Reinsurance Group of America: The Quiet Giant Behind Global Life Insurance

I. Introduction & Episode Roadmap

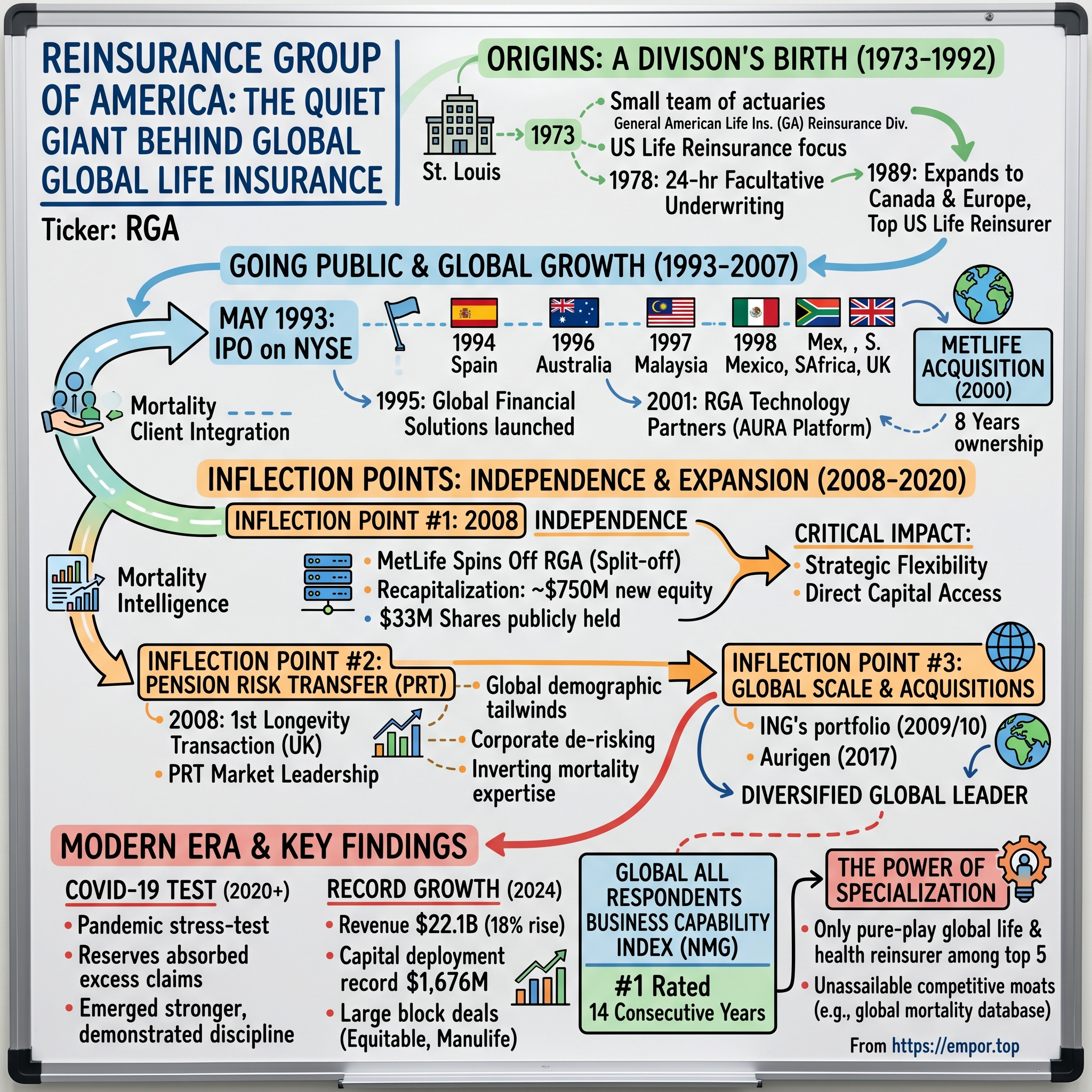

Picture this: a modest office building in St. Louis, Missouri, 1973. While America's attention focuses on Watergate hearings and oil crises, a small team of actuaries at General American Life Insurance Company quietly launches what would become one of the most consequential financial institutions most people have never heard of. Half a century later, that internal division has evolved into Reinsurance Group of America, Incorporated—a holding company for a global life and health reinsurance entity based in Chesterfield, Missouri, with approximately $3.9 trillion of life reinsurance in force and assets of $118.7 billion as of December 31, 2024, grown to become the only international company to focus primarily on life and health-related reinsurance.

The question that animates this deep dive is deceptively simple: how did an internal division of a regional St. Louis insurance company become the world's only pure-play global life and health reinsurer?

The answer spans corporate spin-offs, a perfectly-timed independence in the teeth of the 2008 financial crisis, and the relentless demographic tailwind of aging populations demanding pension security. Since debuting on the Fortune 500 in 2010, RGA has steadily grown, entering the top 200 in 2025. That trajectory tells a story of disciplined specialization in an era of financial conglomeration—and suggests lessons for investors trying to understand what creates durable competitive advantages in complex financial services.

The themes we'll explore are independence, specialization, global expansion, and the pension risk transfer revolution. Each represents a strategic inflection point that transformed RGA from a captive division into a global leader. Along the way, we'll examine how a company that operates almost entirely outside public consciousness has built one of the most enviable competitive positions in financial services.

For investors, RGA represents a fascinating case study: a deeply technical business with enormous barriers to entry, serving clients who desperately need what it offers, in markets that demographic forces are expanding inexorably. But as we'll see, the business also carries risks that require careful monitoring—from pandemic-driven mortality spikes to the concentration of longevity assumptions that could prove catastrophic if wrong.

II. What Is Reinsurance? (And Why Should Anyone Care?)

Before we can understand RGA's remarkable journey, we need to demystify its core business. Reinsurance is often described as "insurance for insurance companies"—but that shorthand obscures the profound financial engineering at its heart.

When a life insurance company sells you a policy, it takes on risk: the obligation to pay a death benefit when you die, or annuity payments for as long as you live. The timing of these payments is uncertain, but their eventual occurrence is not. An insurer writing thousands of policies accumulates enormous exposure to mortality and longevity risk—exposure that can strain capital reserves and limit the company's ability to write new business.

Enter reinsurance. Reinsurance is one of the most flexible risk and financial management tools. It should be considered alongside traditional capital instruments and corporate actions. RGA pioneered use of reinsurance as a financial management and portfolio-optimizing tool, and remains a leading provider of such solutions worldwide.

Think of it as a wholesale risk transfer mechanism. The primary insurer (called the "ceding company") pays premiums to the reinsurer in exchange for assuming some portion of the policy risk. This accomplishes several objectives simultaneously: it reduces the capital the insurer must hold against potential claims, stabilizes earnings by smoothing out the volatility of mortality experience, and frees capacity to write additional business.

But life and health reinsurance is fundamentally different from property and casualty reinsurance—a distinction crucial to understanding RGA's competitive position. P&C reinsurance deals with discrete events: hurricanes, earthquakes, fires. These events are unpredictable but relatively short-tailed—claims are filed and resolved within years. Life reinsurance, by contrast, deals with the statistical inevitability of human mortality across decades-long time horizons. A life insurance policy written today might not generate a claim for fifty years.

This temporal dimension creates both challenges and opportunities. The challenge: assumptions made today about mortality rates, investment returns, and lapse behavior will determine profitability decades hence. Get them wrong, and losses compound silently until they become catastrophic. The opportunity: the entity that builds the deepest understanding of mortality and longevity—through data, actuarial expertise, and accumulated experience—develops a nearly unassailable competitive advantage.

RGA has amassed one of the largest mortality databases in the world, and transforms this global perspective and local market insight into new ways to improve risk management, increase capital efficiency, and position partners and clients for success. Perhaps that is why RGA was rated #1 on NMG Consulting's Global All Respondents Business Capability Index in 2024, based on feedback from life and health insurance companies worldwide.

The mortality database deserves special attention. Every case RGA underwrites—every death claim processed, every longevity pattern observed—adds to a proprietary repository of mortality intelligence that took decades to build and would be nearly impossible for a new entrant to replicate. This data asset compounds in value with scale, creating a virtuous cycle where expertise attracts business, which generates data, which enhances expertise.

For investors, the key insight is this: reinsurance may be invisible to consumers, but it's essential to the financial system. Without reinsurance markets, primary insurers would need vastly more capital, insurance would cost more, and fewer people would be protected. RGA operates at the intersection of demographic inevitability and financial necessity—a position that creates remarkable durability even as it remains hidden from public view.

III. Origins: General American & The Birth of a Division (1973-1992)

St. Louis in the early 1970s was quietly becoming an unlikely hub of insurance innovation. The city's conservative Midwestern culture fostered a deep-rooted financial services ecosystem, anchored by institutions that valued actuarial precision over flashy growth. It was in this environment that General American Life Insurance Company decided to create something new.

General American Reinsurance, a reinsurance division formed in 1973 by General American Life Insurance Company (GA), was the forerunner to RGA. The company began as a reinsurance arm of General American Life Insurance. It wrote its first life reinsurance policy that same year in the U.S. market.

What began as an internal experiment quickly showed promise. In 1977, the division hired its first salesperson and secured its first mutual insurance client. In 1978, it adopted facultative underwriting with 24-hour turnaround standard. By 1980, the reinsurance business had grown to 40 clients and incorporated as RGA Reinsurance Company.

That 24-hour turnaround standard for facultative underwriting deserves emphasis. Facultative underwriting involves case-by-case assessments of individual policies that fall outside automatic treaty parameters—typically large face amounts or substandard risks. In an era before email, achieving consistent 24-hour turnaround required operational discipline that few competitors could match. This service orientation became part of RGA's cultural DNA.

The leadership during these formative years laid crucial groundwork. Greig Woodring joined General American in 1979 as an actuary, and assumed responsibility for General American's reinsurance business in 1986. Woodring would become the architect of RGA's strategic vision, combining actuarial precision with entrepreneurial ambition. His approach emphasized building deep client relationships over aggressive pricing—a philosophy that would prove prescient as the industry consolidated.

By 1989, the division had expanded into Canada and Europe, rising as the top US life reinsurer. This international expansion—beginning with the acquisition of the life reinsurance business of National Reinsurance of Canada—represented an early recognition that geographic diversification would be essential to managing the concentrated risks inherent in mortality-based businesses.

By 1992, it became a holding company with growing global operations. Incorporated in 1992 in the state of Missouri, Reinsurance Group of America, Incorporated was formed as a holding company for GA's U.S. and Canadian reinsurance businesses.

The decision to formalize RGA as a distinct holding company was strategic. By separating the reinsurance operations from General American's primary insurance business, the structure enabled cleaner regulatory treatment, more transparent capital allocation, and—crucially—the option to eventually access public capital markets. The groundwork was being laid for the next chapter.

What's remarkable about this origin story is how organic it was. RGA originated as the reinsurance arm of General American Life Insurance Company. It wasn't a typical startup but an internal division of General American Life. Leadership evolved organically as the operation grew and eventually became independent. There was no venture capital backing, no celebrated founders with Stanford MBAs—just actuaries in St. Louis who saw an opportunity to help insurers manage risk more efficiently.

The St. Louis culture mattered more than it might seem. The city's financial services community was tightly networked, with executives who valued long-term relationships over short-term transactions. This cultural inheritance shaped RGA's client-centric approach and would become a source of enduring competitive advantage as Wall Street-style approaches to financial services increasingly emphasized transactions over relationships.

IV. Going Public & Early Expansion (1993-1999)

May 1993 marked a pivotal moment. RGA was taken public by IPO in 1993 on the New York Stock Exchange (NYSE: RGA), with General American retaining a 65% share. The timing was propitious: the early 1990s insurance market was consolidating, and primary insurers increasingly sought reinsurance partners who could bring capital, expertise, and stability to complex transactions.

By 1993, GA's reinsurance division had grown its life reinsurance in force to $114.7 billion. From a standing start two decades earlier, RGA had assembled a substantial book of business and established relationships with major insurers across North America. The IPO provided currency for expansion and established a public valuation that would prove useful in future strategic moves.

General American's reinsurance division led to the formation of RGA, which Greig Woodring led through its initial public offering in May 1993. After more than 20 years of his leadership, RGA grew to become one of the world's leading life reinsurers, with offices in 26 countries and annual revenues of more than $10 billion.

The post-IPO years were marked by systematic international expansion. In 1994, RGA opened the company's first office in Spain. In 1995, RGA launched the business unit that would evolve into RGA Global Financial Solutions. In 1996, RGA opened its first office in Australia. In 1997, RGA opened its first office in Malaysia. In 1998, the company opened offices in Mexico, South Africa, and the United Kingdom.

This expansion strategy was deliberate but disciplined. Rather than pursuing growth for its own sake, RGA targeted markets where it could leverage its mortality expertise and client service model. Each new office was staffed with local professionals who understood regional regulatory environments and cultural nuances, but connected to the global platform's actuarial capabilities and mortality database.

Throughout the 1990s and 2000s, RGA pursued an aggressive expansion strategy, establishing operations in key international markets and acquiring several reinsurance companies to strengthen its global presence. The company expanded into Canada in the early 1990s, followed by entry into European markets and Asia Pacific regions. This international expansion strategy positioned RGA as one of the leading global life reinsurers.

The Global Financial Solutions business unit launched in 1995 represented a strategic evolution. Traditional reinsurance transfers mortality and morbidity risk; financial reinsurance uses reinsurance structures to address capital, accounting, and balance sheet optimization objectives. This capability expansion positioned RGA to serve insurers' full spectrum of needs—not just risk transfer, but comprehensive financial management.

Throughout this period, General American retained majority ownership, providing RGA with strategic stability while allowing operational independence. The arrangement worked well: RGA could pursue its global ambitions while benefiting from its parent's capital support and credibility. But changes were coming that would reshape the ownership structure entirely.

V. The MetLife Era & Growing Under a Giant (2000-2008)

The turn of the millennium brought seismic changes. MetLife acquired General American in 2000, including its interest in RGA, and after 8 years of ownership, MetLife spun RGA off to become a fully independent company.

MetLife's acquisition of General American wasn't primarily about RGA—it was a broader strategic consolidation move. But RGA came along as part of the package, suddenly finding itself a minority-owned subsidiary of one of America's largest life insurers. The implications were complex.

The benefits were tangible. MetLife's size conferred credibility with clients and rating agencies. As for RGA's A+ rating at the time, Fitch said the company "benefited from explicit and implicit financial support from Met that will no longer be available." Access to a major insurer's capital resources provided flexibility that a standalone reinsurer might lack. And MetLife's global footprint opened doors to client relationships RGA couldn't have accessed independently.

But the arrangement also created constraints. Operating as a subsidiary of a major life insurer introduced potential conflicts of interest—MetLife was both a competitor and a client to many of the insurers RGA served. Strategic decisions required MetLife approval. And RGA's growth ambitions sometimes competed with MetLife's own capital allocation priorities.

RGA, led by President and Chief Executive A. Greig Woodring, was primarily engaged in traditional life reinsurance. It was considered one of the leading life reinsurers in North America based on premiums and in-force business. Jack Lay, executive vice president and chief financial officer of RGA, said, "MetLife has been a very good company for us and has essentially allowed RGA's management team to run the company in the way it sees fit."

The MetLife years weren't merely a holding pattern—they were a period of continued expansion and capability building. In 2001, the company launched RGA Technology Partners, a dedicated unit to develop and implement innovative software solutions for the life insurance sector, including the Automated Underwriting and Risk Analysis (AURA) platform designed to streamline underwriting processes and improve efficiency for clients. Complementing this, RGA entered the Indian market in 2002 by opening a liaison office in Mumbai, aimed at marketing reinsurance support for individual and group life business amid India's growing insurance sector. These initiatives underscored RGA's commitment to innovation and global outreach under MetLife ownership, setting the stage for its 2008 spin-off into full independence.

The AURA platform deserves particular attention. Automated underwriting was transforming the life insurance industry, enabling faster policy issuance and more consistent risk assessment. By developing proprietary technology and offering it to clients, RGA deepened its integration into insurers' operations—creating switching costs that would reinforce long-term relationships.

RGA opened a representative office in Beijing in 2005. In 2006, RGA opened an office in Poland and expanded in the Central and Eastern Europe markets.

The Asia expansion was particularly significant. Asian insurance markets were growing rapidly as rising prosperity drove demand for protection products. RGA's early moves into China, India, and Southeast Asia established beachheads that would become major contributors to growth in subsequent decades.

By the mid-2000s, however, strategic logic increasingly pointed toward independence. RGA had grown to a scale where the benefits of MetLife ownership were diminishing while the constraints were becoming more limiting. Both management teams began exploring options for a clean separation.

VI. INFLECTION POINT #1: Independence (2008)

The date was September 12, 2008. Lehman Brothers had filed for bankruptcy just days earlier. Credit markets were seizing up. The global financial system was lurching toward what would become the worst crisis since the Great Depression. And in St. Louis, RGA was completing one of the most consequential transactions in its history.

This transaction, completed on September 12, 2008, recapitalized RGA with approximately $750 million in new equity capital and eliminated MetLife's controlling stake, enabling RGA to pursue independent strategic initiatives and expand its market presence.

The timing seems almost impossibly bad in retrospect. Who launches a financial services company into independence in the middle of a global financial crisis? But the deal's structure had been negotiated months earlier, and both MetLife and RGA had compelling reasons to proceed despite the chaos.

MetLife and RGA jointly announced their agreement on a transaction for MetLife to divest substantially all of its 52% interest in RGA through a tax-free split-off of RGA stock to MetLife stockholders. MetLife believed that the transaction would provide numerous benefits to MetLife and its stockholders, as well as to RGA and its shareholders, including facilitating MetLife and RGA's respective expansion and growth. MetLife and RGA also believed that the transaction would strengthen each company's ability to focus on developing and growing its core businesses. RGA believed that the transaction would be beneficial to its shareholders because, among other things, it would significantly increase the liquidity and public float of RGA's common stock by nearly doubling the number of shares held by public shareholders and would provide RGA management with greater flexibility in dealing with the opportunities and challenges specific to its businesses.

As a result of the recapitalization and split-off, RGA would no longer be majority-owned by MetLife, which would own, through its subsidiaries, 3,000,000 shares of RGA Class A common stock. As of September 11, 2008, and giving effect to the transaction, there were 33,079,838 shares of RGA Class A common stock and 29,243,539 shares of RGA Class B common stock outstanding.

Not everyone was optimistic. Fitch placed its A+ rating on RGA on its creditwatch negative list. The placement on creditwatch negative meant when the deal closed in September 2008, RGA's ratings probably would be downgraded. Fitch noted it would lower the rating by no more than two notches. As for RGA's A+ rating, Fitch said the company "benefited from explicit and implicit financial support from Met that will no longer be available."

The concerns were understandable. RGA was separating from its corporate parent precisely as capital markets were collapsing. But what looked like terrible timing proved to be remarkably advantageous.

The financial crisis created unprecedented demand for reinsurance. Primary insurers, their capital bases stressed by investment losses and increased regulatory scrutiny, needed risk transfer solutions more than ever. Meanwhile, many competitors had either failed, pulled back, or become distracted by their own crisis-related challenges. RGA, newly independent with fresh capital, was positioned to write business at attractive terms.

Moreover, independence unlocked strategic flexibility that had been constrained under MetLife ownership. RGA believed that the transaction would be beneficial to its shareholders because, among other things, it would significantly increase the liquidity and public float of RGA's common stock by nearly doubling the number of shares held by public shareholders and would provide RGA management with greater flexibility in dealing with the opportunities and challenges specific to its businesses.

The company could now pursue acquisitions without needing parent company approval, access capital markets directly, and compete for business without potential conflicts of interest clouding client relationships. The leash was off.

What followed vindicated the timing. Throughout the crisis, RGA maintained its conservative risk management approach, absorbed reasonable losses from investment portfolios, and emerged stronger relative to competitors who had taken on excessive risk in search of yield. The crisis became a competitive weapon—demonstrating to clients that RGA could be counted on even when markets were dislocating.

VII. INFLECTION POINT #2: The Longevity & Pension Risk Transfer Revolution (2008-2015)

Even as RGA was completing its separation from MetLife, the company was pioneering a business line that would reshape its strategic profile: longevity reinsurance and pension risk transfer.

RGA executed its first longevity reinsurance transaction in 2008 in the United Kingdom. Since then, RGA's Global Financial Solutions team has expanded its longevity risk transfer solutions set for clients in the U.S., Canada, the Netherlands, France, Ireland, and Spain. In Canada, RGA executed the first in-force longevity transaction in 2010 and the first longevity transaction including an underlying pension plan in 2015. Drawing on the extensive knowledge gained from other markets, RGA supported the U.S. Pension Risk Transfer market by executing the first longevity transaction in the U.S. in 2018.

To understand why this matters, consider the demographic trends reshaping retirement security worldwide. Corporate defined benefit pension plans—which promise employees specific retirement payments regardless of how long they live—had become enormous liabilities for sponsoring companies. As lifespans extended and interest rates declined, these obligations ballooned to levels that threatened corporate balance sheets.

Companies desperately wanted to transfer this longevity risk—the uncertainty about how long their retirees would live—off their books. Insurance companies were willing to assume these obligations through "buy-in" and "buy-out" transactions, but they in turn needed reinsurers to help manage the concentrated longevity exposure.

RGA is a market leader in addressing global longevity and pension risk transfer (PRT) solutions, offering unique insights and risk appetite. While the industry is familiar with the traditional longevity swap reinsurance protection, insurers are increasingly using complementary funded reinsurance. Use of this risk protection can create a win for all parties involved: the reinsurer, the insurer, the trustee, and the members themselves. RGA is a market leader in addressing global longevity and pension risk transfer (PRT) solutions, offering unique insights and risk appetite.

RGA's mortality expertise—built over decades from traditional life reinsurance—provided a unique advantage in longevity. The same database that helped price death benefits could be inverted to understand how long people would live. The actuarial skills were directly transferable, but few competitors had both the expertise and the appetite for the long-duration commitments longevity business requires.

The first longevity swap made public in the US was provided by RGA in 2018, and since then discussions around longevity swaps have only become more common, with a second transaction announced in late 2022.

The UK market led development of longevity reinsurance, driven by regulatory pressures on defined benefit pension schemes and a sophisticated buy-out insurer market. RGA's 2008 UK transaction established the company's credibility and provided operational experience that would prove valuable as other markets developed.

The team executed a $1.7 billion longevity swap covering approximately 11,000 single premium immediate annuity contracts with one of the world's largest life insurance groups, highlighting the rising interest in longevity risk management among U.S. clients. GFS leveraged its 15 years of longevity experience and long-term commitment to the U.S. market to expand its capabilities in the emerging U.S. pension risk transfer space.

The pension risk transfer market represents one of the most significant growth opportunities in financial services. Global pension liabilities run into tens of trillions of dollars, and a substantial portion will eventually need to be transferred to entities better positioned to manage longevity risk. RGA's early moves established it as the leading independent reinsurer in this space—a position reinforced with each successful transaction.

For investors, the longevity business is both exciting and concerning. The opportunity is enormous and growing. But longevity assumptions are inherently uncertain—medical breakthroughs could extend lifespans far beyond actuarial projections, transforming profitable books of business into long-term liabilities. RGA manages this risk through conservative reserving and diversification across geographies and vintages, but the tail risk remains.

VIII. INFLECTION POINT #3: Global Scale & Strategic Acquisitions (2010-2020)

Rather than a single moment, the consistent, strategic approach to entering new markets and making targeted acquisitions (like ING's portfolio and Aurigen) cumulatively transformed RGA. It shifted from a U.S.-centric operation to a diversified global leader with deep expertise across numerous life and health reinsurance niches.

The decade following independence was marked by systematic expansion—both organic and through strategic acquisitions. The approach was distinctly RGA: disciplined, relationship-focused, and opportunistic rather than empire-building.

In 2009, RGA acquired the U.S. and Canadian group life, accident, and health reinsurance business from ReliaStar Life Insurance Company, a subsidiary of ING Groep N.V., in a deal announced on October 16, 2009, and finalized effective January 1, 2010; this move diversified RGA's portfolio into group reinsurance markets in North America.

The ING acquisition was particularly significant. Group life and health reinsurance operates differently from individual life—the risks are smaller per life but more numerous, requiring different operational capabilities. Adding this business diversified RGA's risk profile and expanded relationships with major employers and group insurance carriers.

The Asia Pacific region became an increasingly important growth vector. Asia Pacific operations serve clients throughout the region from offices in Australia, China, Hong Kong, India, Japan, Malaysia, New Zealand, Singapore, South Korea, and Taiwan. Primary reinsurance products include individual and group life, living benefits, health, high net worth, Retakaful, superannuation, annuity, and financial solutions.

In recognition of RGA's commitment to innovation and client collaboration across Asia, RGA earned recognition: Rated #1 by insurers in Asia on NMG Consulting's 2024 All Respondents Business Capability Index. The Asia performance reflected decades of investment in local relationships, product development capabilities, and actuarial expertise tailored to regional markets.

Throughout this period, RGA maintained its pure-play focus on life and health reinsurance—a strategic choice that distinguished it from diversified competitors. Among the top five players, RGA is the only pure life reinsurer. The other four—Hannover Re, Munich Re, SCOR SE, and Swiss Re—operate in both the life and non-life spaces.

This focus created what Hamilton Helmer might call "counter-positioning"—a strategic choice that competitors couldn't easily match without sacrificing their own diversified business models. For Munich Re or Swiss Re to match RGA's specialization would require divesting their profitable P&C businesses, something their shareholders and organizations would resist.

The acquisitions during this period weren't just about scale—they were about capability building. Each transaction brought specialized expertise, client relationships, or market access that enhanced RGA's competitive position. And the company's disciplined approach to integration ensured these acquisitions generated value rather than distraction.

IX. Modern Era: COVID-19, Digital Transformation & Record Growth (2020-Present)

The COVID-19 pandemic represented the most severe test of RGA's business model in its history. About 70% of all respondents to an RGA survey reported additional COVID-19 claims in 2020, with more than one-third describing the volume increase as significant.

For a company whose entire business depends on mortality assumptions, a global pandemic that killed millions was precisely the scenario actuaries had modeled but hoped never to see. Claims surged as COVID-19 deaths overwhelmed historical baselines. RGA's reserves were tested against actual experience.

The third report analyzing mortality takes a more in-depth look at mortality from January 1, 2015, to December 31, 2020, highlighting that the fourth quarter of 2020 saw the largest number of death claims, representing a 9% increase over the second quarter of 2020. The study finds that by the fourth quarter, all face amount bands showed excess mortality over 20%. Offering extensive coverage of COVID-19's impact on mortality on insured lives compared to the general population, the report is based on 31 companies representing approximately 72% of the industry's face amount in force and 2.9 million death claims.

Yet RGA emerged from the pandemic not just intact but thriving. The Board of Directors thanked Anna Manning for her extraordinary leadership of RGA for the last six years, for her exceptional ability to build upon and strengthen RGA's legacy, and for her strong strategic capabilities that successfully led the organization through a pandemic of unforeseen scale in modern history.

The company's conservative reserving practices proved their worth. Years of building excess reserves against unexpected mortality events provided a buffer that absorbed pandemic losses without threatening capital adequacy. And the diversification across geographies and product lines meant that not all regions experienced peak mortality simultaneously.

Following the pandemic, RGA accelerated into an exceptional growth phase. In 2024, Reinsurance Group of America generated excellent financial results, reporting adjusted operating earnings per share excluding notable items of $22.57. Strong performance across all geographies and business lines produced $1.75 billion in adjusted operating income before taxes in 2024. In 2024, this approach produced total revenues of $22.1 billion, compared to $18.6 billion in 2023.

Premiums totaled $17.8 billion, an increase of 18% over 2023, including $2.9 billion in premiums from US pension risk transfer transactions.

The in-force block transaction business emerged as a major growth driver. Full-year capital deployment into in-force transactions reached $1,676 million, a record for RGA and an increase of approximately 80% over the previous record in 2023.

In-force transactions involve reinsuring existing blocks of policies rather than newly written business. As insurers seek to optimize their balance sheets, exit product lines, or generate capital for other purposes, these transactions have proliferated. RGA's scale, expertise, and reputation for execution certainty position it to win disproportionate share of this growing market.

Recent transactions illustrate the scale of opportunity. RGA Canada and Manulife announced the completion of the largest universal life reinsurance transaction in the Canadian market to date. The coinsurance transaction reinsured approximately CA$5.8 billion (US$4.4 billion) of reserves, accompanied by an equivalent asset transfer. This was the third large block reinsurance transaction between Manulife and RGA.

RGA is reinsuring 75% of Equitable's in-force life insurance liabilities. The block includes approximately $18 billion of general account reserves and $14 billion of separate account reserves. RGA expects to deploy $1.5 billion of capital at closing into this reinsurance transaction, based on expected required capital to support the block. RGA expects this transaction to contribute approximately $70 million of adjusted operating income before taxes in 2025.

On October 30, 2025, Reinsurance Group of America reported record third-quarter operating earnings, with revenue reaching US$6.20 billion and net income rising to US$253 million, aided by the successful closure of a US$1.5 billion reinsurance transaction with Equitable Holdings and a completed US$75 million share buyback.

Leadership transition marked another milestone. Tony Cheng was appointed president at RGA effective January 4, 2023, succeeding Anna Manning, who remained CEO. Consistent with her long-held plans, Manning retired as CEO on December 31, 2023. The board appointed Cheng as CEO effective January 1, 2024.

Cheng's background—rising through Asia operations to lead the global company—reflects the geographic diversification that RGA has achieved and the importance of international markets to future growth.

Innovation continues through initiatives like Ruby Re. Tony Cheng commented: "As a pioneer in the asset-intensive business, I am excited about the next step in our continuing support for this growing market segment. Ruby Re provides RGA with alternative capital that expands our capacity at attractive terms benefiting our clients, shareholders, and Ruby investors."

Ruby Re, Reinsurance Group of America's third-party life reinsurance sidecar, has now raised a total of $480 million in capital following the close of its second funding round, which is near the upper limit of the $400 million to $500 million target range for the Missouri-domiciled vehicle. Launched in December 2023 with backing from a number of investors, including insurance-linked securities specialist Hudson Structured Capital Management, Ruby Re writes U.S. asset-intensive life reinsurance business via RGA.

Ruby Re represents a significant strategic innovation. By creating a third-party capital vehicle, RGA can access additional capacity for large transactions without diluting its own shareholders, earn fee income for managing the vehicle, and demonstrate to sophisticated investors the attractiveness of life reinsurance returns.

X. The Business Model Deep Dive

Understanding RGA's competitive position requires examining its business model in detail. The company's core products include traditional life reinsurance, financial reinsurance, asset-intensive reinsurance, health reinsurance, and longevity and mortality risk solutions. RGA serves over 800 clients across more than 25 countries, making it one of the largest life reinsurers globally by premium volume.

RGA is the only global reinsurance company to focus exclusively on life and health solutions.

The business operates through distinct segments that serve different client needs:

The company operates through multiple business segments including U.S. and Latin America Traditional, U.S. and Latin America Financial Solutions, Canada, Europe Middle East and Africa, Asia Pacific, and Corporate and Other.

Traditional Life Reinsurance forms the foundation—transferring mortality and morbidity risk from primary insurers through treaty arrangements. This business generates predictable premium flows and benefits from RGA's mortality database and underwriting expertise.

Financial Solutions (including asset-intensive reinsurance) addresses capital optimization needs. Insurers cede blocks of business to RGA not primarily to transfer mortality risk but to improve regulatory capital ratios, exit product lines, or monetize embedded value. These transactions are often larger and more complex, requiring sophisticated structuring capabilities.

Longevity Reinsurance and Pension Risk Transfer represents the fastest-growing segment, driven by demographic trends and corporate de-risking needs.

Facultative Underwriting handles individual cases that fall outside automatic treaty parameters. Facultative underwriting at RGA involves individualized, case-by-case risk assessments for non-standard policies that fall outside automatic treaty parameters, ensuring thorough evaluation of high-risk or unique cases. Ranked number one by insurers for 11 consecutive years in NMG Consulting's Global Life & Health Reinsurance study, this service utilizes one of the world's largest mortality databases and local market insights to deliver substandard risk pricing and acceptance decisions. Tools like the FAC Exchange platform facilitate seamless digital submissions between insurers and reinsurers.

The mortality database represents perhaps RGA's most significant competitive asset. Accumulated over decades from millions of underwritten cases and claims experiences across diverse geographies, this proprietary data repository enables more accurate pricing than competitors can achieve. Every case processed enhances the database's value—a compounding advantage that becomes more valuable with scale.

RGA has also invested heavily in technology platforms that deepen client integration. AURA NEXT, the company's automated underwriting platform, helps insurers make faster and more consistent underwriting decisions while generating data that flows back to RGA. By making clients' businesses more efficient, these tools create switching costs that reinforce relationship durability.

For investors analyzing the business model, several characteristics stand out:

Recurring Revenue: Most reinsurance treaties extend for years or decades, creating predictable premium flows that aren't subject to annual competitive rebidding.

Negative Working Capital: RGA receives premiums before it pays claims, generating investment income on the float during the interim period.

Operating Leverage: The fixed costs of mortality expertise, technology platforms, and global infrastructure can be spread across growing premium volumes.

Network Effects Through Data: Scale generates data that improves pricing accuracy, which attracts more business, which generates more data.

XI. Porter's 5 Forces Analysis

Threat of New Entrants: LOW

RGA holds a strong competitive position as one of the top five global life reinsurers by premium volume, with particular strength in the North American market where it maintains approximately 15-20% market share in traditional life reinsurance. The company differentiates itself through its broad product portfolio, strong client relationships, and expertise in emerging markets.

Building a life reinsurance business from scratch faces near-insurmountable barriers. Regulatory capital requirements run into billions of dollars. The mortality database that underpins pricing accuracy requires decades of accumulated experience. Client relationships—built on trust established through years of claims payments and service—cannot be purchased. Rating agencies require demonstrated track records before assigning the ratings that clients demand. And the actuarial talent required to compete effectively is scarce and already employed by incumbents.

Bargaining Power of Buyers: MODERATE

Large primary insurers have substantial negotiating leverage—they can divide their reinsurance among multiple providers and credibly threaten to retain more risk internally. However, switching costs are meaningful: migrating reinsurance treaties requires regulatory approvals, administrative transitions, and relationship rebuilding. Long-term partnerships—some spanning decades—create mutual dependence that moderates buyer power. And for specialized capabilities like facultative underwriting or complex longevity transactions, the pool of qualified providers is limited.

Bargaining Power of Suppliers: LOW

RGA's primary "suppliers" are capital markets (for funding) and investment managers (for asset management). The company's scale and credit quality provide strong negotiating position in accessing debt and equity capital. Investment management is a competitive industry where RGA can select among numerous qualified providers.

Threat of Substitutes: LOW-MODERATE

Alternative risk transfer mechanisms—catastrophe bonds, sidecars, and other capital markets instruments—have gained significant traction in property & casualty reinsurance. In life reinsurance, these alternatives remain less developed, though initiatives like Ruby Re suggest they're emerging. In the financial solutions segment, RGA competes with specialized players including Athene Holding and Brookfield Asset Management subsidiaries. The competitive landscape has intensified in recent years as traditional insurers have increased their reinsurance activities and new capital sources have entered the market.

The rise of private equity-backed insurers—like Athene, Resolution, and others—represents a form of substitution threat. These players compete for in-force block transactions using alternative capital structures. However, they typically lack RGA's biometric expertise and often partner with RGA rather than competing directly for risk transfer needs.

Competitive Rivalry: MODERATE-HIGH

RGA operates in the highly competitive global life and health reinsurance market. The company's primary competitors include Munich Re, Swiss Re, Hannover Re, and SCOR SE.

Reinsurance Group of America and RenaissanceRe came in fourth and fifth place for non-IFRS 17 reporting, respectively, with RGA posting $14.3 billion in GWP and RenaissanceRe posting $12.3 billion in GWP.

The competitive landscape is concentrated but intensifying. Top competitors possess comparable scale, expertise, and client relationships. Competition occurs across multiple dimensions: pricing, service quality, product innovation, and relationship development. However, the industry's relationship-based nature limits price competition in favor of value-added service differentiation.

XII. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

With approximately $3.9 trillion of life reinsurance in force and assets of $118.7 billion as of December 31, 2024, RGA has grown to become the only international company to focus primarily on life and health-related reinsurance.

Scale generates multiple advantages. The mortality database improves with every case processed, enhancing pricing accuracy. Fixed costs—technology platforms, actuarial talent, regulatory compliance infrastructure—spread across larger premium volumes. Geographic diversification enables risk absorption that smaller competitors cannot match. And scale attracts talent, as actuaries and underwriters seek opportunities to work on significant, complex transactions.

2. Network Effects: MODERATE

Life reinsurance doesn't exhibit classic network effects where each additional user increases value for others. However, indirect network effects operate through data advantages and reputation. Each client relationship generates data that improves mortality insights. The industry's relationship-based nature means satisfied clients become references for prospective clients.

3. Counter-Positioning: STRONG

RGA is the only global reinsurance company to focus exclusively on life and health solutions.

This is arguably RGA's most significant competitive moat. Diversified competitors like Munich Re and Swiss Re generate substantial profits from property & casualty reinsurance. Matching RGA's life and health specialization would require either spinning off or de-emphasizing profitable P&C businesses—a strategic shift their shareholders and organizations would resist.

The pure-play focus enables deeper specialization: every technology investment, every talent hire, every strategic initiative advances life and health capabilities rather than being diluted across diverse business lines. Counter-positioning typically proves durable because it requires competitors to make painful strategic choices to respond.

4. Switching Costs: HIGH

Reinsurance relationships are designed for longevity. Treaties often extend for decades, with reserves transferred between parties and administrative systems integrated. Switching reinsurers requires regulatory approval, reserve recalculation, administrative migration, and relationship rebuilding. Perhaps most importantly, reputation considerations discourage switching: insurers don't want to be known as disloyal partners who abandon relationships for marginal pricing advantages.

5. Branding: STRONG

For the 14th consecutive year, RGA was rated #1 on NMG Consulting's 2024 Global All Respondents Business Capability Index, based on feedback from insurance companies worldwide. RGA has earned this recognition every year since the inception of NMG's Global Life & Health Reinsurance Study.

Ranked 223 on the 2023 Fortune 500 list, and named to the 2023 Fortune's list of the "World's Most Admired Companies." RGA was also named to Forbes' "America's 50 Most Trustworthy Financial Companies" 2014 list.

In a business built on trust, brand reputation matters enormously. RGA's consistent recognition by clients validates its service quality and market position. This brand equity becomes particularly valuable in competitive situations where technical capabilities are similar and clients must choose based on relationship factors.

6. Cornered Resource: STRONG

The mortality database represents a cornered resource that competitors cannot replicate through investment or acquisition. Built over fifty years from millions of cases across diverse geographies and risk profiles, this proprietary data asset underpins pricing accuracy that new entrants cannot match. The actuarial talent pool, while not exclusively "cornered," favors RGA given its scale and reputation as an employer of choice for mortality specialists.

7. Process Power: STRONG

Woodring's peers consistently characterize him as a thought leader who combines extraordinary intellectual curiosity, acumen, and capabilities with substantial solutions-oriented creativity. He is fascinated by the insurance industry's challenges and has an unusual track record for conceiving of and developing innovative and successful industry-altering solutions. One such solution is AURA, RGA's award-winning proprietary electronic underwriting solution.

Process power accumulates through embedded organizational capabilities that are difficult to articulate and transfer. RGA's underwriting processes, client service protocols, and actuarial methodologies have been refined over decades. The culture of client-centricity established by early leadership persists through organizational norms and hiring practices. Competitors can observe RGA's outputs but cannot easily replicate the processes that generate them.

XIII. Key KPIs for Investors

For investors monitoring RGA's ongoing performance, three metrics deserve particular attention:

1. Adjusted Operating Return on Equity (ROE)

RGA has updated its intermediate term financial targets, including raising its adjusted operating ROE target to 13% to 15%.

ROE captures how efficiently RGA converts shareholder capital into earnings. The reinsurance business is fundamentally about deploying capital to assume risk—ROE measures how well management prices that risk and manages expenses. Sustainable ROE above cost of capital indicates the competitive moat is generating economic profit rather than merely accounting profit.

2. Life Reinsurance In Force Growth

$3.9 trillion of life reinsurance in force as of December 31, 2024.

In-force represents the cumulative face amount of policies RGA has reinsured. Growth in this metric reflects both new business production and retention of existing treaties. Importantly, in-force growth doesn't require immediate revenue recognition—it represents future premium and profit potential that will emerge over time.

3. Capital Deployment into In-Force Block Transactions

Full-year capital deployment into in-force transactions reached $1,676 million, a record for RGA and an increase of approximately 80% over the previous record in 2023.

This metric captures RGA's success in winning large reinsurance transactions that involve acquiring existing blocks of policies. These transactions are episodic and competitive—success requires having both capital available and the expertise to execute complex deals. Sustained capital deployment at attractive returns indicates competitive strength in this growing market segment.

XIV. Bull Case & Bear Case

Bull Case

The structural tailwinds supporting RGA's business are extraordinary. Aging populations across developed economies are creating unprecedented demand for pension risk transfer solutions. Corporate sponsors are desperate to exit defined benefit obligations, and RGA has established itself as the leading independent reinsurer in this space. Each completed transaction reinforces relationships and reputation, creating a virtuous cycle of opportunity.

The competitive moat appears deep and durable. Fifty years of mortality data cannot be replicated through investment. Counter-positioning against diversified competitors creates strategic protection. Client relationships built over decades generate trust that switching cannot easily erode. And the regulatory complexity of life reinsurance creates barriers that new entrants cannot easily overcome.

Recent financial performance demonstrates operating leverage emerging from scaled infrastructure. Revenue growth is translating into even faster profit growth as fixed costs spread across larger volumes. The Ruby Re sidecar structure provides access to additional capacity without shareholder dilution, enabling participation in larger transactions.

Management succession has been smooth, with Tony Cheng bringing international experience and fresh perspectives while maintaining strategic continuity. The culture of client-centricity established by founding leadership appears institutionalized rather than personality-dependent.

Bear Case

Concentration risk deserves serious consideration. RGA's entire business depends on mortality and longevity assumptions that could prove materially wrong. A breakthrough in life-extension technology could transform profitable longevity business into long-term liabilities. A new pandemic more lethal than COVID-19 could overwhelm reserves. These tail risks are difficult to quantify but potentially catastrophic.

Competition is intensifying. Private equity-backed platforms like Athene and Resolution have raised substantial capital to compete for in-force transactions. Diversified reinsurers are investing in their life capabilities. Alternative capital is entering the market through structures like RGA's own Ruby Re. Market share gains may require pricing concessions that compress margins.

Interest rate sensitivity creates earnings volatility. RGA's investment portfolio generates income that contributes significantly to earnings. Declining rates compress investment returns; rapidly rising rates create mark-to-market losses on bond portfolios. Management skill in asset-liability matching matters, but cannot eliminate this sensitivity entirely.

Regulatory risk represents an ongoing overhang. Insurance regulation is complex, varies by jurisdiction, and can change in ways that disadvantage reinsurers. Accounting standards transitions (like LDTI and IFRS 17) create one-time disruptions and ongoing compliance costs. Political pressure could constrain offshore reinsurance structures that RGA and competitors use for capital efficiency.

Myth vs. Reality Box

Myth: Life reinsurance is a boring, low-growth business. Reality: RGA's revenues have grown from $18.6 billion in 2023 to $22.1 billion in 2024—nearly 19% growth. Demographic trends are creating unprecedented demand for longevity risk transfer. The business is growing faster than most "exciting" growth stories.

Myth: COVID-19 proves life reinsurers cannot manage pandemic risk. Reality: RGA emerged from the pandemic with strengthened competitive position. Conservative reserving absorbed excess claims. Diversification limited geographic concentration. The crisis demonstrated risk management discipline that enhanced credibility with clients.

Myth: RGA competes primarily on price. Reality: Service quality, relationship depth, and technical expertise differentiate competitive position. RGA's #1 NMG ranking for 14 consecutive years reflects client perception of value beyond pricing. Switching costs make price competition less relevant than in commoditized industries.

XV. Conclusion: The Power of Specialization

The RGA story defies conventional wisdom about competitive strategy in financial services. In an era when scale-through-diversification became the dominant paradigm—when Citigroup aspired to be a financial supermarket and European bancassurers combined banking, insurance, and asset management—RGA doubled down on specialization.

The company that began as an internal division of a regional St. Louis insurer became the world's only pure-play global life and health reinsurer by resisting the temptation to expand into adjacent businesses. That strategic clarity enabled investment in capabilities that diversified competitors couldn't match without cannibalizing other profit centers.

RGA is the only global reinsurance company to focus exclusively on life and health solutions.

The result is a competitive position built on cornered resources (the mortality database), counter-positioning (pure-play focus), switching costs (long-term treaty relationships), process power (accumulated underwriting expertise), and scale economies (global infrastructure). Few companies can claim strength across so many dimensions of strategic advantage.

For investors, RGA offers exposure to several secular trends: aging populations demanding pension security, corporate de-risking of defined benefit obligations, insurance industry consolidation creating block transaction opportunities, and emerging market growth in life insurance penetration. The company's conservative culture and proven risk management provide protection against the tail risks inherent in mortality-based businesses.

The path from a 1973 startup division to $3.9 trillion in reinsurance in force required patience, discipline, and strategic clarity. RGA's leaders resisted the temptation to diversify, maintained client focus through ownership changes and market cycles, and invested consistently in capabilities that compound over time.

In St. Louis, far from the spotlight of financial center glamour, that quiet giant continues building value. Most people will never know RGA exists. But for the insurance companies that rely on its expertise, the pension beneficiaries whose payments it underwrites, and the shareholders who benefit from its competitive advantages, RGA's obscurity belies its significance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube