Royal Caribbean Group: Sailing to New Heights

I. Introduction & Episode Roadmap

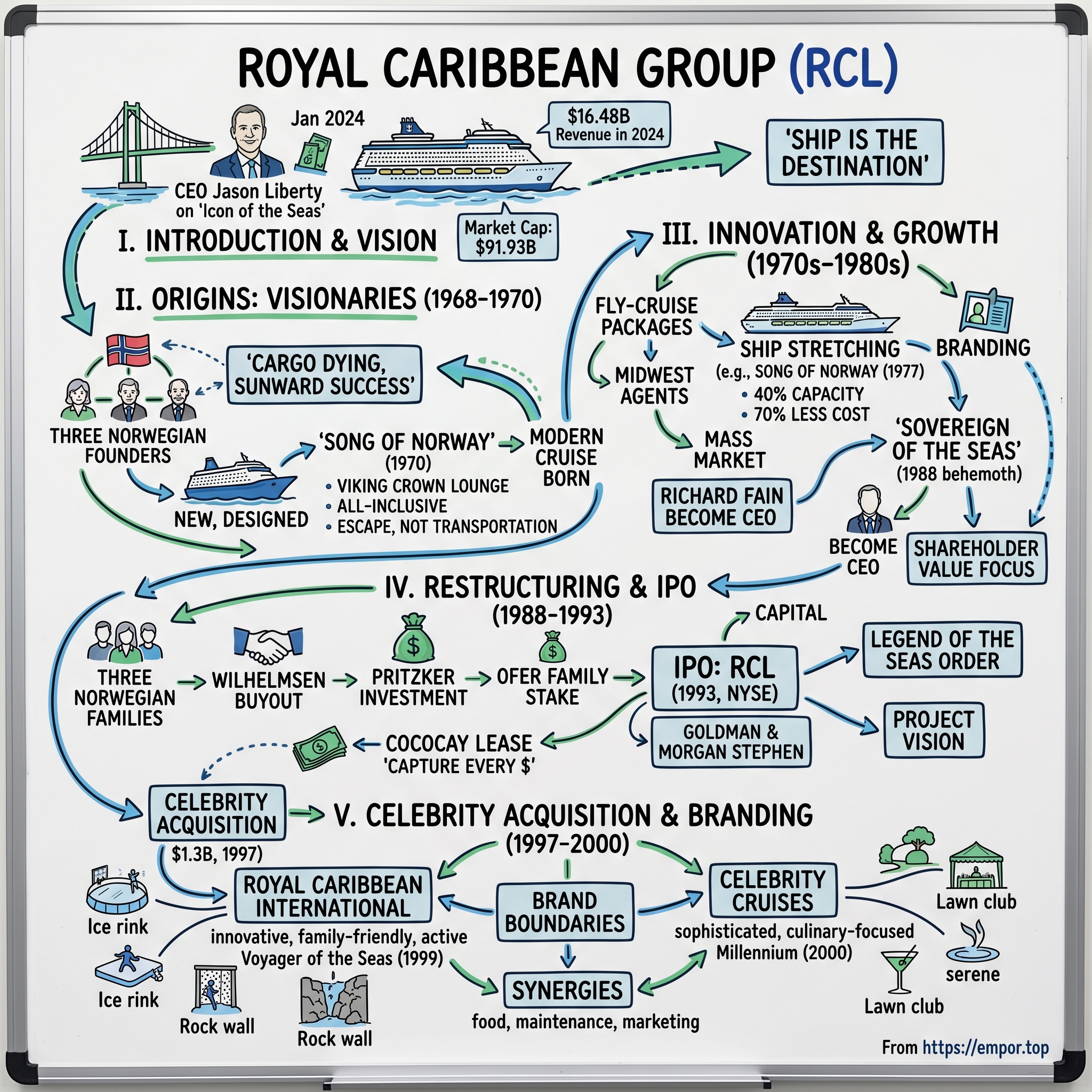

Picture this: It's January 2024, and Jason Liberty, CEO of Royal Caribbean Group, stands on the bridge of Icon of the Seas—the world's largest cruise ship—as it prepares for its maiden voyage. At 1,198 feet long and weighing 250,800 gross tons, this floating city can carry nearly 10,000 people including crew. It has the world's largest waterpark at sea, seven swimming pools, and more restaurants than many small towns. The ship cost $2 billion to build, yet it will pay for itself in less than five years. Liberty looks out at the Miami skyline and reflects on a remarkable fact: his company just posted $16.48 billion in revenue for 2024, surpassing pre-pandemic levels with fewer ships operating.

This is the story of Royal Caribbean Group—a $91.93 billion market cap empire that emerged from three Norwegian shipping companies with a radical idea: what if cruising wasn't about getting somewhere, but about the journey itself? What if the ship was the destination?

Today, Royal Caribbean Group operates 65 ships across three luxury brands, employs over 100,000 people, and has fundamentally reimagined what a vacation can be. They've built floating cities with ice rinks, surf simulators, and Central Park replicas. They've acquired private islands and transformed them into exclusive destinations that generate hundreds of millions in pure profit. They've survived existential crises—from 9/11 to the 2008 financial crisis to COVID-19—emerging stronger each time.

But here's what's truly remarkable: in an industry where ships cost billions and take years to build, where a single outbreak can shut down operations, where fuel costs and environmental regulations constantly squeeze margins, Royal Caribbean has consistently out-innovated, out-executed, and out-earned its competitors. Their secret? A relentless focus on innovation, a multi-brand strategy that captures every segment of the market, and perhaps most importantly, an understanding that they're not really in the cruise business—they're in the memory-making business.

This episode explores three fundamental tensions that define Royal Caribbean's journey. First, the innovation paradox: how do you justify spending $2 billion on experimental features when shareholders demand returns? Second, the scale challenge: how do you maintain intimacy and personal service when you're hosting 7,000 guests at once? And third, the resilience test: how do you build a business that can survive when your entire industry can be shut down overnight?

As we'll discover, the answers to these questions have created one of the most fascinating business stories of our time—a tale of Norwegian pragmatism meeting American ambition, of engineering marvels floating on economic models, and of a company that turned the simple act of going on vacation into a $150 billion global industry.

II. Origins: Three Norwegians and a Vision (1968–1970)

The conference room at the Norge Hotel in Oslo was thick with cigarette smoke on that November morning in 1968. Three men sat around a mahogany table, each representing shipping dynasties that had survived Nazi occupation, post-war reconstruction, and the brutal cycles of the freight business. Anders Wilhelmsen, the soft-spoken heir to a century-old shipping empire, spread out blueprints across the table. Sigurd Skaugen, whose family company I.M. Skaugen had been moving cargo since 1920, leaned forward to examine them. Across from them sat Harry Gotaas, representing Gotaas Larsen, already one of Norway's largest tanker operators.

"Gentlemen," Wilhelmsen began in his measured English, "the cargo business is dying."

It was a stark admission from men whose families had built fortunes moving oil, grain, and goods across the world's oceans. But the numbers didn't lie. Containerization was revolutionizing shipping, squeezing margins for traditional operators. Air travel had killed the transatlantic passenger business—the Queen Mary and Queen Elizabeth were already being retired. Meanwhile, something curious was happening in Miami: a Greek shipping magnate named Ted Arison was making money—real money—sailing tourists to the Caribbean on converted cargo ships.

The three Norwegians had each noticed the same trend independently. The post-war boom had created a new American middle class with disposable income and paid vacation time. Jet travel meant people could fly to Florida easily. The Caribbean offered year-round sunshine just a day's sail away. Yet the cruise industry, such as it existed, was still stuck in the past—formal, stuffy, expensive, and focused on transportation rather than entertainment.

Wilhelmsen pulled out a photograph from his briefcase. It showed Arison's ship, the Sunward, departing Miami packed with passengers. "Ted is using a converted car ferry," he said. "Imagine what we could do if we built ships specifically for this purpose."

The idea was radical. No one had ever built a ship designed from the keel up for warm-water cruising. Existing cruise ships were either aging ocean liners or hastily converted cargo vessels. They were designed for crossing the North Atlantic, with heavy hulls, small windows, and dark interiors. They carried lifeboats for abandoning ship, not pools for swimming.

Skaugen, the engineer of the group, was already sketching on a napkin. "Wide beam for stability in calm waters. Larger windows—no, floor-to-ceiling glass. More deck space, less cargo space. Design everything around the passenger experience, not maritime tradition."

But Gotaas raised the critical question: "Who's going to finance ships that only do one thing? A cargo ship can haul anything. A tanker can move oil anywhere. This ship you're proposing—it can only cruise tropical waters with tourists."

Wilhelmsen smiled. This was why they needed each other. Between the three companies, they had relationships with every major shipyard in Europe, decades of operating experience, and critically, access to Norwegian government shipping subsidies. Norway was desperately trying to maintain its shipbuilding industry against Asian competition. A new class of passenger vessels built in Norwegian yards would be politically popular.

They formed Royal Caribbean Cruise Line that day, each company taking an equal stake. The name itself was carefully chosen—"Royal" conveyed luxury and tradition, "Caribbean" specified their focus market, avoiding the Atlantic crossing business entirely. They would build three identical ships, one for each partner, sharing the risk and the rewards.

The first ship would be called Song of Norway, a name that honored their heritage while promising something new. The specifications they agreed on were revolutionary: accommodations for 700 passengers (massive for the time), an observation lounge with 360-degree windows placed high above the deck (inspired by Seattle's Space Needle, which Wilhelmsen had visited), air conditioning throughout (unheard of in European shipping), and most radically, a design philosophy that treated the ship as a destination, not transportation.

They hired a young naval architect named Njål Eide who had never designed a cruise ship—they wanted someone unencumbered by tradition. Eide spent six months in Miami, riding Arison's ships, talking to passengers, understanding what worked and what didn't. He came back with radical proposals: a pool deck that could host parties, not just swimming; dining rooms with windows, so passengers could watch the sunset while eating; cabins with private bathrooms (many ships still had shared facilities).

The Wärtsilä shipyard in Finland won the contract with a bid of $13.5 million per ship—about $100 million in today's dollars. Construction began in 1969, but the partners faced immediate skepticism. Carnival's Ted Arison publicly mocked them: "The Norwegians think they can run a Caribbean cruise line from Oslo? Good luck with that." Travel agents were confused: "Who wants to go on a cruise that doesn't go anywhere important?" Banks were nervous: "What if Americans don't want to cruise?"

But Wilhelmsen, Skaugen, and Gotaas had done their homework. They'd studied American vacation patterns, analyzed Miami's growth as a gateway city, and most importantly, understood something their competitors hadn't: the American middle class didn't want transportation—they wanted escape. They wanted to feel rich for a week. They wanted service, sunshine, and stories to tell when they got home.

Song of Norway launched on November 7, 1970, sliding into the water at the Wärtsilä shipyard as a band played both Norwegian and American anthems. Edwin Stephan, whom they'd hired away from Arison to run operations, stood on the dock and reportedly said, "She's beautiful. Now we just have to hope Americans agree."

The ship featured innovations that would define the industry: the Viking Crown Lounge, a glass-wrapped observation deck that became Royal Caribbean's signature; a pool deck designed for parties, not just swimming; and bright, airy interiors that felt more like a resort than a ship. But the real innovation was the business model: seven-day cruises, Saturday to Saturday, allowing working Americans to use just one week of vacation; all-inclusive pricing that made budgeting simple; and ports of call chosen for their beaches and shopping, not their historical significance.

When Song of Norway arrived in Miami for the first time in November 1970, she carried something more than just passengers—she carried the blueprint for an entirely new industry. The modern cruise vacation was born.

III. Building the Foundation: Innovation & Growth (1970s–1980s)

Edwin Stephan stood at the Port of Miami on a humid Saturday morning in July 1971, watching Song of Norway return from her 32nd voyage. Every cabin was full—again. The ship had been profitable from her third sailing, exceeding even the most optimistic projections. But Stephan, the former Commodore Cruise Lines executive whom Royal Caribbean had poached to run their operations, saw problems brewing. Three couples had just stormed off the ship, furious that they couldn't get dinner reservations at the restaurant they wanted. The pool deck, designed for 400 people, regularly held 600. The Viking Crown Lounge, the ship's signature feature, had lines to enter by sunset.

"We're victims of our own success," Stephan told the Norwegian owners on their next conference call. "We need more capacity, and we need it now."

The second ship, Nordic Prince, was already under construction in Finland, but she wouldn't arrive until November. The third ship, Sun Viking, wasn't due until 1972. Meanwhile, Carnival had noticed Royal Caribbean's success and was rapidly expanding. Norwegian Caribbean Line (later NCL) was entering the market. The land grab for Caribbean cruise dominance was on.

Nordic Prince arrived in Miami on November 19, 1971, but her real innovation wasn't visible from the outside. Royal Caribbean had partnered with airlines to create something unprecedented: fly-cruise packages. For one price, a family in Minneapolis could buy airfare to Miami, transfers to the ship, and their cruise. It seems obvious now, but in 1971, it was revolutionary. The cruise was no longer limited to people who lived within driving distance of Miami or could afford separate airfare.

The impact was immediate. Nordic Prince's first-year load factors exceeded 95%. Travel agents in the Midwest, who had never sold cruises before, suddenly had a product their customers could actually buy. Royal Caribbean's marketing chief, Rod McLeod, later recalled: "We went from competing for Florida tourists to competing for every vacation dollar in America."

But the real genius move came in 1972 with Sun Viking. The ship itself was evolutionary, not revolutionary—slightly larger, slightly more refined. But Royal Caribbean did something unprecedented: they painted all three ships in identical livery and marketed them as a fleet. Same white hulls, same blue trim, same Viking Crown Lounge silhouette. A Royal Caribbean ship became instantly recognizable, even from miles away. It was branding at a scale the cruise industry had never seen.

By 1973, the company faced a classic entrepreneurial dilemma: demand far exceeded supply, but new ships took three years to build and cost tens of millions of dollars. During a board meeting in Oslo, Njål Eide, the naval architect who had designed the original ships, proposed something audacious: "What if we cut Song of Norway in half and add a new section in the middle?"

The room went silent. Ships had been lengthened before, but never passenger ships in active service. The engineering challenges were staggering. The financial risks were enormous—Song of Norway would be out of service for months, losing millions in revenue. If something went wrong, they could lose the ship entirely.

But the math was compelling. For $15 million and six months of downtime, they could add 85 feet to Song of Norway, increasing her capacity by 40%. A new ship would cost $50 million and take three years. Wilhelmsen, ever the calculated risk-taker, approved the plan.

On September 15, 1977, Song of Norway sailed into the Wärtsilä shipyard in Finland. Over the next six months, in what observers called "the most ambitious ship surgery ever attempted," workers cut the ship in half, pulled the sections apart, and inserted a prefabricated 85-foot section containing 113 new cabins, expanded dining facilities, and additional public spaces. The engineering precision required was extraordinary—the cuts had to be accurate to millimeters, the new section had to perfectly match the ship's systems, and everything had to be watertight.

When Song of Norway returned to service in March 1978, she was 40% larger but had cost 70% less than a new ship and taken 80% less time. The stretching was so successful that Royal Caribbean immediately scheduled Nordic Prince for the same procedure. The company had invented a new way to grow capacity, and competitors took notice. Within five years, ship stretching became standard industry practice.

But Royal Caribbean's real innovation in this period wasn't engineering—it was market positioning. While Carnival pitched itself as the "Fun Ships" for young people and Holland America maintained its formal, elderly clientele, Royal Caribbean carved out the middle: families who wanted quality but not stuffiness, fun but not chaos. Their marketing tagline, "We're Different Out Here," wasn't just advertising—it was strategy.

The numbers tell the story. In 1970, approximately 500,000 Americans took a cruise. By 1980, that number had grown to 1.4 million, with Royal Caribbean carrying nearly 200,000 of them. The company's revenues had grown from essentially zero to over $200 million. But more importantly, they had proven that cruising could be mass market while maintaining premium pricing.

The decade culminated with two massive bets. First, in 1982, Royal Caribbean launched Song of America, at 37,000 tons the third-largest passenger vessel afloat. She featured the industry's first fully computerized navigation system, a shopping mall at sea, and a theater that could stage Broadway-style shows. The ship cost $140 million—more than the company's entire revenue just three years earlier.

Second, and more audaciously, in 1988 they launched Sovereign of the Seas, a 73,000-ton behemoth that was literally too big for most ports. She had the industry's first open atrium (rising through five decks), glass elevators, and a casino that rivaled anything in Las Vegas. At $185 million, she represented a bet-the-company moment.

The risk paid off spectacularly. Sovereign of the Seas wasn't just bigger—she redefined what a cruise ship could be. She proved that passengers would pay premium prices for innovative amenities. She established Royal Caribbean as the industry's innovation leader, a position they've never relinquished.

But the biggest change came in April 1988, when the board named Richard Fain as Chairman and CEO. Fain, a former investment banker who had married into the Wilhelmsen family, brought a Wall Street sensibility to what had been a Norwegian shipping company. His first board meeting set the tone: "Gentlemen, we're not in the shipping business. We're in the shareholder value creation business. And that means we need to think bigger than anyone has thought before."

The age of financial engineering was about to begin. The family-owned Norwegian shipping company was about to transform into a publicly traded American corporation. And the cruise industry would never be the same.

IV. The Ownership Restructuring & Going Public (1988–1993)

Richard Fain's corner office at the newly built Royal Caribbean headquarters in Miami was sparse by CEO standards—a desk, two chairs, and a whiteboard that covered an entire wall. On this particular morning in October 1988, that whiteboard was covered with a complex web of boxes, arrows, and numbers that would make an investment banker dizzy. Fain, still adjusting to his new role as CEO, was explaining to his CFO the existential challenge they faced.

"We have three Norwegian families who each own a third of this company," Fain said, pointing to three boxes at the top of his diagram. "Skaugen wants out completely—they need capital for their tanker business. Gotaas Larsen is happy to sell if the price is right. Only the Wilhelmsens want to stay in for the long term. But here's the problem: we need $600 million in the next five years to build new ships, or Carnival is going to eat us alive."

The cruise industry in 1988 was at an inflection point. Carnival had just gone public, raising $400 million to fund new construction. Norwegian Caribbean Line was building larger ships. Costa and MSC were expanding from Europe. The arms race for bigger, better ships was accelerating, and Royal Caribbean's ownership structure—a three-way partnership between Norwegian shipping families—was becoming a liability.

Fain had married Luisa Wilhelmsen, daughter of Anders Wilhelmsen, which gave him unique insight into the ownership dynamics. He knew that while the Wilhelmsen family believed in the cruise business's long-term potential, they couldn't fund expansion alone. They needed partners with deeper pockets and patience for a capital-intensive business with long-term payoffs.

The first move came in December 1988. In a series of complex transactions orchestrated by Fain and his investment banking contacts, the Wilhelmsen family bought out both Skaugen and Gotaas Larsen for approximately $230 million, funded largely by debt. For a brief moment, Royal Caribbean was wholly owned by a single Norwegian family. But this was always intended as a temporary state.

"We had maybe six months of runway," Fain later recalled. "The debt service alone was crushing us, and we had already committed to building three new ships. We needed equity partners, fast."

Enter the Pritzker family of Chicago, owners of Hyatt Hotels and one of America's wealthiest dynasties. Jay Pritzker had been watching the cruise industry with interest. He understood hospitality, he understood capital-intensive businesses, and most importantly, he understood that cruising was about to explode. In March 1989, after three months of negotiations, the Pritzkers bought 50% of Royal Caribbean for $515 million.

But the deal structure was ingenious. Rather than a simple equity purchase, they created a new holding company, Royal Caribbean Cruises A/S, registered in Liberia for tax efficiency. The Wilhelmsens retained 50%, the Pritzkers got 50%, but operational control remained with management—essentially, with Fain. It was a structure that balanced Norwegian heritage with American capital, family ownership with professional management.

The Pritzker capital immediately went to work. Royal Caribbean ordered its first true mega-ship, Monarch of the Seas, for delivery in 1991. They also did something unprecedented: they bought an island. Well, technically, they leased it. Little Stirrup Cay in the Bahamas, renamed CocoCay, became Royal Caribbean's private destination. For $10 million plus annual lease payments, they had exclusive access to a tropical paradise where they controlled every aspect of the guest experience—and captured every dollar spent.

The CocoCay deal, negotiated personally by Fain with the Bahamian government, was transformative. "We realized that we were giving away tremendous value by taking passengers to ports where they spent money on shore," Fain explained to the board. "At our own island, every drink, every beach chair, every jet ski rental—that revenue comes to us."

In 1990, with Pritzker capital and confidence, Royal Caribbean made another strategic acquisition: Admiral Cruises. The small Miami-based operator had just two ships, but they came with something invaluable: established Latin American marketing channels and Spanish-speaking crew networks. The Nordic Empress and Viking Serenade were immediately integrated into the Royal Caribbean fleet, but more importantly, the company gained access to the rapidly growing Latin American cruise market.

But even with Pritzker capital, Fain knew they needed more. Carnival's market cap was approaching $3 billion. Their new Fantasy-class ships were revolutionary. Royal Caribbean needed access to public markets, but the ownership structure made it complicated. The Wilhelmsens didn't want to give up control. The Pritzkers wanted liquidity options. And Fain needed growth capital.

The solution came from an unexpected source: the Ofer family of Israel. Sammy Ofer, a shipping magnate who controlled one of the world's largest tanker fleets, had been quietly buying Royal Caribbean bonds. In 1992, he approached Fain with a proposal: he would buy a stake from both the Wilhelmsens and Pritzkers, providing them partial liquidity while keeping the company private. More importantly, he would support a public offering within two years.

The deal closed in September 1992. The new ownership structure was complex but elegant: Wilhelmsen 34%, Pritzker 33%, Ofer 33%. Each family had equal board representation, but operational control remained with management. More importantly, all three families agreed to support an IPO in 1993.

The IPO preparation was a masterclass in financial engineering. Goldman Sachs and Morgan Stanley were hired as lead underwriters. The company was restructured from a Liberian holding company to a Delaware corporation. Complex inter-company agreements were unwound. The fleet was re-flagged to more investor-friendly jurisdictions.

But the real work was in positioning the story. This wasn't just a cruise company going public—this was a growth story. Fain and his team crafted a narrative around three pillars: innovation leadership (backed by patents on ship designs), operational excellence (industry-leading customer satisfaction scores), and expansion potential (the North American cruise market was still less than 2% penetrated).

On April 27, 1993, Royal Caribbean Cruises Ltd. began trading on the New York Stock Exchange under the symbol RCL. The IPO raised $310 million at $14 per share, valuing the company at $1.4 billion. The three founding families retained 62% ownership, ensuring control while accessing growth capital.

The first day of trading was volatile. The stock opened at $15.50, peaked at $16.25, and closed at $15.125. Fain watched from the NYSE floor, surrounded by the Norwegian, American, and Israeli families who had made this moment possible. "We're not just a public company now," he told them. "We're accountable to thousands of shareholders who expect us to grow. And grow we will."

The IPO proceeds were immediately deployed. Royal Caribbean ordered Legend of the Seas and Splendour of the Seas, each costing over $300 million. They announced plans for Project Vision—six identical ships that would revolutionize cruising with features like miniature golf courses, rock climbing walls, and specialty restaurants.

By the end of 1993, Royal Caribbean had transformed from a private Norwegian shipping partnership to a publicly traded multinational corporation. The company's revenue had grown to $1.2 billion. The fleet had expanded to eight ships. And most importantly, they had the capital structure to compete with anyone.

The transformation set the stage for what would come next: a period of aggressive expansion, strategic acquisitions, and innovations that would redefine not just Royal Caribbean, but the entire cruise industry. The family shipping company was dead. The modern cruise corporation was born.

V. The Celebrity Acquisition & Brand Building (1997–2000)

John Chandris was not a man who showed emotion easily. The Greek shipping heir, whose family had built Celebrity Cruises from nothing into the industry's most prestigious premium brand, sat stone-faced in the mahogany-paneled boardroom of Citibank's Manhattan offices on March 15, 1997. Across from him, Richard Fain was making his final offer: $1.3 billion in cash and stock for Celebrity Cruises. It was 10 p.m., they'd been negotiating for fourteen hours, and both men knew this was the number that would make or break the deal.

"John," Fain said quietly, "your father built something beautiful. We want to preserve it, not destroy it. Celebrity will remain Celebrity. But together, we can dominate premium cruising."

Chandris finally spoke: "My father always said, 'Ships are just steel and engines. Brands are what customers buy.' If you destroy our brand, you destroy everything we built."

This tension—between acquisition and preservation, between synergy and autonomy—would define not just this deal but Royal Caribbean's entire multi-brand strategy.

Celebrity Cruises was the anti-Carnival. Where Carnival was mass-market fun, Celebrity was refined elegance. Their ships featured original artwork, sommelier-selected wine lists, and restaurants designed by James Beard Award winners. Their passengers were older, wealthier, and more traveled. Their crew-to-passenger ratio was the industry's highest. Everything about Celebrity screamed premium.

But premium came at a cost. Celebrity's five ships were expensive to operate and struggling to fill at the prices needed to maintain their luxury positioning. The company was caught in the classic premium trap: too expensive for mass market, not luxurious enough for true luxury. Chandris knew they needed scale to survive, but selling to a mass-market operator felt like betrayal.

Fain had been courting Chandris for two years. He understood that Royal Caribbean's future wasn't in building bigger versions of the same ship—it was in segmentation. "Look at the hotel industry," he told his board. "Marriott has Ritz-Carlton, Courtyard, and Residence Inn. Different brands for different customers, but shared back-office, purchasing power, and distribution. We need to do the same."

The deal structure was complex. Royal Caribbean would pay $515 million in cash and $785 million in stock, but the Chandris family would retain a 20% stake in the combined company and two board seats. More importantly, Celebrity would maintain its own headquarters, its own brand identity, and its own management team. It was an acquisition designed to feel like a merger.

When the deal closed on July 30, 1997, Royal Caribbean Cruises Ltd. controlled two distinct brands with twelve ships and a combined market value of $5 billion. But the real work was just beginning. How do you integrate operations without homogenizing brands? How do you achieve synergies without destroying what made each brand special?

The answer came from an unexpected source: Procter & Gamble. Fain hired several P&G brand managers who had experience managing distinct brands in the same category. They implemented a strategy called "brand boundaries"—clear rules about what each brand could and couldn't do.

Royal Caribbean would be innovative, family-friendly, and active. Their ships would have rock walls, ice rinks, and surf simulators. Their marketing would feature families and young couples. Their price point would be premium-mass.

Celebrity would be sophisticated, culinary-focused, and serene. Their ships would have real grass lawns, hot glass shows, and canyon ranches. Their marketing would feature empty nesters and affluent couples. Their price point would be premium-plus.

The boundaries were enforced religiously. When Royal Caribbean wanted to add a specialty restaurant, it had to be a steakhouse or Italian—accessible cuisines. When Celebrity added one, it could be French or molecular gastronomy. When Royal Caribbean built bars, they were sports bars or English pubs. Celebrity built martini bars and wine towers.

But behind the scenes, the synergies were massive. Combined purchasing power reduced food costs by 15%. Shared dry-docking facilities cut maintenance expenses by 20%. Joint marketing in travel agencies increased both brands' visibility. Most importantly, the companies could share innovations while maintaining distinct applications.

The strategy's first test came with the launch of Mercury in November 1997, Celebrity's first new ship under Royal Caribbean ownership. The ship was pure Celebrity—museum-quality art, a two-story specialty restaurant, a spa that rivaled land-based resorts. But hidden in the technical specifications were Royal Caribbean innovations: propulsion systems from Sovereign of the Seas, navigation technology from Rhapsody of the Seas, and waste management systems that would later appear on Voyager of the Seas.

Meanwhile, Royal Caribbean was preparing its own revolution. Project Eagle, later renamed Voyager of the Seas, was under construction in Finland. At 137,000 tons, she would be the world's largest cruise ship. But size wasn't the innovation—the amenities were. Royal Caribbean had decided to put an ice rink on a ship. Not a synthetic rink, not a small rink, but a full-sized, NHL-regulation ice rink in the middle of the Caribbean.

"Everyone thought we were insane," recalled Peter Whelpton, Royal Caribbean's head of guest experience. "The engineering challenges alone were staggering. You're putting a giant block of ice on a ship that moves, in tropical waters, with 3,000 people generating heat around it. The power requirements, the stability issues, the sheer audacity of it—our competitors were literally laughing at us."

But Fain understood something his competitors didn't: Royal Caribbean wasn't competing with other cruise lines anymore. They were competing with Orlando, Las Vegas, and all-inclusive resorts. The ice rink wasn't about ice skating—it was about creating moments of wonder, Instagram-worthy experiences before Instagram existed.

Voyager of the Seas launched on May 21, 1999, from Helsinki. She featured not just the ice rink but the industry's first rock climbing wall, a miniature golf course, and the Royal Promenade—a 445-foot shopping mall with sidewalk cafes, bars, and parades. The ship redefined what was possible at sea.

The impact was immediate and industry-changing. Travel agents reported that customers were booking Royal Caribbean specifically for the ice shows. Families who had never considered cruising were suddenly interested. The rock climbing wall became the most photographed feature on any cruise ship. Voyager's first year operated at 112% capacity (achieved through triple and quad occupancy of cabins).

Celebrity, meanwhile, launched Millennium in June 2000, featuring the industry's first lawn club at sea—real grass where passengers could play croquet or have picnics. It was a perfect illustration of the brand strategy: both lines innovating, but in completely different directions.

By the end of 2000, the multi-brand strategy was validated. Royal Caribbean International (renamed from Royal Caribbean Cruise Line to emphasize the global nature) generated $2.1 billion in revenue with an average ticket price of $1,450. Celebrity generated $800 million with an average ticket price of $2,100. The brands were attracting different customers, commanding different prices, and yet sharing billions in costs.

The Celebrity acquisition had transformed Royal Caribbean from a one-brand cruise line into a multi-brand vacation company. It established a template for future acquisitions and proved that in cruising, like in consumer goods, portfolio strategies could work. But most importantly, it positioned Royal Caribbean for the next phase of growth: the race to build the biggest, most innovative ships the world had ever seen.

VI. The Innovation Arms Race: Freedom & Oasis Classes (2000s–2010s)

The napkin sketch was crude but revolutionary. Harri Kulovaara, Royal Caribbean's executive vice president of maritime operations, had drawn what looked like a child's interpretation of a ship—if that child was imagining a floating city with neighborhoods. It was April 2003, and Kulovaara was sitting in a Miami restaurant with Richard Fain and a handful of senior executives, planning what would become the most audacious shipbuilding project in history.

"Forget everything you know about ship design," Kulovaara said, his Finnish accent thickening with excitement. "What if we didn't build a ship with amenities? What if we built neighborhoods that happened to be on a ship?"

The sketch showed seven distinct areas: a boardwalk with a carousel, a Central Park with real trees, a sports zone, an entertainment district, a spa vitality area, a pool zone, and a youth zone. Each would have its own character, its own vibe, its own reason to exist. It was urban planning meets naval architecture.

Fain studied the napkin, then looked up. "How big would this thing need to be?"

"Bigger than anything ever built," Kulovaara replied. "Maybe 220,000 tons. Maybe more."

For context, Royal Caribbean's Freedom of the Seas, launching in 2006 as the world's largest cruise ship, was 154,000 tons. Kulovaara was proposing something 50% larger. The engineering challenges were staggering. The economics were uncertain. The risk was existential—if they built it and passengers didn't come, it could bankrupt the company.

But before they could build Kulovaara's dream, they had to launch Freedom of the Seas. She represented everything Royal Caribbean had learned about innovation, but packaged in a more evolutionary way. The ship featured the cruise industry's first surf simulator—the FlowRider—a $2 million piece of equipment that created an endless wave. It had a full-sized boxing ring, a cantilevered whirlpool extending twelve feet beyond the side of the ship, and the H2O Zone aqua park with water cannons and spray fountains.

"The FlowRider almost didn't happen," recalled Adam Goldstein, then president of Royal Caribbean International. "The insurance companies were terrified. The lawyers were terrified. The board asked, 'What happens when someone breaks their neck?' But we knew that if we wanted to attract younger cruisers, we needed to offer experiences they couldn't get on a Carnival ship."

Freedom of the Seas launched from Oslo on April 12, 2006. The media coverage was unprecedented. ESPN broadcast from the FlowRider. The Today Show did a week of broadcasts from the ship. Travel Weekly called it "the ship that changes everything." First-year bookings exceeded 105% capacity.

But Carnival wasn't standing still. Their Conquest class ships were proving that bigger was better for yields. Costa Concordia was under construction in Italy. The entire industry was in an arms race for size and spectacle. Royal Caribbean needed something that would leap so far ahead that competitors couldn't catch up for a decade.

The board meeting to approve Project Genesis (later renamed Oasis of the Seas) was held in October 2004. The numbers were staggering: $1.4 billion construction cost, 225,282 gross tons, capacity for 6,296 passengers and 2,394 crew. It would be 40% larger than Freedom of the Seas and cost twice as much. The board was skeptical.

"Gentlemen," Fain said, addressing the predominantly male board, "we're not building a ship. We're building a destination. When this ship is in Port Everglades, it will be the tallest structure in Fort Lauderdale. When it's in Cozumel, it will have more restaurants than the entire port. This isn't transportation—it's a resort that happens to float."

The vote was closer than expected: 7-4 in favor. Construction began at STX Europe's Turku shipyard in Finland in 2007. But almost immediately, problems emerged. The ship was so large that traditional design software couldn't handle it. STX had to develop entirely new 3D modeling systems. The Central Park concept—2,700 live plants including full-grown trees—required collaboration with landscape architects who had never worked on ships. The boardwalk carousel had to be engineered to remain level despite the ship's movement.

Then the financial crisis hit.

By October 2008, with Lehman Brothers collapsed and credit markets frozen, Royal Caribbean's stock had fallen from $45 to $8. The company had $8 billion in debt. Oasis of the Seas was consuming $50 million per month in construction costs. Competitors were canceling ship orders. Industry observers were predicting Royal Caribbean's bankruptcy.

"Those were the darkest days," CFO Brian Rice later recalled. "We had this massive ship under construction that we couldn't cancel, our bookings were collapsing, and the credit markets were essentially closed to us. We were burning through cash reserves just to stay alive."

But Fain made a counterintuitive decision: accelerate innovation. "When everyone else is retreating, that's when you advance," he told the board. He authorized completion of not just Oasis but her sister ship, Allure of the Seas. He negotiated with STX to defer some payments but keep construction on schedule. Most audaciously, he maintained pricing rather than slash rates like competitors.

Oasis of the Seas was delivered on October 28, 2009, in the depths of the recession. The christening ceremony in Fort Lauderdale was surreal—a celebration of excess in an era of austerity. Media coverage was mixed. The New York Times called it "a monument to pre-crash excess." The Wall Street Journal wondered if it was "the ship that sank Royal Caribbean."

Then something unexpected happened: it sold out. Not just the inaugural sailing, but the entire first year. In the middle of the worst recession since the 1930s, people were paying premium prices to experience Central Park at sea, to ride the boardwalk carousel, to watch Broadway shows in a 1,350-seat theater that rivals land-based venues.

The ship's first-year financial performance exceeded all projections. Revenue per passenger was 20% higher than Freedom class. Guest satisfaction scores hit company records. Most importantly, 40% of passengers were first-time cruisers—Oasis wasn't stealing share from competitors; it was growing the entire market.

Meanwhile, Royal Caribbean's Quantum class was in development, representing a different kind of innovation. Where Oasis was about size and neighborhoods, Quantum was about technology and flexibility. The ships featured North Star, a glass observation capsule that rose 300 feet above sea level. They had RipCord by iFly, a skydiving simulator. They had Two70, a multi-level entertainment venue with floor-to-ceiling windows that transformed into projection screens.

But the real innovation was behind the scenes. Quantum ships were the first to be designed entirely in 3D, allowing for modular construction that reduced build time by 20%. They featured dynamic dining—no fixed seating times or assigned restaurants. They had virtual balconies in interior cabins, using real-time video feeds to give every room an ocean view. They were 20% more fuel-efficient than Freedom class despite offering more amenities.

The competition between Royal Caribbean and Carnival during this period was fierce but pushed both companies to new heights. Carnival's Dream class ships were beautiful and efficient. Norwegian's Breakaway class introduced Broadway partnerships. But Royal Caribbean's innovation leadership was undeniable. They had the biggest ships (Oasis class), the most technologically advanced ships (Quantum class), and the most innovative private destination.

That destination was Perfect Day at CocoCay. In 2016, Royal Caribbean announced a $200 million renovation of their private island. This wasn't just adding some beach chairs and a bar. They were building the tallest water slide in North America (Daredevil's Peak), a 1,600-foot zip line, a massive freshwater pool, and a helium balloon ride that soared 450 feet above the island.

"We realized that private destinations weren't just nice-to-haves—they were competitive weapons," explained Michael Bayley, president of Royal Caribbean International. "At CocoCay, we control everything. Every dollar spent goes to us. Every experience is branded by us. And most importantly, we can guarantee the experience in a way we can't at public ports."

By 2019, Perfect Day at CocoCay was generating over $300 million in annual revenue with margins exceeding 80%. It had become the most popular destination in Royal Caribbean's itineraries, with ships actually charging more for CocoCay sailings than traditional port-intensive routes.

The innovation arms race of the 2000s and 2010s transformed Royal Caribbean from a cruise line into an experience company. They proved that passengers would pay premium prices for unprecedented experiences. They demonstrated that innovation could drive both revenue and margins. Most importantly, they established a culture where the question wasn't "Can we do this?" but "How can we do this better than anyone imagined?"

But all of this innovation, all of this growth, all of this success would soon face its greatest test. A virus was spreading in Wuhan, China, and the cruise industry was about to confront an existential crisis that would make the 2008 financial crisis look like a minor setback.

VII. The COVID Crisis & Recovery (2020–2022)

Jason Liberty was standing in the lobby of Royal Caribbean's Miami headquarters at 7:30 a.m. on March 13, 2020, when the news broke. The Centers for Disease Control had just recommended that all Americans avoid cruise travel. Within hours, Royal Caribbean announced it would suspend operations for 30 days, starting with Saturday departures. Liberty, then the company's CFO, looked at his team gathered in the crisis room and delivered the stark reality: "We're about to burn through $250 to $275 million per month with zero revenue coming in. We have 26 ships at sea with 50,000 guests who need to get home. We have 60,000 crew members we need to figure out what to do with. And the capital markets are in freefall."

The speed of the collapse was breathtaking. On March 1, Royal Caribbean's ships were operating at full capacity, the stock was trading at $105, and the company was guiding to record earnings. By March 14, Royal Caribbean decided to suspend sailings of their fleet globally at midnight, expecting to return to service on April 11, 2020. By March 18, the stock had crashed to $19.25—an 82% decline in less than three weeks. The entire cruise industry had been brought to its knees by a virus most executives hadn't heard of two months earlier.

Richard Fain, the company's long-serving CEO, convened an emergency board meeting via Zoom—itself a novelty for the traditionally in-person board. "Gentlemen and ladies," he began, "we're facing an existential crisis. This crisis is the most difficult in the Company's history. Our entire business model—putting thousands of people in close quarters for entertainment—is now viewed as a public health threat. We need to raise capital, and we need to raise it now."

The numbers were terrifying. Monthly cash burn was estimated at approximately $250 million to $275 million during a prolonged suspension of operations. The company had about $3.7 billion in customer deposits that passengers would likely want refunded. Debt maturities of $400 million were due in 2020, with another $900 million in 2021. The math was simple: without new capital, Royal Caribbean would be bankrupt by summer.

But raising capital when your entire industry is viewed as toxic—literally—was nearly impossible. Banks that had eagerly financed ship construction six months earlier now wouldn't return calls. Bond investors demanded usurious rates. The company's debt was downgraded to junk status, triggering covenants that limited how much they could borrow.

Liberty and his finance team engineered one of the most creative capital raises in corporate history. In May 2020, Royal Caribbean secured $3.75 billion in additional debt, entering into a $2.35 billion, 364-day senior secured credit facility and obtaining an $800 million, 12-month debt amortization and financial covenant holiday on several export-credit backed facilities. They used a complex structure that gave investors security interests in specific ships without technically violating debt covenants. They guaranteed to investors on a senior unsecured basis a subsidiary that owned all of the equity interests in seven cruise ships, valued at about $7.7 billion.

During 2020, the Company raised approximately $9.3 billion of new capital through a combination of bond issuances, common stock public offerings and other loan facilities. The debt came at a steep price—interest rates as high as 11.5%, compared to the 3-4% they'd been paying pre-pandemic. Royal Caribbean's long-term debt load more than doubled from $8.4 billion at the end of 2019 to $18 billion at the end of 2020.

Meanwhile, the operational challenges were staggering. Ships couldn't just be parked—they needed constant maintenance, skeleton crews, and port fees. The company had to repatriate 60,000 crew members to over 100 countries, many of which had closed their borders. They negotiated with the CDC, the State Department, and health authorities in dozens of nations. Charter flights alone cost tens of millions.

The decision to keep ships in "warm layup"—maintaining them ready for quick restart rather than mothballing them—cost an extra $50 million per month but proved prescient. "We made a bet that this would end, and when it did, we wanted to be first back in the water," Liberty later explained.

By July 2020, in the middle of the crisis, Royal Caribbean completed its acquisition of the remaining shares of Silversea Cruises for $250 million—a deal that had been agreed to pre-pandemic. Many thought they were insane to close an acquisition while bleeding cash. But Fain saw opportunity: "Luxury cruising will come back first. Wealthy travelers will pay for safety and space."

The company also made the painful decision to sell assets. In March 2021, Royal Caribbean Group announced that its Azamara cruise brand would be sold to private-equity firm Sycamore Partners in a $201 million cash transaction, with the firm acquiring the three-ship fleet and all associated intellectual property. They also sold older ships like Majesty of the Seas and Empress of the Seas to Asian operators, generating precious cash.

The restart was agonizingly slow. The first Royal Caribbean ship to return to service was Quantum of the Seas in December 2020, sailing out of Singapore. These were "bubble cruises"—only Singapore residents, mandatory testing, no port stops, reduced capacity. It was barely profitable, but it proved cruising could be safe.

The real breakthrough came with vaccines. Royal Caribbean became one of the first cruise lines to mandate vaccinations for all passengers and crew. This decision was controversial—Florida's governor threatened to fine them for requiring vaccine passports—but it enabled them to restart operations months before competitors.

Freedom of the Seas conducted a simulated voyage from Miami in June 2021, marking the first time a cruise ship had departed a U.S. port with passengers in over 450 days. The emotional scenes of that departure—crew members crying, passengers cheering, executives barely maintaining composure—captured the industry's relief.

But challenges persisted. In June 2021, Royal Caribbean had to delay Odyssey of the Seas' inaugural voyage after eight crew members tested positive for COVID-19. All 1,400 crew members aboard had been vaccinated on June 4, the same day the ship arrived in Port Canaveral, but the positive cases sprang up before their vaccinations could be considered fully effective.

The Omicron variant in late 2021 triggered another crisis. In January 2022, Royal Caribbean had to cancel voyages on four ships, including Serenade of the Seas (sailings from January 8 to March 5), Jewel of the Seas (January 9 to February 12), and Symphony of the Seas (January 8 to January 22). Media coverage was brutal, with images of ships being turned away from ports and passengers quarantined in their cabins.

Through it all, Jason Liberty, who was named CEO in January 2022 after helping navigate the company through the pandemic's unprecedented challenges, maintained a steady hand. His finance background proved invaluable in managing the debt load, while his operational experience helped restart the fleet efficiently.

The company discovered something remarkable during the restart: pent-up demand was massive. Ships that resumed service were selling out at prices 10-15% higher than 2019 levels. Customers were booking suites and balconies instead of interior cabins. Onboard spending jumped 20%. The near-death experience had actually strengthened customer loyalty.

As Harvard Business School's Prof. Nitin Nohria later observed, "In my 35 years in this work, I've never seen a company come out of a crisis and completely lap the competition in such a way." By May 2022, for the first time since March 2020, all 26 Royal Caribbean ships were officially back in service.

The COVID crisis transformed Royal Caribbean in fundamental ways. It proved the resilience of the cruise model—that people's desire for escape and adventure couldn't be permanently suppressed. It accelerated digital transformation, with contactless check-in and app-based services becoming standard. It validated the importance of size and scale in surviving existential threats. Most importantly, it revealed that in the darkest moments, when the very existence of your industry is questioned, bold leadership and creative finance can mean the difference between bankruptcy and eventual triumph.

The company that emerged from COVID was leaner, more leveraged, but also more focused. They had proven they could survive the unthinkable. Now it was time to thrive.

VIII. The Remarkable Recovery & Record Performance (2023–2024)

Jason Liberty stood before a packed auditorium of Royal Caribbean employees in Miami on February 1, 2024, unable to suppress a smile. "Ladies and gentlemen," he began, "we just reported earnings per share of $6.31 for 2023. To put that in perspective, our previous record—set in 2019 before any of us had heard of COVID—was $9.54. Adjusted for the share count changes, we're essentially back. But here's the kicker: we did it with 10% less capacity operating."

The numbers were staggering. Total revenues were $13.9 billion, Net Income was $1.7 billion or $6.31 per share, Adjusted Net Income was $1.8 billion or $6.77 per share, and Adjusted EBITDA was $4.5 billion. For a company that just three years earlier was burning through a quarter-billion dollars monthly with zero revenue, it was a resurrection story for the ages.

The recovery wasn't just about returning to previous levels—it was about discovering that the business was fundamentally stronger than anyone had imagined. During the dark days of 2020, when ships were laid up and crews were stranded, Royal Caribbean's leadership made several contrarian bets that were now paying off spectacularly.

First, they kept their ships in warm layup rather than cold storage, maintaining them ready for quick restart. This cost an extra $50 million per month but meant they could return to service faster than competitors. Second, they maintained their newbuild orders when others were canceling, betting that post-pandemic demand would explode. Third, and most controversially, they raised prices rather than discounting to fill ships.

"We discovered something during the restart that changed everything," Liberty explained to investors during the Q4 2023 earnings call. "Demand for our brands continues to outpace broader travel as a result of consumer spend further shifting toward experiences and the exceptional value proposition of our products."

The pricing power discovery was the real revelation. In 2019, Royal Caribbean's average ticket price was around $1,500. By late 2023, it was approaching $2,000. Onboard spending, historically growing at 3-4% annually, was up 20%. Suite bookings, which commanded prices 3-4x higher than standard cabins, were selling out first. The customer wasn't just coming back—they were coming back richer, more eager, and willing to pay more.

Icon of the Seas, launching in January 2024, embodied this new reality. At a construction cost of $2 billion, it was the most expensive cruise ship ever built. It featured the world's largest waterpark at sea, seven swimming pools, 40 restaurants and bars, and neighborhoods that included an actual park with living trees. The ship's 7,600-passenger capacity made it a floating city larger than most American towns.

Critics called it excessive, a monument to pre-pandemic excess launching into an uncertain world. But Icon's first-year bookings told a different story: the ship was completely sold out through 2024 at prices 30% higher than any Royal Caribbean ship had previously commanded. The Presidential Suite, priced at $50,000 per week, had a waiting list.

The transformation of Perfect Day at CocoCay from a nice beach stop to a profit engine was equally remarkable. The $250 million investment in 2019 to add the tallest water slide in North America, a massive freshwater pool, and the Up, Up and Away helium balloon ride had seemed risky. By 2023, CocoCay was generating over $300 million in annual revenue with margins exceeding 80%. Passengers were spending an average of $150 per person on the island—double what they spent at traditional ports.

But the real strategic masterstroke was the debt refinancing orchestrated by Liberty and CFO Naftali Holtz. "Our accelerated performance and commitment to strengthening the balance sheet allowed us to pay off approximately $4 billion of debt in 2023 and significantly reduce leverage consistent with our Trifecta goal of returning to investment grade metrics." They refinanced high-cost pandemic debt at lower rates, extended maturities, and even got credit rating upgrades from S&P and Moody's.

The "Trifecta" goals Liberty referenced had been set in 2022 as seemingly impossible stretch targets: achieve EBITDA per available passenger cruise day (APCD) of over $100, return on invested capital (ROIC) in the teens, and return to investment grade credit metrics. The company expected to hit them by 2025. They achieved the first two in 2024, a year early.

By the time 2024 results were announced in January 2025, the transformation was complete. Total revenues were $16.5 billion, Net Income was $2.9 billion or $10.94 per share, Adjusted Net Income was $3.2 billion or $11.80 per share, and Adjusted EBITDA was $6.0 billion. The company had grown revenues by 18.6% year-over-year while only adding 8% capacity. The math was simple but powerful: pricing and onboard spending were driving massive operational leverage.

The stock market's reaction was even more dramatic. RCL shares rose to $265 after the January 2025 earnings call, up from the stock's pandemic low point of just over $19 on March 18, 2020. RCL has since traded as high as $355.91, on July 23. The company's market capitalization had grown from under $4 billion at the pandemic's nadir to over $90 billion—a 20x-plus increase that made it one of the best-performing stocks in the entire market.

What made the recovery even more remarkable was how it was achieved. This wasn't a story of cost-cutting and financial engineering. Royal Caribbean was investing more than ever. Capital expenditures for 2024 were $3.4 billion. They were building new ships, developing new private destinations, and installing new technology across the fleet. The company was simultaneously paying down debt, investing in growth, and generating record profits.

The technology investments were particularly prescient. A partnership with SpaceX's Starlink in 2022 brought high-speed internet to the entire fleet, transforming the at-sea experience. App-based check-in, dining reservations, and onboard purchases reduced friction and increased spending. Dynamic pricing algorithms optimized revenue in real-time. The company that had once been a traditional cruise line was becoming a technology-enabled hospitality platform.

Competition remained fierce. Carnival, under new CEO Josh Weinstein, was executing its own turnaround. Norwegian was building new ships and expanding its private island offerings. Virgin Voyages was attracting younger cruisers with its adults-only concept. But Royal Caribbean's scale, innovation pipeline, and operational excellence created a moat that seemed to widen rather than narrow.

The international expansion was another growth driver. While North America remained the core market, contributing 64% of revenue, international source markets were exploding. China, despite COVID-related delays, was showing signs of reopening to cruising. European demand was surging. Latin American markets were growing at double-digit rates. Royal Caribbean's global brand portfolio positioned them to capture all of this growth.

"2024 was exceptional, thanks to our incredible team's flawless execution, which drove elevated demand across our leading brands, the early achievement of our Trifecta goals, and meaningful progress on our strategic priorities," said Jason Liberty. But perhaps the most exceptional aspect wasn't the financial performance—it was the complete transformation of the business model.

Royal Caribbean had entered the pandemic as a capital-intensive, cyclical business with thin margins and existential risk. It emerged as a demand-driven, pricing-powered platform with expanding margins and proven resilience. The crisis that nearly killed the company had instead revealed its true potential. As one analyst put it: "They didn't just survive COVID—they used it as a catalyst to become the company they always should have been."

The recovery story would be studied in business schools for decades. But for Jason Liberty and his team, it was just the beginning. With record earnings, a strong balance sheet, and insatiable customer demand, the question was no longer whether Royal Caribbean could recover—it was how high they could sail.

IX. Current Operations & Strategic Position

The command center at Royal Caribbean Group's Miami headquarters resembles something between NASA's mission control and a Wall Street trading floor. Giant screens display real-time data from 67 ships sailing across seven continents. Heat maps show booking patterns. Weather satellites track storms. Customer sentiment analysis scrolls past in real-time. This is the nerve center of a $91.93 billion empire that has fundamentally redefined what it means to take a vacation.

"People ask me what business we're in," Jason Liberty says, standing before the command center's main display. "We're not in the cruise business. We're not even in the vacation business. We're in the memory creation business. Everything we do—every ship we build, every island we develop, every innovation we introduce—is designed to create moments our guests will remember forever."

The scale of Royal Caribbean Group's operations in 2025 is staggering. The company fully owns three distinct cruise brands: Royal Caribbean International with 29 ships, Celebrity Cruises with 16 ships, and Silversea Cruises with 12 ships. They also hold 50% stakes in TUI Cruises (7 ships) and Hapag-Lloyd Cruises (5 ships), giving them influence over a combined fleet that serves every segment of the cruise market from budget-conscious families to ultra-luxury travelers.

Each brand occupies a carefully defined position in the market hierarchy. Royal Caribbean International, the flagship brand, targets the premium-mass market with ships that are essentially floating resorts. These vessels, including the Icon and Oasis classes, feature amenities that would have seemed impossible just a decade ago: surf simulators, ice rinks, zip lines, and Central Parks with living trees. Average ticket prices range from $1,500 to $2,500 per person for a seven-day cruise.

Celebrity Cruises occupies the premium segment, attracting affluent travelers who want sophisticated experiences without the formality of traditional luxury cruising. Their Edge class ships feature innovative design elements like the Magic Carpet—a moving platform that serves as a restaurant, bar, or tender platform depending on its position. Celebrity's guests are typically older (average age 54 versus 42 for Royal Caribbean), wealthier (average household income $125,000 versus $85,000), and more experienced travelers. Average fares run $2,000 to $3,500.

Silversea represents the ultra-luxury tier, with small ships (300-700 guests) offering all-inclusive experiences to exotic destinations. Launched in 1994 as the world's first all-inclusive, luxury global cruise line, Silversea officially became part of the Royal Caribbean Group in July 2018. Silversea provides one of the most inclusive offerings in luxury cruising. Voyages include butler service in every suite category; a choice of restaurants on every ship, as well as in-suite dining around the clock, and premium beverages served throughout the ship; and a true door-to-door service, with private executive transfers and flights included as standard. Fares often exceed $10,000 per person per week.

The joint ventures add another dimension. TUI Cruises, a joint venture with TUI AG, which began operations in 2009 aimed at a German-speaking market. These ships, including the Mein Schiff fleet, are designed specifically for German tastes—different cuisine, entertainment in German, and itineraries focused on destinations popular with European travelers. The 50% ownership structure allows Royal Caribbean to participate in the European market without the complexity of operating there directly.

The technological infrastructure supporting this fleet is as impressive as the ships themselves. On August 30, RCG signed a deal with SpaceX/Space Exploration Technologies Corporation to use Starlink's satellites for faster, low-latency Internet connections across the global fleet. Trials of the new Starlink Internet services were successfully conducted on Freedom OTS in June. Starlink Internet installations were scheduled to be completed fleetwide in 2023-Q1.

This connectivity enables Royal Caribbean's digital ecosystem. The Royal Caribbean app, downloaded by 80% of guests, serves as a digital concierge—handling check-in, cabin access, dining reservations, shore excursion bookings, and onboard purchases. The app generates vast amounts of data that feed into the company's revenue management systems, optimizing pricing in real-time based on demand patterns.

The revenue model has evolved far beyond simple ticket sales. A typical Royal Caribbean passenger now generates revenue through multiple streams: the base fare (averaging $200 per day), specialty dining (average $95 per meal), beverage packages ($65 per day), spa services ($150 per treatment), shore excursions ($125 per port), casino gaming, retail purchases, and internet packages. On average, passengers spend 50% more onboard than they do on their base fare.

Private destinations have become particularly lucrative profit centers. Perfect Day at CocoCay, after its $250 million transformation, generates average per-passenger spending of $150—pure profit since Royal Caribbean controls every venue. The island can accommodate 14,000 guests daily from two Oasis-class ships simultaneously. With ships visiting 3-4 times per week year-round, CocoCay alone generates over $300 million in annual revenue at margins exceeding 80%.

The company is replicating this model globally. Royal Beach Club developments are underway in Nassau, Cozumel, Costa Maya, and Vanuatu. Each represents a $200-300 million investment but promises similar returns to CocoCay. The Nassau project, scheduled to open in 2025, will feature a massive beach club, pools, restaurants, and exclusive cabanas renting for up to $1,500 per day.

The supply chain and logistics operation supporting this empire is mind-boggling. Royal Caribbean provisions its ships with 30 million pounds of food annually, 3 million bottles of wine, 10 million towels, and enough fuel to power a small city. The company has pioneered just-in-time provisioning, with ships receiving fresh supplies at every port to minimize storage needs and ensure freshness.

Labor management is equally complex. The company employs over 100,000 people from 130 countries, with crew members typically working 8-10 month contracts. The crew-to-passenger ratio varies by brand—1:3 on Royal Caribbean, 1:2 on Celebrity, nearly 1:1 on Silversea—directly impacting service levels and pricing power. Crew costs represent roughly 15% of revenue, carefully balanced against service quality expectations.

Environmental initiatives, once an afterthought, have become central to operations. New ships like Icon of the Seas run on Liquified Natural Gas (LNG), reducing emissions by 20%. Advanced wastewater treatment systems exceed international standards. Food waste digesters reduce solid waste by 85%. These investments, totaling over $1 billion, are partly driven by regulation but increasingly by customer expectations and long-term economics.

The competitive landscape remains intense but rational. Carnival Corporation, with 92 ships across nine brands, remains the largest by passenger capacity. But Royal Caribbean's focus on innovation and higher-yielding passengers has resulted in superior financial performance. Norwegian Cruise Line Holdings, with 29 ships across three brands, competes aggressively but lacks Royal Caribbean's scale advantages. New entrants like Virgin Voyages and expansion from river cruise operators like Viking create niche competition but don't threaten the core business.

The barriers to entry are formidable. A new cruise ship costs $500 million to $2 billion and takes 3-4 years to build. Port access is limited and often locked up in long-term contracts. Brand building takes decades. Distribution requires relationships with thousands of travel agents. The regulatory complexity of operating ships under various flags, complying with international maritime law, and satisfying health and safety requirements in dozens of countries is overwhelming for new entrants.

Royal Caribbean's current capital allocation strategy reflects confidence in the business model. The company is simultaneously investing in new ships (capital expenditures of $5 billion in 2025), developing private destinations ($1.6 billion in non-ship capex), paying down debt (targeting investment grade metrics), and beginning to return capital to shareholders (dividend discussions underway for late 2025).

The forward order book extends through 2028 with seven ships on order. These include more Icon-class giants for Royal Caribbean International, Edge-class vessels for Celebrity, and expedition ships for Silversea. Each new ship incorporates lessons from previous builds and guest feedback, creating a virtuous cycle of innovation and improvement.

"We're not just building bigger ships," explains Harri Kulovaara, Executive Vice President of Maritime & Newbuilding. "We're building better ships. Every new vessel has 10-15% lower operating costs per passenger, 20% better fuel efficiency, and generates 25% more revenue per available passenger cruise day than the ships they replace."

The strategic position Royal Caribbean has built is formidable. They have scale advantages in purchasing, marketing, and operations. They have brand differentiation that allows premium pricing. They have innovation capabilities that competitors struggle to match. They have private destinations that create unique experiences while capturing additional spending. They have technology infrastructure that improves every aspect of operations. And they have a management team that has proven it can navigate through the worst crisis in cruise history.

As Liberty concludes: "Our competitive advantages aren't just about having the biggest ships or the most amenities. It's about the entire ecosystem we've built—the brands, the destinations, the technology, the people, the culture of innovation. Competitors can copy a ship feature. They can't copy the entire system."

X. Playbook: Business & Investing Lessons

The story of Royal Caribbean offers a masterclass in building and scaling a capital-intensive consumer business. The lessons extend far beyond cruising—they're applicable to any industry where massive upfront investments must generate returns over decades, where customer experience drives pricing power, and where operational excellence determines survival.

Lesson 1: Capital Intensity as a Moat The cruise industry's capital requirements are staggering—$2 billion for a single ship that takes four years to build. This creates an almost impenetrable barrier to entry. But here's the key insight: capital intensity only becomes a moat if you deploy that capital better than competitors. Royal Caribbean's ships generate approximately $650 in revenue per available passenger cruise day, compared to Carnival's $450. Same capital intensity, vastly different returns.

The lesson extends beyond cruise lines. Amazon's fulfillment centers, Tesla's Gigafactories, TSMC's chip fabs—all require massive capital that scares away competitors. But the capital itself isn't the moat. It's the operational excellence that makes that capital sing. Royal Caribbean learned this lesson early: it's not about having ships, it's about having ships that customers will pay premiums to experience.

Lesson 2: Innovation Compounds When Royal Caribbean put the first rock climbing wall on a cruise ship in 1999, competitors mocked it as a gimmick. But that wall did something profound—it changed the conversation from "which cruise line has the best food?" to "which cruise line has the most innovative experiences?" Once you own innovation in customers' minds, each new innovation reinforces that perception.

The compounding is powerful. The rock wall led to ice rinks, which led to surf simulators, which led to skydiving simulators, which led to neighborhoods with Central Parks. Each innovation raised the bar for what was possible on a ship. Competitors who tried to copy were always one generation behind. By the time Carnival added rock walls, Royal Caribbean had moved on to surf simulators.

Lesson 3: Multi-Brand Strategy Without Cannibalization Most companies fail at multi-brand strategies because they can't resist the temptation to homogenize. Cost synergies drive them to share everything—products, marketing, operations—until the brands become indistinguishable. Royal Caribbean succeeded by maintaining rigid brand boundaries while sharing invisible infrastructure.

Celebrity guests never see Royal Caribbean marketing. Royal Caribbean families never encounter Celebrity's molecular gastronomy. But behind the scenes, both brands share purchasing contracts, port agreements, and technology platforms. It's the corporate equivalent of a mullet—distinct party in the front, efficient business in the back.

Lesson 4: Vertical Integration Through Private Destinations Perfect Day at CocoCay generates $300+ million in annual revenue at 80% margins. But the real genius isn't the financial return—it's the strategic control. At public ports, Royal Caribbean passengers scatter to local businesses. At CocoCay, every dollar spent flows to Royal Caribbean. Every experience reinforces the brand. Every memory is attributed to the cruise line, not the destination.

This is vertical integration for the experience economy. Disney pioneered it with theme parks, but Royal Caribbean perfected it at sea. The lesson: when your product is an experience, controlling the entire experience chain multiplies value creation.

Lesson 5: Crisis as Catalyst COVID should have killed Royal Caribbean. The entire business model—putting thousands of people in enclosed spaces—became toxic overnight. The company burned through $250 million monthly with zero revenue. Debt ballooned from $8 billion to $21 billion. Yet they emerged stronger, with higher margins and better returns than pre-pandemic.

The crisis forced brutal prioritization. Unprofitable ships were sold. Marginal routes were eliminated. Pricing discipline was enforced. Technology investments were accelerated. The company discovered that customers would pay 30% more for the same experience if it felt safe and special. Crisis didn't just test Royal Caribbean—it revealed capabilities they didn't know they had.

Lesson 6: Demand Elasticity Discoveries For decades, cruise lines assumed demand was highly elastic—small price increases would drive customers to competitors or land vacations. COVID shattered this assumption. When Royal Caribbean restarted operations, they raised prices and ships still sold out. They discovered that for their core customer—middle-class Americans seeking escape—a cruise wasn't competing with other cruises, it was competing with not taking a vacation at all.

This pricing power discovery transformed the business model. Revenue per passenger day increased from $200 pre-pandemic to $280 post-pandemic. Onboard spending jumped 25%. Suite bookings, at 3x the price of standard cabins, doubled. The lesson: you don't know your true pricing power until you test it.

Lesson 7: Operating Leverage at Scale Royal Caribbean's operating model showcases extreme operating leverage. The cost to operate a 5,000-passenger ship is only marginally higher than a 3,000-passenger ship—same captain, same engines, similar crew count. But revenue potential is 67% higher. This leverage explains why the industry relentlessly pursues scale.

But leverage cuts both ways. At 50% occupancy, Royal Caribbean loses money. At 100% occupancy, margins exceed 30%. This volatility makes the business uninvestable for many. But for those who understand the cycle, the volatility creates opportunity. Buy when ships are empty, sell when they're full.

Lesson 8: The Power of Float Royal Caribbean holds $5.5 billion in customer deposits—money paid for cruises not yet taken. This float, similar to insurance companies' premiums or Amazon's negative working capital, provides free financing for operations. In a rising rate environment, earning 5% on $5.5 billion generates $275 million in annual income—pure profit.

Warren Buffett built Berkshire Hathaway on insurance float. Royal Caribbean discovered the same principle applies to cruising. The lesson: businesses that collect payment before providing service have a structural advantage, especially when combined with scale.

Lesson 9: Technology as Enabler, Not Product Royal Caribbean spent billions on technology—Starlink connectivity, mobile apps, RFID wristbands, facial recognition boarding. But they never marketed themselves as a "tech company." The technology is invisible to guests; they just experience seamless service. The app doesn't feel like technology; it feels like a personal concierge.

This is the opposite of the "Uber for X" or "Netflix for Y" positioning that dominates Silicon Valley. Royal Caribbean understood that customers don't want technology—they want what technology enables. The lesson: in consumer businesses, technology should be felt, not seen.

Lesson 10: Long-Term Thinking in a Short-Term World Ordering a new ship requires committing $2 billion for an asset that won't generate revenue for four years. During COVID, when survival was uncertain, Royal Caribbean maintained all its ship orders. Competitors canceled. When the recovery came, Royal Caribbean had new capacity while competitors scrambled to restart construction.

This long-term orientation permeates the culture. Private island investments take five years to pay back. New ship classes require billion-dollar bets on unproven concepts. Brand building takes decades. But in a public market obsessed with quarterly earnings, this patience creates competitive advantage.

The meta-lesson from Royal Caribbean's playbook is that sustainable competitive advantages in capital-intensive businesses come from the intersection of financial engineering and operational excellence. It's not enough to have access to capital—you must deploy it better than competitors. It's not enough to innovate—you must create a culture where innovation compounds. It's not enough to survive crises—you must emerge stronger.

For investors, Royal Caribbean illustrates the power of businesses with high barriers to entry, pricing power, and operational leverage. For operators, it demonstrates that even in mature industries, innovation can create enormous value. For students of business, it proves that the most powerful moats combine multiple reinforcing advantages—scale, brand, innovation, vertical integration, and network effects.

The cruise industry will face new challenges—environmental regulations, demographic shifts, economic cycles. But Royal Caribbean's playbook—deploy capital intelligently, innovate relentlessly, build multiple brands, control the experience, think long-term—provides a template for navigating whatever storms lie ahead.

XI. Analysis & Bear vs. Bull Case

Standing at the intersection of Royal Caribbean's remarkable recovery and its ambitious future, investors face a fascinating dichotomy. The stock has risen from $19 during the pandemic to over $350, a nearly 20x return that has minted fortunes for those who bet on the recovery. Yet the fundamental question remains: is this a story of mean reversion that's now complete, or the early innings of a structural transformation in leisure travel?

The Bull Case: A Generational Transformation

The bulls see Royal Caribbean as the Amazon of cruise lines—a company that used a crisis to fundamentally restructure its economics and emerge with a business model that's virtually unassailable.