Pinterest: The Visual Discovery Engine That Almost Wasn't

I. Introduction & Episode Roadmap

Picture this: It's 2009, and while Facebook races toward 500 million users and Twitter explodes with real-time conversation, three guys in a Palo Alto apartment are staring at a failed mobile shopping app. They've burned through most of their seed funding. The iPhone App Store is barely a year old. Mobile payments are a disaster. Their investors are getting nervous.

What happens next becomes one of Silicon Valley's most unlikely success stories—not because of explosive growth or viral mechanics, but because of patient observation and the courage to build something fundamentally different from everything else in tech. Today, Pinterest stands as something remarkable: 553 million monthly active users generating $1,154 million in Q4 2024 revenue—the company's first billion-dollar quarter. The full year 2024 brought in $3,646 million in revenue, growing 19% year over year. But these numbers only hint at the deeper story.

Here's the paradox that makes Pinterest fascinating: It's not quite social media—there are no status updates, no friend graphs, no real-time feeds of what your college roommate had for breakfast. It's not quite a search engine either—you don't come to Pinterest to find specific answers or navigate to known destinations. Instead, Pinterest occupies this strange, wonderful middle ground as a "visual discovery engine"—a place where 553 million people come not to broadcast their lives or find specific information, but to discover what they don't yet know they're looking for.

The story we're about to tell isn't one of viral growth hacks or winner-take-all network effects. It's about three guys who watched their users carefully, pivoted thoughtfully, and built something that Silicon Valley never quite understood but hundreds of millions of people couldn't live without. It's about choosing to be useful rather than addictive, positive rather than engaging at all costs, and patient in a world that rewards the opposite.

This is the story of how a failed mobile shopping app became a $22 billion visual discovery platform, why it took nine years to go public when others rushed out in four, and how being "uncool" in Silicon Valley might have been Pinterest's greatest strategic advantage.

We'll explore the Tote failure that birthed an empire, the nine months when only 10,000 users showed up, the hockey stick that made Pinterest the fastest site to reach 10 million users, and the modern AI transformation that's driving billion-dollar quarters. Along the way, we'll unpack why Pinterest's business model works, what makes it different from every other platform, and whether this visual discovery engine can continue growing in a world dominated by TikTok, Instagram, and whatever comes next.

II. Pre-Pinterest: The Tote Story & Cold Brew Labs

The year is 2008. Ben Silbermann sits in his cubicle at Google, where he's been working as a product specialist for nearly two years. The son of two doctors—his parents are ophthalmologists who moved from Des Moines to practice in California—Silbermann had followed the expected path: Yale degree, safe corporate job, stability. But something gnaws at him. He's been at Google since 2006, watching the company transform the internet, yet he can't shake the feeling that he's meant to build something himself.

His childhood offers clues to what comes next. Growing up, Silbermann was the kid who collected things obsessively—insects, stamps, anything he could organize and catalog. "I've always been a collector," he'd later tell interviewers. "I think collecting is a really human thing to do. It's a way for people to express who they are."

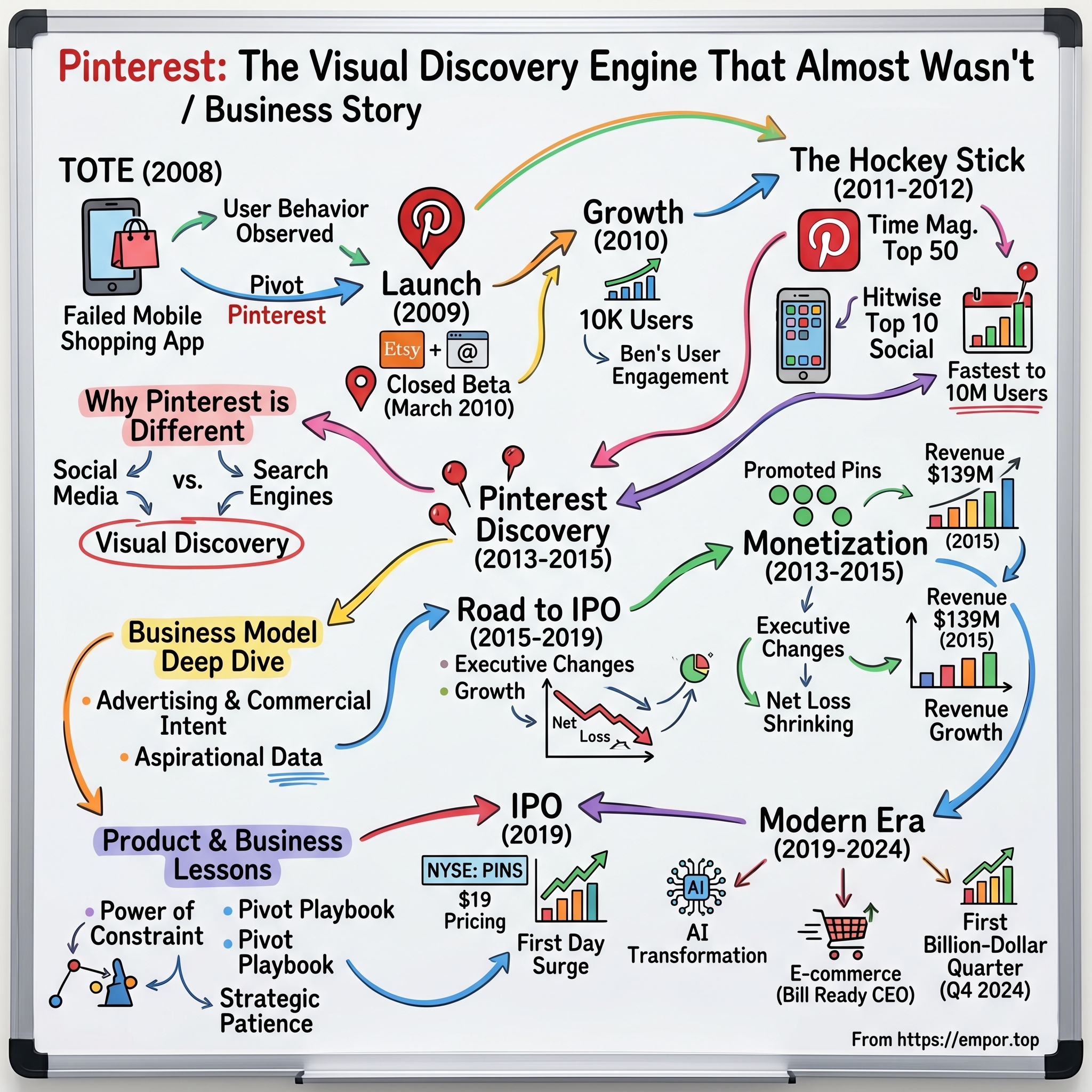

By Christmas 2008, Silbermann makes his move. He leaves Google—much to his parents' bewilderment—and partners with his college friend Paul Sciarra, a Columbia MBA who'd been working at venture capital firm Radius Ventures. Together, they form Cold Brew Labs, a name that sounds hip and caffeinated enough for a startup but reveals nothing about their actual ambitions. Their first product isn't Pinterest—it's Tote. Launched in 2009 roughly six months after Cold Brew Labs was founded, Tote was a shopping comparison app where users could browse apparel and other goods from 30 retailers. Users could save items as favorites and receive push notifications when those items reduced in price. The timing seems perfect: the iPhone App Store has just opened, mobile is clearly the future, and e-commerce is booming.

Except it isn't. Tote struggled as a business, significantly due to difficulties with mobile payments—the technology was not sophisticated enough to enable easy on-the-go transactions, inhibiting users from making many purchases via the app. Shopping and e-commerce had not yet become mainstream in 2009, and consumers weren't using their mobile devices for shopping companion apps.

But here's where the story takes its critical turn. Instead of stubbornly pushing forward or giving up entirely, Silbermann and Sciarra do something remarkable: they watch their users. Tote users were amassing large collections of favorite items and sharing them with other users. The behavior struck a chord with Silbermann, and he shifted the company to building Pinterest, which allowed users to create collections of a variety of items and share them with each other.

Despite Tote's failure, Silbermann and Sciarra discovered something interesting upon analyzing Tote's user data. Tote's users were saving products using the favorite function and discovering new items, often emailing images to themselves. Most searches were by product category rather than brand. They soon realized that very few people searched Tote for brand-specific items. Instead, they searched by product category: shoes, dresses, pants, jackets. This led the team to develop the idea of "buckets" into which users could organize their collections of images.

The insight is profound: People weren't using Tote to buy things. They were using it to collect things, to organize their aspirations and interests, to create visual representations of their ideal selves. The shopping app had accidentally become a curation tool. And Silbermann, the lifelong collector, immediately understood the implications.

Silbermann and Sciarra's new prototype was largely finished by the end of the autumn of 2009. But they need help with the design and technical architecture. During a trip to New York City, Silbermann met Evan Sharp through a mutual acquaintance. Sharp understood what Silbermann and Sciarra were trying to do right away. Sharp would eventually leave New York and move west to California, where he worked as a product designer at Facebook before joining Silbermann and Sciarra to work on their project full-time as a third cofounder.

The transformation from Tote to Pinterest represents something deeper than a simple pivot. It's a fundamental reimagining of what the internet could be used for—not just to transact or communicate, but to dream, to plan, to become. As Silbermann would later reflect, collecting is a deeply human activity, a way for people to express who they are. And that insight, born from a failed shopping app in a Palo Alto apartment, would soon reshape how hundreds of millions of people interact with the visual web.

III. The Birth of Pinterest (2009–2010)

The name comes at Thanksgiving dinner, 2009. Ben Silbermann's girlfriend came up with the name of Pinterest at Thanksgiving dinner in 2009, and the website beta version of Pinterest was launched in March of the following year. The name itself is perfect—combining "pin" and "interest," it immediately conveys both action and purpose. Unlike the abstract tech names proliferating at the time (Twitter, Tumblr, Flickr), Pinterest tells you exactly what it does.

The development of Pinterest began in December 2009, and the site launched the prototype as a closed beta in March 2010. In January of 2010, the first "pin" is posted on Pinterest. It's a Valentine papercut from Etsy. There's something poetic about that first pin—not a product to buy, not a status update, but a piece of handmade art, something beautiful someone wanted to remember.

The design philosophy emerges from Sharp's architectural background and Silbermann's collector's mindset. They reject the dominant social media paradigm entirely. No status updates. No real-time feeds. No friend graphs or follower counts displayed prominently. Instead, they create something that feels more like a personal scrapbook that happens to be online—a place where the content matters more than the person posting it.

In March 2010, Pinterest launches as a closed beta version on the Web. The founders send invites to 100 of their friends, who each get five invites of their own. The invitation system isn't just about creating exclusivity—it's about ensuring that early users understand what Pinterest is for. Each new user comes through someone who can explain this strange new thing that isn't quite social media, isn't quite bookmarking, isn't quite shopping.

But growth is painfully slow. Nine months after the launch, the website had 10,000 users. In Silicon Valley terms, this is a disaster. Facebook had millions of users at this point in its lifecycle. Twitter was exploding. Instagram hasn't even launched yet but will race to 25,000 users on its first day when it does.

Silbermann refuses to panic. Instead, he does something that would become Pinterest lore: he personally engages with users. He sends personal emails. He organizes meetups in coffee shops. He even gives out his personal phone number to early users, telling them to call if they have problems or suggestions. One story has him attending a bloggers' conference in Salt Lake City, walking up to strangers and asking them to try his website.

In June 2010, Pinterest receives $500,000 in angel funding from investors FirstMark Capital, Jeremy Stoppelman, Jack Abraham, Michael Birch, Scott Belsky, Shana Fisher, Kevin Hartz, Cohen, Hank Vigil, Fritz Lanman, and William Lohse. It's not much money by Silicon Valley standards, but it keeps the lights on.

The early Pinterest looks different from other platforms in crucial ways. While Facebook optimizes for engagement and Twitter for real-time information, Pinterest optimizes for something else entirely: inspiration and utility. The infinite scroll of images—what would later be called the "Pinterest Grid"—creates a browsing experience that's both addictive and purposeful. You're not checking Pinterest; you're using it.

By November 2010, there were 80,000 collections and a million items shared on Pinterest. These numbers reveal something important: the average user is creating multiple boards and pinning dozens of items. Engagement is deep, even if user growth is slow. People who "get" Pinterest truly understand and embrace it.

The founders also make a crucial decision about content moderation and community guidelines. Unlike other platforms that would struggle with toxic content, harassment, and misinformation, Pinterest establishes itself early as a "positive" platform. It's not a place for news, politics, or personal drama. It's a place for recipes, home decor, fashion, and DIY projects. This positioning—dismissed by some as limiting—would prove to be one of Pinterest's greatest strategic assets.

What Silbermann, Sciarra, and Sharp are building is something fundamentally different from the social media playbook. They're not trying to connect everyone to everyone else. They're not trying to capture every moment or every thought. They're building a utility disguised as a social network, a place where the social graph matters less than the interest graph, where who you are matters less than what you love.

IV. The Hockey Stick: From 10K to 10M Users (2011–2012)

Everything changes with the iPhone app.

Pinterest launches an iPhone app in March 2011. What happens next stuns even the founders. The app brings more users than anyone anticipated—suddenly Pinterest makes sense on mobile in a way it never quite did on desktop. The ability to pin on the go, to capture inspiration wherever you find it, transforms Pinterest from a destination to a companion. Then comes validation from an unexpected source. On August 10, 2011, Time magazine listed Pinterest in its "50 Best Websites of 2011" article. TIME's Harry McCracken writes about Pinterest with genuine enthusiasm: "Pinterest makes the process painless by offering a Pin It button that lets you grab pictures of your favorite things as you browse the Web. The site then collects the images on 'boards' that other users can follow and comment on. Perusing other folks' boards, featuring everything from picturesque travel scenes to oddly beautiful bacteria, is as enjoyable as building your own."

The TIME feature acts like gasoline on a fire. Suddenly, Pinterest isn't just a quirky site used by design bloggers and craft enthusiasts—it's legitimate, validated by mainstream media. Traffic explodes. In December 2011, the site became one of the top 10 largest social network services, according to Hitwise data, with 11 million total visits per week.

The accolades keep coming. Pinterest won the Best New Startup of 2011 at the TechCrunch Crunchies Awards. This is particularly sweet for Silbermann—TechCrunch had barely covered Pinterest during its slow early growth, and now they're giving it their highest honor.

For January 2012, comScore reported the site had 11.7 million unique U.S. visitors, making it the fastest site ever to break through the 10 million unique visitor mark. Let that sink in: Pinterest went from 10,000 users nine months after launch to becoming the fastest site to reach 10 million users. That's not just growth—that's a complete transformation.

The infrastructure struggles to keep up. Silbermann and a few programmers operated the site out of a small apartment until mid-2011. They're literally running one of the internet's fastest-growing sites from a residential internet connection. The apartment becomes Silicon Valley legend—the scrappy startup that could barely afford servers suddenly processing millions of pins.

The money follows the momentum. In early 2011, the company secured a US$10 million Series A financing led by Jeremy Levine and Sarah Tavel of Bessemer Venture Partners. In October 2011, the company secured US$27 million in funding from Andreessen Horowitz, which valued the company at US$200 million.

But the real story isn't the numbers—it's who's using Pinterest and how. The user base skews heavily female (around 80% at this time), and they're not tech early adopters. They're teachers planning classroom activities, brides organizing weddings, home cooks collecting recipes. Pinterest has somehow vaulted over the early adopter phase entirely and gone straight to mainstream America.

The viral mechanics are unlike anything Silicon Valley has seen. Pinterest doesn't spread through friend networks like Facebook or through influencers like Twitter. It spreads through Google Images. People search for "wedding centerpieces" or "backyard landscaping ideas," find a Pinterest board, and get sucked into the infinite scroll. They don't even realize they're on a social network—they think they've found the world's best idea catalog.

On May 17, 2012, Japanese electronic commerce company Rakuten announced it was leading a $100 million investment in Pinterest, alongside investors including Andreessen Horowitz, Bessemer Venture Partners, and FirstMark Capital, based on a valuation of $1.5 billion. In less than two years, Pinterest has gone from a failed shopping app to a billion-dollar unicorn.

But success brings complications. Co-founder Paul Sciarra left his position at Pinterest in April 2012 for a consulting job as entrepreneur in residence at Andreessen Horowitz. The departure is amicable, but it marks the beginning of Pinterest's transition from scrappy startup to serious company.

The copyright issues begin to surface. Artists and photographers complain about their work being pinned without permission. Pinterest has to scramble to implement better attribution systems and opt-out mechanisms. They're learning what every platform eventually learns: when you become the place where content lives, you become responsible for that content.

Yet through it all, Pinterest maintains its essential character. While other platforms chase engagement through outrage and controversy, Pinterest remains determinedly wholesome. It's the place you go to plan, to dream, to create. The hockey stick growth isn't just about user numbers—it's about Pinterest finding its purpose as the internet's inspiration engine.

V. Finding the Business Model: Promoted Pins & Early Monetization (2013–2015)

For three years, Pinterest has been the internet's feel-good story—millions of users, billions of pins, zero revenue. In Silicon Valley, this is normal. Build the audience first, figure out the business model later. But Pinterest faces a unique challenge: How do you monetize inspiration without destroying it?

The answer comes in 2013 with the launch of "Promoted Pins"—a name so deliberately understated it could only come from Pinterest. Not "ads," not "sponsored content," but "Promoted Pins." The psychology is perfect: these are still pins, still useful, still beautiful. They just happen to be promoted. The first year is modest but promising. In that first calendar year, Pinterest brought in around $24 million or $25 million, depending on reporting. For a company valued in the billions, this might seem embarrassing. But Pinterest isn't optimizing for quick cash—they're building something sustainable.

The execution is remarkably thoughtful. In October 2013, Pinterest began displaying advertisements in the form of "Promoted Pins". Promoted Pins are based on an individual user's interests, things done on Pinterest, or a result of visiting an advertiser's site or app. The ads blend seamlessly into the user experience—so seamlessly that many users don't even realize they're ads at first.

Then comes the rocket fuel. In 2015, Pinterest pulled that off for its investors, clocking revenue of $139 million (sources agree on this one), up 479 percent in a single year. That's not just growth—that's validation of the entire model. Pinterest has proven that you can monetize inspiration without destroying it.

But reality starts to bite. TechCrunch has obtained documents that show Pinterest has been forecasting $169 million in revenue this year and $2.8 billion in annual revenue by 2018. Pinterest was also expecting to grow its monthly active users to 151 million by the end of 2015 and 329 million by 2018. As TechCrunch wrote, the firm expected $169 million in top line during 2015. Turning in $139 million as it did was about an 18 percent flub.

The funding keeps flowing despite the miss. That's the same year that investors poured another $200 million into the firm at a valuation of around $5 billion. Those investors were betting that Pinterest would have a quick revenue ramp. In 2015 Pinterest put $367 million more into its warchest, pushing its valuation over the $10 billion mark. Indeed, the firm was worth a little over $11 billion following its Series G, according to Crunchbase.

The product innovations during this period reveal Pinterest's strategic thinking. In June 2015, Pinterest unveiled "buyable pins" that allows users to purchase things directly from Pinterest. This isn't about becoming an e-commerce platform—it's about closing the loop between inspiration and action, between wanting and having.

The challenge Pinterest faces is unique in Silicon Valley. The first is that Facebook had a vital head start on Pinterest in terms of advertising. By the time Pinterest introduced support for video and built its own native video player in 2016, Facebook had been enjoying strong revenue growth from its video ads for two years. However, aside from Facebook's considerable competitive advantage with video ads (and advertising in general), one of the most serious problems facing Pinterest's advertising team was that many advertisers were reluctant to reallocate their budgets from the proven success of Facebook to Pinterest's cheaper—yet largely untested—Promoted Pins.

There's also the perception problem. Pinterest is seen as "just for women"—around 70-80% of users are female during this period. For some advertisers, this is a feature, not a bug. But for others, it limits Pinterest's appeal. The company would spend years trying to shake this perception while also celebrating the engaged, high-intent audience it had cultivated.

The work culture during this period reflects the tension between Pinterest's deliberate approach and Silicon Valley's need for speed. Decisions take time. Features are tested endlessly. The company operates more like a design studio than a typical tech startup. This frustrates some employees and investors, but it's also why Pinterest maintains its unique character while other platforms devolve into engagement-driven chaos.

By the end of 2015, Pinterest has established its business model but faces hard questions. Can it grow fast enough to justify its valuation? Can it expand beyond its core demographic? Can it compete with Facebook and Google for advertising dollars? The answers will determine whether Pinterest becomes a sustainable business or another Silicon Valley cautionary tale.

VI. The Long Road to IPO: Growth, Challenges & Culture (2015–2019)

The middle years are where most startups either find their groove or lose their way. For Pinterest, it's both—a period of steady growth punctuated by missed expectations, executive turnover, and the constant question: When will they go public?

In 2016, Pinterest grew again, posting $298.9 million in revenue. The growth rate is impressive—more than doubling from the previous year—but still far from the billions Pinterest had projected. Pinterest's top line also expanded to $472.9 million in 2017, up just over 58 percent compared to the prior year.

The work culture becomes a defining characteristic, for better and worse. Pinterest is described as slow when it comes to making decisions. Where Facebook's motto was "Move fast and break things," Pinterest's might as well be "Move deliberately and perfect things." Product releases take months, sometimes years. Features are tested with small user groups, refined, tested again. It drives some employees crazy, especially those who've come from faster-moving companies.

The executive team undergoes significant changes during this period. The most notable addition is Francoise Brougher, who joins as Pinterest's first COO. Brougher brings serious operational credibility—she's ex-Square, ex-Google, someone who knows how to scale a business. Her hiring signals that Pinterest is getting serious about becoming a real company, not just a beloved product.

The funding rounds continue, though with less fanfare than before. The company raised more, went through some secondary transactions, and finally raised another $150 million in 2017 at a valuation of a little more than $12 billion. Pinterest has now raised $1.5 billion through 26 funding rounds—an enormous amount of capital that creates enormous expectations. The billion-dollar milestone approaches slowly. Pinterest is poised to almost double revenue this year, getting close to $1 billion, according to people familiar with the matter. After hitting $500 million in sales in 2017, Pinterest is on pace to almost double that this year. But context matters: Reaching $1 billion in revenue will mark a significant milestone, but it's way below previous estimates. In 2015, TechCrunch reported on leaked financial documents that showed Pinterest was then projecting sales of $2.8 billion by 2018.

The company's strategic position starts to clarify during this period. Advertisers and people familiar with the company say Pinterest has found its footing in the past year and, by combining visual, social and search ads into one platform, has become an important place for retail, fashion, home goods, beauty and do-it-yourself brands. "No platform capitalizes on the social-search marriage like Pinterest does," Boulia said.

Perhaps most importantly, Pinterest avoids the toxicity plaguing other platforms. Additionally, Pinterest has avoided the safety and privacy issues, like online bullying and misinformation, that have plagued other platforms. While Facebook faces Congressional hearings and Twitter battles trolls, Pinterest remains the internet's happy place—a positioning that looks increasingly valuable as brand safety becomes paramount for advertisers.

The data reveals Pinterest's unique value proposition. In Mary Meeker's 2016 Internet Trends Report, the analyst-turned-venture capitalist said that 55 percent of Pinterest users were using the site to find and shop for products, compared with only 12 percent for Facebook and Instagram and 9 percent for Twitter. This isn't just engagement—it's commercial intent, the holy grail of digital advertising.

The user growth continues steadily if not spectacularly. By September 2018, the company reported that it had 250 million monthly active users across desktop and mobile apps, up 25 percent on the year before, with more than half coming from outside the US. International growth becomes both Pinterest's biggest opportunity and biggest challenge—users are there, but monetization lags dramatically.

The IPO drumbeat grows louder. The company is aiming to go public by mid-2019, and has a current valuation of $13 billion to $15 billion, based on secondary market trading, multiple people say. But there's tension in these numbers. Recall that Pinterest had targeted 329 million monthly active users in 2018 and revenue of $2.8 billion. The real results are smaller. The firm was under 250 million monthly active users in May of 2018, and it will graze, but likely not surpass, $1 billion in sales this year. That's a far cry from both projections.

Pinterest's final 2018 numbers tell the story: In the original S-1 it revealed that it had revenue of $755.9 million in the year ending December 31, 2018, up from $472.8 million in 2017. The company posts a net loss shrank to $62.9 million last year from $130 million in 2017. Growth is solid, losses are shrinking, but the gap between promise and performance remains.

By early 2019, the die is cast. Pinterest files confidentially to go public, joining the parade of unicorns heading to Wall Street. But unlike Uber's growth-at-all-costs story or Lyft's winner-take-all narrative, Pinterest's story is harder to tell. It's profitable on a contribution basis, growing steadily, beloved by users. But it's also slower, more deliberate, less explosive than what Silicon Valley has trained investors to expect.

The long road to IPO reflects Pinterest's essential character: patient, thoughtful, unwilling to sacrifice quality for speed. Whether the public markets will reward this approach remains to be seen.

VII. The IPO Story: From "Undercorn" to Public Company (2019)

Wall Street has a new word for companies like Pinterest: "undercorn. "Pinterest plans to sell shares of its stock, titled "PINS," at $15 to $17 apiece, less than the roughly $21 per share it charged private market investors to participate in its mid-2017 Series H, its last private financing. That IPO price translates into a mid-range valuation of $10.64 billion, or nearly $2 billion under the $12.3 billion valuation it garnered after its last round, hence "undercorn."

The term itself captures Silicon Valley's discomfort with reality. Pinterest has the unusual distinction of being an "Undercorn", a multi-billion dollar company going public at a valuation below its last private valuation. The word "undercorn" appears to have been coined circa 2014 by business journalist Dan Primack, but it's evolved to mean a unicorn that goes public at a price below its most recent private market valuation.

The numbers behind the undercorn label tell a complex story. Pinterest posted revenues of $299 million in 2016, $473 million in 2017 and $756 million in 2018. There's no denying the company's clear path to profitability, as its losses are shrinking year-over-year while profits grow, but 2018's revenues are still 16 times less than Pinterest's "decacorn" valuation. The company posts a net loss of $62.9 million in 2018, dramatically improved from $130 million in 2017.But then something remarkable happens. The company originally anticipated an IPO price in the $15 to $17 range, but ended up announcing a finalized IPO pricing of $19 per share on Wednesday. The demand is so strong that Pinterest prices above its expected range—still below its private valuation, but higher than the "undercorn" pricing initially feared.

On April 18, 2019, Pinterest began its first day of trading Thursday at $23.75, up 25%. The stock continued to climb, rising 28.4% to trade at $24.40 per share with a market cap of nearly $13 billion. That puts Pinterest's valuation well above the $12 billion at which it raised its latest round of funds in 2017. The undercorn has become... just a regular unicorn again.

The successful debut provides vindication for Silbermann's patient approach. In interviews following the IPO, he tries to distinguish Pinterest from other platforms. Pinterest CEO Benjamin Silbermann tried to distinguish the company from other major tech firms such as Facebook and Twitter, saying in an interview on CNBC's "Squawk Alley" following the debut that "Pinterest isn't a social network." "We really think about it as a utility," he said. "We're less focused on making it a place where you talk to your friends every day or you follow celebrities."

The IPO raises $1.4 billion, giving Pinterest a substantial war chest for growth. More importantly, it provides liquidity for employees and early investors who've been waiting for over a decade in some cases. Even with Pinterest's new status as an undercorn, Bessemer still owns a stake worth upwards of $1 billion. At a midpoint price, FirstMark and a16z's shares will be worth about $700 million each.

The timing proves fortuitous. Pinterest goes public alongside Zoom Video Communications, which soared 80 percent above its IPO price of $36. The dual success stories help restore confidence in tech IPOs after Lyft's disappointing performance. The strong showing out of Pinterest and Zoom is a big sigh of relief for investors who had been wearily eyeing the IPO market after Lyft failed to take off once it began trading in late March.

The comparison to other tech IPOs is revealing. Lyft had a fast start last month, when its IPO jumped 9% on opening day, but then crashed below its IPO price. Uber, preparing for its own mega-IPO, watches nervously. Pinterest, with its steady growth and shrinking losses, suddenly looks like the responsible adult in the room.

Wall Street's initial reception suggests that Pinterest's "undercorn" status might have been a blessing in disguise. Silicon Valley has a tendency to over-value unprofitable consumer-facing businesses; Pinterest's down round IPO could be a sign of Wall Street's reckoning with Silicon Valley's vanity metrics. By pricing conservatively, Pinterest leaves room for growth rather than disappointment.

The IPO also marks a transition. Pinterest's IPO also marks the end of an era in some regards. It's likely the last of the previous generation of social media startups to enter the public markets. Founded in 2009, it watched as Facebook, Twitter, LinkedIn, and Snap all held IPOs. Pinterest took the longest road, but it arrives as perhaps the most mature, most thoughtful of them all.

The first day surge proves something important: The market values Pinterest not for what it promises to become, but for what it already is—a unique platform with loyal users, growing revenue, and a path to profitability. The undercorn label, it turns out, was just another example of Silicon Valley missing what really matters.

VIII. The Modern Era: AI, E-commerce & Billion Dollar Quarters (2019–2024)

The pandemic arrives like a sledgehammer to most businesses. For Pinterest, it's rocket fuel. Suddenly, everyone is stuck at home with time to plan, dream, and create. Home improvement projects. Recipes for sourdough bread. DIY crafts with the kids. Pinterest becomes the pandemic's unofficial headquarters for aspirational domestic life. User growth explodes. The stock price soars to an all-time high of $89.15 on Feb. 16, 2021.

But the pandemic boom creates its own problems. Growth that seemed sustainable proves temporary. As the world reopens, users have less time for browsing dream kitchens and planning imaginary vacations. The stock begins its long slide back to earth.

Then comes the bombshell. On June 28, 2022, longtime Pinterest CEO Ben Silbermann is stepping down, the company announced Tuesday. Bill Ready, who was previously in charge of Google's commerce business, is taking over the helm, effective Wednesday. Prior to joining Google, Ready was executive vice president and chief operating officer of PayPal. The announcement sends shares jumping more than 5% in after-hours trading—Wall Street's vote of confidence in new leadership.

The transition marks a fundamental shift in Pinterest's strategy. "In our next chapter, we are focused on helping Pinners buy, try and act on all the great ideas they see," Silbermann said in a statement. "Bill is a great leader for this transition. He is a builder who deeply understands commerce and payments." After twelve years building Pinterest from a failed shopping app to a public company, Silbermann moves to the newly created role of executive chairman.

Ready's appointment signals Pinterest's evolution from inspiration to transaction. His background—PayPal, Braintree, Google Commerce—tells you everything about where Pinterest is headed. This isn't about collecting beautiful images anymore; it's about turning those images into purchases, those dreams into reality. The AI transformation under Ready's leadership is comprehensive. At its Pinterest Presents event in 2024, the company unveiled automation and artificial intelligence features for its Pinterest Performance+ offering. Now, brands can modify blank, white or flat backgrounds to make AI-powered lifestyle content. Pinterest claims marketers can update assets quicker, with 50% less input. Early results have shown a 64% decrease in cost per action, and 1.8 times return on ad spend. There was also a 30% increase in conversion rates.

Performance+ represents Pinterest's answer to Meta's Advantage+ and Google's Performance Max—AI-powered advertising tools that optimize campaigns automatically. Performance+ will enhance ad creative, optimize budget management, and use Return on Ad Spend (ROAS) bidding to determine ideal spending levels. It also streamlines A/B testing for more effective campaign performance. Pinterest claims that in early testing, most advertisers saw at least a 10 percent improvement in cost per acquisition.

The visual search capabilities evolve dramatically. Pinterest Lens, which allows users to search with images instead of words, processes billions of visual searches. The platform's AI can now understand not just what's in an image, but the style, mood, and context—understanding that someone searching for "mid-century modern" has fundamentally different tastes than someone interested in "maximalist" design.

"Ad innovation on Pinterest has been at an all-time high," Pinterest chief revenue officer Bill Watkins said. "We're still the place for brands to drive discovery, but we're now delivering on lower funnel and creative too. Brands are increasing Pinterest in their media mix and they no longer need to choose between awareness or lower funnel performance."

The international expansion finally starts paying dividends. While the U.S. still dominates revenue, international users now represent the majority of Pinterest's user base. The challenge remains monetizing these users at anywhere near U.S. levels, but progress is steady.

The platform also benefits from its positioning as the "positive" corner of the internet. While Meta faces scrutiny over mental health impacts and X (formerly Twitter) battles misinformation, Pinterest remains focused on inspiration and utility. During the vaccine misinformation crisis, Pinterest simply blocked all vaccine searches rather than trying to moderate content—a blunt but effective approach that kept the platform clean.

Revenue was $1,154 million for Q4 and $3,646 million for 2024, growing 18% and 19%, respectively, year over year. The billion-dollar quarter finally arrives in Q4 2024—Pinterest's first. "2024 was a banner year for Pinterest, capped off by a milestone Q4 – achieving the company's first billion-dollar revenue quarter and a record 553 million monthly active users, as we continue to drive profitable growth and free cash flow," said Bill Ready, CEO of Pinterest.

The transformation from Silbermann's patient builder approach to Ready's aggressive commercialization proves successful. Adjusted EBITDA was $471 million and $1,032 million for Q4 and 2024, respectively. Free cash flow was $250 million for Q4 and $940 million for 2024. Pinterest isn't just growing—it's profitable, generating substantial cash flow, and positioned for sustainable growth.

The modern Pinterest barely resembles the scrapbooking site it once was. It's an AI-powered visual search and commerce platform, a place where inspiration meets transaction, where machine learning understands human taste. The journey from Tote to today—from a failed shopping app to a billion-dollar quarter—represents one of Silicon Valley's most patient, thoughtful transformations.

IX. Business Model Deep Dive: Not Social, Not Search, But Something Else

Pinterest occupies a space that shouldn't exist according to conventional Silicon Valley wisdom. It's not a social network—there are no status updates, no friend graphs, no real-time feeds. It's not a search engine—people don't come with specific queries expecting specific answers. So what exactly is Pinterest's business, and why does it work?

The answer lies in understanding commercial intent. In Mary Meeker's 2016 Internet Trends Report, the analyst-turned-venture capitalist said that 55 percent of Pinterest users were using the site to find and shop for products, compared with only 12 percent for Facebook and Instagram and 9 percent for Twitter. This isn't casual browsing—this is active planning, consideration, purchasing.

The revenue model is deceptively simple: advertising. But Pinterest's ads work differently than on other platforms. The primary products include Promoted Pins (standard image ads that blend into the feed), Shopping Ads (which allow direct purchasing), Video Pins (for more engaging content), and Carousel Ads (multiple images in a single ad unit). What makes these formats powerful isn't their technical sophistication—it's their context.

When someone searches for "backyard renovation ideas" on Pinterest, they're not just browsing—they're planning a project. They have budget. They have intent. They're looking for inspiration that will turn into action. An ad for outdoor furniture or landscaping services isn't an interruption; it's a solution. This is why Pinterest can charge premium rates despite having far fewer users than Facebook or TikTok.

The unique value proposition extends beyond commercial intent. Pinterest is a positive platform by design. Additionally, Pinterest has avoided the safety and privacy issues, like online bullying and misinformation, that have plagued other platforms. For advertisers, this means brand safety—their ads won't appear next to controversial content, political arguments, or toxic comments. In an era where brand safety has become paramount, Pinterest's wholesome environment is a competitive advantage.

The data Pinterest collects is fundamentally different from other platforms. Facebook knows who your friends are. Google knows what questions you have. Pinterest knows what you aspire to be. It knows you're planning a wedding before you've told your friends. It knows you're thinking about remodeling your kitchen before you've called a contractor. This aspirational data is gold for advertisers.

"The ability to say we know [one person] is a mid century modern guy and [another person] is a maximalist is because you've expressed that to us via your behavior on the platform," Crystal told Digiday, describing it as a special sauce of sorts. Pinterest understands taste in a way other platforms don't, and taste drives purchasing decisions.

The platform dynamics create a virtuous cycle. Users come to Pinterest in a planning mindset, ready to discover and save ideas. Advertisers reach these users when they're most receptive to commercial messages. The visual nature of the platform favors products that photograph well—fashion, home decor, food, beauty. These categories also happen to have high margins and strong e-commerce adoption.

But there are challenges in this model. The biggest is international monetization. Rest of World MAUs: 307 million, growing 15% year over year. While international users make up the majority of Pinterest's base, they generate a fraction of the revenue per user compared to the U.S. and Canada. The ARPU (Average Revenue Per User) dynamics reveal the challenge: U.S. users might generate $20+ per year, while international users generate less than $1.

The demographic concentration is both strength and weakness. Pinterest's user base skews heavily female (around 70%), older (millennials and Gen X), and affluent. This is advertiser catnip for certain categories—wedding planning, home improvement, fashion. But it limits Pinterest's total addressable market and makes it vulnerable to platforms that can serve these audiences plus everyone else.

Pinterest's approach to content moderation deserves special attention. Rather than trying to moderate billions of pieces of content for accuracy or appropriateness, Pinterest simply doesn't host the types of content that cause problems. No news. No politics. No real-time events. When vaccine misinformation became a problem, Pinterest didn't try to fact-check—it simply blocked vaccine-related searches entirely. This blunt approach wouldn't work for Facebook or Twitter, but it works perfectly for Pinterest's use case.

We have doubled outbound clicks to advertisers year-over-year. Both conversions and measurability are improving dramatically on our platform. And we've cut cost-per-clicks in half—and advertisers are telling us that this is having a positive impact on their return on ad spend. The improvement in advertising effectiveness reflects both technical improvements (better targeting, better formats) and the fundamental strength of Pinterest's model.

The competitive moat is subtle but real. Google could build a visual search engine—and has tried with Google Lens and Google Collections. Meta could create inspiration boards—and has experimented with various features. But neither can replicate Pinterest's culture, its established user behavior, or its position as the "positive place" on the internet. Pinterest benefits from what might be called "use case network effects"—the more people use it for planning and inspiration, the better the content becomes for planning and inspiration, which attracts more people looking to plan and be inspired.

The business model's sustainability depends on several factors continuing to hold true: that people will continue to need inspiration for major life events and projects, that visual discovery remains distinct from social networking and search, that advertisers will pay premium rates for high-intent audiences, and that Pinterest can maintain its positive platform positioning while others struggle with content moderation.

The genius of Pinterest's business model is that it's built on human aspiration rather than human connection or information needs. People will always dream about better homes, perfect weddings, ideal vacations. Pinterest has positioned itself as the place where those dreams take shape—and increasingly, where they turn into purchases. It's not social, not search, but something uniquely valuable: a commercial inspiration engine.

X. Playbook: Product & Business Lessons

Every successful company leaves behind lessons, but Pinterest's playbook is particularly instructive because it breaks so many Silicon Valley rules. While others moved fast and broke things, Pinterest moved deliberately and perfected things. While others chased engagement at all costs, Pinterest optimized for utility. While others rushed to IPO, Pinterest took nine years to go public. The lessons from this approach are worth examining.

The Power of Constraint

Pinterest succeeded not by trying to be everything to everyone, but by being very specific about what it was and wasn't. No status updates. No messaging. No news. No real-time feeds. Each constraint made the product simpler, cleaner, more focused. In a world of feature creep, Pinterest proved that subtraction can be more powerful than addition.

This principle extended to the user base. Silbermann said he wrote to the first 5,000 users, offering his phone number and even meeting with some of them. Rather than trying to appeal to everyone, Pinterest focused on people who "got it"—primarily women interested in fashion, food, home decor, and DIY projects. Only after dominating these categories did Pinterest expand to others.

Personal Founder Engagement

Silbermann's hands-on approach with early users became Pinterest lore, but it reveals a deeper principle: in the early days, the founder's vision and enthusiasm can be the product's greatest asset. Those personal emails, phone calls, and coffee shop meetups didn't just recruit users—they created evangelists who understood and shared the vision.

This approach doesn't scale, but it doesn't need to. The first 1,000 or 10,000 users set the culture for the next million. By personally ensuring those early users understood and loved Pinterest, Silbermann created a foundation that supported exponential growth.

The Pivot Playbook

The transition from Tote to Pinterest offers a masterclass in reading user behavior versus forcing original vision. Unfortunately, it soon became evident that Tote wasn't going to work out. Shopping and e-commerce had not yet become mainstream in brick-and-mortar retail in 2009, and consumers weren't using their mobile devices for shopping companion apps.

But instead of stubbornly pushing forward or giving up entirely, Silbermann and Sciarra watched what users were actually doing. Tote users however were amassing large collections of favorite items and sharing them with other users. The behavior struck a chord with Silbermann, and he shifted the company to building Pinterest, which allowed users to create collections of a variety of items and share them with each other.

The lesson: Sometimes the best product is hiding inside your failed product. The key is being humble enough to see it and brave enough to pursue it.

Patient Capital

Pinterest raised $1.5 billion through 26 funding rounds before going public—an enormous amount of capital that created enormous expectations. But this patient capital also allowed Pinterest to build deliberately, to focus on user experience over monetization, to wait until the business model was proven before going public.

Compare this to companies that rushed to IPO with unsustainable unit economics or unclear paths to profitability. Pinterest went public with growing revenue, shrinking losses, and a clear monetization strategy. The patient approach meant less dilution for early investors and employees, and more stability as a public company.

Visual-First Design in the Instagram Age

Pinterest pioneered the infinite scroll of images that Instagram would later perfect, but with a crucial difference: Pinterest's grid was about discovery, not social validation. The design encouraged collecting and organizing, not posting and performing. This subtle distinction created entirely different user behavior and, ultimately, a different business model.

The visual-first approach also made Pinterest inherently mobile-friendly. When the iPhone app launched in 2011, it felt native to the platform in a way that Facebook and Twitter—still text-heavy at the time—did not. Pinterest understood that mobile meant visual before most others did.

Building for Positive Use Cases

"Pinterest isn't a social network." "We really think about it as a utility," he said. "We're less focused on making it a place where you talk to your friends every day or you follow celebrities." This positioning—as a utility rather than a social network—freed Pinterest from the engagement-at-all-costs mentality that has plagued other platforms.

Pinterest optimized for successful project completion, not time on site. For satisfied users who found what they needed, not addicted users who couldn't stop scrolling. This approach seemed to leave money on the table in the short term but created a sustainable, defensible business in the long term.

The Challenge and Opportunity of Being "Uncool"

Pinterest was never cool in Silicon Valley terms. It was for suburban moms, not urban techies. It was about wedding planning and recipe collecting, not disrupting industries or changing the world. This uncoolness was actually a superpower—it meant less competition, less scrutiny, and more focus on serving actual users rather than impressing the tech press.

The lesson for founders: Sometimes the best opportunities are in markets that seem boring or uncool to Silicon Valley insiders. These markets often have real users with real problems willing to pay real money for solutions.

Strategic Patience in Product Development

Pinterest's slow, deliberate approach to product development frustrated some employees and investors, but it prevented the feature bloat that plagued other platforms. Each new feature was tested extensively, refined repeatedly, and launched only when it genuinely improved the user experience.

This patience extended to monetization. Pinterest didn't introduce ads until 2013, three years after launch. When they did, the ads (Promoted Pins) were so well integrated that many users didn't even realize they were ads. The patience to get the product right before monetizing preserved user trust and engagement.

The Platform Paradox

Pinterest faced a unique challenge: How do you build a platform based on other people's content without becoming either a copyright nightmare or a content moderation disaster? The solution was elegant: focus on inspiration and planning rather than ownership and creation. Users weren't claiming content as their own; they were collecting it for personal use. This subtle distinction kept Pinterest out of most copyright disputes while still allowing users to build valuable collections.

International Expansion Lessons

Pinterest's international growth offers both cautionary tales and success stories. User growth outside the U.S. was strong, but monetization lagged dramatically. The lesson: user growth without revenue growth is vanity metric. Pinterest had to essentially build different businesses in different markets, with different advertising relationships, different user behaviors, and different monetization strategies.

The Modern Playbook: AI and Authenticity

Under Bill Ready's leadership, Pinterest has embraced AI aggressively but authentically. "Ad innovation on Pinterest has been at an all-time high. We're still the place for brands to drive discovery, but we're now delivering on lower funnel and creative too," Pinterest Chief Revenue Officer Bill Watkins said in a statement. "Brands are increasing Pinterest in their media mix and they no longer need to choose between awareness or lower funnel performance.

The AI isn't just bolted on—it's integrated into the core product experience, improving search, personalization, and advertising effectiveness. This is the modern playbook: use AI to enhance what makes your product unique, not to chase what everyone else is doing.

The overarching lesson from Pinterest's playbook is that there's no single path to success. Moving slowly can be as effective as moving fast. Serving a specific audience can be as valuable as serving everyone. Being useful can be as powerful as being engaging. The key is understanding your unique strengths and having the conviction to pursue them, even when everyone else is doing something different.

XI. Analysis & Investment Case

As Pinterest enters 2025 with its first billion-dollar quarter behind it and a market cap hovering around $22 billion, investors face a complex question: Is this a mature platform approaching its ceiling, or a commerce engine just hitting its stride?

The Bull Case: Unique Position in the Purchase Funnel

Pinterest sits at a unique point in the customer journey—after awareness but before purchase, in what marketers call the "consideration" phase. This is where dreams become plans, plans become projects, and projects require products. No other major platform owns this space as completely as Pinterest does.

The numbers support this positioning. Pinterest achieves historic $1.15B Q4 revenue, marking its first billion-dollar quarter. Record 553M monthly users and 41% EBITDA margin showcase platform's growing dominance. More importantly, the quality of these users continues to improve. These aren't passive scrollers—they're active planners with commercial intent.

The AI advantages are real and accelerating. Pinterest's visual search capabilities, built on billions of user-curated images, create a dataset that's nearly impossible to replicate. Google has the technology but not the user behavior. Meta has the users but not the use case. Pinterest's combination of technology, data, and user intent creates a defensible moat that's widening, not shrinking.

The international opportunity remains massive. With most users outside the U.S. but most revenue inside it, Pinterest has a clear path to growth: monetize international users at even a fraction of U.S. rates. If Pinterest can achieve just 25% of U.S. ARPU in international markets, it would roughly double revenue.

The platform's positive positioning becomes more valuable every day. As other platforms grapple with content moderation, political polarization, and mental health concerns, Pinterest remains the safe space for both users and advertisers. This isn't just about avoiding problems—it's about being the platform brands want to be associated with.

The Bear Case: Competition from All Sides

Pinterest faces competition from literally everyone. Google is investing heavily in visual search through Lens. Meta continually adds Pinterest-like features to Instagram and Facebook. Amazon wants to own the entire purchase funnel. TikTok is increasingly driving commerce. Each competitor has advantages Pinterest lacks—more users, more data, more resources, or faster growth.

The slow product velocity that once seemed thoughtful now risks seeming sluggish. While Pinterest carefully tests features, competitors launch and iterate rapidly. TikTok went from zero to a commerce powerhouse in less time than it takes Pinterest to roll out a new ad format. In the AI arms race, speed matters, and Pinterest's cultural DNA may not support the pace required.

The ARPU challenges are structural, not temporary. International users generate less revenue not just because Pinterest hasn't figured out monetization, but because those markets have lower advertising rates, less e-commerce penetration, and different user behaviors. The gap may narrow but might never close.

The demographic concentration that once seemed like focus now looks like limitation. Young users gravitate to TikTok and Instagram. Men remain largely absent from the platform. Pinterest's core user base—millennial and Gen X women—is valuable but finite. Without expanding beyond this base, growth will inevitably slow.

The Financial Reality

Adjusted EBITDA was $471 million and $1,032 million for Q4 and 2024, respectively. Net cash provided by operating activities was $254 million for Q4 and $965 million for 2024. Free cash flow was $250 million for Q4 and $940 million for 2024. These aren't just positive numbers—they're accelerating. Pinterest is generating real cash flow, not just adjusted profits.

The balance sheet is clean. With $2.5 billion in cash and marketable securities and minimal debt, Pinterest has the resources to invest in growth, weather downturns, or return capital to shareholders. This financial strength provides options and flexibility that many growth companies lack.

The valuation question depends on your perspective. At roughly 6x revenue, Pinterest trades at a premium to Meta (5x) but a discount to younger, faster-growing platforms. The price-to-free-cash-flow multiple of about 23x seems reasonable for a company growing revenue at nearly 20% with expanding margins.

The Strategic Options

Pinterest has several paths forward, each with different risk-reward profiles:

-

Double down on commerce: Integrate more deeply with e-commerce platforms, enable more direct purchasing, become the discovery layer for online shopping. This is clearly Ready's vision, but execution risk is high.

-

Expand internationally: Invest heavily in salesforce and partnerships outside the U.S., accepting lower margins for growth. This requires patience and capital but could unlock massive value.

-

Broaden the use base: Aggressively court male users, younger demographics, new use cases. This risks diluting what makes Pinterest special but could dramatically expand the TAM.

-

AI-first platform: Become the leader in AI-powered visual discovery and creation. This plays to Pinterest's strengths but requires sustained technical investment.

-

Strategic sale: With its unique assets and clean balance sheet, Pinterest could be attractive to larger players. Google could integrate it with Shopping and Lens. Amazon could use it as a discovery layer. Meta could eliminate a competitor. Microsoft could enter social commerce.

The Gen Z Question

Perhaps the biggest unknown is whether Pinterest can capture Gen Z. These users have grown up with TikTok and Instagram, not Pinterest. They discover through algorithms, not search. They prefer video to static images. Everything about Gen Z seems antithetical to Pinterest's model.

But there are glimmers of hope. Gen Z values authenticity and mental health, areas where Pinterest excels. They're interested in hobbies and personal growth, core Pinterest use cases. They shop online more than any previous generation. If Pinterest can adapt its product without losing its essence, Gen Z could drive the next wave of growth.

The Investment Conclusion

Pinterest represents a rare combination in tech: a proven business model with significant untapped potential. It's profitable but still growing. It's established but not stagnant. It's valuable to advertisers but good for users. These balances are difficult to achieve and even harder to maintain.

For growth investors, Pinterest offers exposure to e-commerce, AI, and digital advertising trends without the regulatory risk of larger platforms or the execution risk of unprofitable startups. For value investors, it's a cash-flow-positive business trading at a reasonable multiple with clear paths to margin expansion.

The key risk isn't that Pinterest will fail—it's that it will succeed but not spectacularly. Pinterest might become a solid, profitable, mid-sized platform that never quite breaks through to the next level. For some investors, that's perfectly fine. For others seeking the next Meta or Google, it's not enough.

The investment case ultimately comes down to whether you believe in Pinterest's vision of being the platform where inspiration meets action. If commerce continues shifting online, if visual search becomes primary, if brands need safe platforms for advertising, then Pinterest is positioned to capture enormous value. If not, it remains a nice business for a specific audience—valuable but not transformative.

What's clear is that Pinterest has proven the skeptics wrong before. The company that was too slow, too niche, too "uncool" for Silicon Valley has built a billion-dollar business with half a billion users. Betting against Pinterest has been a losing proposition for fifteen years. Whether that continues depends on execution, competition, and the evolving nature of how people discover and buy products online.

For long-term fundamental investors, Pinterest offers something increasingly rare: a differentiated platform with a sustainable business model, reasonable valuation, and multiple paths to growth. It may never be the biggest or fastest-growing platform, but it might be one of the most enduring.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube