Armstrong World Industries: From Cork Stoppers to Ceiling Dominance

I. Introduction & Episode Roadmap

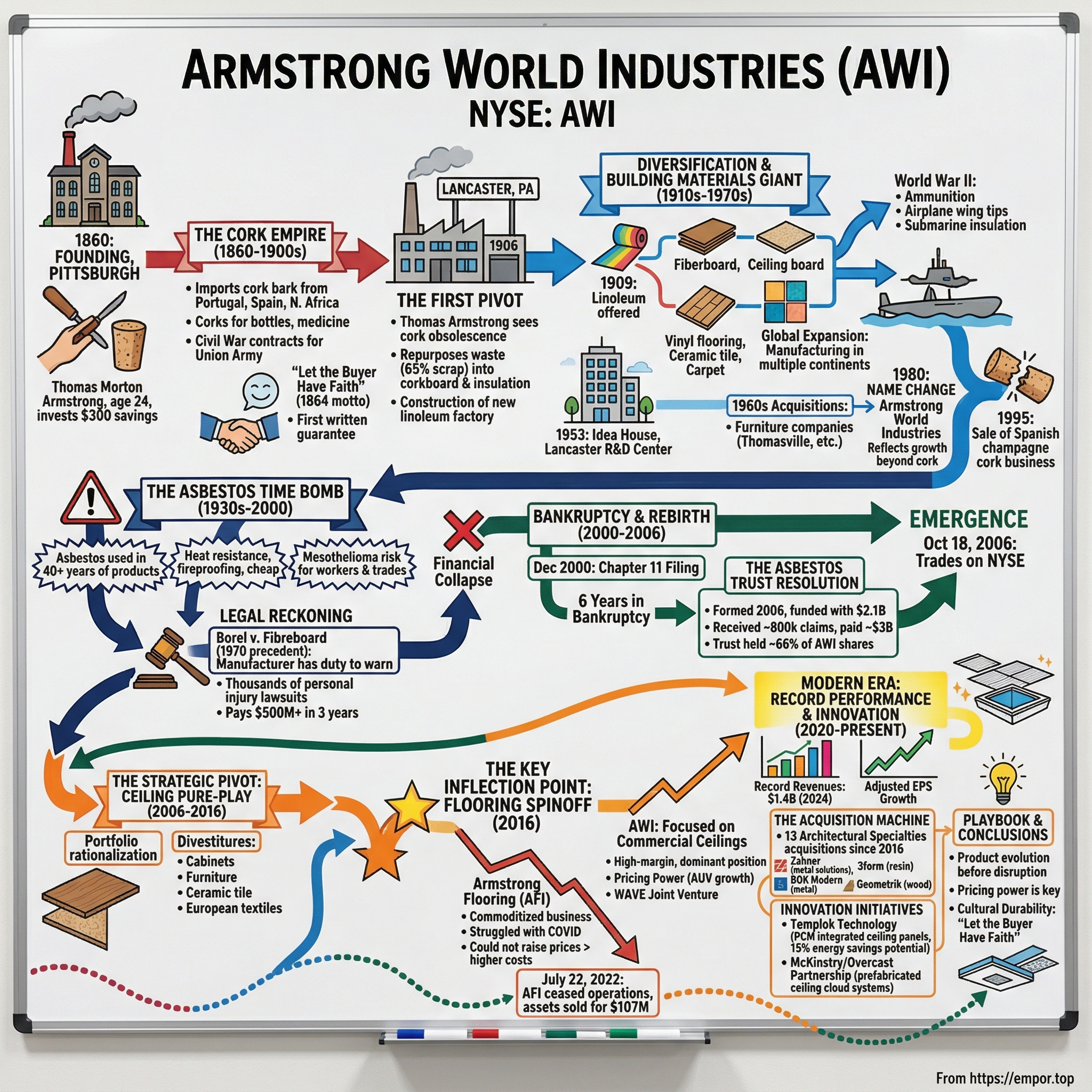

Picture this: A 24-year-old son of Irish immigrants stands in a cramped Pittsburgh workshop in 1860, hand-carving cork stoppers for wine bottles. His savings of $300—scraped together from years as a shipping clerk—represents his entire bet on the future. What Thomas Morton Armstrong couldn't possibly know was that he was planting the seed of a company that would survive the Civil War, dominate global cork production, pivot through multiple industries, weather an asbestos catastrophe that nearly destroyed it, and emerge 165 years later as the dominant force in American commercial ceilings with record profits of $1.4 billion in revenue.

Armstrong World Industries, Inc. (NYSE: AWI) today stands as an Americas leader in the design and manufacture of innovative interior and exterior architectural applications including ceilings, specialty walls and exterior metal solutions. Fourth-quarter 2024 saw net sales of $368 million, an increase of 18%, with operating income up 24% and diluted net earnings per share increasing 34%.

The question that haunts every business school case study is simply this: How does a cork company become a ceiling monopoly? The answer reveals a masterclass in corporate reinvention spanning five distinct eras—and a cautionary tale about how existential crises can forge either destruction or transformation.

The company completed 12 acquisitions since 2016, expanding its portfolio and creating a competitive advantage in the market. This isn't the same company that emerged from six years in bankruptcy court in 2006. It's not even the same company that spun off its flooring business in 2016. AWI has methodically transformed itself into a focused, high-margin, acquisition-driven growth machine with pricing power that its former flooring sibling could only dream of.

The themes that emerge from AWI's 165-year journey read like a playbook for long-term value creation:

Product evolution before disruption forces your hand. Cork → building materials → ceilings focus. Each pivot happened from a position of relative strength, not desperation.

Existential crisis management. The asbestos liability that pushed AWI into bankruptcy ultimately allowed it to shed debt, restructure operations, and emerge with a clean balance sheet.

Strategic divestitures that create value. The 2016 flooring spinoff looked controversial at the time. By 2022, when Armstrong Flooring declared bankruptcy and ceased operations, the decision was vindicated spectacularly.

Acquisition integration as a core competency. With the addition of Geometrik, Armstrong has now completed 13 Architectural Specialties acquisitions since 2016. The company has systematically built capabilities across metal, wood, felt, resin, and architectural applications.

This is the story of a company that refused to die—and the strategic choices that made survival possible.

II. Founding & The Cork Empire (1860–1900s)

The Origin Story

The streets of mid-nineteenth century Pittsburgh were black with coal smoke and alive with industrial ambition. In 1860 Thomas Morton Armstrong, a 24-year-old son of Scottish-Irish immigrants from Londonderry, Ireland, used $300 of savings from his job as a shipping clerk to buy a small cork-cutting shop in Pittsburgh. His partner in the venture, John O. Glass, would eventually sell his interest to Armstrong's brother, but Thomas was the driving force from day one.

Thomas M. Armstrong joined with John D. Glass to open a one-room shop in Pittsburgh, Pennsylvania, carving bottle stoppers from cork by hand. Their first deliveries were made in a wheelbarrow.

The business model was brutally simple: import cork bark from Portugal, Spain, and northern Africa, then cut it into stoppers that sealed bottles of wine, medicine, and every other liquid that needed containing. Armstrong's original business was cutting cork stoppers, first by hand then after 1862 by machine, from the bark of cork trees which grow in Portugal, Spain, and northern Africa. During the Civil War, 1861 to 1865, the company made bottle stoppers for the Union Army and was singled out for official praise for fulfilling its contracts at the agreed prices with top-grade corks.

That government contract marked Armstrong's first brush with institutional credibility. But it was a street festival in Pittsburgh that forged the company's enduring philosophy.

"Let the Buyer Have Faith"

In the very early days of our company, founder Thomas Armstrong had supplied corks to a customer who provided a special soft drink for a street festival in Pittsburgh. The soft drinks went bad, and Tom's customer blamed Armstrong's corks. Tom replaced all of the soft drink – even though the drinks going sour likely had little to do with the corks. That decision cost a pretty penny for a new business in the late 1800s, but he did it to preserve his reputation, stand behind his product and make his name synonymous with trust. The news spread all over Pittsburgh and people learned if the supplier was Armstrong, the buyer could have faith.

This wasn't just customer service—it was calculated brand-building a century before the concept had a name. In 1864 Thomas Armstrong pioneered the concept of brand-name recognition in his industry by stamping "Armstrong" on each cork and offering a written guarantee of quality with each sale. In an era when most products were anonymous commodities, Armstrong was putting his name—literally—on every piece he sold.

Building Market Dominance

This good publicity enabled Armstrong to land a large contract with a New York drug firm after the war, beginning the move toward national distribution of its products. From there, growth accelerated steadily.

Originally cork was purchased from American importers, but in 1878 Armstrong made arrangements to purchase, process, and ship corkwood and corks direct from Spain, thus beginning the foreign operations that eventually would make the company the largest cork processor in the world.

By the 1890s Armstrong was the world's largest cork company, employing more than 750 people, most of whom Thomas Armstrong knew by name. In 1891 the company incorporated as Armstrong, Brother & Company, Inc.

Consider the audacity of that trajectory: from wheelbarrow deliveries to global cork dominance in three decades. The company had built exactly the kind of vertical integration and scale advantages that would define industrial success for the next century.

But Thomas Armstrong understood something that many founders miss: the product that built you may not sustain you.

The Pivot Begins

Cork began being displaced by other closures, but the company introduced insulating corkboard and brick. In 1906, two years before he died, Thomas Armstrong concluded that the solid foundation of the future was covered with linoleum, and construction began on a new factory in a cornfield at the edge of Lancaster, Pennsylvania.

Lancaster, Pennsylvania—where AWI remains headquartered today, 119 years later. That decision to relocate from Pittsburgh to rural Pennsylvania wasn't just about real estate costs. It was about positioning for a manufacturing-intensive future.

In 1909, Armstrong linoleum was first offered to the trade. The cork company had become a flooring company—and that pivot would define its next century.

A core innovation stemmed from addressing high scrap rates—approximately 65% of raw cork discarded during stopper production—by repurposing waste into sound-absorbing corkboard and insulation materials. This resourceful process not only minimized losses but established the groundwork for Armstrong's entry into acoustic and building products, transforming byproducts into commercially viable commodities.

The lesson for investors: AWI's DNA has always included the capacity to see obsolescence coming and pivot before it becomes existential. That instinct would be tested again and again.

III. Diversification & the Building Materials Giant (1910s–1970s)

Product Evolution

The logic of Armstrong's expansion followed the material science of cork itself. After corkboard, the logical move was to fiberboard, and then to ceiling board. Cork tile and linoleum led to vinyl flooring, then ceramic tile, laminate flooring, and carpeting.

Each product extension built on manufacturing competencies, distribution relationships, and the Armstrong brand. The company wasn't randomly diversifying—it was following the thread of related capabilities outward from its core.

During the 1950s cork was largely replaced by chemicals and synthetics as the basis of the company's products. By 1960 building materials accounted for 60 percent of sales, and industrial specialties and packaging were each 20 percent of sales.

The numbers tell a remarkable story of transformation. By mid-century, the cork company had become a building materials conglomerate, with the original business shrinking to a minority of revenue.

War & Post-War Growth

During World War II, Armstrong made 50-caliber round ammunition, wing tips for airplanes, cork sound insulation for submarines, and camouflage. Like many American manufacturers, the war channeled production toward defense needs—but also expanded capabilities and plant capacity.

By 1950 annual sales had climbed to $163 million, and earnings were at record levels. Adjusted for inflation, that's roughly $2 billion in today's dollars—evidence of just how significant Armstrong had become in post-war America.

Backstrand's goal was to use the growth to date to increase profits. He emphasized not only marketing but also research, realizing that product innovation was essential for successful competition in the postwar period. He completed the building industry's biggest research-and-development center. To help sell products in the home-remodeling market, in 1953 Armstrong built in Lancaster an "idea house" filled with Armstrong products, to be used as a showcase for dealers and customers.

The research center in Lancaster represented a bet on innovation-driven differentiation. Armstrong wasn't competing on cost—it was competing on product performance and design.

Global Expansion

By the early 1960s, Armstrong's ambitions had expanded globally. The company operated manufacturing facilities across multiple continents, processing cork in Spain while producing flooring in Canada, Britain, and West Germany. The textile-mill supplies business extended into India.

The Acquisition Spree

The 1960s saw Armstrong aggressively diversify beyond its core:

In 1964, Armstrong bought Phoenix Chair Company, following up with Founders Furniture Company in 1965, Western Carolina Furniture Company in 1966, and both Thomasville Furniture and Caldwell Furniture in 1968. In the 1970s, they expanded with a low-end bedroom-furniture line.

The Thomasville acquisition made Armstrong a major player in furniture—a business that seemed adjacent to its flooring and building materials focus but ultimately proved to be a distraction.

The Name Change

By 1980, the company that began as Armstrong Cork had transformed so completely that the name no longer fit. Armstrong Cork Company changes its name to Armstrong World Industries to reflect the growth of core business beyond cork and to reflect an international presence.

Although of only small financial consequence, the company's sale of its champagne cork business in Spain in 1995 was important symbolically as it marked Armstrong's exit from its original business. The cork company had fully evolved—or perhaps metastasized—into something much larger and more complex.

But embedded in that complexity was a ticking time bomb.

IV. The Asbestos Time Bomb (1930s–2000)

The Asbestos Era

To understand Armstrong's near-death experience, you need to understand the seduction of asbestos for mid-twentieth century manufacturers. The mineral offered extraordinary properties: heat resistance, fireproofing, durability, insulation, and—critically—it was cheap.

From the 1930s until the 1970s, Armstrong continued to use asbestos in its products, well after they were aware of the hazards.

Armstrong made adhesives, backing and floor tiles with asbestos. It also added asbestos to gaskets, corkboard and fiberboard. This put workers at risk of mesothelioma and other asbestos-related diseases. Asbestos was a cheap and effective option for the company's insulation needs. Over the course of 40 years, Armstrong's asbestos products were used in homes, businesses and factories.

Armstrong also made asbestos spray insulation, which is one of the most dangerous forms of exposure. Armaspray contained at least 85% asbestos fibers.

The product lines were extensive: floor tiles, ceiling products, lining felt, backing for sheet vinyl, acoustic cement, gaskets, pipe insulation, and spray insulation. Thousands of workers—in Armstrong plants and in construction trades installing Armstrong products—were exposed to what we now know is a potent carcinogen.

The Legal Reckoning

The first asbestos-exposure case in which Armstrong was involved was the 1970 case of Borel v. Fibreboard Paper Product Corporation. Borel initiated legal action against Armstrong as well as 10 additional companies that manufactured asbestos-containing insulation. Borel developed mesothelioma and asbestos after years of working with the company's products. This case was the first one to recognize that a manufacturer has a duty to warn others about the dangers presented by asbestos.

The jury rendered a verdict in Borel's favor, awarding his family $79,436.24. It also marked one of the first lawsuits where asbestos manufacturers were held responsible for negligently harming workers.

That $79,000 verdict set a legal precedent that would ultimately cost Armstrong billions. Courts had established that manufacturers knew asbestos was dangerous and failed to warn workers—the foundation for strict liability in thousands of subsequent cases.

The Financial Collapse

Armstrong World Industries faced thousands of mesothelioma lawsuits from the 1970s until it went bankrupt in 2000. In the 3 years before filing for bankruptcy, Armstrong paid more than $500 million in asbestos settlements. This included defense costs.

On November 16, 2000 it was reported that Armstrong Holdings Inc. was facing about 173,000 asbestos personal injury claims that would cost between $758.8 million and $1.36 billion through 2006.

The scale of liability was staggering. For perspective: 173,000 claims represent roughly one lawsuit for every six people employed by Armstrong at its peak. The legal system was processing industrial-scale human tragedy, and Armstrong was in the crosshairs.

By 2004, the company had accrued at least $413 million in asbestos liabilities. The math was simple and brutal: the company could not survive outside of bankruptcy protection.

V. Bankruptcy & Rebirth (2000–2006)

Chapter 11 Filing

A Pennsylvania corporation incorporated in 1891, Armstrong filed for reorganization December 6, 2000 and it emerged from Chapter 11 reorganization on October 2, 2006.

December 2000: Lancaster-based Armstrong World Industries enters into bankruptcy due to a surge in costly asbestos personal-injury lawsuits filed against the company. It also uses the bankruptcy to restructure its flooring business.

Six years in bankruptcy. For context: Apple nearly went bankrupt in 1997 and was rescued by Microsoft's investment within months. General Motors' 2009 bankruptcy lasted 40 days. Armstrong's Chapter 11 process extended nearly six years—a testament to the complexity of asbestos liability and the sheer volume of claimants.

The Asbestos Trust Resolution

The solution required creating a mechanism to pay current and future asbestos victims while allowing the company to operate:

The Armstrong World Industries Asbestos Trust was formed in 2006 with funding of $2.1 billion, one of the largest asbestos trust funds in the country.

The Armstrong World Industries, Inc. Asbestos Personal Injury Settlement Trust in 2006 held approximately 66% of AWI's outstanding common shares.

Think about that capital structure: the asbestos trust owned two-thirds of the company. The victims, in effect, became the majority shareholders. It was a creative—and morally appropriate—resolution that aligned ongoing company success with victim compensation.

After it reorganized 6 years later, it funded the Armstrong World Industries Asbestos Trust with more than $2 billion. Since it opened in 2007, the trust has received nearly 800,000 claims and paid more than $3 billion in damages.

Since the trust opened, more than 300,000 claims have been filed, and the company has paid out more than $2.8 billion.

Emerging Leaner

Its stock began trading on the New York Stock Exchange October 18, 2006.

Armstrong emerged from bankruptcy with a restructured balance sheet, resolved asbestos liabilities (channeled through the trust), and a strategic mandate to focus its portfolio. The company that came out wasn't the same sprawling conglomerate that went in.

By 2009, Armstrong's annual net sales totaled approximately $2.8 billion—still a substantial enterprise, but with a clearer identity and cleaner books.

VI. The Strategic Pivot: Becoming a Ceiling Pure-Play (2006–2016)

Post-Bankruptcy Strategic Review

Within months of emerging from bankruptcy, management began evaluating the portfolio:

Armstrong World Industries, Inc. and NPM Capital N.V. sold Tapijtfabriek H. Desseaux N.V. and its subsidiaries, the principal operating companies in Armstrong's European Textile and Sports Flooring business segment, to NPM Capital N.V. in April 2007.

The European textile and sports flooring business was sold first—an early signal that management intended to simplify.

Divestitures & Focus

The portfolio rationalization continued:

2012: Armstrong Cabinets was sold to American Industrial Partners.

1995: (Before bankruptcy) Thomasville Furniture had been sold to Interco for $331.2 million, and the ceramic tile operations divested.

Each divestiture sharpened focus, but the biggest question remained: What to do about flooring?

THE KEY INFLECTION POINT: The Flooring Spinoff

Armstrong Flooring was spun off from Armstrong World Industries in 2016, a move that left Armstrong Industries with the far more profitable ceilings business.

Armstrong Flooring spun off from Armstrong World Industries in 2016.

On April 1, 2016, Armstrong World Industries completed the spinoff of its flooring business into a new publicly traded company: Armstrong Flooring (NYSE: AFI). The transaction was executed as a tax-free distribution to shareholders.

This was the defining strategic moment. AWI kept: - Mineral fiber ceiling tiles: High-margin, dominant market position - The WAVE joint venture: Ceiling suspension systems - Architectural Specialties: Growing premium custom business

Armstrong Flooring received: - Vinyl sheet and tile flooring - Laminate flooring - Wood flooring - International operations in China and Australia

The logic was straightforward: ceilings had pricing power; flooring was commoditized. But making that call required management to admit that a business dating back to Thomas Armstrong's 1906 linoleum factory—over a century of history—was no longer strategically valuable.

The market was skeptical. Critics questioned whether AWI could grow as a ceiling pure-play. They questioned whether the remaining business was too narrow. They questioned whether management was abandoning diversification benefits.

They were wrong.

VII. The Armstrong Flooring Saga: Vindication of the Spinoff (2016–2022)

The Spinoff's Divergent Fates

The Armstrong brand won't face this anonymity anytime soon because the World Industries side is doing just fine.

AWI and Armstrong Flooring, born as twins from the same corporate parent, traveled dramatically different trajectories after their separation.

AWI: Focused on commercial ceilings, grew margins, pursued strategic acquisitions, and consistently delivered profit growth.

Armstrong Flooring: Struggled with margin pressure, commodity competition, and eventually COVID-19 disruption.

Armstrong Flooring's Collapse

Armstrong Flooring Inc, a publicly traded flooring manufacturer founded in 1860, has filed for Chapter 11 bankruptcy protection in the US Bankruptcy Court for the District of Delaware, noting that it could not raise prices enough to counter supply chain disruptions and higher costs for materials and transportation. The Chapter 11 filing came after the company spent months trying to find a buyer and haggling with lenders, according to court papers.

The company struggled through COVID as approximately 70% of its business was commercial, thus missing the boon in consumer spending on home improvements while simultaneously facing losses in demand from its traditional customer base.

The pandemic delivered a cruel irony: residential flooring boomed as homeowners invested in renovations, but Armstrong Flooring's commercial focus meant it missed that surge entirely while seeing its traditional customers—office buildings, hotels, institutions—shut down.

"Simply stated, the company's increasing costs significantly outpaced its pricing power," Mr Vermette said in a court filing.

That single sentence captures everything. Armstrong Flooring couldn't pass through cost increases to customers. It had no moat. It was a commodity business masquerading as a brand.

Effective July 22, 2022, Armstrong Flooring ceased operations. AHF Products purchased certain assets of Armstrong Flooring, Inc., including the rights to license the Armstrong Flooring® brand name.

The proposed transactions stemmed from a court-supervised auction that began on June 27, 2022. A consortium, formed among AHF Products, VION Investments, and Gordon Brothers, would acquire substantially all the assets of Armstrong North America for approximately $107 million in cash.

$107 million. For context: AWI's market capitalization is approximately $8 billion. The flooring business that seemed so valuable in 2016 liquidated for barely 1% of AWI's current value. The spinoff decision that critics questioned was vindicated beyond any reasonable argument.

The Lesson: Pricing Power is Everything

The contrast between AWI and Armstrong Flooring teaches a fundamental lesson about business quality.

AWI's ceilings business has pricing power. Commercial ceiling systems are specified by architects and purchased by contractors who care about performance, acoustics, fire safety, and installation efficiency—not just price. The contractor installing the ceiling isn't paying for it; the building owner is. And the building owner cares about the architect's specification.

Flooring is a commodity. The homeowner or purchasing manager comparing flooring options sees price per square foot. There's no acoustic specification. No fire code requirement. No architect relationship. Just price competition from imports, alternatives, and private label options.

The Mineral Fiber segment achieved 9% average unit value (AUV) growth in the fourth quarter, marking the strongest quarterly growth rate of the year.

AWI consistently grows pricing—average unit value (AUV) improvement—because it sells specified products to customers who value performance. Armstrong Flooring's costs "significantly outpaced its pricing power" because it sold fungible products in a price-driven market.

For investors, the flooring collapse provides a clean natural experiment: two businesses with shared heritage, management training, and brand equity, separated in 2016, with radically different outcomes. The difference was moat.

VIII. The Acquisition Machine: Building Architectural Specialties (2016–Present)

The Growth Strategy

With the flooring business spun off, AWI's capital allocation strategy crystallized around three pillars: organic growth in mineral fiber, acquisition-driven expansion in Architectural Specialties, and returning capital to shareholders.

With the addition of Zahner, Armstrong has completed 12 Architectural Specialties acquisitions since 2016 and vastly expanded its portfolio of products and solutions, including a range of substrate materials for interior and exterior applications, such as metal, wood, felt and architectural resin.

With the addition of Geometrik, Armstrong has now completed 13 Architectural Specialties acquisitions since 2016.

Thirteen acquisitions in eight years. AWI has built a repeatable acquisition process focused on expanding capabilities in premium, custom ceiling and wall solutions.

The WAVE Joint Venture

WAVE is the North America leader in the design and production of suspended ceiling system solutions sold under the Armstrong brand name. A joint venture between Armstrong World Industries and Worthington Enterprises, WAVE combines the culture and strengths of both parent companies. WAVE employs over 400 employees and operates 7 manufacturing facilities.

Founded in 1992, WAVE operates under a long-standing corporate philosophy rooted in the Golden Rule, combining the world-class culture of both parents.

The WAVE partnership illustrates AWI's capital efficiency. Rather than owning ceiling grid manufacturing outright, AWI shares the capital burden while receiving equity earnings that flow through as high-margin income. WAVE provides an elegant solution: Armstrong owns the brand and distribution while Worthington contributes manufacturing expertise.

Key Acquisitions

Zahner (2024): Based in Kansas City, Mo., Zahner is a widely recognized leader in the design, engineering and fabrication of highly crafted, complex exterior architectural metal solutions. Zahner's advanced metal surfaces and engineering systems are unique in the industry and have been used in some of the most iconic commercial buildings, cultural centers and other structures in North America and beyond.

The work of Zahner has shaped some of the most recognized places and spaces in the United States, including SoFi Stadium in Inglewood, Calif., the Petersen Automotive Museum in Los Angeles, Calif., IBM's corporate headquarters in Armonk, N.Y., and the Bloomberg Center in New York City.

The Zahner acquisition directly builds on and complements the exterior architectural metal capabilities of BOK Modern, LLC acquired by Armstrong in 2023.

3form (2024): Architectural resin and specialty materials provider.

BOK Modern (2023): Exterior architectural metal capabilities.

Geometrik (2025): Based in Kelowna, British Columbia, Geometrik is a leading Canadian designer and manufacturer of wood acoustical ceiling and wall systems made from multiple wood species, including Western Hemlock.

Founded in 2007 by Vladimir and Nataliya Bolshakov, Geometrik has built a broad portfolio of wood ceiling and specialty wall solutions using a variety of wood species along with various stains, perforations, shapes, and sizes. The company currently offers nine different wood products across several types of acoustical ceiling and wall systems and a curated palette of 12 standard and custom wood finishes.

Each acquisition extends AWI's capability to participate in more spaces within commercial buildings. Metal exteriors. Wood interiors. Resin specialties. The strategy is systematic: own more of the architect's specification options.

The Two-Segment Model

Today's AWI operates two reporting segments:

Mineral Fiber: Core ceiling tiles—high margin, dominant market position, consistent pricing power, relatively mature growth profile.

Architectural Specialties: Higher growth, premium custom solutions, acquisitions-driven expansion, lower margins but improving as scale builds.

Architectural Specialties segment net sales improved primarily due to a $25 million contribution from the recent acquisitions of Zahner, 3form, LLC ("3form") and BOK Modern, LLC ("BOK"), in addition to increased custom project net sales.

The segment mix is shifting. Architectural Specialties represents a growing share of revenue as acquisitions compound, while Mineral Fiber provides the stable, high-margin cash flow that funds the acquisition machine.

IX. Modern Era: Record Performance & Innovation (2020–Present)

Record Financial Performance

"These strong fourth-quarter results capped off another year of significant growth for Armstrong with record-setting sales and earnings, strong free cash flow generation, and two meaningful acquisitions to grow our Architectural Specialties capabilities," said Vic Grizzle, President and CEO of Armstrong World Industries.

Armstrong World Industries annual revenue for 2024 was $1.446B, a 11.62% increase from 2023.

The growth trajectory has been consistent: Armstrong World Industries annual revenue for 2023 was $1.295B, a 5.04% increase from 2022. Armstrong World Industries annual revenue for 2022 was $1.233B, a 11.43% increase from 2021.

With $1.4 billion in revenue in 2024, AWI has approximately 3,700 employees and a manufacturing network of 21 facilities, plus seven facilities dedicated to its WAVE joint venture.

Pricing Power & AUV Growth

The signature of a quality business is the ability to raise prices faster than costs. AWI demonstrates this consistently through Average Unit Value (AUV) growth in its Mineral Fiber segment.

The Mineral Fiber segment achieved 9% average unit value (AUV) growth in the fourth quarter, marking the strongest quarterly growth rate of the year.

For context: 9% AUV growth means AWI sold essentially the same volume of ceiling tiles for 9% more revenue per unit. That's pure price increase falling to the bottom line with minimal incremental cost—the definition of pricing power.

Mineral Fiber net sales increased 8.1% in the fourth quarter of 2024 due to $20 million of favorable AUV, partially offset by $2 million of lower sales volumes. The improvement in AUV was driven by both favorable mix and like-for-like pricing.

Even with slight volume declines, AWI grows revenue through price. That's not something Armstrong Flooring could ever say.

Innovation Initiatives

Templok Technology:

The new Ultima® Templok® solution features AWI mineral fiber ceiling panels with integrated phase change material (PCM) that can reduce building energy costs and consumption. When integrated with AWI ceiling panels, PCM absorbs and releases heat as temperatures inside a building rise and fall, thereby regulating room temperature with lower energy usage. The company's research estimates that installing these tiles can reduce energy cost and consumption by up to 15%* as measured in lab tests.

Q: What is the potential market size for Templok, and how does it compare to other growth initiatives like Healthy Spaces or Canopy? A: Templok represents a significant opportunity, potentially transforming the entire installed base of 39 billion square feet of Mineral Fiber to energy-saving ceiling tiles. While we haven't publicly sized it, the opportunity is substantial and long-term, driven by the need for energy efficiency in buildings.

This includes our innovative TEMPLOK Energy Saving Ceilings which help save on energy costs and usage. Plus, these ceilings may qualify for up to 50% in Investment Tax Credits.

McKinstry/Overcast Partnership:

Armstrong World Industries, Inc. (NYSE: AWI) announced that it has entered into a strategic partnership with McKinstry, a leading construction and energy services company, by making an equity investment in its Overcast Innovations venture. Overcast Innovations offers integrated building solutions, including prefabricated ceiling cloud systems, modular grid platforms and engineering design services, to reduce waste and inefficiencies in the built environment.

In connection with the transaction, Armstrong has entered into a purchase agreement reflecting an initial equity investment in Overcast of approximately 20%, with future rights to increase its ownership interest.

2025 Performance and Outlook

Armstrong World Industries (NYSE:AWI) reported strong third-quarter 2025 results on October 28, with double-digit sales growth and raised full-year guidance despite some margin pressure. Armstrong delivered solid financial results across key metrics in the third quarter. Net sales increased 10% year-over-year to $425.2 million, while adjusted EBITDA rose 6% to $148 million. Adjusted diluted earnings per share grew 13% to $2.05, and adjusted free cash flow improved 15% to $123 million.

Based on strong year-to-date performance, Armstrong raised its full-year 2025 guidance across all key metrics. The company now expects: Net sales of $1,623-$1,638 million (12-13% year-over-year growth). Adjusted EBITDA of $553-$563 million (14-16% growth). Adjusted diluted EPS of $7.45-$7.55 (18-20% growth). Adjusted free cash flow of $342-$352 million. For the Mineral Fiber segment, Armstrong expects volume to be flat to down 1% on stabilizing market conditions, with AUV growth of approximately 6%.

Leadership

Vic Grizzle has served as president and chief executive officer of Armstrong World Industries since 2016. He joined the company in January 2011 as executive vice president. Vic brings to his role more than 30 years of experience in driving efficient manufacturing and process improvements, managing

Prior to joining AWI, he served from 2005 to 2010 as president of Global Structures, Coatings and Tubing for Valmont Industries, a $3 billion global leader in engineered products and services for infrastructure development, irrigation equipment and services for agriculture. In addition, Vic was president of the commercial power division of EaglePicher Corporation.

Grizzle's tenure has defined the post-bankruptcy, post-spinoff AWI. Under Vic's leadership, AWI shareholder returns have increased over 50%. Vic is proud to work with the talented team of AWI employees in growing the company by making a positive difference in the spaces where we live, work, learn, heal and play.

X. Playbook: Business & Investing Lessons

Lesson 1: The Power of Pivoting Before You Must

Thomas Armstrong saw cork's decline and pivoted to linoleum in 1906—from a position of global dominance, not desperation. Post-bankruptcy management saw flooring's commoditization and spun it off in 2016—from a position of improving profitability, not crisis.

The pattern is consistent: AWI's successful pivots happen when the company still has optionality. Waiting until the business is in crisis leaves fewer options and worse terms.

Lesson 2: Pricing Power Beats Volume

AWI's Mineral Fiber segment demonstrates the value of specification economics. When architects specify AWI ceiling tiles by name, price sensitivity decreases. When contractors know the product, installation efficiency improves. When building codes require acoustic performance, alternatives shrink.

Contrast with flooring: Armstrong Flooring raised prices 10-15% and still couldn't cover costs. AWI grows AUV 6-9% annually and drops most of it to profit.

The impact of tariffs on Armstrong is limited due to our North American supply chain. We have mitigation plans to minimize any impact, and our pricing discipline will cover any cost increases.

Lesson 3: Strategic Divestitures Can Create Value

The 2016 flooring spinoff generated skepticism. By 2022, Armstrong Flooring was bankrupt and sold for $107 million. Meanwhile, AWI reached record profits.

The lesson: holding a mediocre business because of history or emotional attachment destroys value. Strategic divestitures focus resources on high-return opportunities.

Lesson 4: Acquisition Integration as a Core Competency

Thirteen acquisitions since 2016 suggests AWI has built repeatable processes for identifying targets, executing transactions, and integrating businesses. This is a capability that compounds over time.

Lesson 5: Values That Endure

Since our founder first adopted his philosophy, "Let the Buyer Have Faith," in 1864, our values have grown and evolved to meet the needs of our customers employees and communities.

"Let the Buyer Have Faith"—the motto born from a street festival gone wrong in the 1860s—still appears in AWI's corporate communications today. That continuity across 160 years, through bankruptcies and spinoffs and transformations, suggests genuine cultural durability.

XI. Porter's Five Forces & Competitive Positioning

1. Threat of New Entrants: LOW

The commercial ceiling market has high barriers to entry:

- Capital requirements: Mineral fiber manufacturing requires significant plant investment

- Specification relationships: Decades of architect and contractor relationships aren't easily replicated

- Scale economies: AWI's manufacturing network of 21 facilities enables cost advantages

- Brand equity: 160+ years of "Let the Buyer Have Faith"

The study also evaluates company market share and competitive analysis on industry competitors including Armstrong World Industries, Knauf (USG), Saint-Gobain (CertainTeed), and ROCKWOOL (Rockfon).

The market is concentrated among established players. New entrants would need to match scale, build relationships, and survive years of losses against entrenched competitors.

2. Bargaining Power of Suppliers: LOW-MODERATE

Raw materials for mineral fiber production (perlite, clay, recycled content) are relatively commoditized with multiple sourcing options. AWI's scale provides negotiating leverage.

The impact of tariffs on Armstrong is limited due to our North American supply chain. We have mitigation plans to minimize any impact, and our pricing discipline will cover any cost increases. For WAVE, less than 2% of their cost of goods sold is affected by steel and aluminum tariffs, and we have local sourcing options to mitigate this.

3. Bargaining Power of Buyers: MODERATE

The buyer landscape is fragmented: architects specify products, general contractors purchase them, and building owners pay for them. This separation of specifier and purchaser reduces direct price pressure.

Large distributors like Foundation Building Materials have negotiating leverage, but AWI's dominant position in commercial ceilings limits alternatives.

4. Threat of Substitutes: LOW

Suspended ceiling systems are deeply embedded in commercial construction: - Code requirements: Fire safety and acoustic codes often mandate ceiling systems - Functionality: Suspended ceilings hide HVAC, electrical, and plumbing runs while providing access - Cost-effectiveness: Alternatives (exposed structure, drywall ceilings) serve different aesthetic needs

The installed base of 39 billion square feet represents decades of standardization that won't shift quickly.

5. Competitive Rivalry: MODERATE

Competition exists—USG (Knauf), CertainTeed (Saint-Gobain), Rockfon (ROCKWOOL)—but the market isn't characterized by destructive price wars. Players compete on product performance, service, and specification rather than commoditized price.

Hamilton Helmer's 7 Powers Framework

AWI possesses several durable competitive advantages:

Scale Economies: 21 manufacturing facilities provide cost advantages smaller competitors can't match.

Switching Costs: Architects who know AWI products, contractors trained on installation, and building owners with existing AWI ceilings face real costs in switching to alternatives.

Brand: 160 years of "Let the Buyer Have Faith" creates recognition and trust that competitors must spend decades building.

Counter-Positioning: AWI's focus on ceilings after spinning off flooring represents a strategic choice that diversified competitors may be unwilling to match by divesting their own flooring businesses.

XII. Key Performance Indicators for Investors

For long-term investors tracking AWI, three KPIs matter most:

1. Mineral Fiber Average Unit Value (AUV) Growth

This metric captures AWI's pricing power in its core business. Consistent AUV growth (historical range: 4-9% annually) indicates the company can raise prices without volume loss—the hallmark of competitive advantage. Any sustained deterioration in AUV growth would signal competitive pressure.

2. Architectural Specialties Revenue Mix

Track Architectural Specialties as a percentage of total revenue. This segment represents AWI's growth engine—driven by acquisitions and organic custom project wins. Rising AS contribution (currently trending toward 30%+ of revenue) indicates successful portfolio evolution. Stagnation would suggest the acquisition strategy is losing momentum.

3. WAVE Equity Earnings

The WAVE joint venture generates high-margin equity earnings that flow through with minimal capital investment. Growth in WAVE contributions reflects the health of the broader commercial construction market and AWI's position in ceiling suspension systems.

XIII. Bull Case & Bear Case

Bull Case

Dominant position with pricing power. AWI is the market leader in North American commercial ceilings with demonstrated ability to grow prices 5-9% annually regardless of economic conditions. This pricing power flows directly to profit.

Acquisition runway. The Architectural Specialties segment has room to continue consolidating fragmented specialty manufacturers. Each acquisition expands the company's addressable market within commercial buildings.

Templok opportunity. Energy-saving ceiling technology with potential investment tax credits could drive replacement demand across the 39 billion square foot installed base. Even modest adoption rates represent significant revenue opportunity.

Tariff insulation. North American manufacturing protects AWI from tariff exposure that affects import-dependent competitors.

Return of office. Renewed office renovation activity—driven by hybrid work requirements and aging building stock—represents secular tailwind for commercial ceiling demand.

Bear Case

Commercial real estate headwinds. Office vacancy rates remain elevated post-pandemic. Reduced commercial construction activity would pressure volumes.

Acquisition integration risk. Thirteen acquisitions since 2016 creates execution risk. Failed integrations could erode margins and distract management.

Premium valuation. At approximately 27x earnings, AWI trades at a premium to building products peers. Any disappointment could trigger multiple compression.

Customer concentration. Significant revenue flows through large building products distributors. Loss of a major relationship could impact results.

Cyclicality exposure. Despite relative resilience, commercial construction follows economic cycles. Recession would pressure both volumes and pricing.

XIV. Conclusion: The Long Arc of Corporate Reinvention

Armstrong World Industries tells a story that spans three centuries—from the Civil War-era cork shop to today's ceiling dominance. The arc bends through triumph and tragedy: global cork leadership, diversification into building materials, the asbestos catastrophe, bankruptcy and restructuring, the flooring spinoff, and methodical acquisition-driven growth.

What endures across 165 years? The values Thomas Armstrong established when he replaced spoiled soft drinks at his own expense: "Let the Buyer Have Faith." That commitment to standing behind the product, even when easier options exist, created the brand equity and customer relationships that survive corporate transformations.

The modern AWI is a focused, disciplined company with pricing power in its core business and a systematic approach to expanding its addressable market. The flooring spinoff vindication demonstrated management's strategic clarity. The acquisition machine continues adding capabilities.

For investors, AWI offers a rare combination: competitive moat, pricing power, capital discipline, and growth optionality. The valuation premium reflects these qualities—but also leaves less room for error.

The question, as always, is whether the next 165 years can match the first. Thomas Armstrong couldn't have imagined ceiling tiles when he hand-carved cork stoppers. Today's management can't predict what building interiors will look like in 2050. But the capacity to evolve—to see change coming and pivot before it becomes existential—has been the defining characteristic of Armstrong's survival.

That's the bet any long-term investor is making: not on ceiling tiles specifically, but on an organization that has proven, again and again, it knows how to reinvent itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube