Nucor Corporation: The Mini-Mill Revolution That Ate Big Steel

I. Introduction & Episode Roadmap

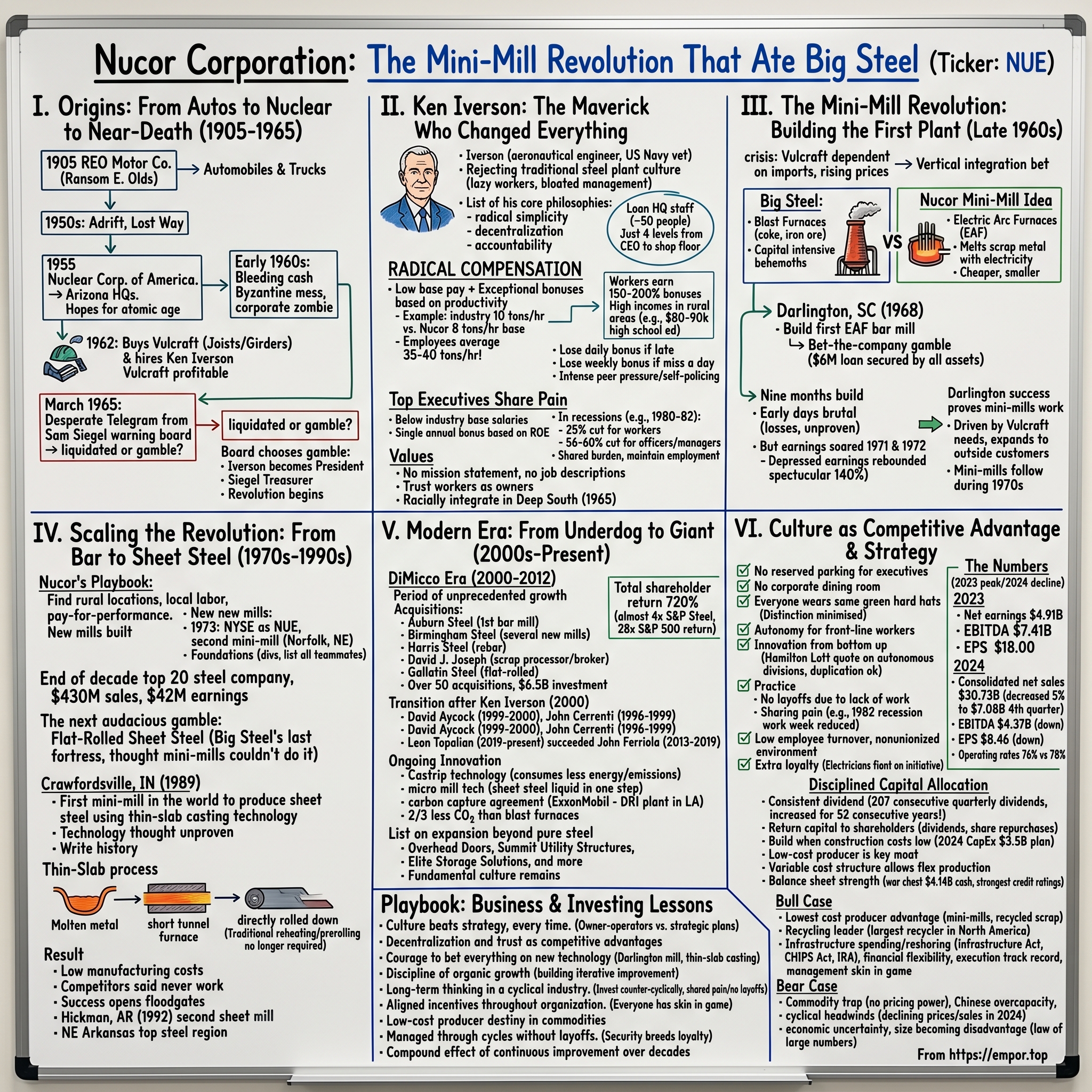

Picture this: It's 1965, and a struggling conglomerate called Nuclear Corporation of America is hemorrhaging cash so fast that bankruptcy seems inevitable. The company—which started life in 1905 as REO Motor Company, founded by Ransom E. Olds of Oldsmobile fame—has wandered through decades of identity crises, from automobiles to nuclear services to whatever might keep the lights on. The board receives a desperate telegram from company president Sam Siegel warning that without immediate action, they'll be insolvent within weeks.

Fast forward to today: That same company, renamed Nucor, stands as America's largest steel producer, North America's largest recycler, and the 16th-largest steel producer globally. How did a nearly bankrupt conglomerate with delusions of nuclear grandeur become the company that fundamentally revolutionized American steel manufacturing? The answer lies in a radical reimagining of what a steel company could be—lean, decentralized, egalitarian, and technologically fearless. The story we're about to explore isn't just about steel—it's about an audacious bet that a radically different approach to manufacturing, management, and corporate culture could topple an entire industry's orthodoxy. It's about Ken Iverson, an aeronautical engineer who saw lazy workers sleeping on the job at a traditional steel plant and vowed never to be part of that system. It's about mini-mills that could produce steel at a fraction of the cost using recycled scrap metal instead of iron ore. And it's about proving that in the commodity business of steel production, culture and innovation could be durable competitive advantages.

In 2024, this revolution generated $30.73 billion in net sales, with full year diluted earnings per share of $8.46 and EBITDA of $4.37 billion—numbers that would have seemed like pure fantasy to that desperate board receiving bankruptcy warnings in 1965. This is the story of how a dying conglomerate transformed into the force that fundamentally reshaped American manufacturing. Welcome to the Nucor revolution.

II. Origins: From Automobiles to Nuclear to Near-Death

The year is 1905. Ransom E. Olds, fresh off his success creating Oldsmobile, decides to launch another venture: REO Motor Company. The initials stood for Ransom Eli Olds himself, and the company would build automobiles and trucks for decades. But by the 1950s, REO had lost its way. The company that once competed with the giants of Detroit found itself adrift in a rapidly consolidating auto industry.

Enter the atomic age. In a move that epitomized the era's fascination with all things nuclear, REO Motor Company transformed itself into Nuclear Corporation of America in 1955. The logic seemed sound at the time—nuclear energy was the future, and any company with "nuclear" in its name would surely ride that wave to prosperity. They moved headquarters to Phoenix, assembled a hodgepodge of businesses they hoped might somehow relate to nuclear services, and waited for the atomic revolution to mint money.

It never came. By the early 1960s, Nuclear Corporation was bleeding cash from nearly every division. The nuclear services strategy had failed spectacularly. The conglomerate structure—so fashionable in that era—had created a Byzantine mess of unrelated, unprofitable businesses. The company was essentially a corporate zombie, shambling toward insolvency. Then, in 1962, came a fateful acquisition that would change everything. Nuclear Corporation bought Vulcraft, a manufacturer of steel joists and girders, and hired Ken Iverson to run it. Vulcraft was actually profitable—a rare bright spot in the constellation of failing ventures. Under Iverson's leadership, Vulcraft tripled sales and profits over the next three years, while the rest of Nuclear Corporation was losing money so quickly that the company was headed toward bankruptcy.

By March 1965, the situation had become terminal. The company filed for bankruptcy. The board faced a stark choice: liquidate everything or take one last desperate gamble. In what might be the most consequential telegram in American industrial history, Sam Siegel, a corporate accountant for the company, resigned but sent a telegram to the Board saying he would reconsider if the board named him treasurer and Iverson president.

The board, with no better options and facing the abyss, agreed. Iverson, head of the only profitable division, took over as head of the company due to lack of interest in the job from others. It was March 1965, and a revolution was about to begin. The dying conglomerate had just handed the keys to an aeronautical engineer who would prove that in the commodity business of steel, the real competitive advantage wasn't scale or technology—it was culture.

III. Ken Iverson: The Maverick Who Changed Everything

F. Kenneth Iverson was born September 18, 1925 in Downers Grove, Illinois, a rural town west of Chicago. He served in the U.S. Navy from 1943 to 1946, rising to the rank of lieutenant. He earned a Bachelor of Science degree in aeronautical engineering from Cornell University and later received a master's degree in mechanical engineering at Purdue University. But it was an early work experience that would shape his entire philosophy of business.

As a young engineer, Iverson had taken a job at an integrated steel plant—one of those massive, traditional operations that dominated American industry. What he saw there disgusted him. Workers literally sleeping on the job. Bloated management ranks. A culture of entitlement and inefficiency so pervasive it seemed baked into the industry's DNA. Iverson made a vow: he would never work for big steel. He didn't know it at the time, but this rejection would eventually lead him to destroy big steel's entire business model.

Iverson's management philosophy was revolutionary. His 1998 book, Plain Talk: Lessons from a Business Maverick, detailed his unique management approach, which has since been used as a model in Harvard Business School case studies and was featured in Jim Collins' popular management book Good to Great. But calling it a "philosophy" almost gives it too much credit for complexity. Iverson believed in radical simplicity, radical decentralization, and radical accountability.

First, the lean corporate staff. To this day, Nucor has one of the smallest headquarter staffs of any Fortune 500 company—about 50 people. Think about that for a moment. Companies a fraction of Nucor's size often have hundreds or thousands of corporate employees. Iverson saw corporate bureaucracy as pure overhead, a tax on the productive parts of the business. Second, the organizational structure: just four levels from CEO to shop floor operator. Think about your typical Fortune 500 company with its VPs, Senior VPs, Executive VPs, and countless gradations of middle management. Iverson stripped all that away. He joined Nuclear Corporation in 1962 when it bought Vulcraft, where he worked, and quickly rose to president in 1965. From there, he built a structure so flat that a janitor was four promotions away from the CEO's job.

But the real revolution was in compensation. Every Nucor teammate's compensation is based on a pay-for-performance system tied to productivity. This wasn't some corporate buzzword—it was radical alignment of incentives. While employees are paid a lower than industry average hourly rate, they qualify for exceptional performance bonuses if they exceed hourly quotas. For example, the steel industry average says an individual should straighten 10 tons of steel an hour. Nucor's goal is 8 tons an hour. Employees get an additional 5 percent bonus for every ton over 8 tons. They typically average 35 to 40 tons an hour.

The math is staggering: workers producing at four times the quota, earning bonuses of 150-200% on top of base pay. In practice, this means that an employee making $20/hour will actually make $40-60/hour depending on the production bonus. Entry-level employees with only a high-school education in rural areas can easily earn $80-90k per year, while production supervisors can make in excess of $150k.

But here's the catch that made it work: If they are late to work they lose their bonus for the day. And if they miss a day of work during the week they lose their bonus for the entire week. The system created intense peer pressure and self-policing. Your teammates weren't just colleagues—they were partners whose paychecks depended on your performance.

The system extended all the way up. Senior officers have one compensation system. They do not get profit sharing, pensions, bonuses or retirement plans, and their base salaries are also set below industry averages. They receive one annual bonus based on the return of shareholders equity above certain minimum earnings. Paid 60 percent in stock and 40 percent in cash, the bonus ranges from 0 to several hundred percent of salary. During the deep recession of 1980-82, when the company had to cut production in half, the average Nucor worker's earnings fell by 25 percent while department heads took a 40 percent cut and general managers and officers had their earnings reduced by 56 to 60 percent. In stark contrast to the competition, Nucor maintained employment and asked all employees to share the pain.

Perhaps most remarkably, Iverson instilled values that seem almost quaint by modern corporate standards. These included: Lean corporate staff. To this day, Nucor has one of the smallest headquarter staffs of any fortune 500 company -- about 50 people. Pay based heavily on performance throughout the organization, with the top executives having the highest percentage of their pay at risk. One of his first initiatives upon taking over was to racially integrate the company—in the Deep South in 1965, no less.

When business school students would call asking for Nucor's mission statement, Iverson would chuckle: "We don't have a mission statement." When they'd ask for job descriptions, he'd say: "We don't have any job descriptions." The callers would invariably respond: "Wait till my professor hears this!" Iverson didn't believe in complex management theories or elaborate strategic planning. He believed in treating people fairly, paying them for performance, and getting out of their way. The revolution wasn't in the technology—it was in trusting workers to act like owners.

IV. The Mini-Mill Revolution: Building the First Plant

By the late 1960s, Vulcraft faced a crisis that would catalyze the entire mini-mill revolution. The company's steel joist and deck businesses were dependent on imports from a single supplier, who kept raising prices. In order to save money, Iverson decided the company should build its own steel mill. This wasn't just vertical integration—it was a bet-the-company gamble on unproven technology.

The traditional steel industry operated massive blast furnaces that turned iron ore into steel—capital-intensive behemoths that cost hundreds of millions to build and required enormous workforces. Iverson had a different idea. He'd seen small electric arc furnace operations in Northern Italy, particularly among the Bresciani mini-mill operators, melting scrap metal with electricity instead of cooking iron ore with coke. The technology existed, but nobody believed it could work at scale in America.

In 1968, unable to get favorable steel prices from American manufacturers and unhappy with imported steel, Iverson extended Nucor vertically into steelmaking by building its first steel bar mill in Darlington, South Carolina. The company purchased an electric arc furnace, far cheaper than traditional blast furnaces, with a $6 million loan secured by all company assets.

Think about that for a moment. Iverson literally bet everything—every asset the company owned—on an unproven technology in an industry he'd never directly operated in. The board could have fired him. The banks could have refused. The whole thing could have been a disaster.

The construction was remarkably fast—nine months from groundbreaking to pouring steel. But the early days were brutal. Production delays and staffing problems resulted in losses. Workers didn't know how to operate the equipment properly. Quality was inconsistent. Traditional steel companies mocked the effort, certain that electric arc furnaces could never produce quality steel at scale. But then something clicked. Production delays and staffing problems resulted in losses, but earnings soared in 1971 and 1972. In 1972, the company, recognizing that it was now misnamed, adopted its current title, Nucor Corporation. That year, it became a public company via an initial public offering. Depressed earnings finally rebounded spectacularly in 1971, jumping 140 percent. In 1972, they leaped another 70 percent.

The success proved that mini-mills could work. Originally intended to supply Vulcraft's needs, the Darlington mill soon expanded to outside customers. The technology that everyone said couldn't compete was suddenly producing steel at costs that made big steel's economics look medieval. A flurry of minimills arose during the 1970s, following Nucor's lead and producing bar steel for the joist business at prices that eventually drove Bethlehem, Republic, and others out of the market.

By 1973, Nucor was listed on the NYSE as NUE and announced a second mini-mill in Norfolk, Nebraska. The company established traditions that would define its culture: the first dividend (paid every quarter since), the Nucor Foundation, and the remarkable practice of listing all teammates on the annual report—not just executives, but everyone.

By the end of the decade, Nucor ranked among the top 20 steel companies in the country, with sales of $430 million and net earnings of $42 million. Within a five-year span, it had more than tripled production through a series of new mill constructions. Its core business, Vulcraft, had also expanded through new plant openings and had virtually secured its position as the biggest steel joist producer in the United States.

The mini-mill revolution wasn't just about technology—it was about proving that a radically different approach to manufacturing could destroy incumbent advantages. Where big steel needed iron ore, coking coal, and massive infrastructure, Nucor needed scrap metal and electricity. Where big steel had unionized workforces and rigid hierarchies, Nucor had performance-based pay and radical autonomy. The revolution had begun, and big steel didn't even realize they were already losing.

V. Scaling the Revolution: From Bar to Sheet Steel

Building a network of mini-mills across America became Nucor's playbook through the 1970s and 1980s. Each new mill followed the same pattern: find a location in a rural area with access to electricity and transportation, hire locally, implement the pay-for-performance system, and let the plant managers run their operations with minimal corporate interference. The formula worked spectacularly.

But Nucor wasn't content to remain in the commodity bar steel business. The real prize—and the real challenge—was flat-rolled sheet steel, used in automobiles, appliances, and countless other applications. This was big steel's last fortress, the product they claimed mini-mills could never economically produce.

Enter the most audacious gamble in Nucor's history: the Crawfordsville, Indiana facility in 1989. This would be the first mini-mill in the world to produce flat-rolled steel using thin-slab casting technology. The technology was so unproven that a rival company produced an inch-thick report explaining why it would never work. Traditional steel companies were certain Nucor would fail spectacularly. The gamble worked. In 1989, Nucor opened the facility in Crawfordsville, Indiana—the first mini-mill in the world to produce flat-rolled steel using thin-slab technology. It was the summer of 1989, in the middle of cornfields at the edge of the small American town, when Nucor wrote history. The slabs, just 50 millimeters thick (compared to traditional 200-250mm slabs), passed through a short tunnel furnace before being directly rolled down to their final dimensions. The energy-intensive slab reheating and prerolling processes were no longer required.

Despite initial skepticism and production challenges—including a major breakout of hot steel in the early days—the plant was commercially successful right from the outset, thanks to its low manufacturing costs. The technology that competitors said would never work was suddenly producing sheet steel at costs that made traditional integrated mills look obsolete. As one executive later said, "We were told that mill will never succeed, and it will also bring down Nucor. We didn't believe that for a second."

The success at Crawfordsville opened the floodgates. In 1992, after three years of successfully producing sheet using thin-slab technology, Nucor opened a second sheet mill in Hickman, Arkansas. With two large mills in Mississippi County, northeast Arkansas became one of the top steel-producing regions in America. Every new plant brought further enhancement of the technology. Before long, Nucor was producing strip for the automotive industry, high-strength grades, and tube steels.

The transformation was complete: Nucor had gone from a joist manufacturer buying steel from others to a company that could produce virtually any steel product more efficiently than the giants that had dominated the industry for a century. A flurry of minimills arose during the 1970s and beyond, following Nucor's lead and producing steel at prices that eventually drove Bethlehem, Republic, and others out of entire market segments.

By the end of the 1990s, Nucor had proven that mini-mills could do everything integrated mills could do, only better, faster, and cheaper. The revolution wasn't just technological—it was a complete reimagining of how steel could be made. Where traditional mills needed billions in capital and thousands of workers, Nucor could build a competitive mill for a fraction of the cost with a fraction of the workforce. The mini-mill revolution had eaten big steel's lunch, and Nucor was leading the charge.

VI. Culture as Competitive Advantage

Walk into any Nucor plant and you'll immediately notice something different from traditional manufacturing facilities. There are no reserved parking spaces for executives. The corporate dining room doesn't exist. Everyone wears the same green hard hats. These might seem like small details, but they represent something profound: a culture where distinction between management and employees has been deliberately minimized.

The egalitarian approach wasn't window dressing—it was fundamental to how Nucor operated. Iverson believed in driving decision-making down to front-line workers who he thought were best positioned to make production decisions. Only five layers of management existed between front-line workers and the CEO. Think about that structure: Supervisor, Department Manager, General Manager, Chairman. That's it. Management consultants would regularly pressure Nucor to add layers, create more specialized roles, build out corporate functions. Iverson and his successors resisted every time. The innovation from the bottom up was perhaps most remarkable. Many or even most of Nucor's great innovations came from down in the divisions rather than from executives. Hamilton Lott, general manager of the Vulcraft Division, once said: "We are honest-to-god autonomous. That means we duplicate efforts made in other parts of Nucor. The company might develop the same computer program six times. But, the advantages of local autonomy are so great, we think it's worth it."

This wasn't inefficiency—it was recognizing that innovation happens closest to the work. When business consultants would ask about synergies and knowledge sharing, Iverson would shrug. He understood that the benefits of local autonomy—speed, ownership, innovation—far outweighed the costs of occasional duplication.

Perhaps most remarkably, "If you do your job today, you can have confidence that you'll have a job tomorrow. Nucor has a long standing practice of not laying off teammates due to lack of work." During the deep recession of 1980-82, when demand for domestic steel caused major companies to eliminate thousands of jobs, Nucor maintained employment. "In 1982 when the company had to cut production in half. This was done by reducing the work week to four days. As a result the average Nucor worker's earnings fell by 25 percent while department heads took a 40 percent cut and general managers and officers had their earnings reduced by 56 to 60 percent."

The pain sharing wasn't just talk. When times got tight, top management took pay cuts before anyone else. The executives earning the highest bonuses in good times took the biggest hits in bad times. This wasn't socialism—it was capitalism with skin in the game for everyone.

The results speak for themselves. "Evidence of this successful method is that the company has one of the lowest employee turnover rates in the industry and remains one of the few remaining nonunionized environments in manufacturing." In an industry dominated by unions, Nucor built an entirely non-union workforce that earned more than their unionized counterparts while maintaining flexibility that allowed the company to adapt quickly to market changes.

The culture also created extraordinary loyalty and initiative. BusinessWeek recounted a story of three Nucor electricians who, upon hearing that a plant's electrical grid had failed, took it upon themselves to drive hours to the plant or book plane tickets to the area without being asked. Once there, they worked 20-hour shifts for three days with no direct financial incentive. They acted like owners because the culture made them feel like owners.

Nucor had achieved something remarkable: proving that in the commodity business of steel production, culture could be a durable competitive advantage. While competitors copied their technology, nobody could replicate the thousands of daily decisions made by empowered employees who thought and acted like owners. The culture wasn't just nice to have—it was the engine that drove innovation, efficiency, and resilience through every market cycle.

VII. Modern Era: From Underdog to Giant

The transition from Ken Iverson's era to the modern age could have destroyed everything Nucor had built. Many companies lose their revolutionary edge when the founding generation steps aside. But Nucor's culture proved more durable than any single leader. In 2000, Dan DiMicco became CEO, succeeding prior CEOs David Aycock (1999-2000) and John Correnti (1996-1999). DiMicco, formerly the general manager of the company's highly profitable Nucor-Yamato Steel joint venture, was appointed CEO in September 2000. He would lead Nucor through a period of unprecedented growth and champion an ongoing fight for fair trade practices to save American jobs and the U.S. manufacturing industry.

DiMicco served as Nucor's CEO longer than anyone since company founder Ken Iverson. Under his leadership, Nucor delivered dramatic growth in profits and shareholder returns. From September 2000 through the end of 2012, Nucor completed over 50 acquisitions for a total investment of $6.5 billion, and Nucor's total shareholder return growth was 720%, which is almost 4 times greater than the total return of the S&P Steel Group Index and 28 times greater than the S&P 500's total return.

The acquisition strategy marked a significant evolution from the Iverson era's focus on building from scratch. The first major move came with Auburn Steel, a bar mill in New York—the company's first steel mill acquisition in its then 36-year history. In 2002, Nucor acquired Birmingham Steel, resulting in several new Nucor mills: Nucor Steel Kankakee, Inc.; Nucor Steel Jackson, Inc.; Nucor Steel Seattle, Inc.; Nucor Steel Birmingham, Inc.; and Nucor Steel Memphis, Inc.

The acquisitions accelerated. In 2006-07, Harris Steel Group was purchased for $1.07 billion, providing entry into the rebar fabrication market. The David J. Joseph Company, one of the nation's largest scrap processors and brokers, was acquired for $1.44 billion, providing Nucor further control of its raw material supply—scrap steel makes up 75 to 90 percent of the material used to recycle steel. In 2014, Nucor purchased Gallatin Steel for $770 million, increasing flat-rolled capacity by 16 percent.

But DiMicco didn't abandon Nucor's innovation DNA. The company continued pushing technological boundaries. Castrip technology went online in Crawfordsville, Indiana—a process that casts molten steel directly into sheet steel at or near its final thickness, consuming about 95 percent less energy and emitting less than one-tenth the greenhouse gases of traditional processes. In 2002, the company pioneered micro mill technology, producing sheet steel from liquid in a single step. Most impressively, in 2023, Nucor entered into a groundbreaking carbon capture agreement with ExxonMobil to capture up to 800,000 metric tons of CO2 per year from their direct reduced iron plant in Louisiana. This transformative project represents a key part of Nucor's decarbonization strategy and will result in some of the lowest embodied carbon DRI in North America. With its recycling-based production method, Nucor's steel mills generate roughly two-thirds less carbon dioxide than traditional blast furnace steelmaking plants, even when accounting for Scope 3 emissions.

The modern era also saw leadership transitions that maintained the culture. John J. Ferriola became President and CEO in 2013, succeeding DiMicco. Then Leon J. Topalian assumed the role of President and CEO in 2019, succeeding Ferriola. Each transition maintained the core values while pushing the company forward. As current CEO Topalian has said, "The U.S. economy is still on the front end of several steel-intensive megatrends and as America's largest and most diversified steel producer, Nucor is well positioned to supply those needs."

The modern Nucor has expanded beyond pure steel production into steel-adjacent businesses—C.H.I. Overhead Doors, Summit Utility Structures, Sovereign Steel Manufacturing, Elite Storage Solutions, Hannibal Industries, CENTRIA, and Metl-Span have all joined the Nucor family. The company that once made only steel joists now produces everything from overhead doors to insulated metal panels.

Yet through all this growth and change, the fundamental culture remains intact. The pay-for-performance system continues. The no-layoff practice endures. The lean corporate structure persists. Nucor has proven that revolutionary cultures can survive their revolutionaries—if they're built on principles rather than personalities.

VIII. The Numbers: Financial Performance & Strategy

The financial story of Nucor reads like a masterclass in disciplined capital allocation and counter-cyclical thinking. Through the Iverson era and beyond, the company has demonstrated that superior returns don't require financial engineering—they require operational excellence and patient capital deployment.

Looking at recent performance, 2023 represented a peak year with net earnings of $4.91 billion and EBITDA of $7.41 billion. Diluted EPS reached $18.00 for the full year. These numbers came during a period of strong steel demand and pricing power. But as any experienced steel investor knows, the cycle always turns.

Indeed, 2024 showed the cyclical nature of the business. Fourth quarter and full year 2024 diluted EPS of $1.22 and $8.46, respectively. Fourth quarter and full year 2024 net sales of $7.08 billion and $30.73 billion, respectively. Fourth quarter and full year 2024 net earnings before noncontrolling interests of $345 million and $2.32 billion, respectively; EBITDA of $751 million and $4.37 billion, respectively. The full-year comparison is stark: Nucor's consolidated net sales decreased 5% to $7.08 billion in the fourth quarter of 2024 compared with $7.44 billion in the third quarter of 2024 and decreased 8% compared with $7.71 billion in the fourth quarter of 2023.

But here's what separates Nucor from typical cyclical companies: the consistency of capital returns to shareholders. The company has paid 207 consecutive quarterly dividends and increased its regular dividend for 52 consecutive years. Think about what that means—through the 2008 financial crisis, through COVID-19, through multiple steel industry downturns, Nucor has never missed a dividend and has increased it every single year for over half a century.

The capital allocation strategy reflects a deep understanding of the cyclical nature of steel. In good times, Nucor generates massive cash flows. Rather than empire-building or diversifying into unrelated businesses, the company follows a disciplined playbook: invest in high-return projects within their circle of competence, maintain a fortress balance sheet, and return excess capital to shareholders.

The balance sheet strength is remarkable for a cyclical commodity business. Nucor's consolidated net sales decreased 5% to $7.08 billion in the fourth quarter of 2024, yet the company maintains the strongest credit ratings in the North American steel sector (A-/A-/Baa1). At the end of 2024, the company held $4.14 billion in cash and equivalents—a war chest that allows opportunistic investments during downturns when competitors are struggling.

The 2024 capital expenditure plan of $3.5 billion demonstrates continued investment in the business even during softer market conditions. This counter-cyclical investment approach—building and modernizing when construction costs are lower and competitors are retrenching—has been a hallmark of Nucor's strategy for decades.

Operating metrics tell the efficiency story. Operating rates of 76% in 2024 versus 78% in 2023 show some softness, but these rates remain well above industry averages. The company's ability to flex production while maintaining profitability comes from the variable cost structure—when demand falls, production can be reduced without the massive fixed cost burden that crushes traditional integrated mills.

Share repurchases provide another lever for value creation. The company opportunistically buys back stock when prices are depressed, effectively increasing the ownership stake of remaining shareholders when the business is undervalued. This isn't financial engineering for the sake of hitting quarterly EPS targets—it's patient, value-accretive capital allocation.

What's remarkable is how consistent the financial strategy has been across different management teams and market cycles. No transformative mergers, no attempts to financialize the business, no complex derivatives or hedging strategies. Just a relentless focus on operational excellence, strategic growth investments, and returning capital to shareholders.

The numbers validate the strategy. Over long periods, Nucor has dramatically outperformed both the broader market and steel industry peers. From 2000 through 2012 under DiMicco's leadership alone, total shareholder returns grew 720%—almost 4 times the S&P Steel Group Index and 28 times the S&P 500's return. This isn't achieved through financial wizardry but through the blocking and tackling of running an efficient, innovative steel company.

For investors, the key insight is that Nucor has created a business model that generates significant free cash flow through the cycle. Even in down years, the variable cost structure and operational efficiency allow for positive cash generation. In up years, the cash generation is enormous. This cash flow reliability, rare in commodity businesses, enables the consistent dividend growth and opportunistic capital deployment that have created so much shareholder value over decades.

IX. Playbook: Business & Investing Lessons

The Nucor story offers a masterclass in business strategy that extends far beyond steel. These aren't abstract management theories—they're battle-tested principles that transformed a dying conglomerate into an industry titan.

Culture beats strategy, every time. Nucor didn't out-strategize U.S. Steel or Bethlehem—they out-cultured them. The egalitarian, performance-based system created thousands of owner-operators who made better daily decisions than any strategic planning department could dictate. When electricians drive hours on their own initiative to fix a plant problem, you've won the culture game. Strategy is what you plan; culture is what happens when no one's watching.

Decentralization and trust as competitive advantages. In an era of big data and centralized control, Nucor proves the opposite can work. Plant managers have real autonomy. Yes, they might develop the same software six times across different plants, but the speed and ownership benefits overwhelm the inefficiency costs. When people own decisions, they own outcomes. When headquarters makes all decisions, the field owns nothing.

The courage to bet the company on new technology. Nucor bet everything—literally all assets—on the first mini-mill. They bet big again on thin-slab casting when everyone said it wouldn't work. But these weren't reckless gambles. They were calculated risks based on deep technical knowledge and conviction. In commodity businesses, technical leadership matters more than most realize. Being 10% more efficient than competitors in a commodity business is like having a permanent tailwind.

Building vs. buying: the discipline of organic growth. While Nucor has made acquisitions, particularly in the modern era, the core business was built plant by plant. Each new facility incorporated lessons from the last. This iterative improvement, compounded over decades, created capabilities that couldn't be bought. When you build, you learn. When you buy, you inherit someone else's problems.

Long-term thinking in a cyclical industry. Steel is viciously cyclical. Most companies panic in downturns, laying off workers and slashing investment. Nucor does the opposite—keeping workers, taking pay cuts from the top, and investing when capital costs are low. This counter-cyclical approach requires a long-term mindset and a balance sheet to support it. In cyclical industries, the spoils go to those who can think in decades, not quarters.

The power of aligned incentives. When production workers can earn 150-200% bonuses but lose them for being late, behavior changes. When executives take the biggest pay cuts in downturns, trust builds. Nucor doesn't just talk about alignment—they live it. Every level of the organization has skin in the game. Incentives aren't everything, but misaligned incentives will destroy everything.

Why being the low-cost producer matters in commodities. In commodity businesses, you can't differentiate on product—steel is steel. You win by being the lowest-cost producer. Nucor's mini-mills, located in rural areas with non-union labor and innovative technology, achieved structural cost advantages. In commodities, costs are destiny. The low-cost producer sets the price floor and captures the profits.

Managing through cycles without layoffs. The no-layoff practice seems impossible in a cyclical industry, yet Nucor has maintained it for decades. How? Variable compensation, operational flexibility, and shared sacrifice. When workers know they won't be laid off, they innovate to save costs. When they share in profits, they work to generate them. Security breeds loyalty; loyalty breeds performance.

The compound effect of continuous improvement. Nucor didn't revolutionize steel overnight. They improved 1% here, 2% there, year after year, decade after decade. Mini-mills got more efficient. Quality improved. New products were added. Costs declined. None of these improvements alone transformed the industry, but compounded over 50 years, they destroyed the competition.

For investors, these lessons translate into a framework for identifying exceptional businesses: Look for companies with strong cultures that translate into operational advantages. Find businesses where incentives align throughout the organization. Identify companies with the balance sheet strength and temperament to invest counter-cyclically. Seek out low-cost producers in commodity industries. Value companies that can maintain pricing discipline and return capital to shareholders rather than empire-build.

The Nucor playbook isn't about financial engineering or strategic brilliance. It's about the daily blocking and tackling of running a great business: treating people fairly, paying for performance, maintaining cost discipline, investing in technology, and thinking long-term. These principles seem simple, even obvious. But as Nucor has proven, common sense isn't common practice. And in that gap between knowing and doing lies the opportunity for extraordinary value creation.

X. Analysis & Bear vs. Bull Case

Bull Case: The Structural Winner

Nucor sits at the intersection of multiple powerful tailwinds that could drive outperformance for years. Start with the lowest cost producer advantage—in commodity businesses, this is the ultimate moat. Nucor's mini-mills using recycled scrap and electric arc furnaces have structural cost advantages over traditional blast furnace operations. As environmental regulations tighten globally, this advantage only widens.

The recycling angle is underappreciated. In 2024, the company produced and sold approximately 18.5 million tons of steel and recycled 18 million tons of scrap. Nucor isn't just North America's largest steel producer—it's the continent's largest recycler of any material. In an era of ESG mandates and carbon consciousness, Nucor's circular economy model looks prescient. The circular nature of remelting recycled scrap in electric arc furnaces means that Nucor's steel mills generate roughly two-thirds less than the carbon dioxide of extractive blast furnace steelmaking plants, even when accounting for Scope 3 emissions, which include all upstream and downstream emissions in the supply chain.

U.S. infrastructure spending and reshoring provide massive tailwinds. The Infrastructure Investment and Jobs Act, the CHIPS Act, and the Inflation Reduction Act collectively represent trillions in steel-intensive spending over the coming decade. Data centers, semiconductor fabs, battery plants, and renewable energy infrastructure all require massive amounts of steel. Nucor, as the largest and most diversified domestic producer, captures a disproportionate share of this demand.

The balance sheet provides optionality that competitors lack. With $4.14 billion in cash and the strongest credit ratings in North American steel, Nucor can act when others can't. They can invest counter-cyclically, acquire distressed assets, or simply return capital to shareholders. This financial flexibility in a cyclical industry is worth a significant premium.

The culture and execution track record deserve a multiple premium. For over 50 years, Nucor has consistently out-executed competitors. They've successfully navigated technology transitions, market cycles, and competitive threats. Management has skin in the game, incentives are aligned, and the company has demonstrated an ability to adapt and evolve while maintaining core principles. In a commodity business, execution alpha is real and sustainable.

Bear Case: The Commodity Trap

But let's not kid ourselves—this is still a commodity business with no real pricing power. When China dumps steel, when demand softens, when scrap prices spike, Nucor suffers along with everyone else. Average sales price per ton in the fourth quarter of 2024 decreased 3% compared with the third quarter of 2024 and decreased 10% compared with the fourth quarter of 2023. The company can't pass through costs or maintain prices in weak markets.

Chinese overcapacity remains the 800-pound gorilla. China produces over half the world's steel and exports its surplus globally, depressing prices everywhere. While tariffs provide some protection, they're political tools subject to change. A shift in trade policy could expose Nucor to devastating price competition from subsidized foreign producers.

The cyclical headwinds are mounting. Nucor's consolidated net sales decreased 5% to $7.08 billion in the fourth quarter of 2024 compared with $7.44 billion in the third quarter of 2024 and decreased 8% compared with $7.71 billion in the fourth quarter of 2023. Average sales price per ton in the fourth quarter of 2024 decreased 3% compared with the third quarter of 2024 and decreased 10% compared with the fourth quarter of 2023. Approximately 6,058,000 tons were shipped to outside customers in the fourth quarter of 2024, a 2% decrease from the third quarter of 2024 and a 2% increase from the fourth quarter of 2023. Operating rates declining from 78% to 76% suggest weakening demand.

Economic uncertainty clouds the outlook. Steel demand correlates highly with industrial production, construction activity, and GDP growth. If the economy enters recession, steel demand could collapse. The automotive industry's struggles, commercial real estate weakness, and potential infrastructure spending delays all pose risks.

Size may be becoming a disadvantage. Nucor is no longer the nimble insurgent disrupting sleepy giants. They're now the giant, with all the challenges that entails. Maintaining culture at scale is hard. Finding growth opportunities that move the needle is harder. The law of large numbers suggests future growth rates must slow.

Environmental regulations could backfire. While Nucor is cleaner than blast furnace producers, steel remains carbon-intensive. Future regulations could impose costs that even efficient producers struggle to absorb. The push toward alternative materials—aluminum, carbon fiber, engineered wood—threatens long-term steel demand.

The Verdict

The bull case rests on Nucor's proven ability to generate returns through the cycle via operational excellence, the bear case on the immutable realities of commodity economics. Both are right. Nucor is simultaneously the best-positioned steel company in North America and still subject to forces beyond its control.

For long-term investors, the question isn't whether Nucor will face challenges—it will. The question is whether the company's advantages—cultural, operational, financial—allow it to emerge from challenges stronger while competitors falter. History suggests yes, but history doesn't guarantee future results.

The current valuation reflects this tension. The market sees a cyclical business in a downtrend and prices it accordingly. But that might be missing the forest for the trees. The strategic position, the balance sheet strength, the cultural advantages, and the long-term tailwinds from infrastructure and reshoring could make current prices attractive for patient capital.

XI. Epilogue & "What Would Iverson Do?"

Ken Iverson passed away in 2002, but his ghost haunts every corner of Nucor's operations. Not in a limiting way—trapped by the past—but as a north star for decision-making. When facing tough choices, Nucor executives still ask themselves: What would Ken do?

The answer usually comes down to first principles. Trust people. Pay for performance. Keep it simple. Think long-term. Don't lay people off. Invest in technology. Stay humble. These principles seem almost quaint in our era of financial engineering and quarterly earnings management. Yet they've created more value than a thousand McKinsey consulting engagements.

The post-Iverson era has tested whether the culture can survive its creator. So far, the answer is yes—but with evolving challenges. Current CEO Leon Topalian faces a different world than Iverson did. China's state-backed steel industry, climate change regulations, and technological disruption from alternative materials all present novel threats. The playbook must evolve while maintaining core principles.

The steel-intensive megatrends Topalian references are real and massive. America needs to rebuild its infrastructure—bridges, roads, electrical grid, water systems. The reshoring of manufacturing requires new factories. The energy transition demands massive steel inputs for wind turbines, solar installations, and grid storage. Electric vehicles require new production facilities and charging infrastructure. Data centers for AI and cloud computing consume enormous amounts of structural steel.

But capturing these opportunities requires continued evolution. Nucor's investments in carbon capture, renewable energy, and small modular nuclear reactors show a company not content to rest on past success. The expansion into downstream products and steel-adjacent businesses demonstrates strategic flexibility while maintaining focus on core competencies.

For founders and leaders, Nucor offers profound lessons on building enduring cultures. Start with trust and radical transparency. Create systems where everyone has skin in the game. Resist bureaucracy and complexity at every turn. Maintain cost discipline especially in good times. Think in decades, not quarters. And perhaps most importantly, recognize that in commodity businesses, culture and execution can be sustainable competitive advantages.

The mini-mill revolution that started in a South Carolina field in 1969 has fundamentally reshaped global steel production. The David that was Nucor didn't just defeat Goliath—it became Goliath, but managed to maintain David's hunger and agility. That's the real miracle.

What would Iverson make of today's Nucor? He'd probably be proud of the consistent dividend growth, the maintained no-layoff practice, and the continued technological leadership. He might worry about creeping bureaucracy or the risk of complacency. But mostly, he'd likely be amazed that the culture he built has not just survived but thrived through multiple generations of leadership.

The story of Nucor isn't really about steel. It's about proving that in an old-economy, commodity business, with no proprietary technology or unique assets, a company can create extraordinary value through culture, execution, and patient capital allocation. It's about demonstrating that treating workers as partners rather than costs can drive superior returns. It's about showing that American manufacturing can compete and win against anyone in the world.

As investors evaluate Nucor today, they're not just betting on steel prices or infrastructure spending. They're betting on whether a 60-year-old culture of ownership, innovation, and execution can continue to create value in an uncertain world. They're betting on whether the principles that Ken Iverson instilled—radical simplicity, aligned incentives, technological courage—remain relevant in the 21st century.

The evidence suggests they do. In a world of increasing complexity, simplicity has value. In an era of misaligned incentives, true partnership matters. In industries facing disruption, technological leadership compounds. Nucor has proven that common sense, uncommonly applied, can create uncommon results.

The mini-mill revolution may be complete, but the Nucor revolution continues. What started as a desperate attempt to save a failing conglomerate has become a blueprint for building enduring industrial companies. The lesson for all of us—investors, operators, entrepreneurs—is clear: in business, as in life, culture eats strategy for breakfast, lunch, and dinner.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube