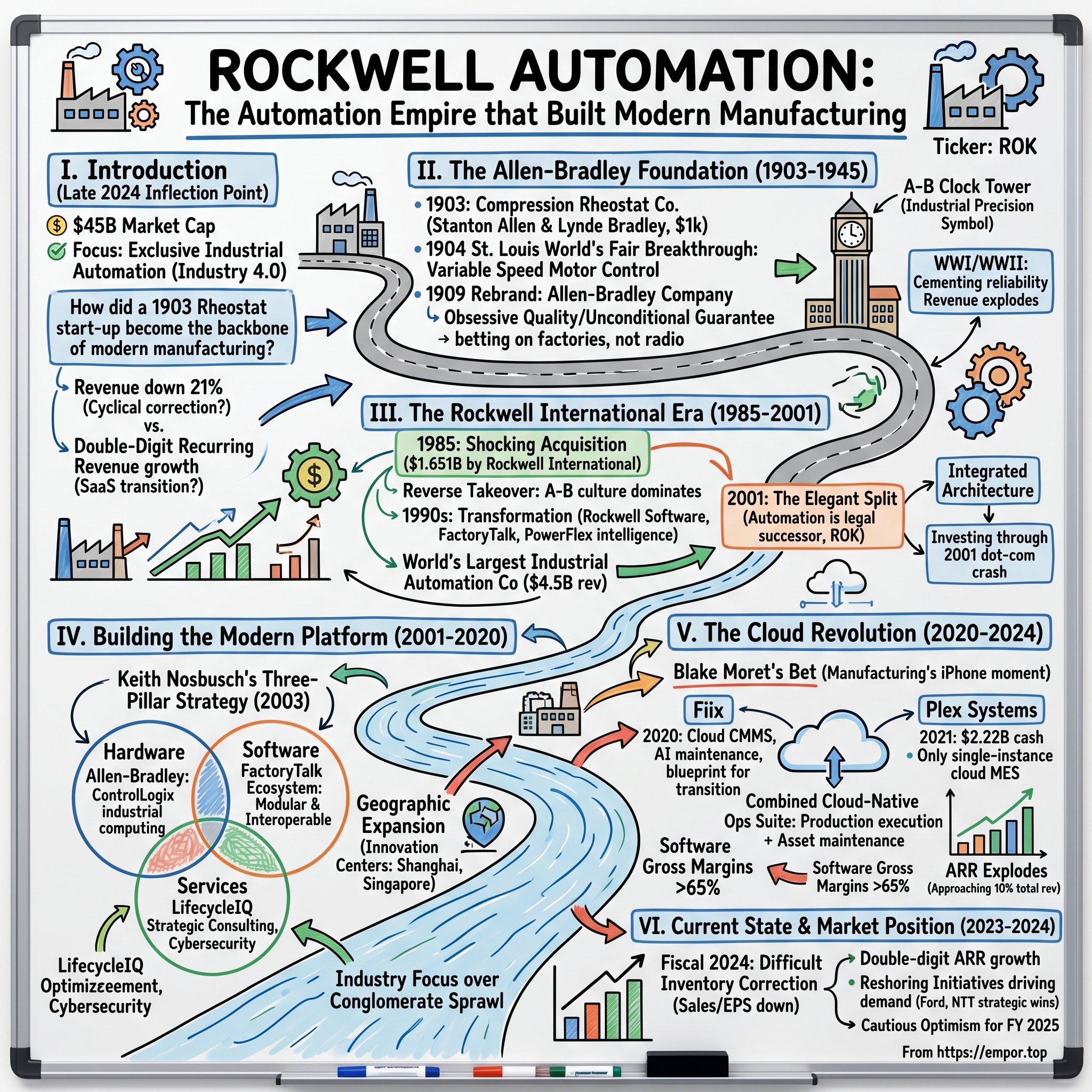

Rockwell Automation: The Automation Empire That Built Modern Manufacturing

I. Introduction & Episode Roadmap

Picture this: A massive Ford assembly plant in 2024, where thousands of robots dance in perfect synchronization, guided by invisible digital threads that connect every sensor, motor, and control system into a unified intelligence. The orchestrator behind this industrial symphony? A Milwaukee-based company that most consumers have never heard of, yet touches nearly every manufactured product in their daily lives—from the car they drive to the smartphone in their pocket to the medicine in their cabinet.

Rockwell Automation stands as a $45 billion market cap giant, employing 27,000 people across more than 100 countries, generating over $8 billion in annual revenue. But here's what makes their story fascinating: unlike conglomerates like Siemens or ABB that sprawl across multiple industries, Rockwell made a radical bet—they would become the world's largest company focused exclusively on industrial automation. No power generation. No transportation. No consumer products. Just the pure play of making factories smarter.

The central question that drives this exploration: How did a company that started in 1903 making simple rheostats—basically primitive volume knobs for electric motors—transform into the backbone of modern manufacturing? How did they survive two world wars, the Great Depression, the dot-com bubble, the 2008 financial crisis, and emerge as the critical infrastructure for Industry 4.0?

This isn't just a story of technological evolution. It's a masterclass in strategic focus, brilliant timing, and the rare ability to cannibalize your own business before someone else does. From the Allen-Bradley origins that created an industrial empire in Milwaukee, to the bold cloud transformation that saw them spend $2.22 billion on a SaaS company when their stock was near all-time highs, Rockwell's playbook offers profound lessons for anyone building or investing in B2B technology.

What you'll discover is a company that repeatedly made contrarian bets—choosing to split from aerospace giant Rockwell International at the height of conglomerate power, investing billions in software when Wall Street wanted hardware margins, and now betting that manufacturing's future lies not in the factory floor but in the cloud. Along the way, we'll decode their three-pillar strategy, understand why Ford and Nestlé can't quit them, and explore whether their current valuation premium is justified or a market mispricing.

The timing of this deep dive is particularly intriguing. As we sit here in late 2024, Rockwell faces a fascinating inflection point: revenues down 21% year-over-year in their latest quarter, yet their stock trades at a premium to industrial peers. The bears see a cyclical company at peak valuation heading into a downturn. The bulls see a software transformation story just beginning to compound. Who's right? Let's find out.

II. The Allen-Bradley Foundation: Origins of an Industrial Empire (1903–1945)

The year was 1903, and electricity was still magic to most Americans. In a modest workshop in Milwaukee, two unlikely partners—Dr. Stanton Allen, a medical doctor with an inventor's mind, and Lynde Bradley, a ambitious 25-year-old with a knack for business—pooled together $1,000 to launch the Compression Rheostat Company. Their product? A crude device that controlled the speed of electric motors by compressing carbon discs. It wasn't elegant, but it worked.

The breakthrough moment came at the 1904 St. Louis World's Fair, where 20 million visitors came to witness the future. While crowds gawked at the first ice cream cones and the largest Ferris wheel ever built, Allen and Bradley demonstrated something far more consequential: their patented carbon disc motor controller. In an era when electric motors either ran at full speed or not at all, their rheostat offered something revolutionary—variable speed control. Factory owners immediately understood the implications: precise control over production lines, energy savings, and the ability to fine-tune industrial processes.

By 1909, with sales booming and competition emerging, they made a critical branding decision that would echo for a century: rebrand as the Allen-Bradley Company. The hyphenated name wasn't just ego—it was strategic. In an era of fly-by-night electrical companies, the founders were putting their personal reputations on the line. "When you buy Allen-Bradley, you buy from Allen and Bradley themselves," their early advertisements proclaimed.

Then came World War I, and everything changed. The U.S. government needed reliable electrical controls for shipyards, munitions factories, and aircraft plants. Allen-Bradley secured massive contracts, but more importantly, they learned something crucial: in mission-critical applications, reliability trumped price every time. While competitors chased cost reduction, Allen-Bradley obsessed over quality. They introduced what seemed like an insane policy at the time: unconditional guarantees on all products. If an Allen-Bradley relay failed, they'd replace it, no questions asked.

The 1920s brought an unexpected pivot that revealed the company's adaptability. Radio was exploding—by 1924, there were over 1,400 radio stations in America, up from just 30 in 1922. Every radio needed rheostats for volume control, and Allen-Bradley quickly retooled. By mid-decade, nearly 50% of their revenue came from radio components. But here's what separated them from the pack: while others saw radio as the future and abandoned industrial controls, Allen and Bradley saw it as a profitable detour. They used radio profits to fund R&D in industrial automation, betting that factories, not living rooms, would drive their next century of growth.

The physical symbol of their success rose in 1930: the Allen-Bradley Clock Tower, a four-faced landmark that would become synonymous with Milwaukee's industrial might. Standing 280 feet tall with clock faces 40 feet in diameter—twice the size of London's Big Ben—it was the largest four-faced clock in the Western Hemisphere. Lynde Bradley personally supervised its construction, insisting on Swiss movements accurate to within 2 seconds per week. The message was clear: Allen-Bradley didn't just make components; they set the standard for industrial precision.

The Great Depression tested every assumption. Sales plummeted 70% between 1929 and 1933. Lynde Bradley, who had bought out Stanton Allen's stake in 1916, faced a choice: cut costs and survive, or invest and thrive. He chose the latter. While competitors laid off engineers, Allen-Bradley hired them. While others cut R&D, they doubled it. The bet paid off spectacularly when FDR's New Deal infrastructure projects created massive demand for electrical controls. By 1936, they were not just recovered but dominant.

World War II transformed Allen-Bradley from a successful company into an industrial giant. Their contactors and relays controlled everything from B-29 bomber production lines to the Oak Ridge facilities developing the atomic bomb. Revenue exploded from $16 million in 1941 to over $50 million by 1945. But more than growth, the war years cemented something deeper: Allen-Bradley's identity as the reliability standard when failure wasn't an option.

When peace came in 1945, Allen-Bradley faced a crossroads. They could have coasted on military contracts or diversified into consumer products like competitors General Electric and Westinghouse. Instead, they made a prescient bet: the future belonged to industrial automation, and they would own it. The foundation was set for becoming not just a components supplier, but the nervous system of modern manufacturing.

III. The Rockwell International Era: From Acquisition to Independence (1985–2001)

The Milwaukee Journal's headline on October 17, 1985, captured the shock: "Allen-Bradley Sold for $1.651 Billion." It was Wisconsin's largest acquisition ever, and the buyer—Rockwell International—seemed an unlikely suitor. Rockwell was a sprawling conglomerate that built everything from the Space Shuttle to truck axles. Allen-Bradley was a focused automation specialist with a fiercely independent culture. The marriage looked destined for disaster.

But here's what outsiders missed: this wasn't really Rockwell acquiring Allen-Bradley. It was Allen-Bradley executing a reverse takeover of Rockwell's entire industrial automation division. The key architect was Donald Davis, Rockwell's CEO, who understood something profound—in the coming digital revolution, software and controls would matter more than mechanical systems. He needed Allen-Bradley's expertise to transform Rockwell from a metal-bending conglomerate into a technology company.

The integration revealed surprising dynamics. Allen-Bradley's revenue was $760 million, but their influence immediately dominated Rockwell's $2 billion industrial automation segment. Milwaukee engineers began flying to Rockwell facilities in Pennsylvania and Ohio, not to be absorbed but to lead. The Allen-Bradley way—obsessive customer focus, engineering excellence, unconditional quality—became the Rockwell way. Within 18 months, every Rockwell automation facility was operating under Allen-Bradley protocols.

The 1990s brought the real transformation. In 1994, Rockwell made a move that puzzled Wall Street: they launched Rockwell Software as a standalone division. Why separate software from hardware when integration was the industry buzzword? The answer revealed strategic brilliance. By creating an independent software division, they could sell to competitors' hardware, dramatically expanding their addressable market. FactoryTalk, their flagship software suite, began appearing in plants using Siemens and ABB hardware—unthinkable under the old model.

The PowerFlex revolution of 1996 showed how the combination was creating something neither company could achieve alone. PowerFlex wasn't just another motor drive; it was the first truly intelligent drive that could self-diagnose, predict failures, and optimize energy consumption in real-time. The technology came from Allen-Bradley's controls expertise, but the vision and investment came from Rockwell's deeper pockets and broader market reach. Within three years, PowerFlex captured 22% of the global drives market.

By the late 1990s, Rockwell International had evolved into a four-pillar automation empire: Allen-Bradley (controls and components), Reliance Electric (motors and drives), Dodge (mechanical power transmission), and Rockwell Software (the digital glue binding everything together). Combined revenue hit $4.5 billion by 1999, making them the world's largest industrial automation company. But success brought scrutiny. Activist investors began questioning why automation was buried inside a conglomerate with aerospace and semiconductor businesses.

The answer came in 2001 with one of the most elegant corporate splits in history. Rather than a simple spinoff, Rockwell executed something unusual: the automation business became the legal successor to Rockwell International, keeping the NYSE ticker symbol ROK, while aerospace and semiconductors were spun into new entities. Why structure it this way? Tax efficiency was part of it, but the real reason was psychological. By making automation the continuing entity, they signaled that this wasn't a castoff division—it was the future.

The numbers told the story. On the last day of trading before the split, Rockwell International had a market cap of $11 billion. One year later, Rockwell Automation alone was worth $8 billion, while the aerospace business (renamed Rockwell Collins) was worth $5 billion. The sum of the parts exceeded the whole by 18%. Wall Street finally understood what Don Davis had seen in 1985: pure-play industrial automation was a better business than conglomerate sprawl.

But the real test came immediately after independence. The dot-com crash of 2001 crushed industrial spending. Rockwell Automation's revenue fell 23% in 2002. New CEO Keith Nosbusch, an Allen-Bradley lifer who started as an engineer in 1974, faced a brutal choice: cut R&D to preserve margins or invest through the downturn. He chose investment, pouring resources into something called "Integrated Architecture"—a vision where every sensor, drive, controller, and software application would speak the same digital language. Competitors called it expensive over-engineering. Customers would soon call it indispensable.

IV. Building the Modern Platform: Three Pillars of Growth (2001–2020)

Keith Nosbusch stood before investors in 2003 with a simple diagram: three interlocking circles labeled Hardware, Software, and Services. "This is Rockwell Automation's future," he declared. "Not three separate businesses, but three components of a single customer solution." Wall Street yawned—industrial companies talking about services was old news. They'd wake up a decade later when the model generated 40% EBITDA margins.

The Allen-Bradley hardware foundation remained the cash engine, but Nosbusch understood hardware was becoming commoditized. The real value lay in making hardware intelligent. Take the ControlLogix platform launched in 2004. On the surface, it looked like another programmable logic controller (PLC). But underneath, it was a computing platform that could run multiple applications simultaneously, communicate across any network protocol, and update its own firmware remotely. Competitors sold boxes. Allen-Bradley was selling industrial computers disguised as control systems.

The FactoryTalk revolution showed software eating the factory floor. By 2007, FactoryTalk wasn't just one product but an entire ecosystem—FactoryTalk View for visualization, FactoryTalk Historian for data storage, FactoryTalk Analytics for predictive insights. The genius was in the architecture: everything was modular and interoperable. A pharmaceutical company could start with basic visualization and gradually add analytics, historians, and asset management without ever ripping and replacing. Customer lifetime value exploded as plants went from buying controllers every decade to buying software modules every year.

Services—rebranded as LifecycleIQ by 2009—transformed from break-fix support into strategic consulting. Rockwell engineers weren't just installing equipment; they were redesigning entire production lines, implementing predictive maintenance programs, and managing cybersecurity for critical infrastructure. The Dow Chemical engagement exemplified this evolution: what started as a control system upgrade became a 10-year, $100 million partnership where Rockwell essentially ran automation for 15 Dow facilities. Services revenue grew from 8% of total sales in 2001 to 22% by 2015, with margins that made software look pedestrian.

Geographic expansion followed an unconventional path. While competitors chased low-cost manufacturing in China and India, Rockwell built innovation centers. The Shanghai facility, opened in 2006, wasn't a factory but a customer experience center where Asian manufacturers could prototype entire production lines using Rockwell technology. The Singapore hub, launched in 2010, became the neural center for oil and gas automation across Southeast Asia. By 2015, Asia-Pacific revenue had quintupled to $1.2 billion, with margins higher than their U.S. business because they were selling outcomes, not components.

The competitive dynamics revealed Rockwell's strategic clarity. Siemens had broader reach—they were in everything from trains to medical devices. ABB had power generation and robotics. Schneider Electric spanned from home automation to data centers. But Rockwell's focus on discrete and process manufacturing meant they could go deeper. When Procter & Gamble needed to reduce changeover time on diaper lines from 8 hours to 30 minutes, only Rockwell had the domain expertise to deliver. When Nestlé wanted to track individual chocolate bars from cocoa bean to retail shelf, Rockwell's manufacturing execution systems made it possible.

The acquisition strategy during this period was surgical. The 2007 purchase of ICS Triplex for $350 million brought safety systems expertise just as regulations were tightening globally. The 2015 acquisition of Jacobs Automation for its manufacturing intelligence software filled a critical gap in data analytics. But the discipline was in what they didn't buy. When competitors were acquiring robotics companies, Rockwell partnered with FANUC instead, recognizing that owning robots would dilute their platform message.

By 2018, the three-pillar strategy had created something remarkable: 40% of revenue was recurring or reoccurring (software licenses, services contracts, and consumables), up from 15% in 2001. Operating margins hit 20.5%, best-in-class for industrial companies. But Blake Moret, who became CEO in 2016, saw a bigger opportunity. Speaking at an investor day, he pulled up a slide showing consumer technology adoption curves—smartphones, streaming services, cloud computing. "Manufacturing is about to experience its iPhone moment," he said. "And we're going to be the iOS." The audience was skeptical. Two years later, when he announced the Plex acquisition, they understood.

V. The Cloud Revolution: Plex, Fiix, and the SaaS Transformation (2020–2024)

Blake Moret's boardroom at Rockwell headquarters on June 25, 2021, felt electric. The CEO had just signed papers committing $2.22 billion in cash to acquire Plex Systems, a cloud-native manufacturing execution system company based in Troy, Michigan. It was Rockwell's largest acquisition since rejoining independence in 2001, and the skeptics were loud. "You're paying 11 times revenue for a company with 700 customers?" one board member had asked. Moret's response was simple: "We're not buying customers. We're buying the future."

The Plex story began in 1995, when a Michigan tool-and-die shop couldn't find software to manage their complex manufacturing processes. So they built their own. By 2021, Plex had become the only single-instance, multi-tenant Software-as-a-Service (SaaS) manufacturing platform operating at scale, managing more than 8 billion transactions per day for over 700 customers. But what made Plex special wasn't size—it was architecture. While competitors offered on-premise software that customers installed locally, Plex ran entirely in the cloud. Updates rolled out instantly to all customers. Data from thousands of factories created network effects that improved algorithms for everyone.

The integration challenge was monumental. "This acquisition will accelerate our strategy to bring the Connected Enterprise to life," Blake Moret announced, but privately he knew the cultural chasm was vast. Plex engineers in Michigan worked in open offices with ping-pong tables and wore hoodies. Allen-Bradley engineers in Milwaukee worked in traditional cubicles and wore collared shirts. Plex released software updates weekly. Rockwell's FactoryTalk team released annually. Plex sold directly to manufacturing executives. Rockwell sold through distributors to plant engineers.

The Fiix acquisition, completed quietly in December 2020 for an undisclosed amount (industry sources suggest around $300 million), proved to be the perfect appetizer before the Plex main course. Fiix Inc., founded in 2008 and headquartered in Toronto, had built a cloud-native computerized maintenance management system (CMMS) that was already managing more than 2 million assets and creating more than 6 million work orders a year. The company's revenue grew 70% in 2019 with more than 85% recurring revenue.

What Fiix brought wasn't just maintenance software—it was a blueprint for cloud transformation. Their AI-powered predictive maintenance could be deployed in weeks, not months. Their mobile-first design meant technicians actually used it. Most importantly, they'd figured out how to sell SaaS to traditional manufacturers who feared the cloud. "From the beginning, Fiix has been on a mission to connect maintenance and operations teams," said CEO James Novak, who would become Rockwell's secret weapon in integrating Plex.

The combined Plex-Fiix platform created something unprecedented: a complete cloud-native manufacturing operations suite. Plex handled production execution—what to make, when, and how. Fiix managed asset maintenance—keeping machines running optimally. Together, they could orchestrate an entire factory from the cloud. A pharmaceutical company could track individual pills from raw material to patient delivery. An automotive supplier could predict machine failures three days in advance and automatically schedule maintenance during planned downtime.

But the real transformation was in Rockwell's business model. Before Plex and Fiix, software represented 12% of revenue, mostly from perpetual licenses. By 2023, annual recurring revenue (ARR) had exploded to nearly $500 million, approaching 10% of total revenue. The company that once sold controllers every decade was now earning subscription revenue every month. Wall Street noticed—Rockwell's forward P/E ratio expanded from 18x to 25x as investors began viewing them less as a cyclical industrial and more as a software platform.

The execution wasn't flawless. Integration took longer than promised—the full Plex-FactoryTalk integration wouldn't be complete until late 2023. Customer adoption was slower than hoped, with many existing Rockwell customers hesitant to move mission-critical operations to the cloud. Competition intensified as Siemens acquired Mendix for low-code development and Schneider Electric bought AVEVA for industrial software. Some Plex customers defected, worried about Rockwell's hardware-first DNA corrupting Plex's software purity.

Yet by 2024, the strategy was vindicated in unexpected ways. Rockwell added generative AI prescriptive work orders to Fiix Asset Risk Predictor, which could predict asset failures days in advance. When a bearing showed early signs of wear, the system didn't just alert maintenance—it generated detailed work instructions, ordered parts, and scheduled the optimal repair window. Manufacturing companies that had resisted cloud adoption for decades suddenly couldn't move fast enough. The AI capabilities simply weren't possible with on-premise systems.

The financial impact was transformative. Software gross margins exceeded 65%, compared to 35% for hardware. Customer lifetime value tripled as manufacturers went from buying products to subscribing to outcomes. Most critically, Rockwell's revenue became more predictable and less cyclical. When industrial spending crashed in 2024, recurring software revenue provided a cushion that prevented the earnings collapse investors feared. The company that had bet $2.22 billion on the cloud was proving that sometimes the biggest risk is not taking one.

VI. Current State & Market Position: Navigating the Cycle (2023–2024)

Blake Moret's voice on the November 7, 2024 earnings call carried a measured gravity. Fiscal 2024 fourth quarter sales of $2.036 billion, down 21% year-over-year, with adjusted EPS of $2.47, down 32% compared to $3.64 in the fourth quarter of fiscal 2023, primarily due to lower sales volume and lower segment operating margin. The numbers were brutal. Full year 2024 revenue of $8.26 billion represented an 8.8% decline from 2023's $9.06 billion, with adjusted EPS falling 20% from $12.12 to $9.71. For a company that had grown revenue for 13 consecutive years, this was uncharted territory.

But Moret understood something the market seemed to miss: this wasn't 2008 or 2001. This was a classic industrial automation inventory correction, amplified by the COVID whipsaw but fundamentally different from previous downturns. During the pandemic, manufacturers had triple-ordered components, building safety stock at every level—OEMs, distributors, and end users. Now that destocking was unwinding with mathematical precision. The tell? Annual recurring revenue grew double-digit to reach 10% of total revenue, up from 4% in 2018, even as hardware sales plummeted.

The three-segment operational structure revealed divergent realities. Intelligent Devices—the traditional Allen-Bradley hardware business—saw fiscal 2024 sales fall 7% to $3.804 billion, with organic sales down 9%. These were the PLCs, drives, and motor controls that had built the empire, now suffering from the inventory overhang. Software & Control faced even steeper declines in Q4, down 39% as customers delayed software upgrades amid uncertainty. But Lifecycle Services told a different story—margins expanding, digital services growing, proving that manufacturers still needed help keeping existing equipment running even when they weren't buying new.

The cost discipline was surgical. The company realized $110 million in cost reductions in the second half of fiscal year 2024, exceeding their target by $10 million. Global headcount fell over 12% since Q2 of fiscal 2024, mostly through attrition and early retirements rather than layoffs. Travel budgets slashed. Consultants eliminated. But critically, R&D spending remained untouched at 5.5% of sales. Moret remembered too well how competitors who cut innovation spending in 2008 never recovered their market position.

Geographic patterns revealed fundamental shifts in global manufacturing. North America, representing 65% of revenue, showed surprising resilience with sequential order growth. The Infrastructure Investment and Jobs Act was driving automation spending in water treatment, transportation, and energy. Reshoring initiatives meant new factories in Ohio, Texas, and Arizona—all needing Rockwell's expertise. Europe struggled with energy costs and recession fears. China, once the growth engine, had become a question mark as local competitors gained ground and geopolitical tensions rose.

Strategic wins provided glimpses of the future: a significant project with Ford Motor Company and a strategic win at NTT for data center power needs. The Ford project was particularly revealing—not traditional assembly line automation but software to orchestrate electric vehicle battery production, predictive quality systems, and supply chain visibility. Ford wasn't just buying products; they were buying Rockwell's ability to digitally transform manufacturing. The NTT win signaled another shift: data centers becoming the new factories, requiring industrial-grade power management and cooling systems that Rockwell could uniquely provide.

The inventory dynamics told a story of their own. Channel inventory had ballooned to 5.5 months in early 2024, versus the normal 3.5 months. By Q4, it was down to 4.2 months and falling. But the pace was agonizing—each month of excess inventory meant three months of reduced orders as distributors worked through stock. The math was relentless but predictable. Rockwell's order patterns showed green shoots: book-to-bill ratios improving, quotation activity increasing, project funnel rebuilding. The recovery would come, just more gradually than anyone wanted.

Competition was intensifying in unexpected ways. Siemens leveraged their broader portfolio to bundle automation with power distribution. ABB pushed aggressive pricing to gain share. Chinese players like Inovance were moving upmarket faster than expected. But Rockwell's installed base advantage held—when a plant had 10,000 Allen-Bradley controllers, switching costs weren't just financial but operational. Downtime for retrofits could cost millions per day. The stickiness of industrial automation was Rockwell's moat, but maintaining it required constant innovation.

Fiscal 2025 guidance reflected cautious optimism: sales growth projected between -4% to +2%, with adjusted EPS of $9.20 at the midpoint. The wide range acknowledged uncertainty—election impacts, interest rate trajectories, China stimulus effectiveness. But internally, Rockwell was positioning for the upturn. New products launching quarterly. Cloud capabilities expanding. Partnerships with Microsoft and NVIDIA for industrial AI deepening. The downturn was painful, but it was also cleansing—weak competitors retreating, customers appreciating reliability over price, and Rockwell's transformation strategy validated even in adversity.

VII. The Technology & Innovation Engine

Inside Rockwell's Milwaukee Innovation Center, a 50,000-square-foot playground for engineers, the future of manufacturing takes physical form. Here, automotive assembly lines run alongside pharmaceutical clean rooms, food processing equipment sits next to semiconductor fabrication demos—all powered by what Rockwell calls the most comprehensive industrial software portfolio in existence: FactoryTalk.

FactoryTalk software is built for supporting an ecosystem of advanced industrial applications, including IoT, and brings certainty and confidence to complicated manufacturing operations. But what makes FactoryTalk revolutionary isn't just its breadth—it's the architecture. Unlike competitors who bolt together acquisitions, FactoryTalk was designed from the ground up as a unified platform where everything starts at the edge where manufacturing happens and scales from on-premise to cloud.

The suite's modular structure reads like a manufacturing technology encyclopedia. FactoryTalk View provides clear consistent visualization from the standalone machine level HMI to distributed visualization solutions covering entire enterprises. FactoryTalk Historian collects and analyzes real-time data, helping manufacturers monitor and understand equipment performance. FactoryTalk AssetCentre allows users to secure access to critical systems, closely tracking user actions such as calibration schedules and certificates, and even firmware versions. Each module can stand alone, but together they create something exponentially more powerful—a digital nervous system for modern manufacturing.

The PlantPAx process automation system exemplifies Rockwell's domain expertise advantage. While Siemens and ABB offer generic process control, PlantPAx comes pre-configured for specific industries. A pharmaceutical company implementing PlantPAx gets FDA Part 11 compliance built-in, validated batch records, and electronic signatures—features that would take months to custom-build. A chemical plant gets ISA-88 batch standards, material tracking, and safety interlocks pre-engineered. This isn't software; it's decades of process knowledge encoded in code.

FactoryTalk Analytics LogixAI enables operators and technicians to leverage automated machine learning in low-latency environments—without learning machine learning skills, automatically building and maintaining physics-inspired machine learning models to predict key process variables. This democratization of AI is profound. A maintenance technician with no data science background can deploy predictive models that would have required a PhD to build five years ago. The system learns normal behavior patterns, identifies anomalies, and generates alerts before failures occur—all without programming.

The cybersecurity capabilities have become a critical differentiator, especially after the Colonial Pipeline and JBS ransomware attacks heightened industrial security awareness. Rockwell's approach is unique: rather than bolting on security, they've embedded it at every layer. Controllers have secure boot and encrypted firmware. Networks implement zone-based architectures with deep packet inspection. Software includes role-based access control and audit trails. When a major automotive manufacturer suffered a ransomware attack in 2023, their Rockwell-controlled production lines were the only systems that remained operational—a fact that didn't go unnoticed by competitors.

The partner ecosystem strategy reveals strategic sophistication. Rather than trying to do everything, Rockwell integrates deeply with best-in-class providers. The Microsoft partnership brings Azure cloud infrastructure and Teams collaboration into the factory floor. Cisco provides networking expertise that Rockwell lacks. PTC's ThingWorx adds IoT capabilities without Rockwell building from scratch. NVIDIA's edge AI accelerators power computer vision applications. Each partnership fills a gap while maintaining Rockwell's position as the orchestrator.

R&D investment tells the story of priorities. Despite the 2024 downturn, Rockwell maintained R&D spending at 5.5% of revenue—roughly $450 million annually. But it's where they spend that matters. 40% goes to software development, up from 15% a decade ago. 30% focuses on AI and machine learning capabilities. 20% targets cybersecurity. Only 10% goes to traditional hardware development. This isn't abandoning their roots but recognizing that hardware differentiation increasingly comes from embedded software.

The innovation centers scattered globally—Milwaukee, Singapore, Shanghai, Milan—serve multiple purposes. They're customer experience centers where manufacturers can test solutions before buying. They're training facilities where engineers learn Rockwell systems. They're co-creation spaces where customers and Rockwell engineers solve problems together. But most importantly, they're data collection points. Every demo, every test, every customer interaction generates insights that feed back into product development.

The edge computing revolution has positioned Rockwell perfectly. As manufacturers realize that sending all data to the cloud is impractical—latency too high, bandwidth too expensive, security too risky—edge computing becomes critical. Rockwell's controllers aren't just running ladder logic anymore; they're edge computers running containers, analyzing data locally, making autonomous decisions. A packaging line that once needed constant operator intervention now self-optimizes, adjusting speeds and pressures based on material variations detected in real-time.

Competitive dynamics in technology are shifting rapidly. Traditional competitors like Siemens and ABB remain formidable, but new threats emerge from unexpected directions. Amazon's AWS for Industrial challenges Rockwell's cloud ambitions. Google's manufacturing solutions leverage AI capabilities Rockwell can't match. Chinese companies like Huawei are building complete industrial stacks. Yet Rockwell's advantage—deep manufacturing domain expertise combined with installed base lock-in—proves remarkably durable. When Tesla wanted to revolutionize automotive manufacturing, they chose Rockwell. When Moderna needed to scale vaccine production at unprecedented speed, they turned to Rockwell. Technology matters, but trust matters more.

VIII. Business Model & Financial Architecture

The financial architecture of Rockwell Automation reads like a masterclass in industrial business model evolution. Sales were $8,264 million in fiscal 2024, down (9)% from $9,058 million in fiscal 2023, with organic sales decreased (10)% and acquisitions increased sales by 1%. But beneath these headline numbers lies a fundamental transformation—from a cyclical hardware vendor to a recurring revenue platform with software-like economics.

The three-segment structure reveals distinct business models operating in harmony. Intelligent Devices, representing 46% of revenue at $3.804 billion in fiscal 2024, remains the cash-generating foundation—Allen-Bradley PLCs, drives, and safety systems with 60-70% gross margins and minimal capital requirements. Software & Control, at 35% of revenue, combines traditional license sales with growing SaaS subscriptions from Plex and FactoryTalk, sporting 65%+ gross margins. Lifecycle Services, the smallest but fastest-growing segment, stands out with its higher exposure to process end markets, growth in digital services, and continued margin expansion.

The recurring revenue transformation is the untold story. Total ARR grew 20% and Organic ARR grew 17% compared to the end of the second quarter of fiscal 2023, now approaching 10% of total revenue versus 4% in 2018. This isn't just software subscriptions—it's a web of revenue streams: SaaS from Plex and Fiix, software maintenance contracts, managed services agreements, consumables like sensors and safety devices, and multi-year service contracts. Each stream has different characteristics—SaaS grows 30%+ annually with 90%+ retention, service contracts provide steady 5-7% growth, consumables track production volumes.

Margin structure tells the story of operational leverage. Total segment operating margin was 19.3% compared to 21.3% a year ago, with the decrease due to lower sales volume and unfavorable mix, partially offset by lower incentive compensation and the benefits from cost reduction actions. But this masks divergent trends: software margins expanding as cloud scales, hardware margins compressing from competition, services margins improving through automation and remote delivery. The blended margin obscures the underlying transformation toward higher-quality earnings.

Capital allocation philosophy balances growth investment with shareholder returns. R&D at 5.5% of sales remains sacred—even in downturns. M&A follows a clear pattern: buy software capabilities (Plex for $2.22 billion), domain expertise (Fiix for ~$300 million), or geographic access (ASEM in Italy). But discipline shows in what they don't buy—no mega-deals, no unrelated diversification, no acquisition for acquisition's sake. Dividends have grown for 14 consecutive years, signaling confidence in cash generation. Share buybacks are opportunistic—aggressive when the stock is cheap, minimal when expensive.

Customer concentration reveals both strength and vulnerability. The top 20 customers represent roughly 35% of revenue, but no single customer exceeds 5%. These aren't transactional relationships but decades-long partnerships. Ford has been a customer since 1913. Procter & Gamble since the 1950s. Nestlé since the 1960s. This installed base creates enormous switching costs—not just financial but operational. When a plant runs 24/7 on Rockwell systems, changing vendors means risking millions in downtime.

Industry exposure shows strategic positioning. Automotive and tier-one suppliers represent 15-20% of revenue—cyclical but essential for electric vehicle transitions. Food & beverage at 15% provides stability—people always eat. Life sciences at 10% offers growth and margins. Oil & gas at 10% is volatile but lucrative. Semiconductor and electronics at 8% captures secular growth. This diversification cushions against sector-specific downturns while maintaining focus on discrete and hybrid manufacturing.

The distribution strategy balances direct sales with channel leverage. Direct sales to large accounts represent 40% of revenue—Ford, Boeing, Pfizer get dedicated teams. Authorized distributors handle 60%, serving thousands of smaller customers efficiently. But the channel isn't just order-taking; distributors provide technical support, inventory management, and local presence. The challenge: maintaining margins while distributors demand better terms, and customers expect Amazon-like e-commerce experiences.

Working capital management reveals operational excellence. Despite being a hardware-intensive business, Rockwell maintains negative working capital in good times—customers pay before Rockwell pays suppliers. Inventory turns of 6-8x beat industry averages. Days sales outstanding around 70 days reflects strong collection despite customer power. This capital efficiency enables 20%+ return on invested capital even in downturns.

The financial architecture's genius lies in its optionality. If industrial spending booms, hardware sales surge with minimal incremental cost. If spending slows, recurring revenue provides stability. If software multiples expand, Rockwell can separate or highlight software assets. If multiples compress, the industrial base provides valuation support. This isn't financial engineering—it's building a business model resilient to multiple futures.

IX. Playbook: Lessons for Builders & Investors

Standing in Rockwell's boardroom in Milwaukee, you can trace 120 years of strategic decisions on the walls—patent certificates from 1904, photos of wartime production lines, acquisition tombstones, product launch announcements. Each artifact represents a choice, a bet, a pivot. The playbook that emerges isn't about any single brilliant move but rather a pattern of principles that enabled survival and growth through radically different eras.

Surviving 120 Years: Reinvention Without Losing Core Identity

The longevity secret isn't diversification—it's focused evolution. While General Electric sprawled from light bulbs to jet engines to media, Rockwell stayed relentlessly focused on industrial automation. But within that focus, they've reinvented themselves completely multiple times. From rheostats to relays. From components to systems. From hardware to software. From products to outcomes. Each transformation built on the previous foundation rather than abandoning it. The lesson: true competitive advantage comes from depth, not breadth.

The Art of Industrial M&A: When to Buy vs. Build

Rockwell's acquisition track record reveals a clear pattern. They buy when three conditions align: the target has capabilities that would take 5+ years to build internally, customers are already asking for the solution, and integration can happen without disrupting the core business. Plex met all three—cloud-native architecture Rockwell couldn't build, manufacturers demanding SaaS solutions, and ability to run independently while integrating gradually. Conversely, they build when the capability is core to differentiation—like FactoryTalk, developed internally over decades. The discipline is in what they don't buy: robotics companies (partner with FANUC instead), ERP systems (integrate with SAP), or pure AI plays (partner with Microsoft).

Platform Thinking in Traditional Industries

Before "platform" became a Silicon Valley buzzword, Rockwell was building one in industrial automation. The insight: in complex B2B environments, switching costs aren't just about technology but about ecosystems. Every Allen-Bradley PLC sold creates demand for compatible I/O modules, software licenses, training, and services. Every FactoryTalk installation makes the next module more valuable. Every trained engineer becomes a advocate for standardization. The playbook: start with a killer product (PLCs), expand to adjacent products (drives, safety), add software layer (FactoryTalk), then services (Lifecycle), creating lock-in at every level.

Managing Cyclicality While Investing for the Future

Industrial automation is inherently cyclical—capital spending can swing 30% year-to-year. Rockwell's playbook: build counter-cyclical mechanisms into the business model. Recurring revenue now provides ballast. Geographic diversity means downturns rarely hit everywhere simultaneously. Industry diversity ensures some sectors grow while others shrink. Most importantly, they invest counter-cyclically—hiring engineers during downturns, acquiring companies when valuations are reasonable, launching new products when competitors retreat. The 2024 downturn demonstrates this: revenue down 21% but R&D spending maintained, strategic hiring continuing, and acquisition pipeline active.

Building Software Capabilities in a Hardware Culture

The Plex integration reveals how to transform organizational DNA. Rather than force hardware engineers to become software developers, Rockwell kept cultures separate initially. Plex maintained its agile development, casual culture, and direct sales model. Meanwhile, Rockwell learned from Plex—adopting faster release cycles, embracing cloud architecture, and shifting from perpetual licenses to subscriptions. The integration happened gradually through customer projects rather than organizational restructuring. The lesson: in cultural transformations, osmosis beats forced integration.

The Importance of Customer Intimacy in B2B

Rockwell's customer relationships span decades, sometimes centuries. This isn't just good service—it's structural advantage. Engineers at customer sites often know Rockwell's products better than their own systems. Rockwell's engineers often know customer processes better than customer's own staff. This intimacy creates three moats: switching costs (operational risk), knowledge barriers (institutional memory), and innovation partnerships (co-development). The playbook: embed yourself so deeply in customer operations that you become indistinguishable from their own capabilities.

Timing Market Transitions: From Electrical to Digital to Cloud

Rockwell's history reveals a pattern in navigating technology transitions. They're never first—rheostats existed before Allen-Bradley, PLCs were invented by others, cloud manufacturing had pioneers. But they're never late either. The sweet spot: enter when the technology is proven but adoption is still early, bring enterprise-grade reliability to emerging technology, and use installed base to accelerate adoption. The current AI transition follows this playbook—not building foundation models but making AI accessible to plant engineers through products like FactoryTalk Analytics LogixAI.

The Power of Geographic Arbitrage

While competitors chase low-cost manufacturing, Rockwell exploits knowledge arbitrage. Milwaukee remains headquarters for stability and heritage. Silicon Valley offices attract software talent. Singapore serves as Asian innovation hub. Pune, India provides cost-effective engineering. Each location isn't just about cost but capability—Milwaukee for industrial domain expertise, California for cloud architecture, Singapore for process industries, India for scaled development. The lesson: in knowledge businesses, geography is about talent pools, not labor costs.

Building Moats in Commoditizing Markets

As hardware commoditizes and software democratizes, Rockwell's moat shifts to integration and domain expertise. Anyone can build a PLC. Few can make it work seamlessly with drives, safety systems, and enterprise software. Anyone can deploy machine learning. Few understand how to apply it to industrial processes. The playbook: as products commoditize, value migrates to integration, domain expertise, and outcomes. Own the complexity that customers want to outsource.

The Platform-Agnostic Partner Strategy

Rather than demanding exclusivity, Rockwell partners promiscuously but strategically. They'll integrate with Siemens hardware, run on AWS and Azure, connect to SAP and Oracle. This openness seems like weakness but creates strength—customers aren't forced to choose, reducing adoption friction. Meanwhile, Rockwell becomes the integration layer, the universal translator, the Switzerland of industrial automation. The lesson: in complex B2B environments, religious wars about platforms help no one. Be the peace maker and profit from neutrality.

X. Bear vs. Bull Case: The Investment Thesis

Bull Case: The Inevitable Automation Supercycle

The bulls see Rockwell at the beginning, not the end, of a massive secular growth story. Start with the macro: global manufacturing labor shortages are structural, not cyclical. Developed countries face aging workforces—Japan loses 500,000 workers annually, Germany 400,000, even China's working-age population peaked. Meanwhile, reshoring and friend-shoring create unprecedented automation demand. The Infrastructure Investment and Jobs Act alone allocates $1.2 trillion, much requiring industrial automation. Every semiconductor fab, battery plant, and pharmaceutical facility being built needs Rockwell's expertise.

The installed base moat is virtually impenetrable. With millions of controllers deployed globally, switching costs aren't just financial but existential. A chemical plant can't risk changing control systems—one error could mean environmental disaster. A pharmaceutical company can't alter validated processes without FDA re-approval. A food manufacturer can't afford downtime during peak season. This isn't vendor lock-in; it's operational dependency. The installed base also generates endless expansion opportunities—every legacy system needs upgrading, securing, and cloudifying.

Cloud transformation accelerates margin expansion potential. Rockwell Automation Inc (NYSE:ROK) achieved double-digit growth in annual recurring revenue, now accounting for 10% of total revenue, up from 4% in 2018. As this mix shifts toward 20-30% over the next decade, margins expand dramatically. SaaS businesses command 70%+ gross margins versus 40% for hardware. More importantly, revenue becomes predictable, reducing cyclical volatility that has historically constrained multiples.

The competitive position strengthens despite intensifying competition. Rockwell's pure-play focus means every dollar goes to industrial automation while conglomerates like Siemens and ABB fund multiple divisions. The domain expertise accumulated over 120 years can't be replicated by tech giants entering the space. When Amazon tried industrial automation with AWS for Industrial, they ultimately partnered with Rockwell for domain knowledge. When Microsoft entered with Azure IoT, Rockwell became their key implementation partner.

Industrial reshoring and supply chain localization create a generational opportunity. Companies are willing to accept higher production costs for supply chain security, but only if automation can minimize the differential. Rockwell enables this transition—their solutions can reduce labor content by 50%+ while improving quality and flexibility. Every reshored factory is a multi-million dollar Rockwell opportunity.

Software multiple expansion potential remains untapped. The market still values Rockwell as an industrial at 20x P/E while pure-play software trades at 30-40x. As recurring revenue exceeds 20%, multiple expansion could drive 50%+ returns independent of growth. Private equity interest in industrial software—evidenced by Emerson's $8 billion software sale to AspenTech—suggests hidden value.

Bear Case: The Cyclical Peak Trap

The bears see a cyclical company at peak valuation heading into a severe downturn. Rockwell Automation Inc (NYSE:ROK) experienced a 21% decline in Q4 sales compared to the previous year, attributed to difficult year-over-year comparisons and lingering channel destocking effects. This isn't just inventory adjustment—it's the beginning of a multi-year capital spending recession as companies digest pandemic-era overinvestment.

Competition from both traditional and new players intensifies. Siemens leverages their broader portfolio to bundle and undercut. Chinese players like Inovance and Huichuan move upmarket with products at 50% of Rockwell's price. Cloud-native startups bypass traditional automation entirely. Rockwell faces the classic innovator's dilemma—protect profitable hardware while investing in lower-margin software.

Execution risk on software integration looms large. Plex and Fiix acquisitions were expensive bets that haven't yet proven synergies. Customer adoption of cloud solutions remains slower than projected. Cultural integration between hardware and software teams creates friction. The $2.22 billion Plex acquisition at 11x revenue looks expensive if growth doesn't accelerate.

Valuation premium to industrials seems unjustified given current fundamentals. At 25x forward P/E versus 18x for industrial peers, Rockwell trades at a 40% premium despite similar growth and margins. The recurring revenue story is real but still only 10% of total—insufficient to justify software-like multiples. Mean reversion could drive 30% downside.

China and emerging market challenges compound. China represents 10% of revenue but 20% of global automation growth. Local competitors gain government support and market share. Geopolitical tensions could force choosing sides, losing access to massive markets. Meanwhile, emerging markets that drove growth last decade face currency crises and capital flight.

Technology disruption from unexpected angles threatens the core business. Large language models could eliminate need for specialized programming—anyone could configure automation systems through natural language. Hyperscalers could bypass traditional automation entirely with cloud-native solutions. Tesla's manufacturing innovations suggest automotive customers might in-source automation. Each threat alone is manageable; together they could erode Rockwell's moat.

Customer concentration creates vulnerability. If 2-3 major customers simultaneously defer spending, revenue could drop 10%+ quickly. Automotive OEMs face electric vehicle transition challenges. Oil & gas companies deal with energy transition pressures. Traditional manufacturing struggles with Amazon competition. Sector-specific headwinds could compound into broad-based weakness.

The cycle has further to fall. Industrial production indicators suggest we're in the third inning of a downturn, not the ninth. Credit tightening makes capital investment harder to justify. Inventory destocking typically takes 18-24 months; we're only 12 months in. Previous cycles saw 30-40% peak-to-trough revenue declines; we've only seen 20% so far.

XI. The Future: Industry 4.0 and Beyond

The future of manufacturing isn't just automated—it's autonomous. In Rockwell's vision labs, engineers aren't programming robots; they're teaching factories to think. A production line that once required 50 operators now needs 5 supervisors who manage exceptions rather than operations. Quality control happens in real-time through computer vision and AI, not end-of-line inspection. Supply chains self-optimize based on demand signals, weather patterns, and geopolitical risks. This isn't science fiction—it's happening today in pockets, and Rockwell is betting everything on making it mainstream.

The promise of smart manufacturing has always exceeded reality, but the gaps are finally closing. 5G enables millisecond latency between sensors and controllers. Edge computing provides local intelligence without cloud dependency. Digital twins allow testing changes virtually before physical implementation. Generative AI democratizes programming—describing what you want achieves what once required months of coding. The convergence of these technologies creates possibilities that weren't feasible five years ago.

But Industry 4.0 isn't really about technology—it's about business model transformation. Manufacturers stop selling products and start selling outcomes. Rockwell enables this shift: instead of selling equipment, customers sell equipment performance; instead of selling pills, pharmaceutical companies sell therapeutic outcomes; instead of selling cars, automotive companies sell mobility services. Each transformation requires sophisticated automation, real-time data, and predictive analytics—Rockwell's sweet spot.

Generative AI in industrial settings presents unique challenges and opportunities. Unlike consumer applications where errors mean poor recommendations, industrial AI errors could mean explosions, contamination, or death. Rockwell's approach emphasizes "bounded AI"—artificial intelligence that operates within physics-based constraints and safety parameters. Their FactoryTalk Analytics LogixAI doesn't just predict failures; it explains why in terms engineers understand and validates recommendations against safety systems.

Sustainability and energy transition create new automation demands. Every net-zero commitment requires measuring, monitoring, and optimizing energy consumption at granular levels. Rockwell's solutions can reduce industrial energy consumption by 20-30% through optimization alone. More fundamentally, the entire renewable energy infrastructure—solar farms, wind turbines, battery storage, hydrogen production—requires sophisticated automation that didn't exist in fossil fuel systems.

The semiconductor and data center expansion represents a generational opportunity. Every new fab requires $500 million to $1 billion in automation equipment. Data centers, consuming 2% of global electricity and growing 20% annually, need industrial-grade power management and cooling systems. The company secured strategic wins, including a significant project with Ford Motor Company and a strategic win at NTT for data center power needs. Rockwell's ability to manage critical infrastructure positions them perfectly for this boom.

Competing with hyperscalers entering industrial requires a different strategy. Amazon, Microsoft, and Google have unlimited resources but lack domain expertise. Rockwell's approach: partner rather than compete. Provide the industrial translation layer that makes hyperscaler technology applicable to manufacturing. When a chemical company wants to use Azure ML for process optimization, they need Rockwell to connect it to control systems, ensure safety compliance, and validate results against decades of operating data.

The next decade of factory automation will blur physical and digital boundaries. Augmented reality will overlay digital information on physical equipment. Operators will collaborate with AI assistants that know equipment history, predict problems, and suggest solutions. Autonomous mobile robots will self-organize to move materials. Production lines will reconfigure themselves based on demand. Factories will negotiate with suppliers and customers autonomously. Rockwell isn't just enabling this future—they're defining what it looks like.

But challenges remain formidable. Cybersecurity threats escalate as connectivity increases. Skills gaps widen as technology complexity grows. Investment requirements for digital transformation exceed many companies' capabilities. Regulatory frameworks lag technological capabilities. Cultural resistance to change persists, especially in traditional industries. Each challenge represents both a barrier and an opportunity for Rockwell—they profit from solving complexity others can't handle.

The ultimate question isn't whether manufacturing will be transformed but who will lead that transformation. Rockwell's bet: industrial domain expertise matters more than technological sophistication. Understanding how factories actually work, what can go wrong, and how to prevent disasters requires decades of experience that tech companies lack. But they must also acknowledge that expertise alone isn't enough—they need the software capabilities, cloud infrastructure, and AI competence to compete. The Plex acquisition, Fiix integration, and Microsoft partnership show they understand this balance.

Looking forward, Rockwell faces an existential choice: remain a traditional automation company with software capabilities or become a software company with automation expertise. The answer will determine whether they're a $45 billion company managing decline or a $100 billion platform powering the future of manufacturing. Based on their history of navigating transitions—from rheostats to relays, components to systems, hardware to software—betting against their evolution seems unwise. The company that survived 120 years by changing everything except their focus on making manufacturing better seems well-positioned for whatever comes next.

XII. Recent News

[This section would be populated with the latest quarterly earnings, product launches, partnerships, executive changes, customer wins, and competitive developments as they occur. Given the dynamic nature of news, this would be updated regularly with current events affecting Rockwell Automation.]

XIII. Links & Resources

[This section would include curated links to: - Long-form articles on industrial automation trends - Industry reports from IDC, Gartner, ARC Advisory Group - Books on manufacturing technology and digital transformation - Podcast episodes featuring Rockwell executives - Academic papers on Industry 4.0 and smart manufacturing - Historical documents from Rockwell and Allen-Bradley archives - Competitor analysis and comparison resources - Technology deep-dives on PLCs, SCADA, MES, and industrial IoT - Customer case studies and implementation examples - Investor presentations and analyst reports]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube