Jones Lang LaSalle: The 240-Year Story of Commercial Real Estate's Global Titan

I. Introduction & Episode Roadmap

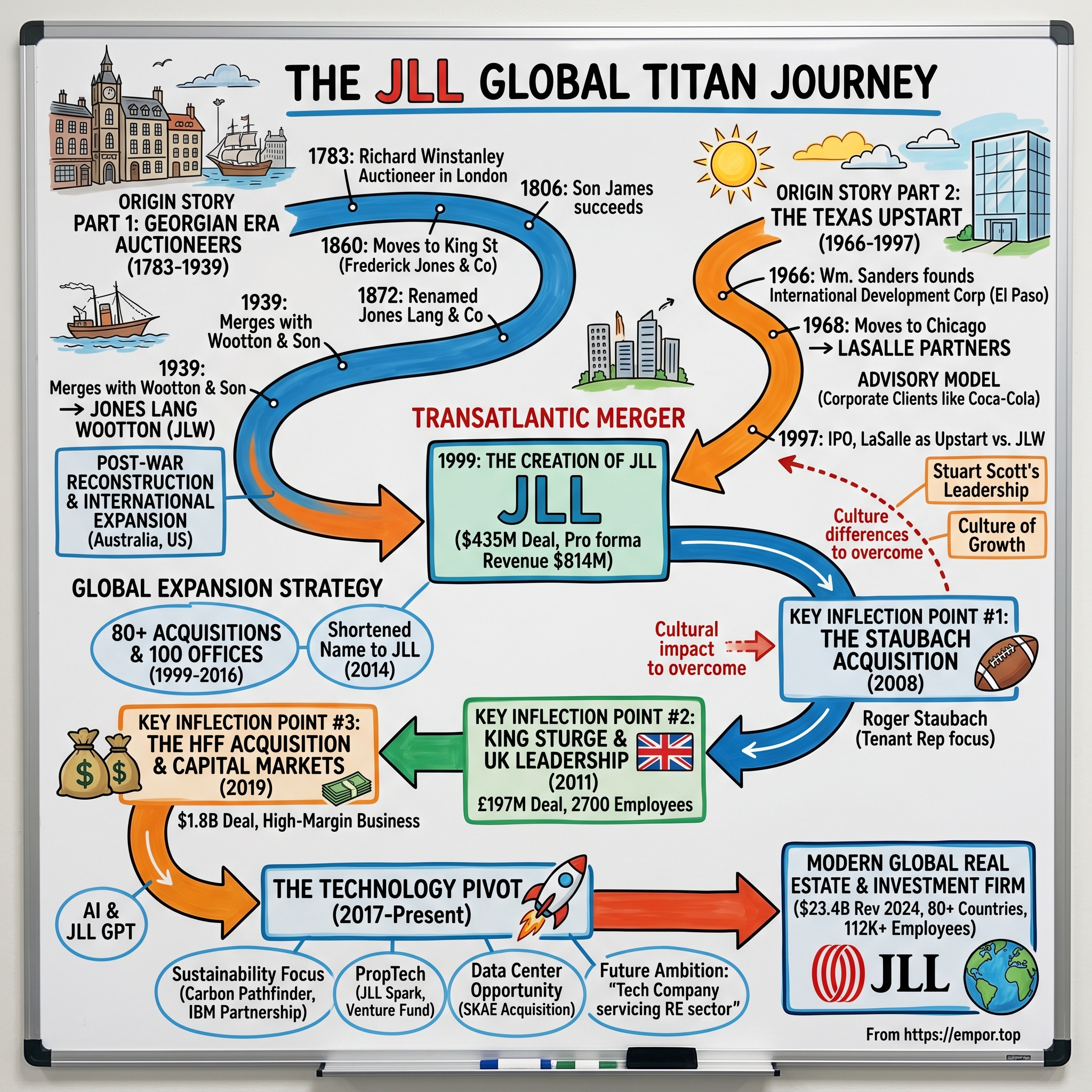

In 1783, as the ink dried on the Treaty of Paris ending the American Revolution, a London auctioneer named Richard Winstanley set up shop on Paternoster Row—a narrow street near St. Paul's Cathedral where booksellers and publishers had congregated for centuries. He couldn't have known that his modest auctioneering business would, over the course of two and a half centuries, evolve into one of the largest commercial real estate services firms on Earth.

Jones Lang LaSalle Incorporated (JLL), a Fortune 500 company with a rich history dating back to 1783, stands as a leading global commercial real estate and investment management firm, boasting $23.4 billion in revenue for 2024 and operating in over 80 countries.

The central mystery of JLL's story is this: How did a Georgian-era London auctioneer and a Texas real estate startup founded nearly 200 years later merge to become one of the "Big Four" commercial real estate titans? Several firms consistently rank among the top commercial real estate companies worldwide. CBRE, JLL, and Cushman & Wakefield are recognized for their substantial influence and market share. They lead in various sectors, including leasing, sales, and property management.

The JLL story is fundamentally about the industrialization of real estate services—the transformation of a fragmented cottage industry of local surveyors, auctioneers, and property managers into a global, technology-enabled platform capable of serving multinational corporations across every continent. It's a story of two corporate cultures separated by an ocean and two centuries of history, brought together by the relentless logic of globalization.

A Fortune 500® company with annual revenue of $23.4 billion and operations in over 80 countries around the world, our more than 112,000 employees bring the power of a global platform combined with local expertise.

This article will trace two origin stories separated by 200 years, examine the transatlantic merger that created modern JLL, dissect the roll-up strategy that built a global empire, and analyze the key inflection points—Staubach, King Sturge, HFF—that transformed the company from a respected player into an industry giant. We'll explore the technology pivot that's reshaping the company's future and assess what all of this means for investors trying to understand commercial real estate services as an asset class.

II. Origin Story Part 1: The Georgian Era Auctioneers (1783–1939)

Picture London in 1783. The American colonies had just won their independence. The British Empire, humbled but hardly defeated, was already pivoting toward India and the East. Paternoster Row, tucked behind St. Paul's Cathedral, was the heart of London's book trade—a cacophony of printers, publishers, and booksellers hawking everything from Bibles to radical pamphlets.

The enterprise that became known as Jones Lang Wootton began operating in 1783. That year, Richard Winstanley established himself as an auctioneer in London's Paternoster Row, where the business would remain for more than 70 years.

Winstanley was not dealing in books. He was an auctioneer—a middleman in an age when property changed hands through public sales, often conducted in coffeehouses and taverns. The 18th-century London property market was a wild affair: no standardized contracts, no professional surveying standards, and precious little transparency. An auctioneer's reputation was his bond.

The business passed through generations. Richard Winstanley sets up shop as an auctioneer in London and is succeeded by his son James in 1806. Father to son, the firm evolved with the city itself, weathering the Napoleonic Wars, the Victorian building boom, and the transformation of London into the capital of a global empire.

In 1860, the London business moves from Paternoster Row to King Street and eventually becomes known as Frederick Jones and Co. In 1872, it was renamed Jones Lang and Co. In 1939, Jones Lang and Co. merged with Wootton and Son to form Jones Lang Wootton.

The name changes tell a story of partnership evolution—different families and principals cycling through the firm, each leaving their mark on the corporate DNA. But the core business remained remarkably stable: valuations, auctions, property management, and increasingly, professional surveying services as the Royal Institution of Chartered Surveyors (founded 1868) established standards for the profession.

The start of World War II in 1939 also marked the year Jones Lang and Co. merged with a 47-year-old company named Wootton and Son. The union created Jones Lang Wootton, a company whose growth would benefit significantly from the destruction caused by a world at war. By the end of the war in Europe, London bore the marks of German air raids. The destruction of property by bombing and fires was exacerbated by the destruction of documents that delineated boundaries and ownership of the property destroyed. Amid the confusion, Jones Lang Wootton stepped into the breach.

War, paradoxically, accelerated Jones Lang Wootton's growth. The company searched for the owners of small land parcels, combined the properties, and secured contracts for either leasing or purchasing the amalgamated land parcels. By so doing, Jones Lang Wootton was able to secure licenses for development, which put the company in an enviable position for growth when the massive task of rebuilding London began in earnest in 1954.

The post-war reconstruction boom transformed Jones Lang Wootton from a respected London firm into an international player. Jones Lang Wootton's participation in post-World War II development and reconstruction delivered powerful growth, providing the financial means and the confidence to expand internationally. The company established its first major overseas presence in Australia. In 1957, a British expatriate residing in Australia, Ronald Collier, approached Jones Lang Wootton officers in London, seeking their support. Although there was no investment market in Australia, company officials foresaw significant potential in the country. In 1958, the company established offices in Sydney and Melbourne.

By the mid-1960s, the company's presence in Australia had become entrenched, developing into an operation consisting of nearly two dozen partners and a staff of 300. Jones Lang Wootton's success in Australia served as a springboard for expansion throughout the Pacific Rim.

By 1976, Jones Lang Wootton had expanded into the United States real estate market in New York City. The firm that had started as a Georgian-era auctioneer was now a multinational operation—though still operating as a traditional partnership rather than a modern corporation.

Of the two companies, LaSalle Partners could be considered the upstart, although the breadth and depth of clients and experience brought to the corporate marriage by the Chicago-based company were considerable. In terms of length of existence, however, the U.S. half of JLL paled when compared with the storied past of its British counterpart. Jones Lang Wootton was founded nearly 200 years before LaSalle Partners.

The Georgian-era origins matter because they established a cultural DNA—a reverence for professional standards, client relationships, and measured expansion—that would later have to be reconciled with the more aggressive, entrepreneurial spirit of its American partner.

III. Origin Story Part 2: The Texas Upstart (1966–1997)

Six thousand miles from London's Paternoster Row, in the sun-baked streets of El Paso, Texas, a different kind of real estate business was taking shape in 1966. William Sanders founded the real estate company International Development Corp in 1966 in El Paso, Texas.

William Sanders was the antithesis of the Jones Lang Wootton tradition. William Sanders is one of the most influential figures in the history of the REIT (Real Estate Investment Trust) industry. Where the British firm had evolved organically over two centuries, Sanders was building something from scratch—and he was building it fast.

Born in Minnesota and raised in El Paso, Sanders was in his 20s and living in Texas when, in 1966, he founded a real estate company called International Development Corp. In 1968, then single, he moved himself and the company to Chicago.

Sanders renamed the company LaSalle Partners in 1968 and relocated to Chicago, Illinois. The name was no accident—LaSalle Street was Chicago's financial corridor, the Wall Street of the Midwest. By choosing this name, Sanders was signaling his ambitions: this wasn't going to be a regional developer; this was going to be a financial services firm that happened to specialize in real estate.

In 1968, Sanders moved to Chicago and founded LaSalle Partners, a real estate advisory firm that worked with major corporations like Ford, Coca-Cola, and Eastman Kodak. The company specialized in helping corporate clients manage, finance, and optimize their property portfolios. This included structuring sale-leaseback deals, developing headquarters buildings, and advising on how to treat real estate as a strategic asset rather than just a line-item expense. LaSalle's model was ahead of its time.

Sanders understood something that few in the industry grasped at the time: corporations owned enormous amounts of real estate, but they managed it poorly. They lacked the expertise to optimize their holdings, and they rarely thought strategically about whether they should own or lease their facilities. LaSalle Partners would become their trusted advisor—essentially an outsourced real estate department for Fortune 500 companies.

The company first offered investment banking, investment management, and land services. By 1997, LaSalle had grown into three business divisions, Management Services, Corporate and Financial Services, and Investment Management.

The business model was inherently scalable in a way that traditional brokerage wasn't. Once you had a relationship with a major corporation, you could provide services across all of their facilities nationwide—and eventually worldwide. Each additional service you offered deepened the relationship and increased switching costs.

Sanders himself was a restless entrepreneur. In 1987, Sanders sold his stake in LaSalle to Japan's Dai-ichi Life Insurance Company for an estimated $65 million, the equivalent of about $185 million today after adjusting for inflation. The timing was notable, as the sale occurred shortly before the late-1980s real estate downturn.

Following his exit from LaSalle, Sanders shifted from advising companies to building them. In 1991, he launched Security Capital Group, a Santa Fe–based holding company designed to incubate and control a new generation of REITs. Rather than simply investing in real estate, Sanders aimed to build operating companies with strong management teams and data-driven acquisition strategies. His goal was to professionalize and scale real estate investment in the same way industrial firms had scaled manufacturing.

The sale of Sanders's stake didn't slow LaSalle Partners' growth. For its part, LaSalle Partners entered the 1990s with ambitious plans to expand its operations. In the last years leading up to its merger with Jones Lang Wootton, the company embarked on an acquisition campaign that added significantly to the might of the soon-to-be created JLL. In 1994, LaSalle Partners acquired a real estate investment advisor named Alex Brown Kleinwort Benson Realty Advisors Corporation. A London-based investment advisor, CIN Property Management Limited, was added two years later, followed by the acquisition of a property and development management company named Galbreath Company in 1997. After completing its initial public offering of stock in July 1997, LaSalle Partners purchased the project management business belonging to Satulah Group in January 1998. Later in the year, the company purchased the fourth largest management services firm in the United States, COMPASS Management and Leasing, Inc.

The 1997 IPO was a watershed moment. Stuart Scott was "one of the leading figures in guiding the strong and successful growth of LaSalle Partners through the 1990s." The man who had built LaSalle Partners into a real estate powerhouse was Stuart L. Scott—a Chicago lawyer-turned-real-estate-executive who brought professionalism and strategic vision to an industry that desperately needed both.

After law school, Scott began working as an attorney for the Securities and Exchange Commission. He also worked briefly for the Vedder Price law firm before entering commercial real estate. His first job was at Arthur Rubloff & Co., where he was a vice president and assistant to the chairman. In 1973, Scott took a job as president and chief operating officer at development company Equity Control Corp., which was renamed Equity Associates. Equity Associates was the development unit of LaSalle Partners, which Sanders had formed in El Paso, Texas, in 1968.

The Texas upstart had become a Chicago institution, a publicly traded company with global ambitions. But to truly compete on the world stage, LaSalle Partners needed something it couldn't easily build: a global footprint. And Jones Lang Wootton needed something it lacked: a dominant U.S. presence and a corporate structure suited for rapid growth.

IV. The Transatlantic Merger: Creating JLL (1999)

After LaSalle Partners' initial public offering (IPO) in 1997, which was led by its first CEO, Stuart Scott, it merged with Jones Lang Wootton in 1999, to form Jones Lang LaSalle (JLL) as part of a $435 million deal. Jones Lang Wootton was a London auctioneer that originated in the 1700s.

The strategic logic was compelling. Large corporate clients were saying, "We want somebody with offices all over the world who is strong in the U.S. and can give us consistent service wherever we go," Scott told the Tribune in 1999. While LaSalle Partners had begun opening offices abroad before acquiring Jones Lang Wootton and had eight foreign offices before the merger, the firm felt it needed closer to 30 offices to be truly global, and Scott had worried that to open them on its own could take LaSalle Partners a decade or more. "We were afraid (other companies) would leave us behind."

By 1976, Jones Lang Wootton had expanded into the United States real estate market in New York City. The company had 4,000 employees in 33 countries around the time of the merger with LaSalle Partners. Jones Lang Wootton brought exactly what LaSalle needed: an established international network with deep roots in Europe, Asia Pacific, and Australia.

Jones Lang Wootton and LaSalle Partners merged in March 1999, creating JLL, a truly global real estate services firm and investment manager with pro forma revenue of $814 million.

But mergers on paper are easy; mergers of corporate cultures are hard. Jones Lang Wootton and LaSalle Partners merged in March 1999, creating JLL, a truly global real estate services firm and investment manager with pro forma revenue of $814 million. Although both companies professed similar corporate values, promising to ease the union of their corporate cultures, the merger proved to be more complex than anticipated.

The challenges were real. You had a 216-year-old British partnership culture—methodical, relationship-driven, conservative—colliding with a 30-year-old American corporate culture—aggressive, growth-oriented, and accustomed to the pace of publicly traded companies. The integration consumed enormous resources.

Jones Lang LaSalle's aim was to standardize real estate services worldwide, Scott said. "We want to be … one global business, with one level (of) service no matter where we go," he said. "We'll be constantly reviewing and honing, so that it will be consistent and cutting edge all over."

As JLL plotted its course for the 21st century, the process of integrating LaSalle Partners and Jones Lang Wootton continued. The early years of the new century saw the company reduce its debt and achieve financial growth, despite the constraints of a difficult global economy. Between 1999 and 2001, JLL reduced its debt by $100 million, eclipsing the company's original two-year projection of $40 million.

Stuart Scott's leadership during this period was crucial. "We are deeply saddened to learn of the passing of Stuart Scott, former chairman and CEO of JLL," says Christian Ulbrich, CEO, JLL. "He was one of the leading figures in guiding the strong and successful growth of LaSalle Partners through the 1990s, and a primary architect of the ground-breaking 1999 merger with Jones Lang Wootton. A truly inspirational figure in US and global real estate circles, Stuart will be sorely missed." A founder of LaSalle Partners, and then JLL, Scott dedicated his life to the challenge of bringing professionalism, superior services, high ethical standards and a commitment to act always "in the client's best interests" to the commercial real estate industry. He led the firm's rapid growth, including its initial public offering in 1997 and a range of mergers and acquisitions highlighted by the 1999 merger of LaSalle and UK-based Jones Lang Wootton to form Jones Lang LaSalle. He remained chairman and chief executive officer of JLL until his retirement in 2005.

"(Scott has) left a legacy of an extraordinary company, which has grown magnificently based upon the infrastructure and governance that he created," said Ariel Investments chairman and CEO John W. Rogers Jr., whose firm has been an investor in Jones Lang LaSalle. "The merger of the two companies that made Jones Lang LaSalle come together was his vision, and it has just worked out beautifully." Rogers also called Scott "a big believer" in diversity. "He's left a great legacy of a very diverse board of directors and a diverse management team."

The transatlantic merger created something genuinely new: a real estate services firm that could credibly claim to serve clients anywhere in the world with consistent standards of service. It was no longer necessary for a multinational corporation to cobble together relationships with different property advisors in each country. JLL could be the single point of contact.

Following the merger, the two business segments were operated as LaSalle Investment Management and Jones Lang LaSalle Hotels. LaSalle Investment, with $22 billion of assets under management by 2002, assisted customers in buying, selling, and managing property, offering services such as property development, property management, project management, leasing, and tenant representation. Jones Lang LaSalle Hotels provided advisory, transaction, financial, and management services.

The merger set the template for what would become JLL's defining strategy over the next two decades: acquire capabilities, integrate them into the platform, and offer clients an ever-broader suite of services.

V. Post-Merger Growing Pains & The Corporate Solutions Pivot (2000–2007)

The early 2000s tested the newly merged company. The dot-com bust of 2000, followed by the September 11 attacks in 2001, created a challenging environment for commercial real estate. Office vacancy rates spiked. Corporate clients were slashing costs, not expanding.

But it was JLL's own organizational structure that posed the biggest challenge. The company had been built through mergers and acquisitions, and it operated as a collection of autonomous business units—leasing, property management, investment management—each with its own P&L, its own leadership, and its own client relationships.

The problem became clear when a major client, Bank of America, signaled that it intended to consolidate its real estate services with only a few providers that could offer integrated global solutions. JLL risked losing this critical account unless it could demonstrate that its various business units could work together seamlessly.

This was the catalyst for a fundamental organizational transformation. JLL created a new Corporate Solutions Group designed to stimulate collaboration across business units. Account managers were appointed to coordinate services for major clients, ensuring that the leasing team, property managers, and project managers were all working from the same playbook.

The pivot reflected a broader industry trend. Corporations were increasingly treating real estate as a strategic asset to be optimized rather than a cost center to be minimized. They wanted partners who could think holistically about their portfolios—advising on whether to own or lease, how to optimize space utilization, where to locate new facilities, and how to manage energy costs and sustainability.

JLL's integrated service model was perfectly positioned for this shift. The more services a client consumed, the stickier the relationship became. A client using JLL for leasing, property management, project management, and investment advisory was far less likely to switch providers than one using JLL for a single service line.

By the mid-2000s, JLL had stabilized the post-merger integration and was positioned for growth. But the company's most transformative acquisition was still ahead—one that would reshape its culture and accelerate its dominance in the Americas market.

VI. Key Inflection Point #1: The Staubach Acquisition (2008)

Heisman Trophy winner Roger Staubach was a 27-year-old rookie when he joined the Dallas Cowboys in 1969, after keeping his commitment of service to the U.S. Navy. Earning a salary of just $25,000, he began looking for work in the offseason. A Naval Academy friend connected him with the Henry S. Miller Co. Staubach joined in 1970, working briefly in its insurance division until he talked firm leaders into letting him get involved on the real estate side of things. "I worked every offseason until I decided that I wanted to make real estate a future for me, outside of football."

Roger Staubach was more than a football legend. He was a business phenomenon—a man who parlayed his fame, work ethic, and genuine passion for real estate into one of the most successful brokerage firms in the country.

After learning the ropes at Miller, Staubach joined developer Robert Holloway in a boutique venture in 1977. He retired from football in the spring of 1980, and two years later formed his own firm, The Staubach Co.

It was an amicable split; Holloway wanted to focus on development, and Staubach wanted to build a company around his interest in representing tenants.

The tenant representation concept was revolutionary. Today, tenant representation is a conventional part of the commercial real estate business. But 40 years ago, it was anything but. Landlords had enjoyed having the leverage in negotiations and not having to compete as much against other properties.

Staubach saw the opportunity: in most real estate transactions, the broker represented the landlord. Who was looking out for the tenant? By exclusively representing tenants, Staubach could offer unconflicted advice—a fiduciary relationship rather than an adversarial one.

Roger Staubach, whose football persona had been one of taking risks, never giving up and of diving into oncoming tacklers to get an extra yard rather than stepping safely out of bounds, was conversely a cautious and conservative businessman. He preferred to avoid risk, disdaining speculative development projects in favor of concentrating his firm's energies on the less glamorous work of brokering leases for tenants.

This counterintuitive combination—famous risk-taker on the field, conservative businessman off it—made The Staubach Company unusual. While competitors chased the boom-and-bust cycles of development, Staubach built a steady fee-based business that could weather economic storms.

With his connections and high profile, Staubach became a broker's business development dream. What's more, he didn't take any of the commissions. "I knew the business we'd win would benefit the company, and the commission stuff can be tricky," Staubach says. "Commissions are important, but they're secondary to making sure you do the right thing for customers."

After experiencing rapid growth in North Texas, clients compelled Staubach to help them in other markets. The firm opened branches in other cities, giving professionals there a stake in their local operations. At its peak, The Staubach Co. had 60 offices across the country with 1,600 employees.

By 2008, Staubach's clients were asking him to help them with deals in international markets. Around the same time, global firm JLL was seeking to expand in the U.S. The two parties seemed to be a good match, and in June of that year, JLL acquired The Staubach Co. for $613 million.

The deal came together at a particularly treacherous moment: the global financial crisis was accelerating. But the strategic logic was unassailable. JLL needed to strengthen its U.S. brokerage capabilities, and Staubach needed global reach to serve its clients' expanding footprints.

"Though 1,000 Staubach employees merged with JLL's nearly 33,000, top execs agree that the culture of The Staubach Co. made a significant impact. "If you look at our company today in the Americas, it looks as much like Staubach as it does like JLL."

The cultural integration was remarkably successful—a testament to the alignment between Staubach's values and JLL's corporate culture. JLL purchased The Staubach Company in 2008. Roger Staubach served as executive chairman of JLL from 2008 until he retired in 2018.

Staubach stayed on with JLL as executive chairman before retiring in 2018. A devout family man, Staubach likens the merger to the most important relationship in his life. "My wife Marianne and I have been married for 56 years, and it's a great marriage," he says. "I'm fortunate that the JLL and Staubach Co. marriage could not have been more perfect, too."

The Staubach acquisition demonstrated something important about JLL's M&A strategy: the company wasn't just buying revenue or market share. It was buying culture, talent, and client relationships. When those aligned with JLL's existing culture, the integrations worked beautifully. When they didn't, they became expensive distractions.

VII. Key Inflection Point #2: King Sturge & UK Market Leadership (2011)

If the Staubach deal strengthened JLL's position in the Americas, the King Sturge merger consolidated its dominance in its ancestral home market: the United Kingdom.

In May 2011, King Sturge was purchased by JLL for £197 million. King Sturge LLP was a British property management and consultancy company with over 210 offices and 4,200 staff in 45 countries. It operated throughout the UK and Europe and had associations and partners in Asia Pacific and North, Central and South America. The firm covered all property sectors and related services such as logistics, plant and machinery. The firm was formed in 1992 from the merger of King and Co, founded in 1918, and JP Sturge, which can trace its corporate roots back to 1760.

The history of JP Sturge was even older than Jones Lang Wootton. In 1760, a farmer named John Player, of Stoke Gifford near Bristol began surveying for mapping. Although still relatively crude, surveying became increasingly important as the enclosure of common land progressed in the early nineteenth century. In 1772 Player was joined by his nephew Jacob Sturge forming the partnership, "Player and Sturge".

Global commercial real estate firm Jones Lang LaSalle (NYSE: JLL) today announced it will merge with international property consultancy King Sturge. The combined firm will be the clear leader in the UK and also in continental Europe, with greatly enhanced strength and depth of service capabilities across the region.

The transaction is expected to close on 31 May 2011. Under its terms, Jones Lang LaSalle will pay consideration of 197 million pounds Sterling ($319 million) to the partners of King Sturge, with 98 million pounds Sterling in cash at closing and the balance paid out in cash over five years. All 43 King Sturge offices and businesses across Europe, including 24 in the UK, will become part of Jones Lang LaSalle and will operate under the Jones Lang LaSalle brand.

The deal was announced by Christian Ulbrich, then JLL's EMEA CEO, who would later become the company's global leader. "The obvious strategic and cultural fit between Jones Lang LaSalle and King Sturge makes this a logical and very attractive proposition for both firms. It gives us a scale and depth of expertise that will make our client service delivery capabilities second to none in both the UK and continental Europe."

JLL merged with UK-based King Sturge in a £197 million deal in 2011. The combined business, with 2,700 employees and 43 offices, created the largest property agent in the UK, as reported by The Telegraph in 2011.

"(The merger) enhances JLL's presence in London, other parts of the UK, and Central and Eastern Europe. It also helps balance the company's business line weightings a bit, as King Sturge has a large capital markets business, while JLL is weighted heavily toward leasing."

The King Sturge deal was strategically important beyond raw market share. It signaled JLL's commitment to its European heritage while also addressing a weakness in its service mix. And it demonstrated that the company could execute major acquisitions even in challenging economic conditions—the aftermath of the 2008 financial crisis was still being felt in commercial real estate markets.

VIII. The Roll-Up Machine: 80 Acquisitions & Global Expansion (2000–2016)

Between 1999 and 2016, JLL transformed itself from a newly merged company into a global acquisition machine. JLL had acquired 80 companies and established 100 offices worldwide by 2016.

The acquisitions weren't random. They followed a clear strategic logic: expand geographic coverage, deepen service capabilities, and build scale in the investment management business.

JLL has made 42 acquisitions across sectors such as Property Management Tech, Facility Management Tech, Investment Tech and others.

JLL has made acquisitions in 7 countries with the most activity in United States and Finland.

The company's investment management arm, LaSalle Investment Management, grew in parallel with the services business. LaSalle Investment Management, a subsidiary of JLL, managed $58 billion in real estate investments for institutional and retail clients, as of 2016.

The company acquired Irish-based Guardian Property Asset Management in 2015.

The strategy delivered results. By 2015, JLL had achieved a milestone that validated the merger strategy and acquisition playbook. In 2014, the organization shortened its name to JLL for marketing purposes, while the legal name remained Jones Lang LaSalle Incorporated.

The rebranding reflected a company that had outgrown its merger origins. "Jones Lang LaSalle" was cumbersome—a clear artifact of the 1999 combination. "JLL" was modern, global, and easier to deploy across digital platforms. The three-letter abbreviation worked equally well in Chicago, London, Sydney, and Shanghai.

The acquisition strategy created a self-reinforcing cycle. Larger scale meant more resources for technology investment, more comprehensive service offerings, and a stronger brand. These advantages made it easier to win mandates from major corporate clients, which generated cash flow to fund additional acquisitions.

But scale also brought challenges. Each acquisition required integration—melding different corporate cultures, rationalizing overlapping service lines, and harmonizing compensation structures. Not every deal worked as planned. Some acquisitions brought talent that couldn't adapt to JLL's culture; others brought client relationships that proved less durable than expected.

IX. Key Inflection Point #3: The HFF Acquisition & Capital Markets Transformation (2019)

By the late 2010s, JLL had a gap in its service portfolio: capital markets. While the company had steadily built its investment sales and debt advisory capabilities, it lagged behind CBRE in this lucrative, high-margin business.

Enter HFF.

In 2007, HFF became a public company via an initial public offering that raised $257 million. In 2012, founders Holliday and Fenoglio went to work for CBRE. In July 2019, JLL acquired the company for $1.8 billion.

JLL and HFF announced that they have entered into a definitive agreement under which JLL will acquire all the outstanding shares of HFF in a cash and stock transaction with an equity value of approximately $2 billion.

HFF, regarded as one of the premier capital markets advisors in the industry, had more than $650 million in revenue in 2018 and approximately 1,050 employees with long-term client relationships, first-class skills and deep knowledge of U.S. as well as global markets. JLL's acquisition of this exceptional firm aligns with one of the key priorities of JLL's Beyond strategic vision, which is to grow its Capital Markets business. The combination of JLL and HFF enables greatly enhanced capital markets services and significantly expanded client reach. Clients will benefit from a global team of more than 3,700 capital markets professionals across 47 countries.

CHICAGO, July 1, 2019 – Jones Lang LaSalle Incorporated (NYSE: JLL) announced today that it closed its acquisition of HFF, greatly expanding JLL's ability to provide world-class capital markets services and expertise to its clients.

Chicago-based JLL has closed its acquisition of HFF, Inc. With the deal complete, Mark Gibson, former CEO of HFF, joins JLL as CEO, capital markets, Americas and co-chair of its global capital markets board. The purchase price for the acquisition was approximately $1.8 billion, consisting of a combination of cash and JLL stock. JLL funded the cash portion of the purchase price consideration with a combination of cash reserves and its existing syndicated credit facility. The combination is expected to deliver significant run-rate synergies, estimated at approximately $60 million over two to three years.

JLL's 2019 acquisition of HFF created a cohesive office investment sales team in Houston that handled by far the largest share of the market's transactions. So there is no question that JLL's acquisition of HFF put it in the position it is in now.

The HFF deal was the largest acquisition in JLL's history, and it fundamentally changed the company's competitive positioning. Capital markets—investment sales and debt placement—is a high-margin business that generates substantial revenue during active transaction periods. By acquiring HFF, JLL significantly closed the gap with CBRE while also gaining access to HFF's talented professionals and deep client relationships.

"We are delighted to bring together JLL and HFF to create one of the most strategic, connected and creative capital advisors in the world," said Christian Ulbrich, Global CEO of JLL. "By combining the impressive capabilities, talent and expertise that distinguish both organizations, we will deliver exciting new growth opportunities and ensure we are best positioned to achieve ambitions for our clients and all our stakeholders."

The integration proved smoother than many industry observers expected. Good communication and collaboration were values instilled in the cultures of both JLL and HFF, starting at the top, which helped the teams jell. The team says there is no jealousy.

X. The Technology Pivot: JLL Spark & PropTech (2017–Present)

Christian Ulbrich has been clear about his vision for JLL's future: the company must become "a technology company servicing the real estate sector." This is also a time of transformational opportunity for commercial real estate, with AI and gen AI tools reshaping operations and commitment to sustainability propelling deep changes to how the industry thinks about building and retrofitting.

The technology pivot began in earnest in 2017. The company expanded from commercial real estate services to include property technology, or "proptech", with the 2017 launch of its JLL Spark division. In June 2018, JLL Spark created a $100 million venture fund to invest in real estate start-ups, such as a technology to link office users with co-working spaces.

JLL Spark represented a new approach to innovation. Rather than building all technology in-house, JLL would identify and invest in the most promising proptech startups, gaining early access to new technologies while also potentially earning returns on its investments.

In late 2021 and early 2022, JLL made two "proptech" acquisitions. In November 2021, it purchased the property management software company Building Engines, and in February 2022 it acquired Hank, a company developing AI-based technology to improve the energy efficiency of buildings.

But the most striking technology bet has been in artificial intelligence. The company developed a large language model (LLM) tool called JLL GPT for its employees, and launched it in August 2023. It was the first such model to be launched by a major real estate services company. The generative AI model is being trained on JLL's data as of 2023 and was developed to be able to answer questions about commercial real estate.

JLL GPT represents a significant competitive advantage if it works as intended. By training a large language model on JLL's proprietary data—decades of transaction information, property valuations, market research, and client interactions—the company could create an AI tool that's genuinely differentiated from generic chatbots.

In June 2023, JLL launched Carbon Pathfinder, a software tool it had developed for companies to identify the carbon emissions from their buildings and ways to reduce those emissions.

In 2024, the company announced a partnership with IBM, using IBM's technology to develop a platform that tracks sustainability data for JLL's clients' commercial properties.

The sustainability focus is strategically important. As corporations face increasing pressure to reduce their carbon footprints, their real estate portfolios are obvious targets. Buildings account for approximately 40% of global energy consumption and roughly one-third of greenhouse gas emissions. A company that can help clients optimize their buildings' environmental performance has a compelling value proposition.

Christian Ulbrich outlined JLL's priorities: "The three most important ambitions we had for this year were to accelerate our top- and bottom-line growth, to make tremendous progress on our AI initiatives, and to further develop our shared-service-center platform. Of course, we have had to adapt to the current geopolitical and economic situation. So not all of our ambitions will progress exactly as we planned. In fact, due to uncertainty, in 2025 we are likely to have more market share than we originally planned to have this year."

XI. Recent Strategic Moves (2020–2025)

Christian Ulbrich (born 1966) is a German business executive who is the president and chief executive officer of real estate services company JLL. After graduating from the University of Hamburg, Ulbrich initially worked in finance roles at MeesPierson and Rabobank Nederland. In 1996, he was named the CEO of Bank Companie Nord, following which he was hired by Warburg Bank to lead its real estate group HIH. He was hired by real estate services company JLL to manage its German operations in 2005. In 2016, JLL named him as its global president and the company's global CEO. According to the German business publication Immobilien Zeitung, he was the first German in global leadership of one of the major real estate companies.

Former company president Christian Ulbrich succeeded Colin Dyer as CEO in October 2016. Sheila Penrose served as board chairwoman starting in 2005, and was replaced by Siddharth ("Bobby") Mehta in 2020. In 2022, JLL founded the JLL Foundation, a non-profit organization focused on climate change and sustainability.

Under Ulbrich's leadership, JLL has continued to execute strategic acquisitions while investing heavily in technology. The firm acquired data center services company SKAE Power Solutions in May 2024, forming a technical services division called SKAE, a JLL company. They also acquired Raise Commercial Real Estate, a firm that had developed a technology platform for companies to manage their real estate holdings.

CHICAGO, May 15, 2024 – As data center demand continues to surge, JLL (NYSE: JLL) today announced it has reached an agreement to acquire SKAE Power Solutions (SKAE), a New York-based provider of data center technical and project management services. This acquisition of SKAE enables JLL to provide solutions across the full data center lifecycle and adds significant technical depth to its existing offerings.

The data center focus is particularly timely. The explosion of AI applications has created insatiable demand for data center capacity. Companies that can help clients site, design, build, and manage data centers are positioned to benefit from one of the most powerful secular trends in commercial real estate.

JLL's most recent acquisition was Javelin Capital, a New York City-based capital raising and M&A advisory firm focused on renewable energy, acquired on March 24, 2025.

The Javelin Capital acquisition signals JLL's interest in the energy transition. As the world decarbonizes, vast sums of capital will flow into renewable energy infrastructure. JLL, through Javelin, can now advise on those transactions—another example of the company's strategy to position itself at the intersection of real estate, technology, and sustainability.

XII. Business Model Deep Dive

Jones Lang LaSalle Incorporated (JLL) is a global real estate services and investment management company with offices in 32 countries spread across five continents. JLL assists institutions, corporations, and wealthy investors in buying, selling, and managing real estate assets. Services provided by the company include investment banking, real estate finance, and corporate finance, as well as property development, property management, project management, and tenant representation. The company has more than $23 billion of public and private assets under management.

JLL's business model encompasses several interconnected revenue streams:

Markets Advisory: This segment includes leasing services—helping tenants find space and landlords find tenants—as well as capital markets services (investment sales and debt advisory). This is the most transactional, cyclical part of the business.

Work Dynamics: This segment includes property management, facilities management, and project management services. These are typically longer-term contracts with more predictable revenue streams—what JLL calls its "resilient" revenues.

JLL Technologies: This segment develops and sells technology solutions for real estate management, including the Building Engines property management software and various data analytics tools.

LaSalle Investment Management: This is the investment management arm, managing real estate funds and separate accounts for institutional investors. Revenue comes from management fees (typically based on assets under management) and performance fees (based on investment returns).

Transactional revenue growth again surpassed 20% and complemented Resilient business line revenues which delivered the fifth consecutive quarter of double-digit growth.

The distinction between "transactional" and "resilient" revenues is fundamental to understanding JLL's business model. Transactional revenues—primarily leasing and capital markets—swing dramatically with market conditions. When interest rates rise and transaction volumes decline (as happened in 2022-2023), these revenues can fall sharply. Resilient revenues—primarily property and facilities management—provide a steadier baseline.

Jones Lang LaSalle Full Year 2024 Results Key Financial Results: Revenue US$23.4b (up 13% from FY 2023). Revenue exceeded analyst estimates by 1.2%.

Adjusted EBITDA: Increased by 20% in Q4 2024; 28% growth for the full year. Adjusted EPS: Grew 17% in Q4 2024; 38% growth for the full year. Free Cash Flow: Significant increase, enabling reinvestment and leverage reduction.

"JLL delivered strong fourth-quarter and full-year 2024 financial results, led by an acceleration in transactional activity and sustained growth in resilient revenues. Throughout 2024, our focus on operating efficiency helped drive significant margin expansion and free cash flow generation," said Christian Ulbrich, JLL CEO.

XIII. Competitive Landscape & Porter's Five Forces Analysis

Competitive Rivalry (HIGH)

The commercial real estate market is highly competitive. Here are some of the key competitors challenging CBRE in 2024: JLL is a leading professional services firm that specializes in real estate and investment management. Like CBRE, JLL operates globally and offers a wide range of services. JLL's strong focus on technology and sustainability initiatives gives it a competitive edge. The company's robust research and data analytics capabilities are also noteworthy.

CBRE ($45.7B) has a higher market cap than JLL ($14.3B). JLL has less debt than CBRE: JLL (4.11B) vs CBRE (9.54B). CBRE has higher revenues than JLL: CBRE (38.1B) vs JLL (24.7B).

Cushman & Wakefield is another major player in the commercial real estate market, offering services similar to CBRE, including leasing, capital markets, and property management. Cushman & Wakefield's extensive local market knowledge and strong client relationships are key differentiators. The company is also focused on expanding its technological capabilities.

The "Big Four" of commercial real estate services—CBRE, JLL, Cushman & Wakefield, and Colliers—compete fiercely for major corporate clients. The industry has consolidated significantly over the past two decades, but competitive intensity remains high because:

-

Services are often commoditized: A lease transaction is a lease transaction. Differentiation comes from execution quality, relationships, and market knowledge—but these are hard to sustain over time.

-

Talent is mobile: Top-performing brokers can (and do) switch firms, taking client relationships with them.

-

Clients multi-source: Most large corporations maintain relationships with multiple service providers to ensure competitive pricing and avoid over-dependence on any single firm.

Threat of New Entrants (MODERATE)

The capital requirements to compete in commercial real estate services are not prohibitive—it's fundamentally a people business. However, the barriers to competing at JLL's scale are substantial:

- Network effects: A global client like ExxonMobil wants a provider with offices in every market where it operates. Building that network organically would take decades and billions of dollars.

- Technology investments: The upfront costs of building platforms like JLL GPT create advantages for incumbents.

- Brand and relationships: Decades of client relationships and a trusted brand cannot be replicated quickly.

The more realistic threat comes from adjacent industries—technology companies that could potentially disintermediate traditional brokerage, or private equity firms rolling up smaller brokerages to create new scaled competitors.

Bargaining Power of Buyers (MODERATE TO HIGH)

Large corporate clients have significant bargaining power. They can credibly threaten to switch providers, they have sophisticated procurement functions that negotiate aggressively on fees, and they can unbundle services to play providers against each other.

However, the shift toward integrated service delivery has increased switching costs. A client using JLL for leasing, property management, project management, and investment advisory would face significant disruption if it switched all of those services to a competitor.

Bargaining Power of Suppliers (LOW TO MODERATE)

JLL's primary "suppliers" are its employees—particularly the talented brokers and advisors who generate revenue. These individuals have meaningful bargaining power because their relationships with clients are portable. Retention of top performers is a constant challenge.

Threat of Substitutes (EMERGING)

The most interesting competitive dynamic is the potential for technology to substitute for traditional services:

- PropTech platforms: Could automated platforms eventually handle routine leasing transactions without human brokers?

- Data analytics: Could clients build their own analytical capabilities rather than relying on JLL's research?

- AI: Could generative AI tools handle some of the advisory work currently performed by human analysts?

JLL is betting that by leading the technology transformation itself, it can capture these opportunities rather than being disrupted by them. The JLL GPT initiative and the JLL Spark investments reflect this strategic intent.

XIV. Hamilton's Seven Powers Framework

Applying Hamilton Helmer's Seven Powers framework to JLL reveals a mixed competitive picture:

Scale Economies: JLL benefits from scale in technology investments (platforms built once can be deployed globally) and brand (marketing costs amortized across a larger revenue base). However, scale economies in brokerage are limited—a local broker can match a global firm on any individual transaction.

Network Effects: Weak to moderate. JLL's global network creates value for multinational clients, but there are no strong two-sided network effects of the type that create winner-take-all dynamics.

Switching Costs: Moderate and increasing. As clients integrate JLL's technology platforms and deepen their service relationships, switching becomes more costly and disruptive.

Branding: Strong within the industry but limited compared to consumer brands. JLL is highly regarded among sophisticated corporate real estate buyers but not well-known to the general public.

Cornered Resource: JLL's talent pool, proprietary data, and technology capabilities represent potential cornered resources, but none are truly defensible moats. Talent can be recruited away; data can be replicated over time.

Counter-Positioning: JLL's integrated service model and technology investments represent a form of counter-positioning against smaller, specialized competitors who cannot afford similar investments. However, CBRE and Cushman & Wakefield can and do match these investments.

Process Power: JLL's acquisition integration capabilities and global operating systems represent accumulated organizational know-how that would be difficult for competitors to replicate quickly.

Net Assessment: JLL has moderate competitive advantages that support premium positioning and stable market share, but lacks the strong structural moats that would protect against determined competition or technological disruption.

XV. Bull and Bear Case

The Bull Case

"Clients continue to look to JLL for innovative real estate management solutions, industry expertise and data-driven insights. With our strong momentum amidst an improving real estate cycle, JLL's talent and differentiated platform position us well to gain market share and drive profitable growth in 2025."

-

Cyclical Recovery: After a challenging 2022-2023 period when rising interest rates crushed transaction volumes, commercial real estate activity is recovering. Office leasing reached its highest level since 2019, signaling a market rebound. As the Fed cuts rates and capital markets normalize, JLL's transactional revenues should accelerate.

-

Market Share Gains: JLL has been consistently gaining market share, particularly in leasing. JLL's Q4 revenue grew by double digits, driven by strong market share gains in leasing. The company's integrated platform and technology investments are resonating with clients.

-

Technology Differentiation: JLL's investments in AI, data analytics, and proptech could create meaningful competitive separation. If JLL GPT delivers productivity improvements for brokers and analysts, it could reduce costs while improving service quality.

-

Sustainability Tailwind: The ESG imperative is driving demand for building decarbonization services. JLL's Carbon Pathfinder tool and sustainability consulting capabilities position the company to benefit from this secular trend.

-

Data Center Opportunity: The AI boom is creating extraordinary demand for data center capacity. JLL's acquisition of SKAE Power Solutions positions the company to capture this opportunity.

-

Disciplined Capital Allocation: JLL's strong balance sheet and liquidity position, with $3.6 billion in liquidity, provide flexibility for capital allocation and investment opportunities.

The Bear Case

-

Cyclical Exposure: Despite the "resilient" revenue narrative, JLL remains highly exposed to commercial real estate cycles. A recession or renewed interest rate pressure could crush transaction volumes again.

-

Office Sector Uncertainty: The post-pandemic shift to hybrid work has permanently reduced office demand in many markets. Despite improvements, the office sector's transaction volumes remain below pre-pandemic levels, indicating a slow recovery in this area. JLL's substantial exposure to office leasing and investment sales could be a drag on performance.

-

Competitive Intensity: CBRE remains significantly larger and more profitable. CBRE has higher annual earnings (EBITDA): 2.19B vs. JLL (1.24B). Scale advantages in technology investment and brand building could widen over time.

-

Technology Risk: JLL's technology investments have not yet proven their ROI. There is a noted decline in JLL Technologies' segment revenue due to lower Technology Solutions bookings, impacting overall segment performance. The company is spending heavily on AI and proptech, but the payoff remains uncertain.

-

Talent Retention: The commercial real estate services business remains fundamentally a people business. Top brokers can and do switch firms, taking client relationships with them. Retention is an ongoing challenge.

-

Geopolitical and Macroeconomic Risk: The company faces potential headwinds from geopolitical developments that may impact decision-making and market conditions. Trade tensions, political instability, and macroeconomic uncertainty could delay corporate real estate decisions.

-

LaSalle Investment Management Challenges: Revenue in the LaSalle segment decreased due to valuation declines and lower fees in Europe, impacting overall performance. Real estate valuations remain under pressure in certain markets, affecting AUM-based fees.

XVI. Key Performance Indicators to Watch

For investors following JLL, three metrics stand above the rest:

1. Leasing Revenue Growth vs. Market Volume This metric reveals whether JLL is gaining or losing market share in its core brokerage business. If JLL's leasing revenue is growing faster than overall market transaction volumes, the company is taking share from competitors—a sign that its platform and talent are resonating with clients. Conversely, underperformance relative to market volumes suggests competitive weakness.

2. Adjusted EBITDA Margin As we continue to invest to both capture future growth opportunities and drive operating leverage, we are targeting a full year 2025 adjusted EBITDA range of $1.25 billion to $1.45 billion reflective of 14% growth at the midpoint.

The adjusted EBITDA margin measures JLL's ability to convert revenue into profit while investing for growth. Margin expansion indicates operating leverage—the company is growing revenue faster than costs. Margin compression could indicate either competitive pressure (forcing lower fees) or excessive investment spending without corresponding revenue growth.

3. Work Dynamics Revenue Growth Rate This metric tracks the health of JLL's most predictable revenue streams—property management, facilities management, and project management. Consistent double-digit growth here indicates that clients are expanding their relationships with JLL and that the company's integrated service model is working. Slowing growth could indicate client churn or market saturation.

XVII. Regulatory and Risk Considerations

Regulatory Environment: Commercial real estate services face relatively light regulatory oversight compared to financial services. The primary regulatory considerations are real estate licensing requirements (which vary by jurisdiction), anti-money laundering compliance (particularly for cross-border transactions), and employment law (given JLL's 112,000-person global workforce).

Legal Overhang: JLL is dealing with a portfolio of loans to a single borrower currently in default with confirmed borrower fraud, requiring discussions with Fannie Mae for resolution. This situation represents a potential liability that investors should monitor, though the company is working toward resolution.

Accounting Considerations: JLL uses non-GAAP metrics (particularly adjusted EBITDA and adjusted EPS) that exclude certain items. Management uses certain non-GAAP financial measures to develop budgets and forecasts, measure and reward performance against those budgets and forecasts, and enhance comparability to prior periods. These measures are believed to be useful to investors and other external stakeholders as supplemental measures of core operating performance. Investors should understand the reconciliations between GAAP and non-GAAP results and assess whether excluded items are truly non-recurring.

XVIII. The Road Ahead

"Our company goes back to 1783, when it was founded in London. When times are particularly challenging, I will say to our people, 'Think about all the events that have happened since 1783. There were good times, and there were bad times, but from each crisis, JLL came out stronger.'"

Christian Ulbrich's invocation of JLL's 240-year history isn't merely corporate mythology—it reflects a genuine competitive advantage. A company that has survived world wars, financial panics, technological revolutions, and geopolitical upheavals has institutional resilience that newer competitors cannot easily replicate.

The JLL story is, in many ways, the story of the professionalization and globalization of commercial real estate services. What began as local auctioneers and surveyors serving their immediate markets has evolved into integrated global platforms serving multinational corporations across every continent.

The company's next chapter will be written by the AI revolution and the sustainability imperative. JLL's investments in JLL GPT, Carbon Pathfinder, and proptech startups represent bets on the future—bets that the company can transform itself from a real estate services firm that uses technology into, as Ulbrich puts it, "a technology company servicing the real estate sector."

Whether that transformation succeeds will determine JLL's competitive position for the next decade. The opportunities are substantial: corporations need help navigating hybrid work, decarbonizing their buildings, and optimizing their real estate portfolios with data and AI. JLL is positioned to provide those services.

But the risks are equally real. Technology investments consume capital and management attention without guaranteed returns. Smaller, more agile proptech startups could potentially disintermediate traditional service providers. And CBRE's scale advantage means that any technology breakthrough JLL achieves can likely be replicated by its larger rival.

For investors, JLL represents a way to gain exposure to commercial real estate activity without owning property directly—and with the operating leverage that comes from a services business model. The company's financial performance will track the health of commercial real estate markets globally, with amplification both on the upside and the downside.

The 240-year journey from Georgian-era auctioneer to AI-enabled global platform is remarkable. The next 240 years—or at least the next decade—will depend on whether JLL can execute on its technology vision while maintaining the client relationships and professional culture that have defined it since Richard Winstanley hung his shingle on Paternoster Row.

Note: This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The commercial real estate services industry is cyclical and subject to macroeconomic factors that can significantly impact company performance.

XIX. LaSalle Investment Management: The Investment Engine

LaSalle Investment Management represents one of JLL's most strategically important but often overlooked business segments. Operating as an independent subsidiary, LaSalle manages institutional capital in real estate investments across the globe—a fundamentally different business model from JLL's fee-for-service advisory work.

LaSalle Investment Management is a leading global real estate investment management firm and an operationally independent subsidiary of Jones Lang LaSalle Incorporated (JLL), specializing in private and public real estate equity and debt investments across major sectors including office, retail, residential, industrial, and emerging areas such as data centers and life sciences. As of June 30, 2025, the firm manages $88.5 billion in assets on behalf of institutional investors worldwide.

This figure represents substantial growth from earlier periods. At this time (2018), LaSalle was managing approximately $58 billion of assets globally. The growth trajectory reflects both market appreciation and successful fundraising efforts.

LaSalle Investment Management is a real estate investment management firm that operates as an independent subsidiary of JLL. The firm invests in real estate for institutional investors such as pension funds, endowments, and sovereign wealth funds. It is headquartered in Chicago, Illinois and has 24 offices across North America, Europe, and Asia.

LaSalle Investment Management operates offices in 23 cities across 13 countries on four continents, enabling localized expertise in real estate investment markets worldwide.

The business has diversified significantly from its origins. Since its inception, LaSalle has expanded from traditional commercial property development into specialized sectors including life sciences, data centers, self-storage, and student housing. The firm has also expanded its debt investment operations.

LaSalle has raised over US$2.2 billion of equity for LaSalle Asia Opportunity VI, including sidecars and co-investment programmes, exceeding its initial target of US$1.5 billion. The committed capital has been secured from global institutional investors and will provide buying power for over US$7 billion worth of assets.

The investment management business contributes to JLL's revenue through management fees (typically based on assets under management) and incentive fees (based on investment performance). This creates a different financial profile than the services business: more stable recurring revenue from management fees, but with meaningful upside when markets perform well and incentive fees are earned.

XX. 2025 Performance Update: Momentum Continues

JLL achieved sixth consecutive quarter of double-digit revenue growth and delivered a 45% increase in diluted earnings per share. On November 5, 2025, Jones Lang LaSalle Incorporated reported operating performance for the third quarter of 2025 with diluted earnings per share of $4.61 (up 45%) and adjusted diluted earnings per share of $4.50 (up 29%).

Transactional revenues returned to double-digit growth this quarter and Resilient revenues extended its growth streak with top-line increases every quarter stretching back to the reorganization of the company's segments in Q1 2022. Third-quarter revenue was $6.5 billion, up 10% in local currency with Resilient revenues up 9% and Transactional revenues up 13%.

Year-to-date results were equally impressive, with revenue up 11% to $18.51 billion and adjusted EBITDA increasing 18% to $864 million through the first nine months of 2025.

The Capital Markets segment demonstrated particular strength. Capital Markets Services demonstrated the strongest growth among all segments, with revenue increasing by 23% in local currency to $612 million and adjusted EBITDA surging 36% to $90 million. This growth was primarily led by debt advisory, investment sales, and equity advisory businesses.

Office Leasing revenue growth outperformed global office volumes (up 14% compared with market volumes up 2% according to JLL Research), highlighted by U.S. outperformance (revenue up 14% compared with market volumes up 4% according to JLL Research).

Geographically, revenue growth was led by the U.S., augmented by strong contributions from Japan and Australia. Globally, investment sales revenues were up 22%, significantly outpacing the broader investment sales market, which grew 12% over the same period according to JLL Research.

The company reported record year-to-date operating cash flow of $182.3 million, and significantly improved its financial structure, driving the Net Leverage Ratio down to a healthy 0.8x. Net Leverage dropped substantially from 1.4x to 0.8x over the trailing twelve months, with Net Debt decreasing roughly 31% from $1.6 billion to $1.1 billion.

JLL continued its share repurchase program, buying back $70 million worth of shares in Q3 2025. The company has approximately $880 million remaining on its share repurchase authorization and has repurchased $1.3 billion of shares since the beginning of 2020 at an average price of $201 per share.

The company maintained its 2025 adjusted EBITDA target of between $1,375 million and $1,450 million.

Jones Lang LaSalle has revised its full-year adjusted EBITDA guidance upward to between $1.3 billion and $1.45 billion. This reflects management's confidence in the company's trajectory and represents meaningful growth from prior year levels.

XXI. Competitive Dynamics: The CBRE Shadow

Any analysis of JLL must grapple with the elephant in the room: CBRE Group, the industry's undisputed leader.

CBRE ($45.7B) has a higher market cap than JLL ($14.3B). CBRE has higher annual earnings (EBITDA): 2.19B vs. JLL (1.24B). CBRE has more cash in the bank: 1.4B vs. JLL (401M). JLL has less debt than CBRE: JLL (4.11B) vs CBRE (9.54B). CBRE has higher revenues than JLL: CBRE (38.1B) vs JLL (24.7B).

The scale differential is substantial. CBRE's revenue is roughly 50% larger than JLL's, and its market capitalization is more than three times JLL's. This gap has persisted for years and reflects CBRE's larger footprint, broader service mix, and stronger capital markets position (though the HFF acquisition narrowed this advantage).

Jones Lang LaSalle Inc., headquartered in Chicago, offers commercial real estate and investment management services. The company's diverse range of products and service offerings, along with its strategic investments, gives it a strong footing. Also, its superior client services and strategic investment in technology and innovation are expected to boost market share and win relationships.

Several firms consistently rank among the top commercial real estate companies worldwide. CBRE, JLL, and Cushman & Wakefield are recognized for their substantial influence and market share. They lead in various sectors, including leasing, sales, and property management.

Baron Real Estate Fund stated the following regarding Jones Lang LaSalle Incorporated in its third quarter 2025 investor letter: "Leading commercial real estate service company Jones Lang LaSalle Incorporated contributed positively to performance during the third quarter, aided by the company's strong second quarter financial report, coupled with broad-based strength across its business. We expect JLL to continue benefiting from structural and secular tailwinds: the outsourcing of commercial real estate, the institutionalization of commercial real estate, and opportunities to increase market share in a highly fragmented market. Looking forward, we continue to believe we are in the early days of a rebound in commercial real estate sales and leasing activity."

XXII. Market Outlook and Industry Dynamics

The recently enacted tax-and-spending bill maintains favorable tax treatment for real estate, which provides confidence in forecasts for commercial real estate fundamentals and deal activity throughout the second half of 2025. Commercial real estate investment activity is expected to grow by 10% this year to $437 billion, 18% below the pre-pandemic (2015-2019) annual average. Although the 10-year Treasury yield has remained somewhat elevated and volatile, it has not derailed a recovery in investment activity.

Lower economic growth and higher inflation than anticipated at the start of the year are expected due to lingering uncertainty over U.S. trade policy. However, more clarity on tariffs later this year should lessen this headwind to investment activity. With continued growth and healthy fundamentals, investors can realize the best returns of the cycle by acquiring assets in coming quarters, as is historically the case just after a peak in cap rates. Savvy investors will find strategic opportunities amid reset pricing.

The global commercial real estate market size was valued at USD 6.72 trillion in 2024 and is expected to reach USD 9.11 trillion by 2033 from USD 6.95 trillion in 2025. The market is projected to grow at a CAGR of 3.44%.

Economic activity, employment growth, office-based employment, interest-rate levels, costs and availability of credit, tax and regulatory policies, and the geopolitical environment are the major factors shaping the real estate market's fate. The industry's performance is anticipated to continue to be greatly influenced by geopolitical instability and macroeconomic uncertainties. Conflicts occurring in various nations have impacted the global economic landscape. These situations have escalated supply-chain disruption, increased inflation and influenced U.S. policies to change. Change in governmental policies within the United States heightened the degree of uncertainty and emerged 2025 as a year of considerable disruption.

XXIII. Organizational Evolution

The presentation also highlighted upcoming changes to the company's reporting structure. Effective July 1, 2025, JLL isolated the activity related to the Proptech Investments portfolio from the Software and Technology Solution segment. Additionally, effective January 1, 2026, Software and Technology Solutions will operate as a fifth business line within the Real Estate Management Services segment.

In September 2024, JLL announced an organizational change that will bring together all building operation groups to address client needs and the changing dynamics of the real estate industry. As a result of these changes, effective January 1, 2025, the company reports its Property Management business (currently included in Markets Advisory) within its Work Dynamics segment. Also effective January 1, 2025, this segment was renamed Real Estate Management Services, and the Markets Advisory segment became Leasing Advisory.

These reorganizations reflect JLL's continuous effort to optimize its structure for client delivery and operational efficiency. The integration of building operations groups signals an increased focus on the "resilient" revenue streams that provide stability during market downturns.

XXIV. Capital Allocation Philosophy

JLL's capital allocation strategy balances growth investments with shareholder returns.

JLL is focused on maintaining balance sheet strength and adequate liquidity to enjoy operational flexibility. The company exited the first quarter of 2025 with $3.31 billion of corporate liquidity and a net leverage of 1.4X. As of March 31, 2025, it enjoyed investment-grade ratings of Baa1 from Moody's and BBB+ from S&P Global, which highlight financial and balance sheet strength, enabling the company to borrow at a favorable rate.

JLL plans to increase share repurchases in the upcoming quarters, focusing on organic growth over mergers and acquisitions.

CEO Christian Ulbrich highlighted the company's strategic investments, stating, "Our investments in data technology and artificial intelligence are integral to our growth strategy." CFO Kelly Howe emphasized financial discipline, noting, "We continue to manage to a full year average leverage ratio of around one point zero times."

The shift toward organic growth and share repurchases represents a maturation of JLL's strategy. After decades of acquisition-driven expansion, the company appears to be emphasizing integration and optimization over further M&A activity.

XXV. Investment Considerations and Conclusion

The JLL story offers several lessons for business analysts and investors.

The Power of Long-Term Compounding: From Richard Winstanley's 1783 auction house to a $25 billion global enterprise, JLL demonstrates how businesses can compound value over centuries through consistent reinvestment, strategic evolution, and measured risk-taking.

Platform Strategy: JLL's success illustrates the power of building integrated platforms. By offering clients a comprehensive suite of services—leasing, property management, project management, investment advisory, capital markets—the company creates switching costs and deepens relationships. Each additional service creates touchpoints that strengthen the overall relationship.

The Roll-Up Playbook: JLL's acquisition strategy shows how roll-ups can create lasting value when executed thoughtfully. The key ingredients: cultural fit (Staubach), geographic rationalization (King Sturge), and capability building (HFF). Not every acquisition worked perfectly, but the overall strategy created a company far more valuable than the sum of its parts.

Technology as Differentiator: The investments in JLL Spark, JLL GPT, and proptech acquisitions represent a bet that technology will increasingly differentiate winners from losers in commercial real estate services. Whether this bet pays off remains to be seen, but the strategic intent is clear.

Cyclical Business, Secular Trends: JLL's business is inherently tied to commercial real estate cycles, which creates volatility that some investors find uncomfortable. However, secular trends—the institutionalization of real estate, the outsourcing of corporate real estate functions, and the sustainability imperative—provide long-term tailwinds.

JLL's return on equity is 10.37% compared with the industry average of 1.94%. This highlights that the company reinvests more efficiently compared with the industry. With a solid balance sheet and financial flexibility, JLL is well-poised to sail through any challenging times and capitalize on solid opportunities.

For 240 years, the businesses that became JLL navigated wars, depressions, technological revolutions, and countless economic cycles. The company's endurance suggests institutional resilience that transcends any individual leader or strategy. As Christian Ulbrich noted, the company has consistently emerged from crises stronger than before.

The next chapter in JLL's story will be written by the intersection of artificial intelligence, sustainability, and evolving workplace practices. Whether the company can successfully navigate these transformations while maintaining its competitive position against CBRE and other rivals will determine whether the next 240 years are as successful as the last.

What remains constant is the fundamental value proposition: helping clients make better decisions about the built environment. From Richard Winstanley auctioning properties in Georgian London to JLL GPT analyzing market trends with artificial intelligence, the core service has remained remarkably consistent—even as the tools and scale have transformed beyond recognition.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube