Gibraltar Industries: The Steel-to-Solar-to-Back-to-Buildings Metamorphosis

I. Introduction & Episode Roadmap

Picture this: A Buffalo, New York industrial campus on a crisp autumn morning in 2025. Inside the corporate headquarters of Gibraltar Industries, CEO Bill Bosway reviews a press release announcing the company's intent to sell its entire Renewables business—the very segment that just five years earlier had been positioned as the crown jewel of the company's future. The decision caps a decade-long experiment with solar energy that began with bold pronouncements about riding "the solar coaster" upward and ends with a strategic retreat to the company's building products roots.

Gibraltar Industries (ROCK) trades on the NASDAQ with a current stock price around $49, valuing the company at approximately $1.5 billion. The company manufactures and provides products and services for the residential, renewable energy, agtech, and infrastructure markets in the United States and internationally, operating through four segments: Residential, Renewables, Agtech, and Infrastructure.

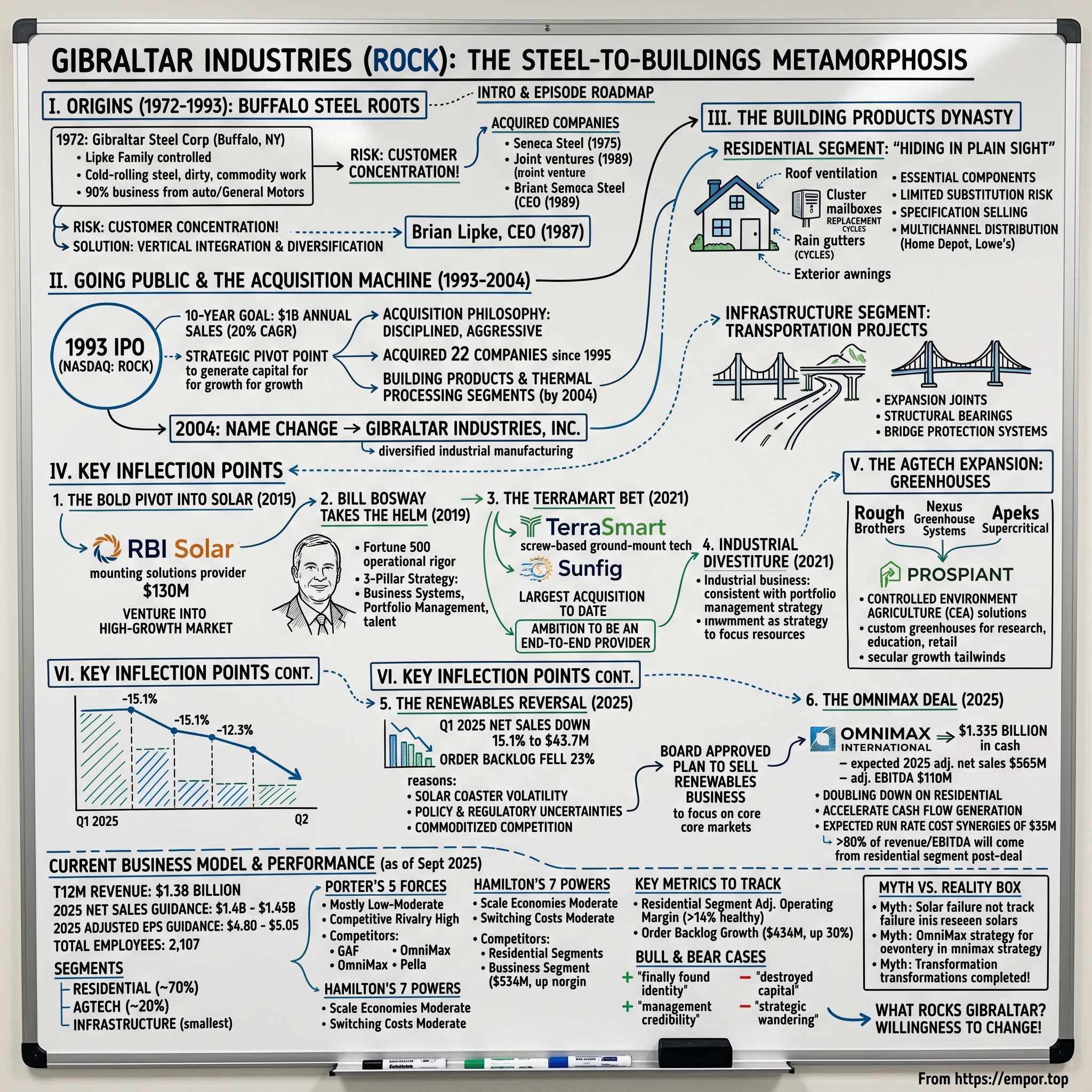

Yet what makes Gibraltar's story compelling isn't just a single pivot—it's the company's serial transformation across more than half a century. Established in 1972 as Gibraltar Steel Corporation in Buffalo, New York, the company evolved from entities controlled by the Lipke family. From a modest cold-rolling steel mill dependent on General Motors for 40% of its business, Gibraltar has reinvented itself multiple times: from commodity steel processor to diversified building products manufacturer, from building products to renewable energy champion, and now back again to building products with the announced $1.335 billion acquisition of OmniMax International.

This is a story about knowing when to enter markets—and knowing when to exit. It's about capital allocation discipline in a diversified industrial conglomerate. It's about the difference between strategic vision and strategic stubbornness. And ultimately, it's about whether Gibraltar's current leadership can execute one more successful transformation while avoiding the pitfalls that have derailed similar industrial roll-ups throughout corporate history.

The central question: Has Gibraltar Industries finally found its true north, or is it simply chasing the next cycle of building products demand as it once chased solar?

II. Origins: The Lipke Family and Buffalo Steel Roots (1972–1993)

Dr. Ken Lipke was not your typical steel baron. He was a chiropractor by training and ran a successful practice for 20 years. However, he was also a risk taker who enjoyed the competition of business. In the 1960s he established a stock brokerage, before raising the money to purchase Gibraltar Steel. The unlikely entrepreneur saw opportunity in Buffalo's fading industrial landscape—a city whose steel glory days were receding but whose infrastructure for the industry remained intact.

His new business was a cold reduction strip mill that bought hot-rolled black steel, then produced sheet metal that was primarily used by automakers. It was dirty, commodity work—the kind of business where margins depended entirely on operational efficiency and the whims of the Detroit auto manufacturers who consumed the product.

Buffalo itself was the perfect, if melancholy, backdrop for this story. With its access to the Erie Canal and Great Lakes, as well the power provided by Niagara Falls, was once a major center for the manufacture of steel. By the 1970s, though, the city epitomized America's Rust Belt decline—factories shuttering, populations declining, and entire neighborhoods hollowing out.

Ken Lipke didn't see despair. He saw consolidation opportunity.

Lipke's first major step in growing the business came in 1975 when he acquired another area cold-rolling operation, Seneca Steel. In that year he also added Buffalo's Beals, McCarthy & Rogers, as well as the Rochester firm of Follansbee Metals. In all, these transactions added $24 million in annual sales.

The acquisitive playbook was established early. Lipke installed a management team that included two of his sons, Brian and Neil. By 1977 Gibraltar Steel posted sales in excess of $50 million dollars.

But the company faced a fundamental problem that would shape its strategic thinking for decades: concentration risk. Management quickly began to realize that it was too dependent on the often cyclical automotive industry. As much as 40 percent of Gibraltar Steel's business came from General Motors alone.

The solution? Vertical integration and diversification. In 1987 the company acquired another cold-rolling operation in Cleveland with customers in a range of industries. In 1989 Gibraltar Steel entered into a joint venture in Ohio with Samuel Steed for steel pickling. In 1990 Gibraltar Steel opened its first materials management facility that serviced a Buffalo Ford Motors plant.

By 1987, Brian Lipke was named chief executive officer—the second generation assuming control at a pivotal moment when the company needed fresh thinking about its future.

The significance of this early history cannot be understated: Gibraltar learned that survival in commodity manufacturing required constant reinvention. The steel processing business was inherently volatile, margins were thin, and customer concentration could be fatal. These lessons would inform every major strategic decision for the next fifty years—sometimes wisely, sometimes not.

Controlled by the second generation of the Lipke family, Gibraltar Steel went public in 1993. The IPO would provide the currency needed to fuel the next phase of transformation—and begin moving away from the steel roots that had built the company.

III. Going Public and the Acquisition Machine (1993–2004)

The 1993 IPO was more than a financing event—it was a strategic pivot point. In order to fuel growth, the company decided to convert from a Subchapter S corporation to a Subchapter C corporation and make a public offering of its stock. Not only would Gibraltar Steel shed $27 million in debt, it would be in a position to use its stock in order to acquire larger companies. Thus, on November 4, 1993, Gibraltar Steel sold 2.5 million shares of common stock at $11 per share, which began to trade on the NASDAQ exchange.

The ambition was audacious. As Dr. Lipke had done when first purchasing the company, his son Brian announced an ambitious ten-year goal, this time to reach $1 billion in annual sales, a number that would require an average sales increase of 20 percent per year.

The acquisition philosophy that emerged was disciplined, if aggressive. Gibraltar Steel opted to grow more by acquisition than by starting new operations. According to Brian Lipke, "If we were to build a brand new plant somewhere, it would take a year to design the plant, a year to build it, and a couple of years to build up the business to the point where you are making a profit. But if you make an acquisition, you get $60 million or $70 million worth of [annual] sales the day you close the deal; then you can refine the business and improve its profitability." Looking to diversify its product offering to make the company less dependent on the automotive industry, as well as broadening it geographic base, Gibraltar Steel established strict guidelines for potential purchases.

The results were remarkable. By 2004, the transformation was undeniable. "We have acquired 22 companies since 1995 (including four so far in 2004), giving us two entirely new business segments: Building Products and Thermal Processing, which today account for more than two-thirds of our sales."

The scope of expansion was breathtaking. "Current annual sales are approaching $1 billion (up nearly six fold since 1993), with a goal to grow sales to $2 billion by 2009, or sooner. Today, we are in some of North America's fastest-growing markets, with 74 facilities in 26 states, Canada, and Mexico (compared to nine facilities in four states, mostly around the Great Lakes, in 1993). We now serve more than 10,000 customers around the globe, including many of the world's largest and most respected companies, compared to 900 customers (mainly in the Northeast) in 1993."

The transformation demanded a new identity. On October 28, 2004, Gibraltar's stockholders approved a proposal to change the name of the corporation to Gibraltar Industries, Inc. from Gibraltar Steel Corp., effective immediately. Gibraltar would retain its existing Nasdaq stock symbol, ROCK.

Gibraltar said that it has repositioned itself over the last decade as a diversified industrial manufacturing company, with a strong involvement in the building products and thermal processing markets, and its new name better reflects its current business mix and performance characteristics.

In the Building Products segment (which has annualized sales of approximately $500 million), we manufacture more than 5,000 products, and we are North America's leading producer of ventilation products.

The eleven years between the IPO and the name change demonstrated Gibraltar's core competency: identifying fragmented building products niches ripe for consolidation, acquiring market leaders, and achieving operational synergies through better purchasing, manufacturing efficiency, and distribution networks.

But the acquisition machine also planted seeds of complexity. Managing dozens of small companies across disparate product categories is inherently challenging. The question that would haunt Gibraltar over the following two decades: Was the company building a coherent industrial platform, or simply assembling a collection of loosely related businesses?

IV. The Building Products Dynasty: Mailboxes, Ventilation & Gutters

Walk into almost any American residential neighborhood built since the 1990s, and Gibraltar's products are hiding in plain sight. The roof ventilation keeping attics cool? Likely Gibraltar. The cluster mailboxes serving the subdivision? Probably Gibraltar. The rain gutters channeling water away from foundations? There's a good chance Gibraltar manufactured them, too.

The Residential segment offers roof and foundation ventilation products and accessories, such as solar powered units; mail and electronic package solutions, including single mailboxes, cluster style mail and parcel boxes for single and multi-family housing, and electronic package locker systems; roof edgings and flashings; soffits and trims; drywall corner beads; metal roofing products and accessories; rain dispersion products comprising gutters and accessories; and exterior retractable awnings.

These products share important characteristics that make them attractive from a business perspective: they are essential components of residential construction, face limited substitution risk, generate recurring demand through replacement cycles, and benefit from regulatory tailwinds. Building codes increasingly require proper ventilation. USPS requirements drive cluster mailbox adoption. Energy efficiency standards push homeowners toward better roofing accessories.

The business model that emerged is classic building products specification selling. Gibraltar's sales force works with architects, builders, and contractors to get products specified into construction plans. Once a product is specified, there's significant inertia—contractors order what's on the blueprint, distributors stock what contractors order, and switching costs are high for everyone involved.

The Infrastructure segment offers expansion joints, structural bearings, rubber pre-formed seals and other sealants, elastomeric concrete, and bridge cable protection systems. This segment may seem disconnected from residential products, but it follows the same strategic logic: find niches in construction where Gibraltar can achieve market leadership and specification advantage.

The company serves solar developers, renewable energy developers, home improvement retailers, wholesalers, distributors, and contractors. The multi-channel distribution strategy provides both reach and resilience—when new construction slows, repair and remodel activity often picks up through retail channels.

The beauty of building products? The demand is remarkably consistent over long periods. Houses always need ventilation. Subdivisions always need mailboxes. Roofs always need replacement eventually. It's not exciting, but it's reliable. And reliability in industrial businesses often beats excitement.

What Gibraltar learned about building products would inform its future strategic decisions—though not always in the ways management expected.

V. Key Inflection Point #1: The Bold Pivot into Solar (2015)

By 2015, Gibraltar faced a classic conundrum of mature industrial companies: decent profitability, solid market positions, but limited growth potential in core markets. The building products business generated cash, but organic growth was tied to housing starts and renovation cycles—not exactly transformational.

Then came solar.

Gibraltar first entered the solar space in 2015 when it acquired RBI Solar, a mounting solutions provider for commercial, utility-scale, and carport solar projects. Gibraltar Industries announced that it has acquired all of the outstanding shares of privately held RBI Solar, Inc., Rough Brothers Manufacturing Inc., and affiliates (collectively "RBI") for $130 million, subject to adjustments, in a transaction that will enable the Company to leverage its expertise in structural metals manufacturing and materials sourcing to meet fast-growing global demand for solar racking solutions.

The strategic logic was compelling. The global market for PV solar racking is estimated at $9.3 billion annually and is forecasted to grow at a 14% CAGR in the next four years, with the North American market estimated at $1.2 billion and forecasted to grow 9.8% annually over the next four years.

RBI itself had an impressive pedigree. Capitalizing on more than 80 years of design-build experience, Ohio-based RBI Solar has established itself during the past five years as North America's leading provider of photovoltaic (PV) solar mounting solutions to both the utility and commercial sectors.

The thesis made sense on paper: Gibraltar had deep expertise in metal fabrication, structural engineering, and manufacturing efficiency. Solar racking required all three. Unlike solar panels themselves—commodity products manufactured primarily in China—solar racking and mounting systems required local engineering, customization, and installation. It seemed like a natural adjacency.

"Acquiring RBI is an important step in the transformation of Gibraltar into a company with a higher rate of growth and best-in-class financial metrics," said Gibraltar Chief Executive Officer Frank Heard. "This acquisition directly aligns with key end markets and product platforms that we have strategically vetted and previously communicated to investors. Renewable energy, and solar racking in particular, is one of these markets, and a key opportunity for global business expansion."

Gibraltar Industries announced its acquisitions of RBI Solar and affiliate companies including Renusol Solar on June 10, 2015. RBI Solar would operate as a strategic business unit within Gibraltar, leveraging Gibraltar's strategic, tactical and financial resources to accelerate its global growth.

The bet paid off initially. RBI has established itself during the past six years as North America's fastest-growing provider of solar racking solutions. RBI was accretive to the Company's third-quarter results, adding adjusted earnings of $0.16 per diluted share on revenues of $81.6 million.

Gibraltar grew its portfolio in 2018 with SolarBOS, an electrical balance-of-systems company. The platform strategy was taking shape—Gibraltar wasn't just selling racking, it was building an integrated renewable energy solutions provider.

What management couldn't fully anticipate was how the "solar coaster"—the industry's notorious boom-bust cycles driven by policy changes, tariffs, and supply chain disruptions—would challenge even the best-laid plans. The thesis was right about solar's long-term growth. The execution would prove far more challenging than expected.

VI. Key Inflection Point #2: Bill Bosway Takes the Helm (2019)

Every transformation story needs a transformational leader, and Gibraltar's board found theirs in an unlikely place: Dover Corporation's Refrigeration & Food Equipment division.

Bill Bosway was appointed Chief Executive Officer and Director of Gibraltar in January 2019. Bosway joined Gibraltar with 29 years of experience in Fortune 500 industrial companies. Prior to joining Gibraltar, he served as President & CEO of Dover's Refrigeration & Food Equipment business. Prior to Dover, he served as Group Vice President of Refrigeration and Solutions at Emerson Electric, where he led global research and innovation, advanced manufacturing and engineering, supply chain, and quality organizations, which supported the $4 billion revenue climate technologies business.

For the past 29 years, Mr. Bosway, 53, has worked for two Fortune 500 industrial companies. For the past three years, he was Chief Executive Officer and President of Dover Corporation's Refrigeration and Food Equipment segment, with annual revenue of $1.6 billion. Prior to joining Dover, Mr. Bosway was with Emerson Electric for 26 years in a number of increasingly important roles. In addition to being Group Vice President, Refrigeration and Solutions, with $1.8 billion in revenue, he led global research and innovation, advanced manufacturing and engineering, and supply chain and quality organizations.

Bosway represented a new kind of leader for Gibraltar. The Lipke family had built the company through scrappy acquisitions and deal-making. Bosway brought Fortune 500 operational rigor—the systematic approach to lean manufacturing, continuous improvement, and portfolio optimization that defines the best industrial conglomerates.

Gibraltar Industries announced the appointment of William T. Bosway as President and Chief Executive Officer, and Director, effective January 2, 2019. As part of the Company's planned succession strategy, Frank Heard will remain employed with the Company in the newly created role of Vice Chairman of the Board through March 3, 2020, with the principal responsibility of ensuring a smooth leadership transition.

The succession was explicitly framed as continuing—not disrupting—Gibraltar's transformation strategy. "Since Bill Bosway was named CEO, he and his management team are doing an outstanding job of forming and executing a strategy to expand Gibraltar's leadership in growing markets that address core economic needs and leverage the company's key competencies during an unprecedented business environment."

With a three-pillar strategy focused on business systems, portfolio management, and organization and talent development, Gibraltar's mission is to create compounding and sustainable value with strong leadership positions in higher growth, profitable end markets.

Bosway's arrival coincided with a philosophical shift. Under previous leadership, Gibraltar had been an aggressive acquirer willing to enter new markets opportunistically. Under Bosway, the company adopted a more disciplined framework—evaluating businesses through a rigorous lens of growth potential, margin profile, and strategic fit.

This discipline would lead to both expansion and contraction. Some businesses would receive more investment. Others would be cut loose. The portfolio management approach that Bosway championed would ultimately lead to the biggest strategic decision of his tenure: exiting solar entirely.

Gibraltar Industries announced that it has named President and Chief Executive Officer William Bosway as Chairman of the Board of Directors effective January 1, 2022. The combined Chairman-CEO role signaled the board's full confidence in Bosway's vision—and concentrated decision-making authority in his hands.

VII. Key Inflection Point #3: The TerraSmart Bet & Solar Doubling Down (2021)

If the 2015 RBI acquisition was Gibraltar dipping its toe into solar, the 2021 TerraSmart deal was diving headfirst into the deep end.

Gibraltar Industries announced the further expansion of its solar energy portfolio through the acquisitions of TerraSmart and Sunfig. TerraSmart, the leading provider of screw-based, ground-mount solar racking technology, particularly used for solar projects installed on challenging terrain, was acquired for $220 million, subject to working capital adjustments.

In early January, New York-based Gibraltar acquired both solar racking company TerraSmart and software provider Sunfig in separate deals totaling nearly $225 million. Gibraltar Industries' largest acquisition to date was in 2021, when it acquired TerraSmart for $220M.

The vision was expansive. "Adding TerraSmart and Sunfig to our existing solar business significantly increases our presence in the $14.3 billion domestic solar energy market, strengthens our renewable energy platform, and advances our ambition to deliver higher growth and returns," said President and Chief Executive Officer Bill Bosway.

Gibraltar viewed these acquisitions as a way to expand its footprint in the U.S. market and become an end-to-end, turnkey provider of ground-mount infrastructure, tracker tech, and design software.

The financial projections were bullish. Gibraltar expects its solar energy platform within its Renewable Energy and Conservation segment to surpass $700 million in organic revenue by 2025 from an anticipated pro forma fiscal 2020 revenue base of approximately $400 million.

Management's optimism was infectious. "The solar coaster is going up," said Bill Vietas, president of the renewable energy group at Gibraltar Industries. The phrase captured the industry's notorious volatility while dismissing concerns. Yes, solar was cyclical—but the secular trend was unmistakably upward. Or so the thinking went.

RBI Solar, SolarBOS, Sunfig and TerraSmart, all part of the renewable energy group of Gibraltar, announced they are unifying under a shared brand, Terrasmart, to deliver a seamless customer experience through integrated product lines, and services. Fusing the history, experience, and strengths of four brands, the new Terrasmart will provide leading solar technologies and smart solutions across the project lifecycle. With a combined installed capacity of 19 GWs across 4,600 projects, Terrasmart is poised to power progress for commercial and utility PV sectors.

The combined platform looked formidable on paper. TerraSmart's screw-based technology solved real problems for developers. According to Reid, solar developers sometimes run into "land refusal" when trying to install ground-mount systems, leading to delays, pile deformations, or other issues. He said TerraSmart's ground-screw technology can help eliminate such problems and open project development for more difficult sites.

Yet even as Gibraltar doubled down on solar, warning signs were emerging. The industry faced trade investigations, tariff uncertainties, and policy volatility that would soon overwhelm even the best-positioned players. The solar coaster was indeed going up—but it was about to have a very steep drop.

VIII. Key Inflection Point #4: Industrial Divestiture & Portfolio Sharpening (2021)

While the TerraSmart acquisition grabbed headlines, a quieter transaction in 2021 revealed equally important strategic thinking: Gibraltar was willing to shrink to grow.

Gibraltar Industries announced the completion of the sale of its Industrial business to Pacific Avenue Capital Partners, a private investment firm focused on corporate divestitures and other special situations. "Our Industrial team has done a tremendous job of driving continuous improvement and accelerating growth of higher margin product lines," said President and Chief Executive Officer Bill Bosway. "For Gibraltar, the decision to divest the non-core Industrial business is consistent with our portfolio management strategy, and this sale enables us to focus more time, talent, and energy on executing to deliver higher growth and returns by increasing our participation in our core markets."

The divestiture of the lower-margin Industrial segment in 2021 underscored the commitment to concentrating resources on the higher-growth, higher-margin businesses.

Gibraltar will classify the Industrial business as a discontinued operation in its fourth quarter 2020 results. Gibraltar expects to use the cash received to reduce outstanding debt.

The Industrial divestiture embodied a crucial lesson: sometimes shrinking is growing. Capital tied up in lower-margin, slower-growth businesses can be redeployed more productively elsewhere. Management bandwidth is finite. Every hour spent managing a non-strategic business is an hour not spent on higher-potential opportunities.

This was Bosway's Fortune 500 playbook in action—the kind of portfolio rationalization that private equity firms and activist investors often demand but that family-controlled companies frequently resist. The Lipke-era Gibraltar might have held onto the Industrial business out of sentiment or inertia. The Bosway-era Gibraltar evaluated it dispassionately and acted decisively.

The irony, of course, is that this same portfolio management discipline would eventually be applied to solar—but not before Gibraltar had invested hundreds of millions more into the segment.

IX. The Agtech Expansion: Greenhouses & Controlled Environment Agriculture

Beyond solar and building products, Gibraltar built a third platform that has received far less attention but may prove strategically significant: controlled environment agriculture (CEA).

Controlled environment agriculture (CEA) solutions for growing fruits, vegetables, and flowers. Premium supplier of custom greenhouses for research, education, and retail.

The platform traces back to the RBI acquisition, which included greenhouse manufacturing operations with decades of history. Over the last 6 years, the renowned, US-based construction company Gibraltar has grown to be a significant player in the greenhouse industry. It started back in 2015 with the acquisition of Rough Brothers, a US-based designer and installer of greenhouses, conservatories, and related control systems.

With the acquisition of six brands in the horticultural and cannabis value chain, NASDAQ-listed Gibraltar Industries has gained a significant position in the Northern American Controlled environment growing and processing industry. Starting from today, they will operate in the market under one name: Prospiant. "With the launch of our new brand Prospiant, we're bringing all our experiences together to serve customers holistically," says Prospiant group president Mark Dunson. This new company unites the products and services of Apeks Supercritical, Delta Separations, Nexus Greenhouse Systems, Rough Brothers, Inc. (RBI), Tetra, and ThermoEnergy Solutions (TES).

Prospiant, the agriculture technology portfolio of Gibraltar Industries, Inc. (NASDAQ: ROCK), is a leading North American provider of controlled-environment agriculture (CEA) ag-tech solutions and custom greenhouses. Prospiant, the leading U.S. provider of controlled-environment agriculture (CEA) greenhouse solutions, is proud to announce the appointment of Burk Metzger as the company's new President. Burk will report directly to Gibraltar CEO Bill Bosway.

The thesis behind Agtech mirrors the original solar investment: secular tailwinds driving long-term growth. Local food production reduces supply chain vulnerabilities. Climate change makes outdoor farming less predictable. Consumer preferences increasingly favor fresh, local produce.

Backlog reached a record level $434 million, up 30%. During the quarter, the Lane Supply acquisition also delivered solid performance.

The segment has shown strong growth potential. Gibraltar Industries completed the acquisition of Lane Supply, Inc. on February 11, 2025 for $120 million, adding structural canopy manufacturing capability that serves the retail petroleum industry, restaurants, and more.

Unlike solar, the Agtech business has clearer competitive advantages for Gibraltar: engineering expertise, construction management, and long-term customer relationships. A commercial greenhouse is not a commodity—it's a complex, customized structure requiring decades of specialized knowledge.

X. Key Inflection Point #5: The Renewables Reversal (2025)

The announcement came on June 30, 2025, and it effectively declared defeat.

Gibraltar Industries announced that its Board of Directors has approved a plan to sell the Renewables business to focus its asset portfolio and resources on its building products and structures businesses – namely the residential, agtech and infrastructure segments. "As part of our ongoing strategic assessment and portfolio evaluation process we assess the overall attractiveness and key drivers of the end markets we are participating in, as well as our ability to extract value and generate returns in each of these end markets. We anticipate a simpler portfolio with the right resources and capital focused on building products and structures markets will yield stronger growth, margin expansion, and cash flow performance."

The exit from the renewables business was announced in June 2025, representing 20% of the previous portfolio.

What happened to the $700 million solar platform projection? What about the solar coaster going up?

The numbers tell a stark story. In the first quarter of 2025, net sales in the segment dropped 15.1% to $43.7 million, while the order backlog fell 23%, reflecting weaker demand and slower bookings in late 2024.

Multiple factors contributed to the reversal. "The solar industry continues to deal with trade and regulatory uncertainties driven by the impact from the two independent AD/CVD investigations, the second of which is currently in process. With the expiration of the tariff moratorium on panels associated with the first investigation expiring on December 3, 2024, the industry is working diligently to complete panel installations where projects are permitted and ready to move forward."

The solar coaster had indeed proven volatile—but not in the direction management expected.

Gibraltar Industries has announced its Board of Directors' approval to sell its Renewables business segment as part of a strategic portfolio restructuring. The company aims to streamline its focus on building products and structures businesses, specifically the residential, agtech, and infrastructure segments.

A sale of the renewables business is expected to close by year end 2025. As CEO Bosway explained, "those of you that know us, we announced in June that we were exiting our renewables business. If you think of the portfolio going forward, and you can go online and you can see our presentation where we've done some restatements, you get an idea of what the continued operations of the business looks like without renewables. Effectively, really what that does is about 70% of our portfolio is now building products, and that's really residential and some light commercial. Then we have about 20% or so as in agtech, and then we have a small sliver still in infrastructure."

The reversal raises uncomfortable questions. Was the original solar thesis wrong? Was the execution flawed? Were there structural problems in the solar racking industry that Gibraltar failed to anticipate?

The answer is probably some combination of all three. Solar racking proved more commoditized and competitive than expected. Policy volatility created unpredictable demand cycles. And Gibraltar may have lacked the scale to compete effectively against larger, more specialized players.

Whatever the cause, the decision represents a significant write-down of strategic capital—not just financial, but organizational and reputational. Gibraltar spent a decade building solar expertise, hiring talent, and making acquisitions. Walking away means those investments didn't generate the returns expected.

XI. The OmniMax Deal: Doubling Down on Residential (2025)

Less than five months after announcing the solar exit, Gibraltar unveiled its new strategic direction—and it involved going back to the future.

Gibraltar Industries announced that it has reached an agreement to acquire OmniMax International from funds managed by Strategic Value Partners, LLC and its affiliates for a cash purchase price of $1.335 billion. OmniMax is a leader in residential roofing accessories and rainware solutions with expected 2025 adjusted net sales of $565 million and adjusted EBITDA of $110 million. The purchase price represents an effective multiple of 8.4x based on OmniMax's expected 2025 adjusted EBITDA, run rate cost synergies of $35 million, and cash tax benefits of approximately $100 million.

The deal transforms Gibraltar's portfolio. Gibraltar expects the addition of OmniMax to immediately enhance EBITDA margins, accelerate cash flow generation, and create a more robust residential platform. Once the deal is completed, more than 80 percent of Gibraltar's revenue and adjusted EBITDA will come from its residential segment.

The acquisition is expected to drive stronger cash flow, significant cost synergies, and improved working capital to support deleveraging from a post-transaction leverage level of 3.7x 2025E adjusted EBITDA – including expected synergies – to 2.0-2.5x within 24 months from the close of the acquisition.

The financing is substantial. Gibraltar has in place committed financing from Bank of America, Wells Fargo and KeyBanc Capital Markets to finance the transaction in the form of up to $1.3 billion new term loan facilities and an upsized $500 million revolving credit facility.

The acquisition, which has been unanimously approved by Gibraltar's Board of Directors, is expected to close in the first half of 2026, subject to the satisfaction of customary closing conditions, including receipt of required regulatory approvals.

Gibraltar Industries will acquire OmniMax International for $1.335 billion, expanding its residential building products portfolio with brands including Amerimax, a maker of vinyl and metal rainware systems. OmniMax's product lines includes vinyl, aluminum and steel products for home improvements and construction, including rainwater diversion systems.

The strategic logic is clear: consolidate in building products where Gibraltar has proven expertise, generate synergies through combined purchasing and manufacturing, and build market leadership in categories with defensible competitive positions.

It's a full-circle moment. Fifty years after Ken Lipke bought a cold-rolling steel mill, Gibraltar is doubling down on the building products business that emerged from that original foundation. Solar was an interesting experiment. Residential building products is the main course.

XII. Current Business Model & Financial Performance

As of September 2025, Gibraltar Industries has a trailing 12-month revenue of $1.38 billion.

2025 Net Sales Guidance: $1.4 billion to $1.45 billion, growth of 8% to 12%. 2025 Adjusted Operating Margin Guidance: 13.9% to 14.2%. 2025 Adjusted EPS Guidance: $4.80 to $5.05, growth of 13% to 19%.

Gibraltar Industries has 2,107 total employees.

The company operates across distinct segments with different characteristics:

Residential accounts for approximately 70% of continuing operations revenue. This includes ventilation products, mail and package solutions, roofing accessories, rain dispersion products, and exterior awnings. The segment benefits from both new construction and repair/remodel demand.

Agtech represents roughly 20% of continuing operations. Through the Prospiant brand, Gibraltar designs, engineers, manufactures, and installs commercial greenhouses and controlled environment agriculture solutions.

Infrastructure is the smallest segment, providing expansion joints, structural bearings, and bridge protection systems for transportation infrastructure projects.

Operating margins increased 230 basis points driven by strong execution, supply chain management, and product line mix. Gibraltar Expands Presence in Residential's Metal Roofing Business: On March 31, 2025, Gibraltar completed the acquisition of two businesses in the Residential segment that primarily specialize in the manufacturing of metal roofing systems, along with metal wall panels, siding and trim products. The considerations paid for these two businesses totaled approximately $90 million in cash. During 2024, these acquired businesses recorded combined revenue of $73 million and adjusted EBITDA of approximately $13 million.

Under his tenure, 2024 net sales were $1.31B with adjusted EPS of $4.25, ROIC of 15.9%, and free cash flow equal to 11.8% of net sales.

The business model emphasizes lean manufacturing, specification selling, and multi-channel distribution. Gibraltar sells through home improvement retailers like Home Depot and Lowe's, wholesale distributors, and direct to contractors. This diversified channel strategy provides resilience against any single distribution partner gaining too much leverage.

XIII. Competitive Analysis: Porter's 5 Forces

Threat of New Entrants: LOW-MODERATE

Building products manufacturing requires significant capital investment in facilities, tooling, and distribution networks. But the real barrier is relationships: specification selling depends on decades of architect, builder, and contractor relationships that new entrants cannot replicate quickly. Gibraltar has acquired 22 companies since 1995, giving it two entirely new business segments. In the Building Products segment, the company manufactures more than 5,000 products and is North America's leading producer of ventilation products. That market leadership creates specification momentum that protects against new competition.

Bargaining Power of Suppliers: MODERATE

Steel and aluminum are commodity inputs whose prices fluctuate with global markets. Gibraltar manages this through multiple supplier relationships, forward purchasing contracts, and some vertical integration. The company's scale provides negotiating leverage, but it remains exposed to input cost volatility.

Bargaining Power of Buyers: MODERATE-HIGH

Its building products are sold through a number of sales channel including major retail home centers and building material wholesalers. Large retailers like Home Depot and Lowe's have significant negotiating power and can demand promotional allowances, inventory terms, and pricing concessions. The fragmented contractor base has less individual power, and specification by architects creates some switching costs.

Threat of Substitutes: LOW-MODERATE

Ventilation, mailboxes, and roofing accessories face limited substitutes—these are required components of residential construction. Metal roofing competes with asphalt shingles, but the value propositions differ enough that direct substitution is limited. The solar exit itself illustrates substitute risk: different solar mounting technologies competed for the same projects.

Competitive Rivalry: HIGH

Ameristar Fence Products, Pella, GAF Materials, Apogee Enterprises, and OmniMax International are some of the 8 competitors of Gibraltar Industries. The building products industry is fragmented with numerous regional and national competitors. Price competition can be intense in commodity-like segments, though Gibraltar's market leadership in ventilation and cluster mailboxes provides some pricing power.

XIV. Hamilton's 7 Powers Analysis

Scale Economies: MODERATE

By 2004, annual sales neared $1 billion, a substantial increase from its 1993 IPO. The company operated 74 facilities across 26 states, Canada, and Mexico, serving over 10,000 customers globally. Gibraltar's manufacturing scale provides purchasing leverage and distribution efficiency advantages over smaller regional competitors. However, building products manufacturing is not winner-take-all—regional players can compete effectively in local markets.

Network Effects: WEAK

Building products lack traditional network effects. Gibraltar's products don't become more valuable as more people use them.

Counter-Positioning: MODERATE

Gibraltar's willingness to exit solar demonstrates capital discipline that some competitors lack. The focus on "boring" building products while others chase growth markets provides strategic differentiation.

Switching Costs: MODERATE

Once Gibraltar products are specified into construction plans, contractors and distributors face switching costs to change suppliers mid-project. Repeat customers develop familiarity with Gibraltar products and ordering systems.

Branding: LOW-MODERATE

Building products are largely B2B with limited consumer brand awareness. Gibraltar's various brand names (Air Vent, Gibraltar Mailboxes, Prospiant) have professional recognition but not consumer brand power comparable to consumer products companies.

Cornered Resource: LOW

Gibraltar lacks proprietary resources that competitors cannot access. Manufacturing expertise can be replicated; customer relationships can be poached.

Process Power: MODERATE

Decades of acquisition integration and lean manufacturing experience provide operational advantages that competitors cannot easily replicate. The disciplined approach to portfolio management that led to the Industrial divestiture and solar exit represents process power in capital allocation.

XV. Key Metrics to Track

For investors monitoring Gibraltar's ongoing performance, two metrics deserve particular attention:

1. Residential Segment Adjusted Operating Margin

This measures the profitability of Gibraltar's core business and reveals whether the company can maintain pricing power while managing input costs. Operating margins increased 230 basis points driven by strong execution, supply chain management, and product line mix. Margins above 14% suggest healthy competitive positioning; sustained margin compression would signal either competitive pressure or cost management challenges.

2. Order Backlog Growth

Backlog reached a record level $434 million, up 30%. For Gibraltar's project-based businesses (Agtech, Infrastructure), backlog provides forward visibility into revenue. Sustained backlog growth indicates healthy demand; backlog declines could presage revenue challenges. This metric is particularly important as Gibraltar integrates major acquisitions like OmniMax.

XVI. Bull and Bear Cases

The Bull Case

Gibraltar has finally found its identity. After years of diversification experiments, the company is concentrating on building products where it has genuine competitive advantages: manufacturing expertise, specification relationships, and market leadership positions. The solar exit, while painful, demonstrates capital discipline that long-term investors should appreciate.

The OmniMax acquisition transforms scale in residential building products. Once the deal is completed, more than 80 percent of Gibraltar's revenue and adjusted EBITDA will come from its residential segment. Combined purchasing power, manufacturing optimization, and distribution efficiency should drive meaningful synergies.

The Agtech business provides optionality. Controlled environment agriculture remains a secular growth market, and Gibraltar's Prospiant brand has established expertise that differentiates it from commodity competitors.

Management credibility remains intact. Say‑on‑Pay Support: 97% support at the 2024 annual meeting. Bill Bosway has delivered operational improvements and made difficult decisions about portfolio composition. The board's confidence in his leadership is evident.

Valuation provides margin of safety. At roughly 1x sales and 10x EBITDA, Gibraltar trades at meaningful discounts to building products peers, potentially reflecting solar overhang that should dissipate once the divestiture closes.

The Bear Case

Gibraltar has destroyed capital through strategic missteps. The solar investment consumed hundreds of millions in acquisitions, capital expenditures, and management attention over a decade—and the ultimate return on that investment is almost certainly negative. Shareholders funded an expensive experiment that didn't work.

The OmniMax deal significantly increases leverage at a challenging time. Post-transaction leverage level of 3.7x 2025E adjusted EBITDA leaves limited margin for error. If residential construction weakens or integration proves difficult, the debt burden could constrain strategic flexibility.

The building products market faces secular headwinds. Housing affordability challenges, higher interest rates, and demographic shifts could suppress construction activity for years. Gibraltar is concentrating exposure in a market that may disappoint.

Management credibility is questionable. The same leadership team that championed solar as transformational is now framing the exit as strategic discipline. Both narratives cannot be true. Either the original solar thesis was flawed, or circumstances changed dramatically and management failed to adapt quickly enough.

The serial transformation pattern suggests strategic wandering. Gibraltar has reinvented itself multiple times over five decades. Is this strategic agility or lack of coherent vision?

XVII. Conclusion: What Rocks Gibraltar?

Gibraltar Industries' five-decade journey from Buffalo steel mill to diversified building products manufacturer illustrates both the opportunities and pitfalls of industrial transformation. The company demonstrated that commodity businesses can evolve into higher-margin, more defensible positions through disciplined acquisition and operational improvement. But it also showed how growth-seeking diversification can lead astray.

The solar chapter will likely be studied in business schools as a cautionary tale about market entry timing, capital allocation discipline, and knowing when to exit. Gibraltar entered solar with a compelling thesis—metal fabrication expertise transferring to solar racking—but underestimated competitive intensity, policy volatility, and execution challenges.

The return to building products represents either strategic focus or strategic retreat, depending on perspective. Optimists see a company finally concentrating resources where it can win. Pessimists see a company chasing the next cycle after the previous growth thesis failed.

"We anticipate a simpler portfolio with the right resources and capital focused on building products and structures markets will yield stronger growth, margin expansion, and cash flow performance which will drive higher returns for our shareholders."

Only time will reveal whether this latest transformation succeeds. But Gibraltar's history suggests that adaptation—even when it involves painful reversals—beats stagnation. Ken Lipke bought a steel mill and built a building products empire. His successors built a solar platform and abandoned it. Now Gibraltar bets its future on residential building products once again.

What rocks Gibraltar? The same thing that has always rocked it: the willingness to change, even when change is difficult. Whether that willingness translates into sustainable value creation depends on execution of the OmniMax integration, successful Renewables divestiture, and the wisdom to avoid the next shiny object when it inevitably appears.

Myth vs. Reality Box

Myth: Gibraltar's solar business failed because the company lacked technical expertise.

Reality: Gibraltar had legitimate solar racking expertise through multiple acquisitions. The business faced challenges from policy volatility, competitive pressure, and industry-wide disruptions that affected many players—not just Gibraltar.

Myth: The OmniMax acquisition represents a new strategy.

Reality: OmniMax represents a return to Gibraltar's historical playbook: acquiring building products companies to achieve scale and synergies. It's a new transaction but an old strategy.

Myth: Gibraltar's transformation is complete.

Reality: The Renewables divestiture must close, OmniMax must integrate successfully, and the combined company must demonstrate the synergies promised. Transformation is ongoing, not concluded.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube