Ryder System: America's Fleet Pioneer & The Quiet Supply Chain Revolution

Introduction: From $35 to $12 Billion

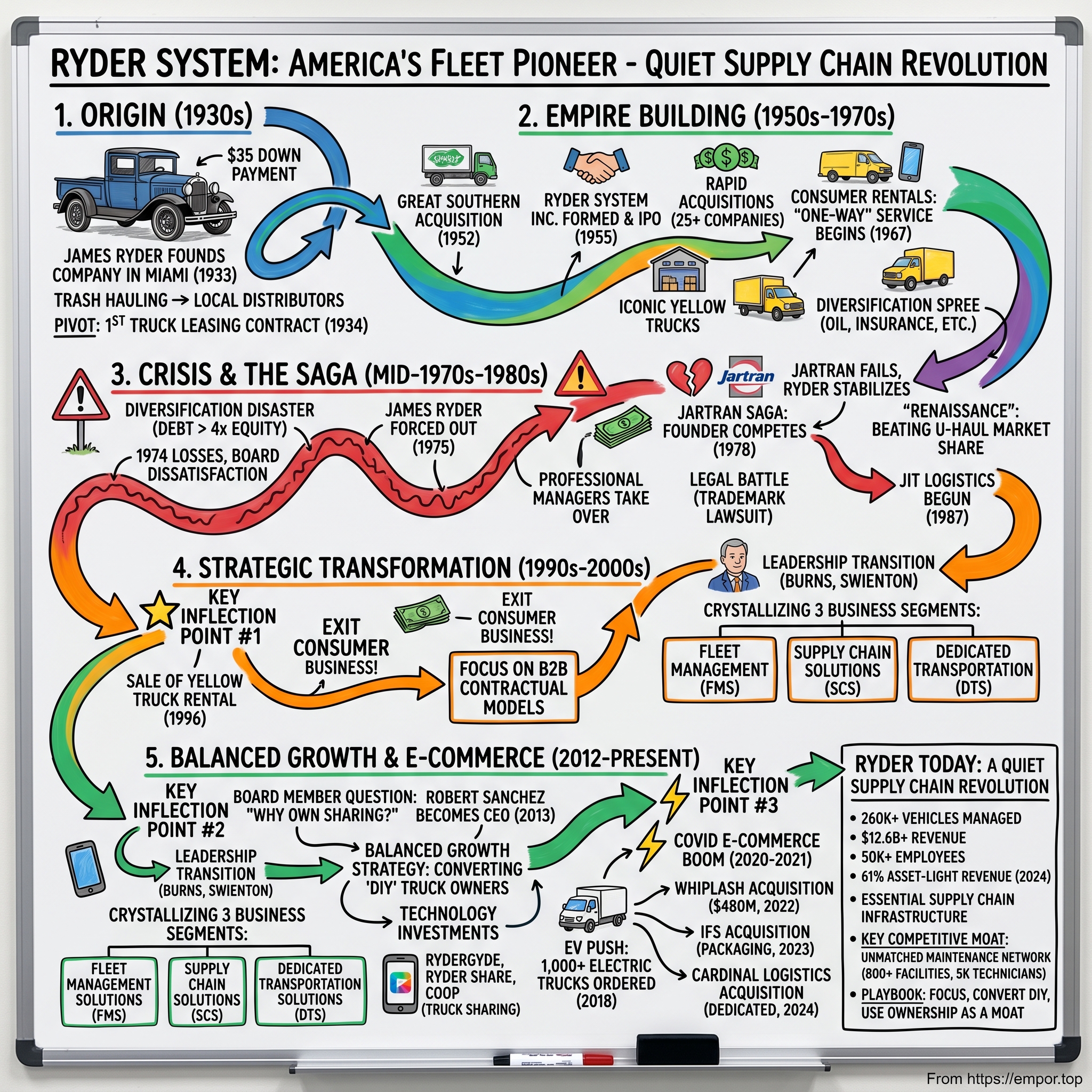

In the summer of 1933, amid the depths of the Great Depression, a 20-year-old former construction worker named James Ryder handed over $35—equivalent to a week's wages for most Americans who still had jobs—as a down payment on a dusty Model A Ford pickup truck. That truck would haul concrete and debris from the beaches of Miami to construction sites in Palm Beach. Today, Ryder System manages a fleet of approximately 260,000 commercial vehicles across North America, generates $12.64 billion in annual revenue with 7.24% growth in 2024, and employs 50,700 people globally, including approximately 13,400 drivers, 5,000 technicians, and 34,000 hourly employees.

This is the story of how a scrappy Miami entrepreneur invented an entire industry, lost control of his company to professional managers, founded a rival to compete with his own creation, and watched from the sidelines as his successors transformed Ryder into something he might not recognize—a technology-enabled supply chain powerhouse that has quietly become essential to how modern commerce functions.

"Ryder delivered strong results in 2024 and year-over-year earnings growth during the fourth quarter, despite ongoing freight market headwinds," declared CEO Robert Sanchez in February 2025. "This marks the first quarter in the last eight with year-over-year comparable earnings growth." Behind that understated corporate-speak lies a remarkable tale of strategic reinvention—one that saw the company sell its most famous asset, the iconic yellow moving trucks, to focus on a B2B empire built on contractual relationships, maintenance networks, and supply chain sophistication.

The central question this story explores: How did a company best known for consumer moving trucks become a behind-the-scenes infrastructure provider for global brands—and what does that transformation reveal about the economics of asset-heavy businesses, the value of focus, and the hidden power of maintenance networks?

The Origin Story: $35, a Model A Ford, and Miami Beaches

The Depression-Era Entrepreneur

Born in 1913 in Columbus, Ohio, James Ryder moved to Miami at the age of six. As a teenager, he worked in construction and hauled concrete. In 1933, fresh out of high school, he bought a $35 Model A Ford truck and started a trucking business. The image is almost impossibly American: a young man with nothing but ambition and $35 building an empire in one of the country's most dynamic cities during its darkest economic hour.

In 1932 James A. Ryder gave up his job as a straw boss in a construction firm and bought a Model A pickup truck. Ryder hauled trash from Miami beaches and delivered construction materials to Palm Beach. Those early days were hand-to-mouth—literally exchanging labor for cash, with no clear vision of what the company would become. But Miami in the 1930s was a peculiar place: devastated by the 1926 hurricane and the subsequent real estate bust, it was nonetheless rebuilding, creating demand for exactly the kind of hauling services Ryder could provide.

The Pivot That Changed Everything

The inflection point came in 1934 when Ryder landed a contract that would define his industry. In 1934 he entered the truck-leasing business through a contract with a local beer distributor. At the age of 21, Ryder was the owner of the first truck-leasing firm in the United States, Ryder Truck Rental System, Inc.

The insight was elegant in its simplicity: a beer distributor needed trucks to deliver product but didn't want the headache of owning, maintaining, and managing a fleet. Ryder realized he could provide vehicles as a service rather than selling hauling labor by the hour. The business model shift—from operating trucks to owning and leasing them—would prove transformative.

By 1938, momentum was building. Ryder signed a five-truck lease deal with Champagne Velvet Beer, increasing Ryder's fleet to 20 trucks. By the following year, the fleet had more than 50 trucks. This led to Ryder changing its focus from distribution to leasing.

Industry Tailwinds

Ryder's timing was impeccable—or perhaps lucky. Highway trucking began to rival rail as a means of overland shipping, based partly on the vast network of better highways constructed during the 1930s. World War II boosted demand for trucking as the war economy stretched the existing transportation system to capacity, and Ryder's trucking and leasing operations grew. The postwar era brought continued growth to the trucking industry as the interstate highway program further improved the efficiency of trucking.

In 1939, Ryder brought on a partner. In 1939 Ryder took on a partner, Roy Reedy, and the business began to expand rapidly. The growth trajectory was steep: By 1946 he was grossing $1.5 million a year. By 1952 Ryder was bringing in $3 million annually by renting 1,300 trucks.

For investors, this origin story illustrates a critical pattern: capital-light innovation (conceptualizing the leasing model) followed by capital-heavy execution (actually building the fleet). Ryder didn't invent trucking—he invented a business model that would transform how companies thought about fleet ownership.

Building an Empire: The Acquisition Era (1950s–1970s)

The Great Southern Deal

The acquisition that put Ryder on the national map came in 1952. Ryder bought Great Southern Trucking Company in 1952. This wasn't just another fleet acquisition—Great Southern was an established motor carrier operation, giving Ryder both geographic reach and diversification into actual freight operations.

The corporate structure evolved to match the growing ambition. In 1955 Ryder System, Inc. was formed to combine Great Southern and Ryder Truck Rental. Ryder System, Inc. incorporated as a public company and issued 160,000 shares of common stock at $10 per share.

The IPO was modest by any measure—$1.6 million raised at a $10 share price. But it provided the currency Ryder needed for expansion. Jim Ryder began leasing trucks to a local beer distributor in the Miami area in 1934. This venture made him, at the age of 21, the owner of the first truck-leasing firm in the United States. By the time he received a Horatio Alger award in 1960, his stake in the company was worth $11 million, the equivalent of more than $59 million today.

Rapid Acquisition—and Its Problems

The newly public company went on a buying spree. In the five years following the IPO, Ryder acquired more than 25 companies. But rapid expansion created problems that would foreshadow future governance crises.

The challenge with acquisition-driven growth in asset-heavy businesses is that each deal adds not just revenue but complexity, maintenance obligations, and working capital requirements. Ryder's financial controls couldn't keep pace with its ambition. By 1960, the company was forced to write off $2 million in bad debt, and profits dropped from $2.7 million in 1959 to approximately $1 million in 1960—a decline of more than 60% despite continued revenue growth.

Strategic Refocusing

Ryder System focused on the fast-growing truck-leasing business and, despite common misconceptions, had not operated as a freight carrier since 1965. In 1965 Ryder System sold the motor carrier division to International Utilities (IU), a diversified holding company.

This 1965 divestiture is often overlooked but represents an early instance of strategic focus that would become Ryder's recurring playbook: exit commodity businesses, concentrate on differentiated capabilities.

In 1967, Ryder made what seemed like an obvious move: In 1967 Ryder began offering one-way truck rental service. This service had been introduced and popularized by the U-Haul Company several years earlier. Ryder started with 1,000 trucks and expanded the one-way fleet to 7,630 the first year.

The consumer rental business would eventually become Ryder's most visible brand asset—the bright yellow trucks that millions of Americans associated with moving day. But it would also, three decades later, become the business that Ryder famously exited.

The supply chain seeds were also planted in this era. In 1971, Ryder entered the supply chain solutions business, providing logistics services to commercial customers—a business line that would eventually generate the majority of the company's revenue.

The 1970s Crisis & The Founder Steps Down

Diversification Disaster

By the early 1970s, James Ryder had caught acquisition fever again—and this time, the targets made less strategic sense. The company expanded into mobile homes, insurance, petroleum distribution, and even technical schools. Each acquisition added complexity without obvious synergies.

Other problems—adjustments in the calculation of receivables from the education unit, tax assessments on the mobile home subsidiary, and reserve assessments on the insurance subsidiary—resulted in a 13 cents per share adjustment to Ryder stock following the company's 1973 audit. The truck leasing and rental businesses continued to borrow in order to finance an expanded fleet. Ryder's debts were more than $400 million, four times shareholders' equity. Thus, Moody's Investors Service downgraded Ryder's rating on commercial paper in late 1974. Ryder System lost $20 million, and the company's investors were deeply concerned. The board of directors began to question James Ryder's ability to guide the future of the growing concern. The recession of 1973-74 had taken a heavy toll on Ryder's vast contract carriage and automotive carriage operations, which were heavily dependent upon the welfare of the automotive industry.

The financial situation was dire: four-to-one debt-to-equity, a credit downgrade, $20 million in losses, and subsidiaries requiring write-downs across multiple business lines. The diversification strategy had failed spectacularly.

The Boardroom Coup

Although Ryder's core business of truck leasing and rental was holding its own despite the hard times, company borrowing had gotten out of control. Stockholders, displeased with the company's troublesome acquisitions from the early 1970s, demanded a refocusing of attention back on Ryder's basic businesses. In 1975 James Ryder, under pressure from the boardroom and his bankers, announced that he was seeking a "more professional manager" to run the still growing company. In the summer of 1975, after disposing of such unprofitable subsidiaries as Toro Petroleum and Miller Trailers, Inc., as well as the major portion of the technical schools, James Ryder stepped down as head of the company he had founded. Ryder's successor was Leslie O. Barnes, former head of Allegheny Airlines. Barnes inherited a company that was tattered after weathering a great storm, and the 59-year-old CEO was intent on whipping Ryder System back into shape.

The forced departure of a founder is one of the most dramatic events in corporate governance. At 62 years old, after four decades of building his company, James Ryder was given "the title of chairman, a big office and no responsibilities. Most sexagenarians would have quietly accepted the sinecure, which carried a lifetime annual pension of $100,000."

But Jim Ryder was not most sexagenarians.

The Jartran Saga: Founder vs. Company He Built

The Comeback Attempt

But idleness was inconceivable to the scrappy Ryder, who still did 50 push-ups before breakfast, despised losing a badminton match and had a third wife 27 years his junior. Says he: "I'm sort of a rough person. I like rough things. Concrete, steel, debris, cast-iron pipes. I always liked working, and I just couldn't get used to working for somebody else, I guess." In 1978 Ryder decided to start up another firm to rival his own. Using $5 million of his own money and a fleet of trucks assembled on credit from Ford, Chrysler and Fruehauf, he launched Jartran (an acronym for James A. Ryder Transportation) in Coral Gables, Fla., under the noses of his former colleagues.

The name itself was a provocation: James A. Ryder TRANsportation. Giving up a $100,000 annual stipend to get out of his noncompetition agreement with Ryder System, James Ryder founded Jartran, which made a smashing entry into the field, building a 30,000 vehicle fleet in less than 18 months. James Ryder's new company became a thorn in the side of his former company. The feisty Ryder appeared in Jartran ads as "the man who invented truck rental," and his new vehicles resembled Ryder System's enough to spark a lawsuit.

The Legal Battle

Now the saga of Ryder vs. Ryder is heading into the courtroom. Ryder System last spring sued Jartran for stealing its trademark, logo and business methods. Both Ryder and Jartran trucks have two parallel, horizontal stripes across their sides and display the slogan RENT ONE WAY & LOCAL in similar designs.

The lawsuit alleged that James Ryder had deliberately designed Jartran's trucks to confuse customers—a remarkable claim given that he had created the original design language in the first place.

Jartran ads feature large pictures of James Ryder and tout him as "the man who invented truck rental." Moreover, Ryder contends that Jartran is raiding its personnel and that some 150 former Ryder employees work for the new company. Admits James Ryder: "Most of them have come on their own, but we went after some." Jartran has got into similar legal battles with another major competitor, U-Haul, which has charged it with running ads that make inaccurate and misleading price comparisons between the two companies. Jartran has fought back, alleging that U-Haul set "predatory" prices that were aimed at driving Jartran off the road. Protests Ryder: "We're offering good, clean competition. Ryder and U-Haul are trying to snuff us out before we get big."

The Collapse

For all his energy and market knowledge, James Ryder fell into the same trap twice. Nevertheless, Jartran had trouble making a profit. Once again, it appeared that James Ryder had grown the company too big too fast. As a downturn in the economy in 1979 killed the short-term rental market, Jartran cumulatively lost $30 million in 1979 and 1980. By July 1981 Jartran had dumped its commercial leasing division, and the company was foundering.

Ryder System, on the other hand, grew under the balanced leadership of Barnes and his new executive vice-president, M. Anthony Burns. The contrast was stark: professional management versus entrepreneurial instinct, disciplined capital allocation versus aggressive expansion.

The business lesson is sobering: the same traits that make founders successful—risk tolerance, willingness to move fast, conviction in their own judgment—can become liabilities as companies mature. Ryder System thrived under professional management precisely because it constrained the impulses that had nearly destroyed the company under its founder.

The 1980s Renaissance: Winning the U-Haul Battle

A Distracted Competitor

While Ryder System was professionalizing under Barnes and Burns, its main competitor in consumer truck rental was imploding from within. U-Haul started renting all kinds of equipment, from rototillers to hoists, and its truck fleet quietly grew old. In 1987 the average age of a U-Haul truck was ten years. Ryder's, on the other hand, averaged two years, and boasted all sorts of features not found at U-Haul, such as power steering, air-conditioning, AM-FM radios, fuel efficient engines, and radial tires.

The U-Haul family was locked in a bitter internal dispute over control of the business—a distraction that allowed Ryder to surge. Ryder's market share was 45 percent, equal to U-Haul's in 1987, and surging forward.

Disciplined Acquisitions

Between 1983 and 1987 Ryder System spent $1.1 billion on 65 acquisitions. This time the company's rapid expansion was readily digested. The difference from the 1970s was discipline: targets were selected for strategic fit, integration was planned carefully, and financial controls remained robust.

In 1985 Ryder entered the school-bus leasing business and quickly grew to be the second-largest private student transport company in the United States.

The company also expanded into aviation services. Ryder also entered the aviation leasing field with its purchase of Aviation Sales Co. and other companies in the early 1980s. By late 1986 aviation services accounted for 20 percent of the company's revenue. In 1988, just a few years after entering the field, Ryder was the world's largest jet engine overhaul and rebuilding company, the largest aviation parts distributor, and one of the largest engine and jet-engine leasing companies.

This diversification looked different from the 1970s debacle. Aviation services leveraged Ryder's core competency—maintaining complex mechanical assets and leasing them to operators who preferred to avoid ownership complexity. The logic was sound, even if the execution would prove challenging when the airline industry suffered in the early 1990s.

The Just-In-Time Revolution

Perhaps the most strategically significant development of the 1980s came in 1987, when Ryder Distribution Services implemented North America's first large-scale Just-In-Time supply delivery system supporting a new state-of-the-art auto plant in Kentucky. This was the future: not just leasing trucks, but orchestrating entire supply chains.

Key Inflection Point #1: The Yellow Truck Exit (1996)

The Counterintuitive Decision

In business strategy, few decisions are as counterintuitive as selling your most recognizable asset. Yet that's precisely what Ryder did in 1996.

No divestment was larger than the October 1996 sale of the company's consumer truck rental business, its famed yellow Ryder rental truck fleet. The sale of the consumer truck rental business represented a $574 million deal, stripping the company of more than $400 million in annual revenue.

Ryder System Inc. agreed to sell its most recognizable asset - the yellow consumer rental trucks - to a group of investors for $575 million. With a 33,000-truck fleet, Ryder has about 30 percent of the nation's consumer truck rentals. It generated about $547 million in revenue last year. The buyers, led by Southfield, Mich.-based investment group Questor Management Co., agreed to begin shifting to a new name after five years.

The yellow trucks were ubiquitous in American culture. They appeared in movies, TV shows, and the collective memory of anyone who had ever moved. Selling them felt like abandoning the company's heritage.

The Strategic Logic

But CEO Tony Burns saw the situation differently. With the divestiture of the consumer truck rental business and the automotive carrier business, Burns felt his company was "leaner, more focused, more disciplined, more profit-minded," and less vulnerable to the vagaries of capricious market conditions, ridding Ryder of businesses that were "seasonal, transactional, highly volatile, and in difficult markets." With these two business segments gone, along with others, Burns pinned the company's hopes for the future on three main business areas: logistics, corporate truck leasing and rental, and public transportation services. As Ryder entered the late 1990s, the company could not point to strong, tangible evidence that its "new" operating structure would provide all the answers for the new century ahead—and it did not expect to.

The consumer rental business had several structural problems: - Seasonality: Moving activity peaks in summer, creating boom-bust cycles - Price sensitivity: Consumers shop aggressively on price, compressing margins - Asset intensity without pricing power: You need lots of trucks, but can't charge premium prices - One-time transactions: Each rental is a discrete event; no ongoing relationship

Contrast this with the commercial B2B business: - Contractual relationships: Multi-year leases create predictable revenue - Maintenance as a profit center: Ryder maintains the trucks, creating recurring service revenue - Customer switching costs: Once a fleet is integrated into a customer's operations, switching is disruptive - Less price sensitivity: Businesses value reliability over the lowest price

The 1996 sale of the well-known consumer truck rental division was pivotal. It allowed Ryder to concentrate resources exclusively on the higher-margin B2B market, including fleet management, dedicated transport, and complex supply chain solutions, shaping its current identity.

In 1996, Ryder decided to focus on commercial truck rental and leasing, and exited the "one-way" consumer truck rental business; which was purchased by equity firm Questor Partners Fund LP, who later sold it to Budget Truck Rental in June 1998.

The lesson for investors: sometimes the highest-profile business is not the highest-quality business. Brand recognition and competitive advantage are different things.

The 2000s: Divestitures & Focus

Leadership Transition

The late 1990s and early 2000s brought continued refinement of Ryder's portfolio. In 1999, the company sold Ryder Public Transportation Services. M. Anthony Burns retired as CEO, and Gregory T. Swienton was named President and CEO.

In 2001, Ryder launched Asia-Pacific headquarters with the acquisition of Singapore-based Ascent Logistics Pte Ltd.—a brief experiment with international expansion that would later be largely unwound. In 2002, Burns retired as Chairman, and Swienton added the chairman role to his responsibilities.

Building the Three-Segment Model

During this period, Ryder crystallized its modern operating structure around three business segments:

- Fleet Management Solutions (FMS): Full-service truck leasing, commercial rental, and maintenance services

- Supply Chain Solutions (SCS): Warehousing, distribution, transportation management, and logistics

- Dedicated Transportation Solutions (DTS): Providing vehicles, drivers, and management as an integrated service

This structure would prove remarkably durable, remaining essentially unchanged through 2025. Each segment has distinct economics:

- FMS is asset-heavy with high capital requirements but generates steady lease revenue and maintenance income

- SCS is more asset-light, requiring warehouses and technology but not necessarily truck ownership

- DTS combines assets (trucks) with labor (drivers) in a bundled offering

The strategic value lies in the connections between segments. A customer might start with truck leasing, add dedicated drivers, and eventually outsource their entire supply chain operation. The maintenance network that supports FMS also services DTS vehicles. Technology platforms span all three segments.

Key Inflection Point #2: The "Balanced Growth Strategy" Transformation (2012–Present)

The Board Question That Changed Everything

Robert Sanchez was named CEO in January 2013, becoming only the fourth CEO in the company's 80-year history. Sanchez has been CEO of the transportation and supply chain management company since 2013, and when he got the job he brought with him two decades of experience in finance, technology, and operations. Five short months after being named CEO, he became board chair in May 2013.

Robert E. Sanchez is chairman and chief executive officer of Ryder System, Inc. (NYSE: R), a leading supply chain, dedicated transportation, and commercial fleet management solutions company. He was named CEO in January 2013 and chairman of the board in May 2013. Over the course of more than 30 years at Ryder, Mr. Sanchez has held many senior executive leadership positions including president and chief operating officer, chief financial officer, president of Fleet Management Solutions, chief information officer, SVP of transportation management, and VP of asset management. He has been a member of the company's executive leadership team since 2003.

The transformative strategic insight came from an unexpected source. A question about market share triggered a major aha moment for the leader of one of the largest trucking fleets in North America. It was at an annual strategy session, Sanchez told Fortune, that one of the most illuminating moments emerged. Sanchez and the other senior executives were talking about market share in the truck leasing and rental business known as Fleet Management Solutions, while the board members listened. At the time, Ryder held 35% to 40% of the truck leasing market segment—nothing to sneeze at. And then one board member from a completely different industry raised his hand to ask a question that would ultimately become a hugely pivotal moment for Sanchez and his team and Ryder.

"Does that mean that 40% of the trucks that are on the road are from Ryder?" the director asked. "And I said, 'Well, no, of course not,'" Sanchez recalled. "Then he goes, 'Why is that? What do all the other truck owners do? Are they leasing from somebody else? Are they getting dedicated service from somebody else?'"

For context, the leasing market at the time was only 15% to 20% of all the trucks on the road. Meaning, 80% to 85% purchased and maintained their own trucks. So the big takeaway was really about why Ryder wasn't going after that truck ownership market—the 80% to 85%. So for a full year afterward, Sanchez and his team strategized how to chip away at all the companies that don't lease trucks from Ryder or any of its competitors, nor outsource transportation to them. "We realized that a large percentage of the market is do-it-yourselfers," said Ryder. "So our strategy over the last probably 12 to 13 years has been chipping away at the do-it-yourself market when it comes to trucking and transportation." The independent director who asked the question? His background is in office supplies and has nothing to do with trucking. But he asked the question that crystallized a strategic insight that helped push more than a decade of execution.

Technology Investments

The balanced growth strategy required technology investments to reach "do-it-yourselfers" with compelling value propositions:

Launched in April 2018, the company operates a peer-to-peer truck-sharing platform, COOP, that allows owners of commercial vehicles to rent unused trucks and trailers to businesses. The program expanded to Florida in January 2019 and further expanded in Texas in February 2020. COOP by Ryder expanded fleet management services and bulk rentals nationwide in 2022.

In May 2018, Ryder introduced RyderGyde™, a smartphone app for drivers and fleet managers to monitor and manage their fleets. In May 2020, RyderShare was introduced as a collaborative logistics platform.

Electric Vehicle Push

The company began positioning for transportation's electrification: In November 2018, Ryder ordered 1,000 electric trucks to add to their fleet.

During the Advanced Clean Transportation (ACT) Expo, Ryder introduces new turnkey solution, RyderElectric+™, with EV advisory, vehicle lease, charging, telematics, and maintenance services. Ryder System, Inc. (NYSE: R), a leader in supply chain, dedicated transportation, and fleet management solutions, today unveils RyderElectric+™ as its new turnkey electric vehicle (EV) fleet solution. The new offering navigates the EV landscape for customers and provides electrification advisors, vehicles, charging, telematics, and maintenance all for one price. During ACT Expo in Anaheim, Calif., Ryder will introduce RyderElectric+ at its exhibit.

Ryder is expanding its electric vehicle offerings, including recently announced plans to introduce 4,000 BrightDrop Zevo 600 and Zevo 400 electric vans to its lease and rental fleet through 2025. Ryder offers a range of electric vehicles for lease, include Ford E-Transit vans, Navistar's International eMV Series trucks, Lonestar EVs with Dana's electric powertrain, and Freightliner's MT50e vans, medium-duty eM2 and heavy-duty eCascadia. Ryder said it also has reserved Tesla Semi tractors and continues to partner with multiple vehicle manufacturers to offer new EV options to its customers.

Key Inflection Point #3: E-Commerce & The Whiplash Acquisition (2021–2022)

The E-Commerce Imperative

The COVID-19 pandemic accelerated e-commerce adoption dramatically. As Ryder executives observed, e-commerce growth had been averaging 12% per year prior to the pandemic—already healthy but not transformational. During 2020-2021, that growth rate spiked to approximately 30%.

For a supply chain company, e-commerce presents both opportunity and challenge. The opportunity: vast new volumes of goods need to be stored, picked, packed, and shipped. The challenge: e-commerce fulfillment is operationally more complex than traditional B2B distribution, requiring different warehouse layouts, technology systems, and transportation networks.

The Whiplash Deal

Ryder System, Inc. (NYSE: R), a leader in supply chain, dedicated transportation, and fleet management solutions, announces it has entered into a definitive agreement to acquire Whiplash, a leading national provider of omnichannel fulfillment and logistics services, for approximately $480 million in cash. Based in City of Industry, Calif., Whiplash provides scalable e-commerce and omnichannel fulfillment solutions to an impressive roster of more than 250 brands. The company's 19 dedicated and multi-client warehouses total nearly seven million square feet and provide access to key port operations and gateway markets. The transaction is accretive to shareholders and is expected to add approximately $480 million in gross revenue to Ryder's supply chain solutions business segment in 2022 and provide incremental growth to Ryder's earnings in 2022.

Ryder completed the Whiplash transaction on Jan. 1, 2022 for approximately $480 million in cash. It is accretive to shareholders and is expected to add approximately $480 million in gross revenue to Ryder's supply chain solutions business segment. Ryder completes acquisitions of Whiplash and Midwest Warehouse & Distribution System to accelerate growth in Ryder's higher-return supply chain solutions business. The deals expand Ryder's e-commerce fulfillment network, add a proven e-commerce technology and operating platform, and add multi-client warehousing capabilities to the 3PL's end-to-end supply chain offerings.

"With the expanded footprint following the acquisition, Ryder's e-commerce and omnichannel fulfillment solution is expected to be able to deliver to 100% of the U.S. within two days and 60% of the U.S. within one day."

Continued Acquisitions

The e-commerce build-out continued with additional deals:

In November 2023, Ryder completed the acquisition of Impact Fulfillment Services ("IFS"), which added contract packaging and contract manufacturing to its SCS service offerings and expanded its warehousing business.

Ryder System, Inc. (NYSE: R), a leader in supply chain, dedicated transportation, and fleet management solutions, announces it has acquired Cardinal Logistics (Cardinal), enabling growth and further strengthening Ryder's position as a leading customized dedicated contract carrier in North America. Based in Concord, N.C., Cardinal predominantly provides dedicated fleets and professional drivers to service complex route structures across distribution centers, suppliers, and stores, as well as complementary freight brokerage services; and, to a lesser extent, last-mile delivery and contract logistics services.

Ryder System acquired Cardinal Logistics, significantly expanding its dedicated transportation services (DTS). The acquisition price was undisclosed, but Cardinal Logistics had approximately $1.1 billion in revenue in 2022, compared to Ryder's DTS revenue of $1.786 billion in the same year.

Ryder System, Inc. acquired Cardinal Logistics Management Corporation from H.I.G. Capital, LLC for $290 million on February 1, 2024.

Both started their logistics career at Ryder in the 1980s and early 1990s. The statement described Cardinal's activities as primarily being focused on "consumer packaged goods, omnichannel, grocery, building products, automotive, and industrial verticals."

The acquisition was expected to add about $1 billion in revenue and $800 million in operating revenue annually.

The Modern Business Model Deep Dive

Three Segments, One System

Ryder System, Inc. operates as a logistics and transportation company worldwide. It operates through three segments: Fleet Management Solutions (FMS), Supply Chain Solutions (SCS), and Dedicated Transportation Solutions (DTS).

Ryder's fleet management business is its largest business segment. This arm of the business does contract-based full-service leasing, contract maintenance, commercial rental and fleet support services. Under full-service leasing Ryder owns and maintains the trucks and the customer determines the destination.

The company operates a massive physical infrastructure: Ryder provides services throughout the United States, Mexico, and Canada. In addition, Ryder manages nearly 260,000 commercial vehicles and operates approximately 300 warehouses encompassing more than 95 million square feet.

The Revenue Mix Transformation

The strategic transformation Sanchez initiated is visible in the revenue mix. "In 2024, a year we believe will represent trough freight cycle conditions, our transformed business model generated meaningfully higher earnings and returns than it did during the 2018 peak. Through organic growth, strategic acquisitions and innovative technology, we have shifted our revenue mix towards supply chain and dedicated with 61% of 2024 revenue coming from these asset-light businesses compared to 44% in 2018."

This shift matters enormously for earnings stability and valuation:

- FMS is cyclical, tied to used vehicle prices, rental utilization, and lease sales activity

- SCS and DTS are more contractual, with longer customer relationships and more predictable revenue

- Asset-light SCS generates higher returns on capital than asset-heavy FMS

The Maintenance Network Effect

One of Ryder's least appreciated competitive advantages is its maintenance network. With approximately 800 maintenance facilities across North America and 5,000 technicians, Ryder has built what amounts to a healthcare system for commercial trucks.

This network creates multiple forms of value: - Switching costs: Once a customer's fleet is integrated with Ryder's maintenance system, switching providers is disruptive - Data advantages: Ryder accumulates maintenance data across its fleet, enabling better predictive maintenance - Utilization of fixed costs: Each maintenance facility can service multiple customers, spreading fixed costs - Competitive barrier: Replicating this network would require billions in capital and years of execution

Current Performance & Outlook

2024 Results

Ryder System annual revenue for 2024 was $12.636B, a 7.24% increase from 2023.

For the full year, Ryder reported net income of $489 million, $11.06, on revenue of $12.6 billion, compared with net income of $406 million, $8.73, on revenue of $11.8 billion in 2023.

"These results were driven by double-digit earnings growth in each of the segments, reflecting the strength of our contractual lease, supply chain, and dedicated businesses. Our ability to generate ROE of 16% during this extended freight cycle downturn continues to demonstrate consistent execution and the resilience of our transformed business model."

Capital Allocation

Debt-to-equity as of December 31, 2024 was 250%, compared to 232% at year-end 2023, and is at the bottom end of the company's long-term target of 250% to 300%. "We expect the positive momentum in our contractual businesses to continue into 2025, contributing to higher earnings in all business segments," says Ryder Chief Financial Officer Cristina Gallo-Aquino. "The high end of our 2025 forecast range assumes continued contractual earnings growth and a very modest improvement in rental demand later in the year. We remain well-positioned to benefit from a cycle upturn in all our business segments and are confident that secular growth trends continue to support long-term revenue and earnings growth."

Full year capital expenditures decreased to $2.7 billion in 2024 compared to $3.3 billion in 2023, primarily reflecting reduced investments in the ChoiceLease fleet due to lower sales activity. Full year net cash provided by operating activities from continuing operations was $2.3 billion compared to $2.4 billion in 2023.

Shareholder Returns

An InvestingPro Tip highlights that Ryder "has maintained dividend payments for 49 consecutive years." This streak speaks to the durability of the business model across multiple economic cycles.

Stock Performance

The latest closing stock price for Ryder System as of December 04, 2025 is 180.01. The all-time high Ryder System stock closing price was 193.18 on October 06, 2025. The Ryder System 52-week high stock price is 195.48.

Management provided full-year 2025 EPS guidance of $12.85-$13.05, projecting growth from contractual earnings, strategic initiatives, and a potential freight market recovery. CEO Robert Sanchez expressed confidence in Ryder's 'cycle-tested business model.'

Competitive Landscape & Business Model Analysis

Direct Competitors

Direct competitors offer similar services, such as truck leasing, fleet management, and supply chain solutions. These companies compete directly with Ryder's core business segments. Key players include J.B. Hunt Transport, Penske Truck Leasing, and Schneider National.

J.B. Hunt Transport offers a broad range of transportation and logistics services, directly competing with Ryder's Dedicated Transportation Solutions (DTS) and Supply Chain Solutions (SCS) segments. Penske Truck Leasing provides full-service truck leasing, rental, and contract maintenance, posing a direct threat in the Fleet Management Solutions segment.

According to industry reports, Ryder holds approximately 25% market share in the U.S. full-service truck leasing market, positioning it as one of the market leaders alongside Penske. In the broader third-party logistics (3PL) market, Ryder is among the top 10 providers in North America, though it faces intense competition from larger global players like DHL Supply Chain, XPO, and C.H. Robinson.

Porter's Five Forces Analysis

Supplier Power (Moderate): Ryder purchases trucks from major OEMs like Freightliner, Navistar, and PACCAR. While these suppliers have market power, Ryder's scale provides meaningful purchasing leverage. The bigger constraint is supply availability during periods of OEM production constraints.

Buyer Power (Moderate to Low): Large customers have negotiating leverage, but switching costs are significant. Integrating a new fleet management provider requires operational disruption, systems integration, and often capital investment.

Threat of New Entrants (Low): The maintenance network alone represents billions in capital investment. New entrants would need to build facilities, hire technicians, develop technology systems, and establish customer relationships—a multi-year, capital-intensive process.

Threat of Substitutes (Moderate): The "do-it-yourself" market—companies that own and maintain their own fleets—represents the primary substitute. Ryder's strategy specifically targets converting these DIY operators to outsourced solutions.

Competitive Rivalry (High): Competition is intense, particularly in SCS and DTS where asset-light competitors can enter more easily. Price competition pressures margins, though Ryder's integrated offering provides differentiation.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Ryder benefits from scale in maintenance (spreading fixed costs across more vehicles), purchasing (better OEM pricing), and technology (amortizing development costs across larger revenue base). However, competitors Penske and J.B. Hunt also have meaningful scale.

Network Effects: Limited direct network effects, though the COOP peer-to-peer platform attempts to create a network-driven business.

Counter-Positioning: Ryder's integrated, full-service model represents counter-positioning against pure-play competitors. An asset-light 3PL would struggle to replicate the maintenance network; a pure leasing company lacks supply chain capabilities.

Switching Costs: Meaningful switching costs exist in FMS (vehicle integration, maintenance systems) and DTS (driver relationships, operational integration). SCS has lower switching costs given more competitive 3PL market.

Branding: Limited consumer brand value after the yellow truck sale, but strong B2B reputation for reliability.

Cornered Resource: The maintenance network of 800+ facilities and 5,000 technicians represents a resource that would take years and billions to replicate.

Process Power: Decades of operational experience in fleet management and maintenance create process advantages that are difficult to observe and replicate.

Key Risks

Freight Cycle Volatility: Despite the transformation, Ryder remains exposed to freight market conditions through rental utilization and used vehicle prices.

Used Vehicle Residual Values: Ryder owns its fleet and records residual value estimates. If used truck prices decline faster than expected, impairment charges could affect earnings.

Technology Disruption: Autonomous vehicles could fundamentally change the economics of trucking. Ryder's investments in EV technology position it for one transition but not necessarily for autonomy.

Driver Shortages: CEO Robert Sanchez noted "challenges from new CDL regulations that may reduce the driver market by 5%." DTS requires professional drivers; shortages constrain growth and increase labor costs.

Debt Load: Debt-to-equity as of December 31, 2024 was 250%. While within target range, high leverage increases sensitivity to interest rates and limits financial flexibility during downturns.

Playbook: Business & Investment Lessons

Lesson 1: The Power of Strategic Focus

Selling the yellow trucks in 1996 looked like brand suicide. It proved to be strategic clarity. By exiting a consumer business with challenging economics—seasonality, price sensitivity, one-time transactions—Ryder could concentrate on B2B markets with better characteristics: contractual relationships, switching costs, and maintenance as a profit center.

The lesson applies broadly: brand recognition and competitive advantage are different things. Sometimes the highest-profile business is a strategic distraction.

Lesson 2: Asset-Heavy vs. Asset-Light Tradeoffs

Owning 260,000 trucks creates both moat and burden. The moat: competitors can't easily replicate the fleet and maintenance network. The burden: capital intensity, depreciation, residual value risk, and cyclicality.

Ryder's transformation balanced these tradeoffs by shifting mix toward asset-light SCS and DTS revenues while maintaining the asset-heavy FMS base. The result: more stable earnings with continued competitive differentiation.

Lesson 3: The Maintenance Network Effect

800 facilities and 5,000 technicians represent a "cornered resource" that would take years and billions to replicate. This infrastructure supports all three business segments and creates meaningful switching costs for customers.

For investors analyzing any asset-heavy business, the question is: does ownership of assets create defensible competitive advantage, or just capital requirements? Ryder's maintenance network is a positive example.

Lesson 4: Converting "Do-It-Yourselfers"

The insight triggered by the board member's question—that 80-85% of trucks are owned rather than leased—revealed a massive addressable market. Rather than fighting for share in the 15-20% leasing market, Ryder could grow by converting DIY operators.

This requires understanding why customers do things themselves: cost, control, customization. Then addressing those concerns with compelling value propositions: predictable costs, technology integration, expertise leverage.

Key KPIs to Track

For ongoing monitoring of Ryder's business, two metrics matter most:

-

SCS/DTS Revenue Mix: The percentage of revenue from contractual businesses (SCS + DTS) versus cyclical FMS. Higher is better for earnings stability. Currently at 61% versus 44% in 2018.

-

Return on Equity Through the Cycle: ROE during trough conditions reveals the true earnings power of the transformed model. Ryder targets "high-teens" ROE; 16% during 2024's freight downturn demonstrates resilience.

Secondary metrics include rental utilization (75%+ indicates healthy demand), used vehicle pricing trends (affects residual values), and free cash flow generation.

Conclusion: The Quiet Revolution

James Ryder never could have imagined what his $35 truck purchase would become. He invented an industry, built an empire, lost control of it, tried to compete against his own creation, and watched it transform into something entirely different from his original vision.

Today's Ryder System operates behind the scenes—maintaining the trucks that deliver your packages, managing the warehouses that store retail inventory, providing the drivers that keep supply chains flowing. The yellow trucks that once defined the brand are gone, operated by Budget under a different name. What remains is something less visible but arguably more valuable: a technology-enabled infrastructure provider essential to modern commerce.

The company's transformation offers lessons that extend beyond trucking. Focus beats diversification. Maintenance networks create switching costs. Contractual relationships provide stability. Asset ownership can be a source of competitive advantage rather than just capital burden—if managed properly.

Ryder System, Inc. is a leading supply chain, dedicated transportation, and fleet management solutions company. Ryder's stock (NYSE: R) is a component of the Dow Jones Transportation Average and the S&P MidCap 400® index.

Ninety-two years after a young man used his last dollars to buy a truck in Miami, Ryder System endures—transformed beyond recognition, yet still fundamentally in the business of making transportation work for customers who would rather not do it themselves. In an era obsessed with software and disruption, that's a quietly revolutionary value proposition.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube