Annaly Capital Management: America's Mortgage Money Machine

I. Introduction & Episode Roadmap

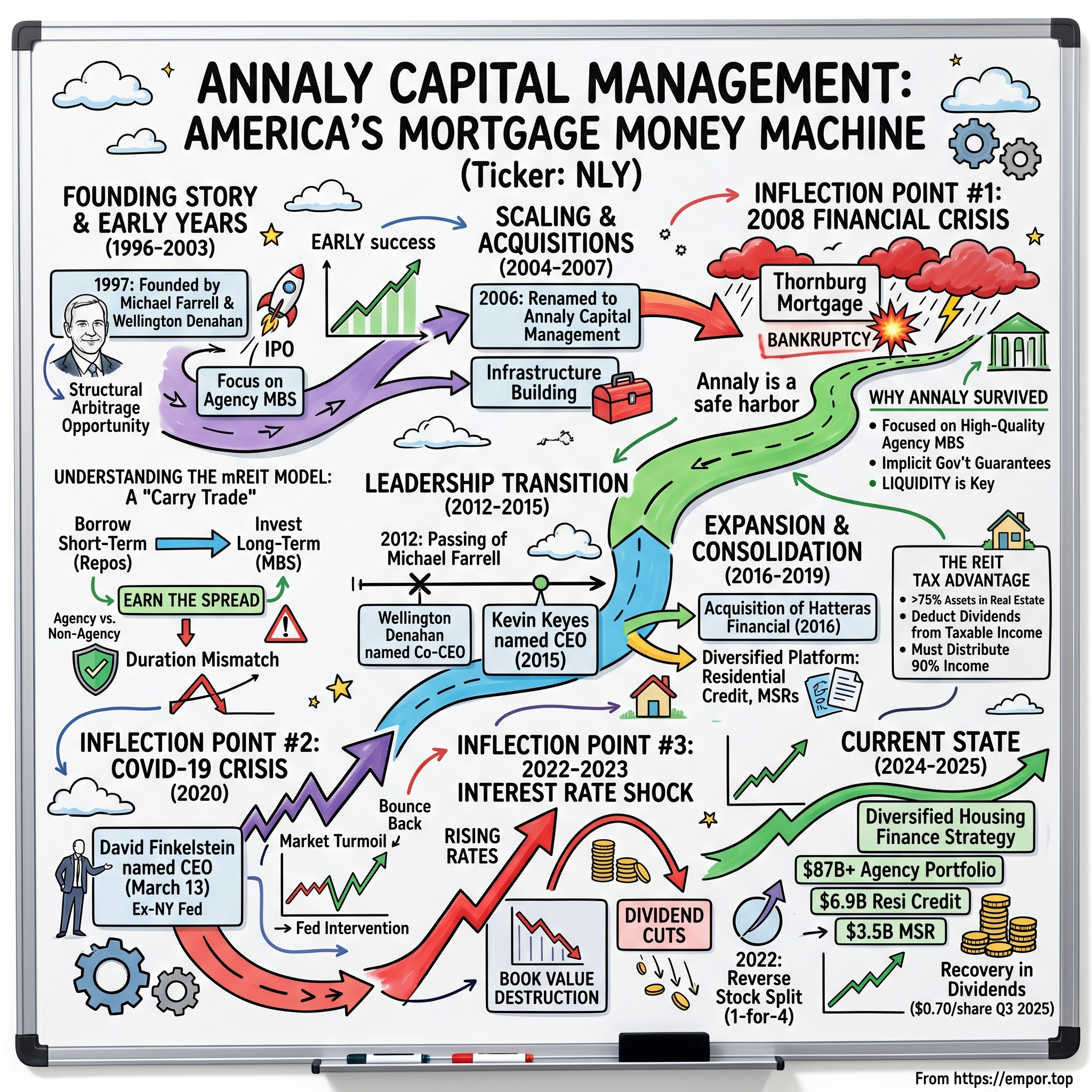

Picture this: a company with roughly 200 employees managing $100 billion in assets by essentially arbitraging the U.S. government's implicit guarantee of the American housing market. No factories, no inventory, no physical products to ship—just a sophisticated balance sheet machine that borrows short-term and invests long-term, collecting the spread in between. Welcome to Annaly Capital Management, the largest mortgage REIT in America and perhaps the purest financial engineering play ever to trade on the New York Stock Exchange.

Annaly Capital Management, Inc. is one of the largest mortgage real estate investment trusts. It is organized in Maryland with its principal office in New York City. The company borrows money, primarily via short-term repurchase agreements, and reinvests the proceeds in asset-backed securities. As of December 31, 2023, 88% of the company's assets were mortgage-backed securities issued by either Fannie Mae or Freddie Mac.

The story of Annaly is, in many ways, the story of modern American housing finance. Founded in 1996 by two Wall Street veterans who spotted a structural arbitrage opportunity, the company has since become one of the largest buyers of mortgage debt in the world—channeling private capital into the home loans that finance the American Dream. The company is named after Annaly, Ireland, which was ruled by the ancestors of the company's founder. In a sector littered with spectacular failures, Annaly has survived—and at times thrived—through the 2008 financial crisis, the COVID market crash, and the 2022 interest rate shock that devastated its peers.

But survival has come at a cost. This is also the story of a company that has cut its dividend 15 times since 2008, seen its book value erode by more than half over a decade, and executed a reverse stock split that many viewed as a tacit admission of long-term shareholder value destruction. As of September 30, 2025, the company manages a total portfolio of approximately $98 billion, including $87.3 billion in agency mortgage-backed securities (64% of capital allocation), $6.9 billion in residential credit (17%), and $3.5 billion in mortgage servicing rights (19%), supported by $15 billion in permanent capital from stockholders' equity.

Understanding Annaly means understanding the elegant-yet-fragile business model of mortgage REITs, the structural quirks of REIT tax law that enable double-digit yields, and why the company has managed to survive crises that destroyed competitors like Thornburg Mortgage. It also means confronting uncomfortable questions about whether this business model creates genuine value for shareholders over the long term, or whether it simply offers high current income at the expense of capital destruction.

II. Understanding the mREIT Business Model

The Core Mechanism: A "Carry Trade" on Steroids

To understand Annaly, you first need to understand what a mortgage REIT actually does. Think of it as a glorified carry trade—but instead of a hedge fund running this strategy with a few billion dollars and questionable leverage, it's a publicly traded company deploying tens of billions in what amounts to a massive bet on the spread between borrowing costs and mortgage yields.

Mortgage REITs (mREITs) provide financing for income-producing real estate by purchasing or originating mortgages and mortgage-backed securities (MBS) and earning income from the interest on these investments. mREITs help provide essential liquidity for the real estate market.

Here's how it works in practice: The primary debt source for mortgage REITs is repurchase agreements, which are also known as repos. Repurchase agreements are short-term collateralized loans. In a repo agreement, the mortgage-REIT sells its MBS holdings to a lender for cash and then promises to buy back the MBS later at a higher price. The MBS buyer earns interest, which is effectively the difference between the prices that the MBS was sold for and bought back. Essentially, the mortgage REIT borrows money to buy MBS and in turn, those securities serve as collateral for additional debt financing.

A Mortgage REIT might use $1 million of equity capital and $4 million of leverage to purchase $5 million of MBS. If the MBS portfolio earns a 5% yield and the leverage has a cost of 3% then the Mortgage REIT will generate a 2% net interest margin. Leaving aside other expenses, this example would result in equity investors generating a 13% return on equity with 4x leverage. In the case of Mortgage REITs, the Return on Equity (ROE) is usually a close proxy for the ultimate dividend yield.

This math looks elegant on paper. But here's the catch: the mortgage REIT borrows short-term (often with maturities measured in days or weeks) while investing in assets with much longer durations (30-year mortgages). This duration mismatch is the source of both the profits and the peril.

Agency vs. Non-Agency MBS: The Safety Blanket

Agency loans are created and guaranteed by one of three government-sponsored agencies: Government National Mortgage Association ("Ginnie Mae"), Federal National Mortgage ("Fannie Mae"), and Federal Home Loan Mortgage Corp. ("Freddie Mac"). Investors generally treat these agency loans as obligations of the U.S. government and so they are relatively low-yielding and very liquid. Non-agency loans are issued by financial institutions and tend to trade at higher yields since they are less liquid and carry a risk of default.

Annaly's strategic choice to focus primarily on agency MBS has been perhaps the single most important decision in its nearly three-decade history. The amount of leverage and the resulting ROE the Mortgage REIT generates is largely a function of the type of securities that are being leveraged. Agency MBS is the gold standard and the lower yields these securities distribute require higher leverage to generate an attractive dividend yield. On the other end of the spectrum, CMBS generate higher yields but are usually purchased with less leverage to account for the increased credit risk.

By focusing on agency securities, Annaly essentially outsources credit risk to the U.S. government. If homeowners default, Fannie Mae or Freddie Mac absorb the losses—Annaly still gets paid. This sounds like a free lunch, but it isn't. Agency MBS yields less than non-agency securities precisely because the credit risk has been removed. To generate returns that justify the mREIT structure, Annaly must use substantial leverage.

The REIT Tax Advantage: Paying Out (Almost) Everything

The REIT must have more than 75% of its assets invested in real estate (including mortgages backed by real estate), government securities, or cash. 75% or more of the REIT's gross income must be derived from real estate activities. At least 90% of the REIT's taxable income must be distributed to shareholders as dividends. If a U.S. REIT meets the requirements, it can deduct its dividend payments from its taxable income, which means REITs pay little if any income tax.

IRS guidelines for mREITs require them to distribute 90% of net income to shareholders via dividend payments, which explains the high dividend yields for most mREITs. This structural requirement is why Annaly has historically offered yields in the double digits—the company literally cannot retain most of its earnings. What looks like generosity is actually a legal mandate.

The Levers mREITs Can Pull

Despite the apparent simplicity of "borrow short, lend long," running a mortgage REIT requires constant calibration of several key variables:

Managing the effects of changes in short- and long-term interest rates is an essential element of mREITs' business operations. Changes in interest rates can affect the net interest margin, which is mREITs' fundamental source of earnings, but also may affect the value of their mortgage assets, which affects corporate net worth. mREITs typically manage and mitigate risk associated with their short-term borrowings through conventional, widely-used hedging strategies, including interest rate swaps, swaptions, interest rate collars, caps or floors and other financial futures contracts.

Interest Rate Risk/Duration: How long are the mortgages they're buying? Longer-duration mortgages typically offer higher yields but also carry more interest rate risk. When rates rise rapidly, long-duration assets get crushed.

Leverage: As of December 31, 2019, the company had a GAAP leverage ratio of 6.8:1. As of December 31, 2023, the weighted average days to maturity of its repurchase agreements was 44 days. Higher leverage amplifies returns but also magnifies losses.

Below is a summary of some of the other additional risks that can affect the performance of mortgages or mortgage REITs: Prepayment Risk: Falling interest rates or greater interest rate volatility can accelerate the pace of mortgage refinancing. This can change the duration characteristics of a portfolio of mortgages as well as cause reinvestment risk, where mREITs must reinvest repaid principal at a lower rate than before. Extension Risk: the flip side of prepayment risk occurs if interest rates rise and homeowners remain in their existing mortgages longer than anticipated. This can have a negative effect on mortgage values because homeowners lock in their low interest rate for longer. Hedging Risk: mREITs often use hedging instruments in an effort to control for various changes in interest rates, credit risks, and macro scenarios. The value and accuracy of these bets can have a material effect on bottom line profits.

For long-term investors, the key insight is that mREITs like Annaly operate in a world of constrained optimization. They cannot simultaneously maximize yield, minimize risk, and preserve book value. Every decision involves tradeoffs, and those tradeoffs ultimately determine shareholder returns.

III. Founding Story & Early Years (1996-2003)

The Founders: Wall Street Veterans with a Vision

The story of Annaly begins in the early 1990s, when Michael A.J. Farrell was running fixed income at Wertheim Schroder & Co. Born in Brooklyn, N.Y., as one of seven siblings, his parents were Irish immigrants. Farrell graduated from high school at the age of 16, but never completed college. He got his start in the financial industry after getting a clerical job at brokerage firm E.F. Hutton in 1971 before becoming a trader for the company.

Farrell told the publication he wanted to be a rock star after giving up on becoming an artist. Instead he ended up trading bonds, specializing in mortgages. In 1991, while head of fixed income at Wertheim Schroder & Co., where he also hired Cantor Fitzgerald's Matthews, he met Denahan-Norris, with whom he founded Annaly six years later. Farrell had concluded that REITs and mortgage bonds were a "perfect marriage between asset class and vehicle structure," in part because they can be "buy-and-hold" investors.

Annaly Capital Management was founded in 1997 by Michael A.J. Farrell (1951-2012) and Wellington Denahan. Mike Farrell spent 26 years working for investment banks including E.F. Hutton & Co., Morgan Stanley, and Merrill Lynch.

What Farrell saw was a structural opportunity. REIT shareholders, unlike hedge fund investors, cannot simply withdraw their capital when markets get choppy. Unlike hedge funds or many mutual funds, REIT shareholders can't withdraw money from the firms. Instead they buy and sell shares in the companies. This permanent capital structure meant a mortgage REIT could ride out short-term market dislocations that would force hedge funds to liquidate at the worst possible moments.

The IPO and Initial Strategy

Annaly Capital Management was established on November 25, 1996, by Michael A. J. Farrell and Wellington J. Denahan as a mortgage real estate investment trust (mREIT) focused on investing in agency mortgage-backed securities (MBS). The founders, drawing from their prior experience in fixed-income advisory through Fixed Income Discount Advisory Company (FIDAC), aimed to create a vehicle for generating net income through leveraged investments in federally guaranteed residential mortgage securities issued or backed by government-sponsored enterprises like Fannie Mae and Freddie Mac.

This strategy targeted the spread between the yields on these low-risk assets and the cost of borrowing, providing a stable income stream in an era of recovering housing markets and declining interest rates following the early 1990s recession.

The timing was propitious. The late 1990s saw a confluence of factors favorable to the mREIT business model: declining interest rates, a recovering housing market, and investor appetite for yield in an era when dot-com stocks dominated the headlines but paid no dividends.

Following its initial public offering in 1997, Annaly Capital Management experienced significant portfolio expansion throughout the 2000s, leveraging the housing market boom to grow its investments primarily in agency mortgage-backed securities (MBS). The company's assets under management increased substantially during this period, benefiting from favorable interest rate environments and rising demand for residential financing. By the mid-2000s, Annaly had renamed itself from Annaly Mortgage Management to Annaly Capital Management in 2006, reflecting its broadening scope while maintaining a core focus on agency assets for stability.

Farrell co-founded Annaly in 1997, and today it is the largest mortgage REIT listed on the New York Stock Exchange. The company's early years were characterized by steady growth and consistent dividend payments—a pattern that would establish Annaly's reputation as a reliable income vehicle.

Early Dividend Track Record

Annaly has returned more than 600 percent to shareholders since its initial public offering, outpacing the 94 percent gain for the Standard & Poor's 500 index. Shareholders almost doubled their money in the past five years as Farrell and Denahan-Norris, 48, navigated the financial crisis and then forecast how Federal Reserve efforts to boost housing and the economy would impact bond markets.

The company's early success established a template that would define its identity: high yields, agency-focused investing, and careful navigation of interest rate cycles. But the real test would come in 2008, when the global financial system nearly collapsed—and when Annaly's competitors discovered just how fragile the mREIT business model could be.

IV. Scaling & Strategic Acquisitions (2004-2007)

Building the Infrastructure

As the 2000s housing boom accelerated, Annaly moved to expand its capabilities beyond pure-play agency MBS investing. In 2013, the company acquired CreXus Investment for $996 million. But before that milestone, the company was already building out its investment advisory capabilities.

By the mid-2000s, Annaly was navigating an increasingly frothy housing market. Home prices were rising at double-digit rates, mortgage origination volumes were at all-time highs, and a proliferation of exotic mortgage products—interest-only loans, negative amortization mortgages, "NINJA" loans requiring no income, no job, and no assets—was fueling unprecedented demand for mortgage-backed securities.

Throughout this period, Annaly maintained its disciplined focus on agency securities. While competitors chased higher yields in the non-agency subprime market, Annaly stuck to the relative safety of government-guaranteed mortgages. This decision would prove prescient.

The Housing Boom Context

The mid-2000s housing bubble represented both opportunity and danger for mortgage REITs. On one hand, abundant mortgage supply and strong MBS demand created favorable investing conditions. On the other hand, the leverage buildup across the financial system was creating systemic risks that few fully appreciated.

Annaly's leadership appeared to recognize that the party couldn't last forever. Rather than reaching for yield by venturing into subprime securities, the company maintained its agency focus—a decision that would prove crucial when the music stopped.

The name change in 2006 from Annaly Mortgage Management to Annaly Capital Management signaled ambitions beyond pure mortgage investing, but the core strategy remained constant: agency MBS, levered returns, and disciplined risk management.

V. Key Inflection Point #1: The 2008 Financial Crisis

The Storm That Destroyed Competitors

Thornburg Mortgage was a United States real estate investment trust (REIT) that originated, acquired and managed mortgages, with a specific focus on jumbo and super jumbo adjustable rate mortgages. The company experienced financial difficulties related to the subprime mortgage crisis in 2007 and filed for bankruptcy on April 1, 2009. It was founded in 1993 and prior to its failure it was a publicly traded corporation headquartered in Santa Fe, New Mexico. It got caught up in the 2008 financial crisis when it moved from a passive REIT to wholesale origination of mortgages in 2006.

Thornburg Mortgage declared bankruptcy after struggling to find investors to fund its core business: providing expensive mortgage loans to well-credited buyers. With home sales down dramatically and defaults on the rise, the value of the company's mortgages fell; after a $1.35 billion bailout from private investors failed to stop the collapse, the company was forced into Chapter 11 on May 1, 2009.

At its peak, Thornburg was the second largest mortgage lender in the country behind Countrywide, but the company became embroiled in controversy when it filed for bankruptcy in May 2009.

The Thornburg failure illustrated the mortal dangers facing mortgage REITs during periods of market stress. Thornburg Mortgage indicated on March 19 that it had reached an agreement with five of its creditors which stopped additional margin calls for one year but included several conditions, the most urgent of which was to raise US$948 million within seven business days. The five creditors were identified as Bear Stearns, Citigroup, Credit Suisse, Royal Bank of Scotland and UBS.

Why Annaly Survived—and Thrived

Co-founder and CEO Michael A. J. Farrell passed away in October 2012, leading to leadership transitions that included Wellington J. Denahan serving as co-CEO. During the 2008 financial crisis, Annaly navigated the turmoil by concentrating on high-quality agency securities, which provided implicit government backing and liquidity.

Shareholders almost doubled their money in the past five years as Farrell and Denahan-Norris, 48, navigated the financial crisis and then forecast how Federal Reserve efforts to boost housing and the economy would impact bond markets.

The contrast with Thornburg could not have been starker. While Thornburg was drowning in margin calls, Annaly's agency-focused portfolio actually benefited from the government's intervention to support the housing market. When the Federal Reserve began purchasing MBS to stabilize the financial system, it was effectively buying what Annaly already owned.

The Agency MBS Advantage

The key to Annaly's survival was liquidity. Agency MBS securities are among the most liquid fixed-income instruments in the world, trading in markets with daily volumes measured in hundreds of billions of dollars. When Annaly needed to raise cash or meet margin calls, it could sell securities quickly without accepting fire-sale prices.

Non-agency securities, by contrast, became virtually illiquid during the crisis. Holders couldn't sell at any price, couldn't meet margin calls, and ultimately faced forced liquidation or bankruptcy.

Post-Crisis Tailwinds: Fed Intervention

From 1913 until 2008, the Fed owned precisely zero mortgage-backed securities. While the Fed's monetary policy decisions still impacted conditions in the housing and mortgage markets, they did so indirectly through the influence the Fed's purchases and sales of Treasury securities had on market interest rates. In a radical "temporary" policy response to the 2008 financial crisis, the Fed began intervening directly in the mortgage market. Through a series of MBS purchases, the Fed's MBS portfolio ballooned from $0 to $1.77 trillion by August 2017.

This unprecedented Fed intervention created a golden era for mortgage REITs. With the central bank hoovering up agency MBS, spreads tightened, prices rose, and Annaly's portfolio appreciated in value while continuing to generate attractive yields. It was as close to a free lunch as exists in financial markets—courtesy of U.S. monetary policy.

VI. Leadership Transition & The Farrell Era Ends (2012-2015)

The Passing of a Founder

Wellington Denahan-Norris, who co-founded Annaly with Farrell, was named co-CEO earlier this year following Farrell's cancer diagnosis. Denahan-Norris is also the company's vice chairman and chief investment officer. "He was a fantastic leader and friend and will be greatly missed."

Michael A.J. Farrell, who built Annaly Capital Management Inc. (NLY) into the world's largest mortgage real estate investment trust, has died after being diagnosed with cancer earlier this year. He was 61. His death was confirmed yesterday in a statement by the New York-based company, which didn't provide additional details. Farrell, who graduated high school at 16 with plans to become a commercial artist, instead turned to Wall Street, beginning at E.F. Hutton & Co. in 1971. After stints at Morgan Stanley and Merrill Lynch & Co., he started Annaly in 1997 and increased assets to about $128.3 billion at the end of June, turning the firm into one of the largest buyers of home loan debt backed by the U.S.

Farrell stood out for his colorful conference calls and shareholder letters that discussed broader themes through historical allusions and literature such as Christopher Marlowe's "Doctor Faustus" and the 1970 book "Future Shock" by Alvin Toffler.

Farrell was not only synonymous with Annaly, he was seen as a pioneer in the field of mortgage finance and an icon of the Mortgage REIT sector. "Mike was larger than life, and it's difficult to step into those shoes," Denahan says.

Diversification Push and Leadership Changes

Following Farrell's passing, Wellington Denahan assumed leadership and continued the company's diversification strategy. In 2013, the company acquired CreXus Investment for $996 million. Effective September 30, 2015, Kevin Keyes was named CEO of the company.

The CreXus acquisition represented Annaly's move into commercial real estate finance, marking a significant expansion beyond the residential agency MBS that had defined the company since inception. This diversification reflected management's recognition that relying solely on agency MBS spreads left the company vulnerable to Fed policy changes and interest rate volatility.

The first four months of 2014 showed why. The Mortgage REIT thundered back with a total return of nearly 20 percent through the end of April.

VII. Expansion & Consolidation (2016-2019)

Strategic Acquisitions

The Hatteras Financial acquisition in 2016 represented a transformational deal for Annaly. In 2016, the company acquired Hatteras Financial for $1.5 billion in cash and stock. In 2017, the company sold its Pingora servicing subsidiary.

Hatteras commenced its operations in 2007 as an agency REIT and performed well even during the turbulent times of recession. Now, with Annaly acquiring Hatteras, shareholders of the latter are likely to benefit from a diversified portfolio base of the former. Further, the operating scale, capital alternatives and liquidity of the larger merged entity are expected to have a positive impact on investor sentiment.

Expands and further diversifies Annaly's investment portfolio: Hatteras' portfolio, which consists of agency residential mortgage backed securities, residential whole loans and mortgage servicing rights is complementary to Annaly's existing businesses.

"This strategic transaction represents a unique and sizeable value creation opportunity for our shareholders," commented Kevin Keyes, CEO and President of Annaly. "With the acquisition of Hatteras, we significantly grow our diversified portfolio and broaden our investment options, further fortifying Annaly's position as the market leading mortgage REIT."

Portfolio Evolution

Annaly is the parent company of Onslow Bay Financial LLC ("Onslow Bay"). Onslow Bay was a wholly owned subsidiary of Hatteras Financial Corp., which Annaly acquired in July of 2016.

The Hatteras acquisition brought not just agency MBS, but also mortgage servicing rights (MSRs)—a business that would become increasingly important to Annaly's strategy. MSRs behave differently from MBS in response to interest rate changes, providing a natural hedge and diversification benefit.

By the late 2010s, Annaly had evolved from a pure-play agency mREIT into a diversified mortgage finance company with capabilities across agency MBS, residential credit, and mortgage servicing.

VIII. Key Inflection Point #2: COVID-19 Crisis (2020)

New Leadership Amidst Chaos

The COVID-19 pandemic struck just days after Annaly announced new leadership. Annaly Capital Management announced today the Board of Directors has elected David L. Finkelstein as its Chief Executive Officer and a member of the Board, effective March 13, 2020. Mr. Finkelstein will also retain his current role as Chief Investment Officer. Mr. Finkelstein succeeds Glenn Votek, who has acted as Interim CEO and President since November 2019. Mr. Finkelstein has demonstrated his leadership in shaping the Company's investment and corporate strategy since joining Annaly in 2013.

Mr. Finkelstein has 25 years of experience in fixed income investments. Prior to Annaly, Mr. Finkelstein served for four years as an Officer in the Markets Group of the Federal Reserve Bank of New York where he was the primary strategist and policy advisor for the MBS Purchase Program. Previously, Mr. Finkelstein held senior Agency MBS trading positions at Salomon Smith Barney, Citigroup Inc. and Barclays PLC. Mr. Finkelstein received a B.A. in Business Administration from the University of Washington and a M.B.A. from the University of Chicago, Booth School of Business.

Finkelstein's background at the New York Fed, where he was instrumental in designing the very MBS purchase programs that supported Annaly's portfolio, made him uniquely qualified to navigate the crisis ahead.

Market Turmoil

The March 2020 market meltdown was brutal for mortgage REITs. As investors fled to cash, even the most liquid markets seized up. Agency MBS prices plunged, margin calls accelerated, and several mREITs faced existential threats.

Fed Intervention and Recovery

The Fed subsequently altered policy and slowly reduced its MBS holdings. By March 2020, it held about $1.4 trillion in MBS. When the COVID crisis hit in March 2020, the Fed decided to reinstate its 2008 financial crisis rescue plan. It resumed purchasing MBS as well as Treasury notes and bonds. By the time it stopped its purchases in the spring of 2022, it owned $2.7 trillion in MBS. The Fed had become the largest investor in MBS in the world.

The Fed's intervention stabilized MBS markets and allowed Annaly to weather the crisis. Once again, the company's focus on agency securities—and its ability to benefit from Fed support—proved decisive.

IX. Key Inflection Point #3: The 2022-2023 Interest Rate Shock

The Fed's Pivot and Its Impact

The mortgage boom of 2020 and 2021 was fantastic for the mortgage industry. Loan originations and home refinancing reached record levels thanks to super-low interest rates. Origination demand doesn't directly affect a company like Annaly, which purchases existing loans on the secondary market. But the low cost of borrowing did help it achieve a higher net interest margin, which is how it makes its money.

Then everything changed. At the start of 2022, the federal funds rate, which sets the cost for short-term borrowing, was at 0.25%—making Annaly's cost of capital extremely cheap. So far this year, the Federal Reserve has raised the fed funds rate six times, which has seriously hurt Annaly's earnings. Rising interest rates negatively impact a mortgage REIT's profitability because it narrows the margins on its spread between the interest its earns from its loans and its cost of borrowing. In the third quarter of 2022, Annaly's net interest spread fell by 1.37 percentage points from the quarter prior. Its net interest income, which makes up the bulk of its revenue, fell by 41% from last quarter, and 23% from last year. As a result, the company reported a per-share loss of $0.70, its first negative quarter in more than a year.

The company's net interest margin has fallen by 100 basis points since last quarter to 1.42%. But such a wafer-thin margin is hardly sufficient to sustain a 16% dividend yield, which means the company would eventually have to borrow money to continue growing its portfolio as well as revenue.

Book Value Destruction

In the third quarter of 2022, Annaly's book value fell 15% from the quarter prior, while its share price dropped by 27%.

In reflecting on the past year, it is difficult to overstate how challenging 2022 has been for financial markets, particularly for fixed income. However, I believe it is important to provide perspective on where we are today relative to history.

The Yield Curve Inversion Problem

The 2022 rate shock exposed a fundamental vulnerability in the mREIT business model. When the yield curve inverts—with short-term rates exceeding long-term rates—the carry trade that generates mREIT profits can turn negative.

By late 2022, mortgage-backed security spreads were the highest since 2008. For most of 2022, mortgage-backed securities underperformed Treasuries, which is why mREITs in general reported declines in book value per share. The last six weeks have been extremely volatile as the bond market whipsawed between higher-than-expected inflation and a bank crisis. This volatility pushed out mortgage-backed securities spreads again, and that was probably the catalyst for Annaly's dividend cut.

The Inevitable Dividend Cut

While we generated EAD that covered our dividend this quarter, we witnessed the moderation discussed in recent quarters, and we anticipate some further pressure on EAD going forward. As a result, subject to determination by our Board, we expect to reduce our quarterly dividend in the first quarter of 2023 to a level closer to Annaly's historical yield on book value of 11% to 12%, which compares to the approximately 16% yield on book we are paying today.

Leading mortgage REIT Annaly Capital just cut its dividend by 26%, with a new quarterly payout of $0.65 per share.

The 2022 Reverse Stock Split

Annaly announced that its Board of Directors unanimously approved a reverse stock split of the Company's common stock at a ratio of 1-for-4. The reverse stock split became effective following the close of business on September 23, 2022.

The Company is implementing the reverse stock split with the objective of reducing Annaly's number of shares of common stock outstanding to more closely align with the number of common shares outstanding for companies of a similar market capitalization. As a result of the reverse stock split, the number of outstanding shares of Annaly's common stock will be reduced from approximately 1.8 billion to approximately 445 million.

Its quarterly dividend payout has been on a downward trend over the past decade. That has dragged the price of the stock down along with it. For income investors, that's a terrible outcome. The yield, which remained high because of the falling price, may have somewhat hidden the trend for those who didn't dig a little deeper.

X. Current State & Portfolio Structure (2024-2025)

Diversified Platform

The Agency portfolio saw a 10% growth quarter-over-quarter, reaching over $87 billion in market value, driven by significant investments in Agency MBS. The Residential Credit portfolio also expanded to $6.9 billion, supported by record securitization and loan purchases.

The precipitous decline in interest rate volatility during the quarter also provided meaningful support to our portfolio by lowering convexity costs and fueling much of the agency's spread tightening that occurred. We generated an economic return of 8.1% for the third quarter and 11.5% year to date, notably recording a positive economic return for eight consecutive quarters, exhibiting the benefits of Annaly Capital Management's diversified housing finance strategy. Our portfolio's earnings power remains strong with EAD of $0.73 per share, out-earning our dividend each quarter since we increased it at the outset of the year. Also to note, we raised $1.1 billion of accretive equity in Q3, including $800 million through our ATM program. We also reopened the mortgage REIT preferred market with Annaly's first preferred issuance since 2019 and the first residential MREIT issuance in multiple years.

"Annaly generated an economic return of 11.9% in 2024 supported by strong performance from each of our three investment strategies," remarked David Finkelstein, Chief Executive Officer and Co-Chief Investment Officer. "Throughout 2024, we grew our Agency portfolio by nearly $5 billion as we deployed proceeds from accretive capital raised while continuing to migrate up in coupon. Our Residential Credit business grew 17% year-over-year driven by record production from our whole loan correspondent channel, which achieved nearly $12 billion in loan fundings. With respect to MSR, we enhanced our leadership in the sector, growing our portfolio by 24% year-over-year and expanding our recapture and subservicing relationships."

Current Dividend Profile

Annaly announced its 3rd Quarter 2025 Common Stock Dividend of $0.70 per Share. This represents a meaningful recovery from the 2023 dividend cut, though still substantially below the pre-2022 levels.

Economic Return: 8.1% for Q3 2025; 11.5% year-to-date. Earnings Available for Distribution (EAD): $0.73 per share, exceeding the dividend. Book Value Per Share: Increased 4.3% from $18.45 to $19.25. Agency Portfolio Market Value: Over $87 billion, up 10% quarter-over-quarter. Residential Credit Portfolio: Increased to $6.9 billion in economic market value. MSR Portfolio Market Value: Increased by $215 million to $3.5 billion.

XI. Competitive Landscape & Strategic Analysis

Primary Competitors

AGNC is an internally managed mortgage REIT built with the objective of generating favorable long-term stockholder returns with a substantial yield component through levered investments in Agency residential mortgage-backed securities.

AGNC allocates over 98% of its portfolio to agency MBS assets backed by Fannie Mae, Freddie Mac, or Ginnie Mae. Fannie and Freddie are both government-sponsored enterprises, and Ginnie is a government-owned organization within the U.S. Department of Housing and Urban Development (HUD). AGNC says that government support "substantially eliminates credit risk and protects us in the event borrowers default on their mortgage payments."

When AGNC Investment started paying monthly dividends in 2014, it set the rate at $0.22 per share. Today, it pays $0.12 per share, with the last cut coming in 2020. Given the history of reductions, investors can't bank on the REIT continuing to pay its current rate forever.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The mREIT space has significant barriers to entry including capital requirements, expertise in MBS trading and hedging, and established relationships with repo counterparties. However, once entered, there's limited protection from competition.

Bargaining Power of Suppliers (Capital Markets): HIGH mREITs are fundamentally dependent on their ability to borrow at attractive rates. When repo markets seize up or counterparties become reluctant to lend, the business model faces existential risk. The 2008 crisis demonstrated this vulnerability clearly.

Bargaining Power of Buyers (MBS Markets): MODERATE Agency MBS trades in highly liquid markets with many participants. Annaly cannot dictate prices but operates in markets deep enough to execute significant trades without moving prices dramatically.

Threat of Substitutes: HIGH Investors seeking yield have many alternatives: equity REITs, dividend stocks, bonds, preferred securities, and more. The mREIT value proposition of double-digit yields must constantly be weighed against these alternatives and their associated risks.

Industry Rivalry: HIGH Competition among mREITs is intense. Players like AGNC, Two Harbors, and others pursue similar strategies, making differentiation difficult. Scale provides some advantages in terms of operating cost efficiency and market access.

Hamilton Helmer's 7 Powers Framework

Analyzing Annaly through the 7 Powers lens reveals a company with limited durable competitive advantages:

Scale Economies: Moderate. Larger mREITs have lower operating expense ratios and better access to capital markets.

Network Effects: None. There is no network dynamic in the mREIT business.

Counter-positioning: None. Annaly's strategy can be replicated by any competitor with sufficient capital.

Switching Costs: None. Investors can easily sell Annaly shares and buy a competitor's.

Branding: Limited. While Annaly has name recognition as the largest mREIT, this doesn't command premium pricing.

Cornered Resource: None. Agency MBS are publicly traded securities available to any buyer.

Process Power: Potentially moderate. Decades of experience in hedging, risk management, and market navigation may provide some operational edge, though this is difficult to measure.

The honest assessment is that mREITs operate in a business with few durable competitive advantages. The primary differentiator is management skill in portfolio construction and risk management—something that's difficult to assess ex-ante and may not persist across management changes.

XII. Myth vs. Reality: Common Narratives Examined

MYTH: "High dividend yields mean mREITs are great income investments."

REALITY: The high yields reflect high risk, not generous management. Over time, dividend cuts and book value erosion have often more than offset the income received. They show that the dividend and the stock price have headed steadily lower over the past decade, meaning that shareholders would have been left with capital losses and less income if they were using the dividend income to pay for living expenses. But notice the blue line, which is dividend yield. Because of the basic math of dividend yield, it has remained high the whole time despite the terrible outcome for the dividend and stock price.

MYTH: "Agency MBS are risk-free because they're government-backed."

REALITY: Agency MBS eliminates credit risk but retains significant interest rate risk. When rates rise rapidly, agency MBS prices fall substantially. The government guarantee protects against default losses, not market value losses.

MYTH: "mREITs benefit from Fed rate cuts."

REALITY: It depends. Rate cuts steepen the yield curve and can improve net interest margins. But they also accelerate prepayments (as homeowners refinance), forcing reinvestment at lower yields. The relationship between Fed policy and mREIT profitability is complex and non-linear.

XIII. Key Performance Indicators to Watch

For investors monitoring Annaly, three KPIs matter most:

1. Book Value Per Share (BVPS) This is the single most important metric for mREIT investors. BVPS reflects the net asset value of the portfolio after accounting for liabilities. A declining BVPS signals that the high dividend is being paid at the expense of capital—a pattern that cannot continue indefinitely.

2. Net Interest Margin (NIM) / Net Interest Spread The spread between what Annaly earns on its assets and pays on its liabilities drives profitability. Investors should track this metric quarterly and understand the factors driving changes.

3. Economic Leverage Ratio Higher leverage amplifies returns but also magnifies losses. Tracking leverage relative to historical norms and peer levels provides insight into management's risk appetite and the portfolio's sensitivity to market movements.

XIV. Regulatory and Accounting Considerations

Material Overhangs: - GSE Reform: The status of Fannie Mae and Freddie Mac in government conservatorship has persisted since 2008. Any change to the GSE model could impact agency MBS markets and Annaly's core business. - Interest Rate Policy: Fed policy directly impacts mREIT profitability. The unpredictable nature of monetary policy creates ongoing uncertainty.

Accounting Judgments: - Portfolio valuations rely on mark-to-market accounting for securities. Illiquid positions may involve judgment in determining fair value. - Hedge accounting treatment affects how gains and losses flow through the income statement.

XV. Bull and Bear Cases

The Bull Case

Agency MBS continues to exhibit attractive spreads on both an absolute and relative basis to competing asset classes further supported by a better balanced supply and demand picture and improved carry. Our residential credit business is a clear market leader with strong momentum for continued growth after another year of record loan production and securitization volume. We expect the non-QM origination market to grow in 2025 with Onslow Bay well-positioned to further expand our market share and capabilities. Within MSR, our deep capital base, low leverage and partnerships with originators and servicers all support further growth of the portfolio. We expect the Annaly platform to continue to outperform in the current operating environment as our diversified strategies, conservative leverage and ample liquidity are key differentiators.

Looking ahead, Annaly's guidance is driven by expectations of continued fixed income demand, further Federal Reserve rate cuts, and a stable housing finance environment. Management believes that tightened Agency spreads and healthy MSR supply will support portfolio growth, while the company's capital flexibility should help navigate uncertain macroeconomic conditions.

The Bear Case

To be clear, mREITs are by far the most risky ultra-high-yield class of equities you can own, and most dividend investors would be better off ignoring the sector entirely. That's because this is an industry that has come to prominence during a time of historically falling interest rates, which may have created a decades-long tailwind for the business model that may not be repeated as rates gradually climb in the coming years.

They show that the dividend and the stock price have headed steadily lower over the past decade, meaning that shareholders would have been left with capital losses and less income if they were using the dividend income to pay for living expenses. But notice the blue line, which is dividend yield. Because of the basic math of dividend yield, it has remained high the whole time despite the terrible outcome for the dividend and stock price.

XVI. Conclusion

Annaly Capital Management represents one of the most fascinating case studies in American finance—a company that has survived and evolved over nearly three decades in a business model that has killed many competitors. Its focus on agency securities, disciplined risk management, and ability to navigate market crises has earned it the position of largest mortgage REIT in the United States.

Yet survival is not the same as value creation. The historical pattern of dividend cuts, book value erosion, and the need for a reverse stock split raise legitimate questions about whether the mREIT business model creates durable value for shareholders, or whether it simply offers high current income at the expense of long-term capital.

CEO David Finkelstein emphasized the success of Annaly's diversified housing finance model, which has consistently delivered results, and expressed confidence in the market, noting, "We feel good about the market. Spreads are tighter."

For investors, Annaly represents a clear value proposition: exposure to agency MBS markets with professional management, meaningful yield, and the liquidity of a publicly traded security. But this comes with commensurate risks: interest rate sensitivity, book value volatility, and the structural challenges of the mREIT business model.

Understanding Annaly means understanding American housing finance at its most sophisticated—and its most fragile. The company embodies both the elegant financial engineering that can transform leverage and duration mismatch into double-digit yields, and the inherent instability that can turn those same factors into catastrophic losses. Nearly three decades after its founding, Annaly continues to navigate this tightrope, generating substantial income for shareholders while testing the limits of what a highly leveraged, interest-rate-sensitive business can sustainably deliver.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube