Flex: The Physical Cloud and the Electric Backbone of the AI Era

I. Introduction & Episode Roadmap

Walk into any conversation in Silicon Valley about "the cloud" and you will hear language borrowed from theology. The cloud is everywhere and nowhere. It is weightless. It scales infinitely. It is, in the popular imagination, pure software — bits floating in some abstract ether, summoned by an API call and billed by the second.

That story is a beautiful fiction. The cloud is, in fact, one of the heaviest things humanity has ever built. It lives inside windowless concrete buildings the size of aircraft carriers, drawing the electricity of a mid-sized city, packed with metal racks that run so hot they now have to be cooled by liquid pumped directly across the silicon. Somebody has to design those racks. Somebody has to take raw grid power at medium voltage and step it down, distribute it, protect it, and shove it into thousands of GPUs without a flicker. Somebody has to bolt the whole thing together and ship it as a working unit. And it turns out that "somebody" is very often a company most consumers have never knowingly touched: Flex.

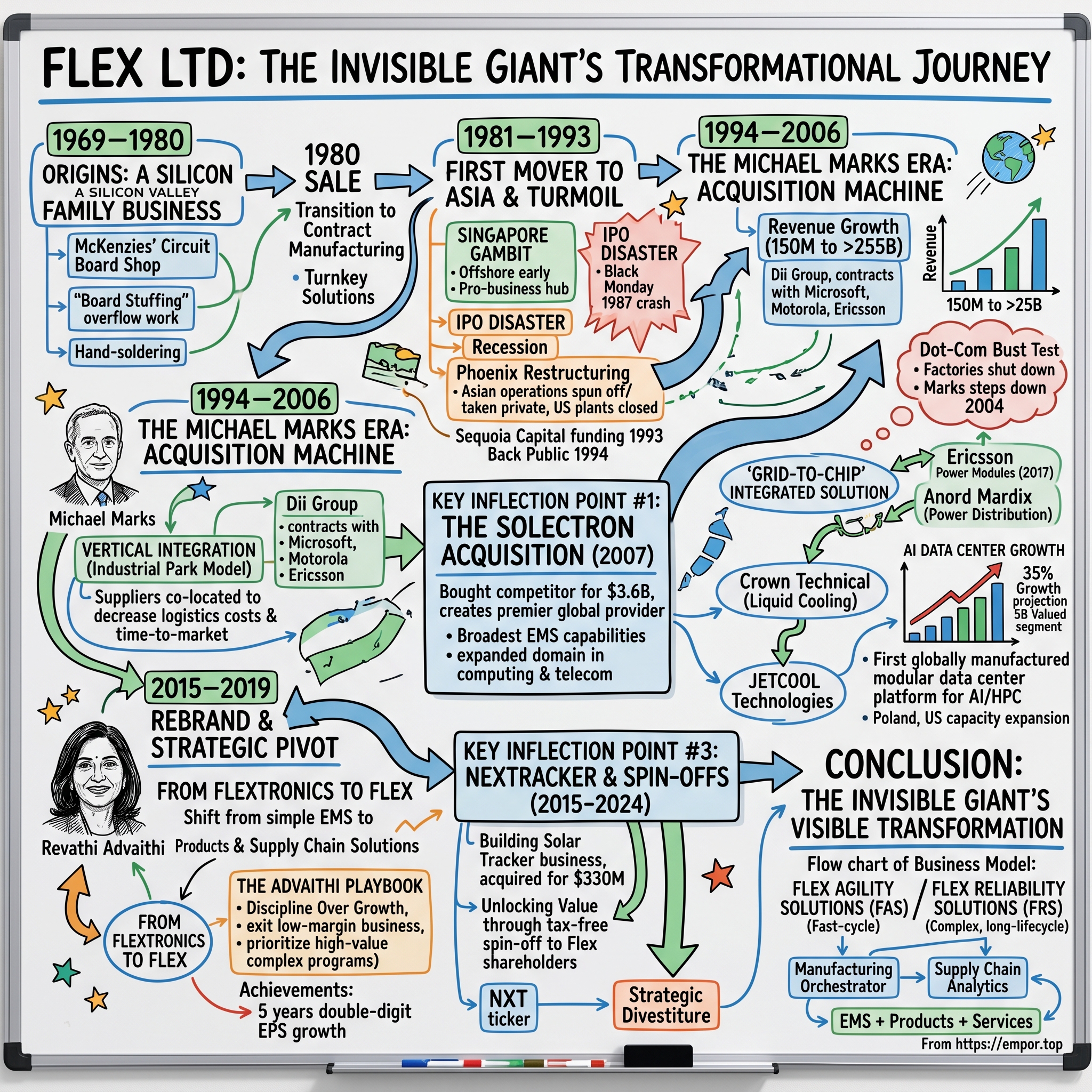

Here is the puzzle this article tries to solve. How does a business that started in 1969 as a husband-and-wife operation hand-soldering circuit boards in a San Jose garage end up, fifty-seven years later, as an S&P 500 component — added to the index on June 22, 2026 — supplying the electrical guts of the artificial-intelligence boom?17 The path runs through a near-death leveraged buyout in 1990, a re-listing out of Singapore, a manic decade of empire-building, a $3.6 billion merger that is taught as a cautionary tale, a brutal portfolio purge, and — most importantly for investors today — the discovery of a repeatable trick: take a low-margin, low-multiple contract-manufacturing business, use its scale to incubate a high-margin proprietary technology hidden inside, and then spin that technology out to shareholders at a valuation many times what the parent ever paid for it.

Flex did exactly that with Nextracker, turning a $330 million solar-tracker acquisition into a roughly $6.7 billion public company handed to its own shareholders tax-free.2 And on May 5, 2026, Flex announced it would run the same playbook again — this time with its Cloud & Power Infrastructure segment, the unit riding the AI data-center wave.[^3]

The thesis we will test is whether Flex has genuinely transformed from a commodity "board stuffer" into a structurally advantaged designer of physical infrastructure — or whether it is simply a cyclical manufacturer wearing the AI story as a costume, buying assets at the top of a hype cycle, and about to hand activists a victory lap that leaves the leftover "RemainCo" trading like the low-margin business it has always been.

Our roadmap: the Singapore restructuring; the Michael Marks scale wars and the Solectron mistake; the Revathi Advaithi "Eaton-ization" pivot; the Nextracker masterclass; the Cloud & Power Infrastructure crown jewel and its 2027 spin-off; the unglamorous-but-enormous core of medical and automotive manufacturing; the competitive war-game; the activist stress test led by Elliott Management; and finally the playbook lessons. Let's start in the garage.

II. From Silicon Valley Garages to Singapore LBO

Before the cloud, before the GPUs, before any of it, there was solder smoke in a San Jose garage. In 1969 Joe McKenzie and his wife Barbara-Ann started a small operation they called Flextronics, hand-assembling printed circuit boards for the first wave of Silicon Valley semiconductor companies.1 This was the most literal version of the business that exists: a chip company designs a board, and somebody has to physically place and solder the components onto it. The McKenzies did it by hand. In the industry it was called, with affectionate contempt, "board stuffing."

It is worth pausing on what kind of business this is at birth, because the DNA never fully leaves. Contract electronics assembly is, at its core, an arbitrage on two things: labor cost and logistics velocity. You are paid to do something the customer could theoretically do themselves but would rather not — buy the components, run the lines, manage the yield, ship the product. Your margin is the sliver between what the customer pays and what it costs you to execute. That sliver is thin, and it is always under attack, because your customer knows roughly what your costs are. This structural fact — that the customer can see your costs and squeeze them — is the gravitational force the entire rest of this story is about escaping.

The first attempt to professionalize came in 1980, when the McKenzies sold to a group of private investors who brought in Bob Todd as CEO. Todd is often credited with coining the phrase "contract manufacturing" to describe the category — an attempt to dignify board-stuffing into a strategic service.1 More consequentially, Todd understood the arbitrage in his bones. If the game is labor cost, you go where labor is cheap. In 1981 Flextronics became the first American contract manufacturer to set up offshore, opening a plant in Singapore.1 This was years before "offshoring" became a boardroom buzzword, and it planted the company's flag in Asia at the precise moment Asia was becoming the workshop of the electronics world.

Then came the near-death experience. The 1987 market crash and the recession that followed hit the U.S. electronics industry hard. Flextronics, still anchored to expensive American operations, started bleeding cash. By 1990 the situation was dire enough that a leveraged buyout was the only exit. The LBO did something brutal and clarifying: it shut down U.S. assembly entirely and carved out the healthy, fast-growing, low-cost Asian operations into a fresh entity, Flextronics International Ltd., domiciled and headquartered in Singapore.1

This is the first real strategic lesson buried in the rubble, and it rhymes with everything Flex does later. When a business contains both a dying engine and a growing one, the cleanest value-creating move is often a surgical geographic and legal split — let the dead part die under its own debt, and let the living part run free with a clean balance sheet and a low-cost base. The 1990 restructuring was, in embryonic form, the same logic Flex would one day apply to spinning out Nextracker and Cloud & Power Infrastructure: separate the high-growth asset from the low-growth one so each can be valued on its own terms. The company that emerged from the LBO was leaner, Asian, and hungry — and it was about to find a leader who would push that hunger to its limits.

III. The Michael Marks Era: The Scale and Consolidation Wars

In 1994, a Harvard MBA named Michael Marks took the slimmed-down, Singapore-based Flextronics public again. At the time it was a minnow — annual revenue under $100 million — re-entering the market as a survivor rather than a star.1 What followed over the next thirteen years was one of the most aggressive scale-building campaigns in the history of manufacturing, and it reveals a worldview: Marks believed that in contract manufacturing, scale was not just an advantage, it was the only durable advantage. Get big enough, buy enough, and the math would take care of itself.

His first signature innovation was the "Industrial Park." Instead of running a final-assembly plant that depended on a web of outside suppliers for plastic housings, metal frames, and cables — each adding shipping time, cost, and the risk of a missed delivery shutting your line down — Marks co-located everything on a single low-cost campus. Plastics injection molding, metal stamping, cable assembly, and final assembly under one roof, or one fence, in places like Guadalajara, Mexico and Sárvár, Hungary.1 The point was velocity. When the molded housing comes off a line a hundred meters from where it gets bolted onto the product, your supply chain measured in days collapses to one measured in hours. In a business where your customer's product can become obsolete in a quarter, speed is margin.

The second move was the great factory roll-up, and it is genuinely clever financial engineering dressed up as operations. Marks went to OEMs — Xerox, Ericsson, Hewlett-Packard — and made them an offer. Sell us your factories. We'll buy the physical plant, hire your workers, and in exchange you sign a multi-year contract to have us build your products. For the OEM the appeal was irresistible: factories are heavy, capital-hungry, low-return assets that drag down return on invested capital and clutter the balance sheet. Hand them to Flextronics and your reported returns improve overnight while you keep the part you actually care about — design and brand. For Flextronics, it bought instant scale and a guaranteed revenue stream. The catch, which would matter enormously later, is that Flextronics was absorbing exactly the low-return physical asset weight the OEMs were thrilled to shed. You can build a giant on that diet, but not necessarily a profitable one.

The high-water mark of the era's prestige was the original Xbox. When Microsoft decided to enter the console wars in 2001, it needed a partner who could manage the staggering logistics of a global consumer hardware launch — millions of complex units, hitting shelves worldwide on the same day, with brutal holiday-season deadlines. Flextronics won that work, and it was a statement: contract manufacturers were no longer just stuffing boards, they could orchestrate the entire physical realization of a flagship consumer product.1

But scale-as-religion has a dark side, and Flextronics walked straight into it in 2007. The context was an arms race. On the other side of the Pacific, 鴻海精密工業 Hon Hai Precision Industry — better known as Foxconn — was scaling at a velocity no Western firm could match, fueled by Apple's iPod and soon the iPhone. To Marks, the answer to bigger competition was to get bigger himself. So Flextronics acquired its largest American rival, Solectron, for $3.6 billion in cash and stock.1

On paper, consolidation in a scale business makes sense. In practice, Solectron was a trap. It was itself a roll-up — by some counts the product of more than thirty separate acquisitions — running a patchwork of incompatible ERP systems and a collection of factory cultures that had never truly been welded into one company. Flextronics did not buy a clean machine; it bought a museum of other people's integration debt. Standardizing the combined operating system took years, and during those years the friction showed up exactly where it hurts: margins. Adjusted operating margins sagged into the low single digits, the 2-3% range that defines the most commoditized end of the business. And the strategic prize never materialized, because Foxconn simply won the pure consumer-electronics scale war outright, with Apple as its engine.

The lesson Flex learned in blood here is the one that animates the modern company: bigness is not a strategy if the bigness is in a commodity. The Solectron deal made Flextronics enormous and structurally unprofitable at the same time — a contradiction that would eventually force the company to ask a much harder question than "how do we get bigger?" It would have to ask "how do we escape the commodity?" But that reckoning was still a decade away, and the next chapter of the company was about chasing volume even harder, until a new CEO arrived to tear up the strategy entirely.

IV. The Pivot: Revathi Advaithi and the Power Pivot

For most of the 2010s, Flex did what the Solectron logic told it to do: chase volume. The company built phones — including, fatefully, a substantial relationship assembling smartphones for Huawei — and a sprawling portfolio of consumer and industrial programs of wildly varying quality. The trouble with volume-at-any-margin is that it makes you a hostage. You are hostage to a single customer's product cycle, hostage to component shortages, and — as the U.S.-China trade war made painfully clear by 2018 — hostage to geopolitics you cannot control. When Washington moved against Huawei, a meaningful chunk of Flex's revenue became a liability overnight. After CEO Mike McNamara departed in late 2018, the board faced a company that was large, volatile, and structurally low-return.1

Their choice of successor in February 2019 told you the diagnosis. They did not hire a software visionary or a financial engineer. They hired an industrialist. Revathi Advaithi came to Flex from Eaton Corporation, where she had run the Electrical Sector as President and Chief Operating Officer, after earlier years at Honeywell.3 This matters enormously, because the mental model a leader brings is usually the model the company adopts. Advaithi's world was not consumer gadgets and quarterly hit-products; it was switchgear, circuit breakers, power distribution — high-reliability industrial gear where products are engineered to stringent specifications, qualified over years, and replaced rarely. In that world, you do not win by being the cheapest box-builder. You win by being the supplier nobody dares to switch.

She moved fast and unsentimentally. The first act was subtraction. Advaithi walked away from commoditized, high-volume, low-margin contract assembly — exiting underperforming sites and ending the volatile Huawei consumer relationship that had exposed the company to geopolitical whiplash.1 Walking away from revenue is one of the hardest things a manager can do, because it shrinks the top line and invites criticism. It is also the single clearest signal that a company has chosen profit over vanity.

What replaced the chase for volume was what we might call the "Eaton-ization" of Flex: import the industrial playbook wholesale. Prioritize margin over revenue. Enforce strict capital discipline. Push deeper into high-reliability end markets — healthcare, automotive, industrial — where engineering requirements are demanding, qualification cycles are long, and the resulting customer relationships are sticky enough to defend a real margin. This is the strategic pivot point of the entire company: the deliberate migration away from the part of the business where the customer can see and squeeze your costs, toward the part where switching away from you is so painful that pricing power finally tilts back in Flex's direction.

Did it work? The numbers offer a genuinely impressive answer, and they are worth reading as evidence rather than cheerleading. In fiscal 2026, Flex reported total revenue of $27.9 billion, up 8% year over year, with adjusted operating margin reaching a record 6.3% — up from the sub-4% swamp the company lived in for much of the prior decade.4 In the fourth quarter alone, adjusted operating margin hit 6.7%, the sixth consecutive quarter above 6%.4 For a business whose history is measured in 2-3% margins, moving the structural floor by several hundred basis points is not a rounding error; it is a different company.

Capital allocation tells the same story. Under Advaithi, Flex has bought back its own stock aggressively while it was cheap, reducing diluted shares to roughly 378 million in fiscal 2026 from about 398 million the year before, with $944 million in repurchases in fiscal 2026 alone — part of a multi-year reduction of more than 20% of the share count.4 Buying back a low-multiple stock and shrinking the count is the most reliable way for a mature manufacturer to compound per-share value, and it signals a management team that would rather return capital than empire-build for its own sake — a pointed contrast with the Marks era.

The board has backed that record with eye-watering pay alignment. Advaithi's fiscal 2026 total compensation was $44.39 million, a 63% jump from the $16.42 million of fiscal 2025, with roughly 97% of it equity-based and performance-contingent — leaving base salary at about 3% of the total.5 She beneficially owns roughly 1.4 million Flex shares, a stake worth well over $170 million at mid-2026 prices.5 A skeptic should note the obvious: a 63% raise in a single year invites scrutiny, and the structure is only as good as the targets behind it. But the directional point holds — when nearly all of a CEO's wealth rides on the share price and on hitting performance hurdles, her incentives are pointed where shareholders' are. The question that pay package was designed to answer was the AI data-center buildout and the coming spin-offs. To understand why those matter so much, you first have to understand the trick Flex perfected with a solar company nobody expected it to own.

V. The Nextracker Masterclass: The Incubate-and-Spin Playbook

In September 2015, Flex did something that made industry observers scratch their heads. It paid up to $330 million — $245 million in upfront cash plus up to $85 million in earnouts — for a company called Nextracker, which made solar trackers.2 Solar trackers are the steel-and-motor contraptions that tilt photovoltaic panels to follow the sun across the sky, squeezing more energy out of every panel. The reasonable reaction at the time was: why on earth is an electronics contract manufacturer buying a heavy-steel solar hardware business? It looked like classic conglomerate wandering — the "diworsification" that destroys value when a company buys things it has no business owning.

What the skeptics missed is that Flex was not really buying a solar company. It was buying a high-growth technology business and planning to feed it the one thing Flex had in abundance: global supply-chain scale. Inside Flex, Nextracker got two gifts it could never have bought on the open market. First, insulation. As a unit of a larger company, Nextracker was sheltered from the quarter-to-quarter brutality of being a small-cap public company in a boom-bust clean-energy sector; it could invest through cycles. Second, procurement muscle. Solar trackers are mostly steel and motors and electronics, and Flex buys metal, motors, and electronics by the mountain. Flex's logistics network and purchasing leverage let Nextracker scale its physical product faster and cheaper than a standalone start-up ever could, while Nextracker's own software for optimizing panel angles kept it ahead on the part customers actually paid a premium for. The combination carried it to the number-one position in global solar tracking.

Then came the masterclass — the multi-stage value unlock, executed with a patience that the Solectron-era Flex never possessed. In 2022, TPG Rise Climate invested $500 million into Nextracker at a $3.0 billion valuation, an outside party effectively stamping a price tag nine times Flex's original outlay on the asset.6 In February 2023, Nextracker went public on Nasdaq under the ticker NXT at roughly a $3.5 billion valuation, raising about $638 million in the IPO while Flex retained majority control.6 And then, on January 2, 2024, Flex completed the endgame: it distributed its remaining 51% stake directly to Flex shareholders in a tax-free spin-off, with Nextracker carrying a market capitalization of roughly $6.7 billion at that point.[^8]

Run the arithmetic and the elegance becomes obvious. Flex bought Nextracker for $330 million and delivered to its shareholders, across the staged sale and final distribution, value on the order of twenty times that — and crucially, the final transfer was structured to be tax-free, meaning shareholders received the full value of their Nextracker shares without the parent paying a corporate-level tax on the gain.[^8] This is the difference between running a high-multiple business inside a low-multiple one, where the market essentially ignores it, and liberating it so it can be valued on its own terms by investors who pay up for growth.

The deeper lesson — the one that reframes how to value Flex itself — is that the company proved its factories and supply chain could function as an incubator. The same boring scale that earns 2-3% building someone else's commodity hardware can, when pointed at a proprietary product with software content and a structural growth tailwind, manufacture not just the product but the multiple expansion. Flex's stock, the theory goes, perpetually undervalues whatever crown jewel is buried inside it, because the market prices the whole thing as a contract manufacturer. The fix is to keep finding, incubating, and then surgically removing those jewels. Having proven the playbook once, Flex went looking for the next jewel. It found it in the hottest corner of the global economy: the electrical infrastructure of artificial intelligence.

VI. The Current Crown Jewel: Cloud & Power Infrastructure

Picture the inside of a modern AI data center and forget the romance of "the cloud." What you are actually looking at is a power problem and a heat problem stacked on top of each other. A single rack of the latest AI accelerators can draw more electricity than a small office building, and each GPU can dissipate over a thousand watts of heat off a chip smaller than a playing card. Air cooling — fans, basically — has simply run out of road. The grid delivers power at voltages far too high to feed a server directly. Somewhere in between the high-voltage line outside and the silicon inside, an enormous amount of unglamorous, mission-critical engineering has to happen, and getting it wrong means either a melted chip or a dark building. This is the problem Flex's Cloud & Power Infrastructure segment exists to solve.

The financial materiality is the first thing to grasp, because it explains why this segment, not the legacy business, is what moves Flex's valuation. In fiscal 2026, Cloud & Power Infrastructure generated roughly $6.6 billion in revenue, up 38% year over year and ahead of management's own 35% target.8 On the fourth-quarter earnings call, management guided to extraordinary forward growth — on the order of 65% to 75% in fiscal 2027 and over 80% in fiscal 2028 — driven by the non-discretionary capital spending of hyperscalers building out AI capacity, a group Flex has confirmed includes Google.8 Those are growth rates you almost never see attached to a multi-billion-dollar hardware business, and they are the entire reason the AI narrative attached itself to a fifty-seven-year-old contract manufacturer.

A neutral reader should immediately ask the hard question: is that 9.2% segment operating margin in the fourth quarter — down 100 basis points year over year as the company absorbed infrastructure investment and cloud ramp costs — a sign of a business scaling into pricing power, or of a contract assembler dressing up commodity rack integration?8 The answer hinges on what CPI actually does, and here the vertical integration is the whole argument. CPI is not just bolting servers into frames. It designs and integrates the full power-and-cooling chain: medium-voltage switchgear and substations that take raw power off the grid; busways and power distribution units that route that power to the racks; direct-to-chip liquid cooling loops that pump coolant across thousand-watt-plus GPUs; and finally full-rack integration, assembling servers, switches, and cooling into single plug-and-play AI clusters that arrive at a data center ready to switch on.[^3] The more of that chain Flex owns as proprietary product rather than contract labor, the more the economics look like an industrial-equipment company and the less they look like board-stuffing.

And the way Flex assembled that chain was not by inventing it — it was by buying it, cheaply and deliberately, before the AI boom made these assets expensive. The M&A trail is worth reading as a single coherent strategy. In 2021 Flex acquired Anord Mardix, a critical-power and switchgear specialist, for $540 million.9 The benchmark is what makes it interesting: that was roughly 1.5 times revenue, at a time when pure-play critical-power companies like Vertiv, Eaton, and Schneider Electric traded at three to five times revenue. Flex bought a data-center power business at a fraction of where the public market valued comparable assets, by virtue of folding it into its industrial segment where nobody was paying for the growth.9

The buying continued and accelerated as the AI thesis sharpened. In November 2024, Flex acquired Crown Technical Systems for $325 million, adding medium-voltage switchgear and modular power enclosures and pushing the company's reach further up the chain toward the utility connection.10 The same month, it picked up JetCool Technologies for about $53 million — a small check for a specific and increasingly urgent capability: advanced direct-to-chip liquid cooling, the technology you need when air can no longer carry the heat away from the densest AI accelerators.[^3] Then, in March 2026, came the largest acquisition of the Advaithi era: Electrical Power Products, known as EP2, for $1.1 billion, securing more of the electrical backbone that connects the U.S. grid to the data-center floor.[^13]

That EP2 price tag is exactly where the bull and bear cases collide, and an honest analysis has to hold both. The bull says Flex is methodically vertically integrating the single scarcest input in the AI buildout — power delivery — and that owning the switchgear and the cooling and the rack integration lets it sell an integrated solution at industrial-equipment margins rather than assembly margins. The bear says Flex spent $1.1 billion on a power-equipment business in March 2026, near what may prove to be a cyclical peak in data-center capital spending, and that a single "digestion" phase in hyperscaler capex could turn today's prized acquisitions into tomorrow's impairment charges. Both can be true; which dominates depends on whether AI infrastructure demand is a multi-year secular build or a bubble, and nobody — including management — actually knows.

What management did do, on May 5, 2026, was reach for the proven playbook. Flex announced it will spin off the Cloud & Power Infrastructure segment into a separate public company, "SpinCo," targeted for the first calendar quarter of 2027 — explicitly running the Nextracker move again, liberating the high-growth jewel so the market can value it on its own terms rather than burying it inside a contract manufacturer.[^3] The leadership choreography is the tell. Revathi Advaithi will step down as Flex CEO to lead CPI SpinCo as its chief executive, while Michael Hartung, currently Chief Commercial Officer, will become CEO of "RemainCo," the core manufacturing business.[^3] When the architect of the turnaround chooses to follow the spun-out growth asset rather than stay with the legacy parent, it tells you where she — and the board's confidence — believes the value is going. It also raises an uncomfortable question for everyone holding the other half. Before we get to that, we should understand what RemainCo actually is, because it is far larger and far less glamorous than the headlines suggest.

VII. The Core Business: Inside ITS & RMS

Here is the fact that gets lost in every breathless AI headline about Flex: the Cloud & Power Infrastructure segment, for all its growth, is the minority of the company. Roughly three-quarters of Flex's revenue comes from the two unglamorous divisions that will constitute RemainCo after the spin-off.4 If you are an investor trying to figure out what you will actually own once the jewel is removed, this is the business that matters most, and it deserves more than a footnote.

The two divisions are Integrated Technology Solutions and Regulated Manufacturing Solutions. Integrated Technology Solutions, or ITS, the successor to what Flex used to call its Agility segment, runs on the order of $11 billion in revenue and handles complex systems integration for enterprise networking, telecom, lifestyle products, and cloud infrastructure.1 Regulated Manufacturing Solutions, or RMS, the successor to the old Reliability segment, runs on the order of $10 billion and is the heart of the Eaton-ized strategy: highly regulated, long-lifecycle manufacturing in healthcare — think medical imaging systems and drug-delivery pens — and automotive, including EV power electronics and advanced driver-assistance systems.1

The reason RMS is the strategic core, even though it grows slowly, comes down to one phrase: switching costs that are measured in years, not pennies. Consider what it actually takes to build a medical device or a safety-critical automotive component. A factory making FDA-regulated medical equipment must operate under ISO 13485 quality systems; an automotive supplier building safety systems lives under functional-safety standards like ISO 26262. Qualifying a manufacturing line for these products means multi-year facility audits, process validations, and regulatory sign-offs. Now imagine you are the medical-device company. A rival contract manufacturer offers to build your insulin pen 2% cheaper. To take that offer, you would have to re-qualify the entire line, re-validate the process with regulators, and accept the risk of a supply disruption on a product that, if it fails, can kill someone. You do not switch for 2%. You barely switch for 20%. That regulatory and qualification moat is what converts a commodity assembly relationship into a genuinely sticky one, and it is the structural reason RMS can hold a margin that the smartphone business never could.

To see whether Flex's roughly 6.3% blended operating margin is good, you have to put it next to the field, and the field is revealing.4 At the top by sheer mass sits Foxconn — 鴻海精密工業 Hon Hai Precision Industry — with revenue around $200 billion, the undisputed king of ultra-high-volume consumer assembly, the company that builds the iPhone, and historically a 2-3% operating-margin business. Foxconn is the cautionary picture of what maximal scale in a commodity buys you: enormous revenue, razor-thin profitability. 和碩聯合科技 Pegatron, at roughly $40 billion in revenue, plays a similar high-volume consumer and computing game at similarly thin margins.

The more instructive comparisons are the Western peers, because they are all running variations of the same escape-the-commodity strategy at the same time. Jabil, Flex's closest peer at about $29.8 billion in fiscal 2025 revenue and adjusted margins in the mid-5% range, made its own decisive move to shed consumer volatility: in December 2023 it sold its Apple-concentrated mobility manufacturing business to 比亚迪电子 BYD Electronic for $2.2 billion in cash.[^14] That is the same instinct that drove Flex out of Huawei phones — get the volatile, single-customer consumer concentration off the books. BYD Electronic, a roughly $26 billion-revenue arm of the Chinese EV-and-battery giant, was happy to buy exactly the kind of high-volume assembly the Western players were fleeing.11

Celestica is the peer that should make Flex investors both envious and thoughtful. At about $12.2 billion in fiscal 2025 revenue, it has posted industry-leading non-GAAP operating margins in the 7%-plus range, well above Flex's blended figure, precisely because it got early and concentrated exposure to hyperscaler AI server designs.12 Celestica is, in a sense, what a pure-play on the CPI thesis looks like — and the fact that the market has rewarded it richly is part of why Flex wants to liberate its own AI exposure into a separate stock. Meanwhile Sanmina, at roughly $8.1 billion in fiscal 2025 revenue and mid-5% margins, made its own bet on the AI server boom by acquiring ZT Systems' manufacturing operations from AMD for $3 billion in cash and stock, completed in October 2025 — AMD keeping the design talent and handing the physical manufacturing to Sanmina.[^17] Every one of these moves rhymes: the design-and-brand owner keeps the high-value intellectual property and offloads the heavy, capital-intensive physical manufacturing to a specialist. The whole industry is sorting itself into "asset-light designers" and "asset-heavy builders," and Flex is trying to be the builder that also owns a slice of the design.

So how does RemainCo actually win from here, stripped of its AI engine? The most concrete answer is geography. Flex's enormous nearshoring footprint in Guadalajara and Juárez, Mexico, positions it to capture U.S. clients desperate to de-risk away from Asia after a decade of trade wars and supply shocks. When an American medical or industrial company decides it can no longer afford to have its entire supply chain hostage to a single geopolitical flashpoint, a qualified, regulated factory a truck-drive from the U.S. border is a genuinely scarce and valuable thing. That is a real edge — but it is an edge in a slow-growth, mid-single-digit-margin business, and the central question for RemainCo holders is whether the market will pay a respectable multiple for stickiness and nearshoring, or revert to pricing it as the commodity manufacturer it descends from. To frame that debate properly, it helps to run the business through the standard strategic lenses.

VIII. Strategic Frameworks: Hamilton's 7 Powers & Porter's 5 Forces

Frameworks are only useful if they are applied with a skeptic's eye rather than as a checklist that flatters the company, so let's grade Flex honestly against Hamilton Helmer's 7 Powers — the seven distinct, durable sources of competitive advantage — and then run Porter's classic five-forces map of the industry's structure.

Scale Economies (Strong, but commoditized). With more than $26 billion in annual purchasing, Flex commands volume discounts from semiconductor and raw-material distributors that a small contract manufacturer simply cannot access.4 This is real. The caveat is that Foxconn, at roughly eight times Flex's revenue, has more of it, so scale is a defense against the small, not a weapon against the largest. Scale matters most where Flex can combine it with something proprietary — which is the whole CPI bet.

Switching Costs (High in RMS and CPI, low in commodity ITS). This is Flex's best-earned power, and it is unevenly distributed. In regulated medical and automotive manufacturing, the multi-year qualification and re-certification burden makes switching genuinely cost-prohibitive, as described above. In custom-engineered power infrastructure, bespoke tooling and integration create similar friction. In the more commoditized corners of ITS, switching costs are far lower. The strategic migration of the company is precisely a migration up the switching-cost curve.

Counter-Positioning (the most interesting, and Strong in CPI). Counter-positioning is when an incumbent cannot copy your model without damaging its own. Flex is doing something neither of its two natural competitor classes can comfortably match. Traditional contract manufacturers only build the box the customer designed — they have no proprietary power or cooling products to sell. Pure industrial-power players like Eaton or Vertiv have proprietary switchgear and cooling but lack Flex's scale in actually integrating full server-and-compute racks. Flex sits in the seam: it can both manufacture at scale and sell its own proprietary power and cooling content, integrating the whole AI cluster. For a box-builder to add proprietary products means becoming a different company; for an equipment maker to add rack-scale integration means the same. That genuine in-between position is the strongest part of the bull case — though it is young and unproven across a full cycle.

Cornered Resource (Moderate). Flex's proprietary direct-to-chip cooling designs from JetCool and its modular enclosure systems from Crown and EP2 are real, differentiated assets. But they were bought, not invented, which means a deep-pocketed rival could in principle buy comparable capabilities. This is a power of moderate, not overwhelming, durability.

Process Power (High). Decades of running complex, multi-tier global logistics and executing factory-line transitions across thirty-odd countries is a genuinely hard-to-replicate organizational capability — the accumulated "Flex Playbook." This is tacit knowledge embedded in people and systems, and it is one of the more durable things the company owns.

Network Effects (Weak). There is essentially no mechanism by which one Flex customer makes Flex more valuable to the next. This is simply not a network-effects business, and pretending otherwise would be dishonest.

Brand (Moderate). In mission-critical medical and automotive work, a long reputation for reliable quality has real value — buyers in those fields are intensely risk-averse. But it is a B2B reliability reputation, not consumer pricing power.

Now Porter, which describes the industry's attractiveness rather than Flex's individual edge. Bargaining power of buyers is moderate-to-high: hyperscalers and large OEMs are enormous and sophisticated, and they squeeze. The whole point of Flex's proprietary-product push is to shift a little of that power back toward itself. Bargaining power of suppliers is moderate: Flex depends on silicon fabs and component distributors, but its purchase volumes blunt their pricing power. Threat of new entrants is very low — replicating a footprint of audited, certified medical and automotive factories across thirty countries requires billions in capital and decades of accumulated trust, which is the single best structural feature of this industry. Threat of substitutes is low: the only real substitute is insourcing, where an HPE, Dell, or hyperscaler builds its own factories, and that is so capital-inefficient that the long-run tide runs the other way, toward outsourcing. Competitive rivalry is high but increasingly disciplined and consolidated: the big players — Jabil, Flex, Celestica, Sanmina, Foxconn — are shifting their competition away from suicidal price wars and toward engineering and specialized AI and power-infrastructure capability.

Add it up and the honest verdict is a business with a genuinely improving structural position — strong switching costs and process power, a real counter-positioning angle in CPI, operating in an industry with formidable entry barriers — but with no single overwhelming moat, meaningful buyer power, and an edge in cooling and power that was purchased rather than invented. That is a good business getting better, not an unassailable one. Which is exactly the kind of situation that attracts activists, and Flex has now attracted two of the most famous in the world.

IX. Activist / Skeptical-Investor Stress Test

Activists do not waste their time on companies they cannot move. The fact that Flex has, within five years, attracted two marquee activist firms is itself a statement: it tells you sophisticated investors believe there is trapped value here that management can be pushed to release. The history is instructive precisely because the first campaign worked so well.

In 2021, Scott Ferguson's Sachem Head Capital Management built a stake of roughly 4.7% in Flex and pushed for exactly the move that would later be celebrated as a masterclass — separating Nextracker to unlock its value.13 Flex complied, and the result was the staged sale and tax-free spin-off that delivered billions to shareholders. Sachem Head's campaign is the cleanest possible proof of the trapped-jewel thesis: an outsider looked at Flex, saw a high-multiple business buried inside a low-multiple wrapper, applied pressure, and was vindicated by the outcome.

Which brings us to May 2026, when Paul Singer's Elliott Management — perhaps the most feared activist firm in the world — disclosed a $1.5 billion stake in Flex, a position that coincided almost exactly with the announcement of the Cloud & Power Infrastructure spin-off.14 The timing is doing a lot of work here, and a neutral observer should sit with the ambiguity. One reading is that Elliott arrived to enforce the spin-off and capital discipline. Another is that Elliott saw a management team already executing the very playbook an activist would demand and simply wanted exposure to the value unlock. Either way, the presence of a $1.5 billion Elliott position is both a vote of confidence in the strategy and a warning that this management team will be held relentlessly accountable for executing it well. Elliott does not accept value-destructive missteps quietly.

So what would a genuinely skeptical investor — a thoughtful long or an outright short — challenge about Flex right now? Four things stand out, and none of them have clean answers.

First, the RemainCo value trap. Once CPI is spun out in early 2027, the company left behind is ITS and RMS — a slower-growing, mid-single-digit-margin contract manufacturer stripped of its AI growth engine. The entire spin-off thesis assumes the sum of SpinCo and RemainCo is worth more than the combined company. But what if RemainCo's multiple compresses straight back to a legacy contract-manufacturer level — say a high-single-digit price-to-earnings ratio — erasing a chunk of the value the spin was supposed to unlock? Nextracker worked partly because what remained was still a large, improving business; the bet is that RemainCo's switching costs and nearshoring edge earn it a respectable multiple rather than the commodity discount its lineage suggests. That is a real open question, not a settled win.

Second, overpayment at the AI peak. We have already named the tension: the $1.1 billion for EP2 in March 2026 and the $325 million for Crown in late 2024 were spent acquiring power-infrastructure assets while AI data-center spending was running white-hot.10[^13] If hyperscaler capex enters a digestion phase or a genuine cyclical slowdown, those assets could require painful write-downs, and Flex would have repeated, in miniature, the Solectron error of buying aggressively at the wrong moment. Management's bet is that AI power infrastructure is a secular, multi-year build; the bear's bet is that it is a cycle that will turn. This is the single biggest swing factor in the story.

Third, executive disruption. The most respected operator in the company, Revathi Advaithi, is leaving to run SpinCo. Michael Hartung inherits the slower-growth RemainCo. The bull frames this as putting the best leader where the value is; the bear asks whether draining the turnaround architect from the core medical and automotive franchise weakens execution in exactly the regulated, exacting end markets where execution is everything. Leadership transitions in complex manufacturing are not cost-free, and this one removes the person most identified with the company's revival from the larger of the two halves.

Fourth, customer concentration. Flex's cloud business leans on a small number of hyperscalers, with Google a confirmed customer.8 If a major customer redesigns its servers, brings work in-house, or shifts to a rival — Sanmina's newly acquired ZT manufacturing arm being an obvious alternative — the revenue impact on the growth engine could be severe and sudden. Concentration is the dark twin of landing whale customers: the wins are huge, and so is the exposure when one wobbles.

None of these is a knockout blow, but together they explain why a stock riding an AI narrative can still trade with a discount baked in. The market is pricing both the dream of two clean, fairly valued public companies and the risk that the leftover half disappoints or the cycle turns. With the stress test on the table, the playbook lessons come into sharper focus.

X. Playbook & Core Business Lessons

Strip away the fifty-seven years of history and three durable lessons remain, each of which generalizes well beyond Flex.

Lesson 1: The incubation model for physical conglomerates. The central insight Flex stumbled into and then weaponized is that a high-multiple business buried inside a low-multiple parent is, from the market's point of view, nearly invisible. The fix is structural, not operational: incubate the jewel using the parent's scale, then surgically separate it so it can be valued on its own terms — ideally tax-free. Nextracker turned $330 million into roughly $6.7 billion of liberated value; the CPI spin-off is the same bet at larger scale.2[^3] The caveat, which the RemainCo debate makes vivid, is that this only creates value if what remains is itself worth owning — serial spin-offs can hollow out a parent if every good asset eventually walks out the door.

Lesson 2: Margin over volume. The Solectron era taught Flex, expensively, that scale in a commodity buys revenue and not much else. The Advaithi era inverted the priority: walk away from volatile, low-margin, geopolitically exposed volume — even when it shrinks the top line — and redeploy toward sticky, regulated, high-switching-cost markets. The proof is in the structural margin floor moving from sub-4% to a record 6.3%.4 For any business tempted to chase revenue for its own sake, Flex is a fifty-year case study in why the quality of revenue matters more than the quantity.

Lesson 3: The Eaton playbook applied to tech. The deepest move was importing an industrialist's mindset into a contract-manufacturing company. The transition from pure service — building the box the customer designed — to a "products plus services" model, where Flex sells its own switchgear, enclosures, and cooling, is the mechanism that shifts bargaining power back toward the manufacturer. A service provider competes on cost and is squeezed; a provider of differentiated, integrated products earns the right to a real margin. Whether CPI fully delivers on that promise across a cycle is unproven, but the strategic logic — escape the commodity by owning proprietary content — is the throughline connecting the 1990 LBO to the 2027 spin-off.

XI. Epilogue

Flex is no longer accurately described as a board stuffer, and it has not been for some time. What it has become is harder to name: something like the physical holding company of the digital world, the firm that designs, powers, cools, and assembles the heavy infrastructure so that software giants can pretend the cloud is weightless. The 1969 garage and the 2026 AI data center are connected by a single thread — the relentless effort to turn the thankless work of physically building other people's products into something that earns a durable, defensible profit.

The verdict on whether that transformation is real or costumed will be written over the next eighteen months, and the things to watch are concrete. Track the execution of the Cloud & Power Infrastructure spin-off targeted for early 2027 — whether it completes cleanly and at what valuation the market assigns the two halves. Track RemainCo's margin under Michael Hartung — whether the regulated-manufacturing core holds its mid-single-digit profitability without the architect of the turnaround in the chair. And track how the data-center power acquisitions perform when the macro cycle next turns, because that is where the overpayment risk either materializes as write-downs or proves to have been farsighted positioning.

If you want to follow this company with two or three numbers rather than twenty, watch the Cloud & Power Infrastructure revenue growth rate against management's 65%-plus guidance — the single cleanest read on whether the AI demand is real and durable — and watch the consolidated adjusted operating margin, the master gauge of whether the escape from the commodity is holding. Everything else in the Flex story, from Singapore to Solectron to the spin-offs, ultimately resolves into those two questions: is the growth real, and does it pay?

References

-

Flex Annual Report for Fiscal Year 2025 (Form 10-K) — SEC, 2025-05-16 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Flextronics Acquires Nextracker for up to $330M — Greentech Media, 2015-09-08 ↩↩↩

-

Flex Reports Fourth Quarter and Fiscal 2026 Results — PR Newswire, 2026 ↩↩↩↩↩↩↩

-

Flex Proxy Statement (Form DEF 14A) detailing Executive Compensation — SEC, 2026-06-24 ↩↩

-

Marvell Technology and Flex Set to Join S&P 500 — S&P Global, 2026-06-05 ↩

-

Flex Ltd. Q4 Fiscal 2026 Earnings Call Transcript — Flex Investor Relations, 2026 ↩↩↩↩

-

Flex to Acquire Anord Mardix for $540 Million — Flex Press Room, 2021-10-18 ↩↩

-

Flex Completes Acquisition of Crown Technical Systems for $325M — Flex Press Room, 2024-11-19 ↩↩

-

BYD Electronic Annual Financial Results 2024 — HKEX News, 2025-03-27 ↩

-

Celestica Announces Fourth Quarter and FY 2025 Financial Results — Celestica Inc. ↩

-

Sachem Head Takes Flex Stake, Plans to Push for Solar Spinoff — Bloomberg, 2021-03-15 ↩

-

Elliott Management Builds $1.5 Billion Stake in Flex — Reuters, 2026-05-12 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube