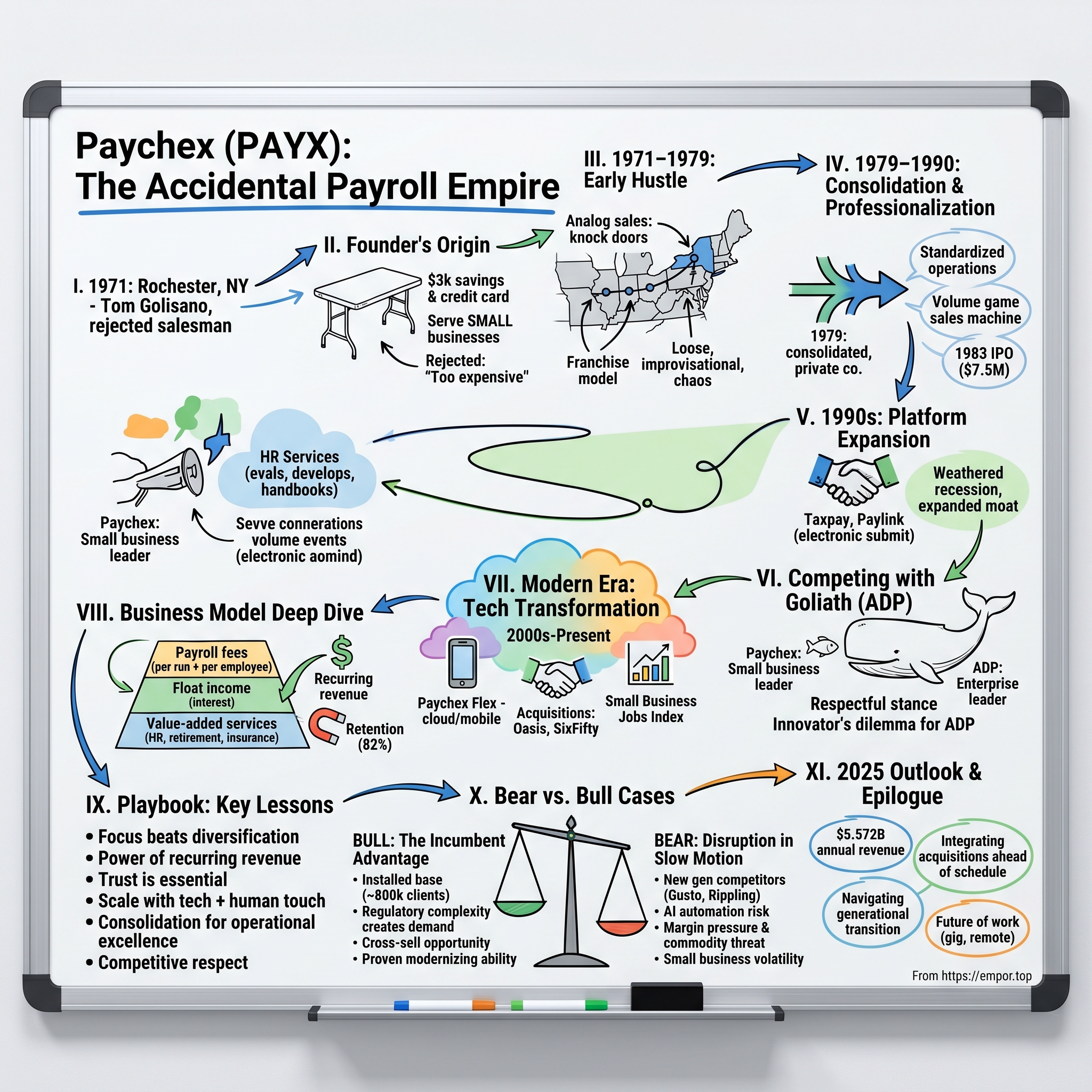

Paychex: The Accidental Payroll Empire

I. Introduction & Episode Roadmap

Picture this: It's 1971 in Rochester, New York. A sales manager at a payroll company walks into his boss's office with what he thinks is a brilliant idea—why not serve small businesses too? The boss laughs him out of the room. "Too expensive to service," he says. "Not worth our time." That rejected salesman, Tom Golisano, walks out with $3,000 in savings and a credit card, and proceeds to build one of America's most enduring business services empires.

Today, Paychex processes payroll for one out of every 11 American private sector workers. The company generates $5.2 billion in annual revenue, manages $13 billion in assets, and sits at number 681 on the Fortune 500 list. Not bad for a business that started with door-to-door sales calls and a folding table in a Rochester suburb. The story of Paychex is fundamentally a story about seeing opportunity where others see only hassle. It's about understanding that in business, the most lucrative markets are often the ones everyone else thinks are too difficult to serve profitably. And perhaps most importantly, it's about the compound power of recurring revenue when you solve a painful problem for millions of customers.

In this deep dive, we'll trace the journey from Tom Golisano's initial rejection to Paychex's current position as 681st on the Fortune 500 list, generating $5.2 billion in revenue and managing $13 billion in assets in 2024. We'll explore how a franchise model gave way to centralized operations, how technology transformed the business, and how the company continues to defend its moat against both established competitors and venture-backed upstarts.

But this isn't just a business history lesson. It's a masterclass in market positioning, operational excellence, and the art of building a business that becomes more valuable with every customer it adds. The payroll processing industry might not be sexy, but as we'll see, it's one of the best business models ever created—sticky customers, predictable revenue, and float income that turns your customers' money into your profit center.

So buckle up. We're about to explore how a macaroni salesman's son built one of America's most enduring business services companies, why small business payroll is actually a brilliant market to dominate, and what the future holds for a company that's both a technology platform and a high-touch service provider. This is the story of Paychex—the accidental empire that processes one out of every 12 American private sector employees' paychecks.

II. Tom Golisano: The Founder's Origin Story

The year is 1971. Richard Nixon is in the White House, "All in the Family" dominates television, and in Rochester, New York, a 29-year-old sales manager is about to learn that sometimes the best business ideas are the ones your boss thinks are stupid.

Tom Golisano wasn't born into privilege. His father sold macaroni for a living, his mother worked as a seamstress, and young Tom grew up in the working-class neighborhoods of Rochester understanding exactly what it meant to make every dollar count. This wasn't the typical pedigree of a future billionaire, but perhaps that's exactly why Golisano could see what the establishment couldn't.

By 1971, Golisano had worked his way up to sales manager at Electronic Accounting Systems (EAS), a payroll processing company that served large corporations. EAS was doing well enough—after all, companies with thousands of employees desperately needed help managing the complexity of payroll taxes, withholdings, and regulatory compliance. The mainframe computers that made this possible cost millions, and the expertise required to operate them was scarce.

But Golisano kept noticing something during his sales calls. For every large company that could afford EAS's services, there were dozens of small businesses—restaurants, retailers, small manufacturers—struggling with the same payroll headaches. They'd spend hours every week calculating wages, figuring out tax withholdings, and filing the endless stream of government forms. One mistake could trigger an audit or penalties that might cripple a small operation.

The entrepreneurial epiphany came not as a lightning bolt but as a persistent itch. Why couldn't small businesses have access to payroll services too? When Golisano pitched the idea to his bosses at EAS, their response was swift and dismissive. The economics would never work. Small businesses couldn't afford the fees necessary to justify the infrastructure investment. The sales costs alone would eat up any potential profit. Forget it, kid. Focus on the big fish.

But Golisano couldn't forget it. He'd done the math differently. Yes, serving small businesses would require a completely different model—lower price points, streamlined operations, and efficient sales processes. But the market was enormous. There were millions of small businesses in America, and virtually none of them had access to professional payroll services. If you could crack the code on serving them profitably, you'd have a market all to yourself.

In 1971, Tom Golisano started the company with only $3,000—his entire savings—and a credit card. He didn't have venture capital. He didn't have a trust fund. He didn't even have a particularly good credit score. What he had was conviction and a willingness to do whatever it took to prove his thesis.

The name he chose was deliberate: Paychex. Not "Payroll Processing Inc." or some other corporate-sounding moniker. The "chex" spelling was playful, approachable—exactly the kind of company a small business owner might trust. This wasn't going to be another intimidating financial services firm. This was going to be the neighborhood payroll guy who understood your business because he was a small business owner too.

Golisano's initial vision was elegant in its simplicity: make payroll outsourcing easy and accessible for small businesses. No complex contracts. No massive upfront investments. Just a simple fee structure that small business owners could understand and afford. He would democratize a service that had been the exclusive domain of large corporations.

The first office was actually Golisano's home in Rochester. The first desk was a folding table. The first employees were Golisano himself and whoever he could convince to help him for free. But what he lacked in resources, he made up for in hustle. Golisano would drive from business to business, knocking on doors, explaining how he could save them time and protect them from costly mistakes.

The pitch was compelling because Golisano understood his customers' pain intimately. He didn't talk about computer processing power or regulatory expertise. He talked about giving small business owners their weekends back. He talked about sleeping better knowing the IRS forms were filed correctly. He talked about having more time to focus on growing the business instead of drowning in paperwork.

These early days established patterns that would define Paychex for decades. First, the company would always maintain a deep empathy for small business owners—understanding their constraints, their fears, and their aspirations. Second, it would prioritize simplicity and accessibility over feature complexity. And third, it would build its business through relentless, face-to-face sales efforts.

What Golisano didn't know in 1971 was that he was pioneering what would become one of the most attractive business models in corporate America: recurring revenue from essential services to a fragmented customer base. But we're getting ahead of ourselves. First, he had to figure out how to scale beyond Rochester, and that would require a strategy as unconventional as his original insight. The franchise model he adopted would spread Paychex across the country—but nearly tear it apart in the process.

III. The Early Hustle: Building a Franchise Network (1971–1979)

Tom Golisano's first year in business was a masterclass in entrepreneurial grit. By day, he was CEO, salesman, and operations manager. By night, he was the delivery guy, personally driving to clients' offices to pick up their payroll data. He'd return home, calculate the withholdings on a basic calculator, type up the checks on a rented typewriter, and then drive back to deliver them. It was hardly scalable, but it proved the concept: small businesses would absolutely pay for payroll services if you made it simple enough.

The company's first name wasn't even Paychex—B. Thomas Golisano established it as PayMaster, a name that would soon create legal complications with existing businesses. But names were the least of his problems. The real challenge was growth. By 1974, Golisano had built a steady business in Rochester, but he was bumping against the limits of what one person could accomplish.

The impetus for expansion came from an unexpected source: two friends approached Golisano independently in 1974, each wanting to start their own payroll business in different cities. Rather than see them as competition, Golisano saw opportunity. If he could help them set up operations using his model, he could expand Paychex's footprint without needing capital he didn't have.

This was the birth of the franchise strategy—though "strategy" might be too generous a term for what was essentially making it up as they went along. The model was loose, almost improvisational. Some partners would be franchisees, paying Golisano for the right to use his systems and brand. Others would be joint ventures, where Golisano would own a piece of the local operation. Still others were somewhere in between, with handshake deals and verbal agreements that would make a corporate lawyer break out in hives.

But it worked—sort of. The franchise model allowed Paychex to spread like wildfire across the Northeast and Midwest. Each franchisee brought local market knowledge, their own capital, and most importantly, their own hustle. They were entrepreneurs themselves, not corporate drones executing a playbook. They understood small business owners because they were small business owners.

The sales approach during this period was gloriously analog. Franchisees would literally walk into every small business in their territory—restaurants, dental offices, small manufacturers, retail shops. The pitch was always the same: "How much time do you spend on payroll every week? What if I told you I could give you that time back for less than you're probably spending on coffee?"

By 1979, Golisano had 17 partners, 11 of them joint ventures, and six franchises. The network was processing payroll for thousands of small businesses across multiple states. Revenue was growing exponentially. From the outside, Paychex looked like a rocket ship.

But inside, it was chaos. Each franchise operated differently. Some maintained high service standards; others cut corners. Pricing was inconsistent—one franchise might charge $5 per payroll while another charged $15 for the same service. Customer data was scattered across dozens of independent operations with no central oversight. The technology infrastructure, such as it was, consisted of whatever each franchisee had cobbled together.

The franchise agreements themselves were a mess. Some were written on napkins (literally). Others had contradictory terms or unclear territory boundaries. Franchisees would poach each other's clients. Quality control was nearly impossible. Golisano would get calls from angry customers in cities he'd never even visited, complaining about service from franchisees he barely knew.

By 1979, the situation was becoming untenable. The loose organization that had enabled rapid growth was now threatening to destroy the company. Competitors were starting to notice the small business market. ADP, the 800-pound gorilla of payroll processing, was beginning to make noises about serving smaller clients. If Paychex was going to survive, it needed to transform from a collection of independent operations into a real company.

The decision to consolidate wasn't easy. Many of the franchisees had built successful businesses. They liked their independence. They'd taken the risks, done the hard work of building their local markets. Why should they give up control? The negotiations were brutal. Golisano had to convince, cajole, and sometimes strongarm his partners into selling their operations back to the parent company.

The operation's 18 franchises and partnerships were eventually consolidated into one private company in 1979. Some franchisees became employees. Others took buyouts and left. A few fought the consolidation and had to be bought out at premium prices. It was expensive, messy, and exhausting.

But it was also necessary. The consolidated Paychex that emerged in 1979 was a fundamentally different animal than the loose confederation it had been. It had standardized operations, consistent pricing, and unified technology infrastructure. It had professional management and real corporate governance. Most importantly, it had the foundation to scale efficiently.

The franchise era of Paychex was over, but it had served its purpose. It had proven that small business payroll was a viable market. It had established Paychex's presence across multiple geographic markets. And it had generated enough revenue and customers to make consolidation possible.

Looking back, the franchise years seem almost quaint—a bunch of entrepreneurs with calculators and typewriters building what would become a Fortune 500 company. But they established something crucial: Paychex's DNA as a company that understood small business because it was built by small business owners, for small business owners. That DNA would prove to be its greatest competitive advantage as it entered its next phase—going public and competing with the giants of the payroll industry.

IV. Going Public & Professionalization (1979–1990)

The newly consolidated Paychex of 1979 was like a teenager who'd just had a growth spurt—all gangly limbs and unrealized potential. Tom Golisano had successfully herded his cats into a single company, but now came the hard part: building a real business that could compete with established players and scale efficiently. The next decade would transform Paychex from a scrappy startup into a public company with institutional credibility.

The first order of business was sales—specifically, turning the ad hoc, door-to-door hustle of the franchise era into a repeatable, scalable machine. Golisano knew that small business acquisition was a volume game. You needed lots of salespeople making lots of calls to generate the steady stream of new clients necessary for growth. But you also needed those salespeople to be productive, or the economics would collapse.

The sales transformation was remarkable. By 1982, the average Paychex salesperson was bringing in 100 clients a year—a staggering number that would make enterprise software sales teams weep with envy. How? The company had cracked the code on small business sales: keep it simple, make it fast, and focus relentlessly on volume over deal size.

Salespeople were trained to close deals in a single visit. No proof of concepts. No committee reviews. No months-long sales cycles. You walked in, demonstrated value, and walked out with a signed contract—or you moved on to the next prospect. The average new client might only represent $2,000 in annual revenue, but when you're signing 100 of them a year, the math works.

In 1983, the company (ticker symbol: PAYX) became a public company via an initial public offering. The IPO was modest by today's standards—Paychex raised just $7.5 million—but it represented a crucial transition. Public markets meant accountability, transparency, and access to capital for growth. It also meant Golisano had to learn to manage for quarterly earnings while building for the long term.

The public markets initially didn't know what to make of Paychex. Here was a company serving the smallest of small businesses—clients that most financial services firms wouldn't touch with a ten-foot pole. The average Paychex client had fewer than 15 employees. How could you build a sustainable business on such a fragmented, seemingly risky customer base?

But Golisano understood something the Wall Street analysts initially missed: small businesses were actually incredibly sticky customers. Once you handled their payroll, you became essential to their operations. Switching providers meant risking errors, learning new systems, and potentially missing tax deadlines. The retention rates were extraordinary—over 80% annually, despite the higher failure rate of small businesses compared to large corporations.

The operational infrastructure built during this period was deliberately unsexy but incredibly effective. Paychex invested heavily in standardized processes, quality control, and error prevention. Every step of the payroll process was documented, measured, and optimized. The company became fanatical about accuracy—a single missed tax payment could destroy a small business's trust forever.

Growth came both organically and through strategic acquisitions. In 1987, Paychex bought Purchase Payroll, a Minneapolis company that brought 900 clients overnight. But unlike the roll-up strategies common in business services, Paychex was selective about acquisitions. Each had to bring either geographic expansion, new capabilities, or a client base that fit the Paychex model perfectly.

The late 1980s also saw Paychex begin to expand beyond pure payroll processing. In 1987, the company opened a Benefit Services division, helping clients track and manage employee benefit plans. This wasn't just about revenue diversification—it was about deepening client relationships. The more services a client used, the stickier they became.

By 1990, Paychex had 335 sales representatives and around 125,000 clients. The company had grown from Golisano's one-man operation to a sophisticated enterprise with hundreds of employees and a systematic approach to growth. Revenue had grown from practically nothing to over $100 million annually.

But perhaps the most important development of this period was cultural. Paychex developed a unique corporate personality—professional enough to be trusted with critical business functions, but humble enough to serve the smallest businesses with respect and attention. Employees were taught to see themselves as partners to small business owners, not vendors.

The company also maintained its founder's scrappy mentality despite its public company status. Expenses were watched carefully. Offices were functional, not fancy. Marketing was minimal—the sales force was the marketing department. Every dollar saved was a dollar that could be invested in service improvement or sales expansion.

By 1990, Paychex had proven something remarkable: you could build a large, profitable, public company by serving the smallest businesses in America. The infrastructure was in place. The model was proven. The sales engine was humming. But the real growth was still to come. The 1990s would bring new challenges—economic recession, technological change, and increased competition—but also opportunities to transform Paychex from a payroll processor into something much more valuable: a comprehensive platform for small business HR and financial services. The foundation built in the 1980s would prove strong enough to support ambitions that even Tom Golisano hadn't initially imagined.

V. The Platform Expansion: Beyond Payroll (1990s)

The 1990s began with a recession that should have crushed Paychex. Small businesses were failing at alarming rates. Unemployment was rising. The companies that survived were cutting costs wherever possible. For a company dependent on small business health, this should have been catastrophic. Instead, 1991 saw record sales of $137 million and record earnings of $9.6 million.

How did Paychex thrive during a downturn that destroyed so many of its clients? The answer revealed the hidden genius of the business model. When times get tough, small business owners have even less time to deal with payroll complexity. They need to focus on survival, not tax forms. And at $20-30 per payroll, Paychex was a bargain compared to the cost of errors or the time required to do it yourself. The recession actually accelerated outsourcing adoption.

But Golisano and his team saw opportunity beyond just weathering the storm. If Paychex could become indispensable for payroll, why not for other back-office functions that small businesses struggled with? In 1991, the company formed a Human Resource Services division, offering clients a package that sounded almost too good to be true: employee evaluation tools, employee handbooks, insurance services, customized job descriptions, and other benefits that typically only large corporations could afford.

The HR expansion was brilliant for several reasons. First, it leveraged the existing sales force—the same rep who sold you payroll could now sell you HR services. Second, it dramatically increased revenue per client without proportionally increasing service costs. Third, and most importantly, it made switching away from Paychex even more painful. You weren't just changing payroll providers; you were dismantling your entire HR infrastructure.

The technology investments of this period were transformative. Remember, this was the era when the internet was just beginning to enter mainstream business use. Most small businesses still operated on paper and fax machines. Paychex saw the opportunity to leapfrog competitors by investing aggressively in digital capabilities.

The introduction of Taxpay was a game-changer. This service handled all federal, state, and local payroll tax deposits and filings—the most complex and error-prone part of payroll processing. By 1991, the company had around 26,000 Taxpay customers. That number rose to over 50,000 by 1993. Small business owners could finally stop worrying about tax deadlines and penalty notices.

Then came Paylink in 1993, which allowed clients to submit payroll information electronically rather than over the phone or via paper forms. This might seem trivial today, but it was revolutionary for small businesses that were just getting their first computers. It reduced errors, saved time, and made Paychex feel cutting-edge rather than old-fashioned.

The acquisition strategy during the 1990s was surgical and strategic. Paychex acquired Pay-Fone in 1995, a company that had developed technology for phone-based payroll data entry. In 1996, the company acquired Olsen Computer Systems and National Business Systems, adding both technology capabilities and geographic reach.

Each acquisition was integrated carefully into the Paychex model. Unlike many acquirers who maintain separate brands and operations, Paychex absorbed these companies completely. Their clients became Paychex clients. Their technology was integrated into the Paychex platform. Their best employees were retained and trained in the Paychex way. This wasn't empire building—it was capability accumulation.

By 1997, the company had secured five consecutive years of over 30% earnings growth—a stunning achievement for a company of Paychex's size. Wall Street was finally beginning to understand what Golisano had known all along: small business services, done right, could be incredibly profitable and sustainable.

The international expansion attempts of this period were less successful but instructive. Paychex tried to replicate its model in Europe, discovering that payroll processing was far more country-specific than anticipated. Different labor laws, tax systems, and business cultures made it impossible to simply export the American model. The company would eventually succeed internationally, but it would take years of patient investment and local adaptation.

What's remarkable about the 1990s expansion is how disciplined it remained. While dot-com companies were burning cash on Super Bowl ads and lavish parties, Paychex maintained its frugal culture. Marketing remained minimal. Offices remained functional. The focus remained relentlessly on service delivery and sales execution.

The company also began to recognize the value of its float—the money it held between collecting from clients and paying out wages and taxes. With interest rates relatively high during much of the 1990s, this float generated significant income. Paychex was essentially running a bank alongside its service business, earning interest on billions of dollars of other people's money.

By the end of the 1990s, Paychex had transformed from a payroll processor into what we'd now call a platform company. It offered a suite of integrated services that small businesses could access through a single relationship. The recurring revenue model, combined with high retention rates and increasing revenue per client, created a compound growth machine that seemed unstoppable.

But success breeds competition. As Paychex proved the viability of the small business market, others took notice. The next phase of the company's evolution would be defined not just by growth, but by defending its territory against both traditional competitors and new technology-enabled entrants. The battle for small business payroll was about to intensify.

VI. The ADP Dynamic: Competing Against Goliath

The elevator pitch was killing him. Every single time Tom Golisano walked into a prospect's office in the early days, the conversation would go something like this: "So you do payroll? Like ADP?" It was maddening. Here he was, trying to build something different, something specifically for small businesses, and everyone wanted to compare him to the 800-pound gorilla that had been ignoring them for years.

ADP (Automatic Data Processing) was everything Paychex wasn't. Founded in 1949, it was already a billion-dollar company by the time Golisano was going door-to-door in Rochester. ADP served Fortune 500 companies with complex, customized solutions. Their sales cycles were measured in months. Their implementations required teams of consultants. Their minimum client size was larger than most of Paychex's biggest customers.

But rather than run from the comparison, Golisano developed a response that would become Paychex doctrine. When prospects brought up ADP, he'd lean in with a smile: "Absolutely! ADP is the leader in large-company payroll processing, and we are the leader in small-business payroll processing. In fact, without ADP's pioneering work, Paychex wouldn't exist. They proved that payroll outsourcing makes sense. We just made it accessible for businesses like yours."

This wasn't just clever positioning—it was psychological jujitsu. By acknowledging ADP's dominance in the enterprise market, Golisano removed them as a direct competitor in the prospect's mind. ADP was for the big guys; Paychex was for businesses like theirs. It was a different category entirely.

The strategy worked so well that Golisano made it company policy: no Paychex employee should ever disparage the competition. "Competition is good," he would tell his sales teams. "Good competition is better. It validates the market. It educates customers. It keeps us sharp."

This respectful stance toward competition was unusual in the aggressive world of B2B sales, but it had practical benefits. When ADP salespeople bad-mouthed Paychex as "too small" or "unsophisticated," they looked petty. When Paychex salespeople spoke respectfully about ADP while highlighting their own strengths, they looked professional and confident.

The real competitive dynamics were more complex than the public positioning suggested. By the late 1980s and early 1990s, ADP had noticed Paychex's success in the small business market. They launched their own small business division, trying to compete directly. But they faced the classic innovator's dilemma—their entire organization was built to serve large clients with high-touch, high-margin services. Serving small businesses profitably required a completely different operating model.

ADP's small business efforts were half-hearted at best. Their sales force was accustomed to long sales cycles and big commission checks. Asking them to close $2,000 annual contracts felt like a demotion. Their technology infrastructure was built for complexity and customization, not the simplicity and standardization small businesses needed. Their cost structure made it nearly impossible to serve small clients profitably at Paychex's price points.

Meanwhile, Paychex faced its own challenges competing upmarket. As successful small businesses grew, they would eventually outgrow Paychex's services and graduate to ADP or other enterprise providers. This created a natural ceiling on client lifetime value. Paychex tried various strategies to serve larger clients, but struggled to compete with ADP's sophisticated capabilities and enterprise sales force.

The solution was elegant: focus and differentiation. Rather than trying to be all things to all businesses, Paychex doubled down on being the absolute best provider for small businesses. They defined their sweet spot precisely—businesses with 10-100 employees—and optimized everything for that segment.

This focus allowed Paychex to build competitive moats that even ADP couldn't cross. Their sales force became experts at small business needs and concerns. Their technology was designed for simplicity and ease of use, not flexibility and customization. Their service model assumed clients had no HR department and needed hand-holding through basic tasks.

The market positioning became even clearer over time. ADP was IBM—powerful, sophisticated, expensive. Paychex was Apple (in the pre-iPhone era)—simpler, friendlier, more accessible. Both companies thrived because they served different needs for different customers.

The competitive respect Golisano preached had another unexpected benefit: talent flow. As Paychex grew and professionalized, it was able to recruit talented executives and salespeople from ADP who understood the industry but wanted to be part of building something new. These transfers brought valuable knowledge and relationships while maintaining professional relationships between the companies.

By the 2000s, the competitive landscape had evolved into a stable détente. ADP dominated the enterprise market with 70%+ market share. Paychex owned the small business segment with similar dominance. Both companies were hugely profitable. Both grew steadily. Neither seriously threatened the other's core market.

But this comfortable dynamic wouldn't last forever. The rise of cloud computing and software-as-a-service would bring new competitors—venture-backed startups that didn't respect the old boundaries. Companies like Gusto, Rippling, and others would challenge both ADP and Paychex with modern technology and aggressive pricing. The gentlemanly competition between the two incumbents would give way to a more chaotic battle for the future of payroll. But that's a story for another section.

VII. The Modern Era: Technology Transformation (2000s–Present)

The millennium turned with Paychex at the height of its powers. In fiscal 2001, the company posted its 11th consecutive year of record revenues and net income. The business model seemed bulletproof—recurring revenue, high retention, steady growth. But underneath this success, tectonic shifts were beginning that would force Paychex to reinvent itself or risk irrelevance.

The first shock was personal. In 2004, Tom Golisano stepped down as CEO after 33 years at the helm. The founder who had knocked on doors, consolidated the franchises, taken the company public, and built a Fortune 500 company was passing the torch. His successor, Jonathan Judge, faced a daunting challenge: modernizing a company built on high-touch service for the digital age.

The technology transformation wasn't optional—it was existential. A new generation of small business owners was coming of age, and they expected their business services to work like consumer internet products. They wanted to submit payroll from their phones. They wanted employee self-service portals. They wanted real-time reporting and analytics. The old model of calling your payroll specialist and reading numbers over the phone suddenly seemed as antiquated as carrier pigeons.

Paychex's response was measured but comprehensive. Rather than trying to out-Silicon Valley the startups, they focused on bringing modern technology to their existing strengths. The rollout of Paychex Flex, their cloud-based platform, was gradual and careful. Existing clients could migrate at their own pace. New features were added incrementally. The high-touch service model remained available for clients who needed it. The major acquisition came in December 2018, when Paychex closed on its acquisition of Oasis Outsourcing Acquisition Corporation for $1.2 billion. This wasn't just about size—Oasis, headquartered in West Palm Beach, Florida, served more than 8,400 clients across all 50 states with its HR solutions, employee benefits, payroll administration, and risk management services. The acquisition represented Paychex's most aggressive move into the Professional Employer Organization (PEO) space, where it essentially becomes a co-employer with its clients, taking on more comprehensive HR responsibilities.

The data analytics push came with an interesting twist. In 2014, Paychex and IHS Markit launched a Small Business Jobs Index that measures the health of businesses employing 50 people or less. This wasn't just corporate citizenship—it was brilliant marketing. By becoming the authoritative source on small business employment trends, Paychex positioned itself as the thought leader in its market. Every month, financial media would cite Paychex data, providing free publicity and reinforcing its position as the small business expert.

Leadership transitions continued to shape the modern era. John Gibson has been CEO of Paychex since October 2022, taking the helm during a period of intense technological change and competitive pressure. Gibson faced the challenge of maintaining Paychex's high-touch service model while meeting the expectations of a new generation of digitally native business owners. The most recent strategic move came in May 2025, when Paychex acquired SixFifty, the legal tech unit of U.S. law firm Wilson Sonsini Goodrich & Rosati, in an all-cash deal worth between $70 million and $85 million. SixFifty specializes in automated employment law compliance and documentation—a perfect complement to Paychex's HR services. This acquisition shows Paychex isn't just responding to technological change; it's anticipating where small businesses will need help next.

The competitive landscape has transformed dramatically. While the old rivalry with ADP continues, new challengers have emerged from Silicon Valley. Companies like Gusto, Rippling, and others have raised billions in venture capital to attack the payroll market with modern, API-first platforms. These companies promise instant setup, beautiful interfaces, and integration with hundreds of other business tools.

Paychex's response has been measured but effective. Rather than trying to out-startup the startups, they've leveraged their advantages: trust built over decades, comprehensive compliance expertise, and the ability to provide human support when technology isn't enough. They've modernized their technology stack while maintaining the high-touch service that many small business owners still crave.

The financial performance has remained remarkably consistent. Despite economic turbulence, pandemic disruptions, and competitive pressures, Paychex has continued to grow revenue and profits. The recurring revenue model that Golisano pioneered continues to generate predictable cash flows, while the float income provides a hedge against operational challenges.

But perhaps the most interesting aspect of the modern era is how Paychex has managed to remain relevant across multiple technological revolutions. From mainframes to PCs to the internet to mobile to cloud to AI—each wave could have disrupted Paychex out of existence. Instead, the company has adapted, evolved, and emerged stronger.

The secret seems to be understanding that technology is a tool, not the product. Small business owners don't buy payroll processing; they buy peace of mind. They buy time to focus on their business. They buy protection from costly mistakes. As long as Paychex remembers this fundamental truth, it can continue to thrive regardless of how the technology changes.

Looking ahead, the challenges are real. Artificial intelligence promises to automate much of what Paychex does. Cryptocurrency could revolutionize how wages are paid. The gig economy is changing the very nature of employment. But if history is any guide, Paychex will find a way to turn these disruptions into opportunities. After all, complexity is good for business when your business is simplifying complexity for others.

VIII. Business Model Deep Dive

To truly understand Paychex's enduring success, you need to appreciate the elegant simplicity of its business model. On the surface, it looks straightforward: process payroll, charge a fee, repeat. But underneath lies a sophisticated financial machine that generates multiple revenue streams, compounds value over time, and creates switching costs that would make a software company jealous.

Paychex's revenue model is diversified and hinges on a recurring revenue structure that Wall Street loves. The core payroll processing service generates predictable, subscription-like revenue. Clients typically pay per payroll run—whether weekly, bi-weekly, or monthly—plus a per-employee fee. This means Paychex benefits both from client growth (more employees) and economic growth (more businesses). It's a beautiful double exposure to economic expansion.

But here's where it gets interesting. Beyond the subscription fees, Paychex generates significant revenues from ancillary services like retirement plan management and insurance brokerage. These additional services don't just add revenue—they deepen the client relationship. The company saw a 10% increase in revenue from these value-added services in 2022, demonstrating the power of the cross-sell.

The real magic, though, is in the float. When Paychex collects money from employers to pay employees and taxes, there's a gap—sometimes days, sometimes weeks—between collection and disbursement. During that time, Paychex invests the money and keeps the interest. In a high-interest-rate environment, this float income can be substantial. Think of it as running a bank without the banking regulations.

The numbers tell the story of operational excellence. Paychex maintains a high gross profit margin, reflecting its ability to efficiently deliver services. The gross profit margin for fiscal year 2024 was approximately 68%. That's software-like margins for what many consider a service business.

Customer retention is where the model really shines. The consistent focus on customer satisfaction is reflected in their high customer retention rate of 82% according to their internal metrics. When you consider that small businesses fail at higher rates than large corporations, this retention rate is extraordinary. It means that when Paychex loses a customer, it's usually because the business failed or was acquired, not because they switched providers.

The network effects are subtle but powerful. Every client that joins makes Paychex's compliance database more robust. Every tax filing improves their error detection algorithms. Every customer service call trains their support team. The millionth client costs far less to serve than the first, but pays the same price. This is the beauty of scale in a standardized service business.

The technology investments have transformed the unit economics. What once required phone calls and manual data entry can now be completed through self-service portals. Clients can run payroll in minutes from their phones. Employees can access pay stubs and tax forms without calling HR. Each automation reduces service costs while improving customer satisfaction.

The regulatory moat deserves special attention. Payroll processing isn't just about calculating wages—it's about navigating a maze of federal, state, and local tax requirements. There are over 10,000 tax jurisdictions in the United States, each with its own rules and rates. Staying compliant requires constant monitoring of regulatory changes and updating systems accordingly. This complexity is Paychex's friend—the harder it is to do payroll correctly, the more valuable their service becomes.

The sales efficiency has improved dramatically over the decades. While the company still employs a large direct sales force, digital marketing and channel partnerships have reduced customer acquisition costs. Approximately 50% of new small-market payroll clients (excluding business acquisitions) come from referral sources, primarily CPAs and banks who recommend Paychex to their clients.

The competitive dynamics create interesting pricing power. Small businesses are remarkably price-insensitive when it comes to payroll. The service typically costs less than 1% of total payroll expenses, but the consequences of errors can be catastrophic. This means Paychex can raise prices modestly each year without significant customer pushback—a steady source of organic revenue growth.

The capital efficiency is remarkable. Unlike manufacturing or retail businesses, Paychex doesn't need factories, inventory, or expensive equipment. The primary assets are people, technology, and reputation. This capital-light model means that growth doesn't require proportional investment, allowing for strong cash flow generation and generous shareholder returns.

The platform economics work in Paychex's favor. Once a client is using payroll services, adding HR services, retirement plan administration, or insurance is relatively frictionless. The marginal cost of serving additional products to existing clients is minimal, while the revenue per client can double or triple. It's the classic "land and expand" strategy, executed at scale.

What makes this business model particularly resilient is its countercyclical elements. During economic downturns, businesses need help navigating layoffs, furloughs, and changing regulations. During expansions, they need help with hiring, benefits administration, and compliance. Paychex wins either way, though obviously growth is stronger in good times.

The subscription nature of the revenue, combined with high retention rates and increasing revenue per client, creates a compound growth machine. Each year starts with 80%+ of the previous year's revenue already locked in. Growth comes from new clients, increased penetration of existing clients, and modest price increases. It's predictable, sustainable, and surprisingly difficult to disrupt. This business model has survived multiple recessions, technology revolutions, and competitive attacks—and emerged stronger each time.

IX. Playbook: Key Business Lessons

The Paychex story offers a masterclass in building an enduring business, with lessons that extend far beyond payroll processing. These aren't just historical curiosities—they're principles that explain why some companies thrive for decades while others flame out after a few years of growth.

Focus beats diversification: Dominating small business payroll

Tom Golisano could have tried to serve everyone from sole proprietors to Fortune 500 companies. Instead, he defined his market with laser precision: businesses with 10-100 employees. This wasn't limiting—it was liberating. Every product decision, every sales training, every marketing message could be optimized for this specific segment. While competitors tried to be everything to everyone, Paychex became the undisputed champion of a massive but focused market.

The lesson here is counterintuitive in our age of platform companies and ecosystem plays. Sometimes the best strategy is to do one thing extraordinarily well rather than many things adequately. Paychex proved you could build a Fortune 500 company by saying "no" to opportunities that didn't fit your core focus.

The power of recurring revenue in B2B services

Before SaaS was a term, Paychex understood the beauty of recurring revenue. Payroll isn't a one-time purchase—it's an ongoing need that repeats as long as a business has employees. This predictability transforms everything about the business: valuation multiples increase, cash flow becomes predictable, and growth compounds rather than resets each quarter.

But Paychex took it further by making the recurring revenue "sticky." Unlike a software subscription you might forget you have, payroll is mission-critical. You can't just skip a month. This combination of recurring revenue plus high switching costs creates a business model that's nearly impossible to disrupt.

Building trust in a trust business

Golisano understood something profound: any aspiring entrepreneur had better learn to sell an idea, product, or service. "Nothing happens in a company until someone sells something," he writes. But in payroll, you're not just selling a service—you're selling trust. Clients are literally giving you their money and trusting you to pay their employees correctly and on time.

Paychex built trust through consistency, not flash. Simple contracts. Transparent pricing. No surprises. When mistakes happened (and they always do), Paychex would make it right immediately, often eating the cost of errors even when they weren't at fault. This wasn't weakness—it was a long-term investment in reputation that paid dividends in retention and referrals.

Scaling through technology while maintaining high-touch service

The conventional wisdom says you must choose: either be high-tech or high-touch. Paychex refused to accept this false choice. They invested aggressively in technology to improve efficiency and accuracy, but never abandoned the human element that small business owners valued.

The key insight was that technology should enhance human service, not replace it. Automation handled the routine tasks, freeing service representatives to focus on problem-solving and relationship building. When competitors went fully digital, they lost the trust and loyalty that comes from human connection. When others remained fully manual, they couldn't compete on price or scale.

The franchise-to-consolidation playbook

The early franchise model of Paychex offers a fascinating template for market entry. When you lack capital but have a proven model, franchising lets you scale quickly using other people's money and effort. But Golisano also recognized when the franchise model had outlived its usefulness. The consolidation in 1979 was painful and expensive, but necessary for the next phase of growth.

This pattern—using a decentralized model for rapid expansion, then consolidating for operational excellence—has been repeated successfully by companies from Waste Management to Amazon (with their third-party sellers). The key is timing the transition correctly and having the courage to disrupt your own successful model before someone else does.

Competing respectfully: The Golisano doctrine on competition

Perhaps the most unusual aspect of Paychex's strategy was its respectful stance toward competition. In an era of combative business leaders and scorched-earth competition, Golisano preached and practiced competitive respect. Never disparage competitors. Acknowledge their strengths. Focus on your own differentiation.

This wasn't just good manners—it was good business. By positioning ADP as the leader in enterprise payroll while Paychex owned small business, both companies could thrive without destructive price wars. It also made it easier to recruit talent from competitors and maintain professional relationships across the industry.

The compound effect of operational excellence

Paychex never had a breakthrough product or revolutionary technology. Instead, they won through relentless operational improvement. Each year, they got a little better at sales efficiency, a little better at service delivery, a little better at cost management. These small improvements compounded over decades into an insurmountable competitive advantage.

The lesson is that sustainable competitive advantages rarely come from big breakthroughs. They come from doing the basics extraordinarily well, consistently, for a very long time. It's not sexy, but it works.

Market timing and patience

Golisano started Paychex in 1971, but the company didn't go public until 1983 and didn't hit real scale until the 1990s. This wasn't a failure of execution—it was patience. The small business market needed time to mature, to understand the value of outsourcing, to trust a third party with payroll.

Too many entrepreneurs try to force market timing, burning capital to educate customers who aren't ready to buy. Paychex grew with its market, never getting too far ahead of customer readiness. Sometimes the best strategy is to build steadily and let the market come to you.

These lessons from Paychex transcend industry boundaries. Whether you're building a software company, a service business, or something entirely different, the principles remain valuable: focus on a specific market, build recurring revenue with high switching costs, invest in both technology and human service, respect your competition, and execute with patience and operational excellence. It's not a formula for overnight success, but it is a blueprint for building a business that lasts.

X. Bear vs. Bull Case Analysis

Bull Case: The Incumbent Advantage

The optimists have compelling data on their side. Paychex has more than 100 offices serving approximately 800,000 payroll clients in the U.S. and Europe, representing a massive installed base that generates predictable, recurring revenue. This isn't just about size—it's about the competitive moat that comes from serving one out of every 12 American private sector employees.

The regulatory complexity argument is particularly powerful. Payroll and HR compliance is becoming more, not less, complicated. New regulations around paid family leave, minimum wage variations, overtime rules, and tax requirements create constant challenges for small businesses. Each new regulation makes Paychex's services more valuable, not less. It's a perverse dynamic where government complexity becomes a tailwind for the business.

The cross-selling opportunity remains largely untapped. Most Paychex clients still only use core payroll services. As these businesses grow and face new challenges—retirement plan administration, health insurance management, HR compliance—Paychex is perfectly positioned to expand wallet share. The lifetime value of a client who uses multiple services is multiples higher than a payroll-only client.

The technology investments are starting to pay dividends. While Paychex may not have the slickest interface, their technology is robust, reliable, and comprehensive. They've successfully migrated to the cloud, launched mobile apps, and integrated AI-powered features without disrupting their existing client base. This is harder than it looks—many legacy companies have failed attempting similar transformations.

The acquisition strategy provides optionality. With a strong balance sheet and consistent cash generation, Paychex can acquire new capabilities or eliminate competitive threats. The Oasis acquisition proved they can successfully integrate large deals. The SixFifty acquisition shows they're thinking ahead about where small businesses will need help next.

The macroeconomic sensitivity is overstated. Yes, Paychex is exposed to employment levels and small business formation. But payroll processing is needed regardless of economic conditions. During downturns, the complexity of layoffs, furloughs, and regulatory changes can actually increase demand for professional services.

Bear Case: Disruption in Slow Motion

The pessimists point to real threats that shouldn't be dismissed. The new generation of competitors—Gusto, Rippling, Deel, and others—aren't just competing on technology. They're reimagining the entire experience of business administration. These companies offer instant setup, beautiful interfaces, and seamless integrations with hundreds of other tools. For a generation of entrepreneurs raised on consumer internet products, Paychex can feel antiquated.

The technology disruption risk is real and accelerating. AI could automate much of what Paychex does today. Why do you need a payroll processor when AI can handle tax calculations, compliance monitoring, and filing? The human expertise that Paychex provides could become less valuable as AI becomes more sophisticated.

The small business market is inherently volatile. Small businesses fail at high rates, and economic downturns hit them disproportionately hard. A recession that culls 20% of small businesses would directly impact Paychex's revenue. Unlike enterprise-focused ADP, Paychex can't rely on a few large, stable clients to weather storms.

The margin pressure is building. As competition intensifies, pricing power erodes. New entrants are willing to operate at losses to gain market share, subsidized by venture capital. While Paychex has to maintain margins to satisfy public market investors, competitors can prioritize growth over profitability. This asymmetry is dangerous in the long term.

The platform migration challenge is more difficult than it appears. Moving hundreds of thousands of clients from legacy systems to modern platforms without disruption is extraordinarily complex. Every migration risks client defection. Meanwhile, new clients increasingly expect modern, API-first platforms that integrate seamlessly with their other tools.

The talent war favors tech companies. The best software engineers, product managers, and designers want to work at high-growth tech companies, not established financial services firms. While Paychex has deep domain expertise, they may struggle to attract the technical talent needed to compete with venture-backed startups.

The commoditization threat is real. As payroll processing becomes increasingly automated, it risks becoming a commodity—a race to the bottom on price. The value-added services that generate higher margins might also face pressure as specialized competitors emerge for each vertical.

The Balanced View

The truth, as always, lies somewhere in between. Paychex faces real threats from technological disruption and new competition, but they also have enormous advantages in terms of scale, trust, and expertise. The company has survived multiple waves of disruption before—from PCs to the internet to mobile to cloud. Each time, pessimists predicted their demise. Each time, they adapted and emerged stronger.

The key question isn't whether Paychex will face challenges—they will. It's whether their advantages (customer relationships, regulatory expertise, operational excellence) will prove more durable than their disadvantages (technical debt, innovator's dilemma, cultural inertia).

History suggests betting against incumbents with recurring revenue, high switching costs, and strong competitive moats is dangerous. But history also shows that disruption, when it comes, can happen faster than anyone expects. The next decade will test whether Paychex can once again reinvent itself for a new era, or whether this time, the disruptors will finally win.

XI. Epilogue & Looking Forward

Standing at the end of 2025, Paychex occupies a fascinating position in American business. The company that Tom Golisano started with $3,000 and a folding table now generates $5.572 billion in annual revenue for the twelve months ending May 31, 2025, a 5.56% increase year-over-year. The quarterly revenue for the quarter ending May 31, 2025 was $1.427B, a 10.21% increase year-over-year, demonstrating accelerating growth momentum.

The financial performance tells a story of consistent execution. Total revenues of $1.4 billion surpassed the consensus estimate by a slight margin and gained 10% from the year-ago quarter. More importantly, the company continues to demonstrate pricing power and operational leverage, with adjusted operating income growing faster than revenue.

Current CEO John Gibson faces a transformed competitive landscape. The old bilateral competition with ADP has given way to a multi-front battle. On one side, venture-backed startups attack with modern technology and aggressive pricing. On the other, enterprise software companies expand into HR and payroll as part of broader platform plays. Meanwhile, the traditional competitors continue to evolve and compete.

The strategic positioning for the next decade revolves around three key questions. First, can Paychex maintain its dominance in the small business segment while successfully moving upmarket? The company now serves approximately 800,000 payroll clients, but the opportunity to expand wallet share within this base remains substantial.

Second, how will artificial intelligence reshape the payroll and HR services industry? AI could automate much of what Paychex does today, but it could also enable new services that weren't previously possible. The company's acquisition of SixFifty suggests they're thinking about AI as an opportunity rather than just a threat—using it to provide automated legal compliance and documentation that small businesses desperately need.

Third, can Paychex successfully navigate the generational transition in business ownership? As millennials and Gen Z entrepreneurs start more businesses, their expectations for business services are fundamentally different. They expect instant setup, beautiful interfaces, and seamless integrations. Paychex must appeal to this new generation while maintaining the trust of their existing base.

The macro environment presents both challenges and opportunities. The continued complexity of employment regulations—from minimum wage variations to paid leave requirements to tax changes—creates ongoing demand for professional payroll services. Every new regulation makes DIY payroll more risky and professional services more valuable.

The future of work itself is evolving. The gig economy, remote work, and hybrid employment models create new complexities that Paychex must address. A company that was built to serve traditional employer-employee relationships must adapt to serve businesses with contractors, freelancers, and distributed teams.

What would Tom Golisano think of Paychex today? He'd probably be amazed at the scale—800,000 clients, billions in revenue, Fortune 500 status. But he'd likely recognize the fundamental business: helping small business owners focus on their business by taking payroll off their plate. The technology has changed, the scale has changed, but the core value proposition remains remarkably consistent.

The investment case for Paychex ultimately comes down to a bet on small business America. As long as entrepreneurs keep starting businesses, as long as those businesses need employees, and as long as payroll remains complex, Paychex has a role to play. The company has survived and thrived through multiple recessions, technology revolutions, and competitive attacks.

Looking forward, Paychex seems well-positioned but not invulnerable. They have the scale, expertise, and financial strength to adapt to whatever comes next. But adaptation isn't guaranteed. The company must continue to evolve, to invest in technology while maintaining human touch, to serve new types of businesses while retaining existing clients.

The next decade will test whether the Paychex model—built on recurring revenue, operational excellence, and deep customer relationships—can survive the age of AI, the expectations of digital natives, and the continued evolution of work itself. History suggests betting against them would be unwise. But history also shows that in technology, things can change very quickly.

The story of Paychex isn't finished. In many ways, it's just entering its most interesting chapter. The accidental empire that Tom Golisano built must now prove it can thrive in a world he could never have imagined when he knocked on his first door in 1971. For investors, employees, and the millions of Americans whose paychecks flow through Paychex systems, the next chapter promises to be fascinating to watch.

XII. Recent News

The payroll processing industry continues to evolve rapidly, with consolidation, technological innovation, and changing workforce dynamics driving significant strategic moves. Paychex delivered robust financial results for the fourth quarter of fiscal 2025, with total revenue increasing 10% year-over-year to $1.43 billion, up from $1.30 billion in Q4 FY24. Adjusted operating income grew 11% to $577 million, while adjusted diluted earnings per share rose 6% to $1.19.

The integration of recent acquisitions is proceeding ahead of schedule. The company has already begun integrating Paycor's operations and has raised its cost synergy expectations to approximately $90 million for fiscal 2026, up from previous estimates. Management has also clarified the market segmentation strategy going forward, with different platforms serving different market segments to optimize service delivery and client satisfaction.

Looking ahead, Paychex provided an optimistic outlook for fiscal 2026, projecting total revenue growth between 16.5% and 18.5%, significantly higher than the 6% growth achieved in fiscal 2025. This acceleration is largely attributed to the full-year impact of the Paycor acquisition. The company expects Management Solutions revenue to grow 20-22%, while PEO & Insurance Solutions revenue is projected to increase 6-8%. Interest on funds held for clients is forecast to reach $190-200 million.

The company's commitment to shareholder returns remains strong. Paychex distributed $1.55 billion to shareholders during fiscal 2025, including $1.45 billion in dividends and $104 million in share repurchases. The company maintained a dividend coverage ratio of 1.2x and a strong return on equity of 42%.

XIII. Links & Resources

Key Company Resources: - Paychex Investor Relations: investor.paychex.com - Annual Reports and SEC Filings: Available through EDGAR database - Small Business Jobs Index: Published monthly in partnership with IHS Markit

Historical and Background Reading: - "Built, Not Born" by Tom Golisano - Founder's autobiography with insights on building Paychex - Harvard Business School Case Studies on Paychex's growth strategy - Rochester Business Journal archives for local perspective on company development

Industry Analysis: - National Association of Professional Employer Organizations (NAPEO) industry reports - IBISWorld Payroll Processing Industry Reports - Gartner Magic Quadrant for Cloud HCM Suites

Competitive Intelligence: - ADP Investor Relations for comparative analysis - Venture capital databases for tracking new entrants (Gusto, Rippling, Deel) - Software review platforms (G2, Capterra) for customer sentiment analysis

Regulatory and Compliance Resources: - IRS Employment Tax resources - Department of Labor compliance guides - State-specific payroll tax resources

Technology and Innovation: - Paychex Flex platform documentation - API developer resources for integration partners - Patent filings for insight into R&D priorities

These resources provide comprehensive background for understanding Paychex's business model, competitive position, and future prospects. For investors conducting due diligence, combining company-specific materials with industry analysis and competitive intelligence offers the most complete picture of the investment opportunity.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube