Philip Morris International: From Spin-Off to Smoke-Free Transformation

I. Introduction & Episode Roadmap

Picture this: It's November 2014 in Nagoya, Japan. A sleek, pen-like device sits on a conference table at Philip Morris International's regional office. No smoke, no ash, just a faint tobacco vapor. The executives around the table are watching something unprecedented—a tobacco company's first real attempt to make cigarettes obsolete. This device, IQOS, would either herald the greatest transformation in tobacco history or become a multi-billion dollar folly.

Today, Philip Morris International commands a $285 billion market capitalization, generates $38 billion in annual revenue, and operates across 180 markets worldwide. Yet this isn't a story about maintaining dominance—it's about a company systematically dismantling its own century-old business model. The question isn't whether PMI can sell cigarettes; it's whether it can stop selling them fast enough.

The paradox is striking: How does a company that perfected the art of selling addiction pivot to selling its own obsolescence? How does management convince Wall Street that destroying 60% of revenue is actually value creation? And perhaps most intriguingly—why would a tobacco company spend $12 billion on R&D to eliminate smoking when cigarettes still generate $8 billion in annual operating income?

This journey spans three distinct acts: the strategic separation from Altria that unlocked international expansion (2008), the aggressive empire-building phase that created a global cash machine (2008-2014), and the radical pivot toward a "smoke-free future" that's rewriting the rules of corporate transformation (2014-present). Along the way, we'll decode how PMI turned regulatory headwinds into tailwinds, why Japan became the unlikely proving ground for tobacco's future, and what the $16 billion Swedish Match acquisition reveals about the next phase of nicotine delivery.

We're about to explore one of the most controversial yet financially successful transformations in modern business—where ethics, addiction, technology, and capitalism collide in ways that challenge every assumption about corporate reinvention.

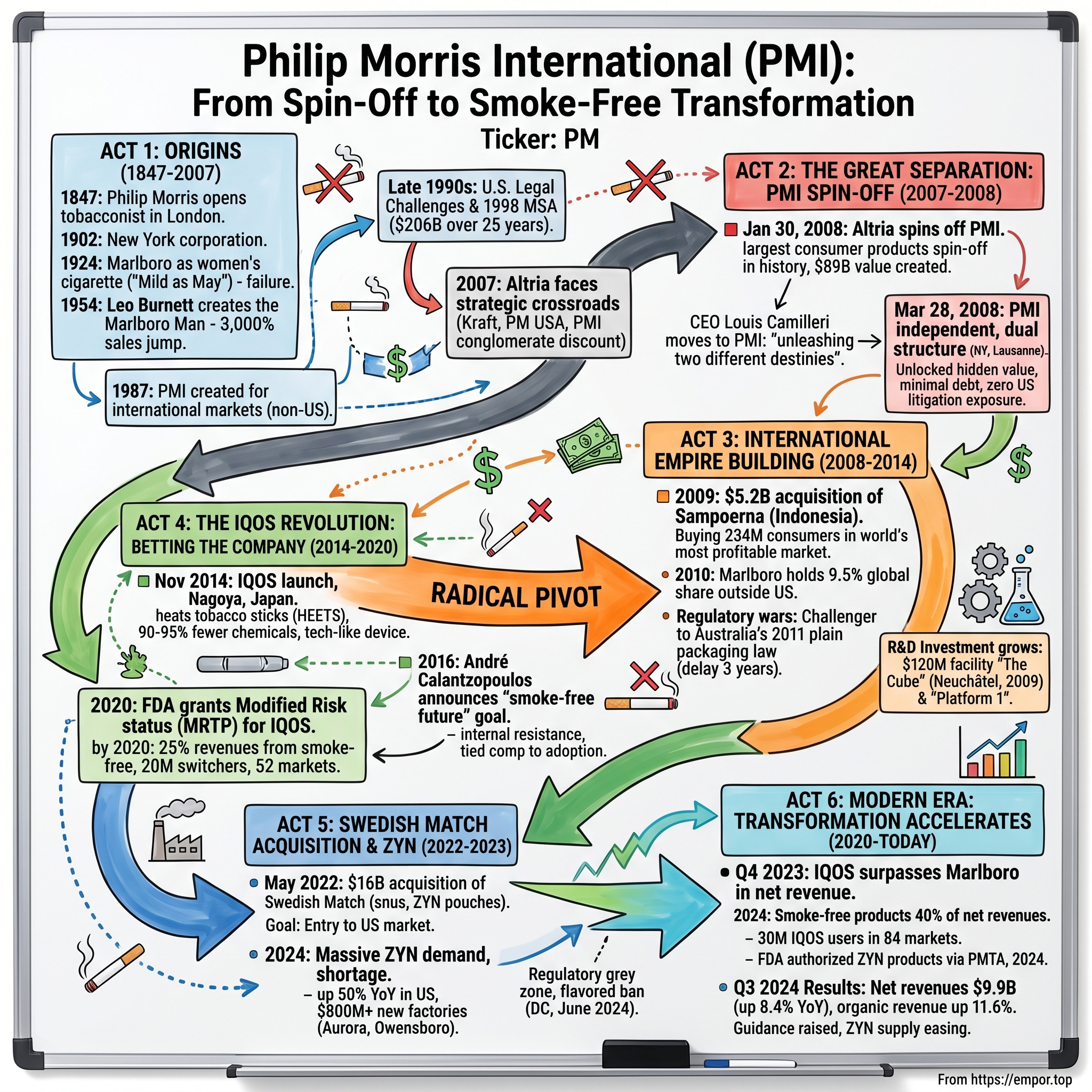

II. Origins & The Pre-Spin Era (1847-2007)

The year is 1847, and on London's Bond Street, a tobacconist named Philip Morris opens his doors for the first time. He's selling hand-rolled Turkish cigarettes to Victorian gentlemen—a luxury product for an exclusive clientele. Morris couldn't have imagined that his name would one day represent the antithesis of exclusivity: mass-market cigarettes consumed by over a billion people worldwide.

The real story begins in 1902 when the business, now Philip Morris & Co., establishes a New York corporation. But it's what happens in 1924 that changes everything. The company introduces Marlboro as a women's cigarette—yes, you read that correctly. Marketed as "Mild as May" with a red filter tip to hide lipstick stains, Marlboro was the cigarette for the sophisticated lady. The tagline? "Ivory tips protect the lips." It was a spectacular failure, capturing less than 1% market share.

Fast forward to 1954. Philip Morris hires Leo Burnett, the advertising genius who would create the Jolly Green Giant and Tony the Tiger. Burnett looks at this failing women's cigarette and sees something else entirely. Within months, Marlboro is reborn with a new filter, new packaging, and most importantly, a new image: the Marlboro Man. The transformation is immediate and stunning—sales jump 3,000% in one year. By 1972, Marlboro becomes the world's best-selling cigarette, a position it maintains to this day.

But here's where strategy meets structure. In 1987, Philip Morris Companies Inc. reorganizes, creating Philip Morris International as a distinct operating company to manage all business outside the United States. This isn't just administrative shuffling—it's recognition that international markets require different approaches, different regulatory strategies, and ultimately, different growth trajectories. While the U.S. market faces increasing litigation and declining smoking rates, international markets—particularly in Asia and Eastern Europe—are expanding rapidly.

The late 1990s bring a cascade of legal challenges. The 1998 Master Settlement Agreement costs the U.S. tobacco industry $206 billion over 25 years. Class action lawsuits multiply. Public sentiment turns hostile. Philip Morris Companies, once proud to bear the founder's name, makes a telling decision in 2003: rebrand as Altria Group. The name, derived from Latin "altus" meaning high, is meant to signal transformation. Critics call it hiding.

By 2007, Altria faces a strategic crossroads. The company owns Kraft Foods (acquired through hostile takeover in 1988), Philip Morris USA, and Philip Morris International. But conglomerate discounts are real, and the sum is worth less than its parts. Kraft, a food company, suffers from association with tobacco. Philip Morris USA faces endless litigation with no international diversification. And Philip Morris International, generating massive cash flows from emerging markets, is shackled to U.S. legal liability.

The solution becomes clear: separation. In March 2007, Altria spins off Kraft Foods. The market responds positively—Kraft shares rise 40% within months. But the bigger move is coming. Internal studies show that Philip Morris International, freed from U.S. litigation risk and regulatory constraints, could be worth $100 billion as a standalone entity. The board begins planning what will become one of the most successful spin-offs in corporate history.

What's remarkable about this pre-spin era is how deliberately Philip Morris built two distinct businesses under one roof. PMI developed separate supply chains, separate management teams, and increasingly, separate cultures. While Philip Morris USA battled lawsuits in American courtrooms, PMI was acquiring companies in Colombia, Indonesia, and Serbia. While U.S. operations focused on defense and compliance, international operations focused on growth and expansion. The spin-off, when it came, wouldn't be a division—it would be a liberation.

III. The Great Separation: PMI Spin-Off (2007-2008)

January 30, 2008, Altria's boardroom in Richmond, Virginia. The vote is unanimous: Philip Morris International will be spun off as an independent company. CEO Louis Camilleri, who's been running Altria since 2002, addresses the board with unusual candor: "We're not just dividing a company. We're unleashing two different destinies." Within hours, the announcement rockets through financial markets—Altria shares jump 8% in after-hours trading.

The mechanics are elegantly simple: On March 28, 2008, every Altria shareholder receives one share of PMI for each share of Altria owned. No cash changes hands, no investment banks take fees for underwriting, no roadshows or IPO pricing drama. Just a clean break—$89 billion in market value created overnight, making it the largest spin-off in consumer products history.

But simplicity in structure masks complexity in execution. PMI must establish entirely new corporate infrastructure in weeks, not years. The company chooses New York City for its official headquarters—close enough to financial markets, far enough from Richmond's tobacco legacy. The operational headquarters lands in Lausanne, Switzerland, offering favorable tax treatment and proximity to emerging markets. This dual structure isn't accidental; it's architected for maximum strategic flexibility.

Louis Camilleri makes a surprising choice: instead of staying with Altria, he follows PMI as CEO. This sends a powerful signal to markets about where the real opportunity lies. Camilleri, who spent years managing Altria's legal battles, suddenly sounds liberated in his first earnings call as PMI chief: "We're no longer playing defense. Every dollar of cash flow can be invested in growth, not settlements."

The market dynamics are fascinating. On day one of trading, PMI opens at $54 per share, valuing the company at $107 billion—already exceeding the most optimistic internal projections. Within six months, while global markets crash during the financial crisis, PMI shares outperform the S&P 500 by 30%. Why? The company has zero U.S. litigation exposure, minimal debt, and generates $8 billion in free cash flow annually—a defensive investor's dream during market turmoil.

Wall Street analysts scramble to recalibrate models. Morgan Stanley's David Adelman captures the sentiment: "PMI is what Philip Morris would have been without the lawsuits—a pure play on emerging market consumer growth." The numbers support this thesis. PMI inherits 77% market share in Argentina, 38% in Indonesia, 36% in Mexico. These aren't just statistics; they're monopolistic positions in markets where smoking rates are still rising.

The separation also unlocks hidden value in financial engineering. As a U.S.-listed but internationally-focused company, PMI can repatriate cash without U.S. tax penalties, access international debt markets at lower rates, and optimize currency exposure across 180 markets. The company immediately announces a $13 billion share buyback program—something unthinkable under Altria's legal constraints.

But perhaps the most profound change is cultural. PMI employees, particularly in research and development, describe a palpable shift. Dr. Manuel Peitsch, Chief Scientific Officer, would later recall: "Suddenly, we could talk about transformation without lawyers vetoing every word. We could invest in reduced-risk products without fear it would be used against us in court." This freedom manifests immediately—R&D spending jumps 40% in the first year post-spin.

The regulatory arbitrage is equally powerful. While the FDA gains authority over U.S. tobacco in 2009, PMI operates in markets with wildly different regulatory frameworks. In Japan, tobacco regulation focuses on tax revenue, not public health. In Indonesia, the government owns significant stakes in tobacco companies. PMI can navigate these varied landscapes without the baggage of U.S. regulatory oversight.

The spin-off also creates an unexpected competitive advantage: speed. Freed from Altria's bureaucracy and legal caution, PMI can make decisions in weeks that previously took years. The company acquires Colombian tobacco company Coltabaco for $452 million just months after the spin—a deal that had been stuck in Altria's legal review for two years.

By December 2008, as the global financial crisis deepens, PMI reports third-quarter earnings that stun analysts: revenues up 15%, operating income up 20%, and margins expanding despite global economic chaos. The stock reaches $60, making early investors 11% returns while the broader market crashes 40%. The separation isn't just successful—it's perfectly timed, creating a defensive growth vehicle just as investors need it most.

IV. Building the International Empire (2008-2014)

The scene: Jakarta, Indonesia, 2009. PMI executives stand in a massive factory where clove cigarettes—kreteks—are still hand-rolled by thousands of workers. They've just completed the $5.2 billion acquisition of Sampoerna, Indonesia's third-largest tobacco company. An analyst asks CEO Louis Camilleri why PMI would pay such a premium for a local brand. His response: "We're not buying cigarettes. We're buying 234 million consumers in the world's most profitable tobacco market."

This acquisition epitomizes PMI's post-spin strategy: aggressive expansion in markets where Western litigation culture doesn't exist, populations are young, and smoking remains socially acceptable. Indonesia offers all three—plus 30% EBITDA margins, nearly double U.S. levels.

The Sampoerna deal also reveals PMI's operational sophistication. Within 18 months, the company modernizes production, reducing hand-rolling from 90% to 30% while maintaining employment through retraining. Cost per unit drops 40%, but retail prices actually increase as PMI premiumizes the brand. It's a playbook they'll repeat globally: acquire local champions, modernize operations, premiumize portfolios, expand margins.

But the real prize remains Marlboro's global march. By 2010, Marlboro commands 9.5% of global cigarette market share outside the U.S.—more than the next four international brands combined. In the Philippines, PMI takes Marlboro from 18% to 31% market share in three years through a single insight: Filipino consumers want aspiration, not affordability. PMI repositions Marlboro as the "graduation cigarette"—what you smoke when you've made it.

The regulatory battles of this era are equally instructive. In 2011, Australia proposes plain packaging for cigarettes—no logos, no colors, just health warnings. PMI responds with a masterclass in regulatory warfare. The company challenges the law through bilateral trade agreements, claiming intellectual property violations. They fund studies showing plain packaging increases illicit trade. They even sue Australia for billions in lost brand value. Though PMI ultimately loses, they delay implementation by three years and discourage other countries from following suit.

Meanwhile, the cash machine hums. From 2008 to 2014, PMI generates $52 billion in operating cash flow—more than the market cap of most Fortune 500 companies. The capital allocation is disciplined: 60% returned to shareholders through dividends and buybacks, 25% invested in emerging market expansion, and critically, 15% poured into R&D.

That R&D investment seems puzzling at the time. In 2009, PMI opens "The Cube"—a $120 million research facility in Neuchâtel, Switzerland. The building's architecture is striking: glass walls, open laboratories, more Silicon Valley than Big Tobacco. Inside, 400 scientists work on projects with code names like "Platform 1" and "Heat-not-Burn 2.0." When asked about the investment, Camilleri is cryptic: "We're building capabilities for products that don't exist yet."

The geographic expansion continues relentlessly. PMI enters Myanmar as military rule ends. They establish operations in Bangladesh through a joint venture. They even return to China—the world's largest tobacco market—through duty-free channels and Hong Kong operations. Each market entry follows a pattern: establish premium position first, volume follows.

By 2013, PMI's transformation from American subsidiary to global empire is complete. The company operates in 180 markets, employs 77,000 people, and sells 850 billion cigarettes annually. International net revenues reach $31 billion, with emerging markets contributing 65%. Operating margins hit 40%—unheard of in consumer products.

But cracks are appearing. Global cigarette volumes peak in 2012 at 5.7 trillion units and begin declining. Smartphone adoption correlates inversely with smoking rates among young adults. E-cigarettes, dismissed by PMI as a "niche product" in 2010, capture 10% of the U.S. market by 2014. The writing isn't just on the wall—it's in the earnings calls where analysts increasingly ask about "next-generation products."

The November 2014 launch of IQOS in Nagoya, Japan, seems like a small event at the time—a pilot program in a single city. PMI's earnings report barely mentions it, buried on page 47 of supplementary materials. But internally, everything is riding on this launch. Five years of R&D, $3 billion invested, and the future of the company condensed into a device the size of a smartphone. The empire has been built. Now it's time to burn it down and build something new.

V. The IQOS Revolution: Betting the Company (2014-2020)

Inside PMI's Nagoya office, November 2014. The IQOS launch team watches real-time sales data on massive screens. Day one: 127 units sold. Day two: 89 units. The product manager turns to colleagues: "We spent $3 billion to sell 200 devices?" But something strange happens in week three—sales triple. By month two, they're backordered. Japanese consumers aren't just buying IQOS; they're evangelizing it.

The technology itself represents a fundamental rethinking of nicotine delivery. IQOS (supposedly meaning "I Quit Ordinary Smoking") heats specially designed tobacco sticks—called HEETS—to 350°C, below combustion's 800°C threshold. No burning means no smoke, no ash, and critically, 90-95% fewer harmful chemicals. The device looks like a premium electronics product: ceramic heating blade, gold-plated charging contacts, aerospace-grade polymer casing. This isn't your grandfather's cigarette—it's tobacco reimagined for the iPhone generation.

The Japan launch location isn't random. Japanese consumers embrace technology, value cleanliness, and respond to premium positioning. More importantly, Japan's regulatory framework allows PMI to make reduced-risk claims without extensive clinical trials. The formula works: IQOS captures 2.9% of Japan's tobacco market in year one, 15.5% by year three—the fastest adoption of any tobacco product in history.

But the real revolution happens in 2016 when CEO André Calantzopoulos makes an announcement that shocks everyone: "We're building PMI's future on smoke-free products. Our goal is to convince all adult smokers who would otherwise continue smoking to switch to better alternatives." The company launches a corporate website—smokefreeworld.com—declaring its intention to eventually stop selling cigarettes entirely.

The internal resistance is fierce. Regional managers, particularly in emerging markets, revolt. One Indonesian executive allegedly tells headquarters: "You want me to tell my team that the products generating 90% of our profits are now evil?" The culture war splits PMI between "traditionalists" protecting cigarette revenues and "transformers" pushing smoke-free alternatives. Calantzopoulos responds by tying executive compensation directly to smoke-free product adoption—convert or forfeit bonuses.

The product engineering behind IQOS reveals PMI's strategic depth. Each HEETS stick contains precisely measured tobacco, optimized for heating rather than burning. The tobacco blend itself is proprietary—higher moisture content, specific leaf cuts, added glycerin for vapor generation. PMI patents everything: the heating mechanism, the tobacco preparation, even the packaging. By 2020, IQOS is protected by 5,500 patents globally, creating a competitive moat that rivals pharmaceutical companies.

Market reception varies wildly. In Japan and Korea, IQOS becomes a status symbol—used openly in offices, restaurants, even hospitals. In Italy, adoption follows Japanese patterns. But in Germany and the UK, growth stalls. The difference? Social acceptance. Where smoking is stigmatized, IQOS is seen as "still smoking." Where smoking remains acceptable, IQOS is perceived as "better smoking."

The FDA authorization process becomes a defining moment. PMI submits 2 million pages of scientific data in 2017, claiming IQOS reduces exposure to harmful chemicals. The FDA's 2019 decision is nuanced: IQOS can be sold in the U.S., but not marketed as "safe." Then, in July 2020, breakthrough: FDA grants Modified Risk Tobacco Product status, allowing PMI to market IQOS as reducing exposure to harmful chemicals. It's the first tobacco product ever to receive this designation.

The economics of cannibalization are counterintuitive but brilliant. IQOS users consume 30% less tobacco by weight than cigarette smokers, but PMI charges 20% premium prices for HEETS. The device itself sells for $100-150, creating upfront revenue. More importantly, IQOS users exhibit 10% higher retention rates than cigarette smokers—they switch brands less frequently. The net result: IQOS users generate 15% higher lifetime value despite consuming less tobacco.

By 2020, the transformation metrics are staggering. IQOS is available in 52 markets. Twenty million adult smokers have switched completely to IQOS. Smoke-free products generate $7.7 billion in net revenues—25% of PMI's total. The company's R&D spending reaches $495 million annually, with 76% dedicated to smoke-free products. PMI employs more scientists, engineers, and technicians than British American Tobacco and Imperial Brands combined.

But the most telling statistic comes from an unexpected source. In 2020, PMI's sustainability report reveals that 38% of company employees are now non-smokers who joined specifically to work on smoke-free transformation. The company that once required employees to smoke during job interviews now attracts talent from Apple, Samsung, and Nestle. The revolution isn't just changing products—it's changing PMI's DNA.

VI. The Swedish Match Acquisition & ZYN (2022-2023)

Stockholm airport departure lounge, May 2022. PMI CEO Jacek Olczak sits across from Swedish Match CEO Lars Dahlgren, a 16-page term sheet between them. The offer: $16 billion for Swedish Match AB, maker of ZYN nicotine pouches. Dahlgren's first reaction: "You're not offering enough." What follows is a six-month negotiation that will reshape the global nicotine industry.

The strategic logic is compelling. Swedish Match generates the bulk of its profit from Swedish-style snuff called "snus" but its relatively new tobacco-free nicotine pouch product ZYN is growing fast in Scandinavia and the United States. PMI sees something others don't: ZYN isn't just another product—it's a platform for entering the U.S. market, which PMI hasn't touched since the 2008 spin-off.

But the deal faces immediate resistance. Elliott Investment Management accumulates a 10.5% stake in Swedish Match, betting they can extract a higher price. Swedish regulators express concerns about market concentration. The European Commission launches an antitrust review. PMI's initial offer of 106 Swedish kronor per share is rejected as "inadequate." By November, after multiple rounds of negotiation, PMI raises the bid to 116 kronor—a 46% premium to Swedish Match's pre-announcement price.

By November 7, 2022, 82.59% of Swedish Match shareholders, including the top 10 shareholders, tender their shares. It's not the 90% PMI wanted for automatic compulsory acquisition, but it's enough. By November 28, PMI acquires 93.11% of shares and initiates compulsory redemption of remaining shares. Swedish Match is delisted from Nasdaq Stockholm on December 30, 2022.

What PMI actually bought becomes clear in the numbers. According to Philip Morris International, 384.8 million ZYN cans were sold worldwide in 2023, up 62% from 237 million cans in 2022. But the real explosion happens in 2024. In Q2 2024 alone, US ZYN shipments reach 135.1 million cans, up 50.3% year-over-year. The growth trajectory is staggering—from a niche Scandinavian product to America's fastest-growing nicotine brand.

The product itself represents a fundamental rethinking of nicotine delivery. ZYN pouches contain no tobacco—just nicotine salts, plant-based fibers, flavorings, and pH adjusters. They're placed between the gum and lip, releasing nicotine through the oral mucosa. No smoke, no spit, no smell. The discretion is the point—you can use ZYN in an office, on a plane, anywhere smoking or vaping is prohibited.

But ZYN's success creates an unexpected problem: PMI can't make enough. A shortage emerges in May 2024, with Philip Morris International stating it was experiencing supply chain tensions. The response is massive. PMI announces over $800 million investment in new ZYN factories—a new facility in Aurora, Colorado, and expansion of the existing Owensboro, Kentucky plant. The Kentucky expansion alone is expected to raise production to around 900 million cans in 2025.

The market dynamics are fascinating. ZYN represented over 70% of the U.S. nicotine pouch industry in 2023, essentially creating a category monopoly. The user base is distinct from traditional tobacco: younger, more educated, more likely to be former vapers than former smokers. One study found a 641% increase in nicotine pouch sales between 2019 and 2022, but just 2.9% of U.S. adults had ever used a nicotine pouch—showing an alarming rate of youth adoption.

The regulatory landscape becomes critical. ZYN operates in a gray zone—not quite tobacco, not quite pharmaceutical. In June 2024, Washington D.C.'s attorney general issues a subpoena to PMI, claiming online ZYN sales violate the district's flavored nicotine ban. PMI immediately halts all online sales, triggering a nationwide shortage and demonstrating how fragile the regulatory foundation remains.

The acquisition also reveals PMI's evolving strategy. This isn't about replacing cigarettes with heated tobacco anymore—it's about building a portfolio of nicotine delivery systems. IQOS for cigarette-like experiences, ZYN for discrete oral nicotine, potentially vaping products in development. Each product targets different use occasions, different consumer segments, different regulatory environments.

By late 2024, the transformation is evident in PMI's financials. Smoke-free products generate 40% of net revenues, with ZYN contributing increasingly to that mix. The company projects shipping 780-820 million ZYN cans in the U.S. alone in 2025—more than double 2023 levels. The Swedish Match acquisition, initially questioned by analysts as expensive, now looks prescient. PMI didn't just buy a product; they bought entry into the U.S. market, a proven technology platform, and most importantly, time—avoiding years of R&D and regulatory approval that building ZYN from scratch would have required.

VII. Modern Era: The Transformation Accelerates (2020-Today)

The moment arrives quietly in PMI's Q4 2023 earnings call. CEO Jacek Olczak pauses before delivering news that would have been unthinkable a decade earlier: "For the first time in our history, IQOS has surpassed Marlboro in net revenue contribution." The architect of global smoking has built something bigger than cigarettes.

The numbers tell a story of accelerating transformation. Smoke-free products reach $13.8 billion in net revenues in 2024—40% of PMI's total. IQOS alone accounts for 30 million users across 84 markets. The company ships 150 billion heated tobacco units annually, each one replacing a traditional cigarette. But the real metric that matters: 73% of IQOS users have completely stopped smoking cigarettes.

The technology evolution continues relentlessly. In 2021, PMI launches IQOS ILUMA, using induction heating instead of blades—no cleaning required, better taste, more consistent experience. The device uses "Smartcore Induction System" technology, heating tobacco from within using a metal heating element embedded in each specially designed TEREA stick. It's tobacco consumption reimagined as consumer electronics, complete with firmware updates and app connectivity.

Geographic expansion follows a sophisticated playbook. Enter premium markets through duty-free shops and flagship stores. Build aspirational positioning before mass market rollout. Partner with local retailers who understand cultural nuances. The formula works: IQOS captures 25% of the Japanese tobacco market, 18% in Lithuania, 15% in Greece. In some cities, heated tobacco outsells cigarettes entirely.

But 2024 brings the most significant development yet. The FDA authorizes marketing of 20 ZYN nicotine pouch products through the premarket tobacco product application pathway—the first nicotine pouches to receive such authorization. This isn't just regulatory approval; it's validation of PMI's transformation strategy. The company now has FDA-authorized products in two distinct categories: heated tobacco and oral nicotine.

The capital allocation tells the transformation story. R&D spending reaches $800 million annually, with 82% directed to smoke-free products. The company employs 1,500 scientists and engineers—more than many pharmaceutical companies. The patent portfolio expands to 8,000 patents globally, creating competitive moats that will last decades. PMI even establishes Vectura Fertin Pharma, a subsidiary focused on inhaled therapeutics beyond nicotine.

Manufacturing transformation is equally dramatic. PMI converts cigarette factories to IQOS production—the Bologna facility, once producing 60 billion cigarettes annually, now manufactures heated tobacco units exclusively. The company invests $8 billion in smoke-free manufacturing capacity from 2020-2025. Production lines use artificial intelligence for quality control, robotics for assembly, and blockchain for supply chain tracking. This isn't your grandfather's tobacco company—it's a technology manufacturer that happens to use tobacco.

The financial performance validates the strategy. Operating margins for smoke-free products reach 38%, approaching cigarette-level profitability years ahead of projections. Cash flow generation remains robust—$12.2 billion in operating cash flow in 2024, supporting both transformation investments and shareholder returns. The dividend yield of 4.5% attracts income investors while growth metrics appeal to momentum traders.

Market perception shifts dramatically. ESG funds that excluded PMI for decades begin reconsidering. The company's inclusion in the Dow Jones Sustainability Index in 2023 signals institutional acceptance of the transformation narrative. Analyst coverage expands beyond tobacco specialists to include technology and healthcare analysts. The stock trades at 18x forward earnings—a premium multiple for a "tobacco" company.

Competition intensifies but PMI maintains advantages. British American Tobacco's Glo and Japan Tobacco's Ploom lag in market share and technology. Chinese companies attempt to enter with cheaper alternatives but can't match PMI's patents or brand equity. The real competition comes from unexpected sources: cannabis companies exploring nicotine, pharmaceutical companies developing cessation products, and technology companies investigating digital therapeutics.

The organizational transformation is perhaps most profound. PMI's employee base shifts from 73% in traditional cigarette operations in 2015 to 45% in 2024. New hires come from Apple, Novartis, Samsung—bringing expertise in user experience, clinical trials, and hardware design. The company establishes "innovation hubs" in Silicon Valley and Shenzhen. Internal culture shifts from defending the past to building the future.

By late 2024, PMI's guidance reveals the endpoint approaching: smoke-free products will exceed 50% of net revenues by 2025, reaching $20 billion. The company maintains its ambition to become "substantially smoke-free" by 2030. Some markets are already there—in Japan, PMI generates 85% of revenues from smoke-free products. The transformation that seemed impossible in 2014 now appears inevitable.

VIII. Playbook: Business & Investing Lessons

The art of the spin-off reaches its apex with PMI's 2008 separation. The formula: identify value trapped by association, create clean structural separation, and unlock different investor bases. PMI's international operations, burdened by U.S. litigation fears, traded at a tobacco multiple when they deserved a consumer goods multiple. The spin-off immediately created $89 billion in market value—not through synergies or cost cuts, but simply by allowing each business to be valued appropriately. The lesson extends beyond tobacco: when different businesses face different risks, serve different markets, or require different strategies, separation often creates more value than combination.

The transformation paradox—cannibalizing yourself before others do—becomes PMI's masterclass. Most companies talk about disruption; PMI actually does it, systematically destroying 60% of its revenue base while maintaining profitability. The key insight: control the pace of disruption. PMI doesn't abandon cigarettes overnight; they manage a 20-year transition, using cigarette cash flows to fund smoke-free development. Each IQOS user generates 85% of cigarette profits while feeling innovative. It's managed obsolescence as art form.

Capital allocation during transformation requires surgical precision. PMI's approach: maintain the dividend to keep income investors, buy back shares to offset dilution, but redirect growth capital entirely to transformation. From 2014-2024, PMI invests $12.5 billion in smoke-free products while returning $80 billion to shareholders. The balance is deliberate—transformation without alienating existing investors. Compare this to Altria's approach: defending cigarettes while making scattered bets on alternatives. PMI's focused transformation versus Altria's hedged bets shows why concentration beats diversification during disruption.

Regulatory arbitrage becomes competitive advantage when executed properly. PMI doesn't fight regulation—they surf it. When Australia mandates plain packaging, PMI shifts focus to markets without such rules. When the FDA delays IQOS approval, PMI builds scale in Japan first. When the EU tightens cigarette regulations, PMI accelerates heated tobacco rollout. The playbook: build regulatory intelligence capabilities, maintain flexibility across markets, and turn compliance into competitive moat. Smaller competitors can't match PMI's regulatory expertise across 180 markets.

Building new categories requires different skills than competing in existing ones. With IQOS, PMI isn't just launching a product—they're creating consumer behavior that didn't exist. This requires education (what is heated tobacco?), infrastructure (charging stations in airports), and patience (seven-year payback periods). The investment is massive but the reward is category leadership. ZYN shows the opposite approach—buying category leadership is faster but more expensive. Both strategies work, but building offers more control while buying offers more speed.

The ESG paradox for tobacco companies reveals important lessons about stakeholder capitalism. PMI's transformation improves health outcomes (reduced-risk products), environmental impact (less agricultural intensity), and social metrics (adult-only marketing). Yet many ESG funds still exclude PMI entirely. The lesson: ESG acceptance lags business transformation by years, sometimes decades. Companies transforming controversial industries face a choice: wait for ESG recognition or focus on fundamental business metrics. PMI chose the latter and outperformed anyway.

Network effects in addictive products create unique dynamics. Traditional network effects (like social media) grow stronger with more users. Addiction network effects work differently—they're individual but socially reinforced. IQOS users don't need other IQOS users, but social acceptance accelerates adoption. PMI leverages this through IQOS lounges, celebrity endorsements, and viral marketing. The product spreads through social circles like fashion, not technology. Understanding these pseudo-network effects explains why some markets (Japan) adopt rapidly while others (Germany) resist.

The M&A integration playbook shows in Swedish Match. Rather than fully integrate, PMI maintains Swedish Match's entrepreneurial culture, Swedish headquarters, and separate brand identity. ZYN remains distinctly un-PMI in marketing and positioning. This "federated model" preserves acquisition value while leveraging PMI's scale in manufacturing and distribution. Too many acquisitions fail through over-integration; PMI's light touch shows when less is more.

Technology adoption in traditional industries requires careful orchestration. PMI doesn't just add technology—they rebuild around it. IQOS isn't a cigarette with electronics; it's consumer electronics that happens to use tobacco. This mental model shift cascades through everything: product development cycles shorten from years to months, software updates improve existing devices, and user experience trumps tobacco quality. Traditional competitors, stuck in tobacco mindsets, can't compete with PMI's technology-first approach.

The ultimate lesson from PMI's transformation: radical change is possible even in the most entrenched industries, but it requires complete commitment. Half-measures fail. PMI's willingness to destroy their core business, invest billions in uncertain outcomes, and maintain conviction through years of losses shows what real transformation demands. Most companies attempting similar pivots fail because they hedge, hesitate, or retreat at the first sign of difficulty. PMI's success comes from burning the boats—making transformation the only option.

IX. Analysis & Bear vs. Bull Case

The Bull Case: Transformation Momentum Accelerating

The smoke-free transformation isn't just working—it's exceeding the most optimistic projections. Smoke-free products reached 40% of net revenues in 2024, ahead of schedule, with margins expanding toward cigarette levels. The math is compelling: IQOS generates $450 revenue per user annually with 73% retention rates, creating predictable, subscription-like revenue streams. With 30 million users growing at 15% annually, the installed base alone guarantees growth through 2030.

The competitive moat widens daily. PMI's 8,000 patents in heated tobacco and oral nicotine create barriers that will take competitors decades to overcome. The FDA's determination that ZYN products meet the public health standard, showing lower risk of cancer and other serious health conditions versus cigarettes and most smokeless tobacco products, provides regulatory validation that money can't buy. First-mover advantage in heated tobacco means PMI defines the category—competitors must follow PMI's lead or risk irrelevance.

Geographic expansion remains in early innings. IQOS operates in 84 markets but generates 70% of revenue from just 10. As PMI enters India, China through duty-free, and Africa, the addressable market multiplies. Each new market follows the proven Japan playbook: premium launch, rapid scaling, market leadership within five years. With 1.1 billion global smokers and only 30 million using heated tobacco, the runway extends for decades.

The financial framework supports aggressive investment while maintaining shareholder returns. Operating cash flow of $12.2 billion funds R&D, capital expenditure, and dividends with room to spare. Net debt of only 2x EBITDA provides flexibility for acquisitions or accelerated investment. The dividend yield of 4.5% attracts income investors while transformation story appeals to growth investors—a rare combination.

Regulatory tailwinds are strengthening globally. Governments recognize harm reduction's role in public health. The UK government explicitly endorses vaping and heated tobacco for smoking cessation. The EU's Tobacco Products Directive allows reduced-risk claims with proper substantiation. Even China, controlling 40% of global cigarette consumption, explores reduced-risk alternatives. PMI's regulatory expertise positions them to benefit regardless of specific frameworks.

The Bear Case: Fundamental Challenges Remain

Despite transformation rhetoric, PMI remains fundamentally an addiction merchant. Whether delivering nicotine through combustion, heating, or oral absorption doesn't change the underlying model: creating and maintaining chemical dependence. Societal tolerance for nicotine addiction is declining, especially among younger generations. PMI may be rearranging deck chairs on a sinking ship.

Regulatory risks remain existential. One FDA reversal on IQOS or ZYN could destroy billions in value overnight. Flavored product bans, already implemented in several jurisdictions, directly threaten ZYN's appeal. Tax authorities increasingly treat all nicotine products equally, eliminating heated tobacco's economic advantage. The regulatory landscape could shift from enabling transformation to preventing it entirely.

Competition intensifies from unexpected directions. Chinese manufacturers produce heated tobacco devices at 30% of IQOS's cost. Cannabis companies eye nicotine as adjacent market. Pharmaceutical companies develop better cessation products. Technology companies explore digital therapeutics. PMI faces threats not just from traditional competitors but from entirely different industries with different capabilities.

The transformation economics remain uncertain. Smoke-free products require continuous R&D investment, shorter product cycles, and technology infrastructure that cigarettes never needed. While revenues grow, the cost structure fundamentally changes. PMI guides to maintaining margins, but history shows technology businesses face margin compression over time. The company may be trading a high-margin declining business for a lower-margin growing one.

Ethical investing concerns limit investor base permanently. Major pension funds, sovereign wealth funds, and ESG-focused institutions exclude tobacco regardless of product evolution. This structural limitation on demand caps valuation multiples. PMI trades at discount to consumer staples peers despite superior growth—this discount may be permanent.

Technology disruption could blindside PMI. What if nicotine becomes deliverable through patches that last months? What if synthetic alternatives eliminate tobacco entirely? What if digital therapeutics make physical products obsolete? PMI invests heavily in current technologies but may miss the next paradigm shift. Kodak dominated film while digital photography developed elsewhere.

Market saturation approaches faster than expected. Developed markets show declining nicotine use across all categories. Emerging markets may follow developed market patterns more quickly due to smartphone penetration and health awareness. The total addressable market for any nicotine product may be structurally declining, making growth a zero-sum game between competitors.

The cannibalization rate accelerates beyond projections. If cigarette volumes decline 10% annually instead of projected 5%, cash flows disappear before smoke-free products compensate. PMI walks a tightrope—transform too slowly and become obsolete, transform too quickly and destroy economics. Current pace seems optimal, but small miscalculations compound over time.

Ultimately, both cases have merit. PMI has engineered one of the most successful corporate transformations in history, building new categories while maintaining profitability. But they're attempting something perhaps impossible: making a tobacco company sustainable in a world increasingly intolerant of addiction. The bull case sees transformation success continuing; the bear case sees structural challenges overwhelming execution excellence. The truth, as always, lies somewhere between.

X. Epilogue & "What Would We Do?"

Standing in PMI's boardroom today, looking at transformation metrics and growth projections, the fundamental question persists: Can a tobacco company truly transform into something else? Or does the original sin of addiction forever define the enterprise, regardless of product innovation?

The answer matters beyond PMI. Every legacy industry faces similar existential questions. Can oil companies become energy companies? Can combustion engine manufacturers become mobility providers? Can banks become technology platforms? PMI's journey offers a template—not perfect, but instructive. Complete transformation requires accepting creative destruction, investing through uncertainty, and maintaining conviction when everyone doubts.

The role of regulation in shaping business strategy emerges as perhaps the most underappreciated dynamic. PMI doesn't operate in free markets—they navigate regulatory mazes that determine what products can be sold, how they're marketed, and what claims can be made. The company that masters regulatory engagement doesn't just comply—they shape the rules. PMI's transformation succeeds partly because they've convinced regulators that harm reduction serves public health. This regulatory arbitrage creates competitive advantages that pure business execution cannot.

What would we do if handed PMI's controls today? First, accelerate the geographic rollout of successful products—ZYN and IQOS have proven product-market fit but remain unavailable in most markets. Second, invest aggressively in the next platform beyond heated tobacco and oral nicotine—perhaps inhaled therapeutics or synthetic nicotine alternatives. Third, separate the declining cigarette business from growth businesses, possibly through another spin-off, allowing each to optimize for different objectives.

The portfolio approach deserves expansion. PMI has IQOS for cigarette-like experiences and ZYN for discrete nicotine. Missing pieces include: cessation products (help users quit entirely), cannabis derivatives (adjacent market with overlapping consumers), and digital therapeutics (behavioral modification through apps). Each addition reduces dependence on any single product while leveraging core capabilities in regulatory navigation and adult consumer marketing.

The sustainability question looms largest. Can PMI achieve their stated goal of becoming "substantially smoke-free" by 2030? The math suggests yes—if current trends continue, smoke-free products will generate 70% of revenues by 2030. But sustainability means more than product mix. It means convincing society that a company built on addiction can transform into one promoting public health. That perception shift may take generations, if it happens at all.

Looking forward, three scenarios seem plausible. The optimistic case: PMI successfully transforms into a healthcare company, leveraging expertise in inhalation and oral delivery for therapeutic purposes beyond nicotine. The realistic case: PMI becomes the dominant reduced-risk nicotine company, accepting the nicotine business's gradual decline while maximizing value during transition. The pessimistic case: Regulatory backlash and social rejection accelerate, forcing PMI into managed decline regardless of product innovation.

The lessons for other legacy industries are clear but challenging. First, transformation requires complete commitment—half-measures guarantee failure. Second, cannibalization is feature, not bug—if you don't disrupt yourself, others will. Third, regulatory engagement matters as much as business execution. Fourth, culture change takes longer than strategy change—plan accordingly. Finally, some transformations may be impossible—knowing when to transform versus when to harvest requires brutal honesty.

PMI's journey from spin-off to smoke-free transformation represents one of business history's most audacious experiments. Whether ultimately successful or not, the attempt itself deserves study. They've shown that even the most entrenched industries can change, that innovation can emerge from unexpected sources, and that corporate transformation, while difficult, remains possible.

The cigarette, invented in the 1880s, dominated the 20th century. PMI is betting that the 21st century belongs to something different—not smoke-free products necessarily, but the idea that harmful products can evolve into less harmful alternatives. It's a bet on harm reduction over prohibition, innovation over resignation, transformation over stagnation.

History will judge whether PMI truly transformed or simply postponed the inevitable. But today, in 2024, the transformation is real, measurable, and accelerating. The company that perfected selling cigarettes is systematically making them obsolete. The paradox remains: Can you build a sustainable future by destroying your past? PMI is finding out, one smoke-free product at a time.

XI. Recent News• **

Q3 2024 Results Exceed Expectations**: Revenue exceeded analyst estimates by 2.3%. Earnings per share (EPS) also surpassed analyst estimates by 11%. Net revenues grew 8.4% year-over-year to $9.9 billion. Organic revenue growth was 11.6%. Net earnings attributable to PMI were $3.1 billion compared to $2 billion in the year-ago quarter.

• IQOS Momentum Accelerates: IQOS achieved a 14.8% year-on-year increase in adjusted in-market sales, with IQOS now available in 92 markets and plans to reach 100 by 2025.

• ZYN Supply Constraints Easing: PMI anticipates meeting consumer demand in Q4, but full inventory replenishment will likely extend into 2025. We have seen some sequential improvement in market share in Q3, and as availability improves, we expect positive market share recovery.

• Full-Year 2024 Guidance Raised: The company raised its full-year guidance for organic revenue growth to around 9.5%, driven by strong performance across its product categories, with strong operating cash flow of around $11 billion for the year.

• FDA Authorization for ZYN Products: The U.S. Food and Drug Administration authorized the marketing of 20 ZYN nicotine pouch products through the premarket tobacco product application (PMTA) pathway following an extensive scientific review. This is the first time the agency has authorized products commonly referred to as nicotine pouches.

• Massive ZYN Production Expansion: Philip Morris International, the owner of Zyn manufacturer Swedish Match, will invest over $800 million in new Zyn factories in the U.S. to meet the growing demand for the flavored nicotine pouches. PMI has announced that a new Zyn factory will be built in Aurora, Colo., and an existing Zyn plant in Owensboro, Ky., will be expanded to increase manufacturing capacity. The expansion of the facility in Kentucky is expected to raise production to around 900 million cans in 2025.

• IQOS U.S. Relaunch: The agreement to end PMI's commercial relationship with Altria Group, Inc. covering IQOS in the U.S. became effective May 1, 2024, allowing PMI direct control of IQOS distribution in the United States for the first time since the spin-off.

XII. Links & References

Long-Form Analysis & Industry Reports

• Philip Morris International Investor Relations: www.pmi.com/investor-relations • FDA Modified Risk Tobacco Product Applications: www.fda.gov/tobacco-products • Truth Initiative Nicotine Pouch Research: truthinitiative.org/research-resources • World Health Organization Tobacco Reports: www.who.int/teams/health-promotion/tobacco-control

Key SEC Filings

• PMI Annual Report (10-K): Latest filing available on SEC EDGAR • PMI Quarterly Reports (10-Q): Quarterly updates on SEC EDGAR • Swedish Match Acquisition Documents: Form 8-K filings from 2022 • Spin-off from Altria Documents: Historical S-1 and 8-K filings from 2008

Recommended Books on Tobacco Industry

• "Ashes to Ashes: America's Hundred-Year Cigarette War" by Richard Kluger • "The Cigarette Century" by Allan M. Brandt • "Barbarians at the Gate" by Bryan Burrough and John Helyar (RJR Nabisco story) • "Thank You for Smoking" by Christopher Buckley (satirical but insightful)

Academic Studies & Research

• "Heated Tobacco Products: A Systematic Literature Review" - Tobacco Control Journal • "Nicotine Pouches and Public Health" - New England Journal of Medicine • "Corporate Transformation in Controversial Industries" - Harvard Business Review • "The Economics of Tobacco Harm Reduction" - Journal of Health Economics

Industry & Competitor Resources

• British American Tobacco Investor Relations: www.bat.com/investors • Japan Tobacco International: www.jti.com • Altria Group Investor Relations: investor.altria.com • Imperial Brands: www.imperialbrandsplc.com

Regulatory & Public Health Resources

• FDA Center for Tobacco Products: Regulatory updates and product authorizations • European Commission Tobacco Products Directive: EU regulatory framework • Campaign for Tobacco-Free Kids: Public health perspective on industry transformation • Public Health Law Center: Legal analysis of tobacco regulation

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube