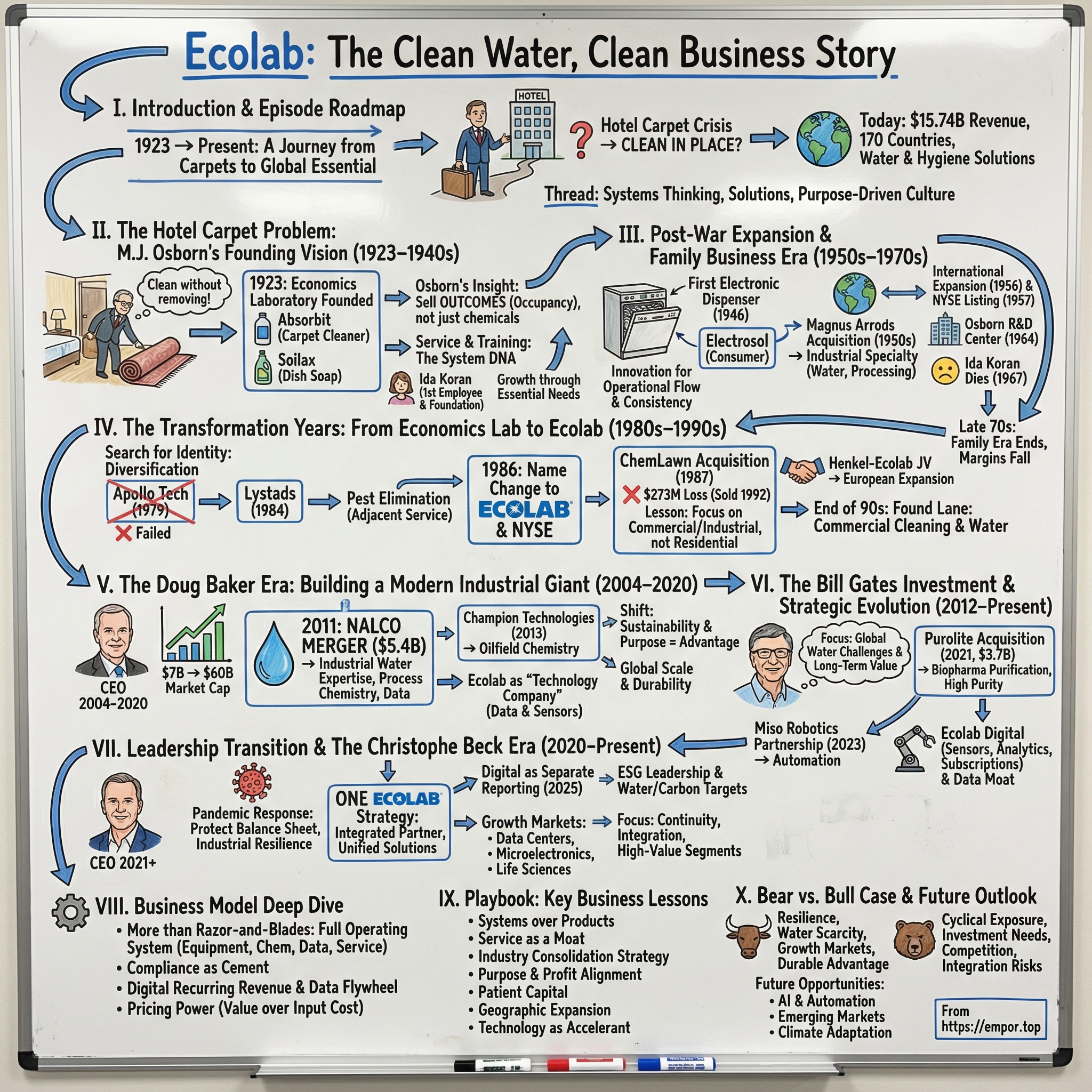

Ecolab: The Clean Water, Clean Business Story

I. Introduction & Episode Roadmap

Picture this: A traveling salesman in 1923, trudging through hotel lobbies across the Midwest, watches as yet another carpet gets rolled up and sent out for cleaning. The room will be closed for a week, maybe more. Revenue lost. Guests turned away. He thinks, "There has to be a better way." That salesman was M.J. Osborn, and his frustration would birth one of the most essential B2B companies you've probably never thought about—until now.

Today, Ecolab touches nearly every aspect of modern life. When you eat at a restaurant, sleep in a hotel, undergo surgery, or even when a semiconductor gets manufactured for your smartphone, Ecolab's invisible hand is there—cleaning, sanitizing, protecting. With $15.74 billion in revenue and $2.11 billion in earnings in 2024, this Saint Paul, Minnesota giant has become the world's leading provider of water, hygiene, and infection prevention solutions.

But here's what's fascinating: Ecolab isn't just a chemical company that got lucky. It's a masterclass in systems thinking, in the transition from selling products to selling outcomes, and in building what might be the stickiest business model in industrial America. How sticky? Warren Buffett once called businesses with Ecolab's characteristics "economic castles protected by unbreachable moats."

The journey from carpet cleaner to water technology titan reveals three transformative insights that every business builder should understand: First, the power of solving the whole problem, not just selling a product. Second, how service can become an impenetrable competitive advantage. And third, why purpose-driven capitalism isn't just feel-good marketing—it's a growth accelerator when done right.

Over the next few hours, we'll trace Ecolab's century-long evolution through family drama, failed acquisitions, brilliant pivots, and the kind of patient empire-building that would make Jeff Bezos jealous. We'll explore how a company founded on cleaning hotel carpets became Bill Gates's favorite water investment, and why data centers and AI might make Ecolab more essential in the next decade than it was in the last century.

II. The Hotel Carpet Problem: M.J. Osborn's Founding Vision (1923–1940s)

The year was 1923, and Merritt J. Osborn was running out of options. At 44, with two sons approaching college age and bills mounting, this veteran salesman had spent decades on the road, learning every corner of America's emerging hospitality industry. But knowledge wasn't paying the bills. He needed something more—he needed to own the solution to a problem that nobody else was solving.

The problem revealed itself in those endless hotel corridors. Osborn watched hotel managers wrestle with a maddening operational nightmare: dirty carpets. When a guest checked out, the carpet often needed deep cleaning. The standard practice? Roll it up, ship it to a cleaning facility, wait a week or more, then reinstall it. Meanwhile, the room sat empty, hemorrhaging potential revenue in an era when every dollar counted.

"What if," Osborn thought, "you could clean the carpet right there, in the room, and have it ready by evening?"

This wasn't just about convenience—it was about unlocking trapped value. A hotel with 100 rooms losing even three room-nights per month to carpet cleaning was sacrificing thousands of dollars annually. Multiply that across America's booming hospitality sector, and you had a billion-dollar problem hiding in plain sight.

Osborn's first product, Absorbit, was deceptively simple: a cleaning compound that could be applied to carpets in place, worked into the fibers, then vacuumed away along with the dirt. No removal, no downtime, no lost revenue. He founded Economics Laboratory—the name itself a statement of intent, marrying chemistry with business efficiency—and hired exactly one employee: Ida Koran, a sharp-minded office manager who would become as essential to the company's culture as Osborn himself.

But here's where Osborn revealed his true genius. While competitors might have stopped at selling a cleaning product, Osborn saw the bigger picture. Hotels didn't want to buy chemicals; they wanted to buy clean rooms ready for guests. So from day one, Economics Laboratory didn't just ship products—it provided training, customized solutions, and ongoing support. The company's salespeople became consultants, teaching hotel staff the optimal cleaning techniques, helping them calculate ROI, and continuously improving their operations.

This systems approach crystallized with the 1928 launch of Soilax, a dishwashing detergent specifically designed for the new mechanical dishwashers appearing in commercial kitchens. Again, Osborn wasn't just selling soap. He was selling a complete solution: the right chemical formulation, dispensing equipment to ensure proper dosage, and expert service to optimize the entire warewashing operation. This trinity—chemical, equipment, and service—would become Ecolab's enduring competitive advantage.

The timing was perfect. The Roaring Twenties had sparked a hospitality boom, with hotels and restaurants proliferating across America. Then came the Depression, which counterintuitively helped Economics Laboratory. As businesses struggled to survive, Osborn's efficiency-focused solutions became even more valuable. A hotel that could turn rooms faster and reduce operational costs had a fighting chance. A restaurant that could ensure spotless dishes with less labor could maintain standards while cutting expenses.

By 1940, Economics Laboratory had expanded across the United States, with sales reaching $5.4 million—roughly $115 million in today's dollars. But more importantly, Osborn had established a culture that would endure for a century: relentless innovation coupled with obsessive customer service. Employees weren't just selling products; they were solving problems. They weren't just visiting customers; they were becoming indispensable partners.

Ida Koran, that first employee, embodied this ethos. She managed the office with military precision while maintaining deep personal connections with customers and employees alike. Years later, when she died in 1967, she would leave her entire estate to create The Ida C. Koran Foundation, providing assistance to Ecolab employees in need—a testament to the family-like culture Osborn had fostered from the beginning.

As World War II approached, Economics Laboratory stood at a crossroads. The company had proven its model in hospitality, but Osborn sensed bigger opportunities. American industry was modernizing rapidly, and every factory, every food processor, every institution needed cleaning and sanitation solutions. The question was: Could a company built on hotel carpets and restaurant dishes transform into something much larger?

III. Post-War Expansion & Family Business Era (1950s–1970s)

The post-war boom hit America like a tidal wave of prosperity, and Economics Laboratory rode it with the precision of a surfer who'd been waiting for exactly this moment. In 1946, as GIs returned home and the economy shifted into overdrive, the company unveiled its first electronic dishwashing dispenser—a machine that seemed almost space-age to restaurant owners accustomed to manual operations. This wasn't just automation; it was the democratization of precision. Every wash cycle delivered exactly the right amount of chemical, eliminating waste and guaranteeing consistent results.

But the real masterstroke came in 1948 with the introduction of the first rinse additive—a product category that literally didn't exist before Economics Laboratory created it. Think about that for a moment: they invented a problem customers didn't know they had (water spots on dishes), then sold them the solution. By 1950, when the company launched Electrasol for consumer dishwashers, American housewives were lining up to buy a product they hadn't known they needed two years earlier.

That same year marked a pivotal transition. M.J. Osborn, now in his seventies, stepped down as president while remaining chairman. His son, Edward Bartley Osborn—E.B. to everyone who knew him—took the helm. Where M.J. had been the scrappy entrepreneur, E.B. was the polished executive, Harvard-educated and ready to transform a successful regional player into a national powerhouse.

E.B.'s first major move revealed his ambitions. In the early 1950s, Economics Laboratory acquired the Magnus Company, a chemical supplier with deep relationships in industrial sectors: pulp and paper, metalworking, transportation, and petrochemical processing. This wasn't just an acquisition; it was a door-opener into the vast world of industrial cleaning and processing. Suddenly, Economics Laboratory wasn't just cleaning dishes and carpets—it was helping paper mills maintain production efficiency, keeping locomotive engines free of deposits, and ensuring petroleum refineries operated at peak performance.

The international expansion that began in 1956 with a subsidiary in Sweden might have seemed quirky—why Sweden?—but it revealed sophisticated thinking. Sweden offered a prosperous, regulated market that valued quality and environmental responsibility, traits that would become Ecolab hallmarks. It was a beachhead into Europe, yes, but also a laboratory for learning how to operate across borders, currencies, and cultures.

Going public in 1957 injected capital and credibility, but it also marked the beginning of a tension that would define the next two decades: Could a family business maintain its culture while satisfying Wall Street's quarterly demands? For a while, the answer seemed to be yes. The 1960s saw explosive growth, crowned by the 1964 opening of the Merritt J. Osborn Research & Development Center in Mendota Heights, Minnesota—a 100,000-square-foot facility that announced Economics Laboratory's transformation from a sales-driven company to a technology-driven enterprise.

The research center wasn't just about chemistry; it was about understanding systems. Teams of scientists worked alongside customers to understand not just what needed to be cleaned, but why, how often, and what the failure costs were. They developed predictive models for soil buildup, optimized cleaning cycles for energy efficiency, and created custom formulations for specific industrial processes. This wasn't R&D in isolation—it was innovation through collaboration.

But success bred complacency, and by the mid-1970s, cracks were showing. The company had expanded into numerous adjacent markets without always maintaining its service excellence. Profit margins, which had routinely exceeded 15% in the 1960s, dipped to 10% by 1978. International operations were subscale and struggling. Most tellingly, E.B. Osborn seemed tired, worn down by nearly three decades of leadership and the increasing complexity of a business that had outgrown its family management structure.

The end came with surprising swiftness. In 1978, after a series of disappointing quarters and pressure from institutional investors, E.B. Osborn announced his retirement. For the first time in 55 years, Economics Laboratory would not have an Osborn at the helm. The family that had built the company retained significant shareholdings but ceded operational control to professional management.

The transition was messy. Employees who had grown up in a paternalistic culture suddenly faced MBA-wielding executives talking about "synergies" and "restructuring." Several senior leaders departed. Sales growth stalled as the organization struggled to find its identity. Was Economics Laboratory a family business that had gone public, or a public company with family heritage?

Yet beneath the turmoil, the fundamental strengths remained: unmatched service networks, deep customer relationships, and a portfolio of essential products with high switching costs. The question was whether new leadership could reignite growth while preserving what made Economics Laboratory special. As the 1980s dawned, that challenge would fall to an unlikely leader—one who would literally change the company's name and transform it into something the Osborns might never have imagined.

IV. The Transformation Years: From Economics Lab to Ecolab (1980s–1990s)

The boardroom at Economics Laboratory in 1979 felt like a wake. The Osborn era had ended, and with it, a certain romanticism about the business. The new CEO, Fred Lanners, came from outside the industry—a professional manager hired to professionalize a company that had grown beyond its family roots. His first presentation to the board was telling: not a single mention of M.J. Osborn's vision or the company's heritage. Instead, slides full of market segmentation analyses and portfolio optimization strategies. One longtime board member later recalled thinking, "We'd hired McKinsey when what we needed was Sam Walton."

Lanners's tenure started with a spectacular misfire. In 1979, the company acquired Apollo Technologies, a high-tech water treatment firm that promised to revolutionize industrial processing. The price tag was steep, the integration was bungled, and by 1983, Apollo was shut down, its assets written off. The failure cost Economics Laboratory not just money but credibility. Employees who had prided themselves on steady, smart growth watched as executives chased shiny objects.

But from failure came clarity. The Apollo debacle forced a reckoning: What was Economics Laboratory actually good at? The answer was both simple and profound—they were good at showing up. Every day, in thousands of locations, Economics Laboratory service representatives walked through customer doors, solved problems, and made operations run smoother. They weren't selling technology for technology's sake; they were selling reliability.

This insight drove the 1984 acquisition of Lystads, Inc., a pest elimination company that might have seemed like another random diversification but actually fit perfectly. Pest control, like cleaning, required regular service visits, deep customer relationships, and solutions tailored to specific environments. It was the same business model, just with different chemistry.

Then came 1986, and with it, one of the most important decisions in company history—one that almost didn't happen. Sandy Greve, the new CEO who had risen through the sales ranks, stood before the board with a radical proposal: change the company's name from Economics Laboratory to Ecolab. The board was split. Some saw it as abandoning heritage; others recognized that "Economics Laboratory" sounded like a Depression-era relic in the go-go 1980s.The debate raged for hours. Finally, Greve called for a vote. In 1986, the company changed its name from Economics Laboratory to Ecolab Inc. and was listed on the New York Stock Exchange. The "Eco" prefix captured both ecological consciousness and economics, while "lab" honored the company's innovation heritage. More importantly, it sounded modern, global, and memorable—everything Economics Laboratory wasn't.

The name change coincided with a broader strategic reset. The listing on the NYSE wasn't just about liquidity; it was a statement of ambition. No longer content to be a Midwest industrial company, Ecolab would compete globally. But first, it had to survive its biggest mistake.

The ChemLawn acquisition of 1987 still causes veterans to wince. In 1987, Ecolab purchased the lawncare servicer provider ChemLawn for $376 million. It sold the acquisition in 1992 to ServiceMaster for $103 million as it couldn't turn ChemLawn into a profitable business. On paper, it made perfect sense: ChemLawn had a nationally recognized brand, 1.5 million residential customers, and a service model similar to Ecolab's. What could go wrong?

Everything, as it turned out. Consumer lawn care was fundamentally different from B2B cleaning. Homeowners were price-sensitive and fickle; businesses valued reliability and expertise. ChemLawn's seasonal revenue patterns clashed with Ecolab's steady cash flows. Most damaging, the cultures were incompatible. ChemLawn's hard-charging, commission-driven sales force collided with Ecolab's consultative, relationship-based approach.

The numbers told the story: ChemLawn lost money every year under Ecolab ownership. When the company finally admitted defeat and sold to ServiceMaster for $103 million—a $273 million loss—it took a $263 million writeoff against 1991 earnings. The lesson was expensive but valuable: stick to what you know.

Yet even as ChemLawn was bleeding red ink, Ecolab was laying groundwork for its European future. Ecolab and the German fast-moving consumer goods firm Henkel KGaA formed a 50:50 European joint venture called 'Henkel-Ecolab' in 1991 to expand into European and Russian markets. The partnership with Henkel was everything ChemLawn wasn't: strategically aligned, culturally compatible, and focused on Ecolab's core competencies.

Henkel brought European distribution and regulatory expertise; Ecolab brought technology and service models. Together, they could attack a fragmented European market where American-style integrated cleaning solutions were still novel. The joint venture would eventually generate billions in revenue and teach Ecolab how to operate in dozens of countries with different languages, currencies, and business customs.

The 1990s also saw Ecolab double down on specialization. The 1994 acquisition of Kay Chemical brought deep expertise in quick-service restaurant cleaning—a segment where speed, consistency, and food safety were paramount. Kay's relationships with McDonald's, Burger King, and other chains gave Ecolab a foothold in one of the fastest-growing segments of the food service industry.

By decade's end, Ecolab had transformed from a troubled family business into a focused, professional enterprise. Revenue exceeded $2 billion. International operations were profitable and growing. The service model—those thousands of representatives making daily customer visits—had proven to be not just defensible but unassailable. Competitors could copy products; they couldn't replicate relationships.

But the real transformation was philosophical. Ecolab had learned that growth for growth's sake was dangerous. ChemLawn taught them that. Instead, they would grow by deepening expertise, by solving harder problems, by becoming so essential to customers that switching would be unthinkable. This discipline would serve them well when, in 2004, a new CEO would arrive with even bigger ambitions.

V. The Doug Baker Era: Building a Modern Industrial Giant (2004–2020)

Doug Baker didn't look like a revolutionary when he joined Ecolab in 1989. Fresh from marketing roles at Procter & Gamble, he was just another MBA in a company suddenly full of them. But Baker had something rare: the ability to see a traditional industrial company as a technology platform waiting to be unleashed. When he became CEO in 2004, after steadily climbing through marketing and operational roles, he inherited a good company with $4.2 billion in sales. By the time he stepped down in 2020, he had built a $15 billion giant worth over $60 billion.

Baker's first insight was deceptively simple: Ecolab wasn't really in the chemical business. "We're in the results business," he would tell anyone who'd listen. "Customers don't buy chemicals; they buy clean dishes, safe food, efficient operations." This wasn't just semantic gymnastics. It fundamentally changed how Ecolab approached innovation, pricing, and competition.

Consider the Circle the Customer strategy Baker launched in 2005. Rather than organizing by product lines—a chemical for this, a dispenser for that—Ecolab reorganized around customer outcomes. A hospital didn't have separate vendors for hand hygiene, surgical instrument cleaning, and environmental sanitation; they had Ecolab, solving all their infection prevention needs holistically. A food plant didn't juggle relationships with cleaning chemical suppliers, water treatment companies, and pest control services; Ecolab integrated everything.

This approach drove organic growth, but Baker knew that transformation required bold moves. The biggest came in 2011 with the announcement of the Nalco merger. In 2011, Ecolab announced a merger with Nalco Holding Company, Inc., an industrial water technology firm. In December 2011, Nalco, later renamed Nalco Water, became a wholly owned subsidiary of Ecolab after Ecolab completed the $5.4 billion acquisition.

The Nalco deal was audacious—Ecolab's market cap was only about $13 billion at the time, making this a bet-the-company acquisition. Nalco brought industrial water treatment expertise, energy services capabilities, and crucially, a data analytics platform that could predict equipment failures before they happened. This wasn't just about adding revenue; it was about evolving Ecolab from a service company to a technology company.

Wall Street was skeptical. The stock dropped 8% on the announcement. Integration would be complex, cultures might clash, and the debt load was substantial. But Baker saw what others missed: water scarcity was becoming the defining industrial challenge of the 21st century, and the combination of Ecolab's service network with Nalco's water expertise would create an unbeatable platform.

The integration was masterful. Rather than forcing Nalco into Ecolab's structure, Baker created a new Water division that preserved Nalco's strengths while leveraging Ecolab's distribution. Within two years, synergies exceeded projections. More importantly, the combination unlocked new capabilities. Ecolab could now offer total water management—from intake to discharge—for entire industrial facilities. The numbers validated Baker's vision spectacularly. Between 2004 and 2019, Ecolab's sales grew 334% to $14.9 billion as net income grew 500% to $1.6 billion. The share price rose from about $27.50 to $225 per share, with market value increasing from $7 billion to $60 billion-plus. But raw financial performance only told part of the story.

In 2012, the same year as the Nalco integration, Ecolab acquired Champion Technologies for $2.2 billion (closed April 2013), deepening its presence in oil and gas markets. This proved to be Baker's rare misstep. As Baker later admitted, "Champion, in hindsight was a mistake." When oil prices collapsed from over $100 per barrel to under $30, these energy-sector acquisitions became millstones. In 2019, Ecolab spun off its upstream energy business, essentially unwinding parts of both deals.

Yet even failures taught valuable lessons. The energy debacle reinforced Ecolab's core insight: stick to markets where water, cleaning, and sanitation create demonstrable value regardless of commodity cycles. This discipline would prove crucial as Baker positioned Ecolab for an even more audacious transformation.

"We're not a chemical company," Baker would insist in investor meetings, often to puzzled looks. "We're a technology company that happens to use chemistry." This wasn't Silicon Valley posturing. By 2015, Ecolab was collecting billions of data points from sensors in customer facilities, using machine learning to predict equipment failures, optimize chemical usage, and prevent food safety incidents before they occurred.

The transformation went beyond technology. As CEO since 2004, Doug Baker infused sustainability and purpose into the company's operations and the work it does around the world to help customers achieve their own sustainability goals. This wasn't greenwashing. Ecolab's entire business model aligned with resource efficiency. Every gallon of water saved, every unit of energy conserved, every foodborne illness prevented created value for customers while advancing environmental goals.

Consider the numbers: The company helped its customers in more than 170 countries conserve 206 billion gallons of water in 2020, equivalent to the annual drinking water needs of 712 million people. This wasn't charity—it was business. Customers paid Ecolab precisely because the company could deliver these savings profitably.

Baker's leadership philosophy was deceptively simple: "Make yourself better, not just bigger." "The real goal is to make yourself better. It's easy to become bigger. It's not as easy to become better. And doing both at the same time is sort of the holy grail." This meant saying no to acquisitions that didn't strengthen core capabilities, investing heavily in R&D even when Wall Street wanted higher margins, and maintaining service levels that competitors deemed uneconomical.

The culture Baker built was equally distinctive. The ranks of people of color grew to 30% under Baker. He championed early childhood education, understanding that Ecolab's long-term success depended on healthy communities with skilled workers. He served on boards from U.S. Bank to Target, becoming a fixture in Minnesota's business community while maintaining the humility of someone who'd started as a brand manager at P&G.

In 2019, Baker ranked 38th on Harvard Business Review's list of the world's best-performing CEOs. But rankings didn't capture Baker's true achievement. He had taken a good company and made it essential—to restaurants that couldn't operate without Ecolab's food safety programs, to hospitals that relied on its infection prevention protocols, to data centers that needed its precision cooling water treatment.

As Baker prepared to hand over the CEO role to Christophe Beck in 2021, he reflected on the transformation. "In total we did 120 acquisitions. We've gotten the vast majority right." More importantly, he had proven that industrial companies could deliver both exceptional returns and positive impact—that purpose and profit weren't opposing forces but reinforcing ones.

The stage was set for the next act, one where technology, sustainability, and global water challenges would converge in ways even Baker couldn't fully anticipate.

VI. The Bill Gates Investment & Strategic Evolution (2012–Present)

The news broke on a quiet Tuesday in 2012, buried in regulatory filings that most investors ignore. Microsoft co-founder Bill Gates, through his investment vehicles Cascade Investment and the Bill & Melinda Gates Foundation, increased his stake of 10.8% in Ecolab to 25%. For a company that had operated in relative obscurity for 89 years, suddenly having the world's most famous philanthropist as your largest shareholder was jarring. Employees wondered: Why Ecolab? What did Gates see that others missed?

The answer lay not in Ecolab's financial statements but in a simple, terrifying fact: water scarcity would define the 21st century. Gates, through his foundation's work in Africa and Asia, had witnessed firsthand how lack of clean water perpetuated poverty, disease, and conflict. He needed industrial-scale solutions, not charity. Ecolab, with its unique combination of water expertise, global reach, and service infrastructure, represented the kind of systems-level intervention that could actually move the needle.

Gates wasn't interested in a passive investment. His team at Cascade Investment engaged deeply with Ecolab's technology roadmap, pushing for more aggressive digitalization and expanded work in emerging markets. The Gates Foundation explored partnerships where Ecolab's expertise could improve sanitation in refugee camps or optimize water use in drought-stricken regions. This wasn't corporate social responsibility; it was recognizing that the same technologies that kept Coca-Cola bottling plants running efficiently could transform water access in Bangladesh.

The partnership accelerated Ecolab's evolution from service provider to technology platform. By 2018, when Bill Gates purchased $230 million in additional shares of Ecolab via Cascade Investments, the company had deployed over 1.5 million connected devices collecting real-time data from customer facilities. Machine learning algorithms analyzed this data stream, identifying patterns humans couldn't see: a slight pressure variation that predicted pump failure, a temperature anomaly that signaled biofilm formation, a usage pattern that suggested employee non-compliance with handwashing protocols.

But technology was just the enabler. The real transformation was in business model innovation. Ecolab began offering "Water-as-a-Service" contracts where customers paid not for chemicals or equipment but for guaranteed outcomes: water quality that met specifications, energy consumption below targets, zero food safety incidents. This shifted risk from customers to Ecolab while creating powerful incentives for continuous improvement.

The 2021 acquisition of Purolite for approximately $3.7 billion exemplified this strategic evolution. In 2021, Ecolab acquired Purolite, a provider of ion-exchange resins for biopharmaceutical purification for approximately $3.7 billion. Purolite wasn't just another chemical company; it was a critical technology for producing COVID vaccines, purifying insulin, and manufacturing the next generation of biological drugs. As pharmaceuticals shifted from small-molecule chemicals to large-molecule biologics, purification became the bottleneck. Ecolab now owned a key piece of that puzzle.

The timing was perfect. The pandemic had elevated hygiene and sanitation from operational concerns to existential ones. Hotels couldn't reopen without credible cleaning protocols. Restaurants needed visible proof of safety. Hospitals required military-grade infection prevention. Ecolab's "Science Certified" program, launched during COVID, became the gold standard—a seal that told consumers this establishment took cleanliness seriously.

Yet even as traditional markets boomed, Ecolab was positioning for the next wave. The 2023 partnership with Miso Robotics seemed odd at first glance. In 2023, Ecolab partnered with and invested in Miso Robotics, a company specializing in automated in-restaurant robotic arms and other equipment for food preparation and staff augmentation. Why was a cleaning company investing in burger-flipping robots? Because Ecolab understood that automation would transform commercial kitchens, and whoever controlled the cleaning and sanitation protocols for these robots would own a crucial piece of the value chain.

The most dramatic shift came in data centers—a market that barely existed when Baker became CEO but now consumed more water than many cities. Every Google search, every Netflix stream, every Zoom call generated heat that required cooling, and cooling meant water. Ecolab's precision water treatment could reduce a data center's water consumption by 30% while improving reliability. As AI drove exponential growth in computing demand, Ecolab found itself at the intersection of two megatrends: digitalization and water scarcity.

By 2022, Gates's stake had declined to 11% as he diversified his holdings, but his impact on Ecolab was permanent. In 2022, Bill Gates purchased additional stock through Cascade, though his overall stake dropped to 11%. The company now thought in decades, not quarters. It invested in technologies that might not pay off for years. It pursued markets where impact mattered as much as margins.

The transformation was visible in how Ecolab described itself. No longer "a cleaning and sanitation company," it was "a global sustainability leader that provides water, hygiene and infection prevention solutions." The shift wasn't just semantic. Ecolab now competed for talent with technology companies, not chemical manufacturers. Its salespeople were called "associates," its service technicians were "field experts," and its R&D wasn't just about chemistry but about data science, robotics, and artificial intelligence.

This evolution positioned Ecolab perfectly for the challenges ahead: a world where water was scarce, regulations were tightening, and customers demanded not just products but guaranteed outcomes. The question was whether new leadership could maintain this momentum while navigating an increasingly complex global landscape.

VII. Leadership Transition & The Christophe Beck Era (2020–Present)

Christophe Beck didn't arrive at Ecolab headquarters on January 1, 2021, with fanfare or revolutionary pronouncements. The Swiss engineer-turned-executive, who had worked on space shuttle projects for the European Space Agency before spending 16 years at Nestlé, understood that following Doug Baker was like conducting Beethoven after Leonard Bernstein—you better respect what came before while finding your own voice.

Beck, a native of Switzerland with dual Swiss and U.S. citizenship, had joined Ecolab in 2007 following 16 years as a senior executive at Nestlé, where earlier in his career, he worked on a space shuttle project for the European Space Agency. His path through Ecolab had been methodical: running regional operations, leading the crucial Nalco integration, serving as president and COO. He understood the company's DNA—that unique blend of chemistry, service, and systems thinking that made Ecolab irreplaceable to its customers.

But Beck also arrived at an inflection point. COVID-19 had simultaneously validated Ecolab's importance (everyone suddenly cared about hygiene) and disrupted its business model (hotels and restaurants were shuttered). The pandemic exposed both strengths and vulnerabilities in ways no strategic review ever could.

Christophe was named Ecolab's president and chief executive officer in January 2021, and chairman in May 2022. His first major decision revealed his strategic priorities: maintain course while accelerating transformation. Where Baker had been the revolutionary, Beck would be the optimizer—but optimization at Ecolab's scale could be revolutionary in its own right.

The "One Ecolab" initiative became Beck's signature strategy. For decades, Ecolab had operated as a federation of businesses—Institutional, Industrial, Healthcare, Life Sciences—each with its own P&L, systems, and culture. This structure had enabled entrepreneurship but created inefficiencies. A hospital might have three different Ecolab representatives calling on it: one for cleaning chemicals, another for surgical instruments, a third for water treatment. Data collected in one division couldn't easily benefit another.

Beck's insight was that digital transformation wasn't just about technology—it was about integration. "Most companies produce products, or solutions, or expertise, or digital technology," Beck explained. "Most companies produce products, or solutions, or expertise, or digital technology. We bring it all together". Under One Ecolab, customer data would flow seamlessly across divisions. A food plant's water treatment data could inform its pest control protocols. A hotel's laundry usage could optimize its housekeeping schedules.

The pandemic had created unexpected opportunities. Ecolab's more than 1,400 global headquarters associates in St. Paul are typically in the office three or more days a week, recognizing that in-person interactions are a key part of collaborative culture, with more than 700 associates at headquarters every day. While other companies went fully remote, Beck understood that Ecolab's field service model required physical presence—you can't clean a restaurant kitchen over Zoom. This commitment to in-person work became a differentiator in recruiting and retention.

Beck's leadership style contrasted sharply with Baker's charismatic presence. Where Baker was the visionary CEO who could inspire a room, Beck was the engineer who could optimize a system. "The most important learning has been that I don't always need to have the answers. Even if I don't know what the solution is because things are changing too fast", Beck reflected on his leadership approach.

The financial results validated Beck's approach. Ecolab's 2024 Growth & Impact Report details record year of business performance by helping deliver $9.1B in cumulative customer value, save enough water for 781M people and protect 1.7B people from illnesses. The company was firing on all cylinders: organic growth accelerating, margins expanding, and sustainability metrics improving.

But Beck's most ambitious moves were still ahead. The push into data centers and microelectronics wasn't just about finding new markets—it was about positioning Ecolab at the intersection of the physical and digital worlds. The company expanded its services to data centers, where, among its offerings, it provides chip-cooling solutions that minimize water use. Every AI model, every cryptocurrency transaction, every metaverse experience required massive computing power, which generated heat, which required cooling, which meant water. Ecolab was becoming essential infrastructure for the digital economy.

The commitment to sustainability under Beck went beyond rhetoric. Achieved 100% renewable electricity in Ecolab's EU operations, reaching 71% renewable globally and on track to 100% by 2030. Accelerated efforts to convert Ecolab's North American sales and service fleet to electric vehicles by 2030. These weren't just environmental goals—they were business strategies. Customers increasingly demanded that suppliers match their own sustainability commitments.

Beck's vision for Ecolab's future was both ambitious and grounded: "We've made the commitment that by 2030, we'll help our customers save enough water for the drinking needs of one billion people. Last year, we helped save enough water for over 780 million people". This wasn't corporate PR—it was a measurable, auditable commitment that aligned perfectly with customer needs and global challenges.

As 2024 drew to a close, Beck had successfully navigated the transition from legendary predecessor to successful successor. "Ecolab's winning formula is to grow fast by growing our impact and growing our team," said Christophe Beck. The company was positioned for its next century: still grounded in M.J. Osborn's original insight about solving whole problems, but now armed with AI, robotics, and data analytics that would have seemed like science fiction to that traveling salesman in 1923.

VIII. Business Model Deep Dive: The Power of Recurring Revenue

To understand Ecolab's business model, imagine you're running a McDonald's franchise. Every morning at 4 AM, before the first customer arrives, an Ecolab representative shows up. They check the dishwasher's chemical levels, inspect the fryer oil quality, verify sanitizer concentrations, test the ice machine for bacteria, and ensure pest control measures are functioning. They don't just drop off chemicals and leave—they're solving for cleanliness, safety, and operational efficiency. Now multiply this scene by 3 million customer locations worldwide, every single day.

This is the genius of Ecolab's recurring revenue model: customers aren't buying products; they're buying peace of mind. And once you're in, getting out is almost unthinkable.

The model begins with what Ecolab calls the "circle the customer" approach. Instead of selling individual products—a detergent here, a sanitizer there—Ecolab provides integrated solutions. That McDonald's doesn't have separate vendors for dish cleaning, floor care, hand hygiene, pest control, and grease management. One Ecolab representative handles everything, armed with data from previous visits, predictive analytics about potential problems, and the authority to adjust protocols on the spot.

The economics are compelling. Organic operating income margin 17.4%, +150 bps as solid sales growth more than offset growth-oriented investments in the business. These aren't software margins, but for an industrial business requiring physical presence and inventory, they're extraordinary. The secret lies in the service layer that wraps around the physical products.

Consider the dispensing equipment—Ecolab's Trojan horse. When Ecolab installs a dishwasher dispenser or a hand hygiene system, it's not just placing hardware. These devices are increasingly connected, reporting usage patterns, flagging anomalies, and automatically reordering supplies. The equipment is often provided at low or no cost, because it locks in years of chemical purchases and service contracts. It's the razor-and-blades model, but with switching costs that would make Gillette envious.

The switching costs are where Ecolab's moat becomes a castle wall. Changing cleaning vendors means retraining staff on new procedures, replacing dispensing equipment, risking compliance failures during the transition, and losing the institutional knowledge that Ecolab's representative has built about that specific facility. One food safety incident during a vendor transition could cost more than a decade of Ecolab's fees. Rational managers don't take that risk.

This stickiness shows up in the numbers. Customer retention rates exceed 95% in most segments. Our team won a significant amount of new business that helped to offset continued soft macro demand, launched a strong pipeline of new breakthrough technologies, drove pricing backed by strong customer value, and further improved our underlying productivity by leveraging our leading digital capabilities. All of this is the result of the work we have done over the last few years to further strengthen Ecolab's key long-term growth drivers.

The pricing power is remarkable. Additionally, we will implement value pricing that reflects the increasing value Ecolab delivers to customers. Even in deflationary periods, Ecolab maintains pricing because customers pay for outcomes, not commodities. When raw material costs decline, Ecolab's margins expand. When costs rise, price increases are passed through with minimal customer pushback because the alternative—managing cleaning and sanitation internally—is operationally terrifying.

The network effects, while subtle, are powerful. Every Ecolab representative who visits a Marriott in Minneapolis learns something that benefits a Marriott in Mumbai. Every food safety protocol developed for Tyson Foods can be adapted for JBS. Every water treatment innovation for an Intel fab can be modified for a TSMC facility. With 25,000 field representatives making millions of customer visits annually, Ecolab operates the world's largest real-world laboratory for cleaning and sanitation.

The "Ecolab Digital" initiative represents the next evolution. We expect to continue this good momentum by generating further market share gains through our One Ecolab initiative and accelerating performance in our growth engines, specifically in data centers, microelectronics, life sciences, and Ecolab digital. By 2025, the company plans to report digital sales as a separate category, recognizing that software subscriptions, digital equipment leases, and data services are becoming material revenue streams.

The model's resilience was tested during COVID and passed spectacularly. When restaurants closed, institutional sales plummeted. But healthcare and food retail sales surged. When hospitality recovered, it came back with unprecedented demand for visible cleaning protocols. The portfolio's diversity—40 different industries served—provides natural hedging against sector-specific downturns.

The capital efficiency is often overlooked but crucial. Unlike software companies that spend heavily on customer acquisition, Ecolab's customers come through word-of-mouth and regulatory requirements. Unlike manufacturers who need massive factories, Ecolab's plants are relatively small and distributed. Unlike pure service companies that scale linearly with headcount, Ecolab's technology leverage means each representative can serve more customers more effectively over time.

The virtuous cycle accelerates with scale. More customers generate more data, which improves predictive models, which enhances service quality, which increases customer retention, which provides stable cash flows for R&D investment, which creates better solutions, which attract more customers. Competitors can copy products but can't replicate this ecosystem overnight.

Perhaps most importantly, the model aligns perfectly with customer incentives. Ecolab only succeeds when customers achieve their cleanliness, safety, and sustainability goals. Ecolab's significant growth and impact demonstrates how companies can drive positive business, operational and environmental outcomes simultaneously. By collaborating with its valued partners, Ecolab will continue to achieve its positive performance into the future. This isn't just good business—it's antifragile business, growing stronger from the very challenges that destroy traditional product companies.

IX. Playbook: Key Business Lessons

After a century of growth, through depressions, wars, pandemics, and technological revolutions, Ecolab's success distills into a playbook that challenges conventional business wisdom. These aren't just lessons—they're contrarian insights that explain why a carpet cleaning company became a $75 billion market cap giant while flashier competitors faded into obscurity.

Systems thinking beats product thinking

M.J. Osborn's original insight remains Ecolab's core advantage: customers don't want to buy cleaning products; they want clean, safe, compliant operations. This seems obvious, yet most of Ecolab's competitors still organize around products. They have a floor care division, a hand hygiene unit, a food safety team. Ecolab has customer solutions that happen to involve chemicals.

Consider how this plays out in practice. A hospital using traditional vendors might excel at surgical instrument sterilization but struggle with environmental cleaning. Different vendors, different protocols, gaps in coverage. Ecolab sees the hospital as an integrated system where a contaminated door handle can negate perfect surgical procedures. One provider, one accountability, one outcome: reduced infection rates.

This systems approach enables pricing power that product companies can only dream about. When you sell bleach, you compete on price per gallon. When you sell infection prevention, you compete on patient outcomes. The former is a race to the bottom; the latter is a partnership where price becomes secondary to performance.

Service as a moat

Those 25,000 field associates aren't a cost center—they're Ecolab's most defensible competitive advantage. Every day, they walk into customer facilities with knowledge accumulated from millions of similar visits. They spot problems before they manifest. They adjust protocols based on seasonal variations. They train staff who turn over constantly in hospitality and food service.

This human network can't be disrupted by software alone. Yes, sensors and AI can monitor and predict, but someone still needs to adjust that dishwasher dispenser, train that new kitchen manager, and respond when the health inspector arrives. Ecolab's representatives become embedded in customer operations, trusted advisors who know more about a facility's cleaning needs than the facility managers themselves.

The switching cost isn't just operational—it's emotional. That Ecolab representative who's been visiting weekly for five years isn't just a vendor; they're part of the team. Replacing them means starting over with someone who doesn't know that the east dishwasher runs hot, that the morning shift needs extra coaching, or that the GM panics about the floors before corporate visits.

Industry consolidation strategy

Ecolab's acquisition strategy follows a clear pattern: buy regional leaders, integrate their customer relationships into Ecolab's platform, then cross-sell the full portfolio. It's not about buying revenue; it's about buying route density and customer access.

The 2021 Purolite acquisition exemplifies this approach perfectly. Purolite brought specialized ion-exchange technology crucial for biopharmaceutical production. But more importantly, it brought relationships with every major pharma company globally. Now Ecolab can offer those customers water treatment, contamination control, and cleaning validation—services worth multiples of the original resin business.

This roll-up strategy works because cleaning and sanitation remain surprisingly fragmented globally. Every country has local players who understand regional regulations and customer preferences. Ecolab acquires that local expertise, then supercharges it with global R&D, digital tools, and best practices from other markets.

Purpose + Profit alignment

When Doug Baker transformed Ecolab into a sustainability leader, skeptics saw it as costly virtue signaling. They missed the strategic brilliance: in Ecolab's business, environmental efficiency IS operational efficiency. Every gallon of water saved reduces customer costs. Every kilowatt-hour conserved improves margins. Every infection prevented avoids litigation.

This alignment makes Ecolab's sales pitch irresistible. CFOs love the cost savings. Sustainability officers love the environmental metrics. Operations teams love the simplified vendor management. Boards love the risk mitigation. Everyone wins, which is why customer relationships last decades.

The purpose-driven approach also attracts and retains talent. The best chemical engineers and data scientists have choices. They choose Ecolab because the work matters—preventing disease, conserving water, ensuring food safety. This talent advantage compounds over time, as motivated employees innovate faster and serve customers better.

The power of patient capital

Ecolab plays a different game than quarterly-focused competitors. The company routinely invests in markets that won't pay off for years. The push into data centers started a decade before AI made it obviously brilliant. The water resilience platform was built before drought made headlines. The infection prevention expertise was developed before COVID made it existential.

This patience extends to pricing. Ecolab often enters new customers at break-even or loss, knowing that once embedded, the relationship will be profitable for decades. It's venture capital economics applied to industrial services—lose money on customer acquisition, make it up over the lifetime value.

Geographic expansion follows the same patient playbook. Ecolab entered China in the 1970s, decades before it became profitable. Today, Asia-Pacific is a growth engine. The company invests in infrastructure, relationships, and regulatory expertise years before markets mature, positioning itself to capture value when industries modernize.

Technology as an accelerant, not a replacement

While competitors chase digital disruption, Ecolab uses technology to make human service more valuable. IoT sensors don't replace field representatives; they tell representatives where to focus. AI doesn't eliminate expertise; it augments it with pattern recognition across millions of data points. Digital platforms don't disintermediate customer relationships; they deepen them through continuous engagement.

This pragmatic approach to technology reflects deep understanding of customer reality. A restaurant manager dealing with a health inspection doesn't need an app; they need an expert who can fix problems immediately. A hospital facing a nosocomial outbreak doesn't need a dashboard; they need someone who's solved this before.

The technology investments pay off through operational leverage. One representative today can serve more customers than five could a decade ago, not because they're moving faster but because they're working smarter. Predictive analytics means fewer emergency calls. Remote monitoring means fewer routine visits. Automated reordering means fewer stockouts. The human touch remains, but technology makes it more valuable.

The compound advantage

Each of these strategies reinforces the others, creating compound advantages that accelerate over time. Systems thinking enables better service delivery. Superior service creates switching costs. High retention generates cash for acquisitions. Acquisitions increase route density. Greater density improves economics. Better economics fund R&D. Innovation strengthens the value proposition. And the flywheel spins faster.

This is why competing with Ecolab is so difficult. You can't just match one element—you need to replicate the entire system. And by the time you've built it, Ecolab has moved further ahead. It's not a moat; it's an expanding ocean.

X. Bear vs. Bull Case & Future Outlook

Bull Case: The Essential Services Compounder

The bulls see Ecolab as Warren Buffett's dream: a business with pricing power, recurring revenue, and exposure to irreversible megatrends. Start with the baseline resilience. Even in the 2008 financial crisis, when industrial production collapsed and hotels sat empty, Ecolab's revenue declined just 8% while maintaining profitability. This isn't discretionary spending—it's operational necessity.

The pathway to 20% margin target over the next three years seems conservative given current momentum. Organic operating income margin 17.4%, +150 bps in Q4 2024 demonstrates accelerating operational leverage. With the One Ecolab initiative eliminating duplicative costs and digital tools improving field productivity, margin expansion could surprise to the upside.

Water scarcity represents a multi-decade tailwind that's still underappreciated by markets. The UN projects that by 2030, global water demand will exceed supply by 40%. Every company on Earth will need to optimize water usage, and Ecolab owns the most comprehensive water management platform globally. This isn't speculative—major corporations are already signing enterprise-wide water resilience contracts worth hundreds of millions.

The data center opportunity alone could double Ecolab's addressable market. AI computing requires 10x the cooling of traditional servers. Every ChatGPT query, every Tesla autonomous mile, every Meta virtual reality session generates heat that must be dissipated. Ecolab's precision cooling water treatment can reduce water usage by 30% while improving reliability—savings worth millions per facility. With thousands of data centers planned globally, this vertical could become a $5+ billion business.

Life sciences expansion through Purolite positions Ecolab perfectly for the biologics revolution. Traditional pharmaceutical manufacturing is shifting from chemical synthesis to biological production—growing medicines in living cells. This requires ultra-pure water, contamination control, and specialized separation technologies. The $3.7 billion Purolite acquisition looks cheap considering biologics are growing 15% annually and will represent 50% of new drug approvals by 2030.

The competitive position keeps strengthening. Each customer that implements Ecolab Digital becomes harder to dislodge. Each sustainability report that credits Ecolab for water savings deepens the partnership. Each food safety incident at a non-Ecolab facility reinforces the value proposition. Network effects are finally kicking in after decades of foundation-building.

Geographic expansion remains early innings. Ecolab generates 50% of revenue internationally but has minimal presence in India, Southeast Asia, and Africa—markets where rising hygiene standards and industrial growth create massive opportunities. As these economies develop, they'll need Ecolab's expertise to meet international standards for exports and tourism.

The balance sheet provides unlimited flexibility with investment-grade ratings and modest leverage. Ecolab could easily fund $10+ billion in acquisitions while maintaining its dividend and buyback programs. Given management's disciplined track record—120 acquisitions under Baker with few failures—capital deployment should enhance returns.

ESG tailwinds are becoming hurricane forces. Ecolab's winning formula is to grow fast by growing our impact and growing our team... As companies around the world seek a path to greater profitability and resource efficiency, the Ecolab team is showing once again how we can achieve simultaneously great performance and positive impact. Every corporate sustainability commitment essentially mandates Ecolab's services. You can't achieve net-zero water commitments without measurement and optimization—Ecolab's core competency.

Bear Case: The Mature Industrials Trap

The bears see a different story: a mature industrial company trading at tech multiples despite facing structural headwinds. Start with valuation—at 35x earnings, Ecolab trades at a premium to Microsoft despite growing at a fraction of the rate. Any disappointment could trigger multiple compression that overwhelms operational improvements.

Economic sensitivity remains underappreciated. Yes, Ecolab proved resilient in past recessions, but those were different economies. Today's Ecolab has heavy exposure to casual dining, hotels, and industrial production—all highly cyclical sectors. A serious recession could impact 60% of revenue simultaneously, and fixed cost deleveraging would savage margins.

The capital intensity is concerning and increasing. The company is also well prepared to manage through the dynamic international trade environment given the strength of Ecolab's world class supply chain, its 'local for local' production model sounds reassuring, but maintaining local production in dozens of countries requires massive capital investment. Management guides to capital expenditure reaching 7% of sales in 2025, up from historical 5-6%. That's $1+ billion annually that won't drop to free cash flow.

Competition is intensifying from unexpected angles. Amazon's entry into B2B supplies threatens distribution advantages. Chemical giants like BASF and Dow are moving downstream into services. Regional players in Asia are consolidating and becoming formidable. Even customers are exploring insourcing as digital tools make self-service feasible.

Technology disruption remains a threat despite Ecolab's digital initiatives. Startups are offering sensor-based monitoring and AI-driven optimization at fraction of Ecolab's cost. While Ecolab argues human service remains essential, younger managers comfortable with digital tools might disagree. The field service model that's been Ecolab's moat could become its anchor.

Regulatory and environmental liabilities lurk beneath the surface. Ecolab handles millions of gallons of industrial chemicals daily. One major incident—a chemical spill, a contamination event, a worker exposure lawsuit—could result in billions in liability. The company operates in 170 countries with different regulatory regimes, any of which could change unfavorably.

Integration complexity multiplies with each acquisition. The One Ecolab initiative sounds strategic, but it's essentially a massive IT and organizational restructuring during a period of rapid growth. Integration failures, system outages, or culture clashes could disrupt customer relationships that took decades to build.

Customer concentration risk is hidden but real. While Ecolab serves 3 million locations, the top 100 customers likely represent 30-40% of revenue. Losing a Marriott, a Walmart, or a major food processor would be devastating. As these customers consolidate, their negotiating power increases.

Input cost inflation could return with vengeance. Ecolab benefited from declining chemical costs in 2023-2024, but this tailwind is reversing. Oil prices, from which many chemicals derive, remain volatile. Labor costs for field service representatives are rising faster than inflation. Transportation costs for daily customer visits keep climbing.

Future Outlook: The Convergence Opportunity

Looking ahead, Ecolab sits at the convergence of multiple transformative trends that could reshape its trajectory over the next decade.

The water-energy-food nexus becomes more critical annually. Producing food requires water. Cleaning water requires energy. Generating energy needs cooling water. This interdependence creates systemic risks that only integrated solutions can address. Ecolab's unique position across all three sectors makes it indispensable for resource optimization.

Climate adaptation will drive massive investment regardless of mitigation efforts. Even if the world achieves net-zero emissions, existing warming guarantees decades of droughts, floods, and extreme weather. Every industrial facility will need to become more water-resilient. Ecolab's water risk monetizer platform, which quantifies financial exposure to water scarcity, could become as essential as insurance.

The biosecurity imperative extends beyond COVID. Antimicrobial resistance, emerging pathogens, and bioterrorism concerns mean infection prevention becomes permanent infrastructure. Hospitals, schools, offices, and public spaces will maintain elevated hygiene standards indefinitely. Ecolab's infection prevention expertise positions it as the biosecurity partner for institutions globally.

AI and automation will transform the service model, but not eliminate it. Ecolab's vision involves AI-powered "digital twins" of customer facilities that continuously optimize operations. Field representatives become data-armed consultants who implement AI recommendations and handle exceptions. This hybrid model could double productivity while strengthening customer relationships.

The circular economy transition creates new business models. Instead of selling chemicals that become waste, Ecolab could offer closed-loop systems that recover, purify, and reuse water and chemicals. This transformation from linear to circular operations could unlock entirely new revenue streams while achieving true sustainability.

Geographic expansion into emerging markets accelerates as infrastructure develops. India's food processing industry, China's semiconductor fabs, Africa's tourism sector—all require Ecolab's expertise to meet international standards. These markets could add $10+ billion in addressable market over the next decade.

The synthesis is compelling: Ecolab has built a platform that becomes more valuable as the world becomes more complex. Water scarcity, climate volatility, disease risk, food security, industrial digitalization—every challenge creates demand for Ecolab's integrated solutions. The question isn't whether Ecolab remains relevant, but whether it can scale fast enough to capture the opportunity.

XI. Recent News

The recent developments at Ecolab paint a picture of a company hitting its stride while navigating an increasingly complex global landscape. ST. PAUL, Minn. – May 13, 2025 – Ecolab Inc., a global sustainability leader offering water, hygiene, and infection prevention solutions, continues to grow fast by growing its impact and team while creating substantial customer value. Ecolab's 2024 Growth & Impact Report details record year of business performance by helping deliver $9.1B in cumulative customer value, save enough water for 781M people and protect 1.7B people from illnesses.

The financial momentum is undeniable. Reported diluted EPS $1.66, +18%. Adjusted diluted EPS, excluding special gains and charges and discrete tax items were $1.81, +17%. Full-year 2024 cash flow from operating activities $2.8 billion. Record full-year 2024 free cash flow of $1.8 billion. This isn't just growth—it's profitable, cash-generative expansion that's funding both dividends and strategic investments.

The strategic repositioning continues with segment realignment that better reflects Ecolab's evolving business mix. Effective in the first quarter of 2025, Ecolab modified its segment reporting. Ecolab's Global Industrial segment was renamed Global Water and includes Light & Heavy (previously named Water), Food & Beverage, and Paper. Ecolab's Global Institutional & Specialty segment continues to include Institutional and Specialty. The company's healthcare business has moved into Institutional. Global Life Sciences was elevated to a standalone segment. The Global Pest Elimination segment remains a standalone segment. This reorganization isn't just corporate shuffling—it signals where management sees the highest growth potential.

The growth engines are accelerating precisely where the future demands them. We expect to continue this good momentum by generating further market share gains through our One Ecolab initiative and accelerating performance in our growth engines, specifically in data centers, microelectronics, life sciences, and Ecolab digital. Additionally, we will implement value pricing that reflects the increasing value Ecolab delivers to customers. The emphasis on data centers and microelectronics positions Ecolab at the heart of the AI revolution's infrastructure needs.

Sustainability achievements are translating into competitive advantages. Water resilience: Continued its work as cofounder of the Water Resilience Coalition (WRC), which has grown to include 40 companies with a combined market capitalization of $5 trillion. As WRC basin champion for California, Ecolab convened the second annual forum of the California Water Resilience Initiative (CWRI), aligning with public sector goals. Renewable energy: Achieved 100% renewable electricity in Ecolab's EU operations, reaching 71% renewable globally and on track to 100% by 2030. These aren't just ESG checkboxes—they're prerequisites for winning contracts with sustainability-conscious corporations.

The outlook remains robust despite macro headwinds. As a result, Ecolab expects full year 2025 adjusted diluted earnings per share to improve further to the $7.42 to $7.62 range, rising 12% to 15% compared with adjusted diluted earnings per share of $6.65 in 2024. Management's confidence in reaching our 20% margin target over the next three years continues to strengthen, suggesting operational improvements are ahead of schedule.

The One Ecolab initiative is delivering tangible results. Our One Ecolab initiative supports these objectives by leveraging our breakthrough innovation, digital technologies, and global service expertise to deliver best-in-class customer performance in their global operations to keep fueling our growth and margin expansion. This integration is creating the operating leverage that will drive margin expansion toward that 20% target.

Innovation continues with strategic investments in emerging technologies. The pest intelligence platform represents a complete reimagining of pest control. This innovative program combines advanced analytics with insight-driven service to enable superior pest elimination for customers while also more effectively leveraging Ecolab's service team. Organic operating income decreased 15% as strong sales growth was more than offset by costs associated with an unfortunate and unusual spike in accidents, compared to Ecolab's historical world class safety levels, and investments in pest intelligence. We expect organic operating income in the first quarter of 2025 to be relatively stable, and for income growth to progressively accelerate through the year as we leverage our investments in pest intelligence to fuel this high-growth, high-margin business.

The macro environment remains challenging but manageable. In the near-term, the global operating environment remains unpredictable, characterized by soft end market demand and impacts from rapidly changing international trade policy. Importantly, with these current macroeconomic assumptions, Ecolab's expectations for 2025 earnings remain unchanged. This resilience in the face of uncertainty demonstrates the defensive characteristics of Ecolab's business model.

Fleet electrification and sustainable aviation fuel initiatives show Ecolab walking the talk on environmental commitments. Fleet electrification: Accelerated efforts to convert Ecolab's North American sales and service fleet to electric vehicles by 2030. Alternative fuels: Collaborated to grow the Minnesota Sustainable Aviation Fuel (SAF) hub alongside the Greater MSP Partnership, Delta Air Lines, Xcel Energy, and Bank of America, aiming to scale SAF production and use. With thousands of vehicles making daily customer visits, this transition will materially impact Ecolab's carbon footprint while potentially reducing operating costs.

XII. Links & Resources

Company Resources: - Ecolab Investor Relations: investor.ecolab.com - 2024 Growth & Impact Report: ecolab.com/corporate-responsibility/growth-and-impact-report - Annual Reports and SEC Filings: investor.ecolab.com/financials/annual-reports

Industry Analysis: - Water Resilience Coalition: ceowatermandate.org/resilience - UN Global Compact Water Mandate: unglobalcompact.org/what-is-gc/our-work/environment/water - Industrial Cleaning Association: issa.com

Historical Context: - Minnesota Historical Society Ecolab Archives: mnhs.org/library/findaids/00309 - Harvard Business School Case Studies on Ecolab (various years) - "Clean: The History of Ecolab" (company-commissioned history)

Sustainability & ESG: - CDP Water Disclosure: cdp.net - Science Based Targets Initiative: sciencebasedtargets.org - Ecolab Water Risk Monetizer: waterriskmonetizer.com

Financial Analysis: - Morningstar Ecolab Analysis: morningstar.com/stocks/xnys/ecl - S&P Capital IQ Reports (subscription required) - Sell-side analyst reports from major investment banks

Technology & Innovation: - Ecolab Digital Platform overview: ecolab.com/digital - Patents database: patents.google.com (search "Ecolab") - Industry 4.0 in cleaning and sanitation research papers

Leadership & Culture: - Doug Baker Harvard Business Review articles - Christophe Beck LinkedIn posts and interviews - Acquired.fm episodes on industrial consolidation strategies

Competitive Intelligence: - Diversey Holdings investor materials - ChemTreat/Danaher water treatment division reports - Regional competitor analysis from industry associations

Books & Long-form Articles: - "The Water Business" by Christopher Gasson - "Cleaning Up: The Transformation of Industrial Services" (Industry analysis) - McKinsey Global Institute reports on water scarcity and industrial efficiency - "From Products to Services: The Ecolab Model" (Stanford Business case study)

Note: This analysis represents an independent business history examination based on public information. It should not be construed as investment advice. Readers should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube