CEMEX: From Monterrey to the World — The Making and Near-Breaking of a Global Cement Empire

I. Introduction & Episode Roadmap

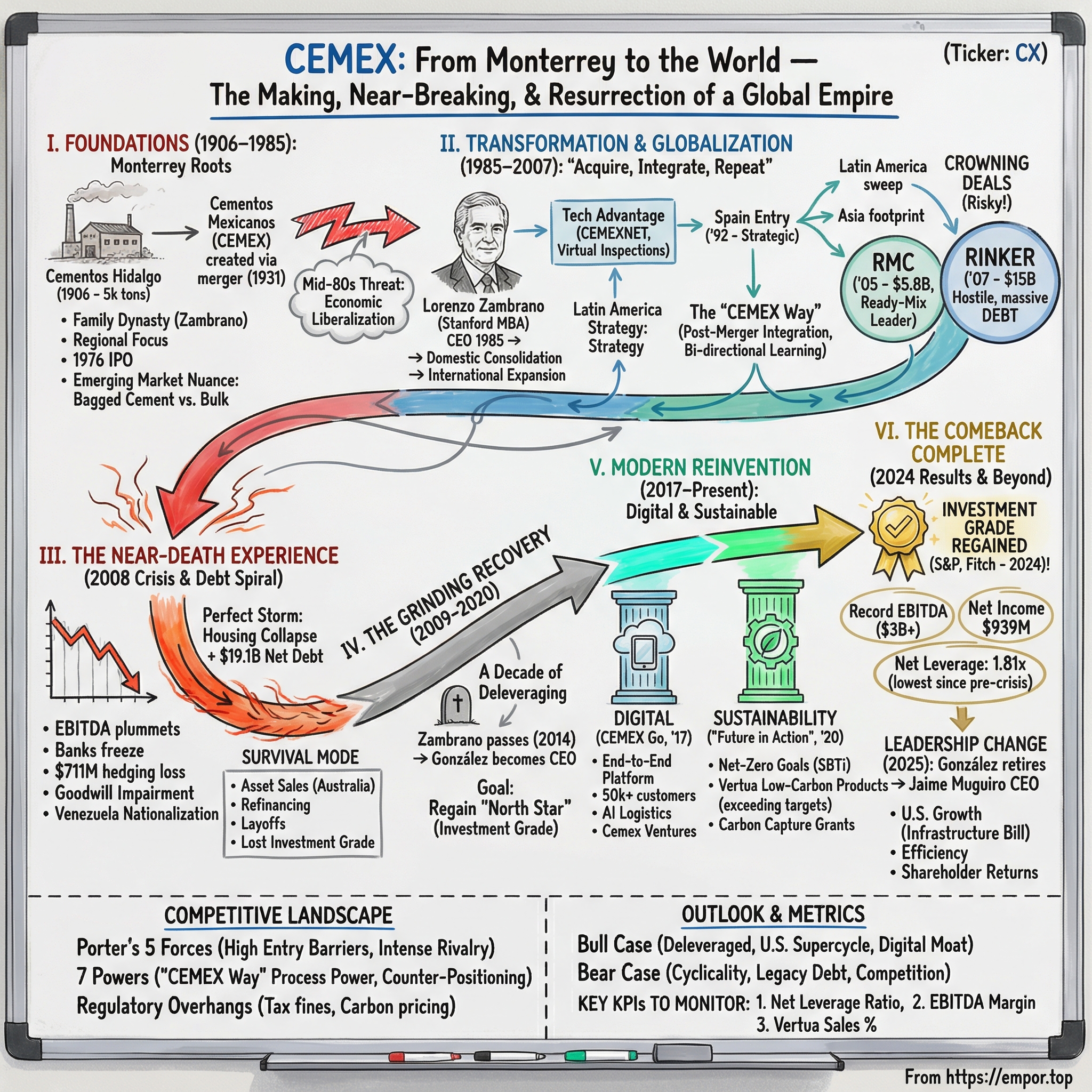

Picture a dusty cement plant on the outskirts of Monterrey, Mexico, in 1906. The machinery is primitive, the capacity laughable by modern standards—just 5,000 metric tons per year. The founders have no way of knowing that this modest operation, Cementos Hidalgo, will one day anchor a $16 billion global enterprise spanning more than 50 countries and rank among the world's five largest cement producers.

Cemex reported its fourth quarter and full-year 2024 results, reaching an annual EBITDA of US$3,079 million and a Net Income of US$939 million, a record in the company's recent history. The company regained an investment-grade rating by Standard & Poor's and Fitch, reached US$939 million in net income, a record level in Cemex's recent history, and announced a progressive shareholder dividend program.

The central narrative of Cemex is one of audacious transformation, near-death experience, and methodical resurrection. How did a regional Mexican cement company become a global titan, nearly collapse under a mountain of debt following an ill-timed acquisition, and then stage a remarkable decade-long comeback that culminated in regaining investment-grade status after fifteen years in the financial wilderness?

The story is built around several interlocking themes: a family dynasty that balanced tradition with ruthless modernization; an aggressive M&A strategy that made "acquire, integrate, repeat" into a corporate mantra; the creation of a proprietary operating system—the "CEMEX Way"—that became a Harvard Business School case study; a near-death experience during the 2008 financial crisis that forced an existential reckoning; and a modern reinvention centered on digital transformation and sustainability leadership.

In February 2025, Cemex announced that its CEO, Fernando A. González, had decided to retire after a successful career of over 35 years in the company. The Cemex Board of Directors appointed Jaime Muguiro as new CEO, with changes becoming effective April 1, 2025. With new leadership taking the helm, the company stands at an inflection point—financially healthy for the first time in nearly two decades, but facing a construction materials industry undergoing fundamental transformation driven by decarbonization imperatives and digital disruption.

II. The Cement Business: Understanding the Foundation

Before diving into Cemex's story, one must understand what makes cement such a peculiar business—and why the industry structure creates both remarkable barriers to entry and unusual competitive dynamics.

Cement appears deceptively simple: combine limestone, clay, and other materials, heat them to 1,500 degrees Celsius to form clinker, grind it up, and you have the binding agent that holds together the world's buildings and infrastructure. But the economics are anything but simple.

The fundamental challenge is that cement has a low value-to-weight ratio. It's heavy, bulky, and relatively cheap per ton. This makes global trade economically punishing—shipping cement across oceans typically doesn't pencil out except in specific circumstances. The result is that cement is inherently a local or regional business, with transport costs creating natural market boundaries.

Yet within those boundaries, well-positioned cement producers enjoy remarkable pricing power. According to the Global Cement and Concrete Association (GCCA), the cement industry is the source of about 5% - 8% of the world's CO₂ emissions. This environmental footprint means new plant construction faces substantial regulatory hurdles, permitting battles, and capital requirements that can stretch into the hundreds of millions of dollars. Once permitted and built, a cement plant becomes a quasi-monopoly within its geographic radius.

The ready-mix concrete business adds another layer of complexity. Unlike bagged cement that can sit in a warehouse, ready-mixed concrete has to be poured within 90 minutes of mixing. This creates what logistics experts call a "last-mile problem on steroids"—coordinating the movement of heavy mixer trucks from batching plants to construction sites, timing arrivals precisely, managing the unpredictability of construction schedules, and ensuring quality during a countdown clock that starts the moment water hits cement.

The global cement market size reached a value of USD 403.70 billion in the year 2024. The market is expected to grow at a CAGR of 5.40% between 2025 and 2034 to reach USD 683.07 billion by 2034.

The industry structure has evolved dramatically over decades. The global cement market is moderately to highly competitive, as there are high capital requirements for entry, numerous environmental regulations, and small room for new entrants due to the top-5 players—China National Building Material Co Ltd, CRH Plc, Anhui Conch Cement Co Ltd, Holcim Ltd, and HeidelbergCement AG—capturing around 39% of the global market.

In 2024, the Swiss company Holcim had the largest number of operational cement plants of any cement producer worldwide, at 180 plants. The China-owned company China National Building Materials (CNBM) had the second-largest number of operational cement plants in that world that year, at 94.

The strategic implication is clear: in a fragmented but regionalizing industry with high barriers to entry, scale matters enormously. Larger players can spread fixed costs across more volume, invest in fuel and raw material optimization, and amortize technology investments more efficiently. This insight would become central to Cemex's strategy.

Why do emerging markets matter disproportionately in cement? Infrastructure demand in developing countries drives volume growth that mature markets simply cannot match. Urbanization trends, housing construction, and infrastructure development in Latin America, Asia, and Africa create demand that compounds for decades. Moreover, the customer mix differs: while developed markets primarily serve sophisticated commercial contractors, emerging markets often feature individual homebuilders purchasing bagged cement—a fundamentally different distribution model with different margin profiles.

III. Founding & Early Years: A Monterrey Story (1906–1985)

The Cemex origin story begins in the industrial crucible of Monterrey, a city that would become Mexico's manufacturing heartland and incubator for some of Latin America's most successful conglomerates. The founding families of Monterrey—names like Zambrano, Garza, and Sada—built empires in steel, glass, and cement, creating an industrial ecosystem that persists to this day.

Lorenzo Hormisdas Zambrano Treviño (27 March 1944 – 12 May 2014) was a Mexican businessman and philanthropist. He took over Cemex, a regional cement company founded by his grandfather, and transformed it into one of the largest cement producers in the world by the time of his death.

The company traces its origins to 1906, when Cementos Hidalgo was founded near Monterrey with a cement plant capacity of just 5,000 metric tons per year. In 1920, Lorenzo Zambrano (grandfather of the future transformational CEO) established Cementos Portland Monterrey and began operating a 20,000-metric-ton cement plant in nearby Monterrey.

The elder Lorenzo Zambrano engineered the 1931 merger of these two companies, creating Cementos Mexicanos—later known as Cemex. This consolidation reflected a pattern that would recur throughout the company's history: growth through acquisition rather than purely organic expansion.

For the first time, Cemex's annual sales exceeded 6.7 million tons of cement and clinker, and the annual sales of three cement plants–Monterrey, Guadalajara and Torréon–each surpassed 1 million tons.

For decades, Cemex remained a small, local company. It adopted a regional profile in 1966–67 when it acquired a plant in Mérida, Yucatán, from Cementos Maya and constructed new plants in Ciudad Valles, San Luis Potosí, and Torreón, Coahuila.

In 1976, the company went public on the Mexican stock exchange, and that same year, became the largest cement producer in Mexico with the purchase of three plants from Cementos Guadalajara.

Mexico's cement market featured a characteristic that distinguished it from developed economies and would later inform Cemex's operating model: more than half of Cemex's cement sales in Mexico came from individual homebuilders who bought bagged cement rather than bulk deliveries to commercial construction sites. This created a fundamentally different business model requiring extensive distribution networks, relationships with hardware stores and building materials retailers, and consumer-oriented marketing—skills that would prove valuable in other emerging markets.

The company continued its domestic expansion through the 1980s. Further acquisitions of Mexican cement companies were made in 1987 and 1989, making Cemex one of the ten largest cement companies in the world.

But by the mid-1980s, storm clouds were gathering. The Mexican government began liberalizing the economy, dismantling the protectionist policies that had sheltered domestic industries from international competition. For Cemex, this meant the end of a cozy market position and the beginning of an existential challenge.

IV. Lorenzo Zambrano Takes the Helm: The Transformation Begins (1985–1992)

On May 30, 1985, Lorenzo Zambrano—grandson of the founder, Stanford MBA, and seventeen-year company veteran—was named CEO of Cemex at age 41. It was a pivotal moment not just for the company but for Mexican business more broadly. Zambrano would become one of the first executives from an emerging market to build a genuinely global multinational company, proving that strategic sophistication and operational excellence were not the exclusive province of developed-world corporations.

Zambrano graduated with a bachelor's degree in Mechanical Engineering from ITESM in 1966. Shortly thereafter, he moved briefly to Palo Alto, California, to complete a master's degree in Business Administration (MBA) at the Stanford Graduate School of Business (1968), where he was the only Mexican student registered at the time.

After completing his studies, he returned to his home city and joined the family business. In 1968 he joined Cemex, and for 17 years he held various executive positions, including plant manager of Torreón and Monterrey, and director of operations.

Zambrano's education and early career shaped his approach to management. Stanford Business School in the late 1960s was pioneering quantitative management techniques and systems thinking—approaches that would later inform Cemex's legendary operational discipline. His seventeen years working through the ranks, from plant manager to director of operations, gave him deep knowledge of the cement business's technical intricacies.

During Zambrano's first year as CEO, Cemex revenues were approximately $276 million.

The existential threat became clear as Mexico's economy opened. "We suddenly found ourselves competing with very large international companies at a time of consolidation in the global cement industry. There were few independent producers left. Either we became large and international, or we would end up being purchased by a bigger player."

Zambrano's response was decisive: consolidate domestically, then expand internationally. The acquisition of Cementos Tolteca, Mexico's second-largest cement producer, gave Cemex 65 percent of the Mexican market and established it as one of the ten largest cement companies globally.

But Zambrano understood that scale alone wouldn't be enough. He needed to transform Cemex into a technologically sophisticated operation capable of competing with global giants. 1987 saw the acquisition of Cementos Anahuac and the start of implementation of a satellite communication system, CEMEXNET, to connect the company's facilities.

This investment in technology was revolutionary for its time and location. CEMEXNET allowed all of Cemex's cement factories in Mexico to communicate in a coordinated and fluid way, avoiding Mexico's erratic, insufficient, and expensive phone service. Along with the communication system, an Executive Information System was implemented in 1990 requiring all managers to input manufacturing data—including production, sales, administration, inventory, and delivery—that could be viewed by other managers.

The system enabled CEO Zambrano to conduct "virtual inspections" of Cemex's operations, including the operating performance of individual factories, from his laptop computer. In an era when most cement companies operated as loose federations of autonomous plants, Cemex was building an integrated, data-driven management system that would later become the foundation for its famous post-acquisition integration capability.

"Information is your ally: you use it to detect problems more quickly and get better faster," Zambrano stated.

V. The Global Expansion Era: Acquire, Integrate, Repeat (1992–2007)

The transformation of Cemex from Mexican champion to global titan occurred in a fifteen-year burst of acquisition activity that remains one of the most aggressive international expansion programs in business history. Between 1992 and 2007, Cemex completed approximately 20 major acquisitions spanning four continents, fundamentally reshaping the global cement industry in the process.

The Spain Entry – A Strategic Masterstroke

Cemex acquired Spain's two largest cement plants in 1992. The purchase of Valenciana de Cementos (Valcem) and Cementos SANSON marked Cemex's push into the international landscape and immediately established its presence in Europe.

The choice of Spain was strategically deliberate. First, Spain was culturally proximate, with strong historical connections to Mexico and a shared language. Second, Spain was less economically developed than other European countries and offered more opportunities for operational improvement—meaning Cemex could apply its emerging best practices to create value. Third, Spain's cement market was more similar to Mexico's than that of many other European countries. Fourth, as Spain had become an important market for major European companies, Cemex could use Spain to "counter" these companies' investments in Mexico.

The market perception was that Cemex not only overpaid for the two Spanish companies, but would also "suffer from indigestion." Cemex set up a post-acquisition integration team, consisting of 23 experienced functional managers. The team analyzed managerial skills of local managers, information technology, business processes and the structure of functional areas in the acquired companies and looked for ways to merge "the CEMEX way" with the current operations. During the 18-month integration process, Zambrano traveled to Spain every month to meet face-to-face with the team.

The team found that the two Spanish companies were very inefficient, especially in the areas of inventory management, energy consumption and plant automation. Moreover, the acquired companies did not use ICT effectively.

The Spain experience birthed what would become Cemex's most valuable competitive asset: a systematized post-merger integration methodology. The company learned that the key to acquisition success wasn't just finding the right targets at the right price—it was having a repeatable process for transforming acquired companies into high-performance operations.

The Latin America & Global Sweep

Cemex acquired Venezuela's largest cement company in 1994, which was ideally positioned for exports. Plants were purchased the same year in the United States and in Panama. In 1995 Cemex acquired a cement company in the Dominican Republic.

Cemex became the third largest cement company in the world with the acquisition of Cementos Diamante and Samper in Colombia in 1996.

Between 1998–1999, Cemex acquired a 25% interest in Indonesia's largest cement producer. It also purchased APO Cement in the Philippines and an additional 40% economic interest in Rizal Cement. Cemex listed on the New York Stock Exchange under the ticker symbol "CX" in 1999.

On 15 September 1999, Zambrano led a ceremony at the NYSE to begin the listing of the Cemex stock (CX).

The "CEMEX Way" – A Case Study in Post-Merger Integration

The "Cemex Way" became synonymous with ruthless efficiency and rapid integration. Following acquisitions, a "post-merger integration team" would be quickly dispatched to analyze the acquired company, identify ways to cut costs and reduce head count, and harmonize technical systems and management methods with those of Cemex—in fine detail.

The Cemex Way: characterized by acquisitions (e.g., the 1992 Spanish acquisition and the 2005 RMC acquisition), global standardization of best practices, and data-driven innovation.

What distinguished the Cemex approach was its emphasis on bi-directional learning. The CEMEX Way was always retrofitted to include the best practices of companies Cemex acquired. Teams would identify people in acquired field operations who had exceptionally smart approaches to doing things, and incorporate those practices back into the CEMEX Way. This was the beginning of recognition on Cemex's part of the importance of global collaboration and knowledge sharing.

Technology as Competitive Advantage

Cemex continued to invest heavily in technology in the late 1990s and early 2000s, staying on the cutting edge of information technology. Because ready-mixed concrete has to be poured within 90 minutes of mixing, it is a major challenge to coordinate and properly time the movements of ready-mixed concrete trucks from the plants to construction sites. Cemex equipped every truck with a computer and a global positioning system receiver.

Building on its long track record in lean operations—"ruthless operating efficiency" became a catchphrase within the company—and its pride in being one of the most successful companies from an emerging economy, Cemex developed a high level of customer responsiveness. It delivered cement within 20 minutes of receiving an order in many locales.

In 2004, Cemex received the Wharton Infosys Business Transformation Award for their creative and efficient use of information technology.

The Crowning Deals – RMC and Rinker

The mid-2000s brought Cemex's most transformative—and ultimately most dangerous—acquisitions.

On March 1, 2005, Cemex completed its $5.8 billion acquisition of the London-based RMC Group, which made Cemex the worldwide leader in ready-mix concrete production and increased its exposure to European markets.

The addition of RMC improved the balance of Cemex's portfolio by diversifying cash flows, better positioning Cemex for profitable growth throughout business and economic cycles. RMC's leading position in Europe extended Cemex's reach into new markets that complement Cemex's solid position in the Americas, increasing trading opportunities and expanding Cemex's ability to service more customers.

Cemex doubled its size with the acquisition of RMC, adding 20 mainly European markets. This integration strengthened Cemex's presence in Europe and positioned the company all the way through the industry value chain.

RMC was a company more than half Cemex's size, with a highly decentralized culture and operating style, spread across Europe, the United States, the Middle East, Asia-Pacific and Latin America. Cemex knew that the post-merger integration (PMI) would be very challenging and that it would have to adapt its new governance structure and business operating model to this new reality.

Then came Rinker.

Cemex of Mexico closed its acquisition of The Rinker Group of Australia in April 2007 after raising its offer to USD15.85 per share. This represented a 54% premium over Rinker's closing price prior to the initiation of the hostile offer.

The Rinker acquisition was transformative in scale—at approximately $15 billion, it was Cemex's largest deal ever and made the company one of the world's largest suppliers of building materials. But the timing and structure would prove catastrophic.

Cemex, in-line with its customary acquisition process, financed the entire purchase with debt.

During the 1990s, Cemex had reached a compounded annual growth rate of 26 percent in operating cash flow, almost double the industry average. Most of its international acquisitions were successful, proving wrong the many commentators who doubted its ability to integrate the acquired firms. But Rinker would test that track record as never before.

VI. The Near-Death Experience: 2008 Financial Crisis & Debt Spiral

The Rinker acquisition closed in July 2007, just months before the U.S. housing market began its historic collapse. What followed was a corporate near-death experience that would reshape Cemex for the next fifteen years.

The Perfect Storm

With Cemex's acquisition of Rinker in 2007, things changed dramatically. Cemex closed 2007 with an EBITDA of US$4.591 billion, better than 2006, but nothing close to what had been forecast when the company had initiated its hostile takeover of Rinker. With US$14 billion of new debt, the company closed 2007 with net debt of US$19.1 billion, above what the banks considered appropriate.

At the time that Cemex had initiated its hostile takeover of Rinker, in October 2006, its EBITDA was forecast to hit US$5 billion for 2007. In the end, actual 2007 results were only US$4 billion. But it was actual EBITDA for 2008 that would pose the biggest problem. Although forecast to hit US$4.6 billion, actual 2008 results were only US$3 billion. This was essentially the same as that for 2005, a full three years before the acquisition of Rinker.

The financial crisis of 2008 sent the housing and construction sectors downward at an ever-increasing rate. Cemex's earnings plummeted, hindering its ability to pay down debt as planned.

The Crisis Hits

What is now commonly called the Global Financial Crisis exploded in the United States in September 2008. On September 6, 2008, the two government-sponsored mortgage associations, Fannie Mae and Freddie Mac, were put into government conservatorship. On September 15, Lehman Brothers filed for Chapter 11 bankruptcy. The next day, September 16, the U.S. government seized control of American International Group (AIG).

As sales and earnings declined at Cemex, banks began freezing up, unwilling to extend, roll over, or refinance debt. The company experienced what executives would later describe as "banks not answering the phone"—regardless of the caller's creditworthiness.

Cemex reported a loss of $711 million for the month of October 2008.

The financial crisis significantly and negatively affected the valuation of Cemex's derivative instruments portfolio. In one particularly volatile period from October 1 to October 16, 2008, changes in the fair value of derivative instruments portfolio represented mark-to-market losses of approximately $976 million. In early December, the company announced that it was unwinding its failed currency hedging program at a cost of $711 million.

For the year ended December 31, 2008, Cemex recognized goodwill impairment losses for approximately Ps18.3 billion (U.S.$1.3 billion), of which the impairment corresponding to the United States reporting unit was approximately Ps16.8 billion (U.S.$1.2 billion). The estimated impairment loss in the United States is mainly attributable to the acquisition of Rinker.

This combination of factors resulted in the worst decline in sales volumes that Cemex had experienced in the United States in recent history. U.S. operations cement and ready-mix concrete sales volumes decreased approximately 14% and 13%, respectively, in 2008 compared to 2007.

Additional Blow – Venezuela Nationalization

In April 2008, the President of Venezuela, Hugo Chávez, announced the nationalization of "the whole cement industry" in that country. In mid-2008 the Venezuelan government took over the Venezuelan operations of Cemex, the largest Venezuelan producer with around a 50% market share.

The Survival Mode

Heavily leveraged from its acquisition spree, Cemex faced immense pressure, forcing a period of intense financial restructuring, divestments, and operational discipline to ensure survival.

In June 2009, Cemex sold its Australian operations to Holcim for A$2.2 billion (US$1.75 billion) helping refinance its US$14 billion debt, which partly was due to the acquisition, two years earlier, of the Rinker Group.

The company lost its investment-grade rating during the global financial crisis and was forced to sell assets, refinance approximately $15 billion in debt, and lay off 10% of its workforce.

The stock steadily retreated to around $5 per share by early 2009. The ill-fated takeover of Rinker had put the future of Cemex in jeopardy.

VII. The Long Decade of Deleveraging (2009–2020)

The period from 2009 to 2020 represented a grinding recovery—a decade of asset sales, debt refinancing, and operational discipline that would test the company's resilience and ultimately set the stage for its modern reinvention.

CEO Transition

The transition came unexpectedly in May 2014.

On 12 May 2014, during a business trip to Madrid, Spain, Zambrano had scheduled a corporate meeting at 7 pm local time. After failing to show up, he was tracked down by members of his staff and found dead inside his third-floor suite at Hotel Villa Magna. His sudden death at the relatively young age of 70 took news outlets and business associates by surprise.

Cemex's chief executive officer, Lorenzo Zambrano, who led the Mexican cement major for almost three decades, died aged 70. A statement by the company said that Mr Zambrano passed away in the Spanish city of Madrid on 12 May 2014 of natural causes.

Zambrano acted as the CEO of Cemex until he passed away, leaving Fernando González, the former chief of planning and finance, to fill his position as CEO in 2014.

Fernando A. González was appointed chief executive officer (CEO) of Cemex in 2014. Mr. González joined Cemex in 1989, when the company was starting its international expansion.

He held several senior management positions in South America and the Caribbean region, was president of the Cemex Europe, Middle East, Africa, Asia, and Australia region, and Executive Vice President of Strategic Planning, Finance, and Administration (CFO).

The newly appointed chief executive made his priorities immediately clear. The number one goal was recovering the investment-grade rating—"Nothing we do can be out of line with that goal," González declared.

The Grinding Recovery

The recovery was methodical and painful. Cemex rebounded from a near bankruptcy during the 2008 economic crisis to regain its position as a leading company in the global construction materials industry.

In February 2018, the company reported record earnings of $750 million for all of 2016, the highest in a decade.

The company continued asset sales and portfolio optimization throughout the decade, divesting non-core operations while maintaining its positions in strategic markets—particularly Mexico, the United States, and select European markets.

VIII. The Modern Era: Digital & Sustainable Cemex (2017–Present)

The transformation from a debt-burdened conglomerate fighting for survival to an industry leader in digital innovation and sustainability represents one of the most significant corporate reinventions in recent memory.

Digital Transformation – CEMEX Go

Since its launch in November 2017, Cemex Go positioned itself as the leading end-to-end multichannel platform for the building materials industry. Today, more than 50,000 customers use the platform, representing 93% of cement and 85% of ready-mix concrete customers.

Cemex Go is the first-of-its-kind, fully digital customer integration platform. With a strong customer-centric approach, it allows its users to increase their productivity, make better business decisions, and have more control over their businesses. This is Cemex's bold step to advance the building materials industry to the interconnected business age.

"Cemex Go moves us closer to our customers by being faster, more transparent, and more efficient, which will enable greater productivity and open up new growth opportunities for our customers and for us. Cemex Go places the power to succeed in today's fast-paced and dynamic market in the hands of our customers," stated González.

In the past 4 years, the company's net promoter score, the most widely used customer loyalty and satisfaction measurement, increased by an impressive 50%, reaching a level of 66.

Among the new Artificial Intelligence capabilities of Cemex Go that are in the process of being implemented or scaled are: Dynamic fleet optimization to improve delivery times and dynamically schedule orders based on traffic, distance to batching plants, and customer location. Predictive demand sensing to improve logistics and customer service in its ready-mix concrete business. The company's industry-leading use of data allows it to foresee demand in advance and optimize production processes to meet the market's needs.

Cemex Ventures is the company's corporate venture capital and open innovation unit. Since its launch in 2017, it has been connecting with startups, entrepreneurs, and universities and other stakeholders to tackle the toughest challenges facing the field and shape the construction ecosystem of tomorrow.

Sustainability – Future in Action

Cemex, the largest concrete producer in the western world, and a global leader in cement production, launched its Future in Action program in March of 2020 to build a more sustainable, circular future, with the primary objective of becoming a net-zero CO2 company.

Future in Action focuses on achieving sustainable excellence through climate action, circularity, and natural resource management with the primary objective of becoming a net-zero CO2 company.

To ensure they are on the right track, Cemex has set the most ambitious 2030 targets available to the industry: Scope 1 Goals of 47% less CO2 per ton of cementitious material and 35% less carbon content in concrete; Scope 2 Goals of 65% clean electricity consumption.

Since 2020, Cemex has reduced cement Scope 1- and 2-specific CO2 emissions by 15% and 18% respectively — a pace that would have previously taken 16 years to achieve.

Vertua products accounted for 63% of total cement sales and 55% of total concrete sales, exceeding their 2025 sales goal of 50%. Cemex was awarded a €157 million EU Innovation Fund grant for CO2 capture at Cemex's Rüdersdorf plant in Germany, which is expected to become their first net-zero plant.

Cemex was ranked #1 by the World Benchmarking Alliance among 91 companies in hard-to-abate industries, including steel and aluminum, achieving the highest climate transition score.

Low-Carbon Products: Vertua

Vertua cement and concrete play an important role in the transition of the built environment to a net-zero world, meeting customer needs through low-carbon products without compromising performance. The development and customer acceptance of Vertua low-carbon products serves as an important milestone in Cemex's journey to become a net-zero CO2 company by 2050.

Vertua products have a CO2 reduction of at least 25% versus traditional cements. In concrete, the CO2 reduction ranges from 30% up to a full net-zero option.

With the current levels of Vertua sales, Cemex achieved its 2025 goal of Vertua lower-carbon cement sales reaching 50% of total cement sales two years ahead of schedule.

The Comeback Complete – 2024 Results

Rating agency Standard & Poor's announced in March 2024 that it had upgraded Cemex's long-term global scale issuer credit rating to Investment Grade (BBB-) due to its strong financial and operating performance, deleveraging strategy, and flexible capital allocation.

In April 2024, Cemex announced that it had reached full investment grade status after being upgraded to BBB- by rating agency Fitch Ratings. This followed S&P Global Ratings' upgrade announced in March 2024.

Cemex SAB had finally achieved what it for years called its "north star": Investment-grade status.

Net Leverage stood at 1.81 times, its lowest level since the outbreak of the 2007 global financial crisis.

"With the recovery of our investment grade ratings, improved free cash flow generation and the execution of US$2.2 billion in asset divestments, we can now pursue more aggressively our capital allocation priorities of growth through small to medium-sized acquisitions, primarily in the U.S., additional deleveraging, and building further on our shareholder return programs," said González.

Leadership Transition

In February 2025, Cemex announced that its CEO, Fernando A. González, had decided to retire after a successful career of over 35 years in the company. The Cemex Board of Directors appointed Jaime Muguiro as new CEO; these changes became effective April 1, 2025.

During his tenure as CEO, González focused on reducing Cemex's debt, expanding its presence in the U.S., Europe and Mexico, and reducing its carbon footprint.

Jaime Muguiro joined Cemex in 1996 and has held several executive positions in the Strategic Planning, Business Development, Ready-Mix Concrete, Aggregates, and Human Resources areas. He has headed several regional operations for Cemex, including the Mediterranean, South, Central America and the Caribbean, and most recently serves as President of Cemex in the United States.

"As Cemex's new CEO, I am committed to providing the highest possible returns to our shareholders, which we will achieve by being the best partner to our customers and having a laser-like focus on operational efficiency," declared Muguiro.

Under Muguiro's leadership, Cemex intends to use its previously announced "Project Cutting Edge" cost savings initiative as the foundation to drive a streamlined organizational transformation. Cemex is targeting recurrent yearly EBITDA savings of at least $150 million in 2025 and US$350 million by 2027.

IX. Competitive Landscape & Industry Analysis

Understanding Cemex's position requires examining the broader competitive dynamics of the global cement industry through both Porter's Five Forces and Hamilton Helmer's 7 Powers frameworks.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The cement industry has formidable barriers to entry. Capital requirements for a new cement plant can exceed $500 million. Environmental permitting processes stretch for years. Established players have locked up prime limestone quarry locations. The result is minimal genuine new entry outside of China and India.

Supplier Power: MODERATE Key inputs include limestone (typically controlled through owned quarries), energy (coal, pet coke, natural gas), and equipment. Energy costs represent a significant expense, and while large cement producers can negotiate favorable contracts, they remain exposed to commodity price volatility. Alternative fuels and waste co-processing have emerged as mitigating strategies.

Buyer Power: VARIES BY SEGMENT In bulk cement and ready-mix concrete sales to large contractors, buyer power is moderate to high—sophisticated commercial buyers understand market pricing and can switch suppliers. In the bagged cement retail segment (important in Mexico and emerging markets), buyer power is lower due to fragmented customers and brand preferences.

Threat of Substitutes: LOW TO MODERATE Concrete remains the world's most used man-made material with no functional substitute for most applications. However, wood construction is gaining share in certain residential segments, and steel framing competes in some commercial applications. The sustainability transition could either strengthen concrete's position (it sequesters carbon over time) or weaken it (high production emissions).

Competitive Rivalry: HIGH Within geographic markets, competition is intense. The industry has experienced significant consolidation, but regional markets typically feature 3-5 major players competing aggressively on price, service, and relationships. Overcapacity in some markets exacerbates price competition.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Cemex benefits from scale advantages in several areas—purchasing power for equipment and energy, technology development amortization, and corporate overhead spreading. However, the local nature of cement markets limits global scale benefits.

Network Effects: Limited in traditional cement operations, but Cemex Go creates modest network effects as more customers adopt the platform, improving data quality and service optimization.

Counter-Positioning: Cemex's early investment in digital transformation and sustainability positioned it ahead of slower-moving competitors. The "CEMEX Way" integration methodology created capabilities that competitors found difficult to replicate.

Switching Costs: Moderate in ready-mix concrete due to quality certifications, mix designs, and service relationships. Lower in bagged cement. Cemex Go increases switching costs through platform integration.

Branding: Important in retail cement markets where Cemex has built consumer brand recognition. Less relevant in commercial bulk markets where purchasing is primarily specification-driven.

Cornered Resource: Quarry positions represent cornered resources in specific geographic markets. Technical talent and proprietary integration methodologies are harder to quantify but represent valuable human capital.

Process Power: The CEMEX Way represents genuine process power—institutionalized operational excellence that has been refined over decades and is embedded in the organization's culture, systems, and training programs.

Material Regulatory and Legal Overhangs

Cemex's subsidiary, Cemex España, paid approximately EUR456m in fines as a result of a tax audit in Spain that commenced in July 2011 and covered the years 2006-09. In terms of the financial impact, the parent company expensed and accrued a liability of ~US$500m in 4Q23 and paid the fines in 1H24.

Free Cash Flow after Maintenance Capital Expenditures increased to US$1,253 million in 2024, adjusting for the US$383 million payment related to the tax fine in Spain.

The cement industry also faces ongoing regulatory pressure related to carbon emissions, with the EU's Carbon Border Adjustment Mechanism (CBAM) potentially reshaping competitive dynamics in European markets.

X. Bull Case & Bear Case

Bull Case

The bull thesis for Cemex centers on several converging factors:

Deleveraging Complete, Growth Optionality Open: With investment-grade ratings restored and net leverage at 1.81x—the lowest since before the financial crisis—Cemex has financial flexibility to pursue growth through bolt-on acquisitions, particularly in the U.S. market where it sees the best risk-adjusted opportunities.

U.S. Infrastructure Supercycle: The Infrastructure Investment and Jobs Act has allocated unprecedented funding for roads, bridges, and public works. Cemex's strong U.S. presence, particularly in Texas and Florida, positions it to benefit from multi-year infrastructure spending.

Sustainability Leadership as Competitive Advantage: As procurement departments increasingly require low-carbon materials, Cemex's head start with Vertua products and validated science-based targets creates differentiation. The company has achieved its 2025 Vertua sales targets two years early.

Digital Platform Moat: Cemex Go represents a customer engagement platform that competitors have not replicated, creating switching costs and operational efficiencies.

Valuation Opportunity: After years in the penalty box, the stock trades at a discount to peers despite improved fundamentals.

Bear Case

The bear thesis highlights persistent concerns:

Industry Structural Challenges: Cement is a mature, capital-intensive, cyclical business with limited organic growth in developed markets. The "hard to abate" emissions profile creates long-term transition risk.

Geographic Concentration Risk: Approximately 30% of EBITDA comes from Mexico, exposing the company to peso volatility, political risk, and economic cycles in a single country.

Legacy Debt Structure: While leverage has improved dramatically, the company still carries significant debt from its acquisition era. Any severe economic downturn could stress the balance sheet again.

Competitive Intensity: The industry remains highly competitive with well-capitalized global players (Holcim, Heidelberg Materials, CRH) pursuing similar strategies in similar markets.

New CEO Execution Risk: The leadership transition to Jaime Muguiro, while orderly, introduces uncertainty about strategic direction and execution capability.

Myth vs. Reality Box

Myth: "Cemex never recovered from the 2008 crisis" Reality: While recovery took 15 years, the company has fundamentally transformed its balance sheet, achieving 1.81x net leverage and investment-grade ratings from both S&P and Fitch in 2024.

Myth: "Cement companies can't be technology leaders" Reality: Cemex Go serves 93% of cement customers and 85% of ready-mix customers digitally, with AI capabilities for fleet optimization and demand sensing. The company won the Wharton Infosys Business Transformation Award as early as 2004.

Myth: "Sustainability is just marketing for cement companies" Reality: Cemex has SBTi-validated targets aligned with the 1.5°C pathway, reduced Scope 1 and 2 emissions by 15% and 18% respectively since 2020, and has exceeded its 2025 Vertua sales targets. The €157 million EU Innovation Fund grant for carbon capture at its German plant represents tangible capital flowing to decarbonization.

XI. Key Metrics to Monitor

For long-term investors tracking Cemex, three KPIs stand out as essential indicators of business health and strategic progress:

1. Net Leverage Ratio (Net Debt/EBITDA)

This remains the single most important metric for monitoring Cemex's financial health. The company's near-death experience in 2008-2009 was fundamentally a leverage crisis, and the subsequent 15-year recovery was measured primarily through this ratio. At 1.81x as of year-end 2024, the company has reached its healthiest leverage position since before the Rinker acquisition. Management has indicated willingness to modestly increase leverage for attractive acquisition opportunities, making this metric crucial for assessing capital allocation discipline.

2. EBITDA Margin

The cement business is fundamentally about operational efficiency. EBITDA margin remained flat in 2024 at 19.0%. Margin trends reflect the company's ability to manage input costs (energy, raw materials, labor), pricing power in its markets, and operational leverage. The "CEMEX Way" has historically driven margin improvement in acquired operations; sustained margins indicate the methodology continues to deliver results.

3. Vertua Sales as Percentage of Total Sales

This metric tracks Cemex's progress on its sustainability transformation and its ability to capture the growing market for low-carbon construction materials. Vertua products accounted for 63% of total cement sales and 55% of total concrete sales, exceeding their 2025 sales goal of 50%. Growth in this metric indicates customer acceptance of premium-priced sustainable products and positions the company for tightening carbon regulations.

XII. Conclusion: The Unfinished Story

The Cemex story is a masterclass in both the possibilities and perils of aggressive corporate strategy. From a regional cement maker in northern Mexico, the company built one of the world's great industrial enterprises through visionary leadership, operational excellence, and audacious acquisition. The "CEMEX Way" became a Harvard Business School case study, and Lorenzo Zambrano earned recognition as one of the first executives from an emerging market to build a truly global multinational.

Yet the Rinker acquisition—$15 billion spent at the peak of the housing bubble, financed entirely with debt—represents a cautionary tale about the dangers of overreach. The 2008 financial crisis nearly destroyed the company, eliminating shareholder value accumulated over decades and forcing a fifteen-year recovery that consumed management attention and capital.

The modern Cemex that emerges from this experience is fundamentally different. "This is a pivotal moment in our company's history. Having achieved our deleveraging objectives and substantially consolidated our operations, we are now well-positioned to transition from financial stabilization to growth, looking primarily at opportunities in the United States, while enhancing shareholder returns and driving sustainable value creation for all stakeholders including our neighboring communities," declared Muguiro.

The company now combines its traditional strengths—operational excellence, integration capability, and emerging market expertise—with new competencies in digital transformation and sustainability. Whether this combination creates lasting competitive advantage in an industry undergoing fundamental transformation remains the central investment question.

Cemex is an industry-leading global construction materials and solutions company that drives innovation to help the world reach the next frontier of sustainable living. With its 100-plus year heritage, the company is committed to achieving carbon neutrality through relentless innovation and industry-leading research and development.

As Jaime Muguiro takes the CEO role, he inherits a company that has paid for past sins and now has genuine strategic flexibility. The decisions made in the coming years—how aggressively to pursue U.S. acquisitions, how to balance growth with shareholder returns, how to navigate the decarbonization transition—will determine whether Cemex's next century matches the transformative ambition of its first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube