American Financial Group: The Specialty Insurance Empire Built by a Dairy Farmer's Son

I. Introduction & Episode Roadmap

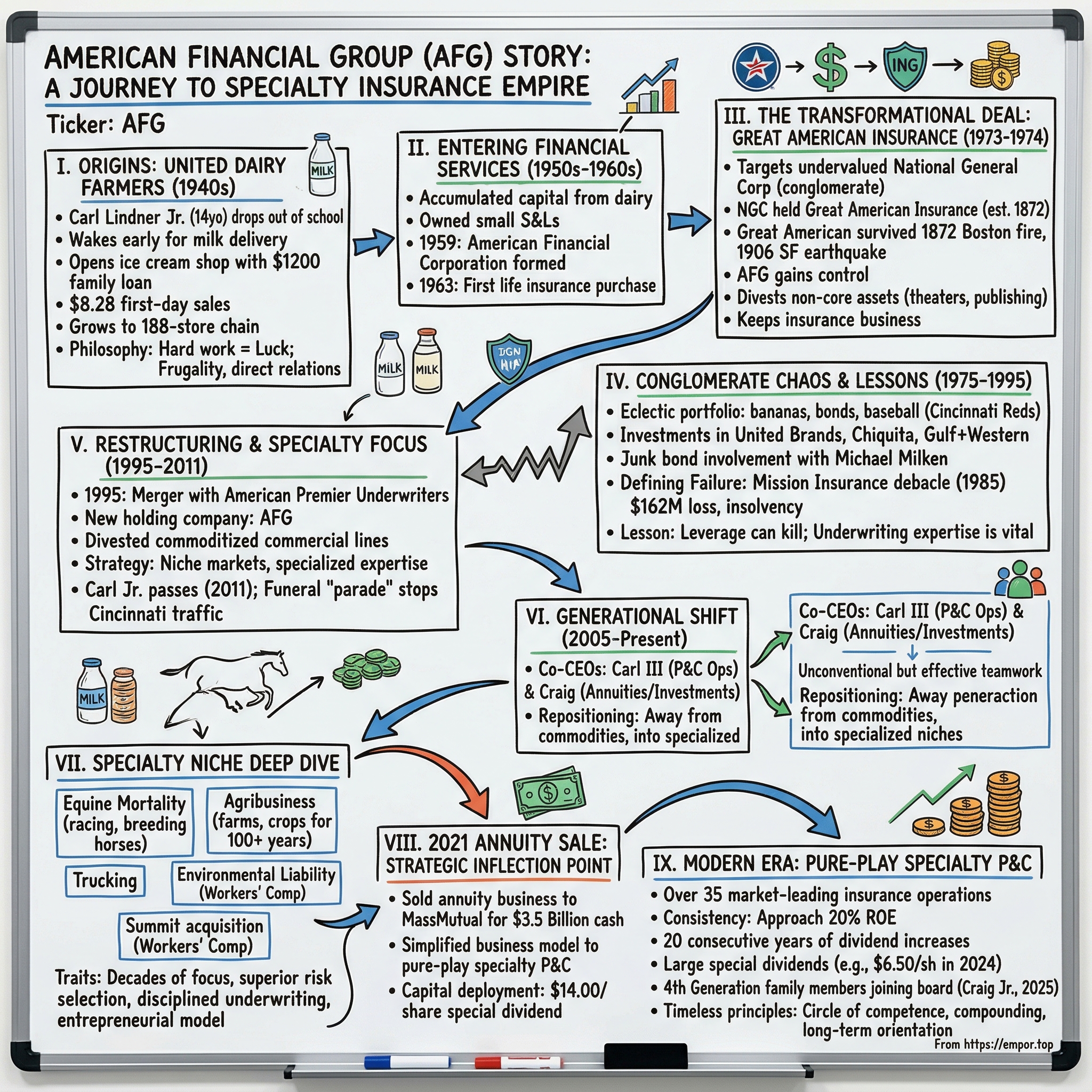

Picture a 14-year-old boy in Depression-era Cincinnati, waking before dawn to deliver milk door-to-door while attending night school. His father has just handed him the keys to an ice cream shop financed with a $1,200 loan—the entirety of the family's savings. That teenager was Carl Henry Lindner Jr., and from those humble dairy routes emerged one of America's most disciplined specialty insurance empires.

American Financial Group, Inc. is an American financial services holding company headquartered in Cincinnati, Ohio. Its primary businesses are insurance and investments. Today, AFG stands as a Fortune 500 company with a revenue of $8.27 billion in 2024, quietly dominating obscure but profitable niches that most insurers overlook entirely.

The central question this deep dive explores: How did a high school dropout who started with a dairy business build one of America's most successful specialty insurers?

The company achieved a full year 2024 ROE of 19.0% and a core operating ROE of 19.3%. That's not a one-year fluke. AFG has consistently delivered returns on equity approaching 20% while its competitors struggle with commoditized pricing and runaway claims. For the twelve months ended December 31, 2024, AFG's growth in book value per share plus dividends was 23.0%.

What makes AFG remarkable isn't just the numbers—it's the story behind them. This is a tale of family business succession across three generations, disciplined underwriting that borders on obsession, the strategic power of focus, and capital allocation mastery that would make Warren Buffett nod approvingly. The Lindner family hasn't just managed money; they've built a culture.

The company traces its roots through multiple transformations: from Depression-era dairy routes, to savings and loan associations in the 1950s, to conglomerate chaos in the 1980s, to the focused specialty insurer that emerged from a defining $3.5 billion divestiture in 2021. Each chapter reveals lessons about what it means to build durable businesses—and what happens when you stray from your circle of competence.

II. The Lindner Family Origin Story & United Dairy Farmers

The Lindner family story begins not with financial wizardry but with milk bottles and manual labor. Mr. Lindner was born in Dayton, Ohio in 1919, and the family moved to Cincinnati in 1930 when he was 11 years old. He developed industrious habits and a devotion to his community at a young age.

The Depression forced difficult choices. Mr. Lindner dropped out of school at age 15, at the bottom of the Depression, and began working countless hours a day, delivering milk door-to-door while attending high school classes at night. While other teenagers worried about homework, young Carl was calculating margins on dairy deliveries and learning that in tough times, providing essential goods at fair prices builds loyal customers.

Carl Lindner Sr., the patriarch, instilled in his children a philosophy that would echo through decades: "You can do anything you want to, children; the sky's the limit." That confidence wasn't just motivational—it was operational. The Lindners didn't just dream; they built.

The business originated as a response to high home milk delivery costs during the late 1930s, with Lindner opening the first store on May 8, 1940, at 3941 Montgomery Road in Norwood, where milk sold for 28 cents per gallon and generated $8 in sales on its debut day. The business model was revolutionary for its time: cut out the middleman, sell direct, pass savings to customers.

Lindner called his company United Dairy Farmers in acknowledgment of its milk suppliers. Lindner's entire family (his wife Clara and their four children, Dorothy, Carl, Jr., Robert, and Richard) dedicated themselves to making Lindner's company a success. They rebuilt used dairy production equipment and fashioned cabinets and signs for the company's new store.

The family's first day sales? $8.28. A modest beginning, but one that would compound relentlessly.

With two brothers, Robert and Richard, and a sister, Dorothy, he opened an ice cream shop with a $1,200 loan in 1940. Lindner's empirical success began with a $1,200 loan in 1940 to open an ice cream shop alongside his siblings, evolving United Dairy Farmers into a 188-store chain before pivoting to financial services.

The business model contained DNA that would later define AFG: frugality, direct relationships, cutting unnecessary costs, and relentless focus on what customers actually needed. Although Lindner's dairy did not extend credit to its customers, his business model enabled him to sell dairy products at a much lower cost than home-delivery dairies because he had done away with delivery expenses.

The Lindner family's rise to prominence began with Carl Lindner Sr. opening a dairy processing plant in Norwood, Ohio in 1940. The business, United Dairy Farmers, had expanded to thirty stores by 1960, and the family bought the American Financial Group with their savings.

By the mid-1960s, Carl Sr.'s sons were running the family's businesses: Carl Jr. was running American Financial Group, Robert was running United Dairy Farmers, and Richard was running the Thriftway Food Drug grocery chain. The division of labor showcased a pattern: each brother to his strengths, but family unity above all.

Carl Jr. developed a distinctive business philosophy that would guide AFG for decades. Carl Lindner Jr. adhered to a business philosophy emphasizing relentless effort, calculated entrepreneurial risk, and long-term value realization through compounding returns, encapsulated in his maxim, "The harder I work, the luckier I get."

The dairy business taught lessons that would transfer directly to insurance: the importance of steady cash flows, the value of serving customers others overlook, and the power of reinvesting profits rather than extracting them. This approach rebutted common critiques of conglomerates by prioritizing decentralized management that enabled efficient capital allocation.

By the late 1950s, the Lindner brothers had accumulated enough capital from their dairy and retail operations to enter a new arena: financial services. The seeds of American Financial Group were planted in the soil of homemade ice cream and early morning milk routes.

III. Building American Financial Corporation (1959–1973)

In 1959, Carl Lindner Jr. took the capital generated from United Dairy Farmers and made a pivot that would define his legacy. American Financial Group traces its history to 1959. In the early days, the Company was known as American Financial Corporation. At its inception, the Company's principal business consisted of savings and loans.

By 1959, the company owned three small savings and loan associations in Ohio and recorded assets of $17.7 million. These weren't glamorous acquisitions—they were small thrifts serving working-class Ohioans. But Lindner saw what others missed: stable cash flows, conservative management, and the opportunity to deploy capital into higher-return ventures.

The 1960s brought rapid expansion and diversification. In 1963, the firm branches out into life insurance with the purchase of United Liberty Life. This marked AFC's first major foray into the insurance business—a sector that would ultimately define the company.

Lindner's approach during this era was opportunistic but disciplined. He targeted undervalued assets, often buying significant stakes in established companies trading below intrinsic value. AFG's principal founders were chairman and president, Carl H. Lindner, and his younger brothers, Robert D. and Richard E. Lindner. The Lindner brothers, born and raised in Ohio, started in business without the benefit of formal education, business connections, or family money. Carl Henry Lindner, born April 22, 1919, and his brothers left high school before graduating to help with the family's small dairy business.

The diversification strategy accelerated. Through their holding company American Financial Group they control Great American Insurance, a holding company for a group of property and life insurance companies. AFG owned the fourth-largest bank in Cincinnati, Provident Bank, and the second-largest savings and loan (Hunter Savings). The Lindners also control seventy shopping centers around Cincinnati. They once owned Bantam Books and the major newspaper of Cincinnati, The Cincinnati Enquirer.

The conglomerate era was in full swing across corporate America, and Lindner was an enthusiastic participant. But unlike many 1960s empire builders who were pure financial engineers, Lindner maintained operational focus. He wasn't just shuffling paper; he was building real businesses.

Acquired S&Ls 1959; diversified into insurance 1971. The insurance pivot proved prescient. While savings and loans would face existential crises in the 1980s, insurance provided the stable float that Lindner needed to compound capital over decades.

Craig and Carl's father, renowned business leader and philanthropist Carl H. Lindner Jr., formed American Financial Group (AFG) in 1959. During their father's tenure as chief executive, AFG served as the umbrella for a sweeping array of holdings including stakes in broadcast and media companies, insurance and banking concerns, food producers and the Cincinnati Reds baseball team.

By the early 1970s, AFC had grown from a collection of small thrifts to a diversified holding company with billions in assets. But the truly transformational deal was about to arrive—one that would anchor the Lindner empire in property and casualty insurance for the next half century.

IV. The Great American Insurance Acquisition (1973–1974): The Transformational Deal

The year 1973 marked the most consequential transaction in AFG's history. Carl Lindner, surveying the landscape of undervalued assets amid a bear market, identified a target that would reshape his company's future: National General Corporation, a bizarre conglomerate that held something Lindner wanted desperately.

National General Corporation, incorporated in Delaware in 1952 as National Theatres, Inc., was involved in the operation of motion picture theaters in the United States and abroad, motion picture production and distribution, and cable and closed-circuit television. However, 70 percent of National General Corporation's (NGC) assets were in insurance and publishing. NGC's holdings included the publishers Grosset & Dunlap, Inc., and Bantam Books, Inc.; the Great American Life Insurance Company of East Orange, New Jersey, procured in 1968; and its parent sponsor, the Great American Insurance Company.

Great American Insurance Company's history stretched back to the Gilded Age. The need for dependable risk management solutions triggered the creation of our founding insurance company, German American Insurance Company, in 1872. The first policy, which insured a factory that manufactured rubber combs, was issued that same year on March 19.

The company had survived catastrophes that destroyed lesser firms. In the same year that German American started, the Boston fire of 1872 cost insurance companies more than $52 million. The fire, following so closely upon the Chicago Fire of 1871, was a staggering blow to many insurance companies and some did not survive. German American's loss in Boston was believed to be $109,000.

As a result of World War I, sentiments had shifted in the country. Recognizing the heightened sensitivity to German affiliation, the company changed its name from German American to Great American Insurance Company in 1918.

The insurer's strength was tested in the devastating 1906 San Francisco earthquake – and German American really shone above the rest of the market. The firm paid all claims, including those from policyholders who didn't actually have viable insurance coverage – all to help the California city recover. In total, German American paid more than $2 million in claims after the 1906 San Francisco earthquake.

This was exactly the kind of company Lindner valued: one with a century of institutional knowledge, a reputation for honoring claims, and stable cash flows. What National General saw as a boring subsidiary, Lindner saw as a crown jewel.

By late 1973, AFC had amassed approximately 96 percent of common stock and 85 percent of the warrants and had gained financial control of a West Coast conglomerate, National General Corporation. The merger was completed in March 1974.

According to Barron's, July 4, 1988, "What attracted [Carl] Lindner to the company [National General Corporation] was its giant property and casualty operation, Great American Insurance Co."

The deal transformed AFC's scale. With the NGC merger and the acquisition of Great American Insurance Company and GALIC, AFC's assets escalated to over $2 billion. The merger also launched American Financial Corporation as one of the country's major international insurance concerns. Great American Insurance Company and its subsidiaries were writing practically all forms of insurance in every state and territory, as well as in Canada and in other countries.

Lindner moved quickly to strip away non-core assets. In 1974, Carl H. Lindner merged NGC into American Financial Corporation (AFC) and disposed of many of the non-insurance assets acquired as a result of the merger. Movie theaters, publishing houses, and fast-food operations were sold. The insurance business was kept and nurtured.

Under AFC's ownership, the company refocused, and Great American developed a niche market presence in specialized commercial insurance products for businesses, and personal line insurance products for individuals. In 1974, Great American Insurance Company established its headquarters in downtown Cincinnati.

But the integration came with challenges. The merger was costly—more than $500 million in cash, security, and debt assumption. By early 1975, American Financial Corporation was facing a serious crisis—the maturity of an $85 million debt issue without cash or bank lines for payment.

The stock market collapse in 1973-1974 lessened the values AFC was able to realize from the sale of Bantam Books, Grosset & Dunlap, and the various theatre units gained from the NGC merger. Inflation caused insurance claims and expenses to soar above premium income. Housing starts plummeted during the 1974-75 recession.

The 1975 crisis taught Lindner a lesson he would never forget: leverage can kill. From that point forward, AFG would maintain conservative balance sheets and excess capital—a philosophy that persists today.

V. The Conglomerate Era: Diversification and Its Discontents (1975–1995)

The late 1970s and 1980s represented AFG's most turbulent period—an era of aggressive expansion, risky investments, and painful lessons about the limits of diversification. Carl Lindner had built a conglomerate, but maintaining it would prove far more difficult than assembling it.

Carl Lindner also had major investments in United Brands (formerly known as United Fruit - Chiquita Bananas which included plantations in El Salvador and other Central American countries), Gulf+Western (later Paramount Communications, now part of Viacom and CBS Corporation), Warner Communications, Kroger, Great American Broadcasting, General Cable and Penn Central.

The portfolio was eclectic to the point of bewilderment: bananas, broadcasting, books, baseball, and bonds. Lindner seemed to believe he could apply his value-investing principles across any industry. For a time, this worked.

But the 1980s brought temptation in the form of junk bonds. Whereas the Lindner companies and financial institutions once operated on conservative, cautious principles they later became involved in riskier ventures. Lindner insurance companies began to invest in junk bonds and other Lindner companies began to issue junk bonds. The SEC noted that Lindner companies were the single largest filers of new issues of securities in the U.S.

He became closely associated with Michael Milken and the others in the junk bond field to the extent that his financial institutions invested in the junk bonds of the others. This association with the junk bond king would prove costly.

The Mission Insurance debacle stands as the defining cautionary tale of this era. During the 1980s, AFC made major stock purchases in Mission Insurance Company (MIC), a property-casualty insurance concern in California, which concentrated on workers' compensation insurance. The insurance industry was beginning to emerge from the past decade's recession years, and by early 1984 Lindner had acquired a 49.9 percent interest in the MIC group. Mission Insurance Company's financial troubles soon came to light—a situation blamed on poor underwriting and the company's reinsurance business.

Stock plunged from $41 to $6.38 a share; a loss of $198 million was recorded in 1984, leaving a net worth of $43 million to support the $400 million of premiums in force. In March 1985, AFC initiated a recapitalization program for MIC.

The rescue failed. In October 1985, the California Insurance Commissioner declared MIC insolvent and placed it under conservatorship. For the first nine months of the year, AFC was $31 million in the red.

"Lindner's American Financial took a loss of $162 million, writing off the entire value of its stock interest and Mission loans." 1985 Mission Insurance Group failed. The insolvency incurred the largest payout by state guaranty funds for a single property/casualty insurance company failure.

The Mission disaster wasn't just a financial loss—it was a philosophical wake-up call. Buying undervalued assets was one thing; rescuing operationally troubled insurers was quite another. Insurance required deep expertise in underwriting, claims management, and reserve adequacy. Capital alone couldn't fix broken fundamentals.

However, the decade's most ambitious move involved a 49.9% stake in Mission Insurance Company (MIC), a California-based workers' compensation specialist, acquired in 1984; this investment aimed to capitalize on MIC's market position but unraveled when MIC was declared insolvent in 1985 amid reserve shortfalls and regulatory scrutiny, resulting in a $162 million pretax loss for AFC.

By the late 1980s, AFC had grown from a small company with $17.7 million in assets and 50 employees to a conglomerate with 53,000 employees and $12 billion in assets. The scale was impressive, but the focus was scattered.

By the early 1990s, AFC shifted toward internal development and selective formations to stabilize and diversify offerings, including the 1992 establishment of Great American Custom Insurance Services as a niche provider for high-risk commercial coverages.

The seeds of AFG's eventual strategic clarity were planted during this chaotic era. The specialty insurance businesses that performed consistently—equine mortality, crop insurance, trucking—shared common characteristics: niche markets, specialized expertise, and limited competition from generalist carriers. These successes would eventually guide the company's future direction.

VI. The 1995 Restructuring: Birth of Modern AFG

By the mid-1990s, the lessons of the conglomerate era had sunk in. Carl Lindner recognized that AFG needed simplification, focus, and a cleaner corporate structure. The 1995 restructuring would prove to be the organizational foundation for everything that followed.

AFC underwent several changes during the 1990s, the most significant being the 1995 merger with American Premier Underwriters, an insurance company partially owned by the Lindner family. Under the terms of the deal, a new holding company entitled American Financial Group Inc. (AFG) was created.

The merger combined two insurance-focused entities under a single, simplified structure. American Premier Underwriters traced its lineage to the remnants of Penn Central—the legendary railroad that collapsed in 1970 and was subsequently restructured. The Lindner family had acquired insurance assets from Penn Central's successors, and now those operations joined the Great American Insurance platform.

Then, in 1997, AFG began a restructuring effort in order to cut back on expenses and merged with two of its subsidiaries, AFC and American Financial Enterprises Inc. It also began selling off unprofitable businesses and, in 1998, GAIC sold the majority of its Commercial Lines Division to Ohio Casualty Insurance Company.

The divestitures signaled a philosophical shift. Rather than being all things to all customers, AFG would focus on businesses where it had genuine competitive advantage. Commoditized commercial lines—the bread-and-butter of many insurers—were sold to competitors willing to accept lower returns. AFG would pursue specialization.

On December 6, 2006, American Financial sold assets acquired from successors to the dissolution of the Penn Central Railroad including the land under Grand Central Terminal and the 156 miles of Metro North track leading to the New York City landmark to Argent Ventures.

This wasn't just financial engineering—it was strategic housecleaning. Real estate holdings from the Penn Central era, while valuable, had nothing to do with specialty insurance. Selling them freed up capital and management attention for the core business.

In 1997, AFG undertook restructuring by divesting underperforming units to streamline operations and focus on profitable niches, setting the stage for further inorganic growth. This culminated in the 1999 acquisition of Worldwide Insurance Co. from an Aegon USA subsidiary for an undisclosed sum, which expanded AFG's footprint in personal lines.

The restructuring established a template AFG would follow for the next quarter century: acquire specialty businesses with defensible niches, divest commoditized operations, maintain conservative capital levels, and return excess capital to shareholders. It was boring compared to the junk-bond-fueled dealmaking of the 1980s—and far more profitable.

VII. The Shift to Specialty P&C: Carl III and Craig Take the Helm (2005–2011)

In January 2005, a generational transition formalized what had been building for years. Carl H. Lindner III was elected Co-Chief Executive Officer in January 2005. He has served as Co-President and a director of American Financial Group since March 1996. He has been principally responsible for the property and casualty insurance operations since 1987.

S. Craig Lindner was elected Co-Chief Executive Officer in January 2005. He has served as Co-President and a director of American Financial Group since March 1996. From 1999 until the sale of the business in May 2021 he served as Chief Executive Officer of Great American Financial Resources, Inc., a wholly owned subsidiary of AFG that marketed traditional fixed and indexed annuities. Mr. Lindner also oversees the investment portfolios of AFG and its affiliated companies.

The co-CEO structure raised eyebrows on Wall Street. The co-CEO model is a rarity, particularly among the ranks of Fortune 500 companies. Some management pundits describe the model as the "knuckleball" of leadership: unconventional, tricky to execute, but with the potential to be exceedingly effective when mastered. If that's the case, Cincinnati-based American Financial Group's Carl H. Lindner III and S. Craig Lindner, who have served as co-CEOs since 2005, have perfected a pretty wicked knuckleball.

As co-CEOs and brothers, Carl and Craig Lindner demonstrate the true power of teamwork. The brothers say it's the right combination of common values, different talents and teamwork. Simply stated: "There's a bigger skill set between the two of us," says Carl.

The division of labor proved remarkably effective. Carl III focused on the specialty P&C operations, applying his two decades of experience in underwriting and claims to build out an increasingly specialized portfolio. Craig oversaw the annuity business and investment portfolio, areas requiring different skill sets.

Their father, Carl Lindner Jr., had set the stage. The parent company, AFG, is owned principally by the family of financier Carl Lindner, Jr., who bought the company in 1973 and served as its chairman until his death in 2011.

Carl, who describes himself as "an entrepreneur and calculated risk taker" gravitated toward AFG's property and casualty operations. "With every policy you write you are making a bet," he says. "You are taking a calculated risk." Under Carl's direction, AFG strategically repositioned its property and casualty operations, moving away from more commoditized offerings and into diversified, highly specialized niches.

The transformation accelerated. The company launched new divisions covering environmental liability, public sector risks, professional liability, aviation, and M&A insurance. Each represented a niche too small for major carriers to pursue aggressively, but large enough to generate meaningful profits for a focused specialist.

"My father loved the co-op concept, and he put a customized co-op program together for his sons," says Carl, who graduated from the University of Cincinnati. The educational philosophy matched the business philosophy: learn by doing, develop expertise through immersion.

He has served as the co-chief executive officer of American Financial Group since January 2005. He has also acted as chief executive officer and majority owner of FC Cincinnati since the club's founding in 2015. Carl III maintained the family tradition of Cincinnati civic involvement, eventually bringing Major League Soccer to his hometown.

When Carl Lindner Jr. passed away in October 2011, he left behind not just a company but a culture. Carl Lindner Jr. died on October 17, 2011, at age 92. When Carl Jr. died in 2011, his funeral "parade" stopped traffic and citizens lined the streets. That's making your mark.

VIII. The Specialty Niche Strategy Deep Dive

To understand AFG's competitive advantage, you must understand its structure. AFG's Specialty P&C Group is comprised of over 35 diversified businesses offering a wide range of specialty commercial coverages in three major groupings: Property and Transportation, Specialty Casualty and Specialty Financial. Many of our businesses are among the top performers in their respective industries.

Insurance specialties also include equine, trucking, executive liability, fidelity and crime, and agribusiness. To an outsider, this looks like a random collection of obscure markets. To AFG, it's a carefully curated portfolio of niches where specialized knowledge creates sustainable competitive advantages.

Our business has entrepreneurial spirit at its core, with a focus on accountability. Business autonomy in our Specialty P&C operations facilitates agility in underwriting, claims and policy servicing, and enables these businesses to develop distribution strategies and relationships in the unique markets they serve.

The decentralized operating model is central to AFG's success. AFG's operational model is built on a decentralized structure, empowering numerous specialized insurance businesses to operate with significant autonomy. Each unit focuses intensely on underwriting profitability within its specific niche market. This involves careful risk assessment, pricing discipline, and proactive claims management tailored to the unique characteristics of the insured risks.

AFG operates through approximately 35 distinct insurance businesses that collectively form the Great American Insurance Group. The company employs a decentralized approach, allowing each business unit to operate autonomously while maintaining central controls for investment and administrative functions. This entrepreneurial model enables local teams to respond quickly to market conditions while developing specialized products for niche markets.

Consider equine mortality insurance—a niche so obscure most investors don't know it exists. One of the world's leading providers of equine mortality insurance and related coverages. Racing horses, breeding stock, and show animals can be worth millions. Insuring them requires understanding bloodlines, veterinary risks, and the economics of horse racing. Generalist insurers can't compete.

We have been committed to insuring your farms, ranches and agricultural operations for over 100 years. From fruit and vegetable farms to equine operations, discover how we can help you manage the uncertainties of doing business.

The acquisition history tells the story of deliberate niche-building. Acquisition of Vanliner · 2010 · Start-up of Public Sector Division · Sale of Medicare supplement & critical illness businesses · 2012 · Start-up of Professional Liability Division · 2013 · Acquisition of Summit Holding Southeast, Inc. Start-up of Aviation Division · Acquisition of Public Sector renewal rights · 2014.

The Summit acquisition exemplified AFG's approach. AFG to add specialist workers' compensation carrier with leading market share in the Southeastern U.S. Based in Lakeland, FL, Summit is a leading provider of workers' compensation solutions with approximately $520 million of premium written. In addition, AFG made a capital contribution of approximately $140 million, bringing its capital investment in Summit to approximately $400 million. AFG did not use any external financing in the acquisition.

Deep Niche Expertise: Decades of focus on specific commercial lines allow for superior risk selection and pricing accuracy compared to generalist insurers. Disciplined Underwriting Culture: A consistent emphasis on profitability over sheer volume growth, reflected in consistently strong combined ratios, often outperforming the P&C industry average. Entrepreneurial Operating Model: The decentralized structure fosters agility, accountability, and allows business units to respond swiftly to market changes.

The product breadth is remarkable. The company offers property and transportation insurance products, such as physical damage and liability coverage for buses and trucks other specialty transportation niches, inland and ocean marine, agricultural-related products, and other commercial property coverages; specialty casualty insurance, including primarily excess and surplus, executive and professional liability, general liability, umbrella and excess liability, and specialty coverage in targeted markets, as well as customized programs for small to mid-sized businesses and workers' compensation insurance; and specialty financial insurance products comprising risk management insurance programs for lending and leasing institutions, fidelity and surety products, and trade credit insurance.

IX. The 2021 Annuity Sale: The Defining Strategic Inflection Point

The most consequential strategic decision of the modern AFG era came in January 2021. American Financial Group announced that it is selling its annuity business to Massachusetts Mutual Life Insurance Company in a $3.5 billion cash deal that primes the seller for growth in its specialty property/casualty businesses.

Under the terms of the agreement, MassMutual will acquire Great American Life Insurance Company (GALIC) and its two insurance subsidiaries, Annuity Investors Life Insurance Company and Manhattan National Life Insurance Company. At December 31, 2020, GALIC and its subsidiaries had approximately $40 billion of traditional fixed and indexed annuity reserves.

This wasn't a distressed sale. The annuity business was profitable. Craig Lindner had built it into a meaningful player in the fixed and indexed annuity market. But AFG's management recognized that the capital markets weren't properly valuing a conglomerate structure that combined specialty P&C with annuities.

Although AFG had long believed there was compelling value in operating both a Specialty P&C business and a market-leading fixed and indexed annuity business, the financial markets had not fully recognized the value of our market-leading annuity business. In MassMutual, AFG identified a buyer committed to establishing a subsidiary in Cincinnati, ensuring that the sale would have no impact on relationships with and commitments to its annuity policyholders and distribution channels. Importantly, we are very pleased that AFG's annuity employees continue to have compelling career opportunities in an annuity business that remains a part of the Greater Cincinnati community.

"With a strong balance sheet and substantial excess capital, we will continue to evaluate opportunities for deploying AFG's excess capital, including the potential for healthy, profitable organic growth, expansion of our specialty property and casualty niche businesses through acquisitions and startups that meet our target return thresholds, as well as share repurchases and special dividends."

The strategic logic was compelling. This transaction simplifies AFG's business model by creating a stand-alone specialty commercial Property and Casualty company that highlights AFG's long-standing top performance as a specialty P&C underwriter, with expertise in over 30 commercial insurance lines.

The capital deployment that followed demonstrated management's commitment to shareholder value. Total after-tax cash proceeds from the sale are approximately $3.5 billion. In connection with the closing of this transaction, the Company has declared a special, one-time cash dividend of $14.00 per share of American Financial Group Common Stock.

"AFG had approximately $3.2 billion of excess capital (including parent company cash and investments of approximately $3.0 billion) at June 30, 2021. The sale of our Annuity business to Massachusetts Mutual Life Insurance Company (MassMutual) significantly enhanced AFG's cash and excess capital.

The annuity sale marked the final step in AFG's decades-long evolution from diversified conglomerate to focused specialty insurer. What Carl Lindner Jr. had built through aggressive acquisition, his sons refined through disciplined divestiture. The company that emerged was leaner, more focused, and better positioned to compound capital over the long term.

X. Modern Era: The Pure-Play Specialty P&C Insurer (2021–Present)

Since the annuity sale, AFG has operated as a pure-play specialty P&C insurer—and the results have been exceptional. Core net operating earnings per share of $3.12 in the fourth quarter; full year core net operating earnings per share of $10.75. Full year 2024 ROE of 19.0%; 2024 core operating ROE of 19.3%.

In addition to producing an annual core operating return on equity in excess of 19%, net written premiums grew by 7% during the year.

The most recent quarters demonstrate operational momentum. AFG reported core net operating earnings of $224 million ($2.69 per share) for Q3 2025, a 16% increase from $194 million ($2.31 per share) in the same period of 2024.

AFG's specialty Property & Casualty operations showed significant improvement in underwriting profitability, with underwriting profit increasing 19% to $139 million and the combined ratio improving to 93.0% from 94.3% in the prior year.

Core net operating earnings for the third quarters of 2025 and 2024 generated annualized returns on equity of 19.0% and 16.2%, respectively.

The company continues expanding its specialty footprint through targeted acquisitions. Most recently, Great American Insurance Group acquired Radion Health, a managing general underwriter specializing in healthcare coverage for small and midsize businesses—another niche market where specialized expertise creates sustainable competitive advantage.

Although insurance and financial services have always been at the core of its businesses, nearly sixty-five years later, the Company has evolved into a holding company with over 35 market-leading insurance operations engaged in the sale of specialty commercial property and casualty (P&C) insurance across a variety of industries.

Great American Insurance Company has received an "A" (Excellent) or higher rating from the AM Best Company for 115 years (most recent rating evaluation of "A+" (Superior) affirmed December 15, 2023). That 115-year streak of A-ratings is remarkable—a testament to conservative reserving and disciplined underwriting across more than a century of insurance cycles.

International expansion continues, though at a measured pace. Start-up of Great American's Singapore branch. The company approaches overseas markets with the same discipline it applies domestically: enter only when there's genuine expertise to leverage.

XI. Capital Allocation & Shareholder Returns: The AFG Playbook

AFG's capital allocation philosophy deserves special attention because it demonstrates what happens when management treats shareholders as owners rather than nuisances.

American Financial Group, Inc. (AFG) has increased its dividends for 20 consecutive years. Two decades of consecutive increases puts AFG among the elite dividend growth companies in financial services.

Ex-Date: Nov 17, 2025 · Dividend Safety · A+ 20 years of consecutive dividend increase.

But regular dividends tell only part of the story. AFG has made special dividends a signature element of its capital return program. AFG also announced a $2.00 per share special dividend, payable on November 26, 2025, highlighting its strong capital position and commitment to shareholder returns.

AFG returned approximately $791 million to shareholders in 2024, including $545 million in special dividends ($6.50 per share).

The philosophy is straightforward: generate excess capital through disciplined underwriting and investment returns, then return that capital to shareholders unless it can be deployed at attractive risk-adjusted returns. It's Buffett-style capital allocation, applied consistently year after year.

AFG paid cash dividends of $4.80 per share during the fourth quarter, which included a $4.00 per share special dividend paid in November. For the three and twelve months ended December 31, 2024, AFG's growth in book value per share plus dividends was 3.4% and 23.0%, respectively.

The company's book value per share was $53.18 at year-end, with growth in book value plus dividends reaching 23.0% for the year.

The management team has articulated clear expectations. While AFG does not provide earnings guidance, for 2025 we expect that performance in line with the assumptions underlying our 2025 business plan would result in core operating earnings per share of approximately $10.50 and generate a very strong core operating return on equity excluding AOCI of approximately 18%. These assumptions include 5% growth in net written premiums compared to 2024, a 92.5% calendar year combined ratio, a reinvestment rate of approximately 5.75%, and a return of approximately 8% on our $2.7 billion portfolio of alternative investments.

XII. Competitive Landscape & Strategic Analysis

The Specialty Insurance Moat

AFG operates in an industry characterized by intense competition, cyclical pricing, and catastrophic tail risks. Yet the company has managed to generate consistent returns on equity approaching 20%—well above its cost of capital—for decades. How?

Porter's Five Forces Analysis:

Threat of New Entrants: Low to moderate in specialty niches. While insurance broadly has low barriers to entry, AFG's specific niches—equine mortality, crop insurance, moving and storage—require decades of accumulated expertise in underwriting and claims. A new entrant can't simply hire actuaries; they need institutional knowledge about horse bloodlines, crop yields by county, or the theft patterns affecting household moving companies.

Bargaining Power of Buyers: Moderate. Most AFG customers are small to mid-sized businesses who lack sophisticated insurance knowledge. AFG's agents serve as trusted advisors rather than commoditized brokers. The relationship nature of specialty insurance reduces price sensitivity.

Bargaining Power of Suppliers: Low. AFG's primary suppliers are capital markets (for investment returns) and reinsurers. The company maintains strong relationships with reinsurers and retains significant risk on its own balance sheet.

Threat of Substitutes: Low. For most specialty commercial risks, there's no substitute for insurance. Self-insurance requires scale that AFG's target customers lack.

Competitive Rivalry: Moderate within niches. Large generalist carriers typically don't pursue the niche markets AFG dominates because the premium pools are too small to move their needle. Competition primarily comes from other specialty insurers, but AFG's breadth across 35+ niches provides diversification most competitors lack.

Hamilton Helmer's 7 Powers Framework:

Scale Economies: Limited. Insurance doesn't have traditional manufacturing scale economies, though AFG's diversification across niches provides some portfolio benefits.

Network Effects: Minimal.

Counter-Positioning: Strong. AFG's decentralized model and niche focus represent a strategy that large insurers find unattractive to replicate because it would cannibalize their existing high-volume businesses.

Switching Costs: Moderate. Insurance relationships, particularly in specialty lines, involve significant trust and institutional knowledge. Switching insurers means re-establishing relationships and re-underwriting complex risks.

Branding: Strong within niches. The Great American brand carries weight in equine circles, among trucking companies, and with crop producers.

Cornered Resource: Partially present. AFG's century of underwriting data in specific niches represents proprietary information competitors can't easily replicate.

Process Power: Strong. The decentralized operating model, disciplined underwriting culture, and conservative capital management represent embedded organizational capabilities that competitors struggle to copy.

Key Performance Indicators for Investors

For investors tracking AFG, three metrics matter most:

1. Combined Ratio: The single most important metric in property and casualty insurance. A combined ratio below 100% means the company earns underwriting profit before investment income. AFG has consistently delivered combined ratios in the 89-94% range across market cycles—exceptional for the industry.

2. Core Operating Return on Equity: AFG targets approximately 18-20% ROE on a core operating basis (excluding non-recurring items). Sustained ROE at this level indicates disciplined underwriting and effective capital allocation.

3. Book Value Per Share Plus Dividends Growth: This metric captures total shareholder value creation, including both retained earnings and cash returned to shareholders. AFG has delivered 20%+ growth on this measure in recent years.

Bull Case

- Continued hard market conditions allow for rate increases exceeding loss cost inflation

- The specialty niche strategy provides protection from commoditization

- Disciplined capital allocation through special dividends and opportunistic buybacks

- Stable family ownership creates long-term orientation

- Decades of accumulated expertise in niche markets represents sustainable advantage

- Conservative reserving reduces risk of adverse development surprises

Bear Case

- Social inflation continues pressuring liability lines, particularly in casualty segments

- Climate change increases frequency and severity of property catastrophes

- Crop insurance faces weather volatility and potential government policy changes

- The co-CEO succession question remains unaddressed (Carl III and Craig Lindner are both in their late 60s)

- Alternative investments introduce earnings volatility

- Premium growth could decelerate if management maintains pricing discipline while competitors chase market share

Risk Factors to Monitor

Social Inflation: The trend of increasing jury verdicts and settlement amounts poses ongoing challenges to casualty underwriting. AFG has responded with rate increases and tighter underwriting, but the secular trend remains concerning.

Climate Risk: AFG's crop and property businesses face direct exposure to climate volatility. While diversification helps, multi-state droughts or increased hurricane frequency could pressure results.

Regulatory Environment: Insurance is heavily regulated at the state level. Changes in workers' compensation regulations, rate approval processes, or reserving requirements could impact profitability.

Succession Planning: With Carl III and Craig Lindner having led the company since 2005, investors should monitor how the next generational transition will be handled. Craig Lindner Jr. was elected to AFG's Board of Directors in February 2025. Mr. Lindner currently serves as the Divisional President of AFG Real Estate Investments, a position he has held since 2017. The fourth generation is being prepared, but execution risk remains.

XIII. The Lindner Legacy

The AFG story illustrates timeless principles of wealth creation: start small, reinvest relentlessly, expand within your circle of competence, learn from mistakes, and compound over decades rather than seeking shortcuts.

Mr. Lindner was a patriot who loved America and never forgot the work ethic he learned in the family's Norwood dairy store. Another of his calling cards read: "Only in America. Gee, am I lucky."

From an $8.28 first-day sales total in a Depression-era ice cream shop to a Fortune 500 insurance holding company generating billions in premiums—the Lindner family built something extraordinary. Not through financial engineering or leverage, but through disciplined underwriting, patient capital allocation, and multi-generational commitment to Cincinnati.

The company's headquarters moved in 2011 to the Great American Insurance Building at Queen City Square—a gleaming tower overlooking the city where Carl Lindner Jr. once delivered milk from the back of a truck. Currently, Great American Insurance Company is rated A+ by S&P, A1 by Moody's and "A+" (Superior) by A.M. Best. Great American Insurance Company is one of only four companies rated "A" (Excellent) or better by A.M. Best for more than 110 years.

That 115-year streak of excellence—spanning two world wars, the Great Depression, multiple insurance crises, and countless economic cycles—captures something about what sustainable business building looks like. It's not glamorous. It doesn't generate headlines. But it compounds.

For long-term investors, AFG represents something increasingly rare in modern markets: a company that knows exactly what it does, does it consistently well, and shares the fruits of that labor with shareholders through generous dividends and disciplined capital allocation. In a world of disruption and transformation, there's something refreshing about a specialty insurer that has been rating horses, inspecting crops, and managing trucking risks for generations—and plans to keep doing so for generations to come.

The story continues to be written. But the foundation built by a high school dropout delivering milk in Depression-era Cincinnati has proven remarkably durable. As Carl Lindner Jr. might have said: "The harder I work, the luckier I get."

Disclosure: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

XIV. Looking Ahead: Strategic Priorities and Industry DynamicsAFG's near-term strategic priorities reflect both the opportunities and challenges facing the specialty insurance sector in 2025. During the company's third quarter 2025 earnings call, Co-CEO Carl Lindner III emphasized the company's ability to find opportunities in uncertain times, while Co-CEO Craig Lindner highlighted AFG's capital management strategy, noting they have "retained a lot of dry powder" for potential share repurchases.

Looking ahead, AFG projects a rebound in premium growth for 2026 and anticipates a long-term annual return of 10% from its alternative investment portfolio. The company's financial flexibility positions it well to pursue growth opportunities as they arise. The company maintains above-target capital levels for all rating agencies and holds financial strength ratings of A+ from both A.M. Best and Standard & Poor's, and A1 from Moody's. AFG has no debt maturities until 2030 and no borrowings under its $450 million credit line, providing significant financial flexibility.

The broader specialty insurance market provides a favorable tailwind for AFG's strategy. The specialty insurance market is experiencing unprecedented transformation. Analysis of current industry data reveals the market is on a robust growth trajectory, with projections indicating expansion from approximately $142 billion in 2024 to nearly $279 billion by 2031. Specialty insurance is experiencing robust growth, outpacing standard insurance lines.

Several industry dynamics favor AFG's positioning:

Climate and Catastrophe Risk: Rising natural catastrophes continue to threaten insurance affordability and accessibility, with the average annual cost from global natural catastrophes reaching a new high of $151 billion. Traditional insurers have responded to worsening wildfires, hurricanes, and floods by restricting coverage or exiting high-risk regions. This vacuum is being filled by specialty markets through parametric catastrophe covers, surplus lines property policies, and facility programs for difficult risks.

Technology Transformation: The global specialty insurance market is projected to exhibit a CAGR of 7% during 2025-2033. The rising digital transformation of the insurance industry, along with the increasing utilization of AI, ML, blockchain technology, big data analytics, and IoT devices with specialty insurance for more precise risk assessment and policy customization, is primarily driving the global specialty insurance market.

Regulatory Complexity: Governments worldwide are tightening compliance and regulations requirements, pushing companies to adopt specialty insurance for directing difficult legal frameworks. The European Union's GDPR and evolving ESG disclosure rules are driving demand for specialized liability and compliance covers.

However, challenges persist that AFG must navigate. Complex liability and class action issues will continue to develop in 2025. The number of class actions is expected to continue to grow and the settlement of funds established has to be managed. The insurance industry will be expected to contribute to settlement programs.

The casualty environment remains particularly demanding. After years of rising rates, the market appears to be stabilizing in many areas such as property, cyber, and management liability. However, casualty and homeowners remains in an unstable "hard market".

While analysts acknowledged AFG's strong premium growth and investment income, concerns were raised about reserve development in social inflation-exposed lines and rising expense ratios. Management has factored in $60 million to $70 million in wildfire losses for 2025. While AFG's catastrophe risk management is robust, these losses pose a challenge to overall profitability.

The third quarter of 2025 marked the company's 37th consecutive period of property and casualty renewal rate increases, with core operating return on equity reaching 19% and continued improvements in underwriting margins. This pricing discipline remains central to AFG's strategy for navigating market challenges.

XV. The Fourth Generation: Succession and Continuity

The question of leadership succession looms for any family-controlled enterprise, and AFG is no exception. With Carl III and Craig Lindner both having served as co-CEOs since 2005, the company must eventually plan for the next generational transition. The fourth generation is already being positioned for leadership responsibility. In February 2025, Craig Lindner Jr. was elected to AFG's Board of Directors. Mr. Lindner currently serves as the Divisional President of AFG Real Estate Investments, a position he has held since 2017. Mr. Lindner joined AFG in 2002.

Lindner brings 20 years of experience in real estate investing and insurance and has played a key role in overseeing AFG's investments in real estate equity and debt. He joined AFG in 2002 and has served as Divisional President of AFG Real Estate Investments since 2017. In this role, he manages the company's portfolio of apartments, resort and marina properties, other commercial real estate, and a large portfolio of commercial mortgages.

Alongside the fourth-generation Lindner, David L. Thompson Jr. was elected to AFG's Board of Directors in February 2025. Mr. Thompson currently serves as Chairman of the Board, President and Chief Operating Officer of Great American Insurance Company, AFG's flagship property and casualty insurance company. Since joining Great American in 2006, he has served in various senior management capacities and has had direct executive oversight of many of Great American's specialty property and casualty businesses, as well as its corporate reinsurance operations, the Company's wholly owned retail agency, Dempsey & Siders, and was instrumental in the formation of its Predictive Analytics function.

The co-CEOs explained the strategic importance of these appointments. "We are pleased to welcome Craig and David to our Board of Directors. Each of them brings extensive operating experience in their respective areas of oversight within our property and casualty and investment operations, making them both valuable additions to our Board. Importantly, Craig and David's roles on the Board demonstrate our family's continued commitment and involvement as significant shareholders of AFG. Their knowledge of our business, culture and values and their passion for the work we do will help to guide our company through numerous opportunities in the years to come."

Mr. Berding was elected President of AFG in June 2023. He has served as President of American Money Management Corporation (AMMC) since January 2011. Prior to his election as President, he held a number of investment-related executive positions with AMMC and other AFG subsidiaries. Mr. Berding has spent his entire 35+-year career as an investment professional with the Company and its affiliates.

The combination of a fourth-generation family member and seasoned operational executives suggests AFG is taking a deliberate approach to succession—preserving family involvement while ensuring day-to-day operations remain in experienced hands.

XVI. Conclusion: The Compounding Machine

The American Financial Group story defies the conventional narrative of American capitalism. In an era obsessed with disruption, blitzscaling, and technological transformation, AFG has quietly built an empire by doing something decidedly old-fashioned: underwriting risks that others overlook, managing capital conservatively, and returning excess profits to shareholders.

From Carl Lindner Jr.'s Depression-era milk routes to today's pure-play specialty P&C insurer, the through-line has been discipline. Not the discipline of spreadsheets and corporate bureaucracy, but the discipline that comes from understanding your circle of competence and refusing to stray beyond it—even when Wall Street rewards empire-building with higher stock prices.

The company's evolution tells a cautionary tale embedded within a success story. The conglomerate era of the 1980s, with its junk bond investments and the Mission Insurance debacle, demonstrated what happens when ambition outpaces expertise. The $162 million loss from Mission Insurance wasn't just a financial setback—it was an education. The lessons learned during that turbulent decade informed the strategic focus that emerged in the 1990s and accelerated after the 2021 annuity sale.

The company maintains above-target capital levels for all rating agencies and holds financial strength ratings of A+ from both A.M. Best and Standard & Poor's, and A1 from Moody's. AFG has no debt maturities until 2030 and no borrowings under its $450 million credit line, providing significant financial flexibility.

The decision to sell the annuity business to MassMutual exemplifies the strategic clarity that now defines AFG. Rather than clinging to a profitable but capital-intensive business, management recognized that focus trumps diversification when you have genuine competitive advantage in your core operations. The $3.5 billion in proceeds didn't sit idle—it funded special dividends, share repurchases, and acquisitions that strengthened the specialty P&C franchise.

The company's extensive buyback program has now repurchased over 46.9 million shares since 2010, shrinking its share count and highlighting a longstanding commitment to shareholder returns.

For investors, AFG represents something increasingly rare: a company that knows exactly what it does well and has the discipline to keep doing it. The decentralized operating model, with its 35+ specialty insurance businesses each pursuing their niche with entrepreneurial intensity, creates barriers to competition that are difficult to replicate. A new entrant can't simply hire underwriters and enter the equine mortality or moving and storage insurance markets—they need decades of loss data, industry relationships, and claims expertise.

Net investment income increased by 5% year over year despite muted returns from alternative investments. As Carl Lindner III noted, "Our compelling mix of specialty insurance businesses, entrepreneurial culture, disciplined operating philosophy, and an astute team of in-house investment professionals continue to position us well for the future and enable us to continue to create value for our shareholders."

The broader specialty insurance industry provides tailwinds for AFG's strategy. The specialty insurance market is experiencing unprecedented transformation. Analysis of current industry data reveals the market is on a robust growth trajectory, with projections indicating expansion from approximately $142 billion in 2024 to nearly $279 billion by 2031. As traditional insurers retreat from complex risks and catastrophe-prone regions, specialists like AFG stand ready to fill the void.

Yet challenges remain. Social inflation continues pressuring casualty lines. Climate change increases the frequency and severity of weather-related losses. The competitive landscape evolves as private equity capital flows into specialty insurance distribution. And the succession question—while being addressed—remains an execution risk for any family-controlled enterprise.

American Financial Group reported third-quarter 2025 results that exceeded analyst expectations on revenue, earnings, and underwriting performance. This quarter marked the company's 37th consecutive period of property and casualty renewal rate increases, with core operating return on equity reaching 19% and continued improvements in underwriting margins.

What Carl Lindner Jr. started with a $1,200 loan in 1940 has grown into something remarkable—not because it's flashy or innovative in the conventional sense, but because it compounds. The milk routes became convenience stores. The convenience stores became savings and loans. The savings and loans became insurance companies. And the insurance companies became a focused specialty platform that generates consistent double-digit returns on equity.

The funeral parade that stopped Cincinnati traffic in 2011 when Carl Lindner Jr. passed away spoke to something deeper than business success. It spoke to what it means to build institutions that serve communities, employ generations of workers, and create value that compounds across decades. AFG remains headquartered in Cincinnati, employing thousands of Ohioans, supporting local institutions, and maintaining the civic commitment that defined its founder.

In the end, the AFG story is about time horizons. While competitors chase quarterly earnings and activist investors demand immediate returns, the Lindner family has consistently thought in decades. They've built a business designed to endure market cycles, leadership transitions, and strategic pivots. That patient capital mindset—inherited from a father who taught his sons that you can do anything if you're willing to work hard enough—remains the company's most durable competitive advantage.

For students of business history, AFG offers lessons that transcend the insurance industry: the power of focus over diversification, the importance of learning from mistakes, the value of family culture in building durable enterprises, and the magic of compounding when applied with discipline over long time periods.

As Carl Lindner Jr. might have said, only in America could a dairy farmer's son build something this enduring. And gee, were they lucky—or was it something more?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube