Rambus: From Patent Wars to AI's Memory Backbone

II. Founding & Stanford Origins (1990-1996)

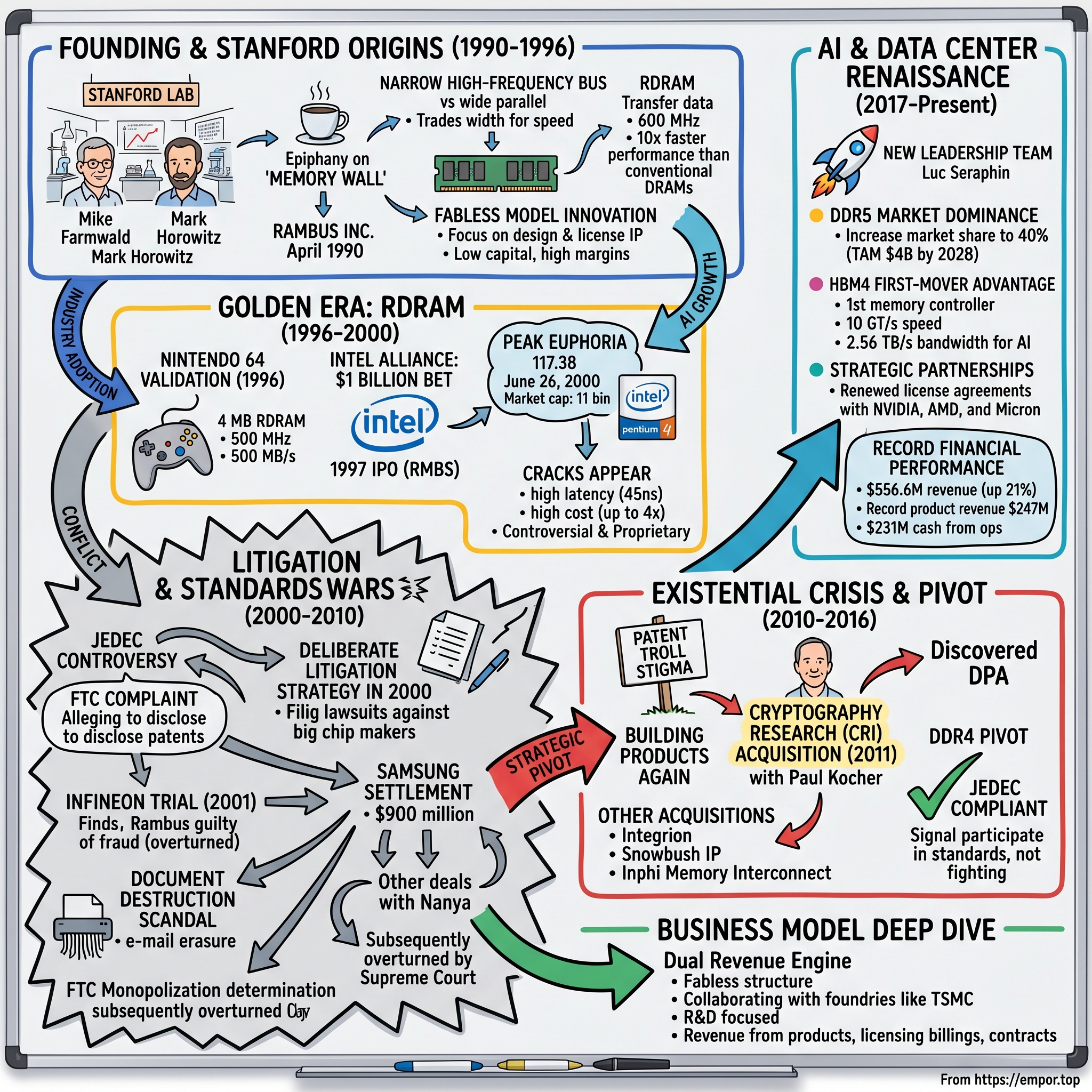

A Coffee-Fueled Epiphany on the Memory Wall

Rambus Inc. was founded in 1990 by Mike Farmwald, an entrepreneur, and Mark Horowitz, an electrical engineering professor at Stanford University, following discussions on addressing memory bandwidth limitations in computing systems. The conversations that led to Rambus reportedly began over coffee, as Farmwald and Horowitz grappled with what computer architects call the "memory wall"—the growing gap between processor speeds and memory access times that was threatening to choke computing progress.

In 1990, Horowitz took a leave of absence from Stanford to work with Mike Farmwald on a new high-bandwidth DRAM design which, in April of that year, led to the formation of Rambus Inc., a company specializing in high-bandwidth memory technology. Horowitz brought impeccable academic credentials to the venture. He had received bachelor's and master's degrees in electrical engineering from the Massachusetts Institute of Technology in 1978. At Stanford his research focused on VLSI circuits and he led a number of early RISC processor designs, including MIPS-X.

Horowitz is a co-founder, the former chairman, and the former chief scientist of Rambus Inc. He has authored over 700 published conference and research papers and is among the most highly-cited computer architects of all time. He is a prolific inventor and holds 374 patents as of 2023. His co-founder Farmwald brought entrepreneurial energy and a complementary engineering background. Dr. Farmwald served as Vice President and Chief Scientist from March 1990 to November 1993. After leaving day-to-day operations, he founded Skymoon Ventures, a venture capital firm, in 2000.

The Technical Insight That Changed Everything

The founders' core innovation was deceptively simple in concept but revolutionary in execution. In the 1990s, Rambus was a high-speed interface technology development and marketing company that invented 600 MHz interface technology, which solved memory bottleneck issues faced by system designers. Rambus's technology was based on a very high speed, chip-to-chip interface that was incorporated on dynamic random-access-memory (DRAM) components, processors and controllers, which achieved performance rates over ten times faster than conventional DRAMs.

The key architectural choice was counterintuitive: instead of the wide parallel buses used by conventional memory, Rambus employed a narrow, high-frequency serial bus. Rambus's RDRAM transferred data at 600 MHz over a narrow byte-wide Rambus Channel to Rambus-compatible Integrated Circuits (ICs). By trading bus width for speed and using both edges of the clock signal for data transfer, Rambus achieved bandwidth that dwarfed existing solutions.

The founders' vision centered on integrating advanced signaling techniques to drive industry standards in semiconductor interconnects. This wasn't just about building a better mousetrap—it was about becoming the technological standard that every computer would require.

Valley Pedigree and the Licensing Model Innovation

Rambus was founded in March 1990 by electrical and computer engineers, Mike Farmwald and Mark Horowitz. The company's early investors included premier venture capital and investment banking firms such as Kleiner Perkins Caufield and Byers, Merrill Lynch, Mohr Davidow Ventures, and Goldman Sachs. The investor roster read like a who's who of Silicon Valley kingmakers.

The company secured initial funding of $2 million from venture capitalists in exchange for 50% equity and appointed Geoff Tate, formerly senior vice president at AMD, as president. The hiring of Tate from AMD signaled that Rambus was serious about commercial execution, not just technical innovation.

The company began its operations in Mountain View, California, right in the heart of Silicon Valley. It was established by Dr. Mike Farmwald and Dr. Mark Horowitz, both with backgrounds linked to Stanford University.

From the beginning, Rambus made a crucial strategic choice that would define its entire trajectory: it would be a fabless intellectual property company. From inception, Rambus adopted a fabless model, focusing on designing and licensing intellectual property for high-performance chip interfaces rather than manufacturing semiconductors. Rambus provided companies who licensed its technology a full range of reference designs and engineering services. Rambus's interface technology was broadly licensed to leading DRAM, ASIC and PC peripheral chipset suppliers in the 1990s.

This wasn't just a business model—it was a philosophy. Rambus would invent, patent, and license. Others would manufacture. The model promised tremendous leverage: low capital requirements, high margins, and royalties on every chip built using Rambus technology. It also created the adversarial dynamics that would nearly destroy the company.

III. The Golden Era: RDRAM & Industry Adoption (1996-2000)

Nintendo's Validation and the Road to Intel

Rambus's technology first found commercial validation in an unexpected venue: video games. Rambus's RDRAM saw use in two video game consoles, beginning in 1996 with the Nintendo 64. The Nintendo console used 4 MB RDRAM running with a 500 MHz clock on a 9-bit bus, providing 500 MB/s bandwidth.

RDRAM allowed N64 to be equipped with a large amount of memory bandwidth while maintaining a lower cost due to design simplicity. RDRAM's narrow bus allowed circuit board designers to use simpler design techniques to minimize cost. The Nintendo 64 wasn't just a technical validation—it was proof that Rambus's approach could work at consumer-scale volumes and price points.

Licensees of Rambus's RDRAM technology included companies such as Creative Labs, Intel, Microsoft, Nintendo, Silicon Graphics, Hitachi, Hyundai, IBM, Molex, Macronix and NEC. The roster of blue-chip licensees seemed to confirm that RDRAM was destined to become the industry standard.

The Intel Alliance: A $1 Billion Bet

The partnership that would define Rambus's golden era—and set the stage for its near-destruction—came in 1996. In November 1996, Rambus entered into a development and license contract with Intel. Intel announced that it would only support the Rambus memory interface for its microprocessors and had been granted rights to purchase one million shares of Rambus' stock at $10 per share.

Intel wasn't just licensing Rambus technology—it was betting its entire platform strategy on RDRAM. DRDRAM was initially expected to become the standard in PC memory, especially after Intel agreed to license the Rambus technology for use with its future chipsets.

The implications were staggering. Intel controlled the PC platform. If Intel mandated RDRAM for its processors, every PC manufacturer would have to use it, and every memory chip would carry Rambus royalties. For Rambus, this was the ultimate validation of its IP licensing model.

Rambus was incorporated and founded as a California company in 1990 and then re-incorporated in the state of Delaware before the company went public in 1997 on the NASDAQ stock exchange under the symbol RMBS. The company had its IPO on May 14, 1997.

Peak Euphoria and the Dot-Com Tailwind

The timing couldn't have been better—or worse, depending on perspective. Rambus went public into the teeth of the dot-com bubble, when investors would pay astronomical multiples for anything connected to technology's future.

The all-time high Rambus stock closing price was 117.38 on June 26, 2000. At its peak, Rambus commanded a market capitalization in the billions for a company with modest revenues but seemingly unlimited upside—after all, every PC in the world would soon pay tribute to Mountain View.

Intel's Pentium 4 arrived in November 2000, and with it a new platform: the 850. This chipset had a quad-pumped 100 MHz FSB similar to the 820's, yielding an effective 400 MHz. Similarly, it mandated the use of RDRAM.

The Cracks Appear: Technical and Economic Headwinds

But the coronation never came. Instead, problems emerged on multiple fronts simultaneously.

Disadvantages of RDRAM technology include significantly increased latency, power dissipation as heat, manufacturing complexity, and cost. PC800 RDRAM operated with a minimum latency of 45 ns, compared to 15 ns for PC133 SDRAM.

The latency issue was devastating. While RDRAM delivered superior bandwidth for sustained transfers, real-world applications often needed quick bursts of data. The 45 ns latency—three times that of conventional SDRAM—meant RDRAM could actually feel slower in common use cases despite its raw bandwidth advantage.

RDRAM was controversial during its widespread use by Intel for having high licensing fees, high cost, being a proprietary standard, and low performance advantages for the increased cost.

The cost differential was even more problematic. RDRAM was also up to four times more expensive than PC-133 SDRAM due to a combination of higher manufacturing costs and high license fees. Memory makers, already operating on razor-thin margins, resented both the price premium customers faced and the royalties flowing to Rambus.

RDRAM got embroiled in a standards war with an alternative technology—DDR SDRAM—and quickly lost out on grounds of price and, later, performance.

IV. JEDEC, Standards Wars & The Litigation Machine (2000-2010)

The JEDEC Controversy: Seeds of Destruction

If RDRAM's technical and cost issues had been Rambus's only problems, the company might have simply faded as a failed technology bet. Instead, what emerged was one of the most contentious intellectual property battles in semiconductor history, centering on Rambus's participation in JEDEC, the industry standards body for semiconductor technology.

The Commission filed an administrative complaint charging that between 1991 and 1996 Rambus, Inc. joined and participated in the JEDEC Solid State Technology Association (JEDEC), the leading standard-setting industry for computer memory. According to the complaint, while a member of JEDEC, Rambus observed standard-setting work involving technologies which Rambus believed were or could be covered by its patent applications, but failed to disclose this to JEDEC.

The allegation was explosive: Rambus had sat in meetings where the industry discussed next-generation memory standards, watched those discussions, and then amended its patent applications to cover the technologies being developed—without telling anyone.

In 1999 and 2000, after JEDEC had adopted industry-wide standards incorporating the technologies at issue and the industry had become locked in to the use of those technologies, Rambus sought to enforce its patents against companies producing JEDEC-compliant memory, and collected substantial royalties from several producers of DRAM.

As Rambus continued its participation in JEDEC, it became apparent that they were not prepared to agree to JEDEC's patent policy requiring owners of patents included in a standard to agree to license that technology under terms that are "reasonable and non-discriminatory", and Rambus withdrew from the organization in 1995.

The Deliberate Litigation Strategy

Internal documents that emerged during litigation painted a picture of a company that had deliberately shifted from technology development to patent enforcement as its primary business model.

Memos from Rambus at that time showed they were tailoring new patent applications to cover features of SDRAM being discussed, which were public knowledge (JEDEC meetings are not secret) and perfectly legal for patent owners who have patented underlying innovations, but were seen as evidence of bad faith by the jury in the first Infineon v. Rambus trial.

In 2000, Rambus began filing lawsuits against the largest memory manufacturers, claiming that they owned SDRAM and DDR technology. Seven manufacturers, including Samsung, quickly settled with Rambus and agreed to pay royalties on SDRAM and DDR memory.

The legal offensive was systematic and well-planned. Rambus officially joined JEDEC in February 1992. JEDEC is a standard-setting body associated with the Electronic Industries Association. JEDEC member companies participate on various committees to develop standards for semiconductor technologies.

The Infineon Trial: Fraud, Documents, and Chaos

The first major legal battle came against Infineon Technologies, and it produced results that devastated Rambus.

In May 2001, Rambus was found guilty of fraud for having claimed that it owned SDRAM and DDR technology, and all infringement claims against memory manufacturers were dismissed.

The fraud verdict sent shockwaves through the industry. Rambus stock cratered. But the legal saga was far from over.

The Court of Appeals for the Federal Circuit (CAFC) rejected this theory of bad faith in its decision overturning the fraud conviction Infineon achieved in the first trial.

The document destruction scandal proved even more damaging. Evidence emerged that Rambus had conducted systematic "shred days" where potentially relevant documents were destroyed.

Specifically, Rambus employees were told to destroy documents at annual "shred days," from 1998 to 2000, prior to filing the patent suits. Because litigation was "reasonably foreseeable," the court ruled, Rambus should have preserved the documents. "Rambus engaged in spoliation of evidence when it engaged in the destruction of documents on all three shred days."

The evidence clearly demonstrates, and Rambus acknowledged, that at least between July 1998 and November 1999 Rambus shredded numerous paper documents and magnetically erased all but 1 of 1,269 backup tapes storing e-mail backups.

The Samsung Settlement: A Pyrrhic Victory

The litigation strategy eventually produced substantial financial returns, even as it destroyed Rambus's industry relationships.

Rambus settled litigation with Samsung Electronics in a deal that was valued at about $900 million. In exchange, Samsung is buying $200 million in Rambus stock (9.75 million shares), will pay another $200 million in cash to Rambus, and then make quarterly payments of $25 million for the next five years.

"This is by far the largest agreement we have ever created," said Harold Hughes, chief executive at Rambus.

The Samsung settlement was followed by other major agreements. In March 2014, Rambus and Nanya signed a 5-year patent licensing agreement, settling earlier claims.

The FTC and the "Patent Troll" Label

The regulatory response was severe. By a unanimous vote, the Federal Trade Commission determined that computer technology developer Rambus, Inc. unlawfully monopolized the markets for four computer memory technologies that have been incorporated into industry standards for dynamic random access memory – DRAM chips. In an opinion by Commissioner Pamela Jones Harbour, the Commission found that, through a course of deceptive conduct, Rambus was able to distort a critical standard-setting process and engage in an anticompetitive "hold up" of the computer memory industry.

"We find that Rambus's course of conduct constituted deception under Section 5 of the FTC Act. Rambus's conduct was calculated to mislead JEDEC members by fostering the belief that Rambus neither had, nor was seeking, relevant patents that would be enforced against JEDEC-compliant products."

However, the FTC ruling was subsequently overturned. On April 22, 2008, the U.S. Court of Appeals for the D.C. Circuit overturned the FTC reversal of McGuire's 2006 ruling, saying that the FTC had not established that Rambus had harmed the competition. On February 23, 2009, the U.S. Supreme Court rejected the bids by the FTC to impose royalty sanctions on Rambus via antitrust penalties.

V. The Existential Crisis & Pivot (2010-2016)

The "Patent Troll" Stigma

By 2010, Rambus had won major settlements but lost something arguably more valuable: its reputation. The company was increasingly viewed not as an innovative technology company but as a litigation machine—a "patent troll" that didn't actually build things.

Rambus said these deals were part of a change in strategy to a less litigious, more collaborative approach, distancing themselves from accusations of patent trolling. Ronald Black, Rambus's CEO, said, "Somehow we got thrown into the patent troll bunch... This is just not the case."

The problem wasn't just perception—it was business sustainability. A company that depends entirely on litigation operates at the mercy of judges and juries. The Infineon verdict, temporarily finding Rambus guilty of fraud, had demonstrated how quickly legal fortunes could reverse.

The Strategic Pivot: Building Products Again

The transformation that saved Rambus began with a recognition that pure IP licensing, enforced through litigation, was not a sustainable business model. The company needed to actually make things.

Rambus purchased Cryptography Research on June 6, 2011, for $342.5M. This will enable Rambus Inc. to develop its semiconductor licensing portfolio to include CRI's content protection and security. According to Rambus CEO Harold Hughes, the CRI security technologies would be applied to a variety of products in the company's IP portfolio.

The Cryptography Research acquisition was transformative. CRI is led by internationally renowned cryptographer and scientist Paul Kocher, whose accomplishments include helping author the SSL 3.0 standard, discovering differential power analysis (DPA), as well as developing techniques for securing electronic systems against DPA attacks.

After Rambus acquired Cryptography Research in 2011, Paul Kocher served as SVP/Chief Scientist for the newly-created security division. The business continued to grow and expand into new areas, including the CryptoManager Solutions. When Kocher left his full time position at Rambus in 2017, the security division had over 200 people and approximately $100M annual revenue.

Building the Product Portfolio

The acquisition spree continued throughout the mid-2010s, each deal adding genuine product capability rather than just patents.

In 2015, Rambus acquired Integrion Microelectronics, a small Toronto-based IP provider of high-speed analog SerDes PHY for an undisclosed amount. Through this acquisition, Rambus opened its first Canadian office and boosted its high-speed serdes IP portfolio offering.

In 2016, Rambus acquired Semtech's Snowbush IP for US$32.5 million. Snowbush IP provides analog and mixed-signal IP technologies, and will expand Rambus' product offerings.

In 2016, Rambus acquired Inphi Memory Interconnect Business for US$90 million. The acquisition includes all assets of the Inphi Memory Interconnect Business, such as customer contracts, product inventory, supply chain agreements, and intellectual property.

The DDR4 Pivot: From Antagonist to Partner

Perhaps the most symbolically important moment came in 2015, when Rambus announced products that were compliant with JEDEC standards—the very organization whose standards process it had allegedly manipulated.

On August 17, 2015, Rambus announced the new R+ DDR4 server memory chips RB26 DDR4 RDIMM and RB26 DDR4 LRDIMM. The chipset includes a DDR4 Register Clock Driver and Data Buffer, and it's fully-compliant with the JEDEC DDR4.

This was Rambus signaling to the industry: we're done fighting standards. We're going to participate in them, build products that comply with them, and compete on merit.

VI. The AI & Data Center Renaissance (2017-Present)

The New Leadership Team

The transformation accelerated under new leadership. On October 29, 2018, Rambus Inc. announced that its Board of Directors had appointed Luc Seraphin as president and chief executive officer, effective immediately. Mr. Seraphin had been performing as interim CEO since June 2018.

Seraphin brought deep operational experience to a company that needed to become a real products business. Prior to this role, Luc was the senior vice president and general manager of the Memory and Interface Division, leading the development of the company's innovative memory architectures and high-speed serial link solutions. Luc also served as the senior vice president of Worldwide Sales and Operations where he oversaw sales, business development, customer support and operations across the various business units within Rambus. Luc started his career as a field application engineer at NEC and later joined AT&T Bell Labs, which became Lucent Technologies and Agere Systems.

Mr. Seraphin has served as Senior Vice President & General Manager of Rambus' Memory and Interfaces Division since 2015. In his current role, Mr. Seraphin has made significant contributions to the development of innovative memory architectures and high-speed serial link solutions, including increasing Rambus' market footprint for its DDR4 memory buffer chipset and positioning the Company to lead in next generation DDR5 memory buffer chips.

DDR5 Market Dominance

The transition from DDR4 to DDR5 provided Rambus with an extraordinary opportunity, and the company executed brilliantly. In the DDR4 generation of products, we were closer to 25% market share. Very nice growth when the market moved from DDR4 to DDR5.

Management believes the company holds early 40% market share in DDR5 and expects continued traction in 2025. The market share gain from 25% in DDR4 to 40% in DDR5 represents a dramatic competitive repositioning.

The TAM for the RCD chip is about $800 million today. In the DDR5 generation of products, what you have on the memory modules, in addition to this RCD chip, are companion chips. These companion chips add an additional TAM of about $600 million. $300 million of that is a power management chip, and $300 million the rest of the companion chips.

The HBM4 First-Mover Advantage

If DDR5 was important, High Bandwidth Memory represents the future—and Rambus has positioned itself at the cutting edge.

Rambus announced the industry's first HBM4 Memory Controller IP, extending its market leadership in HBM IP with broad ecosystem support. This new solution supports the advanced feature set of HBM4 devices, and will enable designers to address the demanding memory bandwidth requirements of next-generation AI accelerators and graphics processing units.

"With Large Language Models (LLMs) now exceeding a trillion parameters and continuing to grow, overcoming bottlenecks in memory bandwidth and capacity is mission critical to meeting the real-time performance requirements of AI training and inference," said Neeraj Paliwal, SVP and general manager of Silicon IP, at Rambus.

Rambus's HBM4 controller not only supports the JEDEC-specified 6.4 GT/s data transfer rate for HBM4 but also has headroom to support speeds up to 10 GT/s. This enables a memory bandwidth of 2.56 TB/s per HBM4 memory stack with a 2048-bit memory interface.

The Rambus Memory Controller engineering team has over a decade of specialized expertise in designing high performance memory interface IP, including over 150 design wins for HBM and GDDR.

Strategic Partnerships: From Adversary to Essential Partner

The transformation from litigation target to essential partner is perhaps best illustrated by Rambus's renewed relationships with the companies it once sued.

On October 5, 2018, Rambus Inc. announced it has renewed a patent license agreement with NVIDIA. The agreement allows NVIDIA's use of innovations in the Rambus patent portfolio, including those covering memory controllers and serial links. Specific terms of the agreement are confidential.

"We are very pleased that AMD has chosen to renew its patent license agreement and look forward to our continued collaboration in the future," said Kit Rodgers, senior vice president of technology partnerships and corporate development at Rambus.

The Micron relationship exemplifies the evolution from litigation to partnership. Rambus extended its patent license agreement with Micron through 2029.

Record Financial Performance

The strategy has produced remarkable results. Rambus's revenue for fiscal year 2024 was $556.6 million, up 21% from 2023.

Annual product revenue reached $247 million in 2024, a record for the company. Cash from operations hit $231 million in 2024, up from $196 million in 2023.

In Q1 2025, Rambus exceeded guidance for revenue and earnings, delivering record quarterly product revenue of $76.3 million, up 52% year over year, and generated outstanding quarterly cash from operations of $77.4 million.

In Q2 2025, GAAP revenue surged to $172.2 million, driven by $81.3 million in product revenue—a 43% year-over-year increase—and $66.4 million in licensing billings. The company's operating margin expanded to 37% from 31% in Q2 2024.

Rambus revenue for the twelve months ending June 30, 2025 was $0.645 billion, a 35.17% increase year-over-year.

VII. Business Model Deep Dive

The Dual Revenue Engine

Today's Rambus operates a hybrid business model that would have been unrecognizable to the litigation-focused company of the early 2000s.

Rambus operates a fabless semiconductor business model centered on the invention, development, and commercialization of intellectual property for high-performance memory interfaces, security solutions, and related technologies. The company licenses its IP portfolio—encompassing patents, design architectures, and verification tools—to semiconductor manufacturers and systems designers, who integrate these into their chips for applications in data centers, AI accelerators, consumer electronics, and automotive systems.

Rambus does not own fabrication facilities but collaborates with foundries like TSMC for product realization, emphasizing R&D investment (approximately $48.1 million or 42.9% of Q3 2024 revenue) to maintain technological leadership in areas such as DDR5, HBM, and GDDR interfaces.

The revenue mix has shifted dramatically toward products. The company achieved total revenue of $161.1 million for Q4 2024, comprising licensing billings of $63.6 million, product revenue of $73.4 million, and contract and other revenue of $29.5 million.

The DDR5 Chipset Opportunity

The chipset business is based on a chip called an RCD, which is an interface chip between processors and memory. That business has been growing quite nicely.

The DDR5 transition has created a dramatically expanded opportunity. The DDR5 penetration will lead to a DIMM chipset market of about approximately US$4 billion in 2028 with a CAGR from 2021-2028 of approximately 28%.

Competitive Position

With the continuous upgrading of Double Data Rate technology, the industry concentration continues to increase. In the DDR4 stage, there were only three vendors: Integrated Device Technology (IDT), which was acquired by Renesas in 2019, Montage, and Rambus.

The market has been reduced to three vendors: Renesas and Montage continue to be traditional competitors on the RCD side.

Regarding the DIMM chipset market revenue, there is head-to-head competition between Montage and Renesas, followed by Rambus. The three suppliers are responsible for 97% of the total revenue.

In October 2024, Rambus unveiled industry-first complete chipsets for both DDR5 RDIMM 8000 (Gen 5 RCD) and DDR5 MRDIMM 12800. The MRDIMM solution was revolutionary—using Multiplexed Registering Clock Drivers and Multiplexed Data Buffers, it doubled effective bandwidth by interleaving two DRAM ranks. No competitor had production MRDIMM solutions.

VIII. Bull Case, Bear Case & Competitive Analysis

The Bull Case

AI Infrastructure Beneficiary: The AI revolution requires massive memory bandwidth. Every NVIDIA H100 and AMD MI300 needs HBM. Every AI server needs DDR5. Rambus provides critical enabling technology for both.

Market Share Gains: The transition from DDR4 to DDR5 saw Rambus increase market share from approximately 25% to 40%. The DDR5 to DDR6 transition could provide similar opportunities.

Expanding TAM: The "companion chip" opportunity adds roughly $600 million to the addressable market beyond the core RCD business.

Management is excited about the MRDIMM opportunity, which will align with Intel's Diamond Rapids platform in the second half of 2026. The demand for MRDIMM remains strong, driven by the need for more memory and speed in AI servers.

Financial Strength: Rambus generated a record $94.4 million in operating cash flow in Q2 2025, swelling its cash reserves to $594.8 million as of June 30, 2025.

The Bear Case

Customer Concentration: The DRAM industry is highly concentrated, with Samsung, SK Hynix, and Micron controlling over 90% of the market. This creates significant customer concentration risk.

Competition: Direct competitors in the memory interface chip market, such as Montage Technology Co. Ltd. and Renesas Electronics Corporation, collectively hold over 80% of the global market share.

Technology Transitions: Each DDR generation represents both opportunity and risk. A poorly executed transition could result in market share loss.

The company faces challenges with the chaotic ramp of DDR5 in the market due to the complexity of making chips work together. Rambus Inc. is still monitoring the impact of new market entrants like NVIDIA's Grace architecture on its business.

Valuation: At first glance, Rambus's valuation appears steep: a trailing P/E ratio of 30 and a forward P/E of 24.62, both above the tech sector average.

Porter's Five Forces Analysis

Supplier Power (Low-Medium): Rambus relies on foundries like TSMC for chip manufacturing. While foundry capacity has historically been tight, Rambus's relatively small volumes give it less leverage than larger customers.

Buyer Power (High): The DRAM industry's extreme concentration means Rambus depends on a handful of massive customers. Samsung, SK Hynix, and Micron have significant negotiating leverage.

Competitive Rivalry (Medium): Only three significant players exist in the memory interface chip market. The oligopolistic structure limits price competition but creates intense technology competition.

Threat of New Entrants (Low): The technical complexity of memory interface chips creates high barriers to entry. These chips are harder and harder to make and to design, which is why the market has been reduced to three vendors.

Threat of Substitutes (Low-Medium): Alternative memory architectures (like NVIDIA's Grace with integrated memory) could reduce demand for traditional memory interface chips in certain applications.

Hamilton Helmer's 7 Powers Framework

Counter-Positioning: Rambus's transformation from pure licensing to hybrid products/licensing creates counter-positioning against IP-only competitors who cannot credibly transition to products.

Switching Costs: Memory module manufacturers must validate and certify interface chips—a lengthy, expensive process that creates meaningful switching costs.

Scale Economies: The fabless model means R&D costs are spread across royalty streams, creating operating leverage as DDR5 adoption accelerates.

Network Effects: Limited direct network effects, though JEDEC standard participation creates ecosystem stickiness.

Process Power: Three decades of memory interface expertise has created specialized knowledge that cannot be easily replicated.

Branding: Ironically, Rambus's notorious litigation history may now work in its favor—competitors are well aware of Rambus's IP strength and ability to defend it.

Cornered Resource: The company's patent portfolio and engineering expertise in high-speed memory interfaces represents a cornered resource that took decades to develop.

IX. Key Metrics to Watch

For investors tracking Rambus, three KPIs matter most:

1. DDR5 RCD Market Share

Currently at approximately 40%, this metric indicates Rambus's competitive position in its core business. Any significant deviation—up or down—signals meaningful changes in competitive dynamics. Watch for quarterly management commentary on market share trends.

2. Product Revenue Growth Rate

Product revenue has been growing at 40-50% year over year, far outpacing licensing revenue. The mix shift from licensing to products transforms Rambus's financial profile—products offer less leverage but greater recurring revenue visibility. Track the ratio of product revenue to total revenue quarterly.

3. Licensing Billings Stability

While product revenue gets the attention, licensing billings provide the high-margin foundation that funds R&D. The company completed a strategic extension of its patent licensing agreement with Micron through 2029, strengthening its long-term licensing foundation. Monitor the timing of major license renewals and any changes in per-unit royalty rates.

X. Conclusion: The Redemption Arc

The Rambus story defies simple categorization. The company that The Wall Street Journal described as "marked by litigation" has become an indispensable enabler of artificial intelligence infrastructure. The transformation required more than strategy—it required a fundamental rethinking of corporate identity.

In the relentless march toward artificial intelligence-driven economies, Rambus has emerged as a quiet but formidable force. The semiconductor memory innovator's recent results underscore its transformation from a niche IP licensing firm to a critical enabler of the AI infrastructure revolution.

The irony is profound. Rambus spent fifteen years fighting against industry-standard DDR memory, trying to force the world to adopt its proprietary RDRAM technology. It lost that battle decisively. But in the process, it accumulated deep expertise in high-speed memory interfaces—expertise that proved invaluable when the AI revolution created unprecedented demand for exactly that capability.

Today, NVIDIA's AI GPUs, AMD's data center processors, and the servers powering every major cloud provider depend on memory interface technology that Rambus pioneered, patented, and—after years of litigation—learned to sell as actual products rather than legal threats.

When you consider the company's 18% trailing ROE (well above the industry's 12%) and its 66% compound annual growth in net income over five years, the premium starts to look justified.

The question investors must answer is whether Rambus can maintain its competitive position as the industry transitions to DDR6 and HBM4, or whether the technical challenges that once made memory interfaces a three-player oligopoly will finally be solved by larger competitors.

What's certain is that Rambus has earned something it spent billions of litigation dollars trying to buy: industry respect. Not through courtrooms, but through engineering excellence. Not through patent threats, but through products that customers actually want to purchase.

That transformation—from industry villain to essential partner—may be Rambus's greatest innovation of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube