Owens Corning: From Accidental Discovery to Building Materials Titan

I. Introduction: The Pink Company with Seven Decades on the Fortune 500

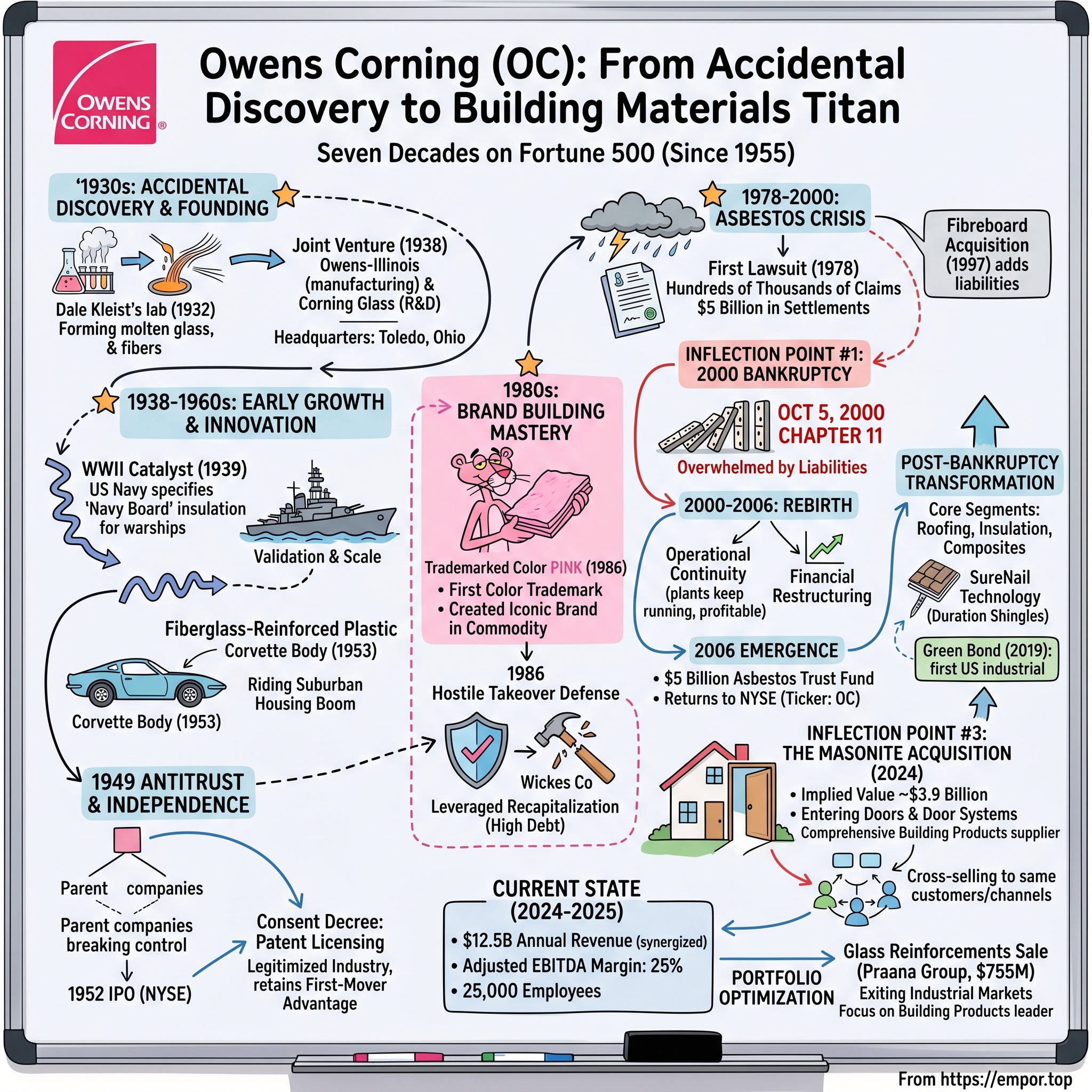

Picture a suburban American home—any suburban American home. The pink batts of insulation tucked into the walls. The asphalt shingles protecting the roof from rain and sun. There's a better than even chance that an 87-year-old company based in Toledo, Ohio, made those products. Owens Corning is an American company that develops and produces insulation, roofing, and fiberglass composites and related products. It is the world's largest manufacturer of fiberglass composites.

What makes Owens Corning's story worthy of deep examination? Start with the numbers: The company reported net sales of $11.0 billion in 2024, a 13% increase from the prior year. But longevity might be the more impressive metric. Owens Corning has been a Fortune 500 company every year since the list was created in 1955. Think about that for a moment. Only a handful of companies have maintained that distinction through seven decades of economic cycles, technological disruptions, and competitive upheaval.

The central question of Owens Corning's story is deceptively simple: How did an accidental laboratory discovery become a multi-billion-dollar industrial powerhouse that survived one of the largest asbestos bankruptcy settlements in American history and emerged stronger on the other side?

The answer involves material science innovation, branding genius (yes, that Pink Panther), crisis management that would make turnaround specialists take notes, and a strategic transformation that continues today. All outstanding Masonite common shares were acquired by Owens Corning for $133.00 per share, with an implied transaction value of approximately $3.9 billion—a May 2024 deal that reshaped the company's portfolio and signaled where management sees future growth.

The themes woven through Owens Corning's history—the value of material science moats, the surprising power of B2B branding, the importance of operational discipline during crisis, and the art of capital allocation—offer lessons for any student of business strategy. Let's dig in.

II. The Accidental Discovery & Founding Context (1930s)

The Origin Story: When Compressed Air Met Molten Glass

The year was 1932. The Great Depression had the American economy in its grip. In Newark, Ohio, at the Owens-Illinois Glass Company's research facilities, a young researcher named Dale Kleist was engaged in seemingly mundane work. At Corning Glass in 1932, researcher Dale Kleist was trying to join glass blocks together to create transparent, weatherproof walls.

What happened next would launch an entire industry. During an unsuccessful attempt to use glass as a sealant, a stream of compressed air hit the flow of molten glass, forming a spray of tiny fibers. Most researchers might have written this off as a failed experiment. Kleist and his colleagues—Games Slayter and Jack Thomas—recognized something remarkable in that spray of glass fibers.

Later that same year, the process was refined by using steam rather than compressed air to attenuate glass fibers. The result was a glass fiber material that was thin enough to be used as a commercial fiber glass insulation. A magazine article from 1938 would proclaim it "a new marvel of science," noting that a single marble, weighing only a quarter-ounce, could produce 90 miles of glass fiber.

This accidental discovery came at a moment when both major American glassworks were looking for new applications. As it happened, Corning Glass, in upstate New York, had also been experimenting with producing glass fibers for insulation, and in 1935 the company suggested to Owens-Illinois that they work together.

The Parent Companies: Glass Titans Join Forces

Understanding Owens Corning requires understanding its parentage. Headquartered in Toledo, Ohio, Owens Corning was founded in the 1930s as a joint venture of Owens-Illinois and Corning Glass. The company was originally established to research and manufacture glass fiber, for which both Owens-Illinois and Corning Glass saw great potential as an insulation material.

Corning Glass Works brought a storied history of material science innovation. Pyrex was first introduced in 1915 as a line of clear, low-thermal-expansion borosilicate glass whose resistance to chemicals, electricity, and heat made it ideal for laboratory glassware and kitchenware. The company had been founded in 1851 and had developed expertise in specialty glass manufacturing that few could match.

Owens-Illinois, meanwhile, had commercialized bottle-making and industrial glass applications. Together, the two companies possessed complementary capabilities: Corning's research prowess and Owens-Illinois's manufacturing scale.

Birth of a New Industry

The company was officially founded on October 31, 1938. Headquarters were established in Toledo, Ohio. The choice of location reflected Owens-Illinois's influence—Toledo was already a glass manufacturing center, with skilled labor and established supply chains.

The timing was both challenging and fortuitous. The Depression was still weighing on the economy, but the construction industry was beginning to stir. More importantly, the first commercial product was the all-fiber (AF) fiberglass wool, which rapidly transformed the insulation sector.

In 1938, the company sales reached $2.6 million. This might seem modest by today's standards, but for a startup venture selling an entirely new material, it demonstrated genuine commercial viability. The insulation market was ready for disruption—existing materials like mineral wool were adequate but not optimal, and the new fiberglass promised better performance at competitive cost.

What made fiberglass insulation revolutionary? It combined several desirable properties: low thermal conductivity (meaning it actually worked as insulation), fire resistance, durability, and relatively low manufacturing cost once scale was achieved. The fine glass fibers trapped air pockets, and those air pockets provided the insulating effect.

The joint venture structure reflected the economic realities of the Depression era. Neither parent company wanted to bear the full risk of commercializing an unproven technology. By pooling resources and expertise, they could pursue the opportunity while limiting downside exposure.

III. Early Growth & Innovation (1938-1960s)

World War II: The First Major Break

Every successful company needs a catalyst for growth. For Owens Corning, that catalyst wore a Navy uniform. In 1939, the U.S. Navy Bureau of Ships made Owens-Corning insulation standard in new warship construction. Warship insulation, called Navy Board, was a permanent form-board insulation covered with woven continuous fiber cloth.

This military specification represented validation at the highest level. If fiberglass insulation could handle the demanding environment of naval vessels—heat, cold, vibration, salt water—it could certainly handle residential and commercial buildings. The Navy contract also provided scale and predictability, allowing Owens-Corning to invest in manufacturing capacity.

World War II accelerated development across multiple applications. Owens-Corning produced a prototype boat hull constructed of fiber glass-reinforced plastic in 1944. In 1945, the company worked with an automaker to produce the first fiberglas-reinforced plastic car body. In 1953, General Motors used this type of body in the Chevrolet Corvette.

The Corvette connection deserves emphasis. When Chevrolet launched America's sports car in 1953, it featured a body made of fiberglass-reinforced plastic. This was revolutionary—no major automaker had ever produced a car with a plastic body. The Corvette demonstrated that fiberglass composites could deliver strength, durability, and design flexibility that traditional materials couldn't match.

Post-War Boom: Riding the Suburban Wave

Owens Corning succeeded because it made effective and affordable insulation that quickly became popular with homeowners and builders. The demand for the product was exceptionally high during the housing boom following World War II.

Consider the context. Millions of GIs were returning home. The federal government was backing mortgages through the GI Bill. Levittown and its imitators were transforming farmland into subdivisions. Every new house needed insulation, and Owens-Corning was positioned to supply it.

The company's manufacturing capabilities expanded dramatically. New plants opened across the country to serve regional markets—shipping bulky insulation products long distances was economically challenging. This geographic dispersion created a natural competitive barrier; any new entrant would need to build a national manufacturing footprint to compete effectively.

Antitrust & Independence: Forced to Stand Alone

Success brought regulatory scrutiny. Owens Corning was so successful that in 1949 Owens-Illinois and Corning Glass Works were accused of illegally monopolizing the fiberglass industry. Under a court-mandated consent decree, Owens Corning was required to license its patents to competitors, and both parent companies were forced to relinquish control.

This antitrust action fundamentally reshaped the company's trajectory. The company held its initial public offering on the New York Stock Exchange in 1952. What had been a controlled joint venture was now an independent public company, accountable to shareholders and free to chart its own strategic course.

The consent decree requiring patent licensing might seem like a setback, but it had interesting consequences. By enabling competitors, it legitimized fiberglass as a standard insulation material. The market expanded faster than it might have under a monopoly structure. Owens-Corning retained first-mover advantages in brand recognition, manufacturing efficiency, and technical expertise even as competitors entered.

Revenue Growth & Strategic Expansion

By 1971, Owens-Corning's annual revenue was over $500 million. Sales surpassed $1 billion in 1976, and sales were over $2 billion by 1979.

Revenue growth from $2.6 million in 1938 to over $2 billion four decades later represents a compound annual growth rate of approximately 18%—an extraordinary trajectory sustained over an extended period. This growth reflected both market expansion and strategic diversification.

In 1977, Owens-Corning acquired Frye Roofing and began production of fiberglass mat to replace traditional paper mat used in roofing. This acquisition represented a pivotal strategic decision. Roofing shingles had traditionally used organic felt (paper-based material) as a base mat. Fiberglass mat offered superior fire resistance and durability. By entering roofing, Owens-Corning could leverage its core competency in fiberglass manufacturing while diversifying into a large adjacent market.

The roofing entry would prove prescient. Today, roofing represents Owens Corning's largest business segment and its most profitable. The company's vertical integration—from raw materials through finished shingles—creates cost advantages and quality control benefits that competitors struggle to match.

IV. The Pink Panther Era: Brand Building Mastery (1980s)

Creating an Iconic Brand in a Decidedly Non-Iconic Category

How do you make insulation memorable? This was the challenge Owens Corning faced in 1980. Insulation is a commodity product that homeowners rarely think about—it's hidden in walls and attics, purchased infrequently, and often selected by contractors rather than end consumers.

In 1980, Owens Corning entered into a long-standing agreement to use the Pink Panther as its brand mascot. The choice was inspired. The Pink Panther—cool, sophisticated, instantly recognizable—transformed how consumers thought about a mundane building material.

But the pink color itself predated the cartoon cat. The company began adding red dye to the naturally tan or yellowish insulation to distinguish it from their rivals' products. Introduced in 1956, the bright pink color became such a powerful marketing tool that the company trademarked it in 1985.

The color PINK was trademarked through Owens-Corning in 1986, making it the first company to trademark a color. This trademark was legally significant and strategically brilliant. No competitor could produce pink insulation without facing legal consequences. The color itself became a brand asset—consumers walking through a home improvement store could immediately identify Owens Corning products.

The Pink Panther campaign ran for decades, becoming one of the most enduring corporate mascots in American advertising. The long-legged cartoon feline, who shares his color with Fiberglas insulation, remains one of the most recognized American advertising figures. Even today, homeowners who couldn't name three insulation manufacturers can probably recall "the pink stuff."

The Asbestos Problem Emerges

While the company was building brand equity in its core insulation business, a legacy issue was quietly growing. Owens Corning, in the 1950s, became involved in the asbestos business when it entered into an agreement to distribute Owens-Illinois' Kaylo-brand high-temperature calcium silicate insulation containing asbestos. In the late 1950s Owens Corning bought all Kaylo's assets and began manufacturing the insulation product.

As the dangers of asbestos became better known in the 1970s, Owens Corning removed asbestos from Kaylo. Owens Corning stopped using asbestos in its manufacturing in 1972. But the damage had been done. Tens of thousands of workers had been exposed to asbestos-containing products over two decades. The lawsuits were coming—it was only a matter of time.

The 1986 Hostile Takeover Defense

The company hit a rough patch in the 1980s during a slowdown in construction and new homebuilding. Owens Corning also fought off a hostile takeover by taking on a lot of debt.

Owens Corning in 1986 rejected a hostile takeover offer from Wickes Companies Inc. To fend off the raiders, management executed a leveraged recapitalization—taking on substantial debt to buy back shares and make the company less attractive to acquirers.

A study examined 22 U.S. companies that underwent leveraged recapitalization between 1982 and 1994, including USG, Owens Corning, Phillips Petroleum, Texaco, Union Carbide, and Goodyear Tire and Rubber. Owens Corning was in notable company. These leveraged recapitalizations were characteristic of the 1980s corporate landscape, where hostile raiders targeted companies seen as undervalued.

Former CEO William Boeschenstein is remembered for his leadership during what Owens Corning describes as "a hostile takeover attempt that began in 1986," which ended with the company maintaining its status as an independent entity.

The defensive recapitalization preserved independence, but the debt load would prove problematic. As the decade closed, the company's annual revenue had reached $3 billion. Growth was strong, but the balance sheet was stressed—and the asbestos litigation wave was building.

V. The Asbestos Crisis & Road to Bankruptcy (1978-2000)

First Lawsuits: The Storm Gathers

Owens Corning faced its first asbestos lawsuit in 1978 when shipyard workers claimed the company knew about the dangers of asbestos in its products. This lawsuit named Owens-Corning and 14 other manufacturers, arguing that the companies had known asbestos was dangerous as early as 1938 but hadn't warned workers about the risks.

For context, asbestos litigation represented one of the largest mass tort actions in American history. Dozens of companies that had manufactured, distributed, or used asbestos-containing products faced lawsuits from workers who developed asbestosis, mesothelioma, and other respiratory diseases.

Over the next three decades, the company was named in hundreds of thousands of asbestos lawsuits. The scale was staggering. By 1990, Owens-Corning was the defendant in about 84,500 asbestos-related lawsuits. And the number kept growing.

The Escalating Crisis

By 2000, it had settled with 440,000 people who claimed Owens Corning's products caused them to develop asbestos-related illnesses. Each settlement required cash payments. The cumulative drain on the company's resources was enormous.

Owens Corning grouped 176,000 asbestos claims in 1998 into the National Settlement Program and planned to settle them for $1.2 billion to avoid bankruptcy. But the number of claims grew quickly to 237,000.

The 1998 settlement attempt illustrated the challenge. Even as Owens Corning tried to resolve existing claims, new claims kept arriving. The number of potential plaintiffs seemed almost unlimited—anyone who had worked with or around asbestos-containing products for decades could potentially file a claim.

The Fibreboard Acquisition: A Fateful Deal

Owens Corning acquired Fibreboard Corporation in 1997. Fibreboard also used asbestos in construction products in the past. Owens Corning took on its asbestos liabilities with the acquisition.

This acquisition might seem puzzling—why would a company already facing massive asbestos liability acquire another company with similar problems? The strategic logic involved consolidating market position in vinyl siding and other building materials. But the additional asbestos exposure would prove costly.

The company was ordered to pay $5 million to an asbestos victim in 1997, making it the highest jury verdict in the history of the United States for a single non-malignant asbestos case. Individual verdicts of this magnitude signaled that juries were increasingly unsympathetic to corporate defendants in asbestos cases.

The Final Straw: October 2000

On October 5, 2000, Owens Corning shares fell to $1 per share when Owens Corning declared bankruptcy and admitted that it had been overwhelmed by the asbestos liabilities.

On October 5th, 2000, Owens Corning filed its petition for Chapter 11 bankruptcy. The stock had fallen from a high of $41 in May 1999 to just $1—a 97.5% decline in roughly 18 months. Shareholders were effectively wiped out.

At the time of filing, the company had 460,000 lawsuits against it and had already paid out $5 billion in settlements. The arithmetic was simply impossible. The company's balance sheet could not support both ongoing operations and the unlimited liability represented by asbestos claims.

Struggling under the growing demands of these lawsuits on its cash flow, Owens Corning filed a petition for reorganization under Chapter 11 of the U.S. Bankruptcy Court. The filing enabled the company "to refocus on operating its business and serving its customers, while it develops a plan of reorganization."

VI. Inflection Point #1: Bankruptcy & Rebirth (2000-2006)

Six Years in Chapter 11: Operations Continue, Lawyers Negotiate

What makes Owens Corning's bankruptcy different from many corporate restructurings was the extended duration and the remarkable operational continuity during the process. The company spent six years in Chapter 11—from October 2000 to October 2006.

Owens Corning eked out a profit of $39 million in 2001, a significant improvement from its results in 2000 when it reported a net loss of $479 million for the year. The company managed to get back into the black in 2001 despite a slight decline in revenue to $4.76 billion from $4.94 billion in 2000.

This is crucial to understand: the underlying business remained profitable throughout bankruptcy. Roofing shingles kept rolling off production lines. Insulation kept shipping to home improvement stores and contractors. Customers, for the most part, continued buying. The Chapter 11 process separated legal and financial restructuring from operational management.

To resolve all of these lawsuits, Owens Corning sought bankruptcy protection in October 2000. As a condition of filing for Chapter 11 bankruptcy, the company had to create an asbestos bankruptcy trust fund to provide compensation to future victims.

The 2006 Emergence: One of the Largest Asbestos Settlements in History

Owens Corning filed for Chapter 11 bankruptcy in October 2000. As part of its recovery plan, the company created the Owens Corning/Fibreboard Asbestos Personal Injury Trust in 2006. This trust was funded with $5 billion.

The settlement represented one of the largest asbestos-related bankruptcy resolutions in American corporate history. The Owens Corning Fibreboard Asbestos Personal Injury Trust was formed on October 31, 2006 as a result of the bankruptcy of Owens Corning and its wholly owned subsidiary Fibreboard to resolve all asbestos claims for which those entities had legal responsibility.

In 2006, the company was listed on the New York Stock Exchange again under ticker "OC." After four years trading on pink sheets (ironically appropriate given the company's signature color), Owens Corning returned to the NYSE with a clean balance sheet and resolved asbestos liability.

The Trust Structure: Ongoing Payments

Approximately 448,300 Owens Corning asbestos trust claims have been paid since the inception of the trust. Approximately $3.11 billion in claim settlements has been paid to asbestos victims since the trust was established.

The trust continues to pay claims to this day, though at reduced percentages. Today, people with approved claims receive only a small portion of their owed amount: 4.7% for Owens Corning claims and 3.7% for Fibreboard claims. The trust model allowed the company to move forward while providing at least partial compensation to victims through a predictable, managed process.

The bankruptcy emergence fundamentally reset Owens Corning. Pre-bankruptcy shareholders received nothing—they were wiped out. Creditors received a combination of cash and new equity. The asbestos victims' trust received funding. The company emerged with a capital structure it could actually support.

VII. Inflection Point #2: Post-Bankruptcy Transformation (2006-2020)

Strategic Focus & Portfolio Reshaping

The name Owens-Corning Fiberglass remained until 1996, when it was officially shortened to Owens Corning, reflecting its growth beyond fiberglass insulation. The simplified name signaled strategic evolution—the company was no longer defined solely by a single material technology.

Post-bankruptcy, management focused on three core segments: Roofing, Insulation, and Composites. This three-pillar structure provided diversification across end markets while leveraging shared capabilities in material science and manufacturing.

The roofing business had become increasingly important. Roofing shingles represented a higher-margin product category than commodity insulation, with greater brand differentiation potential. The SureNail Technology that Owens Corning developed for its Duration shingles provided genuine product differentiation—contractors valued the easier installation, and homeowners valued the improved wind resistance.

Owens-Corning acquired Pittsburgh Corning in 2017. Pittsburgh Corning produced FOAMGLAS cellular glass insulation, adding specialty insulation products to the portfolio. This acquisition reflected a strategy of building depth within the insulation category rather than seeking unrelated diversification.

Building the Modern Company Under New Leadership

Brian Chambers, who would become CEO in 2019, represented the next generation of Owens Corning leadership. Chambers, who was promoted to President and COO in August 2018, would retain the title of President as he assumed the CEO role. Previously, he served as President of the Roofing business since 2014. Overall, he has 15 years of management experience with Owens Corning in a variety of positions.

Before joining Owens Corning in 2000, Chambers worked with Honeywell, BOC Gases and an international engineering firm. Brian Chambers has a Bachelor in science from Bowling Green State University in 1988 and a Master in Business Administration and Management from Northwestern University in 1997.

Chambers joined the company at a pivotal moment—just as the asbestos crisis was reaching its peak. He rose through operational roles during the bankruptcy years and emerged as a leader who understood both the operational and strategic challenges facing the company.

The company issued its first green bond in August 2019. It was the first U.S. industrial company to issue a green bond. Owens Corning committed to spend $445 million on eligible sustainability projects.

This green bond issuance signaled strategic positioning around sustainability. Building materials companies face increasing pressure to demonstrate environmental responsibility—both in their manufacturing processes and in the end-use performance of their products. Insulation, in particular, represents one of the most cost-effective ways to reduce building energy consumption and associated carbon emissions.

VIII. Inflection Point #3: The Masonite Acquisition (2024)

The Strategic Bet: Entering Doors

Owens Corning announced it has completed its acquisition of Masonite International Corporation, a leading global provider of interior and exterior doors and door systems. All outstanding Masonite common shares have been acquired by Owens Corning for $133.00 per share, with an implied transaction value of approximately $3.9 billion.

Founded in 1925, Masonite is a leading provider of interior and exterior doors and door systems for repair, remodeling and new construction. It operates 64 manufacturing and distribution facilities, primarily in North America, with over 10,000 employees globally.

Why doors? The answer lies in Owens Corning's strategic logic around being a comprehensive building products supplier. Roofing, insulation, and now doors represent the major exterior envelope components of a home. A homeowner renovating or a builder constructing needs all three. Distribution channels overlap significantly. Brand-building investments can be leveraged across product categories.

The acquisition also increases Owens Corning's total addressable market by $27 billion and creates a platform to drive new growth opportunities in other product adjacencies.

Rationale & Synergies

With the completion of the acquisition, Owens Corning's annual revenue grows to $12.5 billion, with adjusted EBITDA of $2.9 billion on a synergized basis. Owens Corning expects to achieve approximately $125 million of run-rate cost synergies.

The synergy expectations are meaningful but measured. $125 million in cost synergies against a $3.9 billion purchase price represents a modest contribution to returns—the deal thesis clearly depends more on revenue growth and strategic positioning than on cost cuts.

The acquisition drives meaningful shareholder value creation with ROIC exceeding Owens Corning's cost of capital by the end of Year 3 post-close.

Owens Corning has named Chris Ball as president of its Doors business. Ball previously served as president of Masonite's Global Residential business. He will report directly to Chambers and serve as a member of the company's Executive Committee.

CEO Vision

"Over the past several years, Owens Corning has been on a journey to transform and grow our company through strategic choices and strong execution."

Chambers' framing emphasizes the continuity of strategic direction. The Masonite acquisition wasn't an opportunistic pivot—it was the latest step in a deliberate transformation toward becoming a broader building products platform.

IX. Current State & Financial Performance (2024-2025)

Four-Segment Model

With Masonite integrated, Owens Corning now operates four reportable segments: Roofing, Insulation, Doors, and Composites. According to 2024 filings, these segments accounted for approximately 36%, 32%, 13%, and 19% of total reportable segment net sales respectively. Owens Corning has 25,000 employees.

Financial Highlights

The company reported net sales of $11.0 billion, a 13% increase from the prior year, with newly acquired Doors business contributing $1.4 billion in revenue. The company generated net earnings margin of 6%, adjusted EBIT margin of 19%, and adjusted EBITDA margin of 25%.

The company delivered diluted EPS of $7.37 and adjusted diluted EPS of $15.91, produced operating cash flow of $1.9 billion and free cash flow of $1.2 billion, and returned $638 million, or 51%, of free cash flow to shareholders through dividends and share repurchases.

The gap between GAAP diluted EPS ($7.37) and adjusted EPS ($15.91) reflects transaction and integration costs associated with the Masonite acquisition, along with other one-time items. The adjusted figure provides a cleaner view of underlying operational performance.

"2024 was a transformative year for Owens Corning as we successfully executed three major strategic moves to reshape and focus the company on building products in North America and Europe, while consistently delivering higher, more resilient earnings and cash flow," said Chair and Chief Executive Officer Brian Chambers.

Portfolio Optimization: The Glass Reinforcements Sale

Owens Corning and Praana Group announced that they have signed a definitive agreement for the sale of Owens Corning's glass reinforcements business to Praana Group at an enterprise value of $755,000,000.

Owens Corning's glass reinforcements business, part of the company's Composites segment, manufactures, fabricates and sells glass fiber reinforcements for a wide variety of applications in wind energy, infrastructure, industrial, transportation and consumer markets. The business generated revenue of approximately $1.1 billion in 2024 and has approximately 4,000 employees across a global footprint that includes 18 operations in 12 countries.

"This transaction strengthens Owens Corning as a focused, more capital-efficient building products leader in North America and Europe."

The glass reinforcements divestiture represents strategic clarity. The business serves industrial markets (wind energy, transportation) that have different dynamics than residential and commercial building products. By exiting, Owens Corning can concentrate resources on its core opportunity.

Owens Corning will retain the other businesses within its Composites segment. These include the company's vertically integrated glass nonwovens business that supports its Roofing segment and other building products customers, along with its structural lumber business. Going forward, these businesses will operate within Owens Corning's Roofing segment. Owens Corning's two glass melting plants in the U.S., which provide glass fibers to make nonwovens products, will operate and be integrated within its Insulation segment.

X. Playbook: Business & Strategy Lessons

Material Science as Moat

The accidental discovery of fiberglass in 1932 created competitive advantages that persist nine decades later. Material science knowledge compounds over time—each generation of researchers builds on the work of predecessors. Owens Corning's research and development capabilities, honed over 87 years, represent institutional knowledge that cannot be easily replicated.

Vertical integration amplifies this advantage. The company doesn't just manufacture end products—it controls the upstream processes that produce key inputs. This integration provides cost advantages, quality control, and supply chain resilience.

Brand Power in B2B

The Pink Panther campaign demonstrated that branding matters even for products purchased through professional channels. Homeowners who recognize the "pink stuff" may express preferences to contractors. Contractors who trust the Owens Corning brand may recommend it to customers. The brand creates pull-through demand that supports pricing power.

While both brands are highly respected, Owens Corning benefits from strong consumer recognition thanks to its Pink Panther branding. This recognition translates into tangible business value in a category where most competitors are essentially unknown to end consumers.

Crisis Management

Owens Corning's navigation of the asbestos crisis offers lessons in surviving existential threats. First, continue operating. The business remained profitable throughout bankruptcy because management maintained focus on customers and operations. Second, accept that resolution takes time. Six years in Chapter 11 is a long time, but rushing to an inadequate solution would have been worse. Third, emerge clean. The trust structure provided finality—the company moved forward without lingering litigation uncertainty.

Capital Allocation Evolution

The company returned $638 million, or 51%, of free cash flow to shareholders through dividends and share repurchases.

The capital allocation framework balances growth investment, balance sheet strength, and shareholder returns. The Masonite acquisition demonstrated willingness to make significant bets when strategic logic is compelling. The glass reinforcements divestiture showed discipline in exiting businesses that don't fit the strategy. The consistent shareholder returns signal confidence in cash generation sustainability.

XI. Competitive Analysis & Investment Framework

Porter's 5 Forces Assessment

Threat of New Entrants: LOW

Building materials manufacturing requires substantial capital investment. Owens Corning operates 30 composites facilities, 31 insulation facilities, and 16 roofing facilities globally. Replicating this infrastructure would require billions of dollars and years of time. Established distribution relationships with contractors, home centers, and lumberyards create additional barriers. Brand recognition (Pink Panther, trademarked color) adds yet another layer of protection.

Bargaining Power of Suppliers: MODERATE

Key inputs include asphalt (for roofing), glass, and various chemicals. Owens Corning's vertical integration reduces supplier dependency in many areas. The company operates asphalt processing facilities that supply its roofing shingle manufacturing. Glass melting capabilities provide control over another critical input. However, energy costs (natural gas for glass melting) remain a meaningful input with limited supplier control.

Bargaining Power of Buyers: MODERATE

Distribution channels are somewhat consolidated—big box retailers like Home Depot and Lowe's represent significant customers. However, brand recognition provides pricing power with both contractors and homeowners. The roofing market sees significant competition from companies like GAF, CertainTeed, and Malarkey. These rivals compete on brand recognition, product development, and extensive distribution networks.

Threat of Substitutes: MODERATE

Alternative roofing materials (metal, tile, solar shingles) exist but remain more expensive than asphalt shingles for most applications. Alternative insulation materials (spray foam, cellulose, mineral wool) compete in certain applications. However, fiberglass insulation and asphalt shingles remain the cost-effective standards for most residential construction.

Competitive Rivalry: HIGH

GAF (General Aniline & Film) has been around since 1886 and currently holds about 40% of the North American roofing market. That's huge. GAF (owned by Standard Industries), CertainTeed (owned by Saint-Gobain), and Johns Manville (owned by Berkshire Hathaway) represent formidable competitors with well-capitalized parents. However, industry consolidation and rational pricing behavior have generally prevented destructive competition.

Hamilton's 7 Powers Framework

Scale Economies: Owens Corning benefits from manufacturing scale that spreads fixed costs across larger production volumes. The geographic dispersion of plants reduces transportation costs versus competitors shipping from distant locations.

Network Effects: Limited direct network effects, though contractor certification programs create some lock-in.

Counter-Positioning: The Masonite acquisition represents potential counter-positioning—becoming a broader building products platform rather than a pure-play materials company.

Switching Costs: Moderate switching costs for contractors who have built expertise with specific product lines and systems.

Branding: Strong brand power, particularly the Pink Panther association and trademarked color. Owens Corning has an extensive range of roofing shingles with varying levels of quality, durability, and color options catering to different consumers' roofing needs. These factors contribute to its popularity, not just marketing.

Cornered Resource: The institutional knowledge accumulated over 87 years of material science research represents a cornered resource that cannot be easily acquired or replicated.

Process Power: Operational excellence in manufacturing and distribution, honed over decades, provides process-based advantages.

Key Performance Indicators to Track

1. Roofing EBIT Margins: Roofing is the most profitable segment and generates significant cash flow. Sustained margins above 25% indicate pricing power and operational discipline. Watch for margin compression during housing market slowdowns.

2. Free Cash Flow Conversion: The ratio of free cash flow to net income indicates earnings quality and capital intensity. Owens Corning's consistent strong FCF conversion supports both shareholder returns and strategic flexibility.

3. Adjusted EBITDA Margin: The company has achieved 20 consecutive quarters of adjusted EBITDA margins at 20% or higher. This consistency demonstrates operational resilience across market conditions.

XII. Bull Case vs. Bear Case

Bull Case

The housing market presents structural tailwinds. American housing stock is aging—many homes built in the 1970s and 1980s need roof replacements and insulation upgrades. Energy efficiency requirements are tightening, driving demand for better insulation products. The repair and remodel market provides counter-cyclical buffer when new construction slows.

The Masonite integration creates cross-selling opportunities and strengthens relationships with key distribution channels. If synergy realization meets or exceeds the $125 million target, the deal will appear well-priced. The doors market is fragmented, presenting further consolidation opportunities.

The glass reinforcements divestiture focuses the company on higher-margin building products while generating capital for deployment elsewhere. Management's strategic clarity and execution track record support confidence in capital allocation decisions.

Valuation appears reasonable given the company's market position, margin profile, and capital return commitments. The dividend provides income while management maintains flexibility for opportunistic acquisitions.

Bear Case

Housing market volatility creates earnings uncertainty. Interest rate increases impact both new construction (fewer housing starts) and repair/remodel (homeowners less likely to undertake discretionary projects). A severe housing downturn could pressure all segments simultaneously.

Competition from GAF and others could intensify. GAF currently holds about 40% of the North American roofing market—larger than Owens Corning's share. If GAF's well-capitalized parent pursues share gains aggressively, margin pressure could result.

The Masonite integration carries execution risk. Large acquisitions frequently disappoint, and the doors business operates in a competitive market with different dynamics than roofing and insulation. If synergies fail to materialize or integration distracts management, the deal could prove value-destructive.

Raw material cost inflation (asphalt, energy) could compress margins if the company cannot pass through price increases. The company's vertical integration provides some protection, but commodity exposure remains meaningful.

Material Legal/Regulatory Considerations

The asbestos trust continues to process claims and make payments. While the trust structure provides legal separation from the operating company, ongoing trust administration represents a reminder of past liabilities. The trust contains approximately $1.07 billion. Payment percentages have declined as claims continue while trust assets are depleted.

Environmental regulations affecting building materials could create both risks (compliance costs, product reformulation requirements) and opportunities (demand for energy-efficient products). The company's sustainability positioning and green bond commitments suggest management is actively preparing for a more regulated environment.

XIII. Conclusion: What Owens Corning Teaches Us

Owens Corning's 87-year journey from accidental laboratory discovery to $11 billion building materials leader offers several enduring lessons.

Material science compounds. The knowledge accumulated through decades of working with fiberglass, asphalt, and related materials creates advantages that new entrants cannot easily replicate. Owens Corning's researchers today build on foundations laid by Games Slayter, Dale Kleist, and generations of engineers who followed.

Brands matter everywhere. Even in mundane product categories, brand recognition creates value. The Pink Panther and the trademarked color transformed how consumers think about insulation—making an invisible, rarely-considered product memorable and trusted.

Crises can be survived. The asbestos bankruptcy that seemed like an existential threat in 2000 proved surmountable. By maintaining operational focus while addressing legal and financial restructuring through appropriate processes, Owens Corning emerged stronger. The six-year bankruptcy process required patience and discipline, but the outcome was a company with resolved liabilities and operational capability intact.

Strategy evolves. From fiberglass pioneer to diversified building products platform, Owens Corning has continually adapted its portfolio. The Masonite acquisition and glass reinforcements divestiture represent the latest steps in ongoing strategic refinement.

For investors considering the building materials sector, Owens Corning represents a case study in resilience, operational excellence, and strategic clarity. The company's market position, brand strength, and capital allocation discipline provide a foundation for continued value creation—though housing market cyclicality and competitive intensity ensure that execution will always matter.

The pink insulation in America's walls, the asphalt shingles on millions of roofs, the doors now adorning countless homes—all bear witness to a company that turned an accidental discovery into an industrial giant, survived near-extinction, and continues building toward the future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube