nVent Electric: The Hidden Infrastructure Giant Powering the AI Revolution

I. Introduction & Episode Roadmap

Picture a fluorescent-lit data center in Ashburn, Virginia—one of many in the world's largest concentration of hyperscale computing facilities. Rows upon rows of servers hum in coordinated symphony, their LED indicators blinking like digital fireflies. The air crackles with electricity: millions of dollars of NVIDIA GPUs processing the queries that train ChatGPT, render Netflix recommendations, and execute trades for Goldman Sachs.

Now look closer. Behind those gleaming servers, beneath the raised floor tiles, running through every cable pathway and junction box—there lies a hidden world of infrastructure that most investors have never considered. The protective enclosures keeping moisture from frying a $30,000 chip. The liquid cooling manifolds preventing thermal runaway. The grounding systems that could save the entire facility during a lightning strike. The fastening solutions holding it all together.

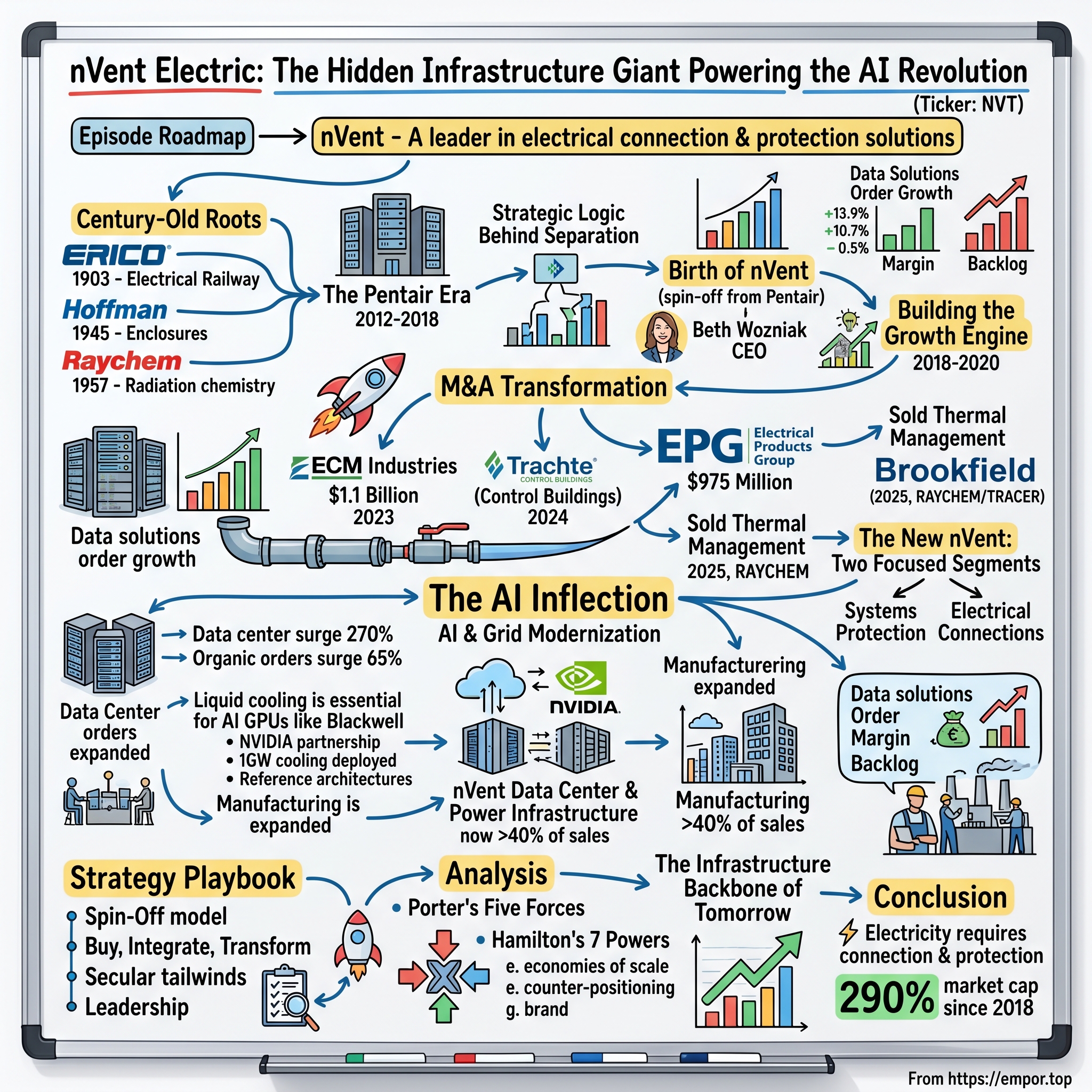

There's a $17.9 billion company behind these invisible essentials—a company whose market cap has increased 290% since April 2018, a compound annual growth rate of nearly 20%. And yet, despite its criticality to every hyperscaler, every power utility, and every industrial facility in America, you've probably never heard of them.

Welcome to nVent Electric.

nVent is a leading global provider of electrical connection and protection solutions. The company's data center and power infrastructure segments now account for approximately 40% of sales—two sectors experiencing explosive growth driven by AI and grid modernization.

In Q3 2025, nVent reported record sales, adjusted EPS, orders, and backlog, driven by AI data center demand. For the first time, quarterly sales exceeded $1 billion. Adjusted EPS reached $0.91, exceeding guidance. Organic orders surged approximately 65%, primarily driven by large orders for the AI data center build-out.

How did a spin-off orphan—separated from a water pump company just seven years ago—become a critical infrastructure enabler for the AI age? How did a collection of century-old industrial brands transform into a growth story that has Wall Street analysts raising price targets after every earnings call? And what does nVent's trajectory reveal about the hidden winners in the great electrification of everything?

The answer involves a founder who invented safety guards to protect factory workers' hands, a California radiation chemistry lab that changed how the world heats pipes, a 1903 railway company that still grounds every data center in North America, and a CEO who was "caught off guard" when told she'd be running an independent public company—yet transformed that shock into one of the most successful industrial spin-offs of the past decade.

II. The Century-Old Roots: The Brands Behind nVent

A. ERICO: Where It All Began (1903)

nVent traces its roots back to 1903—a time when very few homes or businesses even had electricity—with the founding of the Electric Railway Improvement Company (ERICO). The year is significant: Theodore Roosevelt occupied the White House, the Wright Brothers had yet to take their historic flight at Kitty Hawk, and America's cities were just beginning their love affair with the streetcar.

ERICO's rail product line is the company's original business dating back to 1903. The company was formed as the Electric Railway Improvement Company to supply power bonds, signal bonds and related welding equipment to railroads, mining and street railway industries.

In an era when electrified rail was the cutting edge of transportation technology, ERICO's founders recognized a fundamental truth: electricity is dangerous, and connecting electrical systems safely requires precision engineering. The company in 1939 patented its Cadweld exothermically welded connection, an invention that paved the way for rail car companies to make repairs to rail tracks without large welding equipment. More than 100 million nVent ERICO Cadweld connections are now installed in a broad array of applications around the globe.

Think about what that represents: over a century of cumulative expertise in ensuring electrical current flows where it should—and nowhere else. Every hospital, every data center, every telecommunications tower relies on proper grounding and bonding. When a 2,000-gigawatt lightning bolt strikes near a facility, ERICO's products are the difference between business continuity and catastrophic failure.

Based in Solon, Ohio, ERICO grew into a leading global manufacturer and marketer of superior engineered electrical and fastening products. ERICO has 1,200 employees in 30 countries with recognized brands including CADDY fixing, fastening and support products; ERICO electrical grounding, bonding and connectivity products; and LENTON engineered systems.

B. HOFFMAN: The Enclosures Pioneer (1945)

The story of Hoffman Enclosures begins not with a vision for industrial dominance, but with a young factory worker's devotion to his job. When young Harry Hoffman began working for Federal Cartridge in 1936, he had no idea that seven decades later, a multi-million dollar company would be named after him. What he did know, however, was that he loved his work. In fact, he became so absorbed in running the factory loader that he often forgot to punch out on time.

When his supervisor brought this fact to his attention, young Harry replied, "Have you ever tried to keep one eye on the job and one eye on the clock? It doesn't work." His spirit of passion and innovation led him to significant achievements over the next several decades. In 1945, Harry invented the automatic press guard, an electronic device that prevented machinery from functioning if the operator's hand was hazardously close.

The legacy of Hoffman Enclosures began 75 years ago when its founder Harry Hoffman designed an innovative automation press guard. Ahead of its time, the guard product protected workers from injuries, kept factories running and served as the core product for the launch of his namesake company in October 1945.

From safety guards to industrial enclosures is an intuitive leap: if you can protect a worker's hand from a machine, why not protect the electronics that control that machine? A series of other inventions quickly followed: a dandelion digger, a clay target thrower, an electric kitchen mixer, a clothes-line hanger, a Switch-O-Lite used by farmers to operate yard pole lights, a junction box for housing wiring and an outlet for supplying power to farm equipment. The last two are considered to be the forerunners of Hoffman's first line of enclosures.

Today, with more than 12,000 products and tailored solutions, nVent offers a global manufacturing footprint and a uniquely complete range of IEC and NEMA electrical enclosures under the nVent HOFFMAN brand.

C. Raychem: The Radiation Chemistry Revolution (1957-1999)

If ERICO represented 20th-century electrical infrastructure and Hoffman embodied mid-century American manufacturing ingenuity, Raychem was pure California technological disruption.

The Raychem Corporation was founded and headquartered in Menlo Park, California, in 1957 by Paul M. Cook, Bob Helprin, James B. Meikle, and Richard W. Muchmore. Led by Cook and second-in-command Robert M. Halperin, Raychem became a pioneer of commercial products realized through radiation chemistry.

The company was a spin-off from SRI International, and their founding technology was wire and cable that used radiation cross-linked polymer insulation targeted at military and aerospace applications. This was the first known use of radiation chemistry for commercial products. The company soon invented heat-shrinkable tubing also targeted at electronic applications.

The breakthrough came in 1972. The Raychem Corporation introduced the world's first commercially successful electric self-regulating heat tracing cable to control the temperature of pipework without overheating. This seemingly mundane innovation—a cable that adjusts its heat output based on surrounding temperature—revolutionized industries from oil and gas to food processing.

By 1980 the company had expanded to over 30 countries, including a major branch in Swindon, UK and made the Fortune 500 list. It was recognized as one of the fastest-growing companies in the United States at that time. The company had only three CEOs until the company was acquired by Tyco International in 1999.

In a move that created a passive component powerhouse, Tyco International announced its intent to acquire Raychem Corp. for $2.87 billion in cash and stock. The acquisition would set in motion a series of corporate machinations that eventually delivered Raychem's thermal management heritage into nVent's hands.

D. The Pentair Era: Rolling Up the Electrical Industry (2012-2018)

In 2012, Tyco International sold Tyco Thermal Controls to Pentair plc. This transaction brought the Raychem thermal management business into Pentair's growing portfolio of electrical solutions.

Three years later, Pentair made an even bolder move. Pentair announced that it had entered into an agreement with ERICO Global Company whereby Pentair would acquire ERICO for $1.8 billion in cash, including the repayment of ERICO debt. The transaction valued ERICO at approximately twelve times 2015 forecasted EBITDA.

Pentair's Chairman and CEO Randall J. Hogan explained: "The addition of ERICO's complementary business will expand our presence in the commercial and industrial sectors. ERICO has a strong global business and valued brands, making it a perfect fit for Pentair. We have similar cultures and serve similar industries with complementary products."

Hoffman and Schroff were already Pentair brands. With the ERICO acquisition, Pentair had assembled the core pieces of what would become nVent: enclosures (Hoffman, Schroff), thermal management (Raychem, Tracer), and electrical fastening solutions (ERICO, CADDY).

But Pentair was fundamentally a water company. And as the electrical portfolio grew, management recognized that two very different businesses with distinct customer bases were sharing one corporate umbrella—a recipe for neither achieving its full potential.

III. The Spin-Off: Birth of nVent

A. The Strategic Logic Behind the Separation

The Board of Pentair plc announced the spin-off of the electrical business on May 9, 2017. The announcement sent ripples through the investment community, but the logic was straightforward.

After the divestiture, Pentair CEO Randy Hogan said the company had $5 billion in revenue and two businesses that were largely unrelated, with separate management teams and lean manufacturing structures. "And there is no common [sales] channel and no common customers" between the two.

The textbook rationale for spin-offs—strategic focus, capital allocation discipline, targeted investor base—applied perfectly here. The separation from Pentair in 2018 was the foundational moment, allowing nVent to dedicate 100% of its focus and capital allocation to the electrical solutions market, attracting investors specifically interested in this sector.

The reason behind the separation comes straight out of the textbook, as both individual businesses have greater strategic focus and can control their own capital allocation.

B. Beth Wozniak: The Right Leader at the Right Time

Beth Wozniak was only four months into her new job as the head of Pentair's $2.1 billion electrical division when the CEO suggested they talk. Pentair's board had just decided to spin off her electrical division into a separate, public company in an effort to maximize growth opportunities for shareholders. If all went well, the Pentair Electric division she ran would become a stand-alone company called nVent Electric PLC.

"I was caught off guard. But I have always aspired to be a CEO at some point in my career. I'm excited," said Wozniak, a longtime Honeywell executive who joined Pentair in 2015.

That understated response belied formidable credentials. Prior to joining Pentair in 2015, Wozniak had a 25-year career at Honeywell, holding several executive leadership positions including President of the Environmental and Combustion Controls business and President of the Sensing and Control business. Through her career at Honeywell, she held various executive positions in both the Automation and Control, and Aerospace business units.

Beth Wozniak has a Bachelor of Engineering from McMaster University and a Master of Business Administration from York University, Toronto. Wozniak, who grew up in Canada, earned her bachelor's degree in engineering physics. With her STEM background and talent for business, she built a long career at Honeywell, was hired in a key role at Pentair by former CEO Randy Hogan, and has been a public company CEO for five years.

In 2023, it's still a rarity for a woman to be the top executive of a manufacturing company. When Wozniak became the inaugural CEO of nVent, she chose to set a tone that supported diversity at all levels of the company. "The first principle was just around inclusion and diversity, that we wanted this to be a culture where everyone felt that they could be their authentic self," Wozniak says.

C. Day One: The Spin Mechanics

In 2018, nVent became an independent, publicly-traded company (NYSE: NVT) after separating from Pentair plc. The distribution of nVent ordinary shares occurred effective at 4:59 p.m. EDT on April 30, 2018. In the distribution, nVent issued one nVent ordinary share for each Pentair ordinary share held as of the close of business on April 17, 2018, the record date for the distribution.

Pentair plc completed the spin-off of nVent Electric plc for $3.8 billion on April 30, 2018.

nVent didn't raise traditional venture capital. It was capitalized through the distribution of its shares to Pentair shareholders, launching on the NYSE with assets previously valued within Pentair's Electrical division, which generated approximately $2.1 billion in revenue in 2017 prior to the spin.

When Pentair and nVent officially split, Pentair became a company with annual revenue of $2.8 billion. nVent began its journey with $2.1 billion in sales and 9,000 employees, 1,600 of them in Minnesota.

The capitalization wasn't without controversy. nVent borrowed $1 billion and gave almost all of it to its former parent. nVent Finance S.à r.l. issued $800.0 million of senior unsecured notes, consisting of $300.0 million of 3.950% senior notes due 2023 and $500.0 million of 4.550% senior notes due 2028. nVent was expected to have approximately $1.0 billion of indebtedness upon completion of the separation.

Yet this structure, while seemingly burdensome, would prove manageable—and would force management discipline from day one.

D. The Spin Philosophy: Why These Deals Create Value

"With the completion of this spin, nVent has achieved a major milestone in becoming a more focused, global leader in providing electrical connection and protection solutions to customers around the world," said Beth Wozniak. "We are going to be a fast-paced, dynamic growth company, focused on our customers and moving with velocity."

The broader lesson of nVent's spin-off extends beyond its own story. Corporate spin-offs have historically outperformed the market, and nVent exemplifies why. When a division is buried within a conglomerate, it competes for capital against unrelated businesses. Its management is distracted by corporate politics. Its investors are generalists who may not understand the end markets.

Separation unlocks focused capital allocation, attracts specialized investors, and—perhaps most importantly—creates accountability. There's nowhere to hide when you're the only show on the earnings call.

IV. Building the Growth Engine: The First Five Years (2018-2020)

A. Establishing Independence

From day one, Wozniak positioned nVent not as a mature industrial business content with harvest mode, but as a growth company that happened to have century-old brands.

"With this full suite of products, we have tremendous opportunity to grow" both organically and through acquisitions, said Wozniak. "We're going to be a fast-paced, dynamic-growth company focused on the customer and moving with velocity."

The initial investor reception was cautiously optimistic. Analysts appreciated the focused strategy but wanted proof of execution. The company delivered. As UBS Investment Bank analyst Steve Winoker noted, nVent is in some "very lucrative markets" with businesses carrying "healthy" margins. But Winoker also questioned whether nVent would invest enough money into research and development to drive growth long term.

B. The Data Center Opportunity Emerges

The most consequential strategic insight of nVent's early independence came not from the executive suite but from the sales floor. Since spinning off from Pentair in 2018, the company has pursued a strategy to benefit from the electrification of everything, which includes the data centers that support the cloud storage of companies from Amazon, Meta and Google. nVent produces products largely unseen to the public, products that fuel the modern infrastructure that ensure everyday lives run uninterrupted—including the enclosures that protect all sorts of electrical equipment from dust, debris, water and temperature extremes.

"You cannot build any electrical infrastructure without grounding, bonding, power connections, enclosures," CEO Beth Wozniak told investors. "And we benefit from all of these trends."

Hyperscale customers—the Amazons, Microsofts, and Googles of the world—came to nVent directly when they realized the company had a comprehensive offering. They already used the protective electrical enclosures that keep moisture away from components. But they started asking about tools that track temperatures, cool equipment, and sound alarms during heat spikes.

Wozniak launched a new commercial sales team and hired a manager to grow the data center business. The goal was to bring together products from across the company's three segments—enclosures, fasteners, and thermal management—and apply all offerings to data center customers. It worked, spurring double-digit growth.

C. Navigating External Challenges

The late 2010s brought external turbulence that tested nVent's operational resilience. When Trump administration trade tariffs launched, suppliers hiked prices on the steel nVent uses to make electrical cabinets. Management had to execute three price increases over the course of a single year as steel prices spiked, followed by copper increases, then freight cost increases.

Yet nVent's margin discipline held. The company's ability to pass through cost increases while maintaining customer relationships demonstrated the stickiness of its products in critical applications. When the cost of failure is measured in millions of dollars of damaged equipment or days of lost data center availability, customers don't switch suppliers over modest price increases.

V. The M&A Transformation: Key Acquisitions

A. The Acquisition Philosophy

Post-spin-off, nVent deliberately pursued strategic acquisitions like Eldon, WBT, and Texa to fill portfolio gaps, enhance technological capabilities, and expand geographic reach, rather than relying solely on organic growth. This approach has proven effective in building scale and market presence rapidly.

nVent since 2020 has made six acquisitions. The pattern reveals a disciplined approach: target companies with strong brands, complementary customer bases, and room for operational improvement under nVent's management system.

B. ECM Industries: The $1.1 Billion Bet (2023)

In May 2023, Sentinel Capital Partners announced the sale of portfolio company ECM Industries to nVent Electric plc for a purchase price of $1.1 billion.

Headquartered in New Berlin, Wisconsin, ECM is a global manufacturer and supplier of electrical connectors, tools, and test instruments for construction, maintenance, lighting, irrigation, landscape supply, and gas utility applications. ECM serves professional electricians, contractors, maintenance technicians, and do-it-yourselfers with a wide range of premium brands, including ILSCO, Gardner Bender, and King Innovation. ECM has more than 1,400 employees and operates in North America and Shanghai.

ECM Industries is a North American provider of electrical connectivity products with industry-leading brands. Headquartered in New Berlin, Wisconsin with approximately 1,400 employees, ECM Industries had revenues of $415 million and adjusted EBITDA of $104 million in the twelve months ended February 28, 2023.

The effective enterprise value multiple was approximately 10.6 times trailing twelve month ECM Industries' adjusted EBITDA.

The ILSCO brand, in particular, filled a critical gap in nVent's power connections portfolio. nVent traces roots back to the 1894 founding of the Incandescent Lighting and Stove Company (ILSCO), a manufacturer of gas lighting systems. The acquisition reunited one of the industry's oldest brands with nVent's century-old heritage.

C. Trachte: Control Buildings Platform (2024)

nVent announced a definitive agreement to acquire the parent of Trachte, LLC for a purchase price of $695 million. Trachte is a leading manufacturer of custom-engineered control building solutions designed to protect critical infrastructure assets.

Since its founding in 1901, Trachte has been the market leader in quality, customization, reliability, and customer service. Trachte estimated 2024 revenues to be approximately $250 million.

Beth Wozniak explained the strategic rationale: "Trachte will expand our enclosures portfolio in new applications and enhance our system protection capability. It further strengthens our solutions in high-growth verticals, including power utilities, data centers and renewables."

In July 2024, nVent Electric plc completed its acquisition of the parent of Trachte LLC for a purchase price of $695 million.

The Trachte acquisition represented a platform play—not just acquiring a business, but establishing a beachhead in a new product category (prefabricated control buildings) that could be scaled through future acquisitions and organic expansion.

D. Electrical Products Group (EPG): The $975 Million Crown Jewel (2025)

nVent announced a definitive agreement to acquire the enclosures, switchgear and bus systems businesses of Avail Infrastructure Solutions (the "Electrical Products Group") for a purchase price of $975 million. The Electrical Products Group is a leading provider of infrastructure solutions, designed to help ensure safe and reliable electrical operations primarily in the infrastructure vertical, including power utilities and data centers.

The Electrical Products Group business is a leading North American provider of infrastructure solutions with approximately 1,100 employees and nine manufacturing locations in the United States. Electrical Products Group estimates revenues of approximately $375 million in the 12 months ending February 28, 2025, and has a strong backlog.

Announced in March 2025 and completed on May 1, the $975 million all-cash deal added critical capabilities to nVent's portfolio, including custom-engineered control buildings, switchgear, and bus systems.

"We are excited to acquire the Electrical Products Group of Avail," said Beth Wozniak. "The demand for control buildings, switchgear and bus systems is expected to increase with the modernization of aging electrical infrastructure, expanding electrical capacity to meet power demand and the growth of data centers. The Electrical Products Group has long-standing customer relationships with power utilities, data centers, OEMs and EPCs and a significant installed base across the United States."

The EPG acquisition performed ahead of expectations in Q2 and Q3 2025, increasing the adjusted EPS outlook by approximately $0.10.

VI. The Strategic Pivot: Portfolio Transformation

A. Selling Thermal Management to Brookfield

While acquisitions expanded nVent's Systems Protection and Electrical Connections segments, management made an equally consequential decision: to exit a business that had been part of the company since its founding.

nVent announced it had entered into a definitive agreement to sell its Thermal Management business, which includes the industry-leading RAYCHEM and TRACER brands, to funds managed by Brookfield Asset Management for a cash purchase price of $1.7 billion. With 2023 sales of $595 million and approximately 1,700 employees around the world, Thermal Management is a leader in mission critical electrical thermal solutions.

In January 2025, nVent completed the sale of its Thermal Management business to funds managed by Brookfield Asset Management for a sale price of $1.7 billion. "Today marks a significant step in transforming our portfolio with the sale of the Thermal Management business and becoming a higher growth and more focused electrical connection and protection leader," said Beth Wozniak.

nVent expected net after-tax proceeds from the transaction of approximately $1.4 billion and intended to use the proceeds for acquisitions and share repurchases.

The decision to divest Raychem—the brand with the most storied Silicon Valley heritage—was not sentimental but strategic. Thermal management, while profitable, was growing more slowly than the enclosures and connections businesses. By selling to Brookfield at an attractive multiple, nVent recycled capital into higher-growth areas while sharpening its portfolio focus.

B. The New nVent: Two Focused Segments

The Infrastructure vertical now accounts for over 40% of nVent's portfolio, with data centers and power utilities each contributing approximately 20%. This concentration is not accidental but a calculated bet on long-term tailwinds.

Post-divestiture, nVent operates through two segments: Systems Protection (the former Enclosures segment plus Trachte and EPG control buildings) and Electrical Connections (the former Electrical & Fastening Solutions segment plus ECM/ILSCO).

The transformation from the 2018 spin-off is remarkable. At spin, infrastructure revenue represented approximately 12% of the portfolio. Today it exceeds 40%. The company has essentially repositioned itself from a general industrial supplier to an infrastructure-focused growth company—all while maintaining margin discipline.

VII. The AI Inflection: Data Center Dominance

A. Liquid Cooling: The Next Frontier

With over 15 years of experience in liquid cooling, nVent's deep technical application experience and global presence enables creating efficient solutions that ensure optimal performance and reliability for advanced computing environments.

nVent has deployed over 1 GW of cooling solutions and specializes in high-density liquid cooling solutions designed for optimal performance.

With a 4X increase in liquid cooling capacity in 2024, nVent has positioned itself as a go-to partner for data center customers.

TrendForce's recent report states that the launch of NVIDIA's Blackwell platform is set to drive the adoption of liquid cooling solutions from around 10% in 2024 to over 20% in 2025.

The math is compelling. Traditional air cooling struggles above 30-40 kW per rack. AI training clusters using NVIDIA's latest Blackwell GPUs can exceed 100 kW per rack. Liquid cooling isn't optional—it's physics.

B. The NVIDIA Partnership Advantage

nVent announced collaboration with NVIDIA to deploy liquid cooling solutions at scale supporting the NVIDIA GB200 NVL72 and next-generation platforms. The collaboration is expected to deliver cutting-edge, built-to-spec liquid cooling technology to enhance the performance and energy efficiency of NVIDIA-powered data centers.

nVent is contributing to active development programs with hyperscale and high-performance computing (HPC) customers, delivering customized liquid cooling solutions that support NVIDIA NVL36 and NVL72 deployments. nVent worked with NVIDIA to define a reference architecture that utilizes nVent's coolant distribution unit, liquid-to-air heat exchanger and manifold products.

"nVent is delivering the future of liquid cooling. We design customized technologies that manage the operating temperatures of high-performance chips, driving efficiency, scalability and sustainability for our customers," said Eric Osborn, nVent VP and general manager, data center solutions.

nVent was named to the NVIDIA partner network; the new Minnesota facility is expected to begin production early next year and effectively double the liquid cooling manufacturing footprint.

C. Manufacturing Expansion to Meet Demand

nVent announced the lease of new manufacturing space in Blaine, MN. The new 117,000 square foot facility will expand nVent's data center solutions manufacturing production to meet growing liquid cooling demand. This is the second time in two years nVent has expanded its data center solutions manufacturing footprint.

This expansion follows a recent production capacity increase at nVent's Anoka, Minnesota facility. Together, the Anoka and Blaine expansions will add more than 325 jobs.

nVent also announced increased manufacturing capacity in Eleanor, West Virginia, to support continued demand in the data center industry for large enclosures. This expansion will create more than 100 new manufacturing jobs in Eleanor over the next six to eight months.

In Q3 2025, the company experienced a notable 16% growth in organic sales, outperforming projections. Additionally, total orders increased by 65%, with data center orders showing a significant rise of 270%.

VIII. Playbook: Business & Strategy Lessons

A. The Spin-Off Playbook

nVent's journey from Pentair orphan to infrastructure leader offers a masterclass in corporate separation value creation:

-

Focused management attention: When you're the only business on the earnings call, there's nowhere to hide. Every capital allocation decision, every growth initiative, every margin improvement program receives undivided attention.

-

Specialized investor base: Generalist Pentair investors were replaced by investors specifically interested in electrical infrastructure and the "electrification of everything" theme.

-

Disciplined capital allocation: With a clean balance sheet and focused mandate, management could pursue bolt-on acquisitions without competing for capital against unrelated water businesses.

B. The "Buy, Integrate, Transform" Model

nVent's M&A strategy follows a repeatable pattern:

- Target selection: Companies with strong brands, complementary customer bases, and operational improvement potential

- Disciplined pricing: Typically paying 10-12x EBITDA, leaving room for value creation

- Rapid integration: Leveraging the Pentair heritage of lean manufacturing and operational excellence

- Commercial synergies: Cross-selling across the combined portfolio to existing customers

CFO Gary Corona noted on the Q3 2025 call regarding the EPG acquisition: "It's both. We are driving more top line growth than initially expected. And the margins are looking a bit better than we initially forecasted as well. As we drive scale and efficiency through the plant network."

C. Riding Secular Tailwinds

Embracing Electrification Megatrends: Recognizing the significant tailwinds from global trends like decarbonization, digitalization, and automation, nVent strategically pivoted its innovation and resources towards high-growth areas such as renewable energy infrastructure.

More than 70% of the company's portfolio is exposed to secular growth trends. The "electrification of everything" thesis—that the world's energy consumption will increasingly shift from hydrocarbons to electrons—provides a durable tailwind for nVent's products.

Data centers, power utilities, renewable energy, EV charging infrastructure, industrial automation—all require electrical connection and protection solutions. nVent is positioned as a picks-and-shovels play on electrification writ large.

D. Beth Wozniak's Leadership Principles

A fierce competitor since she was a high school swimmer, Beth Wozniak is striving to lead her company to $5 billion in annual revenue. It's a huge leap, because nVent's total sales for electrical products and solutions were around $2 billion a year when the business was spun off from Pentair in 2018. But Wozniak isn't content to savor the fact that she led the public company from $2 billion to $3 billion in total revenue within five years.

"It's conceivable that within three years, while doing acquisitions, that we can get from $3 billion to $5 billion," Wozniak told Twin Cities Business.

Her leadership style balances organic investment with acquisitions, customer-led innovation with operational excellence, and aggressive growth targets with disciplined execution.

IX. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

With over 15 years of experience in liquid cooling, nVent's deep technical application experience and global presence is difficult to replicate.

nVent's robust portfolio of leading electrical product brands dates back more than 100 years.

New entrants face formidable barriers: - Brand heritage: Relationships with customers and specifiers built over decades - Certification requirements: Products must meet stringent safety standards (UL, CSA, IEC) - Manufacturing scale: Global footprint with localized production - Technical expertise: Deep application knowledge in critical infrastructure

2. Threat of Substitutes: LOW

Electrical enclosures, grounding products, and liquid cooling systems are mission-critical components with no viable substitutes. The cost of failure—damaged equipment, downtime, safety incidents—far exceeds any savings from inferior alternatives.

3. Bargaining Power of Suppliers: MODERATE

nVent sources commodities (steel, copper, aluminum) from multiple suppliers. While commodity price volatility creates cost pressure, the company has demonstrated ability to pass through increases via pricing actions.

4. Bargaining Power of Buyers: MODERATE

Hyperscale data center operators have significant purchasing power but prioritize reliability over cost. Industrial and commercial customers are fragmented, reducing collective bargaining power. Specification influence—where products are designed into projects by engineers—creates stickiness.

5. Competitive Rivalry: MODERATE-HIGH

In the enclosures market, nVent competes with Schneider Electric, ABB, and Eaton Corporation. These competitors offer similar industrial enclosure solutions and compete on factors including product quality, technical innovation, and global reach.

Schneider Electric, Vertiv, ABB, Eaton, and Delta Electronics are leading market players in data center power solutions.

However, nVent's diversified product portfolio, specialized focus, and acquisition strategy differentiate it from conglomerate competitors who treat electrical infrastructure as one business among many.

Hamilton Helmer's 7 Powers Framework

1. Economies of Scale (PRESENT)

With over $3.5 billion in revenue, nVent achieves manufacturing and procurement scale that smaller competitors cannot match. Global manufacturing footprint reduces logistics costs and enables local customization.

2. Network Effects (LIMITED)

Unlike software platforms, physical products don't exhibit strong network effects. However, specification influence creates mild network-like dynamics: the more projects feature nVent products, the more familiar engineers become with specifying them.

3. Counter-Positioning (PRESENT)

nVent's focused strategy creates counter-positioning against diversified competitors. Schneider Electric and ABB have electrical infrastructure businesses but must balance capital allocation across numerous segments. nVent's pure-play focus attracts specialized investors and enables more aggressive investment in growth opportunities.

4. Switching Costs (MODERATE)

Customers incur moderate switching costs: - Training on new product lines - Updated specifications and drawings - Relationship rebuilding with new suppliers - Risk of compatibility issues in existing installations

For mission-critical applications, these costs create meaningful stickiness.

5. Branding (PRESENT)

Century-old brands like ERICO, HOFFMAN, and ILSCO carry significant equity with specifying engineers and contractors. Brand recognition reduces sales cycles and supports premium pricing.

6. Cornered Resource (LIMITED)

nVent does not possess unique raw materials or patents that prevent competition. However, accumulated technical expertise in liquid cooling for AI applications represents a knowledge resource that's difficult to replicate quickly.

7. Process Power (PRESENT)

Lean manufacturing heritage from Pentair, combined with acquisition integration expertise, creates process advantages. The ability to quickly integrate acquired businesses and realize synergies is a repeatable capability that compounds over time.

Competitive Comparison

| Company | Focus | Data Center Exposure | M&A Strategy | Pure-Play Status |

|---|---|---|---|---|

| nVent | Electrical connection & protection | ~20% of sales | Aggressive bolt-ons | Yes |

| Schneider Electric | Diversified electrical/automation | Significant | Transformational | No |

| Eaton | Diversified power management | Growing | Selective | No |

| ABB | Diversified automation/robotics | Growing | Selective | No |

| Vertiv | Data center infrastructure | Primary focus | Active | Yes |

nVent occupies a differentiated position: more focused than diversified giants, more diversified than pure-play cooling specialists, and more acquisitive than both.

X. Key Performance Indicators: What to Watch

For long-term fundamental investors tracking nVent's ongoing performance, three KPIs deserve particular attention:

1. Data Solutions Organic Order Growth

When discussing the 65% order growth in Q3 2025, management noted that this was all organic and did not include inorganic contribution from acquisitions like EPG. The core business was up high single digits on orders excluding acquisitions, but data centers overall is driving significant order growth for overall nVent.

Data center orders represent the leading indicator of nVent's AI infrastructure exposure. The 270% increase in data center orders in Q3 2025 signals extraordinary demand, but sustainability is key. Watch quarter-over-quarter trends for signs of demand normalization or acceleration.

2. Adjusted Operating Margin

The company maintained 20.8% operating margins amid inflation.

nVent's ability to maintain margins while integrating acquisitions, investing in capacity expansion, and navigating commodity volatility demonstrates operational discipline. Margin compression would signal execution issues; margin expansion would validate operating leverage.

3. Backlog Conversion Rate

Management noted that backlog has grown, driven by orders in data solutions and liquid cooling, as well as acquired backlog from EPG.

With multi-year visibility into AI data center build-outs, backlog provides forward revenue visibility. The rate at which backlog converts to revenue—and whether backlog continues growing—indicates sustainability of demand trends.

XI. Bull Case and Bear Case

The Bull Case

Secular tailwinds are accelerating. The global data center liquid cooling market is projected to expand from $5.38 billion in 2024 to $17.77 billion by 2030—a compound annual growth rate of 21.6%. nVent's early mover advantage in AI-optimized liquid cooling positions it to capture disproportionate market share.

Acquisition integration excellence creates compounding value. Each successful integration—ECM, Trachte, EPG—builds institutional capability for the next deal. With $1.4 billion of Thermal Management proceeds available, the M&A engine has fuel.

Margin expansion potential remains. As acquired businesses achieve nVent's operational standards and scale economies kick in, margins should expand beyond current levels.

Infrastructure investment cycle is early innings. Grid modernization, renewable energy build-out, EV charging infrastructure, and data center expansion represent multi-decade investment cycles. nVent's product portfolio addresses all of these verticals.

The Bear Case

Data center CapEx cyclicality risk. Investors need to believe that AI-driven data center buildouts will support robust demand. On the other hand, if data center CapEx stalls, the additional capacity could present challenges.

Hyperscale operators could reduce or delay capital spending if AI monetization disappoints or macroeconomic conditions deteriorate. nVent's aggressive capacity expansion would then represent overcapacity.

Acquisition integration risk. The company has now completed multiple large acquisitions in rapid succession. Integration complexity compounds with each deal, and execution missteps could erode value.

Competition from diversified giants. Schneider Electric, ABB, and Eaton have deep pockets and existing customer relationships. If they prioritize data center infrastructure more aggressively, nVent could face intensified competition.

Margin pressure from growth investments. Capacity expansion, R&D, and sales force buildout require investment that could pressure near-term margins. The market may not reward growth if it comes at the expense of profitability.

XII. Myth vs. Reality

MYTH: "nVent is just a boring industrial company with old-economy products."

REALITY: nVent offers the growth of a tech company, the margins of a manufacturer, and the valuation of a value stock. In a market where many industrial firms struggle with cyclical volatility, nVent's focus on secular trends—AI, electrification, and decarbonization—provides a durable edge.

MYTH: "Liquid cooling is commoditized—anyone can make pipes and pumps."

REALITY: nVent's world-class engineering hubs, on-site labs and production facilities have produced liquid cooling technology that is tested and customized to support NVIDIA platforms, enabling customers to deploy and scale next-generation AI technology. Co-development partnerships with NVIDIA are not easily replicable.

MYTH: "The company's best growth is behind it after the AI-driven surge."

REALITY: Management highlighted visibility into data solutions and liquid cooling orders and backlog through 2026 and beyond. The AI infrastructure build-out is measured in years, not quarters.

XIII. Risk Factors & Material Considerations

Regulatory and Legal Considerations

nVent operates in heavily regulated industries where product certifications (UL, CSA, IEC) are mandatory. Changes to electrical codes or certification requirements could require product modifications. The company's global footprint exposes it to varying regulatory regimes.

Accounting Judgments

Key accounting considerations include: - Acquisition purchase price allocation: Significant judgment in allocating purchase prices between goodwill, intangibles, and tangible assets - Revenue recognition: Long-term contracts and custom-engineered products require judgment on timing of revenue recognition - Inventory valuation: In a business with thousands of SKUs, obsolescence reserves require management estimates

Concentration Risk

Data center and power infrastructure segments together account for approximately 40% of nVent's sales. While exposure to high-growth verticals is a strength, concentration creates vulnerability to sector-specific downturns.

XIV. Conclusion: The Infrastructure Backbone of Tomorrow

In 1903, the Electric Railway Improvement Company was founded to solve a seemingly mundane problem: how to safely connect electrical current to railroad tracks. Over the following 122 years, that founding mission—enabling electricity to flow safely where it should—has evolved but never changed.

Today, nVent Electric sits at the convergence of the most significant infrastructure investment cycles of the 21st century. Every hyperscale data center training AI models requires nVent's liquid cooling. Every power utility modernizing the grid relies on nVent's grounding products. Every renewable energy installation depends on nVent's enclosures to protect electronics from the elements.

Since April 17, 2018, nVent Electric's market cap has increased from $4.55B to $17.74B, an increase of 290.18%. Yet relative to the infrastructure opportunity ahead—grid modernization measured in trillions, AI CapEx measured in hundreds of billions, electrification investments spanning decades—the company's story may be just beginning.

What was once a collection of century-old industrial brands buried within a water pump conglomerate has become a focused infrastructure enabler for the AI age. The spin-off unlocked value. The acquisitions accelerated growth. The data center opportunity provided a secular tailwind.

And through it all, the founding insight remains: the world runs on electricity, and electricity requires connection and protection. nVent provides both.

For investors seeking exposure to the electrification of everything without betting on specific technology winners, nVent offers a differentiated proposition: infrastructure picks and shovels with margin discipline, focused management, and multi-decade secular tailwinds.

The hidden infrastructure giant isn't so hidden anymore.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube