James Hardie Industries: From Asbestos Empire to Global Fiber Cement Dominance

Introduction: A Transformation Story Unlike Any Other

How did a company that was once Australia's largest asbestos manufacturer—responsible for one of the most devastating corporate health scandals in the nation's history—transform into the undisputed global king of fiber cement siding with approximately 90% market share in North America?

James Hardie Industries plc is an American-Irish global building materials company and the largest global manufacturer of fibre cement products. Headquartered in Ireland, it is cross-listed on the Australian and New York Stock Exchanges. Its management team currently sits in Chicago, Illinois, United States.

The James Hardie story is one of reinvention—remarkable, controversial, and instructive. It spans more than 135 years, crosses three continents, and touches on themes that define modern capitalism: the brutal tradeoffs between profit and safety, the mechanics of corporate restructuring to limit liability, the power of category dominance, and the extraordinary returns that come from owning a niche rather than competing in one.

In July 2025, the company completed its acquisition of The AZEK Company in a cash-and-stock transaction for $26.45 in cash and 1.0340 ordinary shares of James Hardie for each share of AZEK common stock held for a total of $54.18 per share. This represents an implied value of $8.4 billion, including the value of share-based awards and the repayment of AZEK's outstanding debt.

This article examines the full arc of James Hardie's journey: from Scottish immigrant's trading company to asbestos empire, through the ethical reckoning that threatened to destroy the company, and finally to its emergence as a building products powerhouse now expanding aggressively through M&A. The lessons here apply far beyond building materials—they speak to how companies navigate existential crises, build defensible moats, and create extraordinary shareholder value in seemingly mundane industries.

Origins: A Scottish Immigrant's Australian Dream (1888-1950s)

The Founder's Story

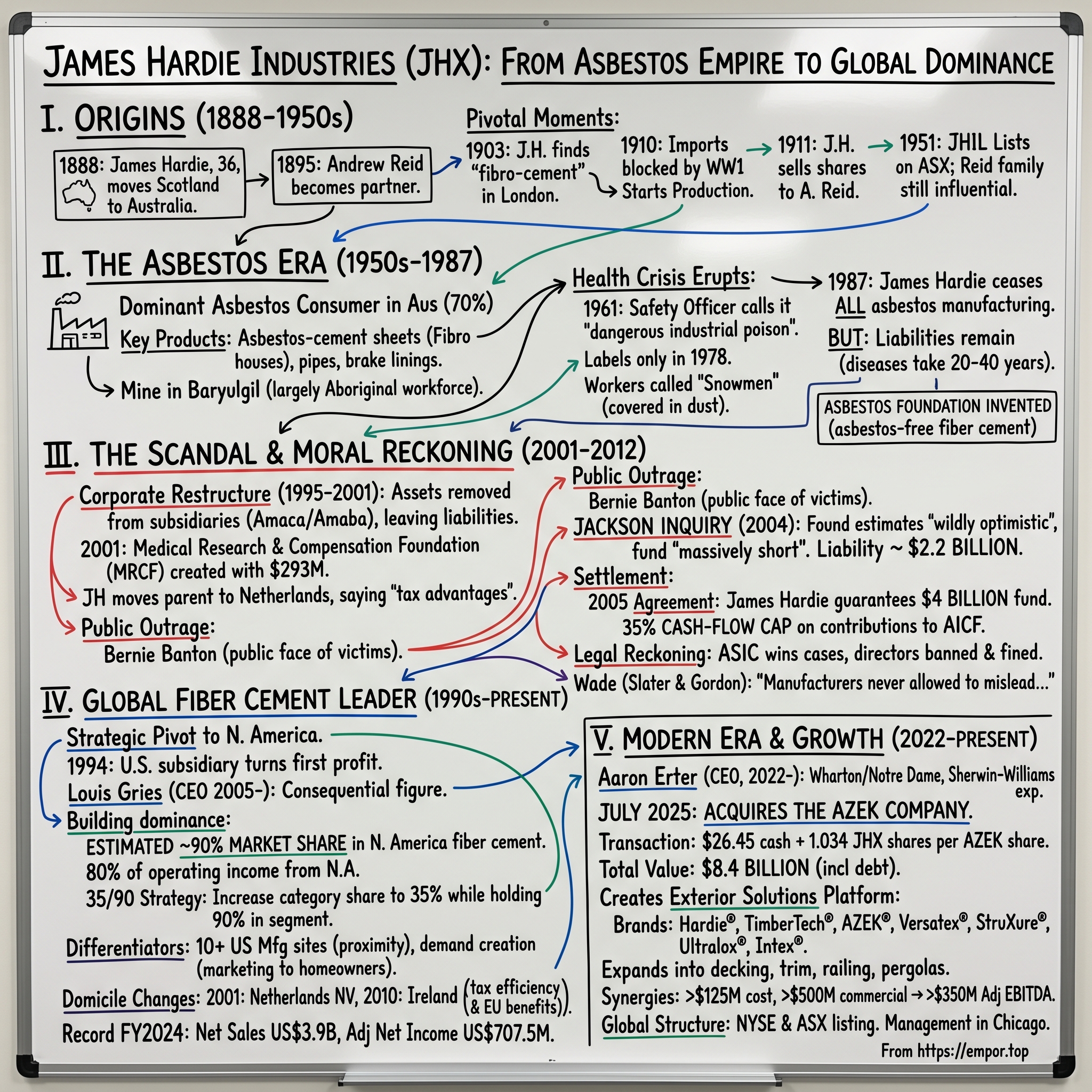

Picture Melbourne in 1888: a young frontier city buzzing with opportunity, its population swelling from gold rush wealth and immigration. Into this world stepped James Hardie—a 36-year-old Scot from Linlithgow, 16 miles west of Edinburgh—carrying little more than his wits and connections from his family's tannery business.

In 1888, when he was 36 years old, James Hardie traveled from Scotland to Australia, where he set up a trading company in Melbourne. Hardie's background in his family's tannery in Scotland led him initially to concentrate on importing animal oils and products for the tanning of animal hides.

Hardie soon began to branch out, however, acquiring the import agencies for a variety of other products. Hardie was joined by Andrew Reid, with whom he had become acquainted while working as a shipping agent in Scotland.

The partnership with Reid would prove fateful. Reid immigrated to Australia in 1892 and by 1895, at the age of 28, had become a full partner in Hardie's business. The two men complemented each other: Hardie the commercial visionary, Reid the technically minded operator. Together, they would build an enterprise that outlasted both of them by more than a century.

The Pivot to Building Materials

The defining moment came during a business trip to London in 1903. While on a trip to London in 1903, James chanced upon 'fibro-cement', a new type of roofing and lining slate that was made in France, and began importing it in to Australia.

The following year marked the invention of a new material that was to play an important role in the company's development—and indeed become its specialty more than one hundred years later. A composite of asbestos and cement that enabled the production of thin cement sheets, this material proved itself useful for a variety of purposes.

James Hardie's instinct was spot-on. Australia's rapidly growing cities needed affordable, durable building materials—and fibro-cement fit the bill perfectly. The climate was harsh, termites were destructive, and traditional wood required constant maintenance. Cement sheeting reinforced with fiber offered a compelling alternative.

When World War I disrupted supply chains from Europe, necessity became the mother of invention. Production of fiber cement begins after imports are blocked during World War I. A U.S. subsidiary is set up in order to introduce fiber cement to American building market.

The transition from importer to manufacturer marked James Hardie's transformation from a trading house into an industrial company. In 1911, at the age of 60 and after almost 23 years of leading the business, James Hardie called it a day. As he left, Hardie sold his half of the business – shares amounting to £17,000 to his partner Andrew Reid.

Even after the company went public in 1951, the Reids were major shareholders and thus maintained their influence over the company. This continued until 1995, where the business was predominantly under the control of the Reid family.

Going Public and the Asbestos Era

A publicly-owned company, later known as James Hardie Industries Ltd (JHIL), James Hardie was listed on the Australian stock exchange in 1951. In the following years, the company built up a diverse portfolio of building and industrial products businesses including a wide range of asbestos-based products.

The 1950s listing on the Australian Stock Exchange provided capital for expansion, and the company leveraged it aggressively. Australia's post-war housing boom created insatiable demand for building materials. Fibro houses—affordable, quick to construct—spread across suburban Australia like wildfire.

The founders built something that survived them. But they also set in motion forces that would lead to tragedy on a massive scale—and a corporate ethics scandal that would shame Australia and nearly destroy the company they created.

The Asbestos Empire: Rise and Moral Reckoning (1950s-1987)

Building a Dominant Position

By the middle of the twentieth century, James Hardie had become the largest manufacturer and distributor of building products, insulation, pipes and brake linings containing asbestos. In Australia, it operated asbestos plants in New South Wales, Queensland, South Australia, Victoria and Western Australia.

Founded by a Scottish leather-goods maker, James Hardie pioneered asbestos manufacturing in Australia when, using Swiss technology, it opened a factory at Camellia in Sydney's west in 1916. The company was called James Hardie Asbestos until 1979, and proudly named its headquarters in York Street Asbestos House.

The scale of James Hardie's asbestos operations was staggering. James Hardie was the dominant consumer of asbestos in Australia, averaging approximately 70% (60,000 tonnes) of all asbestos fibre consumed annually. James Hardie's primary business was the manufacture of asbestos cement products. These came in the form of building products and asbestos cement pipes.

Of all the names linked with the history of asbestos in Australia, that of James Hardie stands out. This was the manufacturing company which dominated the market for asbestos products during the decades following the Second World War. The iconic Australian fibro house which populated the suburbs around much of the country during the postwar housing boom, was built with asbestos-cement roofs, walls and fences. At the same time, James Hardie's asbestos-cement pipes and asbestos lagging were woven through the industrial landscape.

The company didn't just manufacture asbestos products—it mined the raw material. Deposits were mined in Tasmania, in Western Australia's Pilbara, and at Baryulgil in northern NSW a mine owned by James Hardie with a largely Aboriginal workforce.

The Growing Health Crisis

The question that would haunt the company for decades: When did James Hardie know asbestos was deadly?

In 1978 the effects of pleural abnormalities and other asbestos-related diseases were beginning to show up in the former mine workers. While other companies were involved in similar asbestos-related activities, most notably CSR, more than 50% of claims made to the Dust Diseases Tribunal of New South Wales in 2002 were brought against companies in the James Hardie group.

In 1978 the company began putting warning labels on its products explaining that inhalation of the dust could result in cancer.

But evidence presented at multiple trials suggested the company knew far earlier. Meanwhile, in Australia, Peter Russell (the Safety Officer of James Hardie) told the company management in April 1961 that asbestos was 'one of the most dangerous of industrial poisons'. He further advised them in 1964 that the company had a 'moral obligation' to asbestos product users to provide warnings of the dangers in using their products.

Right up until 1986 long after the dangers of asbestos were well documented, and multimillion-dollar compensation awards had been made to victims in United States courts, the company continued to manufacture asbestos, and to deny its products could kill. Australia embraced the "miracle fibre of the 20th century", as the advertising slogan went, more enthusiastically than any other country, bar France, England and the US.

The Camellia factory in Sydney's west became notorious. Workers there described themselves as "snowmen" because they were covered head to toe in white asbestos dust. Many would later die of asbestos-related diseases.

The Decision to Exit Asbestos

In March 1987 James Hardie ceased all asbestos manufacturing activities. As concern grew about the serious adverse health effects of asbestos, in the mid-1980s James Hardie developed an asbestos-free fibre cement technology, without the dangers associated with asbestos.

In the mid-1980's, James Hardie pioneered the development of asbestos-free fibre cement technology, and began designing and manufacturing a wide range of fibre reinforced cement building products that made use of the benefits that came from the products' durability, versatility and strength.

The development of cellulose-based fiber cement was a genuine technological achievement. It allowed the company to continue producing products with similar performance characteristics to asbestos-cement—durability, fire resistance, low maintenance—without the deadly health consequences.

But ceasing production in 1987 didn't end the company's asbestos liabilities. Asbestos-related diseases like mesothelioma can take 20, 30, even 40 years to manifest. James Hardie was sitting on a time bomb of future claims—and how it chose to handle that liability would become one of the most controversial chapters in Australian corporate history.

The Asbestos Compensation Scandal: A Corporate Ethics Crisis (2001-2012)

The Controversial Corporate Restructure

Between 1995 and 2001, James Hardie executed a series of corporate maneuvers that would later be deemed by a judicial inquiry as designed to limit the company's asbestos exposure—at the expense of dying victims.

Between 1995 and 2000, James Hardie (the parent company) began to remove the assets of these subsidiaries (since renamed Amaca and Amaba respectively), while leaving them with most of the asbestos liabilities of the James Hardie group. In 2001 these two companies were separated from James Hardie and acquired by the Medical Research and Compensation Foundation (MRCF) which was essentially created in order to act as an administrator for Hardie's asbestos liabilities.

In 2001 the company established the Medical Research and Compensation Foundation (MRCF) with a total of $293 million dollars in funds, saying that this fund would be able to meet all the future asbestos claims. James Hardie then relocated its company off-shore in Holland.

After this separation, James Hardie moved offshore to the Netherlands for what it claimed were significant tax advantages for the company and its shareholders.

The structure was elegant from a corporate finance perspective: separate the liabilities into undercapitalized shells, move the parent company offshore where it would be beyond the reach of Australian courts, and let the old subsidiaries slowly bleed out while the profitable fiber cement business thrived.

Then CEO of James Hardie, Peter McDonald, made public announcements emphasising that the MRCF had sufficient funds to meet all future claims and that James Hardie would not give it any further substantial funds.

The Jackson Inquiry and Public Outrage

The $293 million proved woefully inadequate.

Shortly after the move, an actuarial report found that James Hardie asbestos liabilities were likely to reach $574 million. The MRCF sought extra funding from James Hardie and was offered $18 million in assets, an offer the MRCF rejected. The estimate of asbestos liabilities was promptly revised to $752 million in 2002 and then $1.58 billion in 2003.

On 12 February 2004, a judicial inquiry into the matter was commissioned by the Government of New South Wales.

The Jackson Report found that this 'best estimate' was 'wildly optimistic' and the estimates of future liabilities was 'far too low'.

When JHIL applied to the NSW Supreme Court in 2001 for permission to liquidate Amara and Amaba and relocate to the Netherlands, it declared that MRCF was fully funded to meet all future liabilities of both asbestos sufferers and creditors. The fund, however, was provided with only $293 million, massively short of the $2.2 billion the company has since acknowledged would be needed.

A commission of inquiry in Australia has found that James Hardie Industries, a company that made building products containing asbestos until 1987, deliberately underfunded a victims' compensation fund when it undertook a corporate restructuring that limited its asbestos liabilities.

The public face of victims' advocacy became Bernie Banton—a former James Hardie employee who had worked at the Camellia plant from 1968 to 1974.

Bernard Douglas Banton AM (13 October 1946 – 27 November 2007) was an Australian builder and, later, social justice campaigner for asbestos-related diseases. He was the widely recognised face of the legal and political campaign to achieve compensation for the many sufferers of asbestos-related conditions, which they contracted after either working for the company James Hardie or being exposed to James Hardie Industries' products.

During this time Banton and his colleagues were called the 'Snowmen". This was between 1968 to 1974 at the James Hardie plant in Camellia. "Because we were covered from head to toe with the white dust of asbestos in the manufacture of kaylite. The factory was just covered in dust."

This led to the key element of the 2005 agreement: the cash-flow cap, which still stands today. This involves an independent actuary firm assessing the company's yearly liability based on the estimated number of asbestos victims. James Hardie is then required to meet that obligation through its contribution to the Asbestos Injuries Compensation Fund (AICF), subject to a limit of 35 per cent of its cash flow.

The Legal Reckoning

In 2009, the Supreme Court of New South Wales found that directors had misled the stock exchange in relation to James Hardie's ability to fund claims. They were also banned from serving as board members for five years. Former chief executive Peter Macdonald was banned for 15 years and fined $350,000 for his role in forming the MRCF and publicising it.

ASIC appealed against the ruling in the High Court of Australia in October 2011. In May 2012 the High Court upheld the 2009 New South Wales court decision and found that seven former James Hardie non-executive directors did mislead the stock exchange over the asbestos victims compensation fund.

Joanne Wade, head of Slater and Gordon's NSW asbestos practice, said the ruling put an end to the long-running saga. 'It will ensure the manufacturers of deadly asbestos products are never allowed to mislead the public about their ongoing commitment and obligations to families devastated by their products.'

The Settlement and Path Forward

In the end James Hardie guaranteed a fund of $4 billion to cover its future obligations to asbestos victims. Prosecutions of James Hardie board members and senior executive have followed. Throughout the saga, Bernie Banton was the public face of victims and was active in all the battles.

Hit by a national boycott, the major Australian building products company James Hardie Industries has agreed to compensate people with diseases induced by its asbestos products by providing approximately $A1.5bn over a period of at least 40 years. Under a heads of agreement negotiated with the Australian Council of Trade Unions and groups representing people with asbestos related diseases James Hardie will, for each year of the term agreed, provide up to 35% of the company's annual cash flow from its global operations to a special purpose fund.

The 35% cash-flow cap became the mechanism through which James Hardie could honor its moral and legal obligations while remaining a viable business. The arrangement was elegant in its simplicity: the company's success would directly benefit victims, while the cap ensured the company wouldn't be forced into bankruptcy—which would have left victims with nothing.

'This percentage figure strikes a three-way balance of appeasing investors, allowing the company to still prosper and ensuring adequate funds are available to continue compensating claimants now and into the future.'

Bernie Banton died in November 2007, just 103 days after being diagnosed with mesothelioma—the cancer he had spent years warning others about. On 21 January 2009, a new asbestos diseases research institute at Sydney's Concord Repatriation General Hospital was named the Bernie Banton Centre. The facility is the world's first standalone research facility dedicated to the treatment and prevention of asbestos-related diseases.

The U.S. Expansion and Fiber Cement Dominance (1990s-2020s)

Strategic Pivot to North America

Even as the asbestos scandal was reaching its crescendo, James Hardie was building an entirely new business—one that would eventually dwarf its Australian operations and provide the cash flows needed to fund both victim compensation and shareholder returns.

The revitalization of the U.S. building market, after several years of economic recession, coupled with increasing industry interest in the strength and versatility of fiber cement, enabled James Hardie's U.S. subsidiary to turn its first profit by 1994. Fiber cement quickly became the company's fastest-growing segment, and the U.S. market was easily its fastest-growing and most profitable market. By 1998, the United States accounted for more than 45 percent of the company's sales and 61 percent of its profits.

Just two years later, the United States represented 60 percent of its annual revenues and 90 percent of its profits.

The architect of this expansion was Louis Gries, who would become one of the most consequential figures in the company's history.

Louis Gries, BSc, MBA, has been the Chief Executive Officer of James Hardie Industries since February, 2005. He joined James Hardie as Manager of the Fontana fiber cement plant in California in February 1991. He served as President of James Hardie Building Products (USA) since December 1993.

Louis Gries joined James Hardie in 1991, becoming CEO in February 2005. During this time James Hardie delivered strong top-line growth and differentiated returns while increasing the market capitalisation from less than A$3.0 billion to A$9.21 billion.

Building Market Dominance

The company holds a dominant position in the fiber cement market, with approximately 90% market share in North America, highlighting its strong competitive standing. We estimate Hardie has about 90% market share in the fiber cement category in its main geography of North America.

We estimate Hardie has about 90% market share in the fiber cement category in its main geography of North America, which contributes about 80% of group operating income. Indeed, over the five years to 2022, the Census Bureau reports that fiber cement siding on newly built houses gained 3% market share in the US compared with vinyl (down 2%), stucco (up 2%), brick (down 2%), and wood (down 1%). Fiber cement siding was the siding of choice in 23% of all new US house completions in 2022.

The company's strategy, crystallized under Gries, became known as "35/90." They refer to this core strategy as 35/90—a plan to increase the fiber cement share of the wood-look siding market from the 22% that it is currently to 35%, while holding on to their 90% market share in the category, across both new construction and R&R.

James Hardie is essentially synonymous with the category of fiber cement, having pioneered the development of the technology for the construction industry since the 1970s. It does face some competition from smaller brands in this segment (Allura, CertainTeed, Nichiha), and also from large companies in the composite wood segment (LP Corp). Due to the availability of these alternatives, JH focuses on keeping prices competitive (defending or increasing its market share) while maintaining higher margins through cost efficiencies from increased volume.

In terms of fixed costs, they have 10 manufacturing sites across the US (and even more in Europe, Australia, and Philippines) which enables them to be physically closer to their customers and deliver product with minimal lag—an important selling point in the construction industry and a differentiator from their smaller fiber cement competitors.

Corporate Domicile Changes

James Hardie's corporate structure reflects its complex history and global aspirations.

Therefore in August 2001, James Hardie undertook a corporate restructuring to establish a new Dutch holding company, James Hardie Industries NV. The new structure was designed to position the company for further international growth, and generate higher returns for shareholders than were possible under the previous structure.

On 19 February 2010, James Hardie moved its corporate domicile from The Netherlands to Ireland, in a transaction designed to transform James Hardie Industries NV into an Irish Societas Europea company.

The moves from Australia to Netherlands to Ireland reflect the reality that James Hardie's business had become predominantly American, while its shareholder base remained substantially Australian. The Irish domicile offered tax efficiency while maintaining EU treaty benefits.

Modern Era Leadership and Strategic Direction (2022-Present)

New CEO: Aaron Erter

Aaron Erter currently serves as the Chief Executive Officer of James Hardie Industries, having been appointed on September 1, 2022. At 51 years old as of April 30, 2025, he holds a strong educational background with a bachelor's degree in economics from The University of Pennsylvania Wharton School and an MBA from the University of Notre Dame. Bringing over 25 years of experience in the consumer and industrial sectors, he has led leadership roles at prominent companies such as PLZ Corp, Sherwin-Williams, Valspar, and Stanley Black & Decker.

Erter, 51, joined James Hardie as CEO in 2022, and before that served as CEO of PLZ Corp, a leader of specialty liquid and aerosol manufacturing; global president for Sherwin-Williams' consumer and industrial businesses; senior vice president and general manager of Valspar's consumer business; and served in numerous leadership roles in sales and marketing while at Stanley Black & Decker. He holds a bachelor's in economics from The Wharton School at The University of Pennsylvania and a master's in business administration from The University of Notre Dame – Mendoza College of Business.

Erter's background in consumer products and paints—particularly his experience at Sherwin-Williams—made him an unusual but fitting choice for a building materials company increasingly focused on homeowner marketing and brand-building.

The Transformative AZEK Acquisition (2025)

The AZEK acquisition represents the most significant strategic move in James Hardie's modern history.

James Hardie Industries plc, a leader in providing high-performance, low-maintenance building products and solutions, and The AZEK Company Inc., a leading manufacturer of high-performance, low-maintenance and environmentally sustainable outdoor living products, announced entry into a definitive agreement under which James Hardie will acquire AZEK for a combination of cash and James Hardie shares with a total transaction value of $8.75 billion, including AZEK's net debt of approximately $386 million as of December 31, 2024. Under the terms of the Agreement, AZEK shareholders will receive $26.45 in cash and 1.0340 ordinary shares of James Hardie.

James Hardie now features a portfolio of high-performance, low-maintenance exterior brands, including Hardie®, TimberTech®, AZEK® Exteriors, Versatex®, StruXure®, Ultralox® and Intex®. Collectively, James Hardie brands offer incredible value, as well as endless design possibilities for homeowners looking for siding, decking, trim, railing, and pergolas.

Delivers best-in-class financial profile: The combination of James Hardie and AZEK creates a company with an accelerated growth rate, peer-leading profitability and robust cash generation. In the 12-month period ended December 31, 2024, James Hardie and AZEK generated $5.9 billion in net sales, more than $1.8 billion in adjusted EBITDA and adjusted EBITDA margin of 31%, on a combined company basis and including the total expected run-rate benefit of synergies. The transaction is also expected to be accretive to James Hardie's cash earnings per share in the first full fiscal year after the closing of the transaction.

Through at least $125 million of cost synergies and $500 million of commercial synergies, James Hardie expects to achieve at least $350 million of additional annual adjusted EBITDA.

NYSE Listing and Global Structure

The previously announced termination of James Hardie's American Depositary Share program took effect on July 1, 2025, and James Hardie's ordinary shares are now listed and traded on the NYSE under the symbol "JHX." James Hardie ordinary shares continue to be listed for trading on the Australian Securities Exchange via CHESS Units of Foreign Securities.

The dual NYSE/ASX listing reflects James Hardie's unique position: an Irish-domiciled company with American management, Australian shareholders, and global operations.

Industry Deep Dive: The Fiber Cement & Siding Market

Market Size and Growth

HTF Market Intelligence projects that the global Fiber Cement Siding market will expand at a compound annual growth rate (CAGR) of 7.1% from 2024 to 2033, from 15.4 Billion in 2024 to 26.7 Billion by 2033.

Fiber cement siding is a durable cladding material made from cement, cellulose fibers, and sand. It is engineered to replicate the appearance of wood, stucco, or stone while offering substantially higher resistance to fire, moisture, pests, and harsh weather conditions. Designed for both residential and commercial buildings, fiber cement siding provides long-term structural stability with minimal maintenance compared to traditional materials.

The growth drivers are compelling: climate resilience concerns are pushing homeowners toward materials that withstand extreme weather; sustainability requirements favor fiber cement's durability and longevity; and aesthetic preferences increasingly favor the "wood look" that fiber cement can deliver without wood's maintenance requirements.

Product Categories

The company operates across multiple product categories and geographic segments. James Hardie is one of the leading player engaged in the production of fiber cement siding and backerboard. It operates through three business units, namely, North America Fiber Cement, Asia Pacific Fiber Cement, and Europe Building Products. The company's fiber cement building materials serve a wide range of internal & external applications, such as external siding, internal walls, ceilings, floors, soffits, fences, facade, cladding, decking, and roofing.

About 65% of their volume now comes from the R&R market. With around 40 million homes in North America over 40 years old—a common age for renovations—JH views the R&R market as its most substantial opportunity for future growth.

Competitive Landscape

Major companies profiled in Fiber Cement Siding Market are: James Hardie, Nichiha, Allura, Cembrit, Everest Industries, Etex Group, SCG, CSR Limited, Swisspearl, Toray, Kmew, Boral.

These three players hold approximately 30% of the global fiber cement market. James Hardie claimed a prominent share of the fiber cement market. It is the dominant key player in terms of individual share amongst the top three players.

While James Hardie competes globally with players like Nichiha, Etex, and CertainTeed, its dominance in North America—its most profitable market—is essentially unassailable. The 90% market share figure represents one of the most concentrated category positions in building materials.

Playbook: Strategic & Business Lessons

Lessons from Crisis Management

The James Hardie asbestos scandal offers a case study in both what not to do—and in how companies can survive existential crises through eventual acceptance of responsibility.

The initial response—the creation of an underfunded compensation fund and the offshore relocation—represented the worst of corporate behavior. It prioritized shareholder value and executive protection over victims' welfare, used sophisticated legal structures to evade moral obligations, and ultimately failed when public outrage, union boycotts, and government inquiry forced a reckoning.

The eventual settlement—the 35% cash-flow cap mechanism—showed a path forward. By linking compensation to the company's ongoing success, the agreement aligned interests: victims had an incentive to see the company thrive, and the company could plan for its obligations without existential uncertainty.

Building Category Dominance

James Hardie's strategic playbook for building and defending its fiber cement moat deserves careful study.

First, the company pioneered the category. When James Hardie developed modern asbestos-free fiber cement in the mid-1980s, it created the technology that would become the industry standard. Being first—and investing continuously in R&D—created lasting advantages.

Second, the company invested in manufacturing scale. They have 10 manufacturing sites across the US (and even more in Europe, Australia, and Philippines) which enables them to be physically closer to their customers and deliver product with minimal lag—an important differentiator from their smaller fiber cement competitors.

Third, the company pursued aggressive pricing to prevent competitor scale. The logic is simple: in a manufacturing business with significant fixed costs, scale creates cost advantages. By keeping competitors from reaching efficient scale, James Hardie makes their economics untenable.

Fourth, the company invested heavily in demand creation—marketing directly to homeowners rather than just to contractors and builders. This created pull demand that reinforced the company's position with professional installers.

Corporate Domicile Strategy

The journey from Australia → Netherlands → Ireland reflects sophisticated tax and corporate planning.

The Australian base made sense when the business was primarily Australian. The Netherlands move in 2001 was designed to reduce tax friction on US profits. The Ireland move in 2010 addressed changes to US-Netherlands tax treaties while maintaining EU benefits.

The management team in Chicago, dual listing in Australia and NYSE, and Irish legal domicile create a complex structure that optimizes for the company's global footprint. It also creates complexity—Australian investors have expressed concern about potential delisting from the ASX—that management must navigate carefully.

M&A as Growth Strategy

The AZEK acquisition represents a new phase in James Hardie's evolution—from organic category dominance to platform building through M&A.

Speaking to the combination, Mr. Erter said, "This combination with AZEK is an extraordinary opportunity to accelerate our growth strategy, deliver enhanced and differentiated solutions to our customers and drive shareholder value. We are uniting two highly complementary companies with large material conversion opportunities and shared cultures centered around providing winning solutions to our customers and contractors. Together, we will be well positioned to drive sustained above-market growth as a leader across exterior building products."

The strategic logic is compelling: AZEK's strengths (decking, trim, railing) complement James Hardie's core (siding); both companies serve the same contractors and homeowners; and the combined entity can offer integrated exterior solutions that neither could deliver alone.

Once run-rate cost synergies are achieved, the combined company is expected to generate robust annual free cash flow of greater than $1 billion, which James Hardie intends to use to support organic growth, deleverage and fund ongoing share repurchases.

Porter's Five Forces & Strategic Analysis

Threat of New Entrants: LOW

The fiber cement industry has substantial barriers to entry. Manufacturing requires significant capital investment, technical expertise accumulated over decades, and proximity to customers for cost-effective delivery. James Hardie's 10+ US manufacturing facilities represent billions in invested capital that would take years for a new entrant to replicate.

Brand matters in this category—homeowners increasingly specify materials by name, and James Hardie has invested heavily in homeowner marketing. The company's ColorPlus pre-finished siding, in particular, has created differentiation that's difficult to replicate.

Bargaining Power of Suppliers: MODERATE

JH focuses on keeping prices competitive (defending or increasing its market share) while maintaining higher margins through cost efficiencies from increased volume.

Key inputs include cement, pulp, and energy. These are commodity inputs with multiple suppliers, which limits individual supplier power. However, the company has noted raw material cost pressures in recent quarters, indicating that input costs can pressure margins during inflationary periods.

Bargaining Power of Buyers: MODERATE

James Hardie sells through distributors to contractors, who in turn serve builders and homeowners. No single customer represents a dominant share of sales. The company has built strong relationships with major homebuilders—the exclusive partnership with D.R. Horton, America's largest homebuilder, is an example.

This growth reflects the encouraging results of our long-term purposeful strategic actions to grow our share with the National Home Builders and expand our presence in key repair and remodel geographies. Our growth in FY2025 through market declines proves we are executing on our plan to win in these large material conversion opportunities.

Threat of Substitutes: MODERATE

Fiber cement competes with vinyl siding (cheaper, but perceived as lower quality), wood (beautiful, but high maintenance), brick and stucco (regional preferences), and newer composite materials.

Indeed, over the five years to 2022, the Census Bureau reports that fiber cement siding on newly built houses gained 3% market share in the US compared with vinyl (down 2%), stucco (up 2%), brick (down 2%), and wood (down 1%).

The trend favors fiber cement, but the company must continue to invest in product development and marketing to maintain its value proposition.

Competitive Rivalry: LOW within fiber cement, MODERATE in broader siding

Within fiber cement, James Hardie's 90% share makes it the category itself. Competitors like Nichiha, Allura, and CertainTeed exist but operate at sub-scale. The company's pricing and volume strategy is explicitly designed to keep them from reaching efficient scale.

In the broader siding category, competition is more intense. LP Corporation's SmartSide, in particular, represents a meaningful alternative in the engineered wood category.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: James Hardie's 10+ US manufacturing plants spread fixed costs across massive volume, creating unit cost advantages that competitors cannot match.

Network Effects: Limited direct network effects, but the company benefits from a large installed base of contractors trained on Hardie products.

Counter-Positioning: James Hardie's heavy investment in homeowner marketing and direct-to-consumer demand creation represents a business model that legacy building materials companies haven't replicated.

Switching Costs: Moderate for contractors (training and familiarity with Hardie products creates stickiness) and low for homeowners (though brand preference is real).

Branding: Strong and growing. The "Hardie" name is increasingly known to homeowners, not just contractors. This creates pull demand that reinforces the company's position.

Cornered Resource: The company's R&D capabilities and manufacturing expertise, developed over decades, represent difficult-to-replicate technical resources.

Process Power: The Hardie Operating System (HOS) and Hardie Manufacturing Operating System (HMOS) represent proprietary operational processes that drive efficiency and margin performance.

Bull and Bear Cases

The Bull Case

Category Tailwinds: The repair and remodel market is poised for long-term growth as the massive cohort of homes built in the 1980s-2000s age into their renovation cycles. Climate resilience concerns are pushing homeowners toward durable, fire-resistant materials like fiber cement.

AZEK Integration Upside: Through at least $125 million of cost synergies and $500 million of commercial synergies, James Hardie expects to achieve at least $350 million of additional annual adjusted EBITDA. If management can execute on these synergies while cross-selling to AZEK's contractor network, the acquisition could prove highly accretive.

Material Conversion Opportunity: Though fiber cement as a general category currently accounts for only 9% of the repair and remodel (R&R) market, it commands a 25% share in new construction, indicating significant potential for long-term growth. As homes built with fiber cement siding age, the material is likely to see increased demand in R&R.

Dominant Market Position: A 90% share in fiber cement creates pricing power, scale advantages, and the ability to invest in growth that competitors cannot match.

The Bear Case

Housing Cyclicality: CEO Erter said, we are prudently planning for market volumes to contract in FY2026, marking a fourth consecutive year of declines in large-ticket repair and remodel activity. The company remains exposed to housing market cycles, and high interest rates have depressed both new construction and R&R activity.

Integration Risk: The AZEK acquisition nearly doubles the company's size and complexity. Integration always carries execution risk, and the $8.4 billion price tag leaves little room for error.

Asbestos Liabilities Overhang: The 35% cash-flow cap creates an ongoing drag on free cash flow, and estimates of future liabilities remain subject to actuarial uncertainty. Any unexpected surge in claims could stress the compensation mechanism.

Competition from LP SmartSide: While James Hardie dominates fiber cement, LP Corporation's engineered wood siding competes for the same homeowners and represents a different value proposition that some customers prefer.

Key Performance Indicators to Track

For investors monitoring James Hardie's ongoing performance, three metrics deserve particular attention:

1. North America Fiber Cement Volume Growth vs. End Market This metric captures whether the company is gaining or losing share. Management has consistently emphasized outperforming end markets through material conversion. Our growth in FY2025 through market declines proves we are executing on our plan to win in these large material conversion opportunities.

2. North America EBITDA Margin In a difficult North America market environment in FY2025, we generated $2.9 billion in North America sales, along with $1 billion of EBITDA, resulting in a 35% EBITDA margin. This margin reflects the company's pricing power, manufacturing efficiency, and ability to manage costs. Material conversion success should support margins even in challenging market conditions.

3. ColorPlus Mix Shift ColorPlus pre-finished products carry higher margins and create stronger homeowner pull. Double-digit growth in ColorPlus indicates success in the company's premiumization and direct-to-homeowner strategies.

Conclusion: A Company Transformed

James Hardie's journey from Scottish trading company to asbestos empire to fiber cement king represents one of the most remarkable—and morally complex—transformations in industrial history.

The company's asbestos legacy remains a permanent stain. Thousands died from exposure to James Hardie products, and the corporate maneuvering of the early 2000s represented an attempt to evade responsibility that failed only because of public outrage and regulatory intervention.

But the same company that produced that moral failure also developed transformative technology, built a globally dominant position in fiber cement, and created extraordinary shareholder value while meeting its compensation obligations.

James Hardie Industries has demonstrated consistent strategic growth and innovation, achieving record Net Sales of US$3.9 billion and Adjusted Net Income of US$707.5 million in fiscal year 2024.

With the AZEK acquisition now complete, James Hardie has positioned itself as a comprehensive exterior solutions platform with approximately $6 billion in combined revenue and the potential for over $1 billion in annual free cash flow. The company's 90% market share in North American fiber cement provides a durable competitive moat, while the expansion into decking, trim, and outdoor living products extends the addressable market significantly.

The key risks—housing cyclicality, integration execution, and ongoing asbestos liabilities—are real and material. But for investors who can look past the quarterly noise of housing starts and R&R activity, James Hardie offers exposure to powerful long-term trends: climate resilience, material conversion, and the premiumization of residential exteriors.

The story of James Hardie reminds us that corporate reinvention is possible—even from the darkest of starting points. What matters is not just where a company has been, but where it's going and how it plans to get there.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube