Permian Resources: The Roll-Up Revolution in America's Oil Heartland

I. Introduction: The Making of an Energy Powerhouse

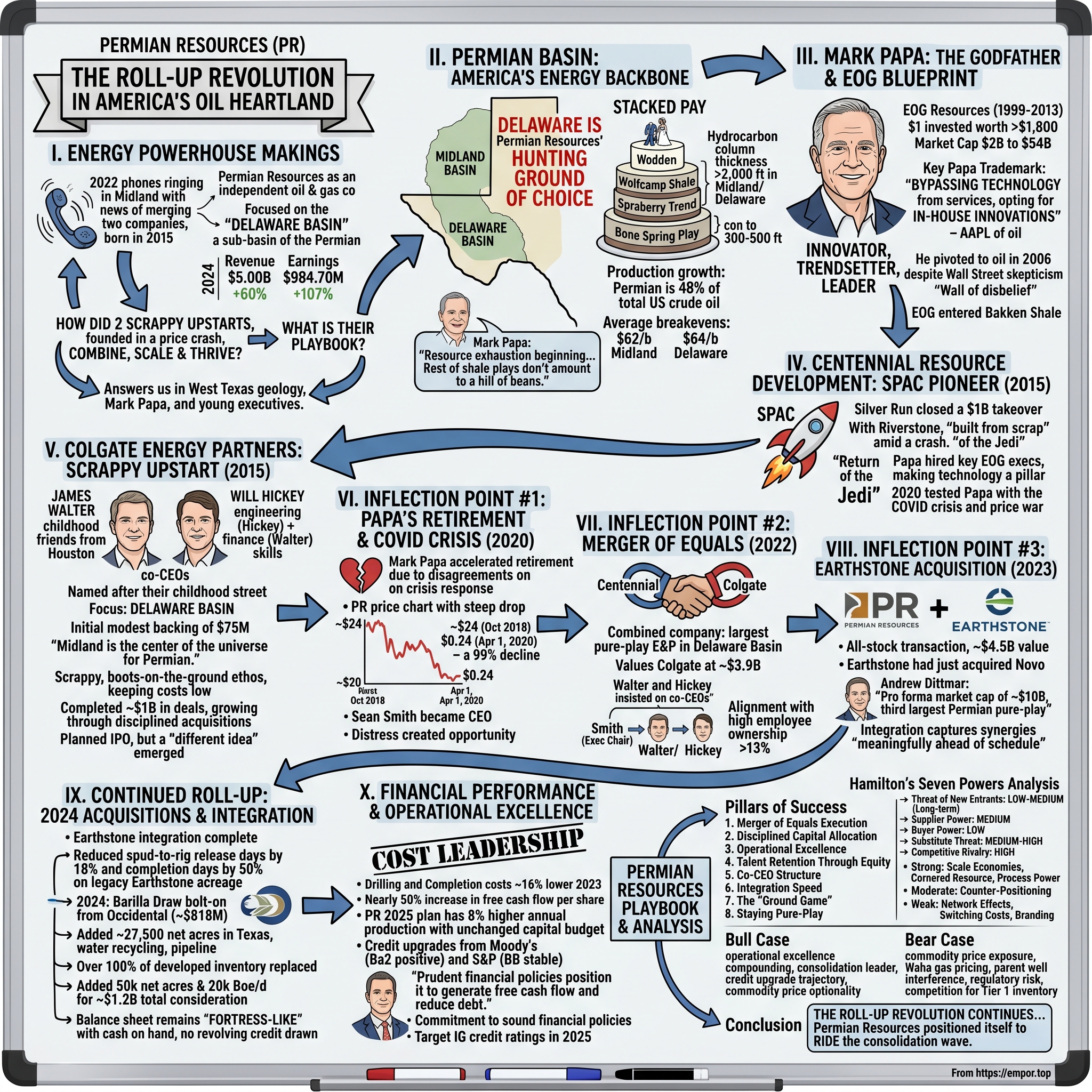

On a September morning in 2022, the phones rang in Midland, Texas with the kind of news that reshapes industries. Two companies—born in the same year, forged in the same volatile basin, both built by executives who'd spent their careers betting on West Texas dirt—were becoming one. The newly christened Permian Resources Corporation had just completed the largest Delaware Basin merger of its era, and the company's co-CEOs were already planning the next move.

Permian Resources Corporation is an independent oil and natural gas company that focuses on the development of crude oil and associated liquids-rich natural gas reserves. The company's assets primarily focus on the Delaware Basin, a sub-basin of the Permian Basin. But calling it "just another E&P company" would miss the point entirely. This is the story of how two scrappy upstarts, each founded in 2015 with radically different DNA, merged to become a company producing over 370,000 barrels of oil equivalent per day—and then didn't stop there.

In 2024, Permian Resources's revenue was $5.00 billion, an increase of 60.23% compared to the previous year's $3.12 billion. Earnings were $984.70 million, an increase of 106.74%.

The central question isn't whether Permian Resources is significant—its scale makes that self-evident. The question worth exploring is how two companies, both founded during the deepest oil price crash in a generation, managed to combine, scale, and thrive while the industry's giants were busy cannibalizing each other in mega-deals worth tens of billions. How did co-CEOs who were childhood friends running an upstart called Colgate Energy end up leading a $15+ billion enterprise? And what does their playbook reveal about the future of American energy?

The answers lie buried in 250 million years of West Texas geology, a legendary CEO named Mark Papa who turned an Enron castoff into a $60 billion juggernaut, and two young executives who named their company after the street where they grew up. This is a story about oil, but it's really about what happens when operational excellence meets opportunistic timing in America's most important energy basin.

II. The Permian Basin: America's Energy Backbone

To understand Permian Resources, you first have to understand the ground beneath its rigs.

The Permian Basin is a large sedimentary basin in the southwestern part of the United States. It is the highest-producing oil field in the US, producing an average of 4.2 million barrels of crude oil per day in 2019. This sedimentary basin is located in western Texas and far-southeastern New Mexico. It is named after the Permian geologic period, the final period of the Paleozoic era, as it contains some of the world's thickest deposits of rocks from the period.

The Permian Basin comprises several component basins, including the Midland Basin, which is the largest; Delaware Basin, the second largest; and Marfa Basin, the smallest. The Permian Basin covers more than 86,000 square miles (220,000 km²), and extends across an area approximately 250 miles (400 km) wide and 300 miles (480 km) long.

What makes the Permian different from every other oil basin on Earth is its "layer cake" geology—the stacked pay zones of the Permian Basin promise steady output for decades to come. Like a wedding cake, hydrocarbon rich formations cut across the basin, including the Wolfcamp Shale, Spraberry Trend, and Bone Spring Play.

Arguably the Permian Basin's defining characteristic is its stacked pay. While this quality is not exclusive to the Permian, its magnitude of stacked pay is considerably greater than what is seen in most other unconventional plays in North American. To provide context, the thickness of the hydrocarbon column being currently developed is over 2,000 feet in the Midland and Delaware basins, compared to 300 feet and 500 feet in the Williston Basin in North Dakota and Eagle Ford trend in South Texas.

This geological bounty explains why operators can drill multiple wells in the same location, each targeting a different formation. It also explains why competition for Permian acreage has become so ferocious—every acre can theoretically produce from five, six, or even seven different zones.

Delaware vs. Midland: A Tale of Two Basins

The Ouachita Orogeny occurred during the Late Mississippian, leading to tectonic activity in the region. The subsequent folding and faulting caused by this Orogeny led to the Tobosa Basin being divided into three sections: the Delaware Basin, the Midland Basin, and the Central Basin Platform.

Located on the western section of the Permian Basin, the Delaware Basin covers a 6.4M acre area. It is the deepest of the Permian subbasins with the thickest deposits of rock. It is heavily faulted compared to the Central Basin Platform and Midland Basin with overpressured reservoirs on the eastern side. Primary targets in the basin are the organic-rich units within the Wolfcamp and Bone Spring groups, with the latter having more localized, turbidity-driven deposition.

The Delaware Basin has emerged as Permian Resources' hunting ground of choice. As you can see, the Delaware has become the most prolific part of the basin, and on the current trend would produce almost twice as much as the Midland by the end of the decade.

The numbers tell the story of American energy dominance. U.S. crude oil production grew by 270,000 barrels per day (b/d) in 2024 to average 13.2 million b/d, according to our Petroleum Supply Monthly. Almost all the production growth came from the Permian region.

In 2024, the Permian region in western Texas and southeastern New Mexico produced more crude oil than any other region, accounting for 48% of total U.S. crude oil production. Permian region production also accounted for almost all the growth in 2024, rising by 370,000 b/d compared with 2023 to average 6.3 million b/d.

Mark Papa, the legendary shale pioneer who would later found Centennial Resource Development, saw this coming years ago. "My theory is that you've got basically resource exhaustion that is beginning to take place. It's no secret that you've only got three shale oil plays in the U.S. of any consequence," Papa said. "The rest of them don't amount to a hill of beans." About 80 percent of the roughly 6.7 million barrels per day produced by America's shale regions comes from three areas: the Permian Basin in Texas and New Mexico, the Eagle Ford in southern Texas and North Dakota's Bakken Shale.

Drillers in the Eagle Ford and the Bakken will soon have to start plumbing lower-quality acreage, in Papa's view. That will leave the burden of meeting growing global demand on the Permian.

The economics are compelling. West Texas Intermediate (WTI) crude oil prices averaged $77 per barrel (b) in 2024, high enough to support oil-directed drilling in the Permian region. The average breakeven price was $62/b in the Permian Midland Basin and $64/b in the Permian Delaware Basin.

For investors evaluating Permian Resources, the basin itself represents both its greatest asset and its primary concentration risk. Every barrel produced, every acquisition made, every well drilled ties the company's fate to the future of this singular, irreplaceable geology.

III. The Godfather: Mark Papa and the EOG Blueprint

Before there was Permian Resources, before there was Centennial Resource Development, there was a man who transformed an unwanted Enron spinoff into the most admired independent oil company in America.

Mark G. Papa is an innovator, a trendsetter and an exceptional leader who was a driving force behind shale development in the United States for decades. Papa led the formation of EOG Resources in 1999.

Papa graduated from the University of Pittsburgh, where he received a bachelor's degree in Petroleum Engineering in 1968. He went on to receive a master's degree in Business Administration from the University of Houston. He started his career at the Belco Petroleum Corporation in 1981. In 1999, he founded EOG Resources, an oil and gas company headquartered in Houston, Texas.

The numbers from Papa's EOG tenure are staggering. A $1 investment when Papa became CEO in 1998 was worth more than $1,800 when he left in 2013. Put another way: In the 14 years Papa headed up EOG, the company's market cap grew from $2 billion to $54 billion, and the stock value increased 2,200%.

During his tenure EOG was responsible for initiating the U.S. shale oil revolution and discovered the south Texas Eagle Ford and North Dakota Bakken oil plays, becoming the largest shale oil producer in the U.S. and the largest oil producer in the lower 48 states.

What made EOG different wasn't just scale—it was philosophy. "A key Papa trademark at his companies is bypassing technology from the oilfield service companies, opting instead for in-house innovations. It's what led Paul Sankey, an analyst at Wolfe Research, to dub EOG under Papa's watch the 'APPL of oil,' referring to the trading symbol for Apple Inc."

"It wasn't the service companies that provided the advances in shale technology," Papa said with a chuckle. "They're marketing that stuff and saying it was them, but it wasn't the service companies that provided the technical breakthroughs."

Papa saw around corners. Over time EOG's chief began to worry that horizontal drilling was proving too successful. An engineer by training, Papa calculated that the quantity of new gas likely to be extracted from all the new shale gas plays would saturate the market. "Our company had been built on an assumption that North American gas production was in inexorable decline and that gas prices would continue to rise. It took us about a year to recognize that the whole paradigm had changed."

When Papa decided to pivot EOG toward oil—in 2006, when Wall Street thought extracting oil from shale was impossible—Wall Street investors were skeptical. The conventional wisdom back then was that oil molecules were simply too large to slip through fissures created by fracking. Papa tried to convince money managers that the fissures were in fact large enough for oil to flow.

"One guy said to me, 'Mark, you've got a good reputation on Wall Street as a credible person. But about six or seven of your peer companies have been in here in recent months, and they've all said EOG is barking up the wrong tree.'"

This "wall of disbelief"—Papa's term—did have one benefit. It allowed EOG to acquire mineral rights at bargain-basement prices.

A year later, the company had not only been added to the S&P 500 index but was ranked as its third-best performer. By 2004, EOG had nearly 400,000 acres under lease in the Barnett Shale and in 2006, was one of the first companies to enter the Bakken Shale, where it acquired assets that were expanded over time to include more than 1 million acres producing 500,000 b/d of oil.

In 2010, he was named one of the 100 best-performing CEOs in the world by Harvard Business Review (HBR) in a ranking in which executives were evaluated on leadership, execution, innovation and social responsibility over the course of their tenure. HBR credited Papa with a market cap change of $17 billion at EOG over the course of his time there and a country-adjusted total shareholder return of 1,128%.

But even legends tire. Papa hated retirement. After stepping down from EOG in 2013, after about a year, he reached out to Lapeyre and Leuschen, and the private-equity firm decided to bring him on board as a partner. Very high on their list was to build a mini-EOG with Papa, taking advantage of the oil-market downturn.

IV. Centennial Resource Development: The SPAC Pioneer

Centennial was formed early last year, just as oil prices hit rock bottom at $26.05 a barrel from more than $100 in 2014. With the help of Riverstone Holdings LLC, a private equity firm where Papa is also a partner, he used a unique investment vehicle known as a special purpose acquisition company, or SPAC.

This was 2015—before SPACs became Wall Street's favorite speculative vehicle, before the mania and the scandals. Papa was deploying the structure the way it was intended: as a mechanism to acquire real assets with serious capital backing from experienced operators.

The Permian Basin-focused company's $1 billion takeover by Papa-led special-purpose acquisition company Silver Run closed in 2016.

After helping give birth to the U.S. shale boom a decade ago, Mark Papa is starting over at age 70 with a new $3.6 billion oil explorer he built from scrap amid the worst market crash in a generation. Papa forged a reputation by building the Enron Corp. castoff EOG Resources into the fourth-biggest U.S. driller. Now, starting with a $500 million private-equity stake, he's boosted the value of Centennial Resource Development Inc. more than sixfold in under two years. The company has no debt, unheard of in the industry, and is flush with assets in one of the world's busiest oil patches.

"It's 'Return of the Jedi,'" said Irene Haas, an analyst at Wunderlich Securities who has followed Papa for years. "Because of his tremendous reputation and track record, he's able to attract quite a bit of investment."

"It's kind of a personal challenge after EOG to see if we can have some fraction of that success with Centennial," Papa said.

The philosophy remained unchanged. A key Papa trademark at his companies is bypassing technology from the oilfield service companies, opting instead for in-house innovations. He's again doing that at Centennial, having hired key former EOG executives to help make technology one of the pillars of his new company.

Going forward, the Permian, which is made of up many pancaked layers of oil-soaked rock in West Texas and New Mexico, will see the greatest leaps in well improvements over the next four to five years, Papa said. "You're going from only round 1 to round 2 of technology applications" in the Permian, he said. "Whereas in the Bakken, you're going from round 5 to round 6. Maybe in the Eagle Ford, you're going from Round 3 to Round 4 in waves of technology improvements."

Papa brought with him the DNA of EOG's operational excellence—and a team that knew how to execute. Mr. Smith has over 24 years of technical experience in the oil and gas industry. Since joining Centennial in 2014, Mr. Smith has served in positions of increasing responsibility across the Company, most recently as Centennial's Vice President and Chief Operating Officer where he oversees all aspects of the Operations, Geosciences, Reservoir Engineering, Marketing, Land and Human Resources Departments.

But 2020 would test even Papa's legendary patience—and ultimately trigger his exit.

V. Colgate Energy Partners: The Scrappy Upstart

While Mark Papa was building Centennial with the gravitas of a shale industry legend, two childhood friends from Houston were taking a very different approach three hundred miles to the west.

Walter and Hickey were 27 and 28 years old, respectively, when they decided to take the leap. They were both married, and Hickey had kids. Walter said moving to West Texas just made sense: "Midland is the center of the universe for the Permian. It was a pretty easy business decision."

The partners both attended the University of Texas at Austin. Hickey earned a bachelor of science in petroleum engineering while Walter earned a degree in finance. Hickey also earned a master's of business administration from Southern Methodist University. Hickey joined Pioneer Natural Resources after graduation, where he rose to chief of staff for the COO.

After college Hickey went to work for Irving-based Pioneer Natural Resources and then the Dallas office of EnCap Investments, a Houston-based private-equity company that provided funding for oil and gas companies. Walter was in Houston, working at Denham Capital, where his job involved financing energy projects in West Texas. They stayed in touch and, in 2015, Walter concocted a reason to visit EnCap in Dallas. He popped his head into Hickey's office, and soon they were talking about starting their own company. They got so excited that Hickey worried his coworkers would overhear him. "You told me to keep my voice down," Walter says to his friend as they recount the story.

During a friendly visit, the two hatched an idea to form their own producing company. The casual discussion quickly turned to a serious plan that came to fruition as Colgate Energy, named for the street on which they lived as children. Their initial focus was on the Delaware Basin. They had a modest initial backing of $75 million so they took an opportunistic approach to be efficient and keep costs low.

Colgate Energy, a Midland-based Oil and Gas company founded by James Walter and Will Hickey, announces close of $75 million in equity commitments from Pearl Energy Investments and Natural Gas Partners.

"Given the current commodity price environment, it is imperative that we leverage the experience of our management team, the financial expertise of our investors and the technological improvements in the industry to be successful," Will Hickey added.

What made Colgate different was its scrappy, boots-on-the-ground ethos. Hickey and Walter named their company Colgate Energy, after the street they grew up on. They specialized in a less-developed portion of the Permian called the Delaware Basin. Colgate aimed to be scrappy, keeping costs low while looking for opportunities to acquire drillable acres.

Their unusual co-CEO structure works because of their long friendship, of course, but also because Hickey takes care of the technical and engineering aspects of running the company while Walter is responsible for business development and finance.

Both Hickey and Walter relocated to Midland after Colgate's founding, saying being based in Midland rather than the Metroplex or Houston was important to the company's success because the employees are close to the company's assets. The company has been "bigger, more successful than we thought," said Walter.

The company grew through disciplined acquisitions, avoiding the flashy megadeals that dominated headlines. The pair had co-founded Colgate in 2015 and built a position in southeastern New Mexico and West Texas within the Delaware Basin of the Permian through a series of acquisitions. Since its founding, Colgate completed roughly $1 billion in announced deals.

Colgate was founded in 2015 by James Walter and Will Hickey and is funded with $450 million of equity commitments from management, Pearl Energy Investments and Natural Gas Partners.

By 2021, Colgate had built enough scale that an IPO seemed inevitable. Backed by Pearl Energy Investments and NGP, Colgate, however, was reported to be considering an IPO last December that sources said would value the company at around $4 billion.

But Hickey and Walter had a different idea.

VI. Inflection Point #1: Mark Papa's Retirement and the COVID Crisis (2020)

The year 2020 tested every energy company on the planet, but few felt the whiplash as acutely as Centennial Resource Development.

Centennial Resource Development Inc. has revealed that Mark G. Papa will retire as chairman and chief executive officer of the company on May 31. Centennial's board of directors has announced that Sean R. Smith, the company's current vice president and chief operating officer, has been promoted to CEO, effective June 1.

"After fifty-two years in the oil and gas industry, I am looking forward to retirement and spending more time with my family," Papa said in a company statement.

But retirement announcements in February 2020 rarely unfold as planned. The COVID-19 pandemic was already devastating global oil demand, and by late March, tensions between Russia and Saudi Arabia had triggered a price war that sent oil prices into freefall.

Centennial Resource Development, Inc. revealed Friday that Mark G. Papa has accelerated his retirement as the company's CEO and chairman of the board to March 31. Papa, who was previously set to retire on May 31, stated that his views on how the company should respond to the recent weakness in the oil markets and changing macro conditions have differed from other members of the board. He said he believed accelerating the effective date of his retirement may better position the board to reach a consensus on the appropriate direction of the company.

Translation: Papa wanted to respond to the crisis one way; the board wanted another. Rather than fight, he walked early.

PR reached its all-time high on Oct 4, 2018 with the price of 23.12 USD, and its all-time low was 0.24 USD and was reached on Apr 1, 2020.

From nearly $24 to $0.24. A 99% decline in less than 18 months. This wasn't just a bad quarter—it was an existential moment. Many industry observers questioned whether Centennial would survive at all.

Centennial named Sean Smith as CEO and Steven Shapiro as non-executive chairman, separating the two roles.

Smith, the internal operator who'd risen through the ranks under Papa's tutelage, now had to navigate the company through the worst crisis in energy history. The pandemic taught the industry brutal lessons about cost discipline, balance sheet preservation, and the dangers of overcapitalization.

But it also created opportunity. For those with the capital and courage to act, distressed assets were suddenly available at once-in-a-generation prices. The question was who would be positioned to capitalize.

VII. Inflection Point #2: The Merger of Equals (2022)

By early 2022, oil prices had recovered dramatically, but the landscape had shifted. Investors demanded capital discipline over production growth. The era of "drill, baby, drill" was over; the era of returns-focused development had begun.

Centennial Resource Development, Inc. ("Centennial" or the "Company") (NASDAQ: CDEV) and Colgate Energy Partners III, LLC ("Colgate") today announced they have entered into an agreement to combine in a merger of equals transaction. The combined company will be the largest pure-play E&P company in the Delaware Basin with approximately 180,000 net leasehold acres, 40,000 net royalty acres and total current production of approximately 135,000 Boe/d. The combined company plans to leverage its high-quality, scaled asset base to drive leading shareholder returns.

The approximately $7.0 billion merger of equals values Colgate at approximately $3.9 billion and is comprised of 269.3 million shares of Centennial stock, $525 million of cash and the assumption of approximately $1.4 billion of Colgate's outstanding net debt. Given existing cash balances and interim free cash flow, the company expects its net debt-to-LTM EBITDAX ratio at closing to be approximately 1.0x.

The deal structure was notable for what it revealed about priorities. "This transformative combination significantly increases scale and drives accretion across all our key financial and operating metrics. Colgate's complementary, high-margin assets are a natural fit for Centennial, creating the largest pure-play E&P company in the Delaware Basin," said Sean Smith, Chief Executive Officer of Centennial.

But the leadership structure was even more telling. When Hickey and Walter agreed to the merger, they made clear one nonnegotiable condition—that they must remain co-CEOs of the newly dubbed Permian Resources. Investors were initially unsure about their youth and the unusual shared-leadership arrangement. But the pair largely put those concerns to rest in the final three months of 2022.

Permian Resources will be headquartered in Midland and, in addition to Hickey and Walter, will be led by George Glyphis, Centennial's former CFO, and Matt Garrison, Centennial's former COO. Sean Smith, formerly CEO of Centennial, will serve as executive chair of the Permian Resources board of directors.

Permian Resources Corporation ("Permian Resources" or the "Company") today announced the successful completion of the combination of Centennial Resource Development, Inc. ("Centennial") (NASDAQ: CDEV) and Colgate Energy Partners III, LLC ("Colgate"). Strong balance sheet protects the business and return of capital program across commodity price cycles. Industry-leading shareholder alignment, with employee ownership exceeding 13%, management compensation highly weighted towards equity and performance. "Permian Resources brings together two successful E&P companies, creating a better, stronger and more strategically compelling company. The combined asset base is highly complementary with a deep inventory of high-quality locations that generate robust free cash flow across commodity price cycles," said Will Hickey, Co-CEO of Permian Resources.

He and James Walter, co-founder of Colgate and now co-CEO of Permian Resources, came to believe that combining Colgate and Centennial would maximize efforts to create value, bringing together two complementary, high-quality asset bases in the Delaware Basin. Hickey said headquartering the company in Midland was a key piece of the deal. "Being here was important to us, given how long we've been in Midland and what Midland means to us," Hickey said. "It creates a strategic competitive edge for us: It's close to the fields, our team can get there in a quick drive, the deals and relationships with the service companies are all done on the ground here."

VIII. Inflection Point #3: The Earthstone Acquisition (2023)

Less than a year after the merger closed, Permian Resources was back on the hunt.

Permian Resources Corporation and Earthstone Energy, Inc. today announced that they have entered into a definitive agreement under which Permian Resources will acquire Earthstone in an all-stock transaction valued at approximately $4.5 billion, inclusive of Earthstone's net debt. Under the terms of the transaction, each share of Earthstone common stock will be exchanged for a fixed ratio of 1.446 shares of Permian Resources common stock. The transaction strengthens Permian Resources' position as a leading Delaware Basin independent E&P.

The deal comes just days after Earthstone closed its acquisition of rival private-equity-backed Novo Oil & Gas for $1.5 billion, adding more than 200 high-return drilling locations and increasing its inventory to 13 years.

"We believe the acquisition of Earthstone represents a compelling value proposition for our shareholders and strengthens our position as a premier Delaware Basin independent E&P. Earthstone's Northern Delaware position brings high-quality acreage with core inventory that immediately competes for capital within our portfolio," said Will Hickey, Co-CEO of Permian Resources. "Additionally, we have identified numerous ways to leverage our deep Delaware Basin experience and incremental scale to improve upon these assets across the board, including approximately $175 million of annual synergies."

Andrew Dittmar, director at Enverus Intelligence Research, said that the deal "will give Permian Resources a pro forma market cap of about $10 billion, moving the company ahead of its peers Matador Resources and Civitas Resources, making it solidly the third largest (nearly) Permian pure-play behind Pioneer Natural Resources and Diamondback Energy." He noted that by acquiring a public company rather than a private equity acquisition, Permian Resources demonstrates a potential new approach for those looking to scale up in the region. "Rather than pursue the common private equity acquisition, Permian Resources is picking up another public company."

Permian Resources Corporation ("Permian Resources" or the "Company") (NYSE: PR) today announced that it has completed its acquisition of Earthstone Energy, Inc. ("Earthstone") (NYSE: ESTE). The transaction was previously approved by Permian Resources and Earthstone shareholders at special meetings held on October 30, 2023.

Through those deals, it built a position with five to six years of inventory that breaks even at less than $50/BBL WTI in the Delaware Basin, just a bit beneath PR's own inventory life of just over six years at that quality threshold.

IX. The Continued Roll-Up: 2024 Acquisitions and Integration Excellence

Having digested Earthstone, Permian Resources accelerated its "ground game" strategy—pursuing smaller, bolt-on deals that wouldn't overstrain the balance sheet while still adding meaningful acreage.

The integration of Earthstone is complete, and synergy capture is meaningfully ahead of schedule. Overall, the Company's success in both the acceleration and magnitude of synergies captured to-date has resulted in an increase of $50 million to the previously stated annual synergy target of $175 million, bringing the updated synergy target to $225 million per year.

As a result of the successful integration and synergy realization, during the quarter the Company reduced average spud-to-rig release days by 18% per well and average completion days by 50% per well on legacy Earthstone acreage compared to Earthstone's results from the first half of 2023. Additionally, Permian Resources has improved legacy Earthstone runtimes, benefiting overall production volumes, and realized approximately $1 per Boe of LOE and margin synergies through workover, compressor and midstream optimization initiatives.

On September 17, 2024, Permian Resources closed the previously announced Barilla Draw bolt-on acquisition of approximately 29,500 net acres, 9,900 net royalty acres and substantial midstream infrastructure located in the core of the Delaware Basin. The Company assumed operations on November 1, 2024 and has begun development on the acquired properties.

The Barilla Draw assets were part of a purchase from Occidental Petroleum Corp. completed Q3 for about $818 million. The transaction comprised about 27,500 net acres on Texas' side of the Permian sub-basin and around 2,000 net acres on New Mexico's side. The acquisition also gave Permian Resources over 100 miles of oil and gas pipelines and a water system with a water recycling capacity of about 25,000 bpd.

Since the beginning of 2023, Permian Resources remained active in high-grading its portfolio through a series of bolt-on acquisitions (3), acreage swaps (2), grassroots acquisitions (>140) and non-core divestitures (2). Overall, Permian Resources' portfolio optimization efforts added approximately 17,000 Permian net acres, 7,300 Permian net royalty acres and over 200 high-quality, gross operated locations in the core of the Delaware basin. The cumulative effect of these transactions resulted in the company replacing over 100% of its developed inventory during 2023 on a standalone basis for less than $100 million net of divestitures.

As a result of these acquisitions, Permian added 50,000 net acres and 20 thousand barrels of oil-equivalent per day of production in 2024 for a total consideration of about $1.2 billion.

The discipline is evident in how the company financed these deals. Permian Resources continues to maintain a strong financial position and low leverage profile upon closing the previously announced Barilla Draw bolt-on acquisition during the quarter. At September 30, 2024, the Company had $272 million in cash on hand and no amounts drawn under its revolving credit facility.

X. Financial Performance and Operational Excellence

The numbers tell a story of transformation.

Fourth Quarter 2024 Financial and Operational Highlights: Reported crude oil and total average production of 171.3 MBbls/d and 368.4 MBoe/d. Announced cash capital expenditures of $504 million, cash provided by operating activities of $872 million and adjusted free cash flow of $400 million.

The company achieved a nearly 50% increase in free cash flow per share compared to 2023 without increasing leverage. PR's 2025 plan is expected to continue generating significant free cash flow per share growth.

Cost leadership has become the company's calling card. The mid-point represents an approximately $0.10 per Boe reduction compared to Permian Resources' 2024 total controllable cash costs, demonstrating the Company's cost leadership and ability to successfully integrate acquired assets. Specifically, controllable cash costs consist of approximately $5.55 per Boe for LOE, $1.30 per Boe for GP&T expense and $0.90 per Boe for cash G&A.

Reported crude oil and total average production of 160.8 MBbls/d and 347.1 MBoe/d during the quarter. Reduced D&C costs to ~$800 per lateral foot, which represents a 16% decrease from 2023.

"Our team continues to do a tremendous job executing in the field and has improved upon the operational efficiencies gained earlier in the year. Most importantly, reduced cycle times have driven a significant reduction in well costs," said Will Hickey, Co-CEO of Permian Resources. "We are now drilling and completing wells for approximately $1 million cheaper than 2023."

The balance sheet remains fortress-like. Net debt-to-LQA EBITDAX at December 31, 2024 was 0.95x. Total liquidity was $3.0 billion.

Credit agencies have taken notice. Since the first quarter 2024, Moody's Ratings upgraded Permian Resources to Ba2 with positive outlook and S&P Global Ratings upgraded Permian Resources to BB with stable outlook. Giving effect to these upgrades, Permian Resources is rated BB (S&P), Ba2 (Moody's) and BB (Fitch).

Thomas Le Guay, a Vice President at Moody's Ratings, noted that Permian Resources' prudent financial policies have positioned it to generate free cash flow and reduce debt, even amidst lower oil price conditions. The Ba1 CFR reflects Permian Resources' large-scale production, primarily in the Delaware basin, and its commitment to sound financial policies and free cash flow generation. The company aims to maintain net leverage between 0.5x and 1.0x, as demonstrated by the 0.95x net leverage as of December 31, 2024.

XI. Playbook: Business and Investing Lessons

The Eight Pillars of Permian Resources' Success

1. The "Merger of Equals" Execution Model Most mergers of equals fail. The Centennial-Colgate combination succeeded because both sides brought complementary strengths: Centennial's public company infrastructure and Papa-era technical pedigree; Colgate's operational scrappiness and cost discipline. The key wasn't preventing culture clash—it was acknowledging that two cultures could coexist.

2. Disciplined Capital Allocation The company has maintained leverage at approximately 1x while executing over $5 billion in acquisitions since 2022. This isn't luck—it's philosophy. Every deal is stress-tested against low commodity price scenarios. The base dividend is designed to be sustainable "below $40 per barrel WTI over a multi-year period."

3. Operational Excellence as Competitive Weapon In a commodity business, cost is the primary differentiator. Reducing drilling and completion costs by 16% year-over-year while maintaining or improving well productivity creates structural advantages that compound over time.

4. Talent Retention Through Equity With employee ownership exceeding 13%, Permian Resources has aligned incentives across the organization. When workers are owners, they think differently about cost control and operational efficiency.

5. The Co-CEO Structure Unusual leadership arrangements usually fail. This one works because Hickey and Walter have complementary skill sets (engineering versus finance) and decades of friendship to fall back on when disagreements arise.

6. Integration Speed Capturing synergies "meaningfully ahead of schedule" isn't just a press release talking point—it's a competitive advantage. The faster integration happens, the sooner the combined entity can focus on growth rather than internal coordination.

7. The "Ground Game" While competitors chase headline-grabbing mega-mergers, Permian Resources has quietly executed over 140 grassroots transactions. This patient accumulation of working interests, royalty acres, and small bolt-ons compounds value without leveraging the balance sheet.

8. Staying Pure-Play Concentration in the Delaware Basin creates both risk and reward. The risk is geographic—a regulatory change in New Mexico or Texas would disproportionately affect the company. The reward is expertise—nobody knows the Delaware Basin better than a team that has devoted their careers to it.

XII. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

Entering the Permian Basin as a meaningful competitor requires billions of dollars in capital, technical expertise that takes years to develop, and access to Tier 1 acreage that simply isn't available at any price. With more than half of Permian production already concentrated among six producers, experts expect the region's consolidation trend to continue.

However, private equity continues to fund new entrants, and the SPAC structure that launched Centennial remains available to well-connected operators.

2. Bargaining Power of Suppliers: MEDIUM

Oilfield service companies have pricing power during upcycles, and labor shortages can constrain activity. But Papa's EOG-forged philosophy of in-house technological development—now embedded in Permian Resources' culture—reduces dependence on service company innovations.

3. Bargaining Power of Buyers: LOW

Oil is a global commodity with transparent pricing. Multiple takeaway options from the Permian mean buyers can't dictate terms. The one exception is natural gas, where local pricing at the Waha Hub can disconnect sharply from broader markets due to infrastructure constraints.

4. Threat of Substitutes: MEDIUM-HIGH (Long-term)

Electric vehicles are reducing gasoline demand growth in developed markets. Renewables are capturing market share in power generation. But petrochemical demand remains robust, global demand continues growing in developing markets, and the timeline for meaningful substitution is measured in decades, not years.

5. Competitive Rivalry: HIGH

The U.S. energy industry recently experienced an extraordinary run of oil and gas mergers in the Permian Basin, with deals exceeding $100 billion in total value. The standout transaction is ExxonMobil's historic $64.5 billion acquisition of Pioneer Natural Resources, a move that cements the region's status as the nation's premier oil-producing area.

Diamondback Energy then stepped in with its own $26 billion deal to acquire Endeavor Energy Resources. This merger potentially makes Diamondback the third-largest Permian producer, trailing only after ExxonMobil and Chevron. Alongside these high-profile acquisitions, Occidental's $12 billion purchase of CrownRock and Permian Resources' $4.5 billion buyout of Earthstone Energy rounded out a record-breaking flurry of deals.

Permian Resources competes daily against the largest, most well-capitalized energy companies on Earth.

XIII. Hamilton's Seven Powers Analysis

1. Scale Economies: STRONG

As of December 31, 2024, we have approximately 450,000 net leasehold acres and approximately 88,000 net royalty acres.

Spreading fixed costs across this acreage base creates meaningful per-barrel advantages. The company's controllable cash costs of approximately $7.75 per BOE position it among the lowest-cost operators in the basin.

2. Network Effects: WEAK

Limited in upstream oil & gas. Some benefits accrue from midstream relationships and takeaway access, but these aren't true network effects.

3. Counter-Positioning: MODERATE

As a pure-play Delaware Basin operator, Permian Resources can move faster than diversified majors. The co-CEO structure with founder-led mentality creates agility that large corporate bureaucracies struggle to replicate.

4. Switching Costs: WEAK

Oil is a commodity; customers buy on price. Some stickiness exists in midstream contracts, but this doesn't create durable advantage.

5. Branding: WEAK

This is a B2B commodity business. Reputation matters for M&A, talent acquisition, and increasingly ESG positioning, but brand doesn't command pricing power.

6. Cornered Resource: STRONG

Through those deals, it built a position with five to six years of inventory that breaks even at less than $50/BBL WTI in the Delaware Basin.

Tier 1 acreage in the Delaware Basin is finite and irreplaceable. The company's concentrated position in Eddy, Lea, Reeves, and Ward counties represents geological advantage that competitors cannot replicate.

7. Process Power: STRONG

The integration track record demonstrates embedded organizational knowledge. Reducing drilling and completion costs by 16% year-over-year while improving cycle times reflects process capabilities that compound over time.

XIV. Bull Case and Bear Case

The Bull Case

Operational Excellence Compounding: The 16% reduction in D&C costs isn't a one-time event—it's the continuation of a multi-year trend. If management can continue extracting efficiencies at even half this rate, the company's cost advantage widens every year.

Consolidation Leader: Conoco could potentially seek to acquire Permian Resources, Civitas, Coterra, Vital Energy or Ovintiv, according to analysts. In a basin experiencing unprecedented consolidation, Permian Resources represents an attractive acquisition target—or could continue acquiring smaller operators itself.

Credit Upgrade Trajectory: "We are proud of our financial strength and have comparable attributes to our investment grade peers. As a result, we are targeting investment grade credit ratings in 2025," said Guy Oliphint, Chief Financial Officer. Investment grade status would lower borrowing costs and potentially attract index inclusion.

Commodity Price Optionality: As of the end of 2024, Permian's reserves totaled 1,026,957 Mboe, which represented an 11% year-over-year expansion. Since the end of 2020, the company has expanded its reserves by 244%. This reserve base appreciates if oil prices rise.

The Bear Case

Commodity Price Exposure: A sustained decline in oil prices to $50/bbl or below would pressure margins, reduce free cash flow, and potentially trigger impairments. The company has limited geographic diversification to offset Permian-specific pricing challenges.

Waha Gas Pricing: Natural gas prices at the Waha Hub have traded at significant discounts—sometimes negative—due to infrastructure constraints. While oil dominates production mix, continued gas pricing pressure affects economics.

Parent Well Interference: As the basin matures, parent-child well interactions increasingly affect productivity. The industry faces mounting evidence of productivity declines in highly developed areas.

Regulatory Risk: Operations in New Mexico and Texas expose the company to state-level regulatory changes. Environmental restrictions, methane regulations, or permitting delays could impact operations.

Competition for Tier 1 Inventory: "In terms of companies that could really move the needle and put a public company into the upper echelon of inventory holders, there's frankly no one to the size of Endeavor left," an analyst told CNBC, referring to private companies that can still be scooped up. Scarcity of attractive acquisition targets may constrain future growth.

XV. Key Performance Indicators to Watch

For investors tracking Permian Resources' ongoing performance, three metrics stand above all others:

1. Controllable Cash Costs per Boe Currently targeting $7.75/Boe, this metric captures lease operating expense, gathering/processing/transportation expense, and cash G&A. Continued reduction signals operational excellence; increases suggest cost pressures or integration challenges.

2. Free Cash Flow per Share Growth The company achieved a nearly 50% increase in free cash flow per share in 2024. This metric captures the combined effect of production growth, cost reduction, and capital discipline. Sustained per-share growth—not just absolute growth—indicates value creation rather than empire building.

3. Net Debt-to-EBITDAX Ratio Currently 0.95x with a target range of 0.5x-1.0x. This metric reveals balance sheet discipline and acquisition capacity. Rising leverage suggests overpayment for deals or operational stress; declining leverage indicates financial strengthening.

XVI. Conclusion: The Roll-Up Revolution Continues

In September 2022, when Permian Resources formed from the combination of Centennial Resource Development and Colgate Energy, the cynics had plenty of ammunition. Mergers of equals rarely work. Co-CEO structures usually fail. The Delaware Basin was already crowded with well-capitalized competitors.

Two years later, the results speak for themselves. In 2024, Permian Resources's revenue was $5.00 billion, an increase of 60.23% compared to the previous year's $3.12 billion. Earnings were $984.70 million, an increase of 106.74%.

The company has completed billions in acquisitions while maintaining leverage around 1x. Integration synergies have exceeded expectations. Credit agencies have upgraded the company multiple times. Production has grown while costs have fallen.

"Permian Resources had another outstanding year in 2024, and we could not be more proud of our team for everything they accomplished last year," said Will Hickey, Co-CEO. "With our low cost structure serving as the foundation, Permian Resources delivered peer leading per share growth during 2024, which helped generate a superior total return for our shareholders." "We are excited to announce our 2025 plan, which is highlighted by 8% higher annual production and no change to our approximately $2 billion capital budget from 2024. This improved year-over-year capital efficiency is driven by our consistent development approach and significantly lower cost structure," said James Walter, Co-CEO.

The Permian Resources story isn't about oil—it's about execution. It's about two childhood friends who moved to Midland with $75 million in backing and refused to leave until they'd built something enduring. It's about the DNA of operational excellence that Mark Papa embedded at EOG, transferred to Centennial, and now lives on in a company he no longer leads. It's about what happens when disciplined capital allocation meets irreplaceable geology.

The roll-up revolution in America's oil heartland continues. Permian Resources has positioned itself not just to survive the consolidation wave, but to ride it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube