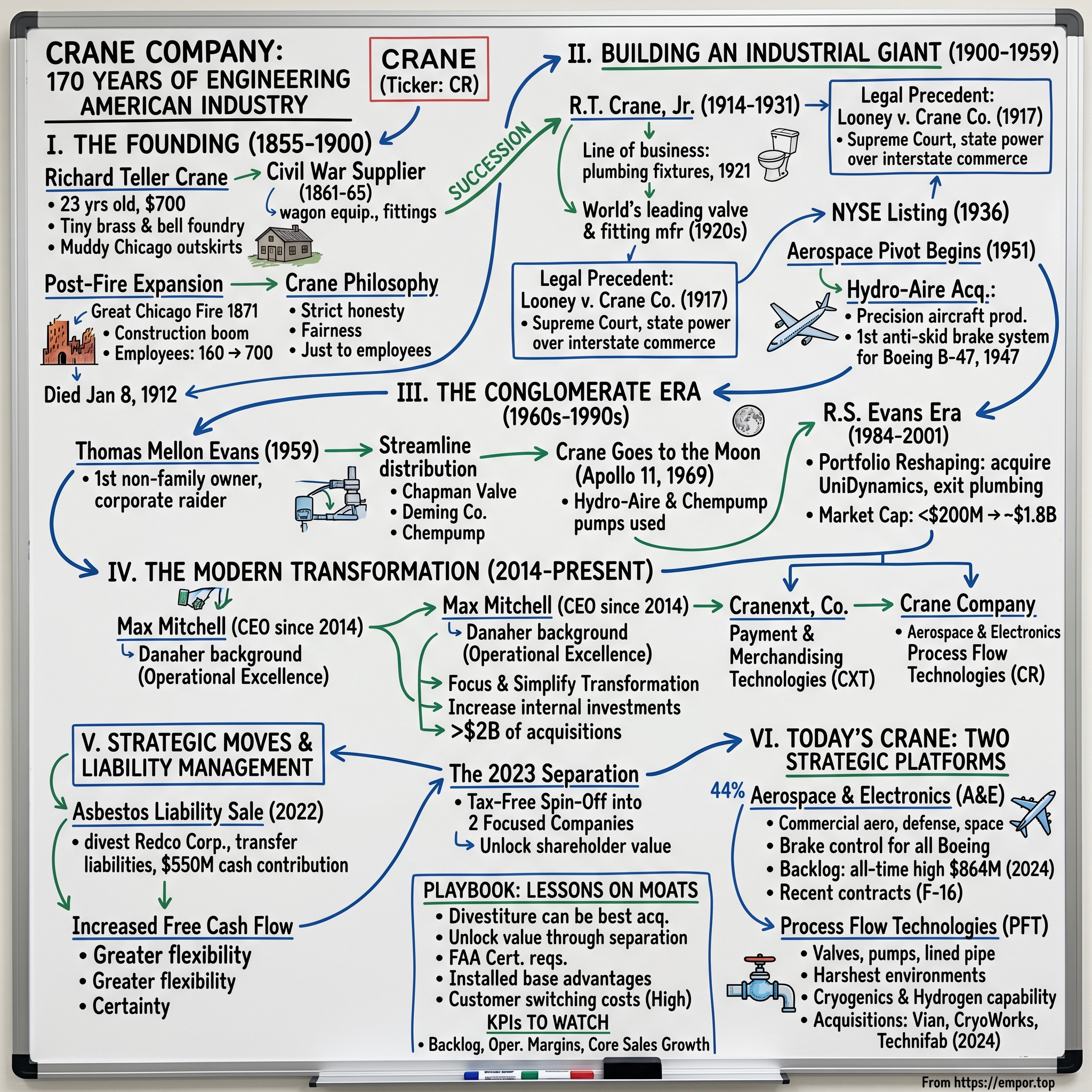

Crane Company: 170 Years of Engineering American Industry

I. Introduction: From Brass Foundry to Boeing's Brakes

On a crisp July 4th morning in 1855, a 23-year-old with just two or three years of formal schooling opened a tiny brass and bell foundry on the muddy outskirts of Chicago. Richard Teller Crane had arrived in the city less than a year earlier, escaping the Panic of 1854 that had cost him his machinist job back East. With $700 in savings—money earned working in foundries since childhood—he started what would become one of America's most enduring industrial enterprises.

Nearly 170 years later, that foundry's successor, Crane Company (NYSE: CR), operates at the intersection of two critical global industries: aerospace and process flow technologies. The company delivered 8% core sales growth with 28% adjusted EPS growth in 2024, capping off a remarkable corporate transformation that saw it shed legacy liabilities, separate into two focused public companies, and position itself squarely for the aerospace and defense renaissance.

The hook for Crane's story lies in an improbable through-line: Crane invented the first anti skid brake control system in 1947 and, since then, has supplied the brake control systems for all Boeing commercial aircraft. That means every time a 737 or 787 touches down safely at an airport anywhere in the world, Crane technology is doing the work. Crane pumps were on the moon—Hydro-Aire and Chempump pumps were used in the Gemini and Apollo Space programs.

How does a company that started making brass fittings in 1855 end up putting brake systems on every Boeing aircraft and pumps on the Apollo moon missions? The answer lies in a uniquely American story of adaptation, acquisition, and the relentless pursuit of mission-critical niches.

Crane Company has delivered innovation and technology-led solutions for customers since its founding in 1855. Today, Crane is a leading manufacturer of highly engineered components for challenging, mission-critical applications focused on the aerospace, defense, space and process industries.

Crane has approximately 7,500 employees in the Americas, Europe, the Middle East, Asia and Australia. Crane Company is traded on the New York Stock Exchange (NYSE: CR).

This article will trace Crane's journey from the Civil War era through its 20th-century conglomeration, its aerospace pivot, and the dramatic "focus and simplify" transformation of the 2020s that created the streamlined company investors see today.

II. The Founding: Richard Teller Crane's American Dream (1855–1900)

A Young Man in a Frontier City

Richard T. Crane was born on May 15, 1832, in Paterson, New Jersey to Timothy Botchford Crane and Maria Ryerson. Crane was a nephew of Chicago lumber dealer Martin Ryerson. He moved to Chicago from New Jersey in 1855.

Richard's father died when he was only nine years old and he took a variety of jobs to support his family, including working in a foundry and as a machinist. In 1854, during an economic downturn, Crane found himself out of work with few prospects in the East and moved to Chicago where his uncle Martin Ryerson was a successful lumber dealer.

Crane grew up in Paterson, New Jersey. His father was a builder-architect. Richard T. only had two or three years of formal schooling before embarking on a series of factory jobs, first in Patterson, and then New York City.

This modest education would prove both a limitation and a liberation—Crane learned by doing, not by reading, and his intimate knowledge of metalworking gave him insights that university-trained engineers might have missed.

The Founding of R.T. Crane & Bro.

He moved to Chicago from New Jersey in 1855. Richard and his brother Charles soon formed R.T. Crane & Bro., which manufactured and sold brass goods and plumbing supplies. The new company soon won contracts to supply pipe and steam-heating equipment in large public buildings such as the Cook County courthouse and the state prison at Joliet.

These early government contracts were transformative. The Cook County courthouse represented validation—here was a company trusted with the plumbing infrastructure of civic institutions. The state prison at Joliet demonstrated scale. Crane wasn't just making fittings for homes; he was building the circulatory systems of America's growing institutional infrastructure.

The onset of the Civil War (1861-65), the company became a major government supplier of fittings for saddlery, brass fittings, plates, knobs, spurs, and wagon equipment. In 1866, the first catalog printed, which contained products as diverse as fire hydrants, ventilating fans, machine tools, water pumps, bung bushings for beer barrels, and steam engines.

In 1865, R. T. Crane and Brother was incorporated and the name of the company was changed to the Northwestern Manufacturing Company. It began to manufacture a full line of industrial valves and fittings in cast iron, malleable iron and brass.

Post-Fire Expansion and the Crane Philosophy

By 1870, when it employed about 160 people, it was making elevators as well. After the Chicago Fire of 1871, the company decided to expand its operations. Just after the firm became Crane Bros. Manufacturing Co. in 1872, it employed as many as 700 men and boys and manufactured over $1 million worth of products per year.

The Great Chicago Fire of 1871 destroyed much of the city's building stock, but it also created a construction boom that would last for decades. Crane was perfectly positioned. Every new building needed plumbing, heating systems, and industrial fittings. The company quintupled its workforce in just two years.

In 1890, when it had sales branches in Omaha, Kansas City, Los Angeles and Philadelphia, the company changed its name to Crane Co. By this time, Crane was supplying much of the pipe used for the large central heating systems in Chicago's new skyscrapers, and it was also selling the enameled cast-iron products that were soon found in bathrooms in residences across the country.

The Values That Built an Empire

Richard Teller Crane articulated a business philosophy that would guide the company for generations:

"I am resolved to conduct my business in the strictest honesty and fairness; to avoid all deception and trickery; to deal fairly with both customers and competitors; to be liberal and just toward employees."

Beyond business success, he was an advocate of new ways of educating children and in 1886 he was the vice president of the Chicago Manual Training School, providing one of the city's first vocational education programs.

This wasn't just rhetoric. Crane built worker housing near his factories, established profit-sharing programs before they were common, and maintained a paternalistic but genuine concern for employee welfare. The Chicago Board of Education eventually named a high school after him.

Crane was married three times, the last at age 73 to 35-year-old Emily Hutchison. Crane was a member of the famous Jekyll Island Club (aka The Millionaires Club) on Jekyll Island, Georgia.

By the turn of the century, Richard Teller Crane had built not just a company but a dynasty. On his death, his personal fortune was estimated at $50-million and in his era he was reputed to have been the second richest man in Chicago.

In 1910, when Crane had begun to manufacture in a plant at Bridgeport, Connecticut, its Chicago plants employed more than 5,000 people. A large new Chicago plant on South Kedzie Avenue was built in the 1910s.

Crane died on January 8, 1912, in Chicago, Illinois. He left behind a company that dominated the American plumbing industry—but his heirs would transform it into something far more.

III. Building an American Industrial Giant (1900–1959)

The Sons Take the Reins

Richard Teller Crane, Jr. was an industrialist like his father. He was the Chief Executive Officer for the "Crane Company" from 1914 to 1931. He was believed to have been the second wealthiest man within the city of Chicago, as the Sears and Roebuck founder was the wealthiest at the time.

The transition from founder to second generation is often a death knell for industrial companies. Not for Crane. After the death of his father, there was some discussion between R. T. Crane, Jr. and his older brother, Charles, over the terms of their father's will. Their lawyers advised both men to submit a closed bid naming a price for buying the other out of the family business. Richard submitted the higher bid and Charles agreed.

This elegant solution—letting the brothers bid against each other for control—avoided a destructive family fight and concentrated ownership in the hands of the more business-focused sibling.

World War I brought a huge increase in business to the company, and it continued to expand. In 1921 with the purchase of the Trenton Potteries Company, the firm launched a line of business for which it is probably most remembered today. A line of plumbing fixtures had been sold since 1894, but after the war ended Crane began an advertising campaign, exceeding a million dollars a year.

The campaign worked. Frank Lloyd Wright's Imperial Hotel in Tokyo, the brand new Drake Hotel, the Field Museum of Natural History, and the 1928 remodeling of Wrigley Field all used the Crane line of plumbing fixtures.

The Legal Precedent That Shaped Commerce

One of the more curious chapters in Crane's history involves a 1917 Supreme Court case that helped define the limits of state power over interstate commerce.

In Looney v. Crane Co., the Court held that "Neither the right of a state to attach conditions when licensing a sister state corporation to do local business nor its power to tax the corporation in respect of such business, when licensed, can sustain impositions which, in the guise of permit charges or franchise or excise taxes, result in direct burdens on interstate commerce."

The Court held "that the franchise and permit taxes both violated the due process clause of the Fourteenth Amendment and directly burdened interstate commerce."

The case arose when Texas attempted to impose franchise taxes calculated on Crane's total national capital, not just its Texas operations. The authorized capital stock of the Crane Company was $17,000,000, which was paid up and issued and just prior to the institution of this suit the surplus and undivided profits of the company amounted to $8,129,000.

The ruling established a principle that states cannot burden interstate commerce through discriminatory taxation—a precedent that continues to shape corporate tax law today.

The NYSE and National Scale

During the 1920s, when Crane expanded overseas, the company was the world's leading manufacturer of valves and fittings. During the next few decades, Crane continued to employ thousands of Chicago-area residents at its Kedzie Avenue plant, and the company's annual sales rose to over US$300 million by the mid-1950s.

The company listed on the New York Stock Exchange in 1936, cementing its status as a blue-chip industrial concern.

The Aerospace Pivot Begins

The most consequential decision in Crane's 20th-century history came in 1951: With the 1951 acquisition of Hydro-Aire Incorporated, Crane entered the business of precision aircraft products and flow control equipment, supplying filters and valves to all manufacturers of turbine type aircraft engines.

Hydro-Aire and Boeing pioneered brake control in 1946 and installed the first system on a Boeing/USAF B-47 in 1947. The B-47 was the world's first high speed, swept wing, jet bomber and led the way for the introduction of modern transport aircraft.

This was a remarkable technological leap. The B-47 was revolutionary—the first swept-wing jet bomber, capable of near-supersonic speeds. Its landing challenges were unprecedented. Traditional braking systems couldn't handle the energy dissipation required to stop an aircraft traveling at such speeds. Hydro-Aire's antiskid technology solved this problem, and Crane was suddenly in the aerospace business.

Crane Aerospace & Electronics has continued to define and refine the science of antiskid brake control since 1947. The systems have evolved from the early tire-savers to the modern, fully adaptive, digital Mark IV system, which is standard equipment on all current production Boeing aircraft.

IV. The Conglomerate Era: Going Global & Going to Space (1960s–1990s)

The Evans Takeover

In 1959, however, the company was acquired by Thomas Mellon Evans, its first owner who was not a member of the Crane family.

Thomas Mellon Evans (September 8, 1910 – July 17, 1997) was an American financier who was one of the country's early corporate raiders, as well as a philanthropist and Thoroughbred racehorse owner and breeder who with Pleasant Colony won the 1981 Kentucky Derby and Preakness Stakes.

Among his major acquisitions was the 1959 takeover of Crane Co. of Chicago, then a large valve and plumbing fixture manufacturer. In April 1959 Evans was appointed Chairman of the Board and Chief executive officer of the company.

Evans was a controversial figure. When Evans moves into a faltering company, he ruthlessly shakes it up. When he took over Crane, he closed or sold 43 of its 130 branch outlets and fired four vice presidents. Six directors have quit the board. Crane executives who watched him in operation call him "crude and brutal." Pickets striking against Crane carried signs at the annual meeting reading MONEY MAD EVANS HAS NO HEART.

But under Evans' firm hand, Crane is doing better. While sales fell last year as Evans slashed unprofitable lines of products, earnings jumped to $6,517,746 (v. $2,167,345 in 1958). This year the trend continues; earnings for the first quarter were 67¢ per share (v. 38¢ for the same period last year).

In 1959, T.M. Evans was elected Chairman and CEO. A new management philosophy moves Crane to streamline the distribution network and concentrate on industrial manufacturing. Industrial expansion is furthered through domestic and international acquisitions such as Chapman Valve, Cochrane Corporation, Deming Company and Chempump.

International Expansion

In 1961, Crane becomes a true multi-national operation with fifty manufacturing facilities across the United States, Canada, England, France, Italy, The Netherlands, and Mexico. In 1963, Crane furthers its commitment to R&D with new engineering and laboratory facilities near Philadelphia.

By the 1960s, Hydro-Aire catered to the space program with production of life-support and coolant pumps. It also expanded its role in the realm of aerospace by taking the lead in antiskid braking systems, fuel and hydraulic pumps, valves and regulators, actuators, and solid-state components.

Apollo: Crane Goes to the Moon

Hydro-Aire and Chempump pumps are used in the Gemini and Apollo Space programs. Crane is well-positioned in four major areas of concentration: fluid and pollution control, steel, building products and aircraft/aerospace.

Crane's Hydro-Aire brand supported the Apollo 11 mission by providing the cooling system for the lunar landing module.

When Neil Armstrong stepped onto the lunar surface in July 1969, Crane technology had helped get him there. The cooling systems that kept the lunar module's electronics from overheating in the extreme temperature swings of space were Crane products. The pumps that circulated vital fluids were Crane products.

The R.S. Evans Era and Portfolio Reshaping

In 1984, Thomas M. Evans resigns as Chairman of the Board after serving Crane for 25 years. His son, R.S. Evans, is elected Chairman and CEO, and the company announces a new strategic plan to build on its strength in special light- to medium-manufacturing and wholesale distribution, while reducing reliance on more capital intensive, cyclical and commodity oriented businesses.

In 1985, Crane acquires UniDynamics, a conglomerate that included the initial components of Engineered Materials (Kemlite) and Merchandising Systems (National Vendors) segments. This acquisition also included Resistoflex, which grew to become one of Fluid Handling's most important brands.

Evans leads Crane as a growth company with a strong acquisition program in areas of fluid handling, engineered materials, merchandising systems, aerospace and controls. During R.S. Evans' tenure as Chairman and CEO from 1984 to 2001, the company's market capitalization increased from under $200 million to approximately $1.8 billion.

Crane exits the plumbing and plumbing distribution businesses in the U.S. The Crane Plumbing unit was sold off in 1990. Crane Plumbing is now a unit of American Standard Brands.

This was a remarkable strategic shift. The company that had been synonymous with American plumbing for a century voluntarily exited the business to focus on higher-margin industrial and aerospace applications.

A study by Jeremy Siegel in The Future For Investors (published 2005) noted that Crane Co. had the 10th best shareholder return (15.1% annually) from 1957 to 2003 among surviving firms of the original 1957 S&P 500 index, a list dominated by large pharmaceutical and well-known consumer brand companies.

V. The Modern Transformation: Max Mitchell & Strategic Focus (2014–Present)

A New Kind of Leader

Max Mitchell is Chairman of the Board, President & Chief Executive Officer of Crane Company, a $2 billion global manufacturer of innovative and technology-led solutions for the Aerospace, Defense, Space, and Process Flow industries. He became President and CEO in 2014 and was appointed to the additional role of Chairman in April 2024.

A native of Pittsburgh, he earned his MBA in Finance from the University of Pittsburgh, Katz Graduate School of Business and his BA from Tulane University.

Mitchell joined Crane Company as an executive officer in 2004 and held increasing roles — including leadership in the Fluid Handling Group, Executive Vice President and Chief Operating Officer, and President and Chief Operating Officer — before being promoted to President and Chief Executive Officer.

Mitchell served in various senior operating roles within the Danaher Corporation and Pentair. Mr. Mitchell began his career with the Ford Motor Company in finance and operations.

Mitchell's background at Danaher was particularly formative. The Danaher Business System is one of the most respected operational excellence frameworks in industrial America, and Mitchell brought those principles to Crane.

The Transformation Strategy

Over the course of his tenure as CEO, Mr. Mitchell led a broad-based transformation of Crane's portfolio. He increased internal investments with a focus on next-generation technologies and new product development in the Company's higher-growth markets, completed more than $2 billion of acquisitions and executed on multiple divestitures. These actions culminated in the 2023 separation into two focused and high-return publicly-traded companies, Crane Company and Crane NXT, Co., and resulted in more than $5 billion of shareholder equity value creation.

Our strategy is to grow earnings and cash flow by focusing on the development and manufacturing of highly engineered industrial products for specific markets where our scale is a relative advantage, and where we can compete based on our proprietary and differentiated technology, our deep vertical expertise, and our responsiveness to unique and diverse customer needs. We continuously evaluate our portfolio, pursue acquisitions that complement our existing businesses and selectively divest businesses where appropriate.

VI. The Asbestos Albatross: A Masterclass in Liability Management (2022)

The Legacy Problem

Like many American industrial companies with roots in the 19th century, Crane accumulated significant asbestos liabilities. At various points, Crane products contained asbestos components—a common practice in industrial manufacturing before the health risks became widely understood.

By the early 2000s, these legacy liabilities had become a drag on the company's balance sheet and a distraction for management. The uncertainty around future claims deterred some investors who otherwise might have been attracted to Crane's strong industrial franchises.

The Bold Solution

Crane Holdings, Co. announced today that it has divested Redco Corporation ("Redco"), a wholly owned subsidiary that holds liabilities including asbestos liabilities and related insurance assets to Spruce Lake Liability Management Holdco LLC ("Spruce Lake" or "Spruce Lake Liability Management"), a long-term liability management company specializing in the acquisition and management of legacy corporate liabilities. The transaction indemnifies Crane for all legacy asbestos liabilities. At closing, Crane contributed approximately $550 million in cash to Redco, and Spruce Lake made a capital contribution of $83 million.

On August 12, 2022, Crane Co. transferred its asbestos-related liabilities to Redco Corporation. That same day, it entered into a Stock Purchase Agreement with Spruce Lake Liability Management Holdco LLC. As part of the transaction, Redco was divested to Spruce Lake, a firm specializing in managing legacy corporate liabilities, along with all related asbestos obligations, insurance assets, and $550 million in cash. This move effectively removed all asbestos liabilities from Crane Co.'s core operations.

Spruce Lake will assume the operational management of Redco, including the administration of all the asbestos claims and collection of existing insurance policy reimbursements. As a result of the transaction, Crane has removed all asbestos obligations and liabilities, related insurance assets, and associated deferred tax assets from the company's consolidated balance sheet. The divestiture will result in an estimated one-time after-tax loss of approximately $170 million.

Strategic Rationale

Eliminating ongoing payments for asbestos related defense and indemnity costs will increase annual free cash flow available for us to invest in our business, both organically and inorganically. The transaction will also give us substantially more flexibility to optimize the capital structures for post-separation Crane Company and Crane NXT in a manner that positions both companies for growth and value creation.

Spruce Lake Liability Management, an entity formed by a joint venture between Global Risk Capital LLC and affiliates of Fortress Investment Group LLC, is a long-term liability management company specializing in the acquisition and management of legacy corporate liabilities and related corporate assets. Spruce Lake draws on the extensive experience of Global Risk Capital LLC, which has made over 140 portfolio acquisitions and investments in the legacy liability sector since 2001. Spruce Lake's mission is to assist corporate stakeholders by restructuring or divesting legacy liabilities, through transactions that optimize corporate balance sheets and allow management to refocus on core business operations.

The $550 million cash contribution was substantial, but it bought Crane something priceless: certainty. No more quarterly earnings calls discussing asbestos claim trends. No more investor questions about tail risk. No more management distraction. The company paid to make a problem disappear, and it worked.

VII. The 2023 Separation: Creating Two Focused Companies

The Strategic Logic

Tax-Free Spin-Off Creates Two Optimized, Technology-Driven Companies with Strong Financial Profiles and Operating Metrics. Crane Co. announced today that its Board of Directors has unanimously approved a plan to pursue a separation into two independent, publicly-traded companies to optimize investment and capital allocation, accelerate growth, and unlock shareholder value.

The spin-off will be effected through a pro rata distribution of all of the outstanding shares of Crane Company common stock to holders of Crane Holdings, Co. common stock in a transaction that is intended to be tax-free to holders of Crane Holdings, Co. common stock for U.S. federal income tax purposes. Each Crane Holdings, Co. stockholder will receive one share of Crane Company common stock for every one share of Crane Holdings, Co. common stock held on the record date of March 23, 2023.

Crane Company: The "New" CR

Crane Co (CR) will break up into two public companies on April 3: Crane Co and Crane NXT. Crane Co, the spin-off, will retain the Crane name/ticker and be comprised of the Aerospace & Electronics and Process Flow Technologies (valves/pumps) businesses. The current CEO (Max Mitchell) and current CFO (Rich Maue) will go with the spin off.

Post completion, Aerospace & Electronics and Process Flow Technologies Businesses will retain the name of Crane Co. and it will continue to publicly traded on New York Stock Exchange under current symbol of CR whereas Payment and Merchandising Technologies Business will Become Crane NXT.

Crane NXT: The Currency Business Departs

US-based technologies firm Crane Holdings Co announced Monday that it has completed the separation of its Payment and Merchandising Technologies business, to be known as Crane NXT. The segment, which includes currency validation firm Crane Payment Innovations (CPI), provides payment technology to the global gaming industry.

Crane NXT will begin trading on the New York Stock Exchange on April 4, 2023 under the ticker "CXT."

The Crane NXT business was remarkable in its own right—the company had supplied currency to the Federal government since 1879 and had been the sole provider since 1964. But its business model and growth trajectory were fundamentally different from aerospace and industrial flow technologies. By separating them, management allowed each to pursue its natural strategy without compromising the other.

Post-Separation Results

Max Mitchell, Crane's Chairman, President and Chief Executive Officer, stated: "Crane Company had an exceptional year with both segments executing at a high level. As a result, we delivered 8% core sales growth with 28% adjusted EPS growth in 2024. Further, we continued to strengthen and focus our portfolio with the acquisitions of Vian, CryoWorks and Technifab, as well as with the divestiture of our Engineered Materials segment."

VIII. Today's Crane: The Two Strategic Platforms

Aerospace & Electronics Segment

Crane A&E comprises approximately 44% of Crane Company, a $2.1B publicly traded company.

Crane's Aerospace & Electronics segment is a trusted industry leader providing reliable, high-precision technologies that drive innovative solutions for our customers in the commercial aerospace, military aerospace, defense, and space markets. Crane A&E delivers proven systems, reliable components, and flexible solutions that excel in tough environments — from engines and landing gear to satellites, missiles and electronic countermeasure devices.

We invented many of the fundamental technologies that are now the industry standard in the areas where we compete, with a track record for performance, reliability and innovation.

The Aerospace & Electronics business is built on heritage brands that have become synonymous with aircraft safety:

The first Hydro-Aire Mark I antiskid was developed for the military Boeing B-47 bomber in 1947.

Military aircraft received the benefit of the significant performance improvement available from the Hydro-Aire Mark III slip velocity control with systems installed on the F-4, F-15, F/A-18, C-9B, C/KC-135, and the B-1A/B. Developmental Mark III systems were also developed for the F-5 and CF-5 aircraft. The C-17 was the first Military aircraft to use the Hydro-Aire digital Mark IV antiskid technology with an integrated Brake Temperature Monitoring System (BTMS).

Recent contract wins demonstrate the segment's continued relevance:

Crane Aerospace & Electronics, a segment of Crane Co. (NYSE:CR), has been selected by Defense Logistics Agency Aviation to provide a brake control system redesign for the United States Air Force fleet of F-16 aircraft.

The brake control system for the F-16 will leverage Crane Aerospace & Electronics' Mark V Brake-By-Wire system technology to deliver safe, reliable and highly efficient braking performance. The brake control system will also incorporate design improvements to simplify system maintenance as well as address existing single point failures for improved safety. Through the contract, valued at $84M, DLA will see the USAF F-16 fleet retrofitted over three years from 2026-2028.

Crane has over 60 years of experience in aircraft grade power conversion, management, monitoring, advanced packaging solutions and energy storage.

Process Flow Technologies Segment

Crane's Process Flow Technologies segment is a global provider of highly engineered products and systems, including valves, pumps, lined pipe, instrumentation and controls, serving chemical, petrochemical, pharmaceutical, water and wastewater, and general industrial markets. With proprietary technology and differentiated designs, we are solving our customers' toughest challenges in mission-critical applications that require high-reliability in many of the harshest and most hazardous environments.

This business traces its lineage directly to Richard Teller Crane's original brass foundry. But today's products are vastly more sophisticated:

Crane ChemPharma & Energy designs and manufactures a variety of high-performance products including highly engineered check valves, sleeved plug valves, lined valves, process ball valves, high-performance butterfly valves, bellows sealed globe valves, aseptic and industrial diaphragm valves, multi/quarter-turn valves, actuation, sight glasses, lined pipe, fittings and hoses, and air operated diaphragm and peristaltic pumps.

Recent Performance

At Aerospace & Electronics, 2024 sales increased 18% compared to 2023, including a 5% benefit from the Vian acquisition. Segment operating margins increased 230 basis points, from 20.1% in 2023 to 22.4% in 2024. These results reflect strong performance, particularly given persistent supply chain and customer challenges in the Aerospace, Defense and Electronics markets. In addition to the financial performance throughout 2024, the segment continues to secure new business, and the segment's backlog reached an all-time high of $864 million at the end of the year.

At Process Flow Technologies, 2024 sales increased 12% compared to 2023, with core sales growth of 5%, and a 7% contribution in the aggregate from the Baum, CryoWorks and Technifab acquisitions. Segment operating margins reached a record level of 20.1%, up 70 basis points compared to 2023, and adjusted Segment operating margins reached a record 20.9%. These results reflect record performance for the Segment despite ongoing macro pressures.

Bolt-On Acquisitions Continue

On January 2, 2024, the Company completed the acquisition of Vian Enterprises, Inc. ("Vian"). Vian is a global designer and manufacturer of multi-stage lubrication pumps and lubrication system components technology for critical aerospace and defense applications with sole-sourced and proprietary content on the highest volume commercial and military aircraft platforms. Vian has been integrated into the Aerospace & Electronics segment.

On May 1, 2024, the Company completed the acquisition of CryoWorks, Inc. ("CryoWorks"). CryoWorks is a leading supplier of vacuum insulated pipe systems for hydrogen and cryogenic applications. CryoWorks has been integrated into the Process Flow Technologies segment.

Crane Company announced that on Friday, November 1, 2024, it completed the acquisition of Technifab Products, Inc. ("Technifab"), a leading provider of vacuum insulated pipe systems and valves for cryogenic applications for $40.5 million on a cash-free and debt-free basis. Founded in 1992 by Noel Short, Technifab is headquartered in Brazil, Indiana. Through September 2024, Technifab had trailing 12-month sales and adjusted EBITDA of approximately $20 million and $4 million, respectively. Technifab joins Crane as part of the company's Process Flow Technologies (PFT) segment and extends our cryogenics capabilities into high growth semiconductor, medical and pharmaceutical end markets.

IX. Playbook: Business & Investing Lessons

The "Focus and Simplify" Playbook

Crane's recent history offers a masterclass in corporate transformation through subtraction:

Lesson 1: Sometimes the best acquisition is a divestiture. The asbestos liability sale wasn't free—Crane paid $550 million to make the problem go away. But it removed an overhang that had depressed the stock's valuation multiple for years, eliminated management distraction, and created the clean balance sheet needed for the separation.

Lesson 2: Conglomerates can unlock value through separation. The 2023 separation wasn't an admission of failure—it was recognition that Crane NXT and Crane Company served different customers, competed in different markets, and needed different capital allocation strategies. Combined, they constrained each other. Separated, each could pursue its natural destiny.

Lesson 3: Century-old industrial companies can reinvent themselves. Crane's journey from plumbing fixtures to space shuttle brake systems illustrates that legacy doesn't have to mean stagnation.

The Long-Term Thinking Advantage

Noteworthy that 20% of shares are held by Crane Foundation as well which adds to the long-term outlook the management communicates. Strong balance sheet paying back long-term debt from COVID in full early. Recent significant share repurchases are a positive signal.

The presence of the Crane Foundation as a major shareholder creates an alignment that many public companies lack. Foundation ownership tends to encourage patient capital allocation rather than quarter-to-quarter optimization.

Capital Allocation Excellence

As of December 31, 2024, the Company's cash balance was $307 million with total debt of $247 million. Subsequent to the end of the fourth quarter, on January 2, 2025, the Company received net proceeds of $208 million related to the divestiture of Engineered Materials. Rich Maue, Crane's Executive Vice President and Chief Financial Officer, added: "As we enter 2025, our balance sheet along with solid expected cash flow, position us well to invest in our organic growth initiatives and pursue strategic acquisitions to drive long-term value creation."

The net cash position gives Crane enormous optionality. Management can pursue acquisitions opportunistically without being forced to issue equity at inopportune times.

Lessons on Moats

Except from the aero business which has some moat through FAA approved products, I don't see how their products are very differentiated.

This critique deserves examination. Crane's aerospace business has genuine moats:

- FAA certification requirements create significant barriers to entry. Getting a brake control system certified for a commercial aircraft takes years and millions of dollars.

- Installed base advantages: Once Crane systems are designed into an aircraft platform, they typically remain for the life of that platform. Boeing isn't going to redesign the 737's brake control system to save a few percentage points on component costs.

- Customer switching costs: Airlines and aircraft manufacturers prioritize proven reliability over cost. A brake failure isn't a warranty claim—it's a potential catastrophe.

The Process Flow Technologies business has narrower moats, but still benefits from: - Customer qualification processes that can take years - Deep application engineering expertise that competitors struggle to replicate - Brand reputation in safety-critical applications

X. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: LOW

Crane Aerospace & Electronics has over 75 years of experience in providing brake control systems, with more than 30,000 systems in operation today.

The barriers to entry in aerospace components are formidable: - FAA and military certification requirements create a multi-year, multi-million dollar gauntlet that new entrants must navigate - Customer qualification processes require years of testing and validation - Capital intensity and engineering expertise requirements filter out undercapitalized competitors - Installed base advantages mean incumbents have decades of service data that new entrants cannot replicate

2. Bargaining Power of Suppliers: MODERATE

Crane's products require specialized materials and components, some of which are sole-sourced. The aerospace supply chain has experienced significant disruption since 2020, and Crane has noted supply chain challenges in earnings calls. However, Crane's scale and long-term relationships provide some negotiating leverage.

3. Bargaining Power of Customers: MODERATE TO HIGH

Crane's customers include Boeing, Airbus, and major defense contractors—not exactly pushovers in negotiations. However, the mission-critical nature of Crane's products and the switching costs involved provide some pricing power. When the alternative to Crane's brake control system is potentially catastrophic failure, price becomes less important than performance and reliability.

4. Threat of Substitutes: LOW

Aircraft need brake control systems. Chemical plants need valves. There's no app for that. While alternative technologies exist (electric braking, for example), they tend to expand the market rather than substitute for existing products.

5. Competitive Rivalry: MODERATE

Crane Aerospace & Electronics's top competitors include Lectratek, Nottingham Scientific, and Rolls-Royce.

The aerospace components market is competitive but rational. Large programs tend to be split among a small number of qualified suppliers, and price wars are rare in safety-critical applications. In Process Flow Technologies, competition is more fragmented, but Crane's focus on niche applications provides differentiation.

Hamilton's 7 Powers Framework

Counter-Positioning: Crane's strategic pivot from conglomerate to focused industrial company represents counter-positioning against larger, more diversified competitors. By concentrating on aerospace and process flow, Crane can invest more heavily in these areas than diversified competitors who must spread resources across many businesses.

Cornered Resource: Crane's 75+ years of brake control system experience, including proprietary data from 30,000+ systems in operation, represents a cornered resource that competitors cannot easily replicate. The institutional knowledge of what works in mission-critical applications has been accumulated over decades.

Process Power: Crane's operational excellence culture, influenced by CEO Mitchell's Danaher background, creates process power. The company's ability to consistently deliver high-quality, certified components reflects manufacturing and quality processes that are difficult to copy.

Scale Economies: In aerospace components, scale matters less than in consumer goods. However, Crane's scale provides R&D leverage—the company can spread development costs across a larger revenue base than smaller competitors.

Network Effects: Limited in industrial components.

Switching Costs: HIGH. Once Crane systems are designed into an aircraft platform, the costs of switching—re-certification, re-testing, supply chain disruption—are prohibitive. Airlines and aircraft manufacturers are not going to switch brake control suppliers to save a few percentage points.

Branding: In industrial components, brand operates differently than in consumer goods. Crane's brand represents reliability and performance in mission-critical applications—attributes that command premium pricing and reduce customer acquisition costs.

XI. Key Performance Indicators to Watch

For long-term fundamental investors, three KPIs matter most for Crane:

1. Aerospace & Electronics Backlog

Aerospace & Electronics' order backlog was $864 million as of December 31, 2024 compared to $701 million as of December 31, 2023.

The backlog represents future revenue visibility. Given the long lead times in aerospace, changes in backlog provide early signals about demand trends 12-24 months in advance. The record backlog level suggests strong demand ahead.

2. Segment Operating Margins

Operating margins reveal whether Crane is capturing the value of its engineering expertise or competing primarily on price. Operating profit margin of 22.4% increased 220 basis points from last year. Adjusted operating profit margin of 23.1% increased 290 basis points from last year.

Margins above 20% indicate pricing power and operational efficiency. Sustained margin improvement suggests Crane is successfully shifting its mix toward higher-value products and services.

3. Core Sales Growth (Ex-Acquisitions)

As a result, we delivered 8% core sales growth with 28% adjusted EPS growth in 2024.

Core sales growth—organic growth excluding acquisitions and currency—reveals the underlying health of the business. Crane's long-term target of 4-6% core sales growth reflects realistic expectations for a mature industrial company. Sustained performance above this target indicates market share gains or favorable end-market conditions.

XII. Bull Case and Bear Case

The Bull Case

Aerospace Recovery Tailwinds: Commercial aerospace production rates remain below pre-pandemic peaks, providing a multi-year recovery runway. Boeing and Airbus both have large order backlogs, and every aircraft produced requires Crane components.

Defense Spending Momentum: Rising geopolitical tensions have driven defense budgets higher globally. Crane's position on military platforms like the F-16, F-15, and KC-46 provides exposure to this trend.

Cryogenics and Hydrogen Optionality: The acquisitions of CryoWorks and Technifab position Crane for potential growth in hydrogen infrastructure and semiconductor manufacturing—two areas with significant long-term investment tailwinds.

Clean Balance Sheet: As of December 31, 2024, the Company's cash balance was $307 million with total debt of $247 million. Subsequent to the end of the fourth quarter, on January 2, 2025, the Company received net proceeds of $208 million related to the divestiture of Engineered Materials.

The resulting net cash position provides optionality for acquisitions, share repurchases, or special dividends.

Management Track Record: CEO Mitchell has demonstrated disciplined capital allocation over a decade, navigating the separation, asbestos divestiture, and portfolio optimization while maintaining operational performance.

The Bear Case

Boeing Dependency: Crane's aerospace business is heavily dependent on Boeing, which has faced significant operational and regulatory challenges. Extended Boeing production issues would impact Crane's revenue and profitability.

Cyclicality: Both aerospace and industrial markets are cyclical. A recession that reduced aircraft production and industrial capex would pressure Crane's results.

Process Flow Technologies Competitive Dynamics: While aerospace components enjoy meaningful moats, the valve and pump business faces more competitive pressure. Margin sustainability depends on maintaining technology leadership in niche applications.

Acquisition Integration Risk: We expect the company to continue to pursue strategic acquisitions, and poor execution of its M&A strategy could destroy shareholder value.

Premium Valuation: CR is trading at a 142% premium. A premium valuation creates less margin of safety and higher expectations for execution.

XIII. Conclusion: The Next 170 Years

When Richard Teller Crane opened his brass foundry on July 4, 1855, he couldn't have imagined that his company would one day help land men on the moon. The 23-year-old with minimal formal education who escaped the Panic of 1854 built an institution that has now survived the Civil War, two World Wars, the Great Depression, multiple financial crises, and fundamental shifts in technology and markets.

Today's Crane Company is in many ways unrecognizable from that original brass foundry—but the DNA persists. The focus on mission-critical applications. The willingness to invest in new technologies. The respect for engineering excellence over financial engineering.

The company initiated its full year 2025 adjusted EPS outlook with a range of $5.30-$5.60 reflecting 12% growth at the midpoint compared to 2024 adjusted EPS.

For investors, Crane offers a rare combination: exposure to aerospace and defense growth trends through a company with genuine competitive moats, a clean balance sheet, disciplined management, and a track record spanning nearly 170 years.

The question isn't whether Crane will survive the next decade—companies this durable don't disappear easily. The question is whether management can continue executing the "focus and simplify" playbook while finding new growth vectors in areas like cryogenics and hydrogen infrastructure.

If history is any guide, betting against Crane has been a losing proposition since 1855.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube