokerage—it starts with a newsletter and a spectacular failure that nearly ended everything before it began.

In 1963, a young Charles R. Schwab partnered with two colleagues to launch Investment Indicator, a stock market newsletter that promised to help ordinary investors navigate the complexities of Wall Street. This wasn't some fly-by-night operation; at its peak, the newsletter boasted 3,000 subscribers, each paying $84 annually—roughly $800 in today's dollars. For context, this was an era when most Americans got their financial advice from newspaper stock tables or their local bank manager, if they got any at all.

Chuck Schwab wasn't your typical Wall Street type. Severely dyslexic, he struggled with reading throughout his childhood in Sacramento, compensating by developing extraordinary listening skills and an ability to simplify complex concepts—traits that would later define his company's entire approach to customer communication. After earning his BA from Stanford in 1959 and his MBA from Stanford Graduate School of Business in 1961, Schwab didn't head to New York like his classmates. He stayed in California, convinced that finance didn't need to be concentrated in Lower Manhattan. By April 1971, the evolution was clear. The firm was incorporated in California as First Commander Corporation, a wholly owned subsidiary of Commander Industries, Inc., for traditional brokerage services and to publish the Schwab investment newsletter. This wasn't just a newsletter company anymore—it was becoming something more ambitious. But the path to revolution would first pass through near-catastrophe.

The turning point came with Schwab's first major entrepreneurial disaster: a mutual fund venture that went spectacularly wrong. In the early 1970s, Schwab launched a no-load mutual fund just as the market was peaking. The timing couldn't have been worse. The 1973-74 bear market—one of the most brutal in post-war history—crushed the fund's value. Investors fled, regulators circled, and Schwab found himself personally liable for significant losses. The experience nearly bankrupted him and left him with a searing lesson: never again would he put himself in a position where his interests conflicted with his customers'.

In November of that year, Schwab and four others purchased all the stock from Commander Industries, Inc., and in 1972, Schwab bought all the stock from what was once Commander Industries. By 1973, the transformation was complete: the company name changed to Charles Schwab & Co., Inc.

The mutual fund debacle had left Schwab nearly broke. His uncle Bill, a successful industrialist who had always believed in his nephew despite the dyslexia that others saw as a limitation, stepped in with a $100,000 loan. It was this capital—family money, not Wall Street money—that would fund the revolution. Schwab set up shop at 629 Montgomery Street in San Francisco, deliberately 3,000 miles from Wall Street's influence.

The location was symbolic but also practical. San Francisco in the early 1970s was experiencing a cultural and technological renaissance. While New York remained hidebound by tradition, the Bay Area was questioning everything. This was the environment where Schwab would reimagine what a brokerage could be. But first, he needed to survive 1974—a year when the Dow Jones fell 45% from its peak and when most Americans viewed the stock market as a casino for the rich to lose money in spectacular fashion.

III. The May Day Revolution: Birth of Discount Brokerage (1975-1982)

May 1, 1975. Wall Street called it "May Day"—and not in celebration. The U.S. Securities and Exchange Commission allowed negotiated commission rates, ending 183 years of fixed pricing that had made stockbrokers rich and kept ordinary investors out. The old guard panicked. Merrill Lynch predicted chaos. E.F. Hutton warned of a race to the bottom. Most established brokers actually raised their commissions on small trades, figuring individual investors had nowhere else to go.

Chuck Schwab saw it differently. Within hours of the regulatory change, he did something that seemed suicidal to traditional brokers: he slashed commissions by 50% across the board. But the real revolution wasn't just the pricing. Schwab instituted two radical policies that fundamentally restructured the economics of the brokerage business. First, those dramatically reduced charges to consumers. Second—and this was the truly revolutionary part—salesmen were (and still are today) paid hourly salaries, rather than commissions on the total sale price.

Think about what this meant. Every other brokerage in America had brokers whose income depended on how much and how often their clients traded. Schwab's brokers had no such incentive. They could give honest advice. They could tell a client not to trade. They could spend an hour educating a novice investor without worrying about their paycheck. It was a complete inversion of Wall Street's incentive structure. In September, Schwab opened its first branch in Sacramento, California—a deliberate choice. This wasn't San Francisco or New York. This was Chuck's hometown, where landlords knew him, where he could prove the concept without the scrutiny of financial centers. The branch was modest, almost apologetic in its simplicity. No mahogany desks, no oil paintings of founders, no suggestion that investing required membership in an exclusive club.

The establishment's reaction was swift and brutal. Banks refused to lend to Schwab. Landlords in financial districts wouldn't rent office space to a "discount" broker—the very word was considered unseemly, like opening a discount surgery clinic. The New York Stock Exchange wouldn't return his calls. Traditional brokers spread rumors that Schwab was a fly-by-night operation that would collapse within months.

But something extraordinary was happening in that Sacramento branch. Middle-class families were opening accounts. Teachers, small business owners, engineers—people who had never owned a share of stock in their lives—were walking through the doors. By 1978, Schwab had 45,000 client accounts total, doubling to 84,000 in 1979. This wasn't just growth; it was validation of a thesis: millions of Americans wanted to invest but had been locked out by prohibitive costs and intimidating brokers.

The real innovation came in 1979, when Schwab made what he later called a "bet-the-company" move. Schwab risked $500,000 on a back-office settlement system called BETA (short for Brokerage Execution and Transaction Analysis), enabling Schwab to become the first discount broker to bring automation in house. Half a million dollars might not sound like much today, but for a company that was still proving its model, it represented months of operating capital.

BETA changed everything. While competitors were still processing trades on paper, taking days to settle transactions, Schwab could do it in hours. The system could handle volume that would have required dozens of clerks at traditional brokerages. It was the beginning of Schwab's strategic insight: technology wasn't just a cost center; it was the key to democratization. Every efficiency gained through automation could be passed on to customers as lower costs.

In 1980, Schwab established the industry's first 24-hour quotation service. Think about what this meant in an era before the internet. An investor in California could call at 9 PM Pacific time and get real-time quotes on their holdings. They didn't need to wait for the morning paper or call their broker during business hours. Information—the lifeblood of investing—was becoming democratized alongside access.

The numbers tell the story of acceleration: total client accounts grew to 147,000 in 1980, to 222,000 in 1981, and to 374,000 in 1982. In 1982, Schwab became the first to offer 24/7 order entry and quote service, and its first international office was opened in Hong Kong. But behind these milestones was a more fundamental transformation. Schwab wasn't just creating a cheaper alternative to traditional brokers; it was building an entirely different kind of financial services company—one that saw customers as partners to be empowered rather than marks to be sold to.

IV. The Bank of America Years: Selling Out & Buying Back (1983-1987)

By 1983, Chuck Schwab faced an existential problem. The company was growing so fast it was choking on its own success. New branch openings required capital. Technology investments demanded millions. Competitors with deeper pockets were beginning to copy the discount model. Schwab needed money—lots of it—and the public markets weren't yet an option for a company still proving that discount brokerage was more than a fad.

Enter Bank of America, the colossus of West Coast banking. To understand what happened next, you need to understand the psychology of Chuck Schwab in 1983. He had built something remarkable, but he was also exhausted. The company needed professional management, systems, capital—all things that Bank of America could provide. When BofA offered $55 million for the company, Schwab saw it as a way to secure his company's future while maintaining operational control.

In 1983, Bank of America acquired Charles Schwab for $55 million. On paper, it looked like a perfect match. Bank of America got a fast-growing brokerage to complement its banking operations. Schwab got the capital and credibility that came with being part of one of America's largest financial institutions. Chuck Schwab himself remained as president of what was now a semi-autonomous unit. The markets loved it. Customers barely noticed. Everything seemed to be going according to plan. But the reality was far messier. Bank of America, however, had its own separate severe problems, and its stock plunged. The SEC investigated Schwab on the possibility he was selling stock to take advantage of insider information; he denied it, and no charges were filed. Tensions between the Schwab unit and Bank of America escalated as the 1980s progressed.

The culture clash was immediate and profound. Bank of America executives couldn't understand why Schwab was spending millions on technology when a simple ledger book had worked fine for decades. They questioned every marketing expense, every new branch opening, every innovation that didn't promise immediate returns. Schwab employees, used to a entrepreneurial, customer-first culture, suddenly found themselves filling out forms in triplicate and waiting weeks for approvals that used to take hours.

In 1984, despite the bureaucratic headwinds, the company managed to launch 140 no-load mutual funds—creating what would become the Mutual Fund MarketPlace. This was revolutionary: investors could now choose from multiple fund families in one place, like shopping for groceries instead of visiting individual farms. But internally, the innovation nearly didn't happen. Bank of America executives worried about channel conflict with their own investment products. It took Chuck Schwab personally threatening to resign to push it through.

At this point the unit had annual sales of $41 million, 600 employees, and 220,000 customers through 40 branches. Expansion was rapid, reaching 1.6 million customers in 1986, with sales of $308 million. The numbers looked fantastic on paper. But behind the scenes, the relationship was deteriorating rapidly.

The breaking point came from an unexpected source: Bank of America's own financial crisis. The bank had made a series of catastrophic loans to Latin American countries that were now defaulting. Real estate loans in California were going bad. The stock price collapsed. Suddenly, the parent company that was supposed to provide stability and capital was itself teetering on the edge of insolvency.

For Chuck Schwab, this created both a crisis and an opportunity. The crisis: his company was now tied to a sinking ship, and customers were beginning to worry about the safety of their assets. The opportunity: Bank of America desperately needed cash and might be willing to sell.

The negotiations were brutal. Schwab assembled a group of investors and management to execute a leveraged buyout. The price: $280 million—more than five times what Bank of America had paid just four years earlier. Bank of America wanted the cash, but they also wanted to save face. The deal was structured to make it look like Bank of America was making a killing, which in some ways they were.

In 1987, management, including Charles R. Schwab, bought the company back from Bank of America for $280 million. The timing seemed insane. The leveraged buyout closed in March 1987. The IPO was rushed through in September 1987, with the company going public at $16.50 per share. And then, just six weeks later, came Black Monday—October 19, 1987—when the Dow Jones Industrial Average fell 22% in a single day.

Schwab's newly public stock crashed along with everything else. Employees who had celebrated their paper wealth from the IPO watched it evaporate. Customers panicked. Phone lines were jammed. The company's computer systems, despite all the investment in technology, buckled under the volume. It was trial by fire for a company that had just regained its independence.

But here's what's remarkable: Schwab didn't just survive Black Monday; it thrived in its aftermath. While competitors laid off staff and closed branches, Schwab hired. While others pulled back on technology spending, Schwab doubled down. Chuck Schwab went on a media tour, calmly explaining that market crashes were temporary but the need for intelligent, low-cost investing was permanent. The message resonated. Within a year, new account openings had returned to pre-crash levels.

V. Innovation Era: Building the Modern Brokerage (1988-1999)

The post-crash period revealed a fundamental truth about Schwab: crises were opportunities if you had the courage to see them that way. While Wall Street was still shellshocked from Black Monday, Schwab embarked on one of the most aggressive expansion and innovation campaigns in financial services history.

The strategy was counterintuitive but brilliant. In 1991, the company acquired Mayer & Schweitzer, a market making firm that gave Schwab the ability to execute trades internally rather than routing them to exchanges. This wasn't just about saving money on execution—though it did that. It was about controlling the entire customer experience from order to settlement.

But the real revolution came in 1992 with the launch of Mutual Fund OneSource. The concept was simple but radical: what if investors could buy mutual funds from hundreds of different fund companies with no transaction fees, all in one account? The fund companies would pay Schwab a small percentage of assets for shelf space, like Procter & Gamble paying Walmart. Investors would get unprecedented choice and convenience.

The mutual fund industry initially resisted. Why should they pay Schwab when investors could buy directly from them? But Schwab had leverage: millions of customers who trusted the Schwab brand more than individual fund companies. Within a year, OneSource had $15 billion in assets. Within five years, it had $170 billion. Schwab had effectively become the Amazon of mutual funds before Amazon was even public.

International expansion followed. London, Hong Kong, Tokyo—Schwab planted flags in major financial centers, not to compete with local brokers but to serve the growing population of globally mobile investors who wanted a consistent platform wherever they were.

In 1995, a crucial acquisition flew under the radar: Schwab acquired The Hampton Company, founded by Walter W. Bettinger. Bettinger had built a successful 401(k) recordkeeping business in Ohio, far from any financial center. What Schwab saw wasn't just the business but the leader—someone who understood that retirement services would become the next frontier in democratizing investing. Bettinger would rise through the ranks to become CEO in 2008, but his influence on Schwab's retirement strategy was immediate. The following year in 1996, they launched Web trading, letting customers trade listed and OTC stocks and check balances and order statuses on their website. This sounds routine now, but in 1996 it was revolutionary. Schwab responded in 1996 by becoming the first major financial services firm to sell online listed and over-the-counter stocks, as well as mutual funds and bonds. The startups charged $36 a trade, and Schwab charged $39 per Internet trade, compared to $160 charged by traditional brokerages using the old technology.

The decision to go online wasn't without controversy. Inside Schwab, executives worried about cannibalizing their phone business. Branch managers feared customers would stop visiting. The technology team warned about security risks. But Chuck Schwab saw it differently: the internet wasn't a threat to their business model; it was the ultimate expression of it. Democratic access to markets required democratic access to technology.

The numbers validated the strategy spectacularly. By 1995 the company was by far the largest discount broker, with revenue of $1.4 billion and $200 billion in total assets managed. By 1996 there were 3.6 million active accounts. Online trading volume exploded from essentially zero to 25% of all trades within two years.

But success brought new challenges. David S. Pottruck, who had spent the majority of his 20 years at the brokerage as Schwab's right-hand man, shared the CEO title with Schwab from 1998 to 2003. This unusual co-CEO structure reflected the tension between Schwab's entrepreneurial past and its corporate future. Pottruck, a former Marine and Wharton MBA, represented the new breed of professional management. Chuck Schwab represented the soul of the company. For a while, the arrangement worked, with Pottruck handling operations while Schwab focused on vision and culture.

The dot-com boom of the late 1990s turned Schwab into a money-printing machine. Day traders opened accounts by the thousands. Trading volumes reached levels that would have crashed their systems just years earlier. The company's market cap soared past traditional Wall Street firms. By 1999, Schwab was worth more than Merrill Lynch. The discount broker from Sacramento had become more valuable than the thundering herd of Wall Street.

VI. Dot-Com Boom to Financial Crisis (2000-2008)

The new millennium began with Schwab at the peak of its powers. In 2000, Schwab purchased U.S. Trust for $2.73 billion, a 147-year-old institution that catered to America's wealthiest families. The acquisition was meant to move Schwab upmarket, to capture the children and grandchildren of U.S. Trust's gilded clientele who might want a more modern approach to wealth management. On paper, it made perfect sense.

In reality, it was a disaster. Efforts to integrate the exclusive U.S. Trust into the discount-broker Schwab yielded a culture clash that ultimately undermined the merger. U.S. Trust bankers, accustomed to managing fortunes for families with names like Rockefeller and Astor, were horrified at being part of a "discount" anything. Schwab employees couldn't understand why U.S. Trust needed marble lobbies and private elevators. Clients fled to competitors who promised more exclusive treatment.

Meanwhile, the dot-com bubble burst with spectacular force. The NASDAQ fell 78% from its peak. Day traders who had made Schwab rich during the boom disappeared overnight. Trading volumes collapsed. Revenue fell by more than half. The company that had seemed invincible suddenly looked vulnerable.

The response to the crisis created a rift that would define the next phase of Schwab's history. Pottruck, now with more operational control, raised fees and pushed the company toward more traditional Wall Street practices. The logic was sound: with trading revenue decimated, the company needed to find other sources of income. But it violated the fundamental Schwab ethos of always lowering costs for customers.

In May 2003, Mr. Schwab stepped down, and gave Pottruck sole control as CEO. For the first time in the company's history, Charles Schwab wasn't running Charles Schwab. Pottruck, finally given full authority, accelerated his strategy of revenue diversification and fee increases.

The market's verdict was swift and brutal. News of Pottruck's removal came as the firm had announced that overall profit had dropped 10%, to $113 million, for the second quarter, driven largely by a 26% decline in revenue from customer stock trading. But the problems went deeper than quarterly earnings. After coming back into control, Mr. Schwab conceded that the company had "lost touch with our heritage", and quickly refocused the business on providing financial advice to individual investors.

On July 24, 2004, the company's board fired Pottruck, replacing him with its founder and namesake. Chuck Schwab, now 67, returned as CEO with a mission to restore the company's soul. He immediately rolled back Pottruck's fee increases, refocused on customer service, and began looking for his true successor—someone who understood that Schwab's competitive advantage wasn't in mimicking Wall Street but in serving Main Street.

The solution came from an unexpected source. In a move to bring in new revenue, the Charles Schwab Bank opened in 2003. While everyone was focused on trading commissions and asset management fees, Schwab quietly built a banking operation that would become crucial to its future success. The bank could take deposits, make loans, and—critically—earn net interest income when rates were favorable. It was a hedge against the volatility of trading revenues.

On November 20, 2006, Schwab announced agreed to sell U.S. Trust to Bank of America for $3.3 billion in cash. The sale price was higher than the purchase price, but considering six years of ownership and integration costs, it was essentially a breakeven deal. More importantly, it was an admission that Schwab's attempt to become a traditional wealth manager for the ultra-wealthy had failed. The company's future lay not in competing for billionaires but in serving millions of millionaires-next-door.

The 2008 financial crisis arrived just as Schwab was finding its footing again. Lehman Brothers collapsed. Merrill Lynch sold itself to Bank of America. Morgan Stanley and Goldman Sachs became bank holding companies. The entire financial system teetered on the brink of collapse.

But Schwab, having learned from previous crises, was prepared. The company had minimal exposure to subprime mortgages. Its balance sheet was conservative. Most importantly, it had the trust of its customers. While clients pulled money from other brokerages, Schwab actually saw net inflows during the worst of the crisis. The company that had started as an insurgent against Wall Street was now seen as a safe haven from Wall Street's excesses.

VII. The Bettinger Era & Modern Transformation (2008-2019)

Walter W. Bettinger II is named president and chief operating officer in 2007, and by 2008, he assumed the role of CEO. The transition from Chuck Schwab to Walt Bettinger represented more than a change in leadership—it was a generational passing of the torch. Bettinger, who had joined Schwab through the acquisition of his company The Hampton Company in 1995, brought a deep understanding of retirement services and a vision for Schwab's next evolution.

Bettinger's first major crisis came immediately. The 2008 financial meltdown was still unfolding when he took the helm. But rather than retreating, Bettinger saw opportunity in the chaos. While competitors were slashing staff and closing branches, Schwab hired aggressively, particularly in technology and customer service. The message was clear: Schwab would emerge from the crisis stronger than it entered. The digital transformation accelerated in 2015 with the launch of Schwab Intelligent Portfolios, entering the robo-advisor space that startups like Wealthfront and Betterment had pioneered. But Schwab's version had a twist: no advisory fees. While competitors charged 0.25% annually, Schwab offered the service for free, making money instead on the cash allocation and expense ratios of its proprietary ETFs. The $5,000 minimum was higher than some competitors, but the zero-fee structure was a classic Schwab move—sacrifice short-term revenue to build long-term relationships. But the most dramatic move of the Bettinger era came on October 1, 2019. Schwab announced it would be slashing its trading commission cost from the previous $4.95 to zero. Starting on Oct. 7, Schwab, which holds about $3.72 trillion in client assets, would no longer charge commission fees for U.S. stocks, ETFs and options trades. The announcement sent shockwaves through the industry. Schwab's stock closed down about 10% Tuesday. Its competitors took a bigger hit, with TD Ameritrade shares falling nearly 26% and E-Trade dropping about 16%.

Charles Schwab said the discount broker's latest move to zero commissions was a longtime goal to deliver to investors. "It was sort of the final solution for investors," the chairman and founder told CNBC. "We have a great deal for investors. You can buy and sell stocks for no commission."

The move was vintage Schwab—sacrifice short-term revenue (an estimated $90-100 million quarterly) to gain long-term market share. But it also revealed sophisticated strategic thinking. By forcing competitors to match zero commissions, Schwab weakened them financially, making them potential acquisition targets. TD Ameritrade, which derived 15-16% of its revenue from commissions compared to Schwab's 3-4%, was particularly vulnerable.

In the month of October, Schwab added 142,000 new brokerage accounts, a gain of 31% from September and 7% more than last October. The new accounts brought Schwab's client assets to a record $3.85 trillion. The strategy was working—Schwab was gaining customers at an accelerated pace while competitors struggled to adjust their business models.

Competition from new entrants like Robinhood had changed the landscape. These app-based brokers targeted younger investors with commission-free trading and gamified interfaces. Rather than dismissing them as toys for day traders, Bettinger recognized them as harbingers of generational change. Schwab's response wasn't to copy Robinhood's interface but to remove the one advantage the upstarts had—free trading—while maintaining Schwab's advantages in breadth of services, financial stability, and trust.

VIII. The TD Ameritrade Mega-Merger (2019-2024)

The zero-commission announcement was more than a pricing decision—it was the opening move in the largest consolidation play in brokerage history. Within weeks of the announcement, rumors began circulating that Schwab was in talks to acquire TD Ameritrade. On November 25, 2019, the deal was confirmed: Schwab would acquire TD Ameritrade in an all-stock transaction valued at $26 billion.

On October 6, 2020, the company acquired TD Ameritrade. As part of the acquisition, Toronto-Dominion Bank acquired around a 12% stake in the company. Soon after, Schwab began the process of transitioning TD Ameritrade accounts to Charles Schwab; once this was finished, TD Ameritrade was shut down in May 2024.

The strategic logic was compelling. The combined entity would have over 24 million client accounts and more than $6 trillion in client assets, creating unprecedented scale advantages. But the real prize was TD Ameritrade's technology platform, particularly thinkorswim—widely considered the best trading platform for active traders. Schwab had always been strong with buy-and-hold investors; TD Ameritrade brought expertise in serving active traders.

Regulatory approval wasn't guaranteed. The Department of Justice scrutinized the deal for potential antitrust violations, particularly in the RIA custody market where the combined company would have significant market share. Schwab's argument was clever: they defined the relevant market not as RIA custody but as overall wealth management, where their combined share was much smaller. After months of review, the DOJ approved the deal without requiring major divestitures.

Integration challenges were immense. Two different technology platforms, two different corporate cultures, millions of accounts to migrate—all during a global pandemic that had sent employees home and markets into unprecedented volatility. The original integration timeline of 18-36 months stretched to nearly four years. But Schwab approached it methodically, migrating accounts in waves, maintaining both platforms during the transition, and obsessively focusing on minimizing client disruption.

Charles Schwab completed final client account transitions associated with the acquisition of Ameritrade, marking the completion of a historic integration. The integration, completed in 2024, was remarkable not for its speed but for its success—client attrition was minimal, and the combined platform offered capabilities neither company could have achieved alone.

The merger also marked a symbolic shift. Effective on January 1, 2021, the company moved its headquarters from San Francisco, California to Westlake, Texas. After nearly 50 years in San Francisco, Schwab was leaving California—driven by lower costs, a more business-friendly regulatory environment, and proximity to its growing Texas operations. The company that had defined itself in opposition to Wall Street was also defining itself in opposition to Silicon Valley's increasingly expensive and regulated environment.

IX. Playbook: Business & Investing Lessons

The Schwab story offers a masterclass in business strategy that extends far beyond financial services. The lessons are deceptively simple but profoundly difficult to execute.

The power of being customer-obsessed versus profit-obsessed: Every major Schwab innovation—from discount pricing to online trading to zero commissions—initially reduced profitability. Traditional business school logic would call this insane. But Schwab understood something deeper: customer value creation eventually translates to shareholder value, but the reverse isn't always true. When you optimize for customer value, you're playing an infinite game. When you optimize for quarterly earnings, you're playing a finite one.

Disruption from below: Schwab never tried to out-luxury Merrill Lynch or out-prestige Goldman Sachs. Instead, they served customers that traditional firms didn't want—the small accounts, the do-it-yourselfers, the cost-conscious retirees. Clay Christensen would later codify this as "disruptive innovation," but Schwab was living it decades before the theory was published. The lesson: don't attack incumbents where they're strong; serve the customers they're ignoring.

Capital allocation as strategy: The Bank of America sale and buyback remains one of the great capital allocation stories in corporate history. Selling for $55 million when you need capital, buying back for $280 million when you have leverage, going public immediately after—it's financial engineering as art form. But the deeper lesson is about timing and optionality. Schwab sold when he had no options and bought when he had maximum leverage.

Platform economics before platforms: The Mutual Fund OneSource model pioneered in 1992 was essentially a platform business model before anyone used that term. Schwab created a marketplace where they didn't manufacture the product (mutual funds) but captured value by reducing transaction costs and aggregating demand. This same model would later be applied by Amazon, Uber, and countless tech platforms. The insight: sometimes the most valuable position isn't making the product but controlling distribution.

Technology as liberation, not replacement: Schwab never saw technology as a way to eliminate human interaction but as a way to make it more valuable. Automated trading freed advisors from paperwork to focus on advice. Online platforms freed customers from phone queues to research at their own pace. The lesson: technology should eliminate friction, not relationships.

Managing through multiple cycles: Schwab survived the 1973-74 bear market, Black Monday in 1987, the dot-com crash, the 2008 financial crisis, and the COVID-19 pandemic. Each crisis became an opportunity to gain market share while competitors retreated. The pattern was consistent: maintain a strong balance sheet, invest during downturns, and emerge stronger. It's easy to say, nearly impossible to do—unless it's embedded in corporate DNA.

Trust as a competitive moat: In financial services, trust is everything. Schwab built trust not through marketing but through consistent behavior over decades. Always lowering costs. Never pushing proprietary products. Admitting mistakes quickly. This trust became a nearly impregnable competitive advantage—customers stayed through market crashes, technology glitches, and integration challenges because they believed Schwab had their interests at heart.

X. Power Analysis & Competitive Position

Using Hamilton Helmer's 7 Powers framework, Schwab exhibits multiple sustainable competitive advantages that compound over time.

Scale economies: With $10.10 trillion in client assets, Schwab can spread fixed costs across an enormous base. A new technology platform that costs $100 million annually represents just 0.001% of assets—for a smaller competitor with $100 billion in assets, it's 0.1%. This 100x cost advantage means Schwab can invest more in technology, service, and innovation while maintaining lower prices. The scale economies are particularly powerful in custody, clearing, and settlement—activities with high fixed costs and low marginal costs.

Network effects: Schwab's advisor ecosystem creates powerful network effects. With over 14,000 independent RIAs using Schwab's custody platform, the company becomes more valuable to each advisor as more join. Advisors benefit from better technology, more educational resources, and stronger negotiating power with fund companies. This creates a virtuous cycle—more advisors attract more resources, which attract more advisors.

Switching costs: Moving brokerage accounts is a hassle. Transferring assets, updating banking relationships, learning new platforms, establishing new advisor relationships—the friction is significant. But Schwab's switching costs go deeper. Many clients have multiple relationships: brokerage, banking, credit cards, mortgages. The more products a client uses, the higher the switching costs. This is why Schwab's focus on becoming a full-service financial firm is so strategic.

Counter-positioning: This is Schwab's original power and remains relevant today. By structuring the entire business around low costs and no conflicts of interest, Schwab makes moves that would be suicidal for traditional firms. Morgan Stanley can't eliminate commissions without destroying its wealth management economics. Goldman Sachs can't embrace index funds without cannibalizing its active management fees. Schwab's counter-positioning means competitors must choose between matching Schwab's model (and destroying their existing business) or ceding market share.

Process power: Schwab's operational excellence isn't easily copied. The ability to handle millions of daily transactions, provide 24/7 service across channels, maintain 99.9% uptime, and do it all at industry-leading low costs—this is process power built over decades. A competitor can't simply hire away a few executives and replicate these capabilities. They're embedded in systems, culture, and countless small optimizations.

Brand power: "Talk to Chuck" isn't just a marketing slogan—it represents five decades of consistent behavior. The Schwab brand means low costs, no conflicts, good technology, and trustworthy advice. This brand allows Schwab to acquire customers at lower costs than competitors and maintain higher retention rates. In financial services, where trust is paramount, brand power translates directly to pricing power (or in Schwab's case, the ability to sustain lower prices).

The combination of these powers creates a formidable competitive position. New entrants face the scale disadvantage. Traditional competitors face the counter-positioning dilemma. Digital-only competitors lack the trust and breadth of services. It's a position built over 50 years that would be nearly impossible to replicate today.

XI. Bear vs. Bull Case

Bull Case: The Compounding Machine

The bull case for Schwab rests on multiple expansion drivers that could compound over the next decade. With $10.10 trillion in client assets across 36.5 million accounts, Schwab has achieved a scale that provides enormous operating leverage. Every basis point of market appreciation adds $1 billion to AUM. Every new service can be amortized across an enormous client base.

The retirement wave represents a generational tailwind. Over the next 20 years, Baby Boomers will transfer an estimated $70 trillion to younger generations—the largest wealth transfer in history. Schwab is uniquely positioned to capture this flow, serving both the retirees who need income solutions and the inheritors who need wealth management. The company's broad platform means they can retain assets across generations rather than losing them to specialists.

Net interest income provides a powerful earnings driver when rates are favorable. With over $500 billion in client cash, every 100 basis point increase in rates can add billions to revenue. While this creates volatility, it also provides upside optionality that pure asset managers lack. The bank subsidiary allows Schwab to optimize this spread income while providing valuable services to clients.

The TD Ameritrade integration, while lengthy, creates synergies that are only beginning to materialize. Cost savings of $1.8-2 billion annually are just the start. Revenue synergies from cross-selling, technology consolidation, and increased scale in negotiating with fund companies could be equally significant. The combined platform serves every client segment from active traders to passive indexers, creating multiple monetization paths.

International expansion remains a largely untapped opportunity. While Schwab has international offices, the company has barely scratched the surface of global wealth management. As international markets develop and regulatory barriers fall, Schwab's low-cost, technology-enabled model could resonate globally just as it has domestically.

Bear Case: The Disruption Scenario

The bear case starts with interest rate sensitivity. Schwab's earnings are significantly exposed to rate cycles. In a prolonged low-rate environment, net interest margins compress, forcing the company to find revenue elsewhere. The 2020-2021 period demonstrated this vulnerability, with earnings under pressure despite record asset levels. While rates have normalized, the cycle will inevitably turn.

Fee pressure remains relentless. Having led the race to zero on commissions, Schwab must now monetize through other channels—cash spreads, proprietary funds, advice fees. But each of these faces its own pressures. Competitors offer higher yields on cash. Index funds push expense ratios toward zero. Robo-advisors commoditize basic advice. The company must run faster just to stand still.

Fintech disruption poses an existential threat. Companies like Robinhood have shown that user experience can trump traditional advantages. Cryptocurrency platforms are capturing younger investors. Neo-banks offer better digital experiences. While Schwab has responded to each threat, playing defense against multiple disruptors is exhausting and expensive. Eventually, one might break through.

Regulatory risks loom large. The DOL's fiduciary rule, SEC's Regulation Best Interest, potential transaction taxes, banking regulation—the regulatory landscape is increasingly complex and costly. Schwab's size makes it a target. A major regulatory change could force business model adjustments that destroy value.

Integration execution risks remain. While the TD Ameritrade integration is largely complete, cultural integration takes years. Key talent might leave. Clients might defect during platform transitions. Technology problems could damage the brand. The history of large mergers in financial services is littered with failures.

Cybersecurity presents an existential risk. A major breach could destroy decades of accumulated trust instantly. As financial services become increasingly digital, the attack surface expands. Nation-state actors, criminal organizations, and hacktivists all target financial institutions. One successful attack could trigger massive client departures and regulatory penalties.

XII. Epilogue: The New Era Under Rick Wurster

As of December 31, 2024, it had $10.10 trillion in client assets, 36.5 million active brokerage accounts, 5.4 million workplace retirement plan participant accounts, and 2.0 million banking accounts. These numbers represent more than just scale—they represent 50 years of consistent execution of a simple idea: investing should be accessible to everyone.

On January 1, 2025, Rick Wurster assumed the CEO position of the company, replacing the retiring Walt Bettinger. Wurster, who joined Schwab in 2016 and most recently served as President, represents continuity rather than revolution. His background—Stanford MBA, management consultant, strategic planner—suggests a focus on operational excellence rather than radical innovation.

But Wurster inherits a company at an inflection point. The easy gains from democratization have been won. Everyone who wants cheap market access has it. The next frontier isn't about access but about outcomes—helping clients not just invest but invest successfully. This requires different capabilities: behavioral coaching, tax optimization, comprehensive planning, alternative investments.

Chuck Schwab, now 87, remains Chairman, a living link to the company's insurgent past. His presence is both asset and challenge—a reminder of core values but potentially a constraint on necessary evolution. The question facing Wurster is how to honor the Schwab heritage while adapting to new realities.

What would Chuck do today if starting from scratch? He wouldn't compete with the existing Schwab—that game has been won. He'd likely look for the next excluded population, the next unfair fee structure, the next technology that could democratize something previously exclusive. Perhaps it's alternative investments, still largely reserved for the wealthy. Perhaps it's small business financial services, still dominated by expensive, relationship-based banks. Perhaps it's something we can't yet imagine.

The Schwab story isn't really about discount brokerage or even financial services. It's about the democratization of opportunity—the radical idea that sophisticated financial tools shouldn't be reserved for the wealthy. In 1975, that meant $50 stock trades instead of $200. In 2025, it means artificial intelligence-powered financial planning, direct indexing, and cryptocurrency exposure—services that would have been unimaginable to that dyslexic kid from Sacramento who just wanted to make investing accessible to everyone.

The measure of Schwab's success isn't just the $10 trillion in assets or the 36 million accounts. It's the millions of Americans who own stocks today who wouldn't have without Schwab's innovations. It's the retirees living comfortably on portfolios they built themselves. It's the first-generation immigrants building wealth their parents couldn't imagine. It's the democratization of capitalism itself.

That's a legacy worth more than any stock price. And it's a reminder that the best businesses aren't just about making money—they're about solving real problems for real people. Chuck Schwab did both, and in doing so, changed American finance forever.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube