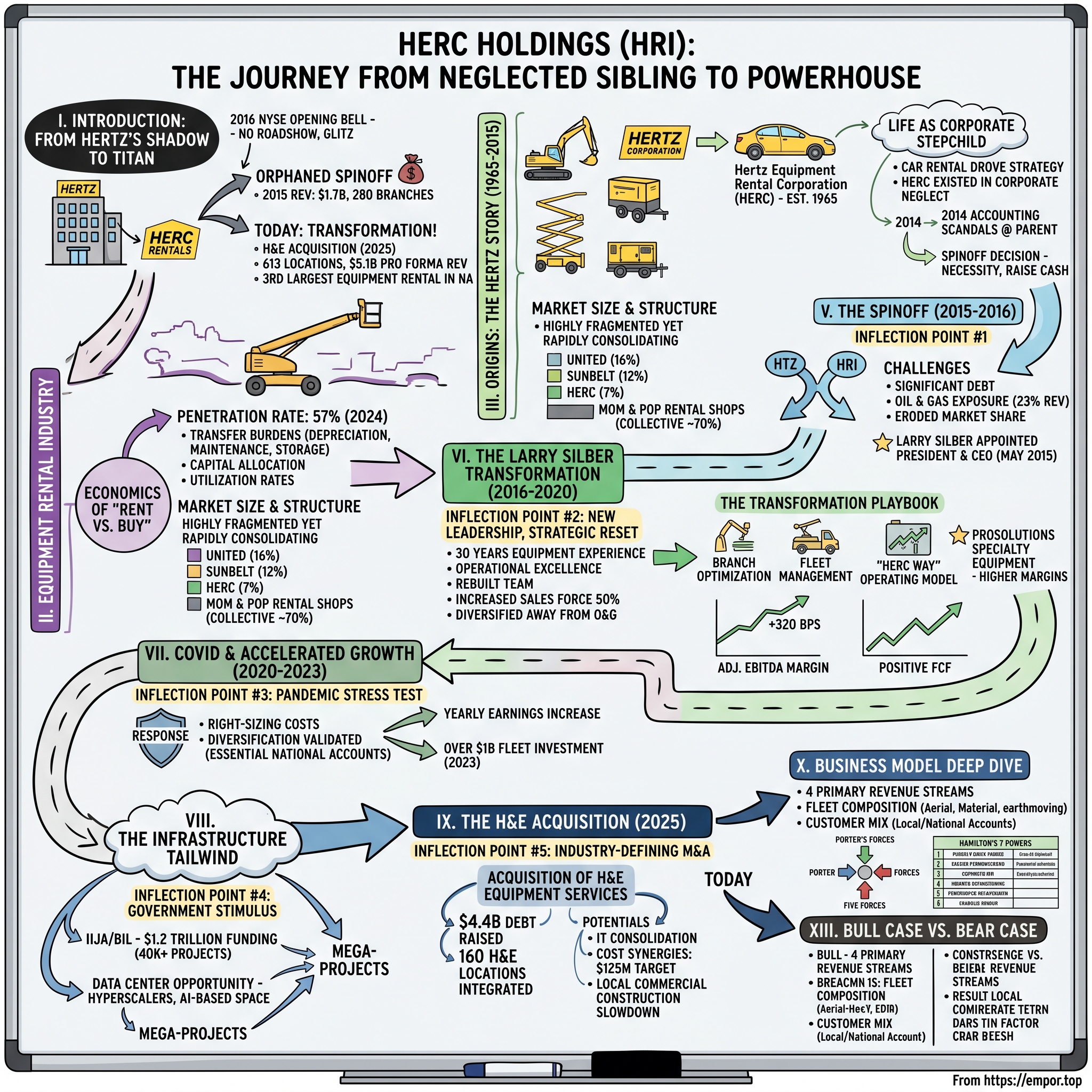

Herc Holdings: The Forgotten Sibling That Became a Powerhouse

I. Introduction: From Hertz's Shadow to Industry Titan

On July 1, 2016, a peculiar ceremony took place on the floor of the New York Stock Exchange. Larry Silber, a soft-spoken industrialist with three decades of equipment experience, stood with his newly independent executive team to ring the opening bell. The company he was launching had no IPO roadshow, no glitzy investor presentations, no celebratory champagne toasts at Goldman Sachs. Instead, Herc Holdings emerged into the world as an orphan—a cast-off business unit from a car rental company drowning in accounting scandals, saddled with $2 billion in debt it had just transferred to its former parent, and facing a North American equipment rental market dominated by competitors who had spent years building scale while Herc languished as a corporate afterthought.

The company's common stock began trading "regular way" on the New York Stock Exchange under the symbol "HRI." Herc Rentals was a premier, full-line equipment-rental firm with approximately 280 company-operated branches, principally located in North America, more than 4,600 employees and 2015 revenues of nearly $1.7 billion.

Few observers gave Herc much chance. The equipment rental industry had already crowned its champions—United Rentals and Sunbelt Rentals had spent years consolidating the fragmented market, building the purchasing power, branch networks, and national account relationships that separate winners from also-rans. "We are thrilled to begin the next chapter in the history of our company," said Larry Silber, president and CEO. "We are strategically positioned to generate above-market growth with significant opportunities for operational and financial improvement. As an independent company, Herc Rentals now has the financial and operational flexibility to pursue strategies that are specific to the equipment rental business."

Nine years later, that orphaned spinoff has transformed into something remarkable. With the recent acquisition of H&E Equipment Services, Herc Holdings now has 613 locations across North America and pro forma 2024 total revenues were $5.1 billion. The company that started with 280 branches now operates more than double that footprint. The third-largest equipment rental company in North America—behind only United Rentals and Sunbelt—Herc has delivered one of the most successful corporate turnaround stories in industrial services.

This is a story about what happens when a neglected subsidiary finally gets the attention it deserves. It's a story about an industry undergoing fundamental transformation, where the economics of renting versus owning are shifting in favor of rental companies at an accelerating pace. And it's a story about a leadership team that understood exactly what was broken and how to fix it.

II. The Equipment Rental Industry: Understanding the Business

Before dissecting Herc's journey, one must understand the industry that shapes its destiny. Equipment rental might sound mundane—excavators, aerial lifts, generators for construction sites—but beneath this utilitarian surface lies one of the most fascinating business models in American industry.

Walk onto any major construction site in North America, and you'll see the business case for rental playing out in real-time. A contractor building a data center in Northern Virginia needs crawler excavators for site prep, aerial lifts for electrical work, generators for power before the grid connects, and climate control equipment for testing server rooms. That equipment represents hundreds of thousands of dollars in capital. For a single project lasting eighteen months, should the contractor buy it outright?

The answer, increasingly, is no. The EquipmentWatch report notes ARA's finding that more businesses are choosing rental over ownership, with the U.S. rental penetration rate increasing for the fourth consecutive year and hitting 57% in 2024. This fundamental shift—from ownership to access—has become the equipment rental industry's central narrative.

The Economics of "Rent vs. Buy"

The math works like this: A contractor who owns a $150,000 excavator faces depreciation, maintenance, insurance, storage, and the opportunity cost of capital. When that excavator sits idle between projects—which happens frequently in the cyclical construction business—those costs don't stop accruing. Rental transfers all those burdens to the rental company, which can achieve utilization rates that individual contractors cannot.

Infrastructure Investment and Jobs Act (IIJA) funding, contractor migration toward asset-light business models, and large data-center and renewable-energy projects collectively keep equipment utilization high across the region. Major federal allocations support more than 56,000 transportation schemes, and projects valued above USD 50 million have risen 42%, sustaining consistent excavator and road-equipment demand.

The trend toward rental accelerates during economic uncertainty—exactly the opposite of what one might expect. Labor shortages—estimated at 439,000 additional workers in 2024—are pushing contractors toward rental subscriptions and push-button technologies that offset skilled-operator gaps. When contractors don't know what the next twelve months hold, they prefer variable costs to fixed assets sitting in their yards.

Market Size and Structure

Equipment rental revenue, comprised of the construction/industrial and general tool segments, is expected to grow by 5.7 percent in 2025 to reach a total of nearly $82.6 billion, topping the nearly $78.2 billion recorded in 2024, according to the latest forecast released in early November by the American Rental Association (ARA).

The North American construction equipment rental market is expected to reach USD 36.76 billion in 2025 and grow at a CAGR of 4.20% to reach USD 45.16 billion by 2030. Deere & Company, United Rentals, Inc., Herc Rentals Inc., Caterpillar Inc. and Sunbelt Rentals are the major companies operating in this market.

What makes this market particularly interesting is its structure: highly fragmented yet rapidly consolidating. The major competitors—United Rentals, Sunbelt Rentals (owned by Ashtead Group), and Herc Rentals—collectively have approximately 30% market share. In North America, most of the remainder of the market is made up of small local independent rental shops.

This creates a classic consolidation opportunity. United Rentals, Sunbelt, and Herc Rentals were the leading three companies for equipment rental services in the United States in 2022. United Rentals controlled about 16 percent of the market, while Sunbelt held 12 percent of the total market.

The industry's characteristics make scale enormously valuable: purchasing power with equipment manufacturers, ability to serve national accounts across multiple geographies, and technology investments that can be amortized across a larger base. Yet the market remains fragmented enough that significant consolidation opportunities persist.

III. Origins: The Hertz Equipment Rental Story (1965–2015)

The company that became Herc Holdings traces its roots to 1965, when The Hertz Corporation—already a giant in car rental—decided to leverage its brand and customer relationships into adjacent rental categories. The company was founded in 1965 as a subsidiary of The Hertz Corporation. It was originally named Hertz Equipment Rental Corporation (HERC). It was the second largest equipment rental company as of 1994.

The strategic logic seemed sound: Hertz had mastered the logistics of renting expensive capital equipment, tracking utilization, managing maintenance, and building customer relationships. Why not apply those capabilities to excavators and aerial lifts?

For three decades, HERC grew into a substantial business—by 1994, it ranked as the second-largest equipment rental company in North America. But that success belied a fundamental tension within the Hertz corporate structure. Car rental and equipment rental might share a common verb ("rent"), but they're vastly different businesses. Car rental operates on short cycles—days, sometimes weeks. Equipment rental involves longer commitments, more complex maintenance requirements, and deeper customer relationships.

Life as a Corporate Stepchild

Ford Motor Company considered acquiring HERC in 2002 but opted not to. In 2013, HERC's headquarters were moved from Park Ridge, New Jersey to Estero, Florida. The company generated over $1.5 billion in revenue in 2013, which was 14% of Hertz's total revenue.

That 14% of revenue figure tells the story. While HERC contributed meaningful revenue, it was never the main attraction. Car rental drove Hertz's strategy, its capital allocation, its management attention. HERC existed in a perpetual state of corporate neglect—enough investment to keep the lights on, never enough to truly compete with focused competitors.

The challenges of this structural disadvantage became increasingly apparent as the equipment rental industry consolidated around United Rentals and Ashtead's Sunbelt brand. While those companies aggressively acquired competitors, invested in technology, and built national account capabilities, HERC largely stood still.

By 2014, the situation had become untenable. Hertz faced its own crises—accounting irregularities that would eventually force restatements of financial results, activist investor Carl Icahn accumulating a stake and demanding change, and a car rental business struggling to adapt to ride-sharing disruption.

In early 2014, Carl Icahn became a major shareholder, and over time, took an increasingly active role while padding his stake in the company (over 15% today). Claiming HERC could lead a better life on its own, Hertz made plans to escape with Icahn's help. It was around that same time investors became privy to waves of internal dysfunction.

The decision to spin off HERC wasn't born of strategic vision—it was born of necessity. Hertz needed to raise cash, simplify its corporate structure, and allow investors to value its businesses separately. For HERC, this represented both crisis and opportunity.

IV. The Industry Revolution: Brad Jacobs and the United Rentals Model

To understand what Herc faced as an independent company, one must understand what Brad Jacobs had built at United Rentals. Few entrepreneurs have left a more distinctive fingerprint on American industry than Jacobs, who by 2016 had created five separate billion-dollar companies through a single playbook: identify fragmented industries where scale creates advantage, then roll up competitors faster than anyone thought possible.

United Rentals was founded as a roll-up in 1997 by serial entrepreneur Brad Jacobs. After dropping out of Brown in 1976 to start an oil brokerage trading firm, he started a roll-up of the garbage hauling industry which he eventually sold to Waste Management before founding United Rentals.

Jacobs saw something in equipment rental that others missed. The equipment-rental industry was 'a $20-billion-a-year market, highly fragmented into more than 20,000 mom-and-pop rental shops; the top 100 companies had less than a 20 percent share of the industry.' Equipment rental was 'a booming business, growing 15 percent a year, where economies of scale' were a tremendous advantage.

The United Rentals playbook was brutally effective. Jacobs started United Rentals by purchasing six leasing companies and bringing the combined company public in 1997. They quickly acquired US Rentals in 1998, making them the largest US rental company, with annual sales of $1.4 billion and market share of ~7%. Jacobs went on to do ~200 acquisitions over the next five years.

The RSC Merger: Industry Transformation

The defining moment in equipment rental consolidation came in 2012. The largest merger in rental equipment history was finalized on April 30, 2012, boosting URI to what was at the time a 13 percent market share of the equipment rental industry. In 2013, United Rentals moved its headquarters from Greenwich, Connecticut, to Stamford, Connecticut.

United has agreed to acquire RSC for $18.00 per share, a total enterprise value of $4.2 billion, including $2.3 billion of net debt. Upon the closing of the transaction, each outstanding share of RSC common stock will be converted into the right to receive $10.80 in cash and 0.2783 of a share of United Rentals common stock. The transaction provides immediate value to RSC stockholders through the cash component. The price of $18.00 per share represents a 58-percent premium over RSC's closing price as of Dec. 15.

This merger created an equipment rental behemoth and set the industry template that Herc would eventually need to follow. Consolidation remains brisk, reinforcing an oligopolistic pricing environment.

V. The Spinoff: Birth of an Independent Company (2015–2016)

Inflection Point #1: The Spinoff Decision

The separation of HERC from Hertz was neither clean nor elegant. Years of accounting problems at the parent company had delayed the process repeatedly. After multiple delayed filings, on June 6, 2014, Hertz issued an item 4.02: non-reliance on previously issued financial statements. The Audit Committee has concluded that the financial statements for 2011 should no longer be relied upon, and Hertz must restate them. Hertz also needs to correct the 2012 and 2013 financial statements to reflect these errors.

When the spinoff finally occurred, it came structured in a way that maximized benefit to Hertz rather than to the newly independent company. The spin-off raised $2 billion for Hertz to reduce its own debt. On July 1, 2016, Herc Rentals Inc. became an independently traded company (NYSE: $HRI).

The mechanics of the transaction revealed its true purpose. To make it simpler, a shareholder with 15 shares of HTZ pre-spinoff should have ended up with 3 shares of the new HTZ and 1 share of HRI. Additionally, as part of the transaction, Hertz received ~$2b in proceeds which it will use to pay down debt and repurchase shares.

The Challenges Facing the New Company

Herc emerged into independence facing a formidable set of challenges. The company carried significant debt from the spinoff transaction. Its oil and gas exposure—roughly 23% of 2015 revenue—was problematic given the collapse in energy prices. Market share had eroded during the years of neglect. And the company had no track record as a standalone public entity.

But Larry Silber saw opportunity where others saw problems. Hertz announced that Lawrence (Larry) H. Silber has been appointed President and CEO of Hertz Equipment Rental Corporation (HERC), replacing Brian MacDonald, who has stepped down, effective immediately. On May 14, 2015, the Company reiterated its intention to separate the equipment and car rental businesses into two publicly traded companies. "Given his deep set of experiences in the heavy equipment sector, we are excited to have Larry Silber lead HERC's business transformation, while also helping us navigate through the HERC separation process," said Mr. Tague.

VI. The Larry Silber Transformation (2016–2020)

Inflection Point #2: New Leadership and Strategic Reset

Larry Silber was not a flashy executive. He didn't court media attention or speak in soaring rhetoric about transforming industries. What he brought to Herc was something more valuable: thirty years of deep operational experience in the equipment business, honed at Ingersoll Rand and tested through multiple business cycles.

Mr. Silber joined Herc Rentals Inc. in May 2015. Prior to that, Mr. Silber served as an executive advisor at Court Square Capital Partners, LLP. Mr. Silber led Hayward Industries, one of the world's largest swimming pool equipment manufacturers, as chief operating officer from 2008 to 2012, overseeing a successful transition through the recession and returning the company to solid profitability. From 1978 to 2008, Mr. Silber worked for Ingersoll-Rand plc, a publicly traded manufacturer of industrial products and components, in a number of roles of increasing responsibility. He led major Ingersoll-Rand business groups, including Utility Equipment, Rental and Remarketing and the Equipment and Services businesses.

Silber understood what HERC needed wasn't revolutionary vision—it needed operational excellence. The company had to execute on fundamentals: fleet management, branch optimization, sales force effectiveness, and customer diversification.

"We will continue to expand our operations and to invest in all areas of our business, including new product lines such as ProContractor Tools and ProTruck line of commercial vehicles to complement our large selection of premium general equipment products," added Silber. "In addition, our new ProSolutions business provides specialty equipment, technical expertise, and full-service, onsite support to solve our customers' toughest challenges. We are also advancing processes and tools designed to drive continuous improvement across our company and to provide a higher level of service for our customers. Most notably, our enterprise-wide 'Herc Way' operating model ensures a consistent branch-to-branch approach to managing, servicing and repairing our fleet and rapidly gets equipment ready to rent, which will greatly improve our opportunities to serve more customers."

The Transformation Playbook

Silber's approach was methodical. First, he rebuilt the leadership team, bringing in experienced operators who understood the equipment rental business. Second, he invested in the sales force—increasing headcount by 50%—because revenue growth required feet on the ground building customer relationships. Third, he diversified away from the oil and gas exposure that had made the company vulnerable to commodity cycles.

The introduction of ProSolutions represented a strategic pivot toward higher-margin specialty equipment. Rather than competing purely on price for commodity excavators and aerial lifts, Herc began building expertise in solutions that required technical knowledge: power generation, climate control, remediation and restoration, pump systems, and trench shoring. These specialty lines demanded more sophisticated sales approaches but generated better margins and stickier customer relationships.

Between 2016 and 2020, the company spent $1.8 billion into expanding its rental fleet.

The results by 2019 spoke for themselves: improved adjusted EBITDA margin by 320 basis points to 39.7%, increased dollar utilization 80 basis points to 40.5%, and transformed free cash flow from negative $7.9 million in 2018 to a positive $172 million in 2019.

The geographic strategy focused on urban markets with dense construction activity, where Herc could achieve better utilization and serve more customers per branch. National account revenue grew to represent about 45% of total rental revenue, providing more predictable revenue streams while local rental revenue at 55% maintained exposure to higher-margin spot opportunities.

VII. COVID and Accelerated Growth (2020–2023)

Inflection Point #3: The Pandemic Stress Test

When COVID-19 swept across North America in March 2020, equipment rental companies faced an immediate stress test. Construction sites shut down in many jurisdictions. Industrial activity collapsed. The economic uncertainty that theoretically favors rental over ownership manifested in a way no one wanted—by crushing demand for both.

Herc's response demonstrated the operational discipline Silber had built. The company right-sized costs rapidly, managed fleet investments prudently, and maintained liquidity. More importantly, the pandemic validated the company's customer diversification strategy. National accounts—primarily essential businesses like utilities, energy companies, healthcare facilities, and agricultural operations—proved far more resilient than local construction accounts.

Post-Pandemic Surge

The recovery that followed exceeded almost everyone's expectations. Its yearly earnings increased by 28% in 2021, and by 35% in 2022. The company continued to grow in 2023, when its revenues increased by 18%.

The company invested between $525 and $575 million into its rental fleet in 2021, and over $1 billion in 2023.

The pandemic had permanently shifted contractor behavior. Supply chain disruptions made purchasing equipment even more challenging. Economic uncertainty reinforced the advantages of variable over fixed costs. And the infrastructure spending bills working through Congress promised years of sustained demand.

M&A Strategy Takes Shape

With strengthened finances and market position, Herc began deploying capital more aggressively for acquisitions. After spinning off, Herc Rentals has acquired a number of other companies, including CBS Rentals, All-Star Rents, Dwight Crane, Reliable Equipment, All Reach, and Champion Rentals.

Prior to this transaction, Herc Rentals had completed more than 50 acquisitions in the past five years.

Each acquisition served the core strategy: building density in attractive markets, adding specialty capabilities, and gaining scale advantages in procurement and operations.

VIII. The Infrastructure Tailwind

Inflection Point #4: Government Stimulus

In November 2021, President Biden signed the Infrastructure Investment and Jobs Act, authorizing the largest federal infrastructure investment in decades. For equipment rental companies, this represented a generational demand catalyst.

The Infrastructure Investment and Jobs Act (IIJA), aka Bipartisan Infrastructure Law (BIL), was signed into law by President Biden on November 15, 2021. The law authorizes $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward "new" investments and programs. Funding from the IIJA is expansive in its reach, addressing energy and power infrastructure, access to broadband internet, water infrastructure, and more.

The impact on equipment rental extends beyond simple infrastructure spending. By the law's second anniversary in November 2023, around $400 billion from the law, about a third of all IIJA funding, was allocated to more than 40,000 projects related to infrastructure, transport, and sustainability. By May 2024, the law's halfway mark, the numbers had increased to $454 billion (38 percent of the Act's funds) for more than 56,000 projects.

The Data Center Opportunity

Beyond traditional infrastructure, a new demand driver emerged: the explosive growth of data center construction. Primary markets had a record 6,350 MW under construction at the end of 2024, more than double the 3,077.8 MW at year-end 2023. This surge was driven by robust demand and extended construction timelines due to power constraints and supply chain delays. The overall vacancy rate in primary markets fell to a record-low 1.9% at year-end.

Hyperscalers such as Amazon, Meta and Microsoft are pushing the trend by ramping up their investments and demanding new artificial intelligence-based data center space. Meta, for instance, was in talks in February to secure a roughly $35 billion financing package for a major data center campus in the U.S. And, in January, Microsoft announced it would invest $80 billion of its budget for the fiscal year 2025 in building data centers in the U.S.

Data center construction is particularly equipment-intensive, requiring excavators for site preparation, aerial lifts for electrical work, generators for temporary power, and climate control systems for testing. These projects run on tight schedules with premium pricing—ideal conditions for equipment rental companies.

IX. The H&E Acquisition: A Transformative Deal (2025)

Inflection Point #5: Industry-Defining M&A

By early 2025, Herc had proven its operational capabilities and built financial strength. What remained was scale—the ability to compete more effectively against United Rentals and Sunbelt for the largest national accounts and procurement leverage with equipment manufacturers.

The opportunity arrived in dramatic fashion. United Rentals had announced its intention to acquire H&E Equipment Services, a significant regional player with strong positions across the Sun Belt states. But under H&E's merger agreement, the company retained a "go-shop" provision allowing it to consider superior offers.

Herc Holdings and H&E have entered into a definitive merger agreement under which Herc will acquire H&E. As previously announced on February 18, 2025, under the terms of the Herc and H&E agreement, H&E shareholders will receive $78.75 in cash and 0.1287 shares of Herc common stock for each share they own, with a total value of $104.89 per share based on Herc's 10-day VWAP as of market close February 14, 2025.

Herc's bid represented a bold strategic bet. Under the terms of the Herc proposal, H&E shareholders would receive $78.75 in cash and 0.1287 shares of Herc common stock for each share they own, with a total value of $104.89 per share based on Herc's 10-day VWAP. Following the close of the transaction, H&E's shareholders would own approximately 14.1% of the combined company. Herc's proposal represents a 14.0% premium to United Rentals' $92.00 per share cash-capped consideration.

In accordance with the terms of H&E's prior agreement with United Rentals, Herc, on behalf of H&E, has paid a termination fee of $63,523,892 to United Rentals.

Acquisition Completion and Integration

Herc Holdings today announced that it has completed its acquisition of H&E Equipment Services, Inc. d/b/a H&E Rentals. "The acquisition of H&E accelerates Herc's proven strategy and strengthens our position as a premier rental company in North America," said Larry Silber, Herc Rentals' president and chief executive officer. "The addition of H&E's network and capabilities provides Herc with a leading presence in 11 of the top 20 rental regions, a larger fleet that provides our customers with a range of specialty and general rental products."

The financing required was substantial. The company raised $4.4 billion in debt at a weighted average cost of debt (WACD) of 6.8% to finance the transaction, despite what it described as bond market volatility.

The company integrated over 160 H&E locations, aiming for $125 million in cost synergies. Industrial and infrastructure spending is expected to boost market opportunities, with forecasts exceeding $2 trillion in megaprojects.

Integration Progress and Challenges

The integration has proceeded rapidly but not without challenges. "In the third quarter, we achieved a major milestone by completing the full IT integration—successfully migrating all of the acquired branches onto Herc's systems and network infrastructure within a best-in-class timeline.

Herc Holdings expects $300 million in incremental EBITDA from the H&E acquisition, with revenue and cost synergies contributing. The integration of H&E is nearly complete, with IT consolidation and field realignment finalized. Herc aims to reduce its leverage ratio to 2-3x by the end of 2027, leveraging both EBITDA growth and debt reduction. The company is optimistic about demand from mega-projects, such as data centers and LNG plants, for 2026.

However, the acquisition came at a challenging moment for H&E's legacy business. Local commercial construction slowed further due to prolonged higher interest rates, impacting H&E's core business. This led to a double-digit decline in H&E rental revenue, with management attributing part of the weakness to employee turnover and project delays.

X. Business Model Deep Dive

Understanding Herc's competitive position requires examining how the business actually generates value. The company operates through four primary revenue streams: equipment rental (the core business), used equipment sales, services (delivery, pickup, maintenance), and supplies.

Fleet Composition and Economics

With a total fleet size of $9.9 billion at original equipment cost (OEC), Herc maintains a balanced mix across equipment categories. The fleet composition breaks down as: aerial equipment (26%), material handling (22%), specialty (18%), earthmoving (14%), and other general equipment (20%).

Fleet management represents the core operational challenge in equipment rental. Each piece of equipment follows a lifecycle: procurement (at negotiated prices leveraging purchasing power), deployment (optimizing utilization across branches), maintenance (extending useful life while maintaining safety and performance), and disposition (selling used equipment at optimal timing and pricing).

The company is focusing on fleet efficiency, with disposals increasing both sequentially and year-over-year to optimize utilization. In Q2 2025, disposals generated proceeds of approximately 44% of OEC, with the average fleet age at 46 months and disposed equipment averaging 85 months.

The ProSolutions Strategy

Herc's specialty business—branded ProSolutions—represents the company's margin-expansion strategy. Herc's specialty business represented 24% of its total $6.9 billion fleet in Q1, Chief Operating Officer Aaron Birnbaum said during its April 22 earnings call.

Specialty equipment—power generation, climate control, pumps, trench shoring—commands higher margins than commodity rental equipment for several reasons. It requires technical expertise to deploy effectively, creating switching costs. Projects that need specialty equipment often have urgent timelines and premium budgets. And the competitive set is smaller than for general equipment.

Customer Mix as Risk Management

Herc's 60/40 split between local and national accounts represents deliberate portfolio construction. Local accounts—contractors working specific projects—offer higher rates but shorter duration and more cyclicality. National accounts—large companies with ongoing equipment needs across multiple locations—provide more predictable revenue but at more competitive pricing.

XI. Competitive Analysis: Porter's Five Forces

1. Threat of New Entrants: LOW-MODERATE

The equipment rental industry presents significant barriers to entry at scale. Capital requirements for fleet investment are substantial—Herc's fleet represents nearly $10 billion at original equipment cost. Established relationships with equipment manufacturers provide procurement advantages. Consolidation remains brisk, reinforcing an oligopolistic pricing environment.

However, entry at local/regional scale remains feasible. A contractor with industry relationships can start a rental operation serving a geographic niche. The challenge is achieving the scale necessary to compete on national accounts or negotiate meaningfully with OEMs.

2. Bargaining Power of Suppliers: MODERATE

Equipment manufacturers—Caterpillar, John Deere, JLG, Terex—hold significant leverage. Their products aren't fully commoditized; brand, reliability, and support matter. However, the largest rental companies have substantial bargaining power. Industry sources suggest larger companies can obtain significant discounts—some reports cite 40% or more on equipment that retails for $50,000 or above.

3. Bargaining Power of Buyers: MODERATE-HIGH

Contractors can switch between rental providers with relative ease. Price sensitivity varies significantly by customer segment—large national accounts negotiate aggressively while smaller local contractors prioritize availability and service. The competitive dynamic in concentrated markets gives buyers alternatives.

4. Threat of Substitutes: LOW

Equipment ownership is the primary substitute for rental. The U.S. construction and industrial equipment rental market continued its upward trend in the first quarter of 2025, with rental penetration reaching a record high of 57%, surpassing pre-pandemic levels. The long-term trend continues favoring rental over ownership as economic uncertainty persists and contractors optimize working capital.

5. Competitive Rivalry: HIGH

Three dominant players—United Rentals, Sunbelt (Ashtead), and Herc—compete intensively across price, availability, service quality, and branch density. United Rentals alone posted USD 13.029 billion rental revenue in 2024. Ongoing consolidation intensifies competition as the largest players achieve greater scale advantages.

XII. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

Scale creates multiple advantages in equipment rental: purchasing power with OEMs, fleet optimization across larger networks, fixed cost leverage, and technology investment amortization. The H&E acquisition explicitly targeted these scale benefits.

2. Network Effects: WEAK

Unlike software platforms, equipment rental doesn't benefit strongly from network effects. A contractor in Phoenix doesn't care that Herc has branches in Boston. However, some benefit exists for national accounts that value single-provider relationships across geographies.

3. Counter-Positioning: MODERATE (historically)

As a Hertz subsidiary, HERC couldn't pursue strategies that conflicted with parent company priorities. Larry Silber noted, "As an independent company, Herc Rentals now has the financial and operational flexibility to pursue strategies that are specific to the equipment rental business."

4. Switching Costs: LOW-MODERATE

Customer relationships and service history create some retention. National account contracts provide switching friction. ProSolutions specialty services may increase switching costs through technical dependencies and ongoing service relationships.

5. Branding: MODERATE

The "Herc" brand—derived from Hertz Equipment Rental Corporation's initials—maintains connection to fifty years of industry presence. Safety records and service quality build reputation in the B2B context where word-of-mouth matters significantly.

6. Cornered Resource: WEAK

No proprietary technology or exclusive resources differentiate Herc. Equipment is available from OEMs to any buyer. Human capital in sales and technical service provides some advantage but isn't truly cornered.

7. Process Power: EMERGING

The "Herc Way" operating model—standardized approaches to fleet management, customer service, and branch operations—represents process improvement that competitors cannot easily replicate overnight. Technology investments in fleet management (ProControl platform) and customer service tools continue building this capability.

XIII. Bull Case vs. Bear Case

The Bull Case

Secular Tailwinds: Infrastructure Investment and Jobs Act (IIJA) funding, contractor migration toward asset-light business models, and large data-center and renewable-energy projects collectively keep equipment utilization high across the region. Major federal allocations support more than 56,000 transportation schemes, and projects valued above USD 50 million have risen 42%.

Rental Penetration Expansion: Rental still only makes up to around 55% to 60% of the North American market compared to around 75% in the UK. However, this is a broad average with penetration levels ranging from low single-digit percentages to high double-digit percentages. We see the potential market penetration for rental equipment to be well over 60% in North America.

H&E Synergy Realization: Expected incremental EBITDA of $300 million, with $175 million from revenue synergies and $125 million from cost synergies. Approximately half of the cost synergies are anticipated by the end of 2025.

Labor Shortage Benefits: Labor shortages—estimated at 439,000 additional workers in 2024—are pushing contractors toward rental subscriptions and push-button technologies that offset skilled-operator gaps.

Specialty Business Growth: Higher-margin ProSolutions offerings drive margin expansion while creating customer stickiness through technical expertise requirements.

The Bear Case

Integration Execution Risk: The H&E acquisition represents a significant integration challenge. The acquisition significantly expands Herc's geographic footprint, though early results show some challenges with H&E legacy branches reporting a 14.1% year-over-year decline.

Leverage Concerns: The company's net debt stood at $8.3 billion as of June 30, with net leverage of 3.8x compared to 2.6x in the same prior-year period.

Interest Rate Sensitivity: Commercial construction remains pressured by elevated interest rates. CEO Lawrence Silber noted, "local markets continue to see pressure as more commercial projects come to completion, while new projects remain on pause due to prolonged higher interest rates."

Federal Spending Uncertainty: Government infrastructure programs face political risk with changing administrations. While committed funding provides multi-year visibility, the pace and scope of future spending remains uncertain.

Cyclicality: Equipment rental is inherently cyclical, tied to construction and industrial activity. Economic recession would pressure both volume and pricing simultaneously.

XIV. Investment Considerations: Key Metrics to Watch

For investors evaluating Herc Holdings, three key performance indicators merit primary attention:

1. Dollar Utilization Rate

Dollar utilization—rental revenue divided by fleet OEC—measures how effectively the company monetizes its asset base. This metric captures both physical utilization (what percentage of equipment is on rent) and pricing power. Improving dollar utilization indicates operational excellence and market strength; declining utilization signals either excess fleet or pricing pressure.

2. Adjusted EBITDA Margin

Adjusted EBITDA for the year increased by 9% to $1,583 million, with an adjusted EBITDA margin of 44.4%. EBITDA margin captures both revenue quality (pricing, mix) and operational efficiency (branch productivity, maintenance costs). Post-H&E integration, margin progression will indicate synergy realization. Management has historically delivered margin improvement through operational excellence, making this metric a proxy for execution quality.

3. Net Leverage Ratio

With $8.3 billion in net debt following the H&E acquisition, deleveraging becomes a critical near-term priority. Herc Holdings targets a leverage reduction to 2-3x by 2027, pausing further M&A activity to concentrate on current operations. The pace of debt reduction—through both EBITDA growth and cash flow application—determines financial flexibility for future growth and vulnerability to economic downturns.

XV. Conclusion: The Road Ahead

Herc Holdings' transformation from neglected Hertz subsidiary to North America's third-largest equipment rental company represents one of the more impressive industrial turnarounds of recent years. Larry Silber and his team took a business that had been starved of investment and strategic attention, implemented disciplined operational improvements, and built the scale necessary to compete effectively.

The H&E acquisition marks a new chapter—one with higher stakes and greater complexity. Success requires executing integration while navigating cyclical headwinds in commercial construction, managing substantial leverage, and maintaining service quality across a dramatically expanded footprint.

The secular tailwinds appear genuine. Infrastructure spending, data center construction, renewable energy development, and the long-term trend toward rental over ownership provide multi-year demand support. Rental penetration in North America has room to expand toward European levels. And consolidation benefits the largest players disproportionately.

But challenges remain. Integration risk is real—the H&E business came with legacy challenges that are taking time to address. The company carries more debt than management would prefer. And the equipment rental industry remains intensely competitive, with United Rentals and Sunbelt continuing to invest aggressively in scale and capabilities.

What makes Herc's story compelling is the clarity of its strategic logic and the consistency of its execution. This isn't a company chasing transformative technology or betting on unproven business models. It's a company doing the hard work of operational excellence in an industry where blocking and tackling matter more than vision statements.

For the neglected sibling that rang the NYSE bell in July 2016, the journey from corporate orphan to industry powerhouse provides a compelling case study in what disciplined management and strategic focus can achieve. The next few years will determine whether that transformation can continue—or whether the ambition of the H&E acquisition exceeded the company's capabilities.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube