Old Republic International: The Century-Old Insurance Compounder

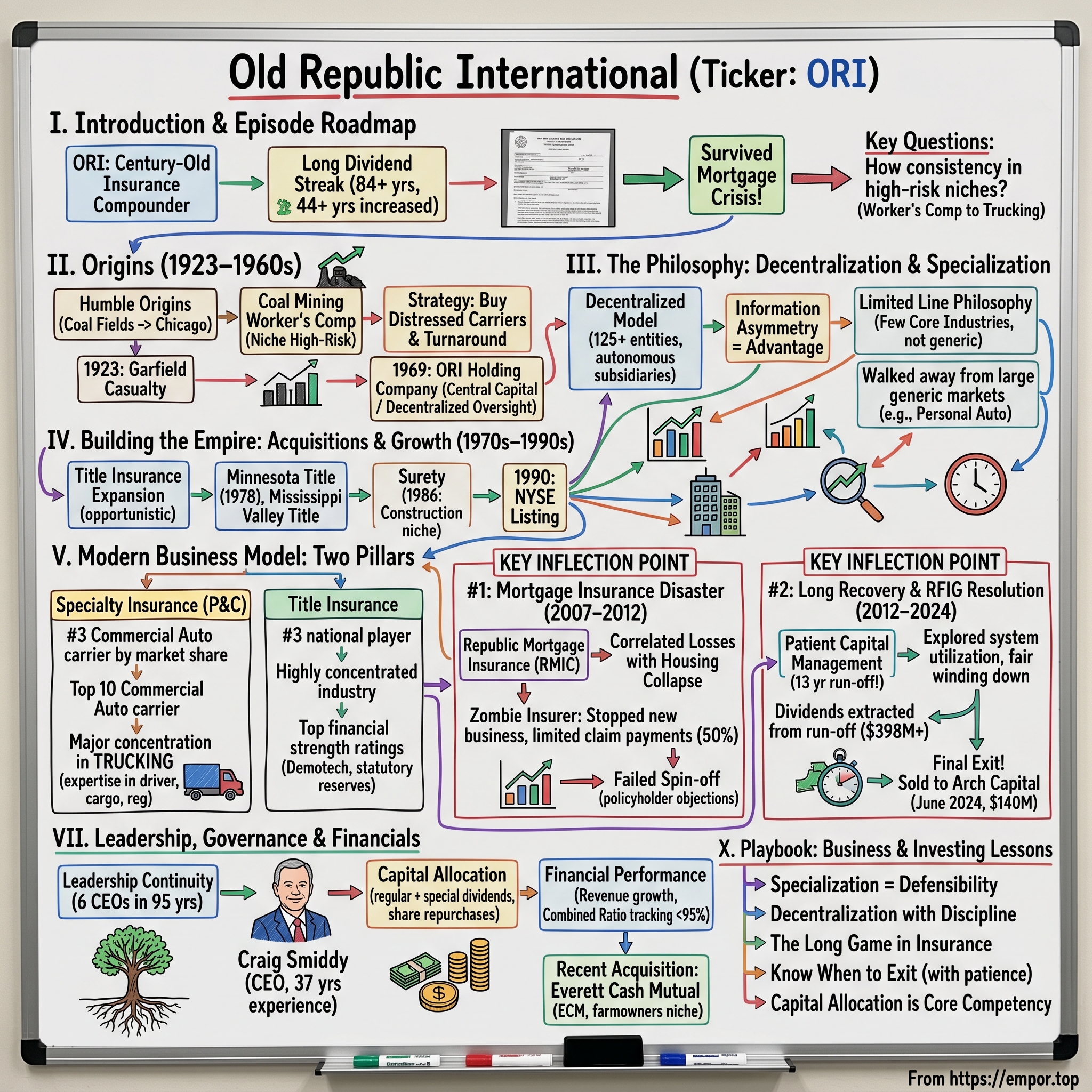

I. Introduction & Episode Roadmap

Picture this scene: It's January 2025, and deep in the bowels of the North Carolina Department of Insurance, the final paperwork is being prepared for one of the longest regulatory sagas in American insurance history. After 13 years in run-off mode, nearly $400 million in dividends extracted, and a business that most observers had written off as a total loss, Old Republic International was about to close the sale of its mortgage insurance subsidiary to Arch Capital for $140 million. The deal would close in June 2024, marking the definitive end of the company's most painful chapter—and perhaps its finest hour of capital stewardship.

Founded in 1923 and a member of the Fortune 500, Old Republic International is a leader in underwriting and risk management services for business partners across the United States and Canada. Old Republic International Corporation (ORI) is one of America's 50 largest shareholder-owned insurance businesses—a distinction earned not through flashy acquisitions or financial engineering, but through a century of patient, disciplined underwriting in industries most insurers prefer to avoid.

The question that animates this deep dive is deceptively simple: How did a small casualty company born in the coal fields of Pennsylvania become a century-old compounding machine that survived the worst housing crisis since the Great Depression while returning dividends for more than 80 consecutive years?

The numbers tell a story of remarkable consistency. 2025 marks the 44th consecutive year that Old Republic has increased its regular cash dividend and the 84th year of uninterrupted regular cash dividend payments. Old Republic International Corporation (ORI) has increased its dividends for 38 consecutive years. In an era when companies routinely cut dividends at the first sign of trouble, this kind of consistency isn't just impressive—it's almost anachronistic.

But Old Republic isn't a story about dividend aristocracy alone. It's a story about specialization versus diversification, about the tension between growth and discipline, and about what happens when a company's worst business decision becomes its greatest lesson in capital allocation. The mortgage insurance disaster that began in 2007 could have destroyed the company. Instead, it became a master class in patient capital management.

Here's the roadmap: We'll trace the company's origins from the coal fields of Pennsylvania to its headquarters in Chicago, examine its unique philosophy of decentralization and specialization, chronicle its expansion into title insurance and commercial trucking, and then dive deep into the mortgage insurance crisis that nearly brought it to its knees. We'll analyze how the company navigated 13 years of run-off operations before finally exiting in 2024, and extract the investing lessons that apply far beyond the insurance industry.

II. Origins: The Coal Fields to Chicago (1923–1960s)

The Founding Story

The first company in the ORI family was incorporated under the name Garfield Casualty Company in 1923. The origins were humble—a casualty company formed to serve the dangerous, high-risk world of American coal mining. In 1930, the company adopted the name Old Republic Life Insurance Company. The flagship company of ORI's General Insurance Group, Old Republic Insurance Company, was incorporated as Coal Operators Casualty Company in 1935.

The context matters enormously. The 1920s marked the apogee of American coal production, with mines scattered across Pennsylvania, West Virginia, and Kentucky feeding the voracious appetite of an industrializing nation. Coal mining was, and remains, one of the most dangerous occupations in the country. Cave-ins, explosions, black lung disease—the risks were constant and severe. Major insurers wanted nothing to do with this business. The premiums seemed insufficient to cover the inevitable claims, and the reputational risk of being associated with coal mine disasters made marketing departments nervous.

This is where Old Republic's founding philosophy began to crystallize: find industries that major insurers avoid, develop deep expertise in their specific risks, and price accordingly. It's a simple formula, but executing it requires a kind of institutional patience that most insurance companies—especially those answering to quarterly-focused shareholders—struggle to maintain.

Early Philosophy Takes Shape

Old Republic's record as a long-term growth company is one of the best in the industry. The Company's performance reflects an entrepreneurial spirit, sound forward planning, and a corporate structure that promotes and encourages assumption of prudent business risks.

The early decades established patterns that persist today. Rather than competing head-to-head with larger insurers in broad market segments, Old Republic carved out niches where specialized knowledge created genuine competitive advantage. Workers' compensation for coal miners required understanding the specific hazards of underground work—the geology of different seams, the technology of ventilation systems, the regulatory environment of mining safety. Casualty insurance for industrial operations demanded similar expertise.

The organization, which traces its origins to the 1920s, achieved much of its growth by purchasing troubled insurance carriers and redirecting them to create profitable subsidiaries. This acquisition strategy—buying distressed companies and applying disciplined underwriting—would become a hallmark of Old Republic's expansion. Rather than paying premium prices for market leaders, the company specialized in turnarounds.

Relocation to Chicago

The company is headquartered in Chicago, Illinois. The move to Chicago made strategic sense for a company aspiring to national scope. Chicago in the mid-20th century was America's railroad hub, its commodities trading center, and increasingly, its insurance capital. The city offered access to a deep pool of insurance talent, proximity to major industrial clients across the Midwest, and the infrastructure to coordinate operations spanning multiple states.

In 1969, the Old Republic International Corporation was organized to serve as a holding company for diversified insurance, financial, and investment operations. This structural change marked Old Republic's transition from a collection of regional insurers to a coordinated national enterprise. The holding company structure allowed each subsidiary to maintain its specialized focus while benefiting from centralized capital allocation and risk management.

The transformation from coal-field casualty company to diversified holding company took nearly half a century—an evolution marked by patient expansion rather than sudden transformation. By the late 1960s, Old Republic had established the organizational framework that would enable its next phase of growth.

III. The Philosophy: Decentralization & Specialization (1960s–1970s)

The Decentralized Model

Old Republic operates in a decentralized manner that emphasizes specialization by type of insurance coverage and industry, ensuring broad diversification and dispersion of risk. This sentence, which appears in virtually every Old Republic corporate communication, encapsulates a philosophy that runs counter to most modern management theory.

In an era of centralization, shared services, and economies of scale, Old Republic deliberately maintains a fragmented organizational structure. Old Republic International Corporation, one of the 50 largest publicly held insurance organizations in the United States, is a holding company for a diversified array of insurance companies. Conducting business through 125 different corporate entities—including 30 autonomous insurance subsidiaries covering all 50 states and Canada—Old Republic International (ORI) specializes in lines of insurance marketed toward specific industries.

Why autonomy? The insurance business is fundamentally about information asymmetry. The insurer who understands a risk better than competitors can price it more accurately, select better customers, and manage claims more efficiently. Centralization tends to homogenize knowledge—the corporate headquarters develops standardized underwriting guidelines that apply across all business lines. Decentralization preserves specialized expertise at the point where it matters most: the underwriting decision.

Our decentralized business model puts specialists directly on the front line, so clients get a level of service and expertise not commonly found in the industry. The operational implications are significant. Each subsidiary maintains its own underwriting team, its own claims organization, and its own client relationships. The holding company provides capital, risk management oversight, and strategic direction—but the day-to-day decisions rest with people who spend their careers understanding specific industries and coverage types.

The "Limited Line" Philosophy

The company's philosophy, as stated in its 1993 Annual Review, is to "offer a limited line of coverages to relatively few industries at the core of the American economy."

This is perhaps Old Republic's most counterintuitive insight. In an industry where diversification is typically viewed as risk reduction, Old Republic argues that doing fewer things better creates superior outcomes. The logic is straightforward but demanding: to be excellent at trucking insurance, you need people who understand trucking—the logistics industry's operating economics, the specific risks of different cargo types, the regulatory environment governing driver hours and vehicle maintenance. To be excellent at title insurance, you need people who understand real estate law, property records, and the peculiar risks associated with different types of transactions.

Attempting to be adequate at twenty different business lines means spreading expertise thin. Better to dominate five niches than to be a marginal player in twenty.

The practical effect is that Old Republic has walked away from enormous market opportunities. The company never competed seriously in personal auto insurance, never built a major homeowners insurance franchise, never pursued the broad commercial lines business that defines companies like Travelers or Hartford. Each of these decisions represented foregone revenue, but also avoided the dilution of specialized expertise that comes with expansion beyond core competencies.

IV. Building the Empire: Acquisitions & Growth (1970s–1990s)

Title Insurance Expansion

The 1970s marked Old Republic's decisive entry into title insurance, a business that would eventually become one of its two core pillars. The acquisition strategy was characteristically opportunistic.

Old Republic National Title Insurance Company was first incorporated in Minnesota in 1907 as the Real Estate Title Insurance Company. In 1928, the Company became the Title Insurance Company of Minnesota (Minnesota Title), which was one of the first title insurance companies to expand beyond state lines in 1938. In 1978, Minnesota Title was acquired by Old Republic International Corporation.

American Guaranty Title Insurance Company, Old Republic Title Insurance Group's oldest title insurance underwriter, began operations in 1889. The acquisition of companies with roots extending back to the 19th century gave Old Republic instant credibility in a business where longevity signals claims-paying reliability.

Another company to come under ORI ownership during the late 1970s was the Mississippi Valley Title Insurance Company. Mississippi Valley had been founded by the Taylor family in 1941 as a sideline to an existing law practice. Following World War II, the company enjoyed quick growth, since VA and FHA loans required title insurance. By 1990, Mississippi Valley reported that it had achieved a 66 percent share of the market in Mississippi.

The Mississippi Valley acquisition illustrates Old Republic's patient approach. The company had achieved remarkable regional dominance—66% market share in its home state—but lacked the capital and infrastructure to expand nationally. Under Old Republic's ownership, that specialized expertise could be leveraged across a broader geographic footprint.

Surety & Reinsurance

In 1986, ORI purchased an organization with a 50-year history and reorganized it as the Old Republic Surety Group, Inc. The original entity, Mutual Surety Company of Iowa, founded in 1936, was succeeded by State Surety in 1956.

Surety bonds—guarantees that contractors will complete projects according to specifications—represented a natural extension of Old Republic's construction industry expertise. The surety business requires understanding both the financial condition of contractors and the specific risks of construction projects. Once again, specialized knowledge translated into underwriting advantage.

Several changes and expansions in ORI's reinsurance activities occurred during the late 1970s and early 1980s. Reinsurance, a process of obtaining insurance on the potential risk faced by an insurer under an existing insurance contract, helped limit the insurance carrier's risk exposure from any one incident.

Building National Brand Recognition

As part of the program aimed at increasing national name recognition, some subsidiaries also changed their names to include an "Old Republic" appellation. This branding consolidation created a unified corporate identity while preserving the operational autonomy that defined Old Republic's competitive advantage.

In 1985, ORI made one of its largest acquisitions to date, merging with Bitco Corporation, previously known as Bituminous Holdings, Ltd. In 1990, ORI's common stock was listed on the New York Stock Exchange.

The NYSE listing marked Old Republic's arrival as a nationally significant insurance company. The company had spent nearly 70 years building specialized expertise in overlooked market niches; now it had the capital markets access to compete at scale.

V. The Modern Business Model: Two Pillars

General Insurance (Specialty P&C)

The Old Republic Specialty Insurance Group (ORSIG) is our largest segment. It includes 18 underwriting subsidiaries, plus many agency and related services companies serving customers in the United States and Canada.

The specialty insurance segment demonstrates Old Republic's niche strategy at its fullest expression. The company is one of the top 10 commercial auto insurance carriers in the U.S. Old Republic provides commercial auto liability insurance for many major trucking and transportation companies.

The Old Republic General Insurance Group is the largest of the company's business segments and offers a variety of property and casualty insurance coverage and services, primarily to commercial customers. Approximately 27.8% of the insurance services are focused on trucking.

Old Republic is the third-largest commercial auto insurance company by market share, controlling about 4.1% of the market, according to the National Association of Insurance Commissioners (NAIC).

Great West Casualty Company specializes in insurance products and services for the trucking industry. We offer flexible underwriting to customize coverages for each unique situation, backed by 24-hour claims and safety services. Our identity, our business, and our success are linked to trucking.

The trucking concentration illustrates both the power and risk of specialization. Old Republic has built extraordinary expertise in commercial auto—understanding driver behavior, cargo risks, regulatory compliance, and claims patterns better than generalist competitors. But this concentration also creates correlation risk: a major shift in trucking industry economics would disproportionately impact Old Republic.

Title Insurance

The Old Republic Title Insurance Group (ORTIG) has built a solid reputation as an industry leader and is one of the largest title insurance groups in the United States.

Old Republic's general insurance business ranks among the nation's 50 largest while our title insurance business is the third largest in its industry.

The title insurance market is highly concentrated, dominated by a handful of national players. First American Title makes up 22% of the title insurance market in the U.S. Old Republic National Title and Fidelity National Title are the second- and third-largest companies at 15% and 13%, respectively. The three largest title insurance companies — First American Title, Old Republic National Title and Fidelity National Title — account for half of title insurance premiums in the U.S.

Of the 10 largest title companies, Old Republic National Title, Chicago Title, Title Resources Guaranty and North American Title have the fewest customer complaints, according to the National Association of Insurance Commissioners (NAIC). Old Republic National Title and Chicago Title are the best companies in the U.S. Both have fewer complaints than other title companies of a similar size. Both companies also have the highest possible financial strength rating from Demotech.

As a measure of claims paying ability, Old Republic Title's statutory reserves and surplus are the strongest of all the national underwriters. As a multiple of 5 year average claim payments, our reserves and surplus far exceed any of our national competitors.

This financial strength matters enormously in title insurance, where policies can be triggered decades after issuance. A title policy written in 2000 for a commercial building might generate a claim in 2030. The insurer needs to remain solvent—and confident of remaining solvent—across that entire horizon.

VI. KEY INFLECTION POINT #1: The Mortgage Insurance Disaster (2007–2012)

The Build-Up: Entering Mortgage Insurance

Since beginning operations in 1972, RMIC has typically insured loans for purchasing or refinancing insured home loans when the amount borrowed exceeded 80% of the property's value.

Old Republic's mortgage insurance business—operated through Republic Mortgage Insurance Company (RMIC)—had been a steady contributor for decades. The business model was straightforward: when homebuyers couldn't afford a 20% down payment, their lenders required private mortgage insurance to protect against default. RMIC collected premiums from these borrowers and paid claims when they defaulted.

For most of its history, this was a stable, profitable business. Default rates on conforming mortgages were low, claims were predictable, and the housing market's steady appreciation provided a cushion against losses. But the housing boom of 2003-2006 transformed the risk profile entirely.

The temptation during these years was enormous. Mortgage origination volumes soared, and every new loan represented premium income for RMIC. Competitors were aggressively pursuing market share, and maintaining discipline meant watching rivals grow faster. The Old Republic Mortgage Guaranty Group insures financial institutions against default on first mortgages for single-family homes, typically those with low down payments of 5 to 10 percent.

The problem, invisible at the time but devastating in retrospect, was correlation. Mortgage insurance losses are highly correlated with housing market conditions. When house prices rise steadily, even borrowers who face financial difficulty can sell their homes and avoid default. When prices fall, defaults cascade—and mortgage insurers face simultaneous claims across their entire book.

The Crisis Hits

For example, the US MI industry was severely affected by the recent global financial crisis. Two of the five big US mortgage insurers (PMI and Republic) are under orders of supervision, and the other three are sub-investment grade.

The housing market collapse that began in 2007 devastated the mortgage insurance industry. Default rates spiked, claims volumes exploded, and the capital cushions that insurers had accumulated over decades evaporated in months.

Just two years ago, Old Republic was forced to announce that its flagship mortgage guaranty insurance unit was operating on a waiver of minimum capital requirements — a waiver granted by its chief insurance regulator. At the time, the firm's mortgage guaranty subsidiary, RMIC Companies Inc. (RMIC), was forced to stop writing new business and told it could no longer pay more than 50% of any claims under any insurance policy it had issued.

This was the worst possible outcome short of bankruptcy: a zombie insurer, unable to write new business but still liable for claims on existing policies, slowly bleeding capital while regulators monitored its death spiral.

Regulatory Intervention & Runoff

In 2011, following the 2007–08 global financial crisis, RMIC shifted to runoff operating mode. Since discontinuing writing new insurance, we continue to support our customers and our in-force book of policies.

In 2011, following the 2007–08 global financial crisis, RMIC shifted to runoff operating mode. Since discontinuing writing new insurance, we continue to support our customers and our in-force book of policies.

Run-off mode is insurance industry euphemism for controlled wind-down. The company would honor existing policies, pay claims as they came due, and wait for the book to attrit naturally as mortgages were refinanced, paid off, or exhausted their coverage periods. No new policies would be written, no new premiums collected.

The Failed Spin-Off Attempt (2012)

Old Republic International Corporation today reported that it has withdrawn the previously announced spin-off of its Republic Financial Indemnity Group, Inc. ("RFIG") subsidiary stock to ORI shareholders. Concurrently the financial effect of the partial RFIG leveraged buy-out has been reversed. These decisions respond to objections raised by certain stakeholders that RFIG's separation from Old Republic would be disadvantageous to their interests and expectations.

The spin-off attempt reveals the strategic calculus Old Republic faced. Management believed that separating the troubled mortgage insurance operations from the healthy parent company would benefit both entities—RFIG could pursue recapitalization without dragging down Old Republic's stock, while Old Republic could focus on its profitable businesses without the overhang of mortgage insurance losses.

Old Republic announced that its RFIG division sold a 20.6% common equity interest in its individual unit to a group of investors and agreed to spin off the remaining shares of RFIG to company shareholders. Old Republic Mortgage Guaranty Group was re-named Republic Financial Indemnity Group earlier this year after Old Republic combined its consumer credit indemnity division with its mortgage insurance segment. The end result of the transition was the creation of RFIG, a division that includes three mortgage insurers, four service-related companies and a credit indemnity insurer. Old Republic made it known back in March that both the mortgage and consumer credit indemnity businesses were operating in run-off mode and struggling with losses as well as a need for additional capital.

But stakeholders objected. Policyholders worried that a separated RFIG would lack the financial resources to pay claims. The spin-off was abandoned, and Old Republic committed to managing the run-off within its existing corporate structure.

VII. KEY INFLECTION POINT #2: The Long Recovery & RFIG Resolution (2012–2024)

Patient Capital Management

What followed was one of the most remarkable examples of patient capital management in recent insurance history. Rather than rushing to exit or writing off the business entirely, Old Republic committed to a methodical run-off strategy designed to maximize value recovery while honoring all legitimate claims.

As we reported last month, we've canceled the planned spin-off of RFIG and have therefore retained these lines of businesses within the Old Republic Holding Company system. As we look at them going forward, our mission with respect to these businesses continues to be the same. First off, to manage them in a fair and economical way, so that we're able to maximize the claim payment resources for the respective policyholders and beneficiaries. Two, to explore ways to utilize their infrastructure and systems and technology and support of unaffiliated businesses.

The timeline was extraordinary. From 2011 to 2024—thirteen years—Old Republic maintained the RMIC infrastructure, processed claims, and waited for the book to mature. This required sustained discipline: the business generated no new revenue but demanded ongoing operational investment.

The Final Exit: Sale to Arch Capital (2023-2024)

Old Republic International Corporation today announced that it has entered into a definitive agreement to sell its mortgage insurance business to Arch Capital Group Ltd. In this transaction, Arch U.S. MI Holdings Inc. will acquire all of the capital stock of Old Republic's wholly-owned subsidiary, RMIC Companies, Inc., and its wholly-owned subsidiaries that together comprise Old Republic's run-off mortgage insurance business. Consideration is expected to be approximately $140 million.

Old Republic President & CEO, Craig R. Smiddy, said "We are pleased to announce this definitive exit from the mortgage insurance business. Since placing this business in run-off in 2011, we have been able to preserve significant value for shareholders and we are grateful for the many years of hard work and dedication of our RMIC associates. In the last five years our run-off reserves have developed favorably, enabling us to receive over $398 million of dividends from these subsidiaries."

The definitive agreement was first announced on November 13, 2023. The deal closed on June 3, 2024.

The math tells the story: $140 million sale price plus $398 million in dividends extracted during run-off, from a business that everyone expected to be a total loss in 2011. The patient capital management strategy didn't just preserve value—it created value that most observers believed had been destroyed.

Upon finalization, RMIC's $1 billion risk in force (RIF) portfolio will become part of Arch MI's US primary mortgage portfolio, which reported a RIF of $75.9 billion as of Sept. 30, 2023. "Our ability to leverage the scale of our platform to gain significant expense and capital synergies makes this an attractive financial transaction for Arch."

For Arch Capital, the acquisition represented an opportunity to add scale to their existing mortgage insurance platform at an attractive price. For Old Republic, it represented the definitive end of a 13-year journey and the opportunity to focus entirely on their core specialty insurance and title businesses.

VIII. The Corporate Culture & Governance

Long-Term Orientation

ORI's performance reflects an entrepreneurial spirit, a necessary long-term orientation, and a corporate culture that promotes integrity and accountability.

The phrase "necessary long-term orientation" captures something essential about Old Republic's philosophy. In insurance, pricing and claims development unfold over years or decades. A policy written today might not generate significant claims for five or ten years. The actuarial assumptions embedded in premium pricing might not be validated—or refuted—for a generation.

The nature of Old Republic's business requires that it be managed for the long run. For the 25 years ended in 2011, the Company's total market return, with dividends reinvested, has grown at a compound annual rate of 9.1 percent per share. For the same period, the total market return, with dividends reinvested, for the S&P 500 Index has grown at a 9.3 percent compound annual rate. During those years, Old Republic's shareholders' equity account, including cash dividends, has risen at an average annual rate of 10.8 percent per share, and the regular cash dividend has grown at a 10.0 percent compound annual rate.

This kind of multi-decade performance comparison is increasingly rare in corporate communications. Most companies prefer to highlight the most recent quarter's outperformance rather than acknowledging that their long-term returns approximate market averages. Old Republic's transparency about its actual track record—competitive but not extraordinary—reflects a culture that prioritizes honesty over marketing.

Leadership Continuity

Old Republic International Corporation today announced several changes in its senior executive ranks effective October 1, 2019. Craig Smiddy (55) ORI's President and Chief Operating Officer will assume the position of President and Chief Executive Officer. He will concurrently join the Board of Directors and its Executive Committee. It has every confidence that the continuity of long-established governance and operating practices will lead to an orderly passage of executive responsibilities to Craig Smiddy as the sixth CEO in ORI's 95-year history.

Six CEOs in 95 years. This kind of leadership stability is almost unheard of in publicly traded companies, where CEO tenure averages around five years. Long tenures enable deep institutional knowledge, consistent strategy execution, and the ability to make decisions whose consequences will unfold over decades.

Craig brings 37 years of insurance and reinsurance industry expertise across numerous disciplines, including claims, product management, underwriting and operations. Immediately prior to joining ORI, he was with Munich Re America for 16 years, where he was President of their Specialty Markets division and a member of their Executive Leadership Team. Craig spent the first 10 years of his insurance career at Progressive Insurance. He holds a Master of Business Administration and a Bachelor of Business Administration degree in Finance, both from The University of Iowa.

Scale and Structure Today

Old Republic International Corporation manages its business through more than 134 corporate entities, of which 27 are insurance subsidiaries covering all 50 states, three United States territories and all 10 Canadian provinces.

IX. Financial Performance & Dividend History

The Dividend Machine

ORI has an annual dividend of $1.16 per share, with a yield of 2.85%. The dividend is paid every three months.

The dividend brings the full year's cash distribution to $1.16 per share, representing a 9.4% increase compared to the $1.06 per share paid in 2024. This marks the 44th consecutive year that Old Republic has increased its regular cash dividend and the 84th year of uninterrupted regular cash dividend payments.

Total capital returned to shareholders during the quarter was $733, comprised of $558 in dividends, and $174 in share repurchases. For the full year, total capital returned was $1,708, comprised of $766 in dividends, and $942 in share repurchases. Changes in shareholders' equity per share for both 2024 periods include the impact of a special cash dividend of $2.00 per share declared in the quarter and paid in January 2025.

The special dividend of $2.00 per share—on top of the regular quarterly dividends—reflects Old Republic's capital allocation philosophy. When excess capital accumulates beyond what's needed for underwriting and acquisitions, it's returned to shareholders rather than hoarded on the balance sheet or deployed into empire-building acquisitions.

Recent Performance

Old Republic International's annual revenue for the twelve months ending Dec 31, 2024 was $8.23 billion, a 13.41% increase year over year.

Old Republic International Corporation today reported the following results for the first quarter 2025: Net income of $245.0, compared to $316.7 last year. Net operating income (net income excluding investment gains) of $201.7, an increase of 9.2%. Net operating income per diluted share of $0.81, compared to $0.67 last year, an increase of 20.9%. Consolidated net premiums and fees earned of over $1.8 billion, an increase of 12.1%. Net investment income of $170.7, an increase of 4.0%. Consolidated combined ratio of 93.7%, compared to 94.3% last year.

Old Republic International Corporation today reported the following results for the third quarter 2025: Net income of $279.5 million, compared to $338.9 million last year. Net income excluding investment gains (losses) (net operating income) of $196.7 million, compared to $182.7 million last year. Net operating income per diluted share of $0.78, compared to $0.71 last year. Consolidated net premiums and fees earned of $2.1 billion, an increase of 8.1% over last year. Net investment income of $182.6 million, an increase of 6.7% over last year. Consolidated combined ratio of 95.3%, compared to 95.0% last year. Favorable loss reserve development of 2.5 points, compared to 1.3 points last year. Book value per share of $26.19, inclusive of cash dividends declared, up 18.5% since year-end 2024. Annualized operating return on equity of 14.4%.

Effective as of year-end 2024, the Company renamed its reportable segment formerly referred to as "General Insurance" to "Specialty Insurance." Management believes this name more appropriately reflects Old Republic's specialty P&C strategy, with 17 underwriting businesses focused on unique niche markets with specialized distribution, underwriting, claims, and risk control models. Specialty Insurance net premiums earned increased 13.3% for the quarter, and 13.5% for the full year.

The rebranding from "General Insurance" to "Specialty Insurance" is more than semantics—it reflects management's desire to clarify Old Republic's positioning. This is not a generalist insurer competing on scale and cost; it's a collection of specialists competing on expertise and service.

Recent Acquisition: Everett Cash Mutual

Old Republic today announced that it has entered into a definitive agreement, pending regulatory and policyholder approval, to acquire Everett Cash Mutual Insurance Co. and affiliated companies ("ECM") following its conversion to a stock company in a sponsored demutualization transaction. ECM is a leading insurer of small farmowners and select commercial agricultural operations. Headquartered in Everett, PA and operating in 48 states and the District of Columbia, ECM wrote $237 million of direct written premium in 2024, ended the year with consolidated statutory policyholders' surplus of $126 million, and has a long-term track record of profitable growth. Following an expected closing in 2026, ORI expects this transaction to be accretive to book value per share and operating income per share.

Randy Shaw, ECM's President & CEO noted, "After 112 years, ECM has found a partner in Old Republic that shares our culture of underwriting excellence. With the combined financial and operational resources available to us, we can continue to pursue our mission of becoming the preeminent farmowners carrier in the country."

The Everett Cash Mutual acquisition exemplifies Old Republic's M&A philosophy: acquire specialized insurers with deep niche expertise, preserve their operational autonomy, and provide the capital and infrastructure to accelerate growth. ECM's 112-year history and focus on small farmowners fits perfectly within Old Republic's portfolio of specialist underwriters.

X. Playbook: Business & Investing Lessons

Lesson 1: Specialization Creates Defensibility

The power of focusing on "relatively few industries at the core of the American economy" goes beyond operational efficiency. Specialization creates knowledge barriers that generalist competitors struggle to overcome. Old Republic's trucking insurance expertise isn't just about having underwriters who understand trucks—it's about institutional knowledge accumulated over decades: claims databases, loss experience by cargo type, relationships with safety consultants, understanding of regulatory changes.

This expertise compounds over time. Each year of trucking insurance experience improves Old Republic's pricing models, claims handling, and risk selection. A new entrant would need years—possibly decades—to develop comparable capabilities.

Lesson 2: Decentralization with Discipline

Old Republic's holding company structure offers a model for managing diverse businesses without bureaucratic bloat. Each subsidiary operates with significant autonomy—its own underwriting authority, its own client relationships, its own specialized expertise. The holding company provides capital allocation, risk oversight, and strategic direction without micromanaging day-to-day operations.

This structure requires trust. Management must believe that subsidiary leaders will make decisions aligned with enterprise-wide goals. It also requires robust information systems that enable the holding company to monitor performance and intervene when necessary.

Lesson 3: The Long Game in Insurance

The insurance business's fundamental characteristic—setting prices before knowing costs—demands long-term thinking. Old Republic's 25-year performance comparisons, its willingness to hold run-off businesses for 13 years, and its 84-year dividend streak all reflect this temporal orientation.

For investors, this creates an interesting dynamic: Old Republic's stock price responds to quarterly results like any other company, but the business's true performance unfolds over much longer horizons. A great underwriting year might not reveal its quality for five or ten years, when claims develop (or don't) according to actuarial expectations.

Lesson 4: Know When to Exit (Even When It Hurts)

The mortgage insurance saga offers perhaps the most valuable lesson: recognizing when a business line violates core disciplines and having the patience to exit on acceptable terms. Old Republic didn't panic-sell at the bottom of the crisis; it methodically managed the run-off, extracted dividends as reserves developed favorably, and ultimately sold for a price that validated the patient approach.

This required 13 years of maintaining infrastructure for a business generating no new revenue. It required explaining to shareholders why the company continued to allocate resources to a wound-down operation. It required confidence that the run-off would eventually produce value.

Lesson 5: Capital Allocation as a Core Competency

Old Republic's capital return strategy—regular dividends, special dividends when excess capital accumulates, share repurchases at attractive valuations—reflects a philosophy that capital belongs to shareholders unless management can deploy it at adequate returns. This discipline prevents the empire-building acquisitions that destroy value in so many insurance companies.

XI. Porter's 5 Forces & Competitive Analysis

Industry Rivalry: Moderate to High

The specialty insurance market is fragmented, with numerous competitors in each niche. Old Republic faces competition from both large diversified insurers entering specialty segments and smaller specialists defending their turf. In trucking insurance, competitors include Progressive Commercial, National Indemnity, and numerous regional players. In title insurance, Fidelity National Financial and First American Title dominate market share.

Supplier Power: Low

Insurance companies' primary inputs are capital and talent. Capital markets provide abundant funding at competitive rates for well-rated insurers. Talent markets are competitive but manageable through compensation and culture.

Buyer Power: Moderate

Commercial insurance buyers—trucking companies, construction firms, real estate developers—have significant negotiating leverage, particularly for large accounts. However, specialized coverage requirements and the importance of claims service limit pure price shopping.

Threat of New Entrants: Low to Moderate

Insurance regulation creates barriers to entry: capital requirements, licensing, and reserve standards. However, well-capitalized new entrants can enter through acquisition or by building de novo operations. The InsurTech wave has introduced new competitors in some segments, though specialized commercial insurance has been less disrupted than personal lines.

Threat of Substitutes: Low

For most of Old Republic's coverage lines, insurance is either legally required (commercial auto liability) or contractually mandated (title insurance for mortgage lenders). Self-insurance and captive arrangements provide alternatives for the largest companies, but most customers require traditional insurance products.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Moderate advantage in title insurance, where national infrastructure enables cost-effective service delivery. Less relevant in specialty P&C, where underwriting expertise matters more than scale.

Network Effects: Minimal. Insurance doesn't exhibit the winner-take-all dynamics of platform businesses.

Counter-Positioning: Significant. Old Republic's decentralized, specialist model is difficult for large centralized insurers to replicate without disrupting their existing organizational structures.

Switching Costs: Moderate. Commercial insurance relationships involve significant switching costs—new underwriting reviews, relationship building, claims history transfers—but aren't prohibitive.

Branding: Limited consumer relevance but significant B2B value. Old Republic's century-long history and consistent financial strength ratings matter to commercial buyers evaluating counterparty risk.

Cornered Resource: The accumulated underwriting expertise in specific niches—trucking, construction, title—represents a cornered resource that competitors cannot easily acquire.

Process Power: Strong. Old Republic's specialized underwriting processes, claims handling procedures, and risk control services create sustainable advantage in served markets.

XII. Bull Case, Bear Case & Key Metrics to Watch

The Bull Case

Old Republic represents a rare combination of defensive characteristics and growth potential. The specialty insurance segment continues to generate double-digit premium growth driven by rate increases and new business wins. The title insurance segment, while cyclical, benefits from any recovery in real estate transaction volumes. The company's conservative balance sheet and consistent profitability support continued dividend growth and opportunistic acquisitions.

The Everett Cash Mutual acquisition demonstrates management's ability to identify attractive targets that fit the company's specialist model. Additional acquisitions in underserved niches could accelerate growth while maintaining underwriting discipline.

The mortgage insurance overhang is definitively resolved, allowing investors to focus on core operations. Management's track record of patient capital management during the run-off period suggests disciplined stewardship going forward.

The Bear Case

Concentration risk in trucking and commercial auto creates vulnerability to industry-specific downturns. Autonomous vehicle technology, while uncertain in timing, could eventually reduce demand for commercial trucking insurance. Rising nuclear verdicts in commercial auto litigation threaten industry profitability.

Title insurance is inherently cyclical, with revenues tied to real estate transaction volumes and housing market conditions. Higher interest rates suppress mortgage origination and refinancing activity, directly impacting Old Republic's title revenues.

The specialty insurance market is increasingly competitive, with new entrants pursuing the same niche strategies that Old Republic pioneered. Margin compression could offset premium growth.

Key Performance Indicators

For investors monitoring Old Republic's ongoing performance, three metrics deserve particular attention:

1. Combined Ratio by Segment: The combined ratio (losses + expenses / premiums) measures underwriting profitability. Old Republic targets combined ratios below 95% for specialty insurance and 90-95% for title insurance. Persistent deterioration would signal competitive pressure or underwriting discipline erosion.

2. Premium Growth Rate (Specialty Insurance): Double-digit premium growth has been driven by rate increases and new business wins. Deceleration would suggest market saturation or competitive loss of share.

3. Book Value Per Share Growth: Including dividends paid, book value per share growth measures comprehensive returns to shareholders. Old Republic has historically grown book value at high single-digit rates; maintaining this trajectory validates the business model.

XIII. Conclusion

Old Republic International defies easy categorization. It's not a growth stock—revenue grows in line with GDP and market conditions. It's not a value play—the stock trades at reasonable multiples reflecting its defensive characteristics. It's not a dividend aristocrat gunning for yield—the payout ratio leaves ample room for reinvestment.

What Old Republic represents is something arguably more valuable: a century-tested model for building durable competitive advantage through specialization, discipline, and patience. The company's philosophy—do fewer things better, maintain operational autonomy within strong governance frameworks, manage for the long run—sounds almost quaint in an era of platform businesses and network effects.

Yet the results speak for themselves. 2025 marks the 44th consecutive year that Old Republic has increased its regular cash dividend and the 84th year of uninterrupted regular cash dividend payments. The mortgage insurance crisis, which could have destroyed the company, instead became a demonstration of capital stewardship that produced over $500 million in value from a business everyone expected to be worthless.

The lessons extend beyond insurance. Any business facing questions about specialization versus diversification, centralization versus autonomy, or short-term optimization versus long-term value creation can learn from Old Republic's approach. The answers aren't universal—different industries and competitive dynamics require different strategies—but the framework of asking these questions thoughtfully, and sticking with answers across decades rather than quarters, has proven remarkably effective.

For long-term investors seeking businesses with genuine competitive moats, consistent capital return policies, and management teams oriented toward multi-decade value creation, Old Republic merits serious consideration. The company won't generate headline-grabbing returns or revolutionary disruption. It will, in all likelihood, continue doing what it has done for a century: compounding value through specialized expertise, disciplined underwriting, and patient capital allocation.

In an investment world increasingly dominated by momentum, narratives, and short-term thinking, there's something refreshing about a company that has spent a hundred years proving that boring works.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube