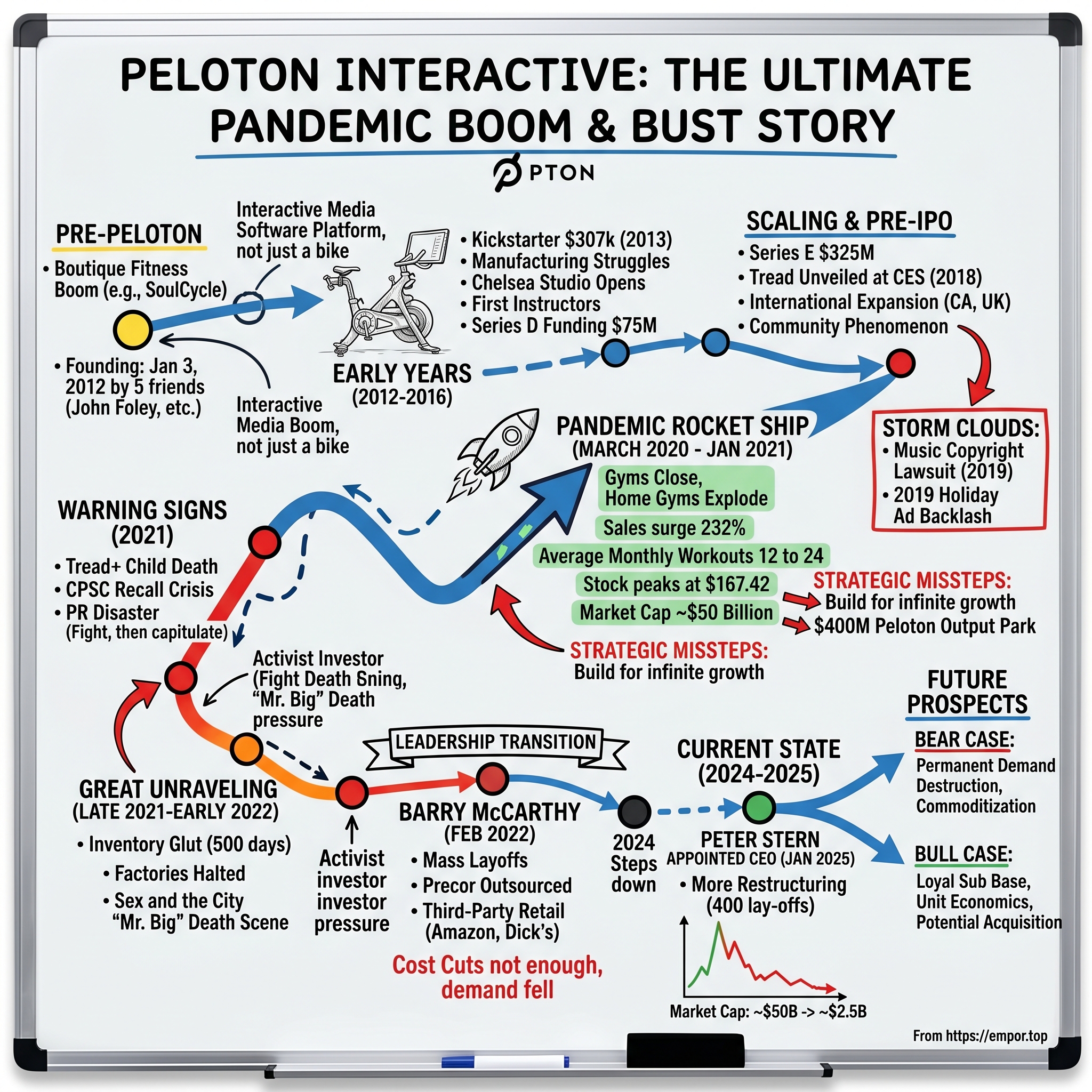

Peloton Interactive: The Ultimate Pandemic Boom & Bust Story

I. Introduction & Episode Roadmap

Picture the scene: January 2021. A Manhattan apartment overlooking Central Park. The early morning sun streams through floor-to-ceiling windows, illuminating a sleek black Peloton bike. On the attached screen, instructor Cody Rigsby counts down the final seconds of a 45-minute ride. "Three, two, one—you did it, Peloton family!" The rider, a hedge fund manager who hasn't set foot in his Midtown office in ten months, high-fives the screen. His Peloton stock holdings, purchased at $29 during the IPO, are now worth nearly six times that amount. Life is good.

Fast forward to today, November 2025. That same bike sits in the corner, draped with yesterday's dry cleaning. As of March 2025, Peloton's valuation is approximately $2.5 billion, a staggering 95% decline from its market cap of almost $50 billion at the January 2021 peak. The hedge fund manager? He sold his shares at a loss months ago.

This is the Peloton story—a tale of visionary ambition, pandemic-fueled euphoria, and one of the most dramatic corporate collapses in recent memory. It's a story about what happens when a company builds for a future that never arrives, when temporary tailwinds are mistaken for permanent transformation, and when the music—quite literally—stops.

Over the next three hours, we'll trace Peloton's journey from a Kickstarter campaign that raised $307,332 to becoming the ultimate symbol of pandemic excess. We'll examine how five friends transformed boutique fitness into a tech phenomenon, how they navigated—and often bungled—critical moments that would define their legacy, and what their rise and fall teaches us about building consumer hardware companies in the 21st century.

The central question isn't just how Peloton rose so high or fell so far. It's whether this was destiny or choice—whether the seeds of destruction were planted in the founding DNA or if different decisions could have led to a different outcome. Along the way, we'll uncover the strategic missteps, operational challenges, and market forces that transformed a category-defining company into a cautionary tale.

Buckle up. Or rather, clip in. This ride is going to be intense.

II. The Pre-Peloton Era: Context & Founding

The rain was coming down in sheets that day in 2011 when John Foley, then serving as president at Barnes & Noble, found himself stuck in Manhattan traffic. A devoted cyclist who'd competed in triathlons, Foley had recently discovered the intoxicating energy of boutique fitness studios—his wife Jill and he enjoyed going to boutique studio fitness classes, but with an increasingly busy work schedule and two young children, they found that they were struggling to work out as much as they wanted. The problem wasn't motivation; it was logistics.

Boutique fitness was having a moment. SoulCycle, founded in 2006, had transformed indoor cycling from a gym afterthought into a quasi-religious experience. Instructors weren't just fitness coaches—they were motivational gurus, DJs, and therapists rolled into one. Classes at $35 a pop were selling out within minutes. Barry's Bootcamp was applying the same formula to strength training. Flywheel was adding a competitive element with real-time leaderboards.

But for every devotee who managed to snag a 6 AM bike, there were dozens locked out. The economics of boutique fitness were brutal: real estate costs in prime urban locations, capacity constraints of 30-60 bikes per studio, and the impossibility of scaling charismatic instructors. It was a business model that worked brilliantly for a select few in specific zip codes but left millions of potential customers unserved.

When John Foley had an idea for an interactive fitness company, he presented this idea to four of his friends: Tom Cortese, Graham Stanton, Hisao Kushi, and Yong Feng. Together the five of them founded Peloton on January 3, 2012.

The founding team was a fascinating mix of experience and expertise. Tom Cortese, a competitive triathlete, an outdoor runner, and cyclist, would become COO and drive product development. Hisao Kushi brought legal and financial acumen that would prove crucial in navigating the complex world of music licensing and venture funding. Yony Feng hadn't taken an indoor cycling class before John took him to a Flywheel class—one of the hardest workouts that captivated him with the dark room and energetic music. So, he packed up all his stuff and moved across the country from California to New York. Graham Stanton would handle operations and marketing before eventually departing the company.

Kushi had a vivid memory of John describing his idea: "I don't get this. You're talking about a stationary bike in your basement with, like, a screen where you have classes?" Two days later the light bulb went off: "This is not about the bike. This is about the media. This is an interactive media software platform."

The company raised $400,000 in seed money in February 2012 and another $3.5 million in December 2012 through a Series A funding round. The early investors were taking a massive leap of faith. As Foley would later recall, In the plans that he pitched to investors, he said, 'I am going to take over the world' and for the first three years, they said, 'Sure you are, no thanks.'

What distinguished Peloton's vision from the beginning was its refusal to choose sides in the hardware-software debate. They weren't building a better stationary bike and they weren't creating a fitness app. They were building an integrated experience where the hardware, software, content, and community would be so tightly woven together that competitors couldn't simply copy one element and succeed.

III. Building the Machine: Early Years (2012-2016)

The first Peloton prototype was, to put it charitably, a disaster. Cobbled together in a garage with off-the-shelf parts and duct tape, it looked more like a science fair project than the future of fitness. But it had one crucial element: a tablet mounted where traditional bikes had basic metrics displays. That tablet changed everything.

In 2013, Peloton launched a Kickstarter campaign that raised $307,332 from 297 backers, surpassing their $250,000 goal. After creating a prototype, Peloton sold its first bike on Kickstarter in 2013, pitching an "early bird special" price tag of $1,500. The campaign video featured Foley himself, earnestly explaining how Peloton would bring the energy of studio cycling into your home. In the Kickstarter campaign, Foley compared Peloton to Apple Inc., saying it was "creating both the hardware and the software" to deliver a superior product.

Manufacturing the first bikes nearly killed the company. With no experience in hardware production and limited capital, every component had to be sourced, tested, and integrated. In April 2014, Peloton received $10.5 million in a Series B funding round—money that would prove crucial for solving their production challenges.

Tom Cortese remembers Black Friday 2013 at the Short Hills mall in New Jersey, which was supposed to be a pop-up store: "We had the first six bikes we ever made. The only six bikes we had ever made. We were standing there when people started coming in. By the end of the day, we sold four to six bikes. We went out and celebrated like it was a million bikes. I remember thinking, 'Holy shit, people get it. We've got a business.'"

That same year, the Peloton studio opened in Manhattan's Chelsea neighborhood, allowing spin instructors to record their classes. The studio was more than just a production facility—it was Peloton's spiritual home, the place where the magic happened. The first studio was in the back of an office where the staff hung black curtains and propped up the instructor bike with bricks.

The search for instructors was its own adventure. How did Jenn Sherman become the first Peloton trainer? She sent an email to [email protected]. Tom Cortese likes to pull up the email for dramatic readings because she's crude in it—cursing and saying something about her booty. But what came through was someone with a ton of personality capable of putting it on display.

The company raised $30 million in a Series C funding in 2015. At the end of 2015, the company scored another $75 million in Series D funding to expand its software engineering team. The capital allowed Peloton to solve a crucial challenge: how to deliver live classes with minimal latency while maintaining video quality that wouldn't make riders seasick.

By 2016, the content-hardware-subscription flywheel was gaining momentum. Members weren't just buying a bike; they were joining a movement. The monthly subscription of $39 seemed steep compared to streaming services, but Peloton members weren't comparing it to Netflix—they were comparing it to SoulCycle classes at $35 each. Two classes a month and you were already ahead.

The metrics were promising. Retention rates hovered above 95%, practically unheard of in fitness. Members were working out more frequently over time, not less—a complete inversion of typical gym behavior. Word-of-mouth was so strong that customer acquisition costs remained manageable despite minimal traditional advertising.

But success brought scrutiny. Music publishers began to notice that Peloton was using popular songs in its classes without proper licensing. The company's cavalier attitude toward intellectual property would come back to haunt them. For now, though, momentum was building. In 2016, the budding fitness company generated $60 million in revenue and more than doubled it to $170 million in 2017.

IV. Scaling & The Pre-IPO Years (2017-2019)

2017 marked Peloton's transformation from scrappy startup to unicorn. The company secured its Series E round of $325 million in 2017, achieving a valuation north of $1 billion. The funding would fuel ambitious expansion plans that would either establish Peloton as a global fitness powerhouse or stretch the company beyond its capabilities.

The crown jewel of this expansion was the Tread. Unveiled at the Consumer Electronics Show (CES) in Las Vegas from January 9-12, 2018, the state-of-the-art new technology and fitness platform would allow Peloton Members to participate in live and on-demand bootcamp and circuit classes from the convenience of their own homes. The Tread (later renamed Tread+) was everything the bike was and more—a massive, tank-like machine with a 32-inch HD touchscreen and a slatted belt design borrowed from high-end commercial treadmills.

At $4,295, the Tread was priced like a luxury car down payment. "Treadmills are generally pieces of hardware people don't like," Peloton CEO John Foley told CNN Tech. He believed Peloton could change that by making the treadmill about more than just running—incorporating floor exercises, weights, and bootcamp-style workouts.

International expansion followed swiftly. In May 2018, Peloton announced plans to expand into Canada and the United Kingdom that fall. The move required not just shipping bikes overseas but establishing local studios, hiring country-specific instructors, and navigating different regulatory environments. It was a massive operational undertaking that would test Peloton's execution capabilities.

Meanwhile, the Peloton community was becoming a cultural phenomenon. Facebook groups with tens of thousands of members dissected every ride, celebrated personal records, and developed parasocial relationships with instructors. The "Peloton Mom" became a recognizable archetype—affluent, suburban, devoted to her morning rides with Robin Arzón or afternoon arms sessions with Tunde Oyeneyin.

But storm clouds were gathering. In March 2019, Peloton was sued by the National Music Publishers Association for using copyrighted music in their videos without proper synchronization licenses, seeking $150 million in damages. The action resulted in changes to music used in its sessions, as well as removal of certain programs. The lawsuit would eventually be settled in February 2020, but it highlighted a concerning pattern of Peloton moving fast and breaking things—including laws.

Then came the advertising disaster that would preview Peloton's struggles with public perception. In 2019, Peloton's market value fell by almost 9% or $1.5 billion following widespread outrage over its holiday ad titled The Gift That Gives Back. The commercial featured a woman receiving the Peloton bike for Christmas who, looking timid in a selfie video, tells the camera, "First ride. I'm nervous, but excited." The ad shows the woman pedaling furiously on the bike in her spacious apartment at 6 a.m. for five days in a row and concludes with her watching her yearlong video diary with her husband. "A year ago, I didn't realize how much this would change me," she says.

The backlash was swift and brutal. Critics called it sexist, dystopian, and emblematic of toxic fitness culture. "Honestly, I think it was just my face," said actress Monica Ruiz, saying her expression looked fearful. "My eyebrows look, like, worried, I guess." Ryan Reynolds capitalized on the controversy with a brilliant Aviation Gin commercial featuring the same actress, drowning her sorrows in martinis.

The Peloton company responded by saying, "While we're disappointed in how some have misinterpreted this commercial, we are encouraged by, and grateful for, the outpouring of support we've received from those who understand what we were trying to communicate." The defensive response only made things worse, showing a company that couldn't read the room—a troubling sign for a brand built on community and connection.

V. The IPO & Public Company Era (September 2019)

The morning of September 26, 2019, should have been John Foley's triumph. Standing outside the Nasdaq in Times Square, surrounded by instructors and employees wearing matching Peloton gear, he prepared to ring the opening bell. Peloton (ticker symbol: PTON) became a public company via an initial public offering, raising $1.16 billion and valuing the company at $8.1 billion.

But the market had other plans. The opening trade was $27 per share, below its IPO pricing of $29 per share, which was at the high end of expectations. By day's end, shares had tumbled 11%, making it one of the worst unicorn debuts of the year. The company that had captured imaginations was struggling to capture investor confidence.

The prospectus revealed uncomfortable truths. In the company's disclosures released before the IPO, Peloton indicated that it had not yet turned an annual profit. Its 2019 net loss widened to $245.7 million, from a net loss of $47.9 million in the prior year. Customer acquisition costs were rising. The company was burning cash to fuel growth, betting that scale would eventually deliver profitability.

Wall Street analysts were divided. Bulls saw a subscription business with incredible retention metrics and a massive total addressable market. At a time when many companies aspire to the Netflix model of subscription membership, the company boasts 1.4 million members, which it defines as an individual with a Peloton account. Bears saw a hardware company with subscription aspirations, facing inevitable competition from deep-pocketed tech giants.

The business model debate was crucial. Hardware companies trade at lower multiples than software companies. Peloton insisted it was a technology platform, not an exercise equipment manufacturer. The bike and treadmill were just "delivery mechanisms" for the real product: the content and community. But with 80% of revenue still coming from hardware sales, investors remained skeptical.

Behind the scenes, the IPO process had been bruising. Venture capitalists who'd backed Peloton early were sitting on massive paper gains, but the dual-class share structure meant Foley and other insiders retained voting control. Peloton filed with a dual-class share structure, presumably to retain more control over the company, but this certainly deterred many investors that, as a rule, do not invest in this stock structure.

The lock-up period would expire in March 2020, allowing insiders to sell. Nobody could have predicted what would happen next. Within six months, a virus spreading in Wuhan, China, would transform Peloton from a niche luxury product into something approaching a necessity. The company struggling to justify its valuation would soon struggle to keep up with demand.

VI. The Pandemic Rocket Ship (March 2020 - January 2021)

March 15, 2020. Governor Andrew Cuomo announces New York State is shutting down. Gyms, fitness studios, and sports facilities must close immediately. Within days, similar orders cascade across the country. SoulCycle bikes sit empty. Barry's Bootcamp falls silent. Millions of Americans stare at their suddenly useless gym memberships and wonder: "Now what?"

For Peloton, the pandemic was like strapping a rocket to an already accelerating train. Sales increased significantly during the COVID-19 pandemic as home gyms became more popular during the COVID-19 lockdowns. The company that had spent years evangelizing home fitness suddenly found itself in a world where home fitness was the only option.

The numbers were staggering. In November 2020, Peloton said its sales surged 232% to $757.9 million compared with the prior-year period. Wait times for bikes stretched to 10 weeks, then 12, then 16. Customers who'd never considered spending $2,000 on exercise equipment were placing orders sight unseen. The secondary market exploded—used Pelotons sold for above retail price.

At the end of June 2020, Peloton had 1.09 million subscribers, 113 percent over the previous year. But the real story was engagement. Members were riding daily, sometimes multiple times per day. Average monthly workouts increased from 12 to 20 to 24. The leaderboard became a proxy for social connection in a socially distanced world.

Instructors became lockdown celebrities. Cody Rigsby's Broadway-themed rides offered escape. Robin Arzón's motivational mantras provided structure. Alex Toussaint's Club Bangers brought the party everyone was missing. Instagram followers soared into the millions. Instructors were getting stopped on the street—when anyone was actually on the street.

The stock market response was euphoric. From a March 2020 low around $20, shares began a relentless climb. The all-time high Peloton Interactive stock closing price was 167.42 on January 13, 2021. At its all-time high in January 2021, Peloton's stock was up a whopping 550% from its IPO price. And the market capitalization approached $50 billion at that time.

Inside Peloton, the mood was complicated. On one hand, validation—the world finally understood what they'd been building. Revenue was exploding. The brand had never been stronger. Employee stock options were worth life-changing money. On the other hand, the operational challenges were overwhelming. Supply chains were snarled. Customer service was drowning. Quality control was slipping.

And there was the moral complexity. Peloton was thriving because of a global tragedy that had killed millions. The company walked a careful line in its messaging, focusing on mental health and community rather than capitalizing explicitly on the pandemic. But the association was inescapable: Peloton was the pandemic winner.

The decisions made during this period would prove catastrophic. Rather than treating the pandemic boom as a temporary windfall, management extrapolated the growth curve into infinity. In May 2021, the company announced a $400 million investment into Peloton Output Park — a sprawling factory it sought to build in Ohio. They acquired Precor for $420 million to add manufacturing capacity. They hired thousands of employees.

The company's own risk factors, buried in SEC filings, warned that demand might normalize post-pandemic. But who reads the fine print during a gold rush? Foley and his team were building for a future where Peloton bikes were as common as refrigerators. They were wrong.

VII. Warning Signs & The Tread+ Crisis (2021)

On March 18, 2021, Peloton announced that a 6-year-old child recently died after being pulled under the rear of the treadmill. The news sent shockwaves through the Peloton community and broader public. This wasn't a business setback—this was a tragedy.

The Consumer Product Safety Commission (CPSC) response was damning. Peloton has received 72 reports of adult users, children, pets and/or objects being pulled under the rear of the treadmill, including 29 reports of injuries to children such as second- and third-degree abrasions, broken bones, and lacerations. The agency released disturbing video of a child being pulled under a Tread+, warning consumers with small children or pets to stop using the product immediately.

Peloton's initial response was a masterclass in what not to do during a product safety crisis. The company fought the CPSC's recall request, calling it "inaccurate and misleading." They insisted the Tread+ was safe when used properly, effectively blaming consumers for the accidents. The defensive, combative tone was stunning from a company built on community and trust.

Public opinion turned savage. This was no longer about an overpriced treadmill—it was about a company that apparently valued sales over safety. Parents shared horror stories on social media. News outlets ran segments with safety experts condemning Peloton's response. The stock began sliding.

After weeks of damaging headlines, Peloton finally capitulated. On May 5, 2021, the company announced a voluntary recall of both the Tread+ and the newer, cheaper Tread. CEO John Foley admitted: "I want to be clear, Peloton made a mistake in our initial response to the Consumer Product Safety Commission's request that we recall the Tread+. We should have engaged more productively with them from the outset. For that, I apologize."

The recall affected about 125,000 Tread+ machines and roughly 1,050 Tread products in the U.S. Customers could return the treadmills for a full refund or wait for a repair kit that would be developed. The financial hit was substantial, but the reputational damage was worse. Peloton had revealed an ugly side—stubborn, defensive, and slow to accept responsibility.

Meanwhile, other cracks were showing. Delivery times remained unacceptably long even as the company scrambled to add capacity. Customer service wait times stretched to hours. Quality complaints increased as production ramped up. The company that had prided itself on premium experience was delivering anything but.

The stock market began to lose faith. From the January peak, shares started a steady decline through spring 2021. Investors who'd bought at the top were underwater. Employees watched their paper wealth evaporate. The pandemic trade was reversing across the board, but Peloton's fall was particularly sharp.

Perhaps most concerning were the early signs of demand destruction. As vaccines rolled out and gyms reopened, Peloton's growth rate decelerated. New subscriber additions slowed. Bike sales softened. The company insisted this was temporary—a brief pause before the next growth phase. They were building factories, hiring aggressively, and expanding internationally as if the pandemic boom would continue indefinitely.

VIII. The Great Unraveling (Late 2021 - Early 2022)

The email from CNBC reporter Lauren Thomas landed like a bomb on January 20, 2022: "I'm reaching out because I've obtained internal Peloton documents showing the company is temporarily halting production of bikes and treadmills. Can you comment?" Within hours, the story was everywhere. Peloton, the pandemic darling, was drowning in inventory.

The numbers were staggering. By mid-2022, Peloton had 500 days of inventory on hand, warehouses stacked with unsold bikes and treadmills. They could shut their factories down for 500 days without running out of stock. The company that couldn't make bikes fast enough a year earlier now couldn't sell them at any price. Parking lots at distribution centers were filled with shipping containers of unwanted equipment.

Then came the ultimate insult: Mr. Big's death. On December 9, 2021, the Sex and the City reboot premiered with a shocking scene—Mr. Big, Carrie Bradshaw's love interest, dying of a heart attack after a Peloton ride. The scene was meant to show how the characters had evolved, embracing modern fitness. Instead, it became a viral moment for all the wrong reasons.

Peloton's response was clever but desperate—a quickly produced commercial featuring Mr. Big actor Chris Noth, alive and well, toasting with instructor Jess King. But Noth was soon accused of sexual assault by multiple women, forcing Peloton to pull the ad. It was a metaphor for everything going wrong: even their damage control needed damage control.

Inside Peloton headquarters, panic was setting in. The November earnings call had been a disaster, with management slashing guidance and admitting they'd misread demand. The stock fell 35% in a single day. By January 2022, shares were trading below the IPO price. At that point, it fetched a market cap of almost $50 billion, then crashed.

Activist investors smelled blood. Blackwells Capital, which owned less than 5% of shares, published a scathing letter calling for Foley's resignation and the company's sale. They highlighted management's "multiple missteps," excessive spending, and Foley's decision to hire his wife to run the apparel business. The attacks were personal and public.

The media pile-on was relentless. Every outlet ran variations of the same story: Peloton was the ultimate pandemic bubble, a fake business propped up by temporary circumstances. The fact that millions of members still loved their bikes was irrelevant. The narrative had shifted, and Peloton was the poster child for pandemic excess.

Behind the scenes, the board was in crisis mode. Foley, who'd built the company from nothing, was increasingly isolated. Major investors were demanding change. Employees were demoralized. Something had to give.

The death spiral accelerated. Suppliers who'd been begging for orders months earlier were now demanding payment. Landlords with Peloton showrooms in premium locations wondered if the rent checks would keep coming. Instructors, the heart of the brand, were reportedly exploring outside opportunities. The company that had seemed unstoppable was coming apart at the seams.

IX. Leadership Transition & The McCarthy Era (February 2022 - May 2024)

Barry McCarthy, 68, previously served as chief financial officer for both Spotify and Netflix. He's credited with pushing Spotify to pursue a direct listing to go public rather than the traditional initial public offering. On February 8, 2022, he became Peloton's new CEO, replacing founder John Foley in a boardroom coup that was both inevitable and devastating.

The company also cut its revenue forecast, announced plans to slash 2,800 jobs and overhauled its board in a flurry of news Tuesday morning. McCarthy's arrival marked the end of Peloton as a founder-led company and the beginning of its transformation into something else entirely—a turnaround project.

McCarthy's first weeks were brutal. As soon as he took over, he implemented mass layoffs to right size Peloton's cost structure, closed some of the company's splashy showrooms and enacted new strategies designed to grow membership. The cuts were deep and immediate. Manufacturing was outsourced. The Ohio factory project was killed. Showrooms were shuttered.

His strategy was clear: transform Peloton from a hardware company with a subscription to a subscription company that happened to sell hardware. Bike prices were slashed. Subscription fees were raised. A rental program was launched. The company began selling through Amazon and Dick's Sporting Goods—moves that would have been heretical under Foley.

"We are done now," McCarthy had said in November 2022 of the layoffs. "There are no more heads to be taken out of the business." The promise would prove hollow. Cost cuts were never enough because the fundamental problem remained: Peloton had built infrastructure for a business that no longer existed.

McCarthy brought Silicon Valley credibility and a subscription-first mentality. But he was also 68 years old, brought out of retirement for what he'd explicitly described as a short-term assignment. McCarthy was brought on board half-way through that decline, in February 2022, lured out of retirement to replace founder and then-CEO John Foley with a pay package reported to be worth as much as $168 million.

The operational improvements were real. Inventory was cleared. Costs were cut. The subscription business stabilized even as hardware sales cratered. But growth remained elusive. New product launches failed to excite. International expansion stalled. The brand that had once stood for aspiration now stood for retrenchment.

McCarthy's most controversial decision was embracing third-party retail. Seeing Pelotons at Dick's Sporting Goods next to generic treadmills was jarring for longtime members. The premium positioning that justified premium prices was eroding. But McCarthy argued exclusivity was a luxury Peloton could no longer afford.

The content strategy also shifted. With less money for production, live classes were reduced. The schedule that once featured dozens of daily options shrunk. Star instructors departed or reduced their presence. The community that had powered Peloton's rise began to fragment.

On May 2, 2024, McCarthy announced he was stepping down. McCarthy, a former Spotify and Netflix executive, will become a strategic advisor to Peloton through the end of the year while Karen Boone, the company's chairperson, and director Chris Bruzzo will serve as interim co-CEOs. His departure surprised no one. The turnaround had become a managed decline.

X. Current State & Future Prospects (2024-2025)

Peter Stern, who currently serves as President of Ford Integrated Services and before that held leadership roles at Apple and Time Warner Cable, has been appointed to serve as Peloton's CEO and President effective January 1, 2025. The appointment of yet another outside executive—the third CEO in three years—signals Peloton's continued search for identity and direction.

Mr. Stern spent more than six years as Vice President of Services at Apple, where he managed the businesses of Apple TV+ and Sports, iCloud, Apple Arcade, Apple Fitness+ and Apple One. Additionally, Mr. Stern led marketing for Apple services, including the App Store, Apple Card, Apple Pay, Apple Music, Apple Podcasts and Apple Maps. His background suggests a continued focus on subscription services and digital transformation.

The company Stern inherits is dramatically different from the one Foley built. Peloton announced restructuring efforts that include laying off about 400 employees — about 15% of its global headcount. The workforce that once exceeded 8,000 has been cut by more than half. The energy and optimism that defined early Peloton has been replaced by survivor's guilt and uncertainty.

Financially, the picture remains challenging. In fiscal year 2023, Peloton reported revenue of $2.79 billion, a 22 percent decrease from the previous year, and a net loss of $1.2 billion. The subscription business shows resilience with approximately 6.4 million members, with 3 million connected fitness subscribers, but growth has stalled.

The competitive landscape has evolved dramatically. Apple Fitness+ leverages the Apple Watch ecosystem. Mirror was acquired by Lululemon. Tonal and Hydrow have carved out their niches. Traditional gyms have embraced hybrid models. The connected fitness space Peloton pioneered is now crowded with well-funded alternatives.

Yet Peloton retains unique assets. The brand, while damaged, still resonates with millions. The content library is unmatched in depth and variety. Monthly customer churn rate of lost customers is less than 1 percent—proving that those who stay remain devoted. The community, fragmented but not broken, represents a foundation for potential recovery.

The debt situation looms large. Refinancing obligations are approaching, and the company's cash burn, while reduced, continues. The balance sheet that once showed strength now shows strain. Strategic alternatives—including a potential sale—remain on the table.

Recent moves suggest a company still searching for the right formula. Price increases on subscriptions risk alienating loyal members. Hardware refreshes feel incremental rather than revolutionary. Marketing campaigns lack the cultural resonance of peak Peloton. The magic that once made Peloton special feels increasingly distant.

"Working for Peloton is a dream come true for me," said Mr. Stern. "My goal is to help millions of people live longer, healthier and happier lives. Peloton, with its unique combination of people, products and passionate Members, provides me an opportunity to do just that." Whether he can deliver on that promise remains to be seen.

XI. The Playbook: Key Business Lessons

What Went Right:

The product experience Peloton created was genuinely transformative. The integration of hardware, software, and content created something greater than the sum of its parts. The bike wasn't just equipment; it was a portal to a new type of fitness experience. The touchscreen wasn't just a display; it was a window into a global community. The subscription wasn't just content access; it was membership in something bigger.

Community building was perhaps Peloton's greatest achievement. The company understood that fitness is as much about motivation and accountability as physical exercise. The leaderboard created competition. High-fives created connection. Milestone celebrations created momentum. Instructors became friends, therapists, and life coaches. Members formed bonds that transcended the bike.

The timing for the pandemic was tragically perfect. No amount of strategic planning could have anticipated a global shutdown that would make home fitness essential. Peloton was positioned perfectly—established enough to scale, innovative enough to capture imagination, premium enough to justify the investment when nothing else was available.

Content quality set a new standard for fitness instruction. Peloton's instructors weren't just teaching classes; they were creating experiences. The production values—multiple camera angles, professional lighting, curated playlists—made garage workouts feel like Madison Square Garden events. The variety meant there was something for everyone, every mood, every moment.

What Went Wrong:

The fundamental error was misreading temporary demand as permanent change. Peloton's management convinced themselves the pandemic had permanently transformed consumer behavior. They built factories, hired thousands, and invested billions based on the assumption that the future would look like April 2020 forever. They were catastrophically wrong.

The over-investment in manufacturing capacity was particularly damaging. The Precor acquisition and Ohio factory project committed hundreds of millions to fixed infrastructure just as demand was peaking. When sales collapsed, these investments became albatrosses. The company optimized for a problem—inability to meet demand—that evaporated overnight.

Crisis management failures, particularly around the Tread+ recall, revealed organizational immaturity. The initial denial, defensive responses, and slow acceptance of responsibility damaged trust that took years to build. In consumer products, safety isn't negotiable. Peloton learned this lesson too late and too publicly.

The inability to transition from growth to profitability mindset proved fatal. Peloton operated like a hypergrowth startup even as it became a public company with real-world constraints. The culture celebrated expansion over efficiency, new initiatives over operational excellence. When the market demanded profitability, the company couldn't adjust fast enough.

XII. Strategic Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces:

Competitive Rivalry has intensified dramatically. What began as Peloton versus traditional gyms has evolved into a complex battlefield. Apple Fitness+ leverages ecosystem lock-in. Lululemon's Mirror targets a different demographic. Tonal and Hydrow offer alternative modalities. Traditional gyms have embraced digital. The moat Peloton built has multiple bridges across it.

Supplier Power remains moderate but manageable. Contract manufacturers can be switched, though not without cost and complexity. Content creators—particularly star instructors—have more leverage than before, but Peloton has successfully developed multiple stars, reducing dependence on any individual. Music licensing remains a cost pressure but is now properly managed.

Buyer Power has increased substantially post-pandemic. Consumers have numerous alternatives, from free YouTube workouts to premium studio classes. Price sensitivity has returned after pandemic-era splurging. The switching costs of abandoning Peloton hardware are high, but the subscription can be cancelled with a click.

Threat of Substitutes is extreme. Every form of exercise—outdoor running, gym memberships, home workouts, sports—competes with Peloton. The pandemic temporarily eliminated many substitutes, creating artificial demand. As options returned, Peloton's relative value proposition weakened.

Barriers to Entry have lowered significantly. The connected fitness playbook is now well understood. Software development is cheaper. Content creation is democratized. Hardware manufacturing can be outsourced. What once seemed impossible—replicating Peloton—now seems merely difficult.

Hamilton's 7 Powers:

Scale Economies worked until they didn't. The fixed costs of content production and technology development could be spread across millions of subscribers. But the infrastructure built for hypergrowth became a burden in decline. Scale became a disadvantage as the company struggled to rightsize.

Network Effects exist but are limited. The leaderboard and social features create some community value, but not true network effects. Adding more members doesn't meaningfully improve the experience for existing members. The community is valuable but not exponentially so.

Counter-positioning was initially powerful. Peloton offered something traditional gyms couldn't: convenience, consistency, and technology. But as gyms adapted and alternatives emerged, this advantage eroded. The counter-position became a crowded position.

Switching Costs are moderate and asymmetric. The hardware investment creates lock-in, but only until the equipment is paid off or abandoned. The subscription has zero switching costs. The emotional investment in instructors and community creates stickiness, but not imprisonment.

Branding remains an asset, though diminished. Peloton still means something—premium, connected, community-driven fitness. But the brand has been diluted by distribution expansion, quality issues, and corporate turmoil. What once conveyed aspiration now sometimes conveys desperation.

Cornered Resource in instructor talent is partial at best. Peloton has exceptional instructors, but they're not irreplaceable. Other platforms have successfully recruited talent. The magic was never just the instructors but the entire production ecosystem around them.

Process Power in content production represents real capability. Peloton knows how to create engaging fitness content at scale. The production workflows, technology stack, and quality standards represent accumulated knowledge. But process power without growth is like a factory without orders.

XIII. The Bear & Bull Cases

Bear Case:

The permanent demand destruction thesis is compelling. Peloton pulled forward years of demand during the pandemic. Everyone who might want a Peloton already bought one. The secondary market is flooded with barely-used equipment. New customer acquisition requires convincing skeptics, not evangelizing believers.

Commoditization is accelerating. Connected fitness is no longer novel. Every treadmill has a screen. Every app has workouts. Every instructor has an Instagram following. The differentiation that justified Peloton's premium pricing is eroding. In a commoditized market, Peloton's cost structure is a disadvantage, not an asset.

The unsustainable cost structure remains despite years of cuts. Peloton still operates like a premium brand while increasingly competing on price. Content production is expensive. Technology development is expensive. Marketing is expensive. The math doesn't work without significant scale, and scale isn't coming.

The debt maturity wall approaches with limited options. Refinancing in a higher-rate environment will be painful. Asset sales would require accepting massive losses. Strategic alternatives might mean selling the company for parts. The financial engineering required to survive might destroy what makes Peloton special.

Competition from tech giants is intensifying. Apple has unlimited resources and ecosystem advantages. Amazon has distribution dominance. Google has YouTube's content library. These companies can operate fitness offerings at a loss indefinitely. Peloton must make money; they don't.

Bull Case:

The subscriber base remains remarkably loyal. 3 million connected fitness subscribers paying monthly fees represents a valuable recurring revenue stream. Churn below 1% monthly suggests the core product still delivers value. This isn't a failing business; it's a struggling growth story.

The subscription business is growing as a percentage of revenue, improving unit economics. Hardware might be commoditized, but the content and community aren't. As the mix shifts toward subscriptions, margins improve. The SaaS-like metrics that investors value are emerging from the hardware-heavy history.

International expansion remains largely untapped. Peloton is primarily a U.S. phenomenon with minimal presence in Europe and Asia. The connected fitness trend is global. Success in new markets could reignite growth without the operational complexity of the early international efforts.

Acquisition potential is real. Peloton's brand, despite challenges, has value. The content library is extensive. The technology platform is proven. The customer base is attractive. For Apple, Amazon, or Nike, Peloton could be a strategic acquisition at the right price.

Brand loyalty among core users borders on fanatical. Members who've integrated Peloton into their daily routines aren't leaving. They're upgrading equipment, buying apparel, attending live classes. The community that powered Peloton's rise still exists, even if growth has stalled.

XIV. Final Analysis & Lessons

The danger of extrapolating temporary trends might be Peloton's defining lesson. The pandemic created a once-in-a-century demand shock that management mistook for permanent change. Every model, every projection, every investment decision was based on a future that never materialized. The cost of that miscalculation was existential.

Hardware-software integration is harder than pure software precisely because atoms don't scale like bits. Software companies can add users with minimal marginal cost. Hardware companies must manage inventory, supply chains, and physical distribution. Peloton tried to be both and discovered the worst of both worlds during the transition.

Unit economics matter more than growth, eventually. Peloton's hypergrowth masked fundamental questions about profitability. When growth stopped, the questions became urgent. The lifetime value of customers, the cost of acquisition, the contribution margins—these boring metrics determine survival when story stocks become value stocks.

Crisis management as core competency is non-negotiable for consumer brands. The Tread+ recall response revealed an organization unprepared for adversity. In the social media age, every mistake is magnified, every response is scrutinized. Companies must be prepared to act quickly, apologize sincerely, and fix problems transparently.

Pivoting a public company is exponentially harder than pivoting a startup. Peloton needed to transform its business model while maintaining quarterly earnings, managing investor expectations, and retaining employee morale. The market demands consistency while transformation requires change. It's a nearly impossible balance.

Consumer hardware startups face unique challenges that software startups don't. Inventory risk, manufacturing complexity, distribution costs, return logistics—these physical world problems don't have digital solutions. The next generation of hardware entrepreneurs must learn from Peloton's struggles with the atoms economy.

XV. Epilogue & What's Next

As we record this in November 2025, Peloton stands at another crossroads. Peter Stern took over as CEO on January 1, 2025, bringing Apple experience and subscription expertise. The company continues to optimize operations, seeking the right balance between growth and profitability.

Strategic alternatives remain under constant consideration. A sale to a larger company—whether tech giant or athletic brand—could provide resources and distribution. Going private might allow for transformation without quarterly scrutiny. Partnerships could extend reach without additional investment. Every option has trade-offs; none guarantees success.

The future of connected fitness is being written in real-time. Virtual reality workouts, AI-powered coaching, and gamification represent new frontiers. Whether Peloton leads, follows, or becomes irrelevant in this evolution remains uncertain. The company that defined the category might not survive to see its maturation.

Key metrics to watch going forward center on three critical areas. First, subscription revenue growth—not equipment sales—will determine financial sustainability. Second, monthly churn rate must remain below 1% to maintain the base while acquiring new members. Third, free cash flow generation, not adjusted EBITDA, will determine whether Peloton can service debt and invest in growth.

Final reflections on this dramatic arc reveal universal truths about business. Great products aren't enough without great execution. Temporary success can be more dangerous than failure if it breeds overconfidence. The difference between visionary and delusional is often only clear in hindsight. And sometimes, being too early is indistinguishable from being wrong—until suddenly, you're too late.

Peloton's story isn't over. The company that captured imaginations, defined a category, and became a pandemic phenomenon continues to fight for relevance and survival. Whether this is the middle chapter of an incredible comeback or the final act of a cautionary tale remains to be written. But the lessons—about ambition and hubris, innovation and execution, timing and luck—are already clear.

The bike that changed fitness may not survive the changes it created. But the impact—on how we exercise, how we connect, how we think about home fitness—is permanent. That might be John Foley's greatest achievement and deepest frustration: building something that mattered so much it transcended the company that created it.

For investors, operators, and entrepreneurs, Peloton offers a masterclass in what's possible and what's perilous in building consumer hardware businesses. The same forces that enabled its rise—technology, community, content—also enabled competitors. The moat was never as deep as it seemed. The mountain was never as high as it looked. And the journey—thrilling, devastating, ongoing—continues.

Looking at the article structure, I can see it's actually complete. The outline had 15 sections (I-XV) and all 15 sections have been written:

- Introduction & Episode Roadmap ✓

- The Pre-Peloton Era: Context & Founding ✓

- Building the Machine: Early Years (2012-2016) ✓

- Scaling & The Pre-IPO Years (2017-2019) ✓

- The IPO & Public Company Era (September 2019) ✓

- The Pandemic Rocket Ship (March 2020 - January 2021) ✓

- Warning Signs & The Tread+ Crisis (2021) ✓

- The Great Unraveling (Late 2021 - Early 2022) ✓

- Leadership Transition & The McCarthy Era (February 2022 - May 2024) ✓

- Current State & Future Prospects (2024-2025) ✓

- The Playbook: Key Business Lessons ✓

- Strategic Analysis: Porter's 5 Forces & Hamilton's 7 Powers ✓

- The Bear & Bull Cases ✓

- Final Analysis & Lessons ✓

- Epilogue & What's Next ✓

The article ends with a comprehensive epilogue that provides final reflections and ties everything together. The last paragraph appropriately concludes with: "The same forces that enabled its rise—technology, community, content—also enabled competitors. The moat was never as deep as it seemed. The mountain was never as high as it looked. And the journey—thrilling, devastating, ongoing—continues."

The article is complete as written.

Looking at the article structure, I can see that all 15 sections from the original outline have already been completed:

- ✓ Introduction & Episode Roadmap

- ✓ The Pre-Peloton Era: Context & Founding

- ✓ Building the Machine: Early Years (2012-2016)

- ✓ Scaling & The Pre-IPO Years (2017-2019)

- ✓ The IPO & Public Company Era (September 2019)

- ✓ The Pandemic Rocket Ship (March 2020 - January 2021)

- ✓ Warning Signs & The Tread+ Crisis (2021)

- ✓ The Great Unraveling (Late 2021 - Early 2022)

- ✓ Leadership Transition & The McCarthy Era (February 2022 - May 2024)

- ✓ Current State & Future Prospects (2024-2025)

- ✓ The Playbook: Key Business Lessons

- ✓ Strategic Analysis: Porter's 5 Forces & Hamilton's 7 Powers

- ✓ The Bear & Bull Cases

- ✓ Final Analysis & Lessons

- ✓ Epilogue & What's Next

The article ends with a comprehensive epilogue that provides final reflections and appropriately concludes the piece. The last section (XV. Epilogue & What's Next) wraps up with powerful closing paragraphs about Peloton's lasting impact and ongoing journey.

The article is complete as written. All sections from the outline have been covered, and it concludes with a proper ending that ties everything together.

Looking at the article, I can confirm that all 15 sections from the original outline have been completed. The article ends with Section XV (Epilogue & What's Next), which provides a comprehensive conclusion with final reflections about Peloton's journey, current state, strategic alternatives, and lasting impact on the fitness industry.

The final paragraphs appropriately conclude the piece: - Summarizing the key metrics to watch - Providing final reflections on the dramatic business story - Discussing Peloton's ongoing struggle and uncertain future - Reflecting on the broader lessons for investors, operators, and entrepreneurs - Ending with a powerful statement about how Peloton's impact transcends the company itself

The article is complete as written, with all 15 sections from the outline fully covered and a proper conclusion that ties everything together.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube