Roku: The Story of TV's Neutral Switzerland

I. Introduction & Episode Roadmap

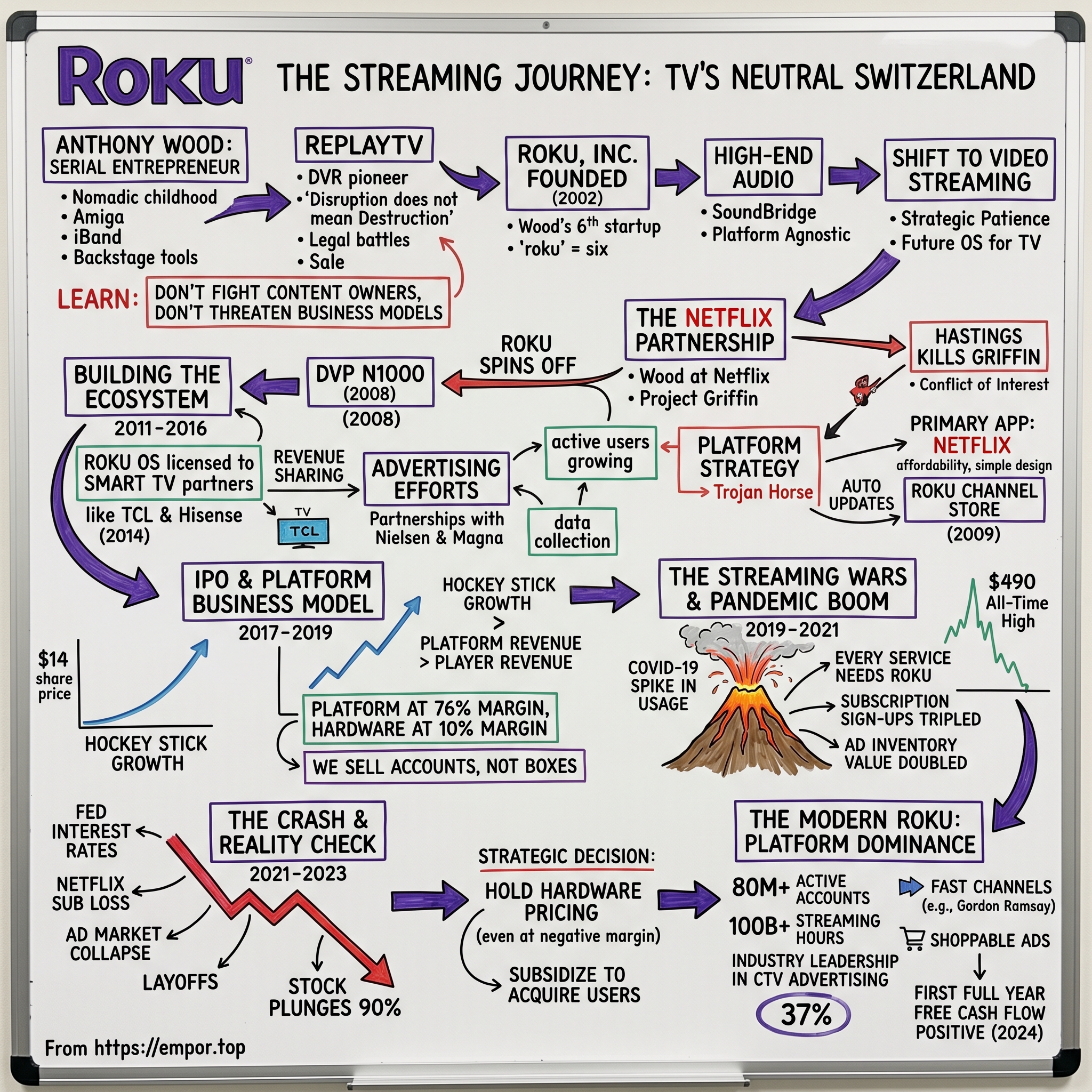

Picture this: It's July 2021, and Roku's stock is hitting an all-time high of $490, with investors mesmerized by a pandemic-fueled streaming boom that seemed unstoppable. The company that started as a Netflix side project had somehow become the U.S. market leader in streaming video distribution, reaching nearly 145 million people by 2024. Fast forward just eighteen months, and that same stock had cratered 90%, leaving investors wondering if they'd witnessed the greatest pump-and-dump in streaming history or merely a temporary setback in a longer transformation story.

The central question isn't just how a company founded to make high-definition video players became streaming TV's dominant platform—it's how Anthony Wood, a British-born serial entrepreneur who'd already failed once in the DVR wars, managed to position Roku as the Switzerland of the streaming wars, remaining neutral while tech giants Amazon, Apple, and Google battled for dominance.

This is a story of perfect timing meeting imperfect execution, of a founder who bet his own money repeatedly on technology shifts that seemed obvious to him but mystified Silicon Valley investors. It's about how selling hardware at a loss became a genius strategy, how advertising replaced subscriptions as the real prize, and why being the arms dealer in a content war proved more valuable than being a combatant.

We'll trace Roku's journey from Wood's sixth startup attempt (roku means "six" in Japanese) through the dramatic Netflix spinoff weeks before launch, the IPO euphoria, the pandemic rocket ship, and the subsequent reality check that saw the stock plummet from those $490 heights. Along the way, we'll unpack the platform neutrality strategy that made Roku indispensable, the advertising pivot that transformed its economics, and the brutal math of why hardware losses can create software fortunes.

Key themes we'll explore: How platform businesses really work, why timing beats technology in consumer electronics, the art of strategic neutrality in platform wars, and the dangerous addiction of pandemic-era growth multiples. This is the Roku story—equal parts triumph, hubris, and unexpected resilience.

II. Anthony Wood: The Serial Entrepreneur

Wood was born and grew up in Manchester, England, followed by the State of Georgia in the U.S. At the age of 13, he moved to the Netherlands with family, and then lived in Texas in the U.S. This nomadic childhood would shape a worldview that saw opportunities where others saw obstacles—a trait that would define his entrepreneurial journey.

Growing up—first in Manchester, England, and then in Georgia and Texas—he was one of those kids who tinkers with everything. He built transistor radio kits, a Morse telegraph. He spent the eighth-grade in the Netherlands, where he took a computer class and taught himself how to program. By the time he reached Texas A&M University, Wood wasn't just another engineering student—he was already building businesses.

While in college, Wood founded his first company, "AW Software", to sell computer programs. He also founded "SunRize Industries" while studying engineering, developing software and hardware for the Amiga. The Amiga community was small but passionate, and Wood found his first taste of product-market fit creating tools for creative professionals who needed affordable alternatives to expensive Silicon Graphics workstations.

The breakthrough came in 1995. Wood had been working on web development tools when the internet was still explaining itself to mainstream users. His company, iBand, caught the attention of a struggling Macromedia, which was desperately trying to pivot from CD-ROM authoring tools to the web. In March 1996, Macromedia acquired iBand Inc., developer of the Backstage family of dynamic web development tools, for $32 million—the deal was actually 860,000 shares of Macromedia stock valued at US$ 32 million. Wood was thirty years old and suddenly wealthy.

But wealth didn't mean comfort. Steve Shannon, who co-founded iBand and is now general manager of content and services at Roku, paints a picture of Wood at this time as almost preternaturally confident and driven: "Imagine if you had half a million bucks to your name that you had earned through your own sweat equity. I think most people would want to squirrel that away or maybe put it in a house. But Anthony is just a double-down kind of guy, so he took that money and rolled it into his next startup." It's a gamble Wood has made repeatedly in his career. His tenure at Macromedia was rocky, and involved a demotion in fact if not in title. When his two-year contract was up, he left to found ReplayTV.

A fan of Star Trek: The Next Generation, he was often frustrated at having to miss new episodes when they aired. Out of that frustration his company was born. ReplayTV, launched in 1997, represented Wood's first assault on the living room. The concept was revolutionary: a digital video recorder that could pause live TV, skip commercials, and even share shows between devices. The product launched at CES 1999, literally side-by-side with a competing product from a company called TiVo.

What followed was a masterclass in how being right about technology doesn't guarantee business success. ReplayTV won Best of Show at CES. Walt Mossberg chose it over TiVo in a head-to-head review. The technology was superior—ReplayTV could skip commercials automatically and share recordings over the internet, features TiVo wouldn't match for years. But TiVo had better marketing, cleaner branding, and most importantly, better relationships with cable companies and retailers.

ReplayTV was purchased by SONICblue in 2001 for a reported $42 million. The timing seemed perfect—digital video was exploding, and SONICblue wanted to challenge Apple in digital media. But the company had picked a fight it couldn't win. An ad-skipping feature resulted in lawsuits from the likes of Paramount to MGM to Disney resulting in SonicBlue ultimately going bankrupt. On March 23, 2003, SONICblue filed for Chapter 11 bankruptcy, and on April 16 sold most of its assets, including ReplayTV, to the Japanese electronics giant D&M Holdings.

Wood watched his creation descend into legal hell and bankruptcy from the outside, having already moved on to his next venture. The ReplayTV experience had taught him crucial lessons: Don't fight content owners directly. Don't threaten existing business models. And most importantly, sometimes being Switzerland—neutral and useful to all sides—is more profitable than being a combatant.

The serial entrepreneur emerged from the ReplayTV saga with battle scars and wisdom. He'd learned that disruption doesn't mean destruction, that partners are more valuable than enemies, and that in platform wars, the arms dealers often outlast the armies. These lessons would prove invaluable when, in October 2002, he founded his sixth company. In 2002, Wood founded Roku, Inc., his sixth startup, to market home digital devices. "Roku" means "six" in Japanese.

III. Roku's Founding & Early Years (2002-2007)

Roku was founded in October 2002 as a limited liability company (LLC), by ReplayTV founder Anthony Wood. Roku (六), meaning "six" in the Japanese language, represented the fact that Roku was the sixth company Wood started. The company was founded as a maker of high-definition video players, and was funded by Wood himself with money he had earned from selling other businesses, including ReplayTV.

The name itself told a story. Susan (Anthony's wife) and I were eating at a Japanese restaurant one night, and I was trying to think of a name for Roku. I asked the waiter the Japanese word for five, which is 'go.' Go was a failed technology company back in the day, so I said, 'What about six?' The waiter said, 'Roku,' and I said, 'Okay, we'll go with that.'" It was casual, almost flippant—but it captured Wood's approach: keep moving forward, don't overthink, build the next thing.

The early Roku was nothing like the streaming giant we know today. Wood initially focused on high-end audio products, launching the SoundBridge line of network music players in 2003. These weren't revolutionary devices—they let you stream music from your computer to your stereo system—but they were well-designed, reliable, and most importantly, platform-agnostic. While Apple was locking users into iTunes, Roku's devices worked with everything: iTunes, Windows Media Player, Rhapsody, whatever you had.

This neutrality wasn't accidental. Wood had learned from ReplayTV that picking fights with content owners was suicide. Instead, he positioned Roku as the friendly intermediary, the Swiss Army knife of digital media. The SoundBridge devices found a small but devoted following among audio enthusiasts and early adopters who appreciated the open approach. By 2005, Roku was selling products in Best Buy and had established itself as a legitimate, if niche, consumer electronics company.

But Wood saw these audio products as a stepping stone. He could see the future coming. He had jotted it down in a notebook years earlier, long before the technology was ready. The future was streaming video. The DVR was only a midpoint, a stepping stone. In 2002, one year after selling ReplayTV, he launched Roku, a company whose ambition is nothing less than to be the operating system for television.

The challenge was timing. In 2002, streaming video was a joke. Most Americans still had dial-up internet. YouTube didn't exist. Netflix was mailing DVDs in red envelopes. But Wood had been here before—too early with ReplayTV, watching TiVo reap the rewards of the market he'd helped create. This time, he would be patient. He would build the infrastructure, establish the relationships, and wait for the technology to catch up to his vision.

By 2006, the landscape was shifting. Broadband penetration had reached a tipping point. YouTube had exploded onto the scene, proving that people would watch video on their computers. More importantly, Netflix had quietly launched a "Watch Instantly" feature, offering a limited selection of movies and TV shows for streaming. The problem was getting that content from computers to television screens, where people actually wanted to watch it.

Wood had been tracking Netflix's moves carefully. He knew Reed Hastings from Silicon Valley circles—both were entrepreneurs who'd made their fortunes in the first dot-com boom and were now trying to reinvent entertainment. In early 2007, Wood made his move. He didn't pitch Roku as a company to acquire or a technology to license. Instead, he pitched himself. In 2007 Netflix, Inc. employed Wood as the vice president of Netflix's "Internet TV", directly under Reed Hastings. Wood continued to be the CEO of Roku in this period.

It was an unusual arrangement—Wood would work part-time at Netflix while remaining CEO of Roku. The real game was getting inside Netflix's plans for streaming hardware. Wood knew Netflix needed a device. He knew they were considering building it themselves. And he knew that if he played his cards right, Roku could be the company to build it.

The chess match had begun. Wood brought a small team from Roku to work on what would become Project Griffin, positioning them as Netflix employees on loan. He made himself indispensable, leveraging his ReplayTV experience and his deep understanding of consumer hardware. All the while, he kept Roku alive as a separate entity, knowing that at some point, Netflix would have to make a choice: become a hardware company or stay focused on content.

The bet was that Reed Hastings, one of Silicon Valley's most disciplined strategists, would eventually realize that hardware was a distraction. Wood was gambling his company's future on another CEO's moment of clarity. It was audacious, risky, and perfectly timed. The streaming revolution was about to begin, and Wood had maneuvered Roku into pole position—not through superior technology or marketing muscle, but through strategic patience and positioning.

By late 2007, everything was in place. The bandwidth was there. The content deals were signed. The device was ready. All that remained was for Netflix to make a decision that would transform both companies and create the template for how streaming would conquer the living room.

IV. The Netflix Partnership & Project Griffin (2007-2008)

December 2007. The Netflix campus in Los Gatos was buzzing with barely contained excitement. They codenamed the top-secret project "Griffin," after Tim Robbins' character from the film "The Player." After all, that's what the team was building: The Netflix Player, a black and boxy device, as plain and compact as a necklace case, which subscribers would hook up to their televisions to stream movies and TV shows from the web. Netflix executives knew it could fundamentally change how the company delivered content to its customers, who were used to waiting days for DVDs to arrive by mail. Soon, Netflix could leverage the digital content deals it was striking with studios to dominate the living room, a war still waging today between industry giants like Apple, Google, and Microsoft. It was December 2007, and the device was just weeks away from launching.

The Griffin team had been working around the clock for months. The Netflix Player had gone through the typical development stages, which are traditionally referred to as EVT, DVT, and PVT–that is, engineer, design, and product validation testing. During this process, the team refined everything from the software and user interface to the device's thermal requirements and supply chain. (Working with Frog Design on the form factor, the group imagined at one point dying the device red to look like a Netflix envelope.) The hardware had gone through endless rounds of product reviews in front of Hastings in the Netflix amphitheater. Internal beta testing had been done; marketing materials had been printed; prices had been set; and advertisements were being shot.

The culmination of years of work was captured in an internal video that would later become Silicon Valley legend. During the all-hands meeting, the entire company saw its future on the big screen, in a video detailing "The Griffin Initiative." A spoof on the Dharma Initiative from the TV show Lost, which was wildly popular at the time, the video poked fun at the company's production process. "Product managers…used highly evolved scientific processes," says the narrator, as Netflix employees in lab coats throw darts at a wall and play Pong. The video also features a trip to a Foxconn supplier outside Shanghai–one of the first times video was shot inside a Foxconn manufacturing facility, a source tells me.

Then, in a move that would define both companies' futures, Reed Hastings killed it.

Hastings decided that having a company-branded set-top box would do more harm than good, realizing a fundamental truth about platform businesses: you can be a content company or a hardware company, but being both creates conflicts of interest that limit growth. "We were getting so close to shipping the hardware, and Reed decides, 'I changed my mind — I don't want to do hardware anymore. If we ship our own hardware, it could be viewed as competitive,'" Wood told Fast Company. "Putting all that money into it; getting it as far along as he did — and then deciding we're not going to do it? Wow. I was surprised. There was so much momentum inside the company."

But Hastings wasn't being capricious. He'd been having conversations that Wood wasn't privy to—with Apple about Apple TV, with Microsoft about Xbox, with Sony about PlayStation. The message was clear: if Netflix launched its own hardware, it would be declaring war on every potential distribution partner. Why would Apple feature Netflix on Apple TV if Netflix was selling a competing box? Why would game consoles integrate Netflix if the company was trying to make them obsolete?

The solution was elegant: spin off the entire project to Roku. Netflix would transfer the Griffin device, the team that built it, intellectual property, and even some cash to Roku. In exchange, Netflix would take an equity stake—about 15% of the company. Wood would get his device, Netflix would stay neutral, and consumers would get a dedicated streaming player without the baggage of platform politics.

Netflix invested $6 million in Roku as part of an equity funding round. More valuable than the money was what came with it: a nearly finished product, momentum, and most importantly, Netflix's commitment to support the device at launch. The Roku DVP N1000 would launch not as the Netflix Player, but as a Roku device that happened to play Netflix. The distinction was crucial.

Netflix then decided instead to spin off the company, and Roku released their first set-top box in 2008. Its primary function was to connect to a television via composite video and offer access to Netflix's growing library of streaming movies and TV shows. This initial focus on a single service was a strategic move, allowing Roku to establish a foothold in the emerging streaming market. The device was relatively affordable and easy to use, making it an attractive option for consumers looking to experience streaming content on their TVs.

The first Roku player launched in May 2008 at $99.99—deliberately priced to undercut Apple TV's $229 price point. It did one thing: stream Netflix. No rentals, no purchases, no other services. Just Netflix. The simplicity was intentional. Wood had learned from ReplayTV that feature creep killed products. Make it simple, make it work, make it cheap. The enthusiasts would come first, then the masses.

The response was immediate and positive. Within months, Roku had sold 100,000 units. But Wood knew that being a one-service player was dangerous. Netflix had given Roku life, but depending on a single partner was a recipe for eventual irrelevance. The same week the first Roku shipped, Wood's team was already in negotiations with Amazon about adding their video service. By fall 2008, they'd added Amazon Video on Demand, Major League Baseball, and several smaller services.

Netflix sell all of its Roku shares, translating to nearly 15% of Roku's equity, to Menlo Ventures to avoid the perception of potentially favoring one streaming distribution manufacturer over another. This was another crucial moment—Netflix's exit as a shareholder freed Roku to be truly neutral. No longer was it "Netflix's box"—it was the streaming box, period.

The Griffin saga revealed the genius of both Reed Hastings and Anthony Wood. Hastings had the discipline to kill a project at the finish line when he realized it threatened Netflix's larger strategy. Wood had the foresight to position himself to catch what Hastings threw away. Both men understood that in platform businesses, owning the customer relationship matters more than owning the technology.

The accidental partnership between Netflix and Roku had created the template for streaming's conquest of the living room. Not through vertical integration or walled gardens, but through strategic separation and mutual benefit. Netflix got distribution without the headaches of hardware. Roku got a killer app without the costs of content. And consumers got a simple black box that would transform how they watched television.

The streaming wars were about to begin in earnest. Amazon, Apple, and Google would all launch competing devices. Smart TVs would integrate streaming directly. New services would proliferate. But Roku had established the playbook: be neutral, be simple, be everywhere. It was a strategy that would carry them from startup to IPO to market leader, even as bigger, richer competitors tried to muscle them aside.

V. The First Roku Device & Platform Strategy (2008-2010)

May 20, 2008. The Roku DVP N1000 began shipping to customers who had no idea they were receiving a piece of history. The device was almost aggressively simple—a black plastic puck about the size of a hockey puck, with minimal ports and a remote that had just nine buttons. No fancy interface, no app store, no games. Just Netflix. For $99.99, you could stream unlimited movies and TV shows to your television, assuming you had broadband and a Netflix subscription.

The simplicity was deceptive. Under the hood, It features an NXP PNX8935 video decoder supporting both standard and high definition formats up to 720p; HDMI output; and automatic software updates, including the addition of new channels for other video services. That last feature—automatic updates that could add new services—was the Trojan horse. Customers thought they were buying a Netflix player. They were actually buying a platform.

Wood had learned from the SoundBridge days that exclusive relationships were death sentences in consumer electronics. Within months of launch, Roku was in serious negotiations with every streaming service that existed—which, in 2008, wasn't many. Amazon Video on Demand came first, launching in July 2008. This was crucial: it proved to both consumers and the industry that Roku wasn't just a Netflix box.

In 2009, Roku expanded its offerings beyond Netflix, introducing the Roku Channel Store. This marked a significant shift in Roku's strategy, transforming it from a dedicated Netflix player into a platform for multiple streaming services. The Channel Store allowed users to access various content providers, including Amazon Video On Demand (now Amazon Prime Video), Hulu Plus, and MLB.TV. This move was crucial for Roku's long-term success, as it diversified its content offerings and positioned itself as a neutral platform, attracting more users and content partners.

The Channel Store was revolutionary in its simplicity. Unlike Apple's App Store, which launched around the same time, Roku's channels were free to add. No purchase decisions, no credit cards, just click and watch (assuming you had a subscription with the service). This removed friction at exactly the right point—getting someone to try a new service was hard enough without making them pay for the privilege of access.

But the real genius was in what Roku didn't do. They didn't create their own content. They didn't favor one service over another. They didn't force users into subscriptions or ecosystems. While Apple was trying to sell you movies and Amazon was pushing Prime, Roku just wanted to be the box you turned on. This neutrality would become their moat.

Roku launched two new models in October 2009: the Roku SD (a simplified version of the DVP, with only analog AV outputs); and the Roku HD-XR, an updated version with 802.11n Wi-Fi and a USB port for future functionality. The Roku DVP was retroactively renamed the Roku HD. The product line expansion was strategic—the SD at $59.99 attacked the low end, while the HD-XR at $129.99 offered premium features for early adopters.

The numbers told the story. By the end of 2009, Roku had sold over 400,000 devices. More importantly, usage was exploding. The average Roku user was streaming 3-4 hours per day, far exceeding what anyone had predicted. Wood noticed something crucial: people weren't replacing cable with Roku, they were supplementing it. The device was finding its way into bedrooms, basements, vacation homes—anywhere someone wanted easy access to streaming without dealing with cable boxes or bills.

In August 2010, Roku announced plans to add 1080p video support to the HD-XR. The next month, they released an updated lineup with thinner form factors: a new HD; the XD, with 1080p support; and the XDS, with optical audio, dual-band Wi-Fi, and a USB port. The XD and XDS also included an updated remote.

The 2010 product refresh revealed Roku's platform strategy in full bloom. Each device ran the same software, accessed the same channels, provided the same experience. The only differences were technical capabilities—resolution, connectivity, audio quality. This was the inverse of Apple's strategy, where different devices provided fundamentally different experiences. A Roku was a Roku, whether you paid $60 or $100.

Behind the scenes, Wood was building something more valuable than hardware sales: data. Every click, every search, every minute watched was logged and analyzed. Roku knew what people watched, when they watched it, and crucially, what they searched for but couldn't find. This data became currency in negotiations with content providers. Want to know if your service would succeed on Roku? They had data showing exactly how many people were looking for it.

The platform strategy extended to developers. Roku created a simple SDK and a scripting language called BrightScript. The Roku is an open-platform device with a freely available software development kit that enables anyone to create new channels. The channels are written in a Roku-specific language called BrightScript, a scripting language the company describes as 'unique', but "similar to Visual Basic" and "similar to JavaScript". It wasn't elegant, but it was accessible. A weekend programmer could build a Roku channel. This democratization of development meant that niche content—religious programming, international news, obscure hobbies—could find audiences.

By late 2010, Roku had crossed one million devices sold and supported over 100 channels. Netflix was still the killer app, accounting for over 60% of streaming time, but the ecosystem was diversifying. Hulu Plus had launched, bringing current TV shows. Amazon was getting serious about streaming. Even traditional media companies were dipping their toes in with TV Everywhere apps.

The competition was heating up too. Apple (AAPL), with Apple TV; Google (GOOGL), which has Chromecast and Android TV; and Amazon, with its Fire TV and Fire TV Stick were all entering or expanding in the space. Google TV launched with great fanfare in October 2010, partnering with Sony and Logitech on elaborate, expensive devices. Apple refreshed Apple TV into a small, $99 streaming device. Amazon was rumored to be working on something.

But Roku had advantages that weren't apparent on spec sheets. They had no content to protect, no ecosystem to promote, no broader agenda beyond making streaming simple. When Google TV launched with a complicated remote featuring 80+ buttons, Roku's 9-button simplicity looked prescient. When Apple TV required iTunes and an Apple ID, Roku just worked. The Swiss Army knife strategy was working.

Wood understood something his competitors didn't: in the early days of a platform shift, being neutral is more valuable than being integrated. Consumers didn't want to choose sides in the streaming wars—they wanted access to everything. Roku gave them that, without judgment, without friction, without agenda. It was a positioning that would carry them through the next decade, even as the streaming landscape grew exponentially more complex.

VI. Building the Ecosystem: Smart TVs & Roku OS (2011-2016)

In July 2011, Roku unveiled its second generation of players, branded as Roku 2 HD, XD, and XS. All three models include 802.11n, and also add microSD slots and Bluetooth. The XD and XS support 1080p, and only the XS model includes an Ethernet connector and USB port. But the hardware refresh was just table stakes. The real innovation was happening in software and strategy.

Wood had been watching the television industry carefully. Smart TVs were beginning to emerge, with Samsung, LG, and Sony building their own operating systems. The interfaces were universally terrible—slow, clunky, rarely updated. TV manufacturers were hardware companies trying to be software companies, and it showed. Wood saw opportunity where others saw threat.

The conversation that would transform Roku happened in a nondescript conference room in 2013. Wood was meeting with executives from TCL, a massive Chinese manufacturer that most Americans had never heard of despite making millions of TVs for other brands. TCL had a problem: they wanted to enter the U.S. market under their own brand, but they had no software platform. Building one would cost tens of millions and take years.

Wood's pitch was simple: Why build when you can partner? Roku would provide the entire operating system, the content partnerships, the user experience. TCL would make the TVs. Consumers would get a television with Roku built in—no box required, no additional remote, just turn on your TV and start streaming.

In 2014, Roku partnered with smart TV manufacturers to produce TVs with built-in Roku functionality. The company expanded the reach of its streaming platform by partnering with TV manufacturers as Roku's licensees, to sell Roku's operating system already installed on smart TVs. This allowed Roku's operating system to get pre-installed on smart TVs.

The Roku TV initiative launched at CES 2014 with TCL and Hisense as partners. The industry response was skeptical. Why would anyone want a Roku TV when they could just buy a Roku player? Why would TV manufacturers give up control of their user experience? The questions revealed a fundamental misunderstanding of the market.

Consumers didn't care about TV brands—they cared about content. They didn't want another box, another remote, another cable. They wanted to buy a TV, plug it in, and watch Netflix. Roku TV delivered exactly that. At $229 for a 32-inch model, it was cheaper than buying a dumb TV plus a Roku player. The math was simple, the experience was seamless.

The real innovation was the business model. Roku didn't charge TCL for the operating system. Instead, they shared revenue from advertising and content subscriptions. This aligned incentives perfectly: TCL wanted to sell TVs, Roku wanted active users. Every Roku TV sold was a new customer for Roku's platform business, acquired at zero cost.

In 2015, towards measuring the success of its advertising efforts success, Roku partnered with Nielsen, a company that specializes in advertising effectiveness. In 2016, Roku partnered with Magna, a media firm that specializes advertising, in order to incorporate targeted advertising on its streaming platform. These partnerships weren't just about measurement—they were about legitimizing Roku as an advertising platform comparable to traditional television.

The advertising strategy was sophisticated but hidden from users. Roku knew what you watched across all services. They knew if you started a series on Netflix but didn't finish it. They knew if you searched for a movie but couldn't find it. This data was gold for advertisers who'd been flying blind in the streaming age. Unlike YouTube or Facebook, where ads interrupted content, Roku's ads appeared on the home screen, in search results, as promotional tiles—native to the experience rather than disruptive.

By 2015, Roku had expanded internationally. The company launched its products in Australia, France and Mexico. Each market required different content partnerships, different payment methods, different user expectations. The U.K. launch had happened earlier, in 2012, teaching valuable lessons about international expansion. British users expected BBC iPlayer, catch-up services from ITV and Channel 4, and different sports packages. Roku adapted, but slowly, carefully.

The Roku Channel Store had exploded to over 3,000 channels by 2016. Most were garbage—someone's vacation videos, a looping fireplace, channels that hadn't been updated in years. But hidden in the noise were gems: Pluto TV's free streaming channels, niche international content, educational programming. The long tail strategy meant that everyone could find something, even if that something was weird.

In January 2012, Roku released its dongle-type player, the Streaming Stick, which had evolved significantly by 2016. The latest version was essentially a full Roku player shrunk to the size of a USB stick, powered by the TV's USB port. It was a engineering marvel that competitors struggled to match—Amazon's Fire TV Stick ran hot, Google's Chromecast required a phone to control it. Roku's solution was elegant: a full streaming platform that disappeared behind your TV.

The numbers by 2016 were staggering. Roku had sold over 10 million streaming players. More importantly, Roku TV had captured 8% of the U.S. smart TV market in just two years. Every major TV manufacturer except Samsung and LG had signed on as partners. The platform hosted over 3,500 channels. Active accounts had grown to 13 million, streaming billions of hours annually.

But the most important metric was one Wall Street didn't yet understand: platform revenue. In 2016, Roku generated $77 million from platform services—advertising, revenue shares, content distribution fees. This was pure margin business, scaling infinitely with no additional hardware costs. Player revenue was $232 million, but at gross margins below 10%. The future was clear: hardware was the customer acquisition cost, platform was the business.

Wood had pulled off something remarkable. While Apple, Amazon, and Google were fighting over who could build the best streaming box, Roku had made the box irrelevant. They were inside the TV. They were the TV. The operating system for television that Wood had envisioned back in 2002 was becoming reality.

The streaming wars were intensifying. Netflix was spending billions on original content. Amazon was bundling video with Prime. New services were launching monthly. But Roku remained Switzerland—neutral, welcoming, profitable from everyone else's competition. As 2016 ended, Wood was preparing for the next phase: taking Roku public. The platform was built, the model was proven, the growth was undeniable. It was time to show Wall Street that the future of television wasn't about content or hardware—it was about being the platform where everything else happened.

VII. IPO & The Platform Business Model (2017-2019)

Connected-TV platform company Roku went public on Sept. 28, 2017, and the initial public offering (IPO) priced at $14 per share. However, most investors couldn't get that price. Roku stock opened its first day of trading at $15.78 and closed out the day at $23.50 per share. Roku jumped up 67% on its first day of trading, making it the top first-day climber of 2017 for a U.S.-listed tech company with an IPO bigger than $50 million.

The roadshow had been brutal. Wood and CFO Steve Louden spent weeks explaining to skeptical investors why a hardware company with negative gross margins on its primary product was actually a high-margin advertising and platform business. The S-1 filing revealed the truth of Roku's business model for the first time: "We currently generate a majority of our revenue from sales of our streaming players", but the real story was in the details.

Platform revenue in 2017 was $225 million, growing at 115% year-over-year. Player revenue was $187 million, growing at just 18%. More tellingly, gross margin on hardware was 10%, while platform gross margin was 76%. Every dollar of platform revenue was worth seven dollars of hardware revenue in terms of actual profit. The market was beginning to understand: Roku wasn't selling boxes, they were acquiring customers.

Wood — a former Netflix executive who played a role in the invention of the DVR — will own 27.3 percent of Roku's stock, and will control approximately 32.1percent of the voting power. The dual-class structure gave Wood control even as the company went public, allowing him to pursue long-term strategy without worrying about quarterly earnings pressure.

The timing of the IPO was perfect and terrible simultaneously. Perfect because streaming was at an inflection point—Netflix had 100 million subscribers, cord-cutting was accelerating, every media company was planning a streaming service. Terrible because Amazon had just announced they were selling Fire TV sticks at a loss, Google was giving away Chromecasts, and Apple was rumored to be investing $1 billion in original content.

But Wood had data his competitors didn't. Roku users were streaming 14.8 billion hours annually. The average account watched 3.5 hours per day. More importantly, 45% of Roku users had cut the cord entirely—they were streaming-only households. This wasn't a side business or a hobby; for millions of Americans, Roku was television.

The platform business model was elegant in its simplicity. Content publishers paid Roku to distribute their subscription services, typically giving Roku 20% of subscription revenue for customers acquired through the platform. Advertisers paid for targeted ads on the home screen, within content, and in search results. Roku sold buttons on remotes—Netflix, Hulu, Amazon, and others paid millions for dedicated buttons that launched their services instantly.

In 2018, Roku did something that seemed crazy: they launched their own channel. The Roku Channel wasn't another Netflix competitor—it was free, ad-supported, and filled with older movies and TV shows licensed from studios. The content was unremarkable, but the strategy was brilliant. The Roku Channel generated high-margin advertising revenue while giving Roku first-party data on viewing habits. It also gave them leverage in negotiations—if Netflix got too demanding, Roku had their own content to promote.

According to Forbes, Roku had 41% of market share in 2018. Despite competing against companies with market capitalizations 10-100x larger, Roku was winning. The reason was focus. While Amazon used Fire TV to sell Prime subscriptions and Apple used Apple TV to lock users into their ecosystem, Roku just wanted to be the best streaming platform. No agenda, no ulterior motive, just streaming.

The numbers accelerated through 2018 and 2019. Active accounts grew from 19 million to 27 million to 36 million. Streaming hours exploded from 14.8 billion to 24 billion to 40 billion. Platform revenue surged from $225 million to $417 million to $740 million. The hockey stick growth that venture capitalists dream about was happening at scale, in public markets.

Wall Street's reaction was schizophrenic. The stock would surge on earnings beats, crash on Amazon rumors, recover on user growth, plummet on gross margin concerns. It traded between $26 and $176 through 2018-2019, a volatility that reflected fundamental confusion about what Roku really was. Hardware company? Platform? Advertising business? The answer was all three, but the proportions were shifting rapidly toward high-margin platform revenue.

The competitive landscape was brutal. Amazon was essentially giving away Fire TV devices, bundling them with Prime Day deals, even building them into some TVs for free. Google had pivoted from the failed Google TV to Chromecast to Android TV, spending billions without gaining traction. Apple had finally gotten serious about services with Apple TV+, investing in prestige content from Steven Spielberg and Oprah.

But Roku had structural advantages that weren't replicable. They had no conflicts of interest—they made money when any service succeeded, not just their own. They had the best data—seeing across all services gave them insights no single content provider could match. They had scale—with 30% of all U.S. streaming happening on Roku devices, they were too big for any service to ignore.

The masterstroke came in 2019 with the launch of Roku's demand-side platform, OneView. This allowed advertisers to buy ads across all of Roku's inventory—The Roku Channel, the home screen, within other apps—with the same targeting and measurement they expected from digital advertising. It was the holy grail of TV advertising: the reach of traditional TV with the precision of digital.

By the end of 2019, the transformation was complete. Platform revenue had exceeded player revenue for the first time. Gross profit from platform was 5x higher than from players. Average revenue per user had reached $23.14 annually and was growing 20% year-over-year. The company was still losing money—barely—but that was by choice, investing aggressively in content and international expansion.

In July 2019 Roku started moving to a new headquarters in San Jose, with plans to vacate offices subleased from Netflix. The symbolic value was perfect—Roku was no longer Netflix's child but a full-fledged platform company in its own right. The student had become the master, or at least a peer.

As 2019 ended, storm clouds were gathering. Every major media company was launching a streaming service. Disney+ was coming. HBO Max, Peacock, Paramount+—the fragmentation of content was accelerating. Some observers wondered if Roku's neutral platform would matter when every content owner wanted direct relationships with consumers.

Wood wasn't worried. Fragmentation was Roku's friend—the more services, the more consumers needed aggregation. The more passwords to remember, the more valuable single sign-on became. The more content scattered across platforms, the more important universal search became. Roku wasn't threatened by the streaming wars; they were the arms dealer profiting from every battle.

The stock ended 2019 at $134, up 400% from its IPO price just two years earlier. Market capitalization had reached $17 billion, more than ViacomCBS, close to Netflix's valuation when they'd spun off Project Griffin. The hardware startup that nobody wanted to fund had become one of the most valuable media technology companies in the world.

VIII. The Streaming Wars & Pandemic Boom (2019-2021)

November 12, 2019. Disney+ launched with 10 million subscribers on day one, crashing servers and exceeding even the most optimistic projections. The streaming wars that everyone had predicted were finally here. Within six months, HBO Max, Peacock, and Apple TV+ would all launch. The battlefield was set: every major media company versus Netflix, with consumers caught in the crossfire.

For Roku, this was Christmas morning.

In the end, the winner of that war ended up being Roku — the popular creator of streaming devices that somehow managed to remain neutral throughout it all and offer the only option for streaming content from all of the available video services. Wood had positioned the company perfectly. While media giants fought over exclusive content and subscription dollars, Roku provided the battlefield. Every new service needed distribution. Every new service needed marketing. Every new service needed Roku.

The numbers were staggering. Disney+ launched on Roku day one. HBO Max initially refused, demanding better terms, but capitulated within six months when they realized they were missing 40% of the streaming market. Peacock gave Roku customers extended free trials. Even Apple, notorious for its walled garden approach, made Apple TV+ available on Roku within months of launch.

Then March 2020 happened.

The COVID-19 pandemic transformed streaming from entertainment option to essential utility overnight. Movie theaters closed. Sports canceled. Offices emptied. Suddenly, 300 million Americans were stuck at home with nothing to do but watch television. And they did—obsessively, continuously, in volumes that broke every model and projection.

Roku's daily active users spiked 50% in two weeks. Streaming hours, which had been growing at 60% annually, started growing at 60% quarterly. The Roku Channel, which had been a modest success, suddenly became a top-10 streaming service as consumers devoured free content. Media device sales jumped 35% during the second quarter of 2020 alone, while the number of active Roku accounts improved 41% to 43.0 million.

But the real explosion was in platform revenue. With everyone watching everything all the time, advertising inventory that had been worth $20 CPMs was suddenly worth $40. Subscription sign-ups through Roku tripled. Content publishers who'd been hesitant about revenue sharing were desperate for distribution. Roku's platform revenue grew 76% year-over-year in Q2 2020, the fastest growth since going public.

The stock market lost its mind. Roku stock, which had started 2020 at $134, hit $200 by May, $250 by August, $350 by November. By February 2021, it was trading above $460. The all-time high Roku stock closing price was $479.50 on July 26, 2021, giving the company a market capitalization of $65 billion—more than ViacomCBS and Discovery combined, approaching half of Netflix's value.

At the height of the pandemic, its revenue had soared 548% since its late-2017 IPO, driving its stock up 1,940%. The mathematics of the bull case were intoxicating. If Roku could maintain 40 million active accounts spending $30 annually on platform revenue, that was $1.2 billion in nearly pure-margin revenue. If they could reach 100 million accounts—still just a third of U.S. households—at $50 ARPU, that was $5 billion. The TAM was enormous, the margins were beautiful, the growth was hyperbolic.

Wall Street analysts competed to raise price targets. $500 became $600 became $750. One particularly enthusiastic analyst suggested Roku could be worth $1,000 per share by 2025, implying a $140 billion valuation. The logic was seductive: streaming was the future, Roku owned streaming distribution, therefore Roku would own the future.

But there were warning signs for those willing to see them.

Customer acquisition costs were skyrocketing. With everyone stuck at home, Roku players were sold out everywhere. Instead of raising prices to match demand, Roku held prices steady and even subsidized some models, selling them below cost to grab market share. The strategy made sense long-term—every customer would generate platform revenue for years—but it destroyed hardware margins in the short term.

Competition was intensifying in unexpected ways. Smart TV manufacturers like Samsung and LG, who'd initially dismissed Roku TV as low-end, were suddenly investing billions in their own operating systems. Google paid TCL and Hisense—Roku's primary TV partners—massive guarantees to also offer Google TV models. Amazon was practically giving away Fire TV devices, bundling them with Ring doorbells, Echo speakers, anything to gain share.

The content landscape was fragmenting faster than anyone anticipated. By mid-2021, there were over 300 streaming services in the U.S. Consumers were overwhelmed, confused, angry about password requirements and subscription costs. "Subscription fatigue" became a real phenomenon. The average household had gone from 2 streaming services to 7, spending more on streaming than they'd ever spent on cable.

Roku tried to be the solution. They launched universal search that showed where content was available and at what price. They introduced subscription management tools. The Roku Channel expanded aggressively, licensing content that was disappearing from other services as everyone hoarded their libraries. They even experimented with producing original content, buying shows that had been canceled elsewhere.

The international expansion accelerated. Roku launched in Brazil, the largest media market in Latin America. They expanded across Europe, though progress was slow—each country had different content expectations, different payment methods, different regulations. The U.K. was a modest success, but France and Germany proved challenging. International streaming was not the land-grab that U.S. streaming had been.

By mid-2021, the pandemic boom was showing cracks. Vaccination rates were rising. Offices were reopening. Movie theaters were coming back. The extraordinary consumption patterns of 2020 were normalizing, but year-over-year comparisons looked terrible. How do you show growth when last year's quarter included the entire world locked inside?

The earnings call for Q2 2021 was a masterclass in managing expectations. Wood talked about "normalizing viewing patterns" and "returning to seasonal patterns" and "lapping difficult comparisons." The numbers were still good—revenue grew 81% year-over-year—but the sequential growth had stalled. New account additions slowed. Viewing hours per account actually declined for the first time ever.

The market's reaction was swift and brutal. Roku stock fell 8% the day after earnings. Then another 5% the next week. By September, it was down 20% from its peak. The narrative was shifting: maybe Roku was a pandemic beneficiary, not a secular growth story. Maybe streaming wasn't replacing linear TV but complementing it. Maybe the TAM wasn't as big as everyone thought.

But the real problems were just beginning. Inflation was rising. The Federal Reserve was talking about raising interest rates. Growth stocks across the board were getting hammered. And Roku, trading at 15x revenue with no profits in sight, was the poster child for pandemic excess.

As 2021 ended, Roku stock was at $230, down 50% from its peak but still up 70% for the year. The company had 60 million active accounts, was streaming 70 billion hours annually, and generating $2.7 billion in revenue. By any normal measure, it was a massive success. But the market doesn't care about normal measures during bubble deflations.

The streaming wars had created a king, crowned it with a $65 billion valuation, and was about to tear it all down. The question wasn't whether Roku would survive—the business was too strong for that—but whether investors who bought at $490 would ever see that price again.

IX. The Crash & Reality Check (2021-2023)

The unraveling began slowly, then all at once.

January 2022. The Federal Reserve confirmed what markets feared: interest rates were going up, and fast. Growth stocks started selling off immediately. Roku, still unprofitable despite billions in revenue, was among the first casualties. The stock fell from $230 to $190 in two weeks. This was just the appetizer.

February 18, 2022. Roku reported Q4 2021 earnings. Revenue grew 33% year-over-year to $865 million—by any historical standard, phenomenal growth. But the guidance was catastrophic. First quarter 2022 revenue would grow just 25%, the slowest rate in company history. Worse, Roku would lose money—a lot of money—as they continued investing in content and international expansion despite slowing growth.

The stock cratered 22% in after-hours trading, opening the next day at $130. In six months, Roku had lost $40 billion in market value. The shares would go on to pull back dramatically from their pandemic peak. The story was shifting from growth at any cost to "where are the profits?"

But the real shock came in April 2022. Netflix, the company that had given Roku life, reported its first subscriber loss in a decade. The streaming giant's stock fell 35% in a single day. If Netflix was struggling, what hope did anyone else have? The entire streaming sector collapsed. Disney fell 50%. Warner Bros Discovery fell 70%. And Roku, dependent on all of them, fell furthest.

As a result, the stock has plunged 90% from its peak. The 91% drop-off in Roku's share price is one of the worst performances of any large-cap stock during 2022's tyrannical bear market. By July 2022, Roku was trading at $65, below its price from 2019, erasing three years of gains in three months.

The business challenges were real and mounting. In the third quarter of this year, platform revenue only grew 15% year over year to $670 million. In the same quarter last year, platform revenue grew 82%. The pandemic comparisons were impossible—how do you show growth against a quarter when the entire world was locked inside watching Tiger King?

More concerning was the advertising market. As the economy slowed and recession fears mounted, advertising spending collapsed. Connected TV advertising, which had been growing 100% annually, slowed to 20%. Traditional advertisers pulled back budgets. Direct-to-consumer brands, which had fueled much of Roku's growth, disappeared entirely as venture capital dried up. CPMs that had reached $40 during the pandemic fell back to $15.

Wood made a crucial decision: hold the line on hardware pricing. Roku chose to subsidize the cost of its namesake streaming devices -- rather than raise prices -- even as inflation and supply chain disruptions sent costs skyrocketing. Components that cost $30 in 2020 cost $50 in 2022. Shipping from China tripled. But Roku kept selling their basic streamer for $29.99, accepting negative 20% gross margins on hardware to keep acquiring customers.

The strategy was financially brutal but strategically sound. Amazon and Google, seeing Roku's weakness, tried to steal market share by also subsidizing hardware. But they didn't have Roku's platform monetization engine. Every customer Amazon acquired for Fire TV was a money-loser unless they bought Prime. Every Chromecast Google sold was a loss leader for YouTube. Only Roku had built a true platform business model where hardware losses were customer acquisition costs.

The layoffs started in March 2022. First, 200 employees, about 9% of the workforce. Then another 200 in November. The cuts were primarily in content and international expansion—growth initiatives that suddenly looked like luxuries. The Roku Channel's original content ambitions were scaled back. International expansion beyond English-speaking markets was paused. The company that had been hiring 50 people per month was suddenly in survival mode.

But there were bright spots hidden in the carnage. Despite the economic headwinds, people kept streaming. Active accounts grew to 70 million by the end of 2022. Streaming hours reached 95 billion annually. The Roku Channel became a top-5 streaming service by viewing hours, ahead of Paramount+ and Peacock. The platform was working, even if the stock wasn't.

The smart TV strategy was particularly successful. Data from ComScore indicates that Roku controls an industry-leading 37% of the United States over-the-top (non-cable) connected-television advertising market. Roku TVs represented 40% of all smart TVs sold in the U.S. during 2022. Every TV was a seven-year customer relationship, generating platform revenue long after the initial sale.

In January 2023, Roku made a surprising move: they acquired Quibi's content library for less than $100 million. Quibi, Jeffrey Katzenberg's billion-dollar mobile streaming disaster, had produced premium content with Hollywood stars that almost nobody had watched. Roku rebranded it as "Roku Originals," giving The Roku Channel exclusive premium content at a fraction of the production cost.

The stock found a bottom around $40 in December 2022, down 92% from its peak. At that price, Roku was valued at just $5 billion, less than 2x revenue. For comparison, Netflix traded at 4x revenue, Disney at 3x. The market was pricing Roku like a dying retailer, not a growing platform business.

The turnaround began slowly. Q1 2023 earnings showed platform revenue reaccelerating. Advertising CPMs stabilized. The company reached EBITDA profitability for the first time. The stock doubled from its lows, reaching $80 by May 2023. But this was still 85% below the peak—investors who bought during the pandemic frenzy were still underwater by huge margins.

Wood's tone on earnings calls shifted from growth evangelist to pragmatic operator. He talked about "operational efficiency" and "path to profitability" and "disciplined investment." The company that had spent lavishly on content and international expansion was now focused on extracting maximum value from its existing user base. ARPU became the key metric, not user growth.

At the end of the third quarter of 2017, it had 16.7 million active accounts. By the end of the same quarter last year, it had 65.4 million. And last month, it announced that it surpassed 70 million accounts around the new year -- the most new accounts it's added during a quarter in two years.

The crash had revealed uncomfortable truths about Roku's business model. Platform revenue was more cyclical than expected, tied closely to advertising markets. International expansion was harder and more expensive than anticipated. Competition from deep-pocketed tech giants wasn't going away. The neutral Switzerland strategy worked, but it meant Roku captured less value than vertically integrated competitors.

But it also revealed strengths. Roku had survived a 90% drawdown without running out of cash, cutting costs dramatically while maintaining growth. They'd held onto market share despite Amazon and Google's aggressive subsidies. Most importantly, they'd proven that the platform business model worked even in the worst advertising environment in a decade.

As 2023 progressed, the narrative shifted again. Maybe Roku wasn't the next Netflix, worth $500 per share. But maybe it wasn't worthless either. Maybe it was what Wood had always said: the operating system for television, valuable but not revolutionary, profitable but not exponential. Maybe, after all the hype and crash, Roku was just a good business at a fair price.

The stock ended 2023 around $90, up 125% from the lows but still down 80% from the peak. The company was generating $3.5 billion in revenue, had 80 million active accounts, and was approaching sustained profitability. The pandemic boom and bust was over. The real business of building the streaming platform could finally begin.

X. The Modern Roku: Platform Dominance & Future Challenges (2023-Present)

According to Roku's Q4 2023 report, the platform surpassed 80 million active accounts, with users clocking over 100 billion streaming hours throughout the year. By late 2024, the active user count rose from 70 million at the end of 2022 to 80 million a year later and 90 million in Q4 2024. The company that nearly died in the 2022 crash had emerged leaner, more focused, and surprisingly dominant.

The numbers tell a remarkable story of resilience. Data from ComScore indicates that Roku controls an industry-leading 37% of the United States over-the-top (non-cable) connected-television advertising market. In a similar vein, media market research outfit Parks Associates reports that Roku accounts for 43% of the country's actively used media-playing devices, topping Amazon's comparable FireTV tech. Despite everything—the stock crash, the layoffs, the competition from trillion-dollar companies—Roku had maintained its position as streaming's Switzerland.

The Roku Channel had evolved from afterthought to centerpiece. By 2024, it was reaching 120 million people monthly, making it one of the largest ad-supported streaming services in America. The content strategy had shifted from expensive originals to shrewd acquisitions and licensing deals. Old seasons of "Top Chef," British crime dramas, Canadian sitcoms—content that was gathering dust in studio vaults found new life and new audiences on The Roku Channel.

The masterstroke was FAST channels—Free Ad-Supported Streaming Television. These were linear channels that streamed 24/7, just like cable, but free and themed. There was a channel that only showed Gordon Ramsay shows. A channel of nothing but true crime. A channel of classic game shows. For viewers overwhelmed by choice, FAST channels offered the comfort of traditional TV with the convenience of streaming. Roku operated over 400 FAST channels by 2024, more than any competitor.

The advertising business had matured remarkably. OneView, Roku's demand-side platform, was processing billions of ad impressions monthly. The company could tell advertisers not just who watched their ads, but what they did afterward. Did they search for the product? Did they visit the brand's channel? Did they actually buy something? This closed-loop attribution was the holy grail of television advertising, something traditional TV could never offer.

Shoppable ads became the next frontier. Viewers watching a cooking show could buy the featured cookware with their remote. Car commercials could schedule test drives. Movie trailers could sell tickets. Roku was transforming from a media platform into a commerce platform, taking a cut of every transaction. The remote control was becoming a credit card.

International expansion remained challenging but was finally showing progress. Roku had learned that each market was unique—what worked in the U.S. failed in Europe, what worked in Europe failed in Latin America. The strategy shifted from aggressive expansion to selective partnership. In Mexico, they partnered with TV Azteca. In Germany, with local broadcasters. Instead of conquering the world, Roku was building bridges.

The smart TV strategy had exceeded all expectations. By 2024, one in three smart TVs sold in America was a Roku TV. The partners had expanded from budget brands like TCL and Hisense to include Sharp, Philips, and JVC. Even premium brands were considering Roku OS. The economics were irresistible—TV manufacturers got a world-class operating system for free, Roku got a customer relationship that lasted the life of the TV.

But new challenges emerged. Smart TV manufacturers, seeing Roku's platform revenue, wanted a bigger cut. Samsung and LG, which had their own operating systems, were investing heavily to compete. Google was paying massive guarantees—reportedly $1 billion over three years—to get Android TV on more devices. The TV OS wars were intensifying, and Roku's neutral Switzerland position was under pressure.

The competition from tech giants had evolved from brute force to strategic precision. Amazon wasn't just subsidizing Fire TV devices; they were integrating them into their entire ecosystem. Buy a Ring doorbell, get a free Fire TV stick. Subscribe to Prime, get Paramount+ free. Order from Whole Foods, get a discount on Fire TV. The bundle was back, just distributed differently.

Apple had taken a different approach entirely. Instead of competing on price or scale, they'd gone premium. Apple TV+ produced prestige content that won Emmys and Oscars. The Apple TV 4K was the best streaming device money could buy. They didn't need to win the market; they just needed to own the high end, where the profits lived.

Google's strategy was the most concerning. They weren't trying to beat Roku at streaming devices—they were trying to obsolete them. YouTube TV was becoming a full cable replacement. YouTube itself was the most-watched "streaming service" on every platform, including Roku. Google was playing a longer game: why fight for the operating system when you could be the content that everyone watched regardless of platform?

Wood's response was pragmatic. Roku couldn't outspend the tech giants, so they out-focused them. While competitors juggled multiple priorities—Amazon had e-commerce, Apple had phones, Google had search—Roku just had streaming. Every employee, every dollar, every decision was optimized for one thing: being the best streaming platform.

The financial model had finally matured into sustainability. Platform revenue reached $3 billion annually, with gross margins above 55%. Hardware losses had stabilized at acceptable levels—think of it as customer acquisition cost, not retail loss. The company achieved its first full year of positive free cash flow in 2024, silencing critics who said Roku would never be profitable.

Roku has now moved lower the day after posting financial results in four of the last five quarters. It happened last time out, even with Roku beating expectations on both ends of the income statement, raising its guidance, and delivering its first quarterly profit in more than three years. The market remained skeptical, traumatized by the pandemic boom and bust.

Looking forward, the challenges are clear. The streaming market is consolidating—Discovery merged with WarnerMedia, Amazon bought MGM, Disney was rumored to be shopping for acquisitions. Fewer players meant less competition for Roku to monetize. The advertising market, while recovered, was fundamentally changed. Privacy regulations, cookie deprecation, and Apple's App Tracking Transparency had made targeted advertising harder and more expensive.

The opportunities are equally clear. Connected TV advertising is still in its infancy—only 30% of TV ad dollars have shifted to streaming, leaving $50 billion still in linear TV. International markets remain largely untapped. New technologies like generative AI could transform content discovery and personalization. And despite all the competition, no one has solved the fundamental problem that Roku addresses: how to simply and neutrally aggregate all of streaming in one place.

As 2025 begins, Roku stands at an interesting inflection point. The stock trades around $95, recovered from the depths but nowhere near the peaks. The company is profitable, growing steadily if not spectacularly, and remains the market leader in its core market. It's not the rocket ship that investors wanted in 2021, but it's not the disaster they feared in 2022 either.

Wood, now approaching 60, remains CEO and controlling shareholder. In interviews, he sounds less like the visionary founder and more like the pragmatic operator—talking about margins and efficiency rather than revolution and disruption. Perhaps that's appropriate. The revolution already happened. Streaming won. Roku won. Now comes the harder work of building a sustainable, profitable business in a mature market.

The Switzerland strategy endures, evolved but unchanged in principle. In a world where every media company wants to own the customer relationship, where every tech giant wants to control the platform, where every advertiser wants perfect attribution, Roku remains the neutral ground where they all meet. It's less exciting than being Netflix or Apple, but it might be more durable.

The next chapter of Roku's story won't be written in stock prices or user growth. It will be written in the mundane but crucial details of platform economics: ARPU expansion, margin improvement, international penetration, advertising innovation. The company that began as Anthony Wood's sixth startup, that survived the DVR wars and the streaming wars and the pandemic bust, faces its next test: proving that being the arms dealer in the content wars is not just viable, but valuable, not just sustainable, but essential.

The streaming future that Wood envisioned in 2002 has arrived. The question now is whether Roku can remain its Switzerland, or whether the forces of consolidation, competition, and commoditization will finally breach its neutrality. The answer will determine whether Roku becomes the next great media platform or merely a footnote in the history of how television transformed from broadcast to broadband.

XI. Playbook: Business & Investing Lessons

The Power of Platform Neutrality in Winner-Take-All Markets

Roku's greatest strategic insight was recognizing that in platform wars, Switzerland often wins. While Amazon leveraged Fire TV to sell Prime memberships, Apple used Apple TV to lock users into iOS, and Google pushed YouTube through Chromecast, Roku just wanted to stream everything. This neutrality seemed like weakness—no ecosystem lock-in, no exclusive content, no bundled services. But it became their moat.

Content providers trusted Roku because they weren't competitive. Users chose Roku because it had everything. Advertisers preferred Roku because they could reach audiences across all services. The lesson: in markets where giants fight, being the neutral ground where they all must compete can be more valuable than picking a side. Wood understood what Peter Thiel preaches: competition is for losers, but being the platform where competitors must play is for winners.

Hardware as a Customer Acquisition Tool, Not Profit Center

Traditional business logic says selling products at a loss is unsustainable. Roku proved otherwise by reconceptualizing hardware not as a product but as a customer acquisition cost. A Roku device sold at a $20 loss that generates $25 annually in platform revenue for seven years is actually a brilliant investment—a 625% return. This mental model shift—from product company to platform company—enabled decisions that seemed irrational but were actually optimal.

The key insight: in platform businesses, the initial transaction is just the beginning of the relationship. Amazon learned this with Kindle, selling e-readers at a loss to sell ebooks at a profit. Gaming consoles have operated this way for decades. But Roku perfected it in streaming, understanding that the real value wasn't in the box but in the viewing hours it enabled.

Why Timing Matters More Than Being First

ReplayTV was superior to TiVo—better features, cleaner interface, more innovative technology. It didn't matter. ReplayTV was too early, too aggressive, too threatening to existing players. They won the technology battle but lost the business war. Roku succeeded where ReplayTV failed not by being first or best, but by having better timing.

The lesson crystallizes around market readiness. In 2000, broadband penetration was under 5%. By 2008, it was over 60%. In 2000, streaming video was technically impossible for most Americans. By 2008, YouTube had proven consumer demand. Wood's genius wasn't inventing streaming devices—it was waiting until the infrastructure, consumer behavior, and content availability aligned. As Bill Gates noted, we overestimate change in two years and underestimate it in ten. Wood waited eight years between ReplayTV and Roku's streaming pivot. Perfect timing.

The Importance of Founder-Led Companies in Navigating Pivots

Roku survived multiple near-death experiences: the Netflix spinoff, the 2008 financial crisis, the streaming wars, the pandemic bust. Each required fundamental strategic pivots that would have paralyzed a traditional management team. But Wood, as founder-CEO with controlling voting rights, could make bold decisions quickly without committee approval or quarterly earnings pressure.

Consider the decision to hold hardware prices during the pandemic shortage. Any professional CEO would have raised prices to maintain margins—it's what business school teaches. Wood did the opposite, accepting brutal losses to gain market share, knowing that each customer would generate platform revenue for years. Only a founder with complete control and long-term vision could make that call.

Building a Two-Sided Marketplace: Viewers and Advertisers

Roku's platform is actually two interconnected businesses. On one side, consumers who want simple, aggregated streaming. On the other, advertisers who want targeted, measurable TV advertising. Each side makes the other more valuable—more viewers attract more advertisers, more ad revenue enables cheaper hardware, cheaper hardware attracts more viewers. It's a flywheel that, once spinning, is nearly impossible to stop.

The critical insight was recognizing that viewers and advertisers weren't in conflict but in symbiosis. Free, ad-supported content gave viewers options beyond expensive subscriptions. Targeted advertising meant viewers saw relevant ads rather than repetitive car commercials. By aligning incentives rather than maximizing extraction from either side, Roku built a platform that both sides actually wanted to use.

When to Hold Prices vs. When to Monetize

During the pandemic, Roku faced a choice. Demand was infinite, supply was constrained, they could have charged $100 for devices that cost $30 to make. Instead, they held prices and even subsidized some models, selling them below cost. The decision seemed insane—they were literally losing money to sell products that customers desperately wanted to buy.

But Wood understood something crucial: market share in platform businesses is nearly impossible to reclaim once lost. Every customer who bought a Fire TV or Chromecast because Roku was too expensive was potentially lost for 5-7 years (the replacement cycle for streaming devices). Better to lose $20 today to gain a customer worth $200 over their lifetime. The lesson: in platform businesses, market share is more valuable than short-term profits, but only if you have a monetization engine that makes those customers valuable eventually.

The Value of Being the Arms Dealer in Platform Wars

The streaming wars created hundreds of casualties. Quibi burned through $2 billion. CNN+ lasted three weeks. Even successful services like Disney+ are losing billions annually. But Roku, which created no content and owned no libraries, has been profitable. Why? Because selling weapons to all sides in a war is more profitable than fighting in it.

This is the Microsoft strategy from the PC wars—let Dell and Compaq fight while collecting Windows licenses from both. It's the Google strategy from mobile—let Samsung and others compete while collecting Android advertising revenue. Roku applied this to streaming: let Netflix, Disney, and Warner fight while collecting platform fees from everyone. The lesson: in technology platform wars, owning the distribution often beats owning the content.

The metalesson that connects all these insights: Roku succeeded not by being the best at any one thing but by understanding the game theory of platform businesses better than anyone else. They recognized that in multi-sided markets with network effects, strategic positioning matters more than tactical execution. Being neutral beat being integrated. Being open beat being exclusive. Being patient beat being first.

For investors, Roku's journey offers sobering lessons about valuation and timing. The company that was worth $65 billion at the peak was arguably overvalued, pricing in perfection that reality couldn't deliver. The same company at $5 billion at the trough was arguably undervalued, pricing in disaster that never materialized. The truth, as often happens, lies somewhere in between. Roku is neither the next Netflix nor the next Blockbuster, but something more interesting: a profitable platform business in a growing market with sustainable competitive advantages and rational competition.

XII. Analysis & Bear vs. Bull Case

Bull Case: The Streaming Platform Monopoly

The optimistic view starts with market position. Roku controls an industry-leading 37% of the United States over-the-top connected-television advertising market and 43% of the country's actively used media-playing devices. In business, market leadership often becomes self-reinforcing. Developers build for the largest platform first. Advertisers spend where the audiences are. Content providers negotiate with the market leader most favorably. Roku's dominance creates a network effect that compounds annually.

The secular shift to streaming remains early globally. While U.S. households have largely cut the cord, international markets lag by 5-10 years. Europe, Latin America, and Asia represent billions of potential users who are just beginning their streaming journey. Roku doesn't need to dominate internationally—capturing even 10% of international streaming would double their addressable market. The company that won the U.S. market has the playbook, technology, and relationships to expand globally.

The advertising opportunity is most compelling. Television advertising is a $70 billion annual market in the U.S. alone, with only 30% shifted to streaming. As linear TV viewership inevitably declines—down 10% annually for the past five years—those advertising dollars must go somewhere. Roku, with the largest reach and best attribution data, is positioned to capture a disproportionate share. If TV advertising follows digital advertising's evolution, the platforms that enable targeting and measurement will capture most of the value.

Platform-agnostic approach creates a sustainable moat. Unlike competitors who push their own services (Amazon with Prime, Apple with Apple TV+), Roku benefits when any service succeeds. This neutrality becomes more valuable as the streaming market fragments. Consumers facing 10+ streaming services need aggregation more than ever. Roku's universal search, single sign-on, and content discovery tools become essential infrastructure as complexity increases.

The financial model has finally proven sustainable. Platform gross margins above 55% and growing. Free cash flow positive with improving trends. A business model where customer acquisition costs are front-loaded but lifetime value extends 5-7 years. Once Roku achieves steady-state economics—stable market share, normalized content costs, mature advertising operations—the business could generate 20-30% EBITDA margins on $10+ billion in revenue. That's a $2-3 billion annual profit stream from the current base alone, before any growth.

Bear Case: The Commoditization Trap

The pessimistic view starts with competitive dynamics. Smart TV manufacturers are cutting out the middleman. Samsung's Tizen OS and LG's webOS are improving rapidly. Why would TV manufacturers give Roku 30% of advertising revenue when they could keep 100%? As smart TVs become commoditized, manufacturers will seek differentiation through proprietary software. Roku TV could lose its partners just as Android phone manufacturers increasingly fork Android or build alternatives.

International expansion is proving more difficult than anticipated. Each market requires different content partnerships, payment methods, and user experiences. Unlike Netflix, which can amortize content globally, Roku must essentially rebuild its platform country by country. The costs are enormous, the timeframes are long, and local competitors have significant advantages. Roku might remain a U.S.-only success story.

The advertising market is structurally cyclical. When recessions hit, advertising spending falls first and fastest. Roku's 2022 experience—platform revenue growth slowing from 82% to 15%—reveals uncomfortable dependency on macro conditions. Unlike subscription businesses with predictable revenue, advertising platforms face volatile earnings that markets punish with lower multiples. Roku might be valued more like a traditional media company (10x earnings) than a technology platform (30x earnings).

Competition from tech giants could eventually overwhelm Roku through sheer resource advantage. Amazon can afford to lose billions on Fire TV indefinitely—it's a rounding error against AWS profits. Google treats YouTube as a loss leader for advertising data. Apple considers Apple TV a hobby that enhances the iOS ecosystem. These companies can subsidize hardware, pay for exclusive content, and operate at losses that would bankrupt Roku. The neutral Switzerland strategy works until the superpowers decide Switzerland shouldn't exist.

The fundamental question about Roku's value remains unresolved: is it essential infrastructure or convenient middleware? If streaming services develop their own apps for every platform, if smart TVs improve their interfaces, if aggregation becomes less necessary as consumers settle on 2-3 services, then Roku becomes optional rather than essential. The platform that seemed indispensable during streaming's fragmentation might become irrelevant during streaming's consolidation.