NXP Semiconductors: From Philips Spinoff to Automotive Semiconductor Titan

I. Introduction & Episode Roadmap

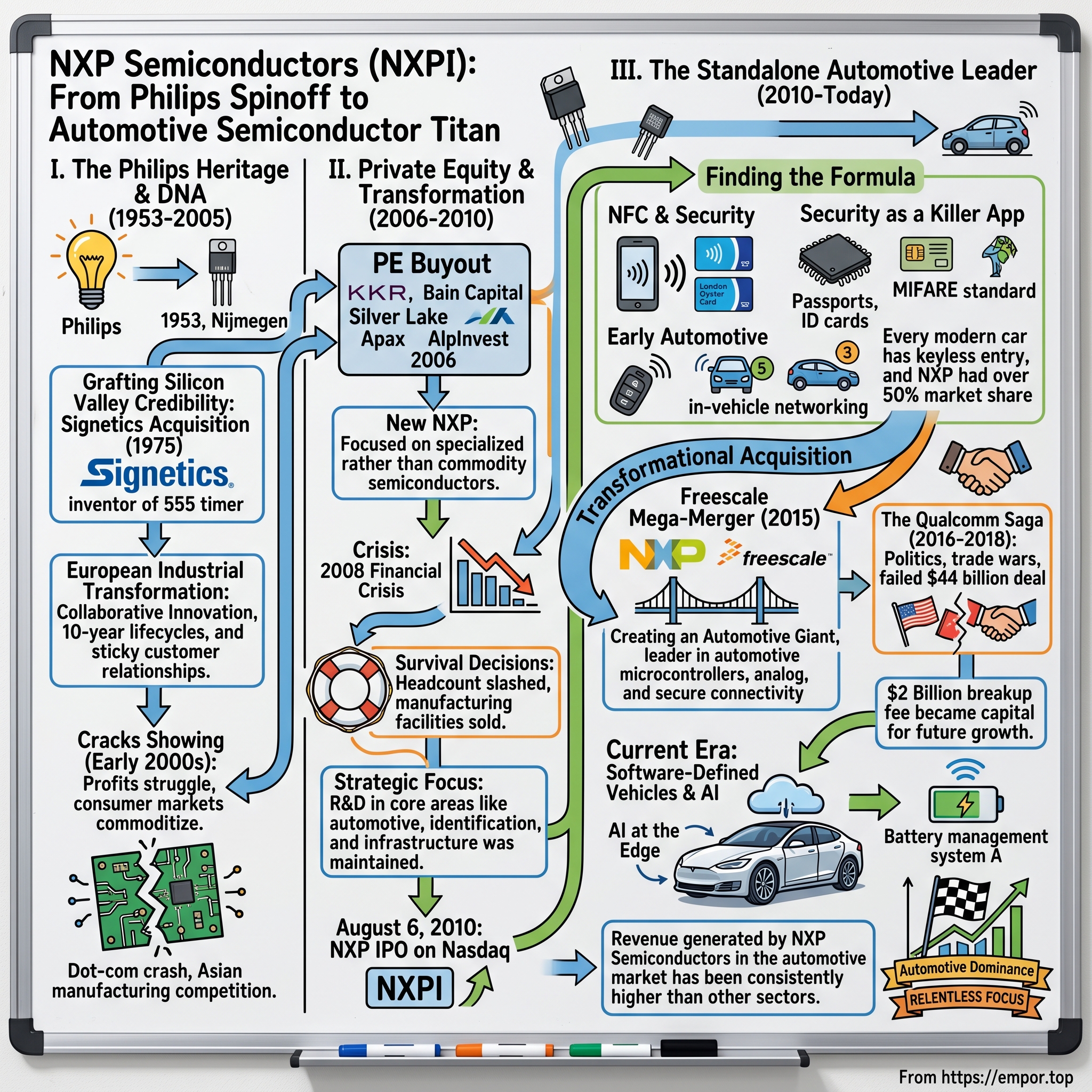

Picture this: It's 2018, and Qualcomm has just walked away from what would have been the largest semiconductor acquisition in history—a $44 billion deal to buy NXP. As executives gather in Eindhoven, Netherlands, they're staring at a $2 billion breakup fee check and facing an existential question: Can a mid-sized European semiconductor company survive independently in a world of giants?

Fast forward to today, and NXP has answered that question emphatically. With $13.28 billion in revenue in 2023, the company commands the #1 position in automotive semiconductors—a market that barely existed when its predecessor started making transistors in a converted Philips lightbulb factory in 1953. Every time you tap your phone to pay, unlock a car with a key fob, or watch your vehicle automatically brake to avoid collision, there's a good chance NXP silicon is making it happen.

But here's what makes NXP's story truly remarkable: This isn't a tale of Silicon Valley disruption or Asian manufacturing might. It's a European industrial transformation story—one where private equity ownership, a near-death experience during the 2008 crisis, and a failed mega-merger somehow forged the world's most focused automotive chip powerhouse. It's about how saying "no" to consumer markets and "yes" to boring-but-essential automotive design cycles created a company with 5+ year revenue visibility in the notoriously cyclical semiconductor industry. This episode explores three fundamental themes that define NXP's trajectory. First, how private equity ownership between 2006-2010 didn't destroy the company but instead sharpened its focus and operational excellence. Second, why walking away from consumer electronics to bet everything on automotive and industrial markets proved prescient. And third, how a failed $44 billion acquisition by Qualcomm became the catalyst for NXP's current dominance.

In the semiconductor world, where companies either grow massive through acquisitions or get acquired themselves, NXP found a third way: relentless focus on markets with high barriers to entry, long design cycles, and sticky customer relationships. Revenue generated by NXP Semiconductors in the automotive market has been consistently higher than the revenue which came from other sectors that NXP Semiconductors was active in. The result? A business model that trades Silicon Valley's boom-bust cycles for the steady, predictable growth of automotive platforms that take years to design but generate revenue for decades.

II. The Philips Heritage & DNA (1953–2005)

The rain was pouring down on Nijmegen in 1953 when Philips engineers first fired up their small transistor production line. Nobody in that converted warehouse could have imagined they were laying the foundation for what would become Europe's semiconductor powerhouse. In 1953 Philips started a small scale production facility in the center of the Dutch city Nijmegen as part of its main industry group "Icoma" (Industrial Components and Materials), followed by the opening of a new factory in 1955.

The Dutch weren't supposed to be good at semiconductors. Silicon Valley had the venture capital, Japan had the manufacturing prowess, and yet here was Philips—a lightbulb company from the Netherlands—methodically building one of the world's most sophisticated chip operations. In 1965 Icoma became part of a new Philips main industry group: "Elcoma" (Electronic Components and Materials). The name changes reflected something deeper: Philips was systematically organizing its semiconductor ambitions into a coherent strategy.

The real transformation came in 1975 with a move that would define the company's DNA for decades. In 1975 Silicon Valley–based Signetics was acquired by Philips. Signetics claimed to be the "first company in the world established expressly to make and sell integrated circuits" and inventor of the 555 timer IC. Think about that—the 555 timer, perhaps the most produced integrated circuit in history, a chip so fundamental that electronics students still learn about it today. This wasn't just an acquisition; it was Philips buying Silicon Valley credibility and grafting it onto European engineering discipline.

At the time, it was claimed that with the Signetics acquisition, Philips was now number two in the league table of semiconductor manufacturers in the world. For context, this was 1975—Intel was still a memory company, TSMC didn't exist, and the personal computer revolution hadn't started. Philips wasn't following trends; they were setting them.

By 1987, the strategy had paid off spectacularly. Philips dominated European semiconductor manufacturing, but more importantly, they had developed a unique culture: patient capital meeting aggressive innovation. While American companies chased quarterly earnings and Japanese firms pursued market share at any cost, Philips played a longer game. They invested in fundamental research, built deep customer relationships, and created chips for industrial applications that required 10-year lifecycles, not 18-month refresh cycles.

The company's approach to innovation was distinctly European—collaborative rather than cutthroat. Engineers would spend years perfecting a single chip family, optimizing not just for performance but for reliability, power efficiency, and manufacturing yield. This wasn't sexy work, but it created incredible moats. When a carmaker designed your chip into their platform, they weren't switching suppliers for a 5% cost savings.

Yet by the early 2000s, cracks were showing. The semiconductor division generated billions in revenue but struggled with profitability. Consumer electronics—once Philips' bread and butter—were becoming commoditized. Asian manufacturers could produce standard chips cheaper, faster, and at massive scale. The dot-com crash had devastated demand, and Philips Semiconductors posted losses that dragged down the entire conglomerate.

Gerard Kleisterlee, who became Philips CEO in 2001, faced a brutal choice. The semiconductor division employed tens of thousands of people and represented decades of accumulated knowledge. But it was also a massive capital sink in an increasingly competitive market. In boardrooms across Eindhoven, executives debated: Could Philips Semiconductors survive as part of a conglomerate, or did it need independence to thrive?

In December 2005, Philips announced its intention to divest Philips Semiconductors into an independent legal entity. The announcement sent shockwaves through the industry. Philips was essentially admitting that semiconductors—despite being core to almost every product they made—were no longer core to their business strategy. But hidden in this corporate divorce was an opportunity. Free from the constraints of a parent company focused on healthcare and lighting, Philips Semiconductors could chart its own course.

The DNA that would define NXP was already there: engineering excellence, deep customer relationships, and a focus on specialized rather than commodity semiconductors. The company had survived multiple technology transitions, economic cycles, and strategic pivots. It had learned that in semiconductors, being excellent at everything meant being exceptional at nothing. That lesson would prove invaluable in what came next—a private equity transformation that would either forge a focused champion or destroy five decades of accumulated expertise.

III. The Private Equity Transformation (2006–2010)

The conference room at Philips headquarters was packed with lawyers, bankers, and executives on that September day in 2006. After months of negotiations, the deal was done: In September 2006, Philips completed the sale of an 80.1% stake in Philips Semiconductors to a consortium of private equity investors consisting of KKR, Bain Capital, Silver Lake Partners, Apax Partners and AlpInvest Partners. The price tag? €6.4 billion for what many considered a troubled asset in a cyclical industry.

This wasn't just any private equity deal—it was a who's who of buyout royalty. KKR, the firm that invented the leveraged buyout. Bain Capital, known for operational transformations. Silver Lake, the tech specialist. Together, they were betting they could transform a sprawling semiconductor conglomerate into a focused, profitable enterprise. The skeptics were numerous: private equity and semiconductors seemed like oil and water. Chip companies needed patient capital for R&D, not financial engineering and cost-cutting.

The new company name NXP (from Next eXPerience) was announced on August 31, 2006, and the company was officially launched during the Internationale Funkausstellung (IFA) consumer electronics show in Berlin. The name itself was a statement—this wouldn't be your father's Philips Semiconductors. But behind the rebranding was a more fundamental transformation brewing.

Frans van Houten, brought in as CEO, understood something crucial: NXP couldn't compete with Intel on processors, Samsung on memory, or TSMC on manufacturing. The company needed to find its niche and dominate it completely. His first moves were surgical. Non-core businesses were identified for divestment. The mobile phone chip division, once a crown jewel, was merged with STMicroelectronics' equivalent unit. Consumer products that competed on price rather than value were abandoned.

Then came 2008. Lehman Brothers collapsed in September, and suddenly NXP's private equity owners faced their worst nightmare: a portfolio company with billions in debt in the midst of a global financial crisis. Semiconductor demand cratered. Customers canceled orders. Credit markets froze. For a leveraged company like NXP, this could have been fatal.

Rick Clemmer, who took over as CEO in 2009, walked into a disaster. The company was burning cash, debt covenants were at risk, and bankruptcy wasn't out of the question. But Clemmer, a Texas Instruments veteran, saw opportunity in crisis. "When you're fighting for survival," he would later say, "you make decisions you should have made years ago."

The transformation was brutal but necessary. Headcount was slashed by 20%. Entire product lines were eliminated. Manufacturing facilities were closed or sold. But crucially, R&D spending in core areas—automotive, identification, and infrastructure—was maintained or even increased. This wasn't mindless cost-cutting; it was strategic focus.

The private equity owners, rather than pushing for a quick flip, provided crucial support. They helped renegotiate debt terms, provided bridge financing, and most importantly, backed management's vision of NXP as an automotive and industrial specialist rather than a broad-line semiconductor company. This patience would prove invaluable.

The newly independent NXP was ranked as one of the world's top 10 semiconductor companies. But rankings mattered less than the fundamental transformation occurring within. The company was shedding its conglomerate mindset and developing the lean, focused culture of a specialist. Engineers who once worked on dozens of disparate projects were now focused on a few key platforms. Sales teams that once called on everyone were now deep specialists in automotive or industrial applications.

By early 2010, the transformation was showing results. Despite the global recession, NXP was generating positive cash flow. The company had weathered the worst financial crisis in generations and emerged leaner, more focused, and surprisingly, more innovative. The automotive business, once a small part of the portfolio, was growing rapidly as carmakers added more electronics to their vehicles.

On August 6, 2010, NXP announced its initial public offering at Nasdaq, with 34 million shares, pricing each $14. The IPO raised $476 million, valuing the company at roughly $6 billion—less than what the private equity consortium had paid four years earlier. On paper, it looked like a failed investment. But the real value creation was in the transformation itself. NXP went public not as a troubled conglomerate spinoff but as a focused, profitable semiconductor specialist with clear market leadership in growing segments.

The private equity era had achieved something remarkable: it had taken a company with 50+ years of history and completely reimagined its future without destroying its core capabilities. The patient engineering culture of Philips had been preserved but coupled with American-style operational discipline and strategic focus. The stage was set for NXP to capitalize on two megatrends that would define the next decade: the explosion of mobile payments and the transformation of the automobile into a computer on wheels.

IV. Finding the Formula: NFC, Security & Early Automotive (2010–2014)

The demo at the 2011 Mobile World Congress was simple but revolutionary. An NXP engineer tapped his phone against a payment terminal, and the transaction completed instantly. No swiping, no PIN entry, just tap and go. The audience of mobile executives and technologists knew they were seeing the future of payments, and NXP owned the underlying technology.

Near Field Communication wasn't born in 2011—NXP (as Philips) and Sony had co-invented it years earlier. But timing in technology is everything, and by 2011, the pieces were finally coming together. Smartphones were ubiquitous, contactless payment infrastructure was expanding, and consumers were ready for a better payment experience. NXP didn't just have NFC chips; they had the entire ecosystem—secure elements, readers, and the software to tie it together.

The MIFARE platform, inherited from the Philips days, was already the global standard for transit cards. Hundreds of millions of commuters worldwide were unknowingly carrying NXP technology in their wallets. London's Oyster card, Hong Kong's Octopus card, Tokyo's Suica—all ran on MIFARE. This wasn't just market share; it was infrastructure lock-in. Once a city standardized on your technology for millions of transit cards, switching costs were astronomical.

But Rick Clemmer and his team saw beyond transit and payments. They recognized that security was becoming the killer app for semiconductors. As everything became connected—cars, homes, industrial equipment—everything needed to be secured. NXP's acquisition of the eGovernment and security assets positioned them perfectly for this transition. The company was already providing chips for passports, driver's licenses, and national ID cards. These weren't high-volume consumer markets, but they were incredibly sticky, high-margin businesses with 10+ year replacement cycles.

The automotive transformation was even more profound. In 2010, the average car had maybe $300 worth of semiconductors. By 2014, that number was approaching $400 and climbing fast. But the real story wasn't the dollar value—it was the changing nature of automotive chips. Cars were no longer just mechanical devices with some electronics; they were becoming rolling data centers.

NXP's automotive strategy was brilliantly focused. Instead of trying to compete everywhere, they targeted specific applications where they could dominate: keyless entry, in-vehicle networking, and car radio systems. These might seem like niche markets, but consider this: every modern car has keyless entry, and NXP had over 50% market share. That's not a business; it's a tollbooth on the automotive industry.

In 2012, revenue for NXP's Identification business unit was $986 million, up 41% from 2011, in part due to growing sales of NFC chips and secure elements. This growth wasn't just about volume—margins were expanding as NXP moved from selling components to selling solutions. A bare NFC chip might sell for $0.50, but a complete secure element solution with software could command $5 or more.

The company's approach to automotive was distinctly different from traditional semiconductor companies. While competitors focused on winning individual chip sockets, NXP thought in terms of platforms and ecosystems. They didn't just sell a CAN transceiver; they provided the entire in-vehicle networking solution. They didn't just offer a radar chip; they delivered complete radar modules with software and reference designs.

This platform approach had profound implications for the business model. Traditional semiconductor companies lived and died by the consumer electronics cycle—boom when a new iPhone launched, bust when PC sales slowed. But automotive design cycles were completely different. It took 3-5 years to design a chip into a car platform, but once you were in, you were guaranteed revenue for 7-10 years of production plus another decade of aftermarket sales.

By 2013, the transformation was complete. On December 23, 2013, NXP was added to the Nasdaq-100 index—recognition that this was no longer a troubled spinoff but a technology leader. The company had found its formula: focus on markets with high barriers to entry, long replacement cycles, and where security and reliability mattered more than raw performance or price.

But Clemmer knew that organic growth wouldn't be enough. The semiconductor industry was consolidating rapidly, and NXP needed scale to compete for the next generation of automotive platforms. The company had proven it could execute a successful transformation. Now it needed to prove it could execute a transformational acquisition. The target was already in sight: Freescale Semiconductor, another storied company with its own private equity transformation story, and the perfect complement to NXP's portfolio.

V. The Freescale Mega-Merger: Becoming an Automotive Giant (2015)

The leak came on a Sunday night in March 2015. The Wall Street Journal reported that NXP was in advanced talks to acquire Freescale Semiconductor for more than $11 billion. By Monday morning, both stocks were soaring, and the semiconductor industry was buzzing with speculation. Could NXP really pull off the largest chip merger in history?

The strategic logic was compelling. Both companies were semiconductor industry orphans—NXP spun out from Philips, Freescale carved out of Motorola. Both had survived private equity ownership and brutal restructurings. Both had abandoned consumer markets to focus on automotive and industrial applications. Both NXP and Freescale had deep roots stretching back to Philips and Motorola respectively, with similar revenue of $4.8 billion and $4.2 billion in 2013—they were almost perfect mirrors of each other.

But similar size didn't mean similar cultures. NXP was European at its core—methodical, engineering-driven, consensus-oriented. Freescale was pure American—aggressive, sales-driven, execution-focused. NXP's strength was in security and connectivity; Freescale dominated in microcontrollers and processors. NXP was strong in Europe and Asia; Freescale had deeper relationships with American automakers.

The negotiations were complex and sometimes contentious. Freescale had just gone public in 2011 after its own private equity ordeal and its shareholders—including Blackstone, Carlyle, and TPG—wanted maximum value. NXP needed to pay a premium but couldn't overleverage given its own recent history with debt. The final structure was elegant: $6.25 billion in cash and 0.3521 NXP shares for each Freescale share, valuing the combined company at roughly $40 billion.

Rick Clemmer's integration philosophy was radical for the semiconductor industry: "No conquest, no dominance." Instead of imposing NXP's way of doing things, he created integration teams with equal representation from both companies. Product portfolios were rationalized based on merit, not company origin. The best executives were retained regardless of which company they came from. It was a merger of equals in practice, not just press releases.

The numbers were staggering. The combined company would have 45,000 employees across 35 countries. The product portfolio included 25,000 different parts. Annual R&D spending would exceed $1.5 billion. But the real prize was market position: the merged entity would be the undisputed leader in automotive semiconductors with roughly 14% market share, almost double the nearest competitor.

On December 7, 2015, NXP and Freescale announced completion of the merger, creating a semiconductor giant with extraordinary market positions. In automotive microcontrollers: #1 globally. In automotive analog and power management: #1. In secure connectivity solutions: #1. This wasn't just market leadership; it was market dominance in the segments that mattered most for the future of transportation.

The timing was perfect. The automotive industry was at an inflection point. Electric vehicles were moving from science projects to mass production. Advanced driver assistance systems (ADAS) were becoming standard equipment. The concept of the "software-defined vehicle" was emerging. Every one of these trends required exponentially more semiconductor content, and NXP-Freescale had the complete portfolio to capitalize.

But the merger's impact went beyond products and market share. It fundamentally changed how automotive companies thought about semiconductor suppliers. Previously, carmakers might work with dozens of chip companies, each providing specific components. NXP could now offer complete platform solutions—from the smallest sensor to the main processor, all designed to work together seamlessly.

The integration proceeded remarkably smoothly. By mid-2016, the companies were fully merged, synergies were ahead of schedule, and the combined entity was winning major design victories. Customers who might have been nervous about NXP's size or Freescale's focus were reassured by the combination. Competitors who had dismissed both companies as second-tier players suddenly faced a formidable rival.

Infineon led the market with a share of 13.9%; it was followed by NXP and STMicroelectronics, holding a market share of 10.8% and 10.4%, respectively The Freescale merger had catapulted NXP into the top tier of automotive semiconductor suppliers, competing head-to-head with companies twice its size.

Yet even as NXP celebrated its newfound scale, storm clouds were gathering. In Silicon Valley, Qualcomm was struggling with slowing smartphone growth and activist investors. The mobile chip giant needed a new growth story, and NXP's dominant position in automotive looked increasingly attractive. The stage was set for one of the most dramatic episodes in semiconductor history—a $44 billion acquisition attempt that would consume two years, involve regulators on three continents, and ultimately fail in the midst of a trade war.

VI. The Qualcomm Saga: Politics, Trade Wars & $2 Billion (2016–2018)

Paul Jacobs was pacing the Qualcomm boardroom in October 2016. The son of Qualcomm's founder had just been pushed aside as chairman, activist investors were circling, and the company desperately needed a new narrative. Smartphone growth was slowing, and Qualcomm's licensing model was under attack globally. His eyes kept returning to one slide: NXP's automotive revenue projections. This could be Qualcomm's bridge to the future.

The initial approach was friendly. Qualcomm offered $110 per share, a 11.5% premium to NXP's stock price—roughly $38 billion total. For NXP shareholders who had ridden the stock from its $14 IPO price to nearly $100, it seemed like a dream exit. For Qualcomm, it was a transformation play: instant leadership in automotive, diversification beyond mobile, and access to NXP's secure connectivity portfolio.

But timing in M&A, like comedy, is everything. Between the October 2016 announcement and the planned closing, the world changed dramatically. Donald Trump became president with an aggressively protectionist agenda. China's semiconductor ambitions collided with American national security concerns. What started as a straightforward industrial merger became a geopolitical chess match.

By February 2017, the deal was already in trouble. NXP shareholders, seeing the semiconductor market heating up, demanded more money. Hedge funds led by Elliott Management accumulated massive positions and refused to tender their shares at $110. Qualcomm, under pressure from its own activists, eventually raised the bid to $127.50—a total value of $44 billion, making it the largest semiconductor acquisition ever attempted.

The regulatory review process was byzantine. Nine jurisdictions needed to approve the deal: the U.S., EU, China, Japan, South Korea, Russia, and others. One by one, they signed off, often with conditions. The EU demanded divestments in certain NFC products. Korea worried about automotive chip competition. But everyone was waiting for China.

The China review became a proxy battle in the escalating trade war. The Ministry of Commerce (MOFCOM) slow-walked the approval, requesting more information, scheduling and rescheduling meetings, finding new concerns. Behind the scenes, Chinese officials made it clear: this wasn't really about antitrust concerns. It was about leverage in broader trade negotiations.

For NXP employees, the uncertainty was agonizing. Should they integrate with Qualcomm or continue standalone planning? Major customers delayed decisions, unsure who they'd be working with. Competitors poached talent, arguing NXP would either disappear into Qualcomm or emerge weakened. The company was in corporate purgatory.

Rick Clemmer managed the situation masterfully. He maintained business as usual, continuing to invest in R&D and even making small acquisitions. His message was consistent: NXP would thrive either as part of Qualcomm or independently. But privately, he was preparing for both scenarios, developing integration plans while also crafting a standalone strategy.

The deadline drama was worthy of Hollywood. Qualcomm had to walk away if China didn't approve by July 25, 2018, at midnight San Diego time—July 26 in Beijing. As the deadline approached, there were frantic last-minute negotiations. Qualcomm's new CEO, Steve Mollenkopf, flew to Beijing. Trump administration officials lobbied their Chinese counterparts. NXP executives watched from the sidelines, powerless to influence the outcome.

On July 26, 2018, Qualcomm announced termination following inability to obtain SAMR's approval, resulting in Qualcomm paying NXP $2 billion as termination compensation The deal was dead, killed not by business issues but by geopolitics. For Qualcomm, it was a disaster—$2 billion termination fee, two years wasted, and no solution to its growth challenges. But for NXP, it was potentially a blessing in disguise.

The $2 billion termination fee was more than just compensation—it was transformation capital. NXP announced a $5 billion share buyback program, returning cash to shareholders who had waited patiently through the saga. But more importantly, the company now had resources to invest in the autonomous driving and electrification trends that were accelerating during the merger limbo.

The failed merger also validated NXP's strategy. Qualcomm, one of the semiconductor industry's giants, had been willing to pay $44 billion primarily for NXP's automotive position. This wasn't a desperate company being rescued—it was a strategic asset so valuable that it became a casualty of great power competition.

In his first all-hands meeting after the deal collapsed, Clemmer was philosophical: "We just got a two-year strategic planning exercise funded by Qualcomm. We know exactly what we're worth, what competitors think of us, and what customers need from us. Now let's go build the future of automotive semiconductors."

The Qualcomm saga had cost NXP momentum and created uncertainty, but it had also steeled the company's resolve. They had survived private equity ownership, the financial crisis, a mega-merger integration, and now a failed acquisition. Each challenge had made them stronger and more focused. The next chapter would prove whether NXP could fulfill its destiny as the semiconductor company that would power the automotive industry's transformation.

VII. The Standalone Strategy: Automotive Dominance (2018–2021)

Kurt Sievers was nervously adjusting his tie backstage at the 2020 Consumer Electronics Show. The German executive, about to be announced as NXP's new CEO, was inheriting a company at a crossroads. Rick Clemmer had navigated the Qualcomm drama brilliantly, but now NXP needed a new vision. Sievers' mandate was clear: prove that NXP didn't need Qualcomm to dominate the automotive semiconductor future.

The strategy Sievers unveiled was deceptively simple: "Secure Connections for a Smarter World." But underneath this tagline was a sophisticated bet on three interlocking trends. First, every device would become connected. Second, these connections needed to be secure. Third, edge computing would become as important as cloud computing. NXP was uniquely positioned at the intersection of all three.

The automotive industry was validating this thesis in real-time. Tesla had shown that over-the-air updates could transform cars into continuously improving platforms. Traditional automakers were scrambling to catch up, and they needed semiconductor partners who understood both the automotive industry's safety requirements and Silicon Valley's software sophistication. NXP was one of the few companies that spoke both languages fluently.

Then COVID-19 hit. In March 2020, automotive production ground to a halt. NXP's revenue dropped 20% in a single quarter. But Sievers, drawing on his 25 years of semiconductor experience, saw opportunity in crisis. While competitors cut R&D spending, NXP accelerated investments in radar, vehicle networking, and battery management systems. The logic was simple: the automotive industry would recover, and when it did, the shift to electric and autonomous vehicles would accelerate, not slow down.

The chip shortage of 2021 proved Sievers right in ways he couldn't have imagined. As automotive production restarted, manufacturers discovered they couldn't get enough semiconductors. A $1 chip shortage could halt production of a $40,000 vehicle. Suddenly, semiconductor suppliers weren't just vendors—they were strategic partners. NXP's broad portfolio and manufacturing flexibility made them indispensable.

In 2021, it was added to the S&P 500 stock index—recognition that NXP had graduated from semiconductor specialist to blue-chip technology company. The inclusion triggered billions in index fund purchases, but more importantly, it signaled that NXP was now considered essential infrastructure for the global economy.

The company's approach to the chip shortage was masterful. Instead of simply raising prices, NXP worked with customers to redesign products for available chips, accelerated qualification of alternative manufacturing sites, and even helped customers secure allocation of non-NXP components. This wasn't profit maximization; it was relationship building. When Toyota's production continued while competitors shut down, it was partly because of NXP's supply chain collaboration.

But the real innovation was happening in NXP's labs. The company was developing single-chip solutions for problems that previously required multiple components. Their new radar chips could detect not just distance and speed but also classify objects—distinguishing between a child and a shopping cart. Their battery management systems could extend EV range by 5% through better cell balancing. Their secure elements could update a car's software while preventing hacking attempts.

The S32 automotive processing platform, launched during this period, exemplified NXP's strategy. Instead of offering discrete processors, NXP created a scalable platform that could power everything from door controllers to autonomous driving systems. Carmakers could use one architecture across their entire fleet, simplifying development and reducing costs. It was the automotive equivalent of Intel's x86 dominance in PCs.

By late 2021, NXP's transformation was complete. The company that had started as a Philips division making discrete transistors was now the world's largest automotive semiconductor supplier. But more than market share, NXP had achieved something rare in the semiconductor industry: predictability. With automotive design wins locked in for the next 5-7 years, the company could forecast revenue with unusual accuracy.

The numbers told the story. Despite the COVID disruption, NXP's automotive revenue grew from $4.8 billion in 2019 to $5.8 billion in 2021. More impressively, operating margins expanded even as the company increased R&D spending. This wasn't growth at any cost; it was profitable growth driven by technology leadership.

Sievers' first two years as CEO had validated the standalone strategy. NXP didn't need Qualcomm's scale or resources to succeed. In fact, independence allowed the company to focus exclusively on automotive and industrial markets without the distraction of smartphones or consumer products. As the automotive industry accelerated its electric and autonomous transformation, NXP was perfectly positioned to benefit. The question was no longer whether NXP could survive independently, but whether anyone could challenge their automotive semiconductor dominance.

VIII. Modern Era: Software-Defined Vehicles & AI (2021–Today)

The prototype vehicle rolling onto the stage at CES 2024 looked like any other luxury sedan—until it didn't. With a software update pushed from NXP's cloud platform, the car's entire personality changed. Suspension stiffened for sport mode, the infotainment system reconfigured, and new autonomous features activated. The audience of automotive executives witnessed the future: cars as software platforms that happened to have wheels.

NXP delivered full-year 2024 revenue of $12.61 billion, a decrease of 5 percent year-on-year. But this headline number obscured a more complex reality. While total revenue declined due to inventory corrections and cyclical weakness, NXP's position in next-generation automotive platforms was strengthening dramatically. The company was trading current revenue for future dominance.

The software-defined vehicle (SDV) revolution was NXP's moment. Traditional cars had dozens of electronic control units (ECUs), each running proprietary software, barely communicating with each other. SDVs would have a few powerful domain controllers running standardized software, all connected by high-speed networks. This architectural shift played to every one of NXP's strengths: processing, networking, and security.

In January 2025, NXP announced it had entered into a definitive agreement to acquire TTTech Auto, a leader in safety-critical systems and middleware for software-defined vehicles (SDVs). This wasn't just another acquisition—it was NXP moving up the stack from silicon to software. TTTech's middleware would allow NXP to offer complete solutions, not just chips, accelerating SDV adoption.

The competitive landscape was shifting rapidly. Nvidia, flush with AI success, was pushing into automotive with powerful but expensive solutions. Qualcomm was trying again, offering Snapdragon automotive platforms. Intel's Mobileye was leveraging its autonomous driving expertise. But NXP had advantages none of them could match: decades of automotive relationships, safety certifications that took years to obtain, and a portfolio spanning from simple sensors to complex processors.

NXP announced industry-first wireless battery management system (BMS) based on Ultra-Wideband (UWB) connectivity, expanding its "FlexCom" family of wired and wireless BMS solutions...NCJ29Dx Ultra Wide Band (UWB) product family in its advanced UWB platform delivering precise and secure real-time localization to enable hands-free secure car access via smart mobile device and other UWB-based features. These weren't incremental improvements but fundamental innovations. Wireless BMS could reduce EV weight and complexity while improving reliability. UWB-based access was more secure than traditional key fobs and enabled new features like precise passenger detection.

The AI revolution presented both opportunity and challenge. While NXP couldn't compete with Nvidia on raw AI computing power, they dominated in edge AI—small, efficient processors that could make intelligent decisions without cloud connectivity. Their i.MX applications processors could run neural networks for voice recognition, gesture control, and driver monitoring while consuming minimal power.

China remained both NXP's largest market and biggest risk. Chinese automakers were leading the EV revolution, and NXP was designed into most of their platforms. But geopolitical tensions and China's push for semiconductor self-sufficiency created uncertainty. NXP's response was nuanced: continue serving Chinese customers while diversifying manufacturing and development outside China.

NXP introduced the S32J family of high-performance automotive Ethernet switches and network controllers to enable the next generation of software-defined vehicle development (SDV). This family represented NXP's vision for automotive networking: speeds up to 10 gigabits per second, deterministic latency for safety-critical applications, and security built into the hardware. As cars became data centers on wheels, NXP would provide the networking backbone.

The market dynamics were fascinating. The global automotive semiconductor market size was valued at USD 65.55 billion in 2023 and is projected to grow from USD 71.97 billion in 2024 and reach USD 123.04 billion by 2032, exhibiting a CAGR of 6.9% during the forecast period. Asia Pacific dominated the global market with a share of 41.5% in 2023. NXP was capturing an outsized share of this growth through strategic positioning in high-value segments.

Kurt Sievers' strategy was paying off. Instead of chasing volume in commoditized segments, NXP focused on products with high barriers to entry and long replacement cycles. A radar chip might generate $20 in revenue but enable thousands of dollars in ADAS features. A secure element might cost $2 but protect a $50,000 vehicle from theft.

Looking forward, NXP faces both enormous opportunity and significant challenges. The transition to electric and autonomous vehicles will require exponentially more semiconductor content. But competition is intensifying, customers are demanding more integrated solutions, and geopolitical tensions threaten global supply chains. NXP's response has been to double down on what made them successful: deep customer relationships, focus on specialized markets, and patient investment in next-generation technologies. The company that began making transistors in a converted Philips factory has become indispensable to the future of transportation.

IX. Playbook: Business & Investing Lessons

The conference room at KKR's offices was tense in 2009. NXP was bleeding cash, the financial crisis was deepening, and the private equity consortium faced a stark choice: double down or cut losses. Henry Kravis himself weighed in: "This is exactly when you separate great companies from mediocre ones. Do they have the courage to invest when everyone else is retreating?" That decision—to maintain R&D spending while cutting everything else—would generate returns that no spreadsheet could have predicted.

Private Equity Value Creation Beyond Financial Engineering

The NXP story demolishes the stereotype that private equity only knows how to cut costs and load debt. Yes, the consortium used leverage, but the real value creation came from strategic focus. They killed sacred cows—divesting the mobile business when smartphones were exploding, exiting consumer markets when volumes were attractive. This wasn't financial engineering; it was strategic surgery.

The PE owners brought something else invaluable: permission to think long-term while acting with urgency. Public company CEOs might have faced revolt for abandoning growing markets. But backed by patient capital with a 5-7 year horizon, management could make painful decisions that wouldn't pay off for years. The lesson: sometimes the best owner isn't the one with the deepest pockets, but the one who aligns timeframes with strategy.

The Power of Strategic "No"

In Silicon Valley, saying no to markets is heresy. The prevailing wisdom is to capture every possible customer, expand TAM relentlessly, and worry about profits later. NXP did the opposite. They said no to consumer electronics, no to mobile phones, no to commodity semiconductors. Each "no" was painful—walking away from billions in potential revenue.

But here's what those "no's" enabled: 60% gross margins versus industry averages of 40%. Five-year revenue visibility versus quarterly volatility. Customer relationships measured in decades, not product cycles. By refusing to compete where they couldn't win, NXP could dominate where they could. The lesson: in commoditizing industries, the only sustainable advantage is choosing your battles.

Platform Consolidation in Fragmented Markets

The Freescale merger wasn't just about scale—it was about creating platforms in a fragmented industry. Before the merger, carmakers worked with dozens of semiconductor suppliers, each providing point solutions. Post-merger, NXP could offer complete platforms—processor, networking, power management, and security from a single vendor.

This platform strategy created powerful network effects. The more components a customer used from NXP, the better they worked together. Development tools were shared across products. Support engineers became deeply embedded in customer organizations. Switching costs compounded with each design win. The lesson: in B2B markets, owning the platform beats owning components every time.

Managing Cyclicality Through Portfolio Construction

Semiconductors are notoriously cyclical, but NXP figured out how to smooth the waves. The key was portfolio balance: automotive for long-term visibility, industrial for stability, mobile payments for growth, and identification for recurring revenue. When smartphone NFC slowed, automotive accelerated. When automotive hit inventory corrections, industrial IoT picked up.

But the real insight was choosing end markets with different cycle timing. Automotive design cycles are 3-5 years, but production runs for a decade. Government ID programs plan in 10-year increments. Industrial equipment gets replaced every 15-20 years. By focusing on these long-cycle markets, NXP transformed from a cyclical semiconductor company into a steady growth story.

Why Automotive Semiconductors Are Different

The automotive semiconductor market breaks every rule of the broader chip industry. Moore's Law doesn't apply—a 10-year-old process node is perfectly fine if it's reliable. Winner-take-all dynamics don't exist—every carmaker wants multiple suppliers for critical components. Price erosion is minimal—once designed in, chips rarely get redesigned for cost savings.

Most importantly, the barriers to entry are enormous. Automotive-grade qualification takes years. Failure rates must be measured in parts per billion, not million. Support must be available for 15+ years. Liability for failures can reach billions. These barriers don't just protect margins—they create dynasties. The lesson: in technology, sometimes the best markets are the ones Silicon Valley ignores.

Capital Allocation Excellence

NXP's capital allocation since 2010 has been a masterclass. They've returned over $15 billion to shareholders while investing billions in R&D and making strategic acquisitions. The secret? Ruthless prioritization. Every dollar of investment had to meet hurdle rates that assumed semiconductor industry cyclicality.

The company's approach to M&A was particularly disciplined. They walked away from deals that didn't meet strategic criteria, even when activists pushed for growth. They paid fair prices, not auction prices. Most importantly, they integrated acquisitions fully, capturing synergies that justified premiums. The $2 billion Qualcomm termination fee? Immediately returned to shareholders rather than wasted on empire building.

Surviving Existential Threats

NXP has faced more near-death experiences than a semiconductor company should survive: the 2008 financial crisis with billions in debt, the Qualcomm merger uncertainty, COVID-19 demand collapse, and ongoing geopolitical tensions. Each crisis taught valuable lessons, but one stands out: maintain strategic flexibility at all costs.

This meant keeping manufacturing partnerships rather than building fabs, maintaining investment-grade credit ratings even if it meant lower returns, and diversifying customer and geographic exposure. It meant having Plan B for every Plan A. When Qualcomm walked away, NXP had a standalone strategy ready. When COVID hit, they had the balance sheet to continue investing. The lesson: in volatile industries, survival options are more valuable than growth options.

X. Analysis & Bear vs. Bull Case

Bull Case: The Inevitable Semiconductor Infrastructure Play

The bullish thesis for NXP isn't complicated: they own the tollbooths on the road to automotive's future. Every major automotive trend—electrification, autonomous driving, software-defined vehicles—requires exponentially more semiconductor content, and NXP is designed into nearly all of them.

Start with the math. The global automotive semiconductor market size was valued at USD 50.43 billion in 2024 and is expected to grow from USD 53.57 billion by 2025 to reach USD 86.81 billion by 2033, growing at a CAGR of 6.22% during the forecast period (2025–2033). But this understates the opportunity. The average semiconductor content per vehicle was $600 in 2024; by 2030, it could reach $1,500 in EVs and $3,000+ in autonomous vehicles. NXP doesn't need to gain share to double revenue—they just need to maintain position as content explodes.

The competitive moat is widening, not narrowing. Each new automotive platform requires 3-5 years of development and 10+ years of support. NXP is already designed into platforms launching through 2030. Competitors can't simply offer better chips—they need to replicate decades of automotive expertise, safety certifications, and customer relationships. By the time they catch up, NXP will have moved to the next generation.

The business model transformation is perhaps most compelling. NXP is evolving from a component supplier to a platform provider. The recent TTTech acquisition signals this shift—offering not just silicon but complete solutions including software and services. This moves NXP up the value chain, increases switching costs, and enables recurring revenue streams through software updates and cloud services.

Financially, the bull case is compelling. The company generates 55%+ gross margins, 30%+ operating margins, and converts nearly 100% of earnings to free cash flow. With automotive design wins providing 5+ year visibility, revenue predictability exceeds most software companies. The balance sheet is fortress-like, with investment-grade ratings and modest leverage. Management has proven disciplined in capital allocation, returning excess cash while investing for growth.

Bear Case: Cyclical Pressure Meets Structural Threats

The bearish view starts with a simple observation: NXP is trading near all-time highs while revenue is declining. Full-year 2024 revenue of $12.61 billion represented a decrease of 5 percent year-on-year. This isn't just inventory correction—it might signal structural challenges in core markets.

The China risk looms large. China represents roughly 35% of NXP's revenue, but more importantly, Chinese automakers are leading the EV revolution. If geopolitical tensions escalate or China successfully develops domestic alternatives, NXP could lose its largest growth market. The company's attempts to diversify are progressing slowly—you can't replace Chinese volume overnight.

Competition is intensifying from unexpected directions. Nvidia's automotive ambitions threaten NXP's processor business. Qualcomm hasn't given up on automotive despite the failed acquisition. Even Tesla is designing its own chips. As automotive semiconductors become more strategic, customers may choose to develop internal capabilities rather than rely on suppliers.

The technology transition risk is real. NXP dominates in traditional automotive architectures—distributed ECUs, CAN bus networking, conventional sensor fusion. But the shift to centralized computing, ethernet networking, and AI-driven processing favors different competencies. NXP's strength in MCUs and analog might become less relevant as cars become rolling supercomputers.

Cyclicality hasn't disappeared; it's just delayed. The automotive industry ordered aggressively during the chip shortage, building inventory buffers. As supply chains normalize, this inventory will need to be digested. Combined with potential recession and slower EV adoption, automotive semiconductor demand could disappoint for years.

The valuation poses challenges. At 20x+ forward earnings, NXP trades at a premium to semiconductor peers despite lower growth. The market is pricing in perfect execution on the automotive transformation. Any disappointment—a lost design win, share loss in key segments, or margin pressure—could trigger significant multiple compression.

The Verdict: Execution Risk in a Structural Growth Story

The truth, as always, lies between extremes. NXP owns irreplaceable positions in growing markets, but faces real challenges in maintaining leadership through technology transitions. The company's track record suggests they can navigate these challenges—they've successfully transformed multiple times before. But past performance doesn't guarantee future results, especially as the automotive industry undergoes its greatest transformation in a century.

For investors, NXP represents a classic quality-versus-value dilemma. The business quality is undeniable: strong competitive positions, excellent financials, proven management. But the valuation assumes continued excellence with little room for error. In a winner-take-all technology world, NXP has carved out a winner-take-most niche. Whether that's worth today's premium depends on your view of automotive's future and NXP's ability to shape it.

XI. Epilogue & "What Would We Do?"

Standing in NXP's Eindhoven headquarters, you can still see the original Philips buildings where this journey began 70 years ago. The contrast is striking: what started as a few engineers making transistors in a converted factory has become a $50 billion enterprise essential to global transportation. But the next decade might bring more change than the previous seven.

The Autonomous Vehicle Paradox

Here's the trillion-dollar question: will autonomous vehicles be NXP's greatest opportunity or existential threat? Bull case: fully autonomous vehicles will require 10x the semiconductor content of today's cars—more sensors, more processing, more redundancy. NXP's portfolio positions them perfectly. Bear case: if autonomy is winner-take-all, and the winner is Nvidia, Tesla, or a Chinese competitor, NXP becomes a commodity supplier.

The smarter bet might be that autonomy arrives gradually, then suddenly. Level 2 and 3 systems—where NXP dominates—will proliferate for a decade before true autonomy emerges. By then, NXP will have either moved up the stack or been acquired. The company's strategy of focusing on "automotive grade" rather than "cutting edge" might prove prescient. Cars need chips that work perfectly for 15 years, not ones that benchmark well for 15 minutes.

M&A Opportunities: Consolidate or Be Consolidated

If we were running NXP, the M&A strategy would be clear: acquire software capabilities aggressively. The TTTech acquisition shows they understand this, but they need to move faster. Every major automotive Tier 1 supplier is trying to move up the stack. NXP has the silicon foundation; they need the software superstructure.

Potential targets would include automotive software companies struggling with the complexity of hardware, sensor fusion specialists who need silicon integration, and edge AI companies focused on inference rather than training. The key: buy capability, not revenue. NXP doesn't need more chip companies; they need software that makes their chips indispensable.

On the defensive side, NXP remains an acquisition target. At $50 billion market cap, only a handful of companies could acquire them: Apple (for automotive ambitions), Amazon (for edge computing), or one of the Chinese giants if politics allowed. But NXP's best defense might be staying just large enough to be difficult to acquire but focused enough to avoid empire-building.

The China Hedge

The geopolitical risk requires a sophisticated response. Complete withdrawal from China would sacrifice too much growth; complete dependence would be existential risk. The solution: create mutual dependence. Design Chinese customers into NXP platforms so deeply that switching would take years. Simultaneously, build alternative supply chains and design centers in India, Vietnam, and Eastern Europe.

The ultimate hedge might be enabling Chinese automotive success globally. If Chinese EVs dominate world markets using NXP silicon, the company becomes too valuable to sacrifice in trade wars. This isn't capitulation; it's realpolitik. In semiconductors, technology leadership matters less than being embedded in winning platforms.

Lessons for Entrepreneurs and Investors

The NXP story offers profound lessons for building category leadership through focus. First, saying no to good opportunities is the price of saying yes to great ones. Second, in B2B technology, switching costs compound—every year you stay designed in makes replacement harder. Third, private equity can create value beyond financial engineering when strategy and capital structure align.

For investors, NXP demonstrates that boring can be beautiful. Automotive semiconductors lack the glamour of AI chips or the growth rates of cloud computing. But they offer something potentially more valuable: predictability in an unpredictable world. When your customer relationships are measured in decades and your design wins provide near-term visibility, volatility becomes opportunity rather than risk.

Final Reflections: The Power of Patient Transformation

NXP's journey from Philips spinoff to automotive semiconductor leader wasn't linear or easy. It required surviving multiple near-death experiences, making painful strategic choices, and maintaining investment through cycles. But the result is remarkable: a European company competing successfully in an industry dominated by American and Asian giants.

The next chapter will test whether NXP's patient, focused approach can survive in an industry increasingly driven by software, services, and winner-take-all dynamics. Can a company built on 20-year product cycles adapt to software updating daily? Can a culture rooted in engineering excellence embrace the messiness of software development? Can a business model based on selling chips evolve to selling solutions?

These questions don't have easy answers. But if history is any guide, NXP will answer them the same way they've answered every challenge: with patient investment, strategic focus, and the engineering discipline that has defined them since those first transistors rolled off the line in Nijmegen. In an industry obsessed with the next big thing, NXP has built an empire by perfecting the current thing. That might not be the Silicon Valley way, but it's proven to be a remarkably effective way to build lasting value in semiconductors.

The company that began in a converted Philips factory has become the backbone of automotive innovation. Whether it remains independent or becomes part of something larger, NXP has already secured its legacy: proving that in technology, focus beats diversification, depth beats breadth, and patience beats speed—at least in the markets that matter most.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube