Aroundtown SA: The Rise and Reckoning of Europe's Real Estate Giant

I. Introduction: When the Music Stopped

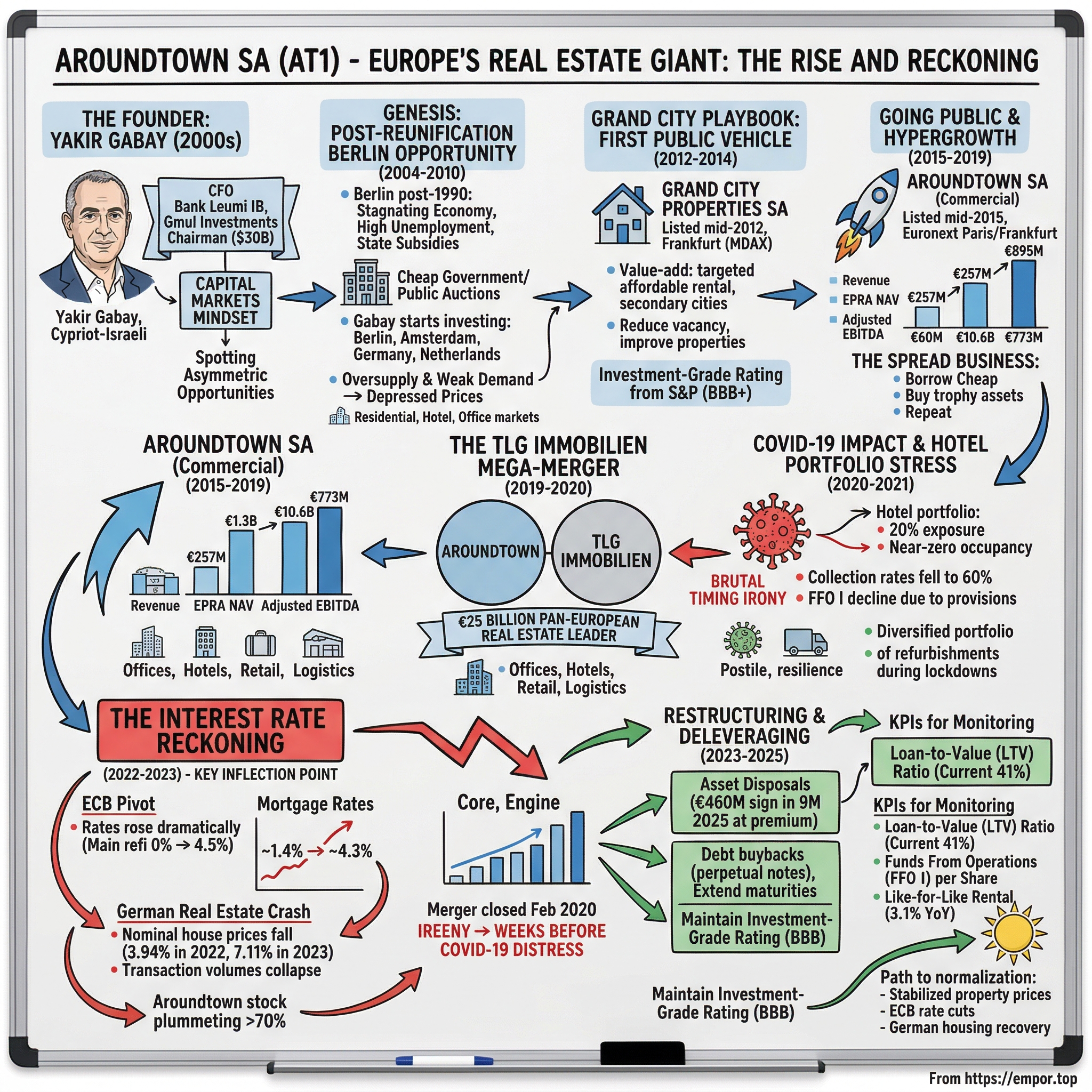

The calendar read February 2020. In a gleaming Frankfurt conference room, executives from Aroundtown SA and TLG Immobilien AG uncorked champagne to celebrate the completion of their €3.1 billion merger—a deal that would create Germany's largest commercial real estate empire with over €25 billion in assets. The timing seemed impeccable. Interest rates had been negative for years. Property values only moved in one direction. The playbook was simple: borrow cheap, buy trophy assets, repeat.

Aroundtown SA and TLG Immobilien AG struck a merger agreement to create one of the largest pan-European commercial real estate companies with total assets surpassing €25 billion. Within weeks, COVID-19 would ravage their hotel portfolio. Within two years, the European Central Bank would embark on its most aggressive rate-hiking cycle in history, sending German real estate into a tailspin and Aroundtown's stock plummeting more than 70% from peak levels.

Aroundtown SA, together with its subsidiaries, operates as a real estate company in Germany, the Netherlands, the United Kingdom, Belgium, and internationally. It operates through Commercial Portfolio and GCP Portfolio segments. The company invests in commercial real estate properties, including hotel, office, retail, logistics, and other properties, as well as in residential real estate properties.

The Aroundtown story poses a central question that has defined an era of European real estate: How did an Israeli entrepreneur turn post-reunification Berlin properties into Germany's largest listed commercial real estate empire—and what happens when the zero interest rate party ends?

As of 30-Jun-2025, Aroundtown's stock price is $3.65. Its current market cap is $3.99B with 1.09B shares. Compare that to peak valuations approaching €10 billion, and the destruction of shareholder value becomes stark. Yet buried within this wreckage lies a fascinating case study in capital markets innovation, the perils of financial engineering, and the resilience—or lack thereof—of business models built on monetary tailwinds.

This piece will take you through the origin story of founder Yakir Gabay, the post-reunification Berlin opportunity that birthed the company, the hypergrowth years powered by zero interest rates, the ill-timed mega-merger, and the brutal reckoning that followed. Along the way, we'll apply Porter's Five Forces and Hamilton Helmer's Seven Powers frameworks to understand what sustainable competitive advantages—if any—Aroundtown possesses, and what it means for long-term fundamental investors.

II. The Founder: Yakir Gabay's Investment Banking Mindset

Every real estate empire begins with a contrarian bet, and Yakir Gabay's formative years explain why he was uniquely positioned to spot one. Yakir Gabay (Hebrew: יקיר גבאי; born 1966) is a Cypriot-Israeli billionaire real estate businessman, based in Cyprus. Gabay was born in Jerusalem. He completed a BS degree in economics and accounting, and an MBA degree in finance and business development at the Hebrew University. Gabay started his career in the Prospectus Department of Israel's SEC. He then served in management positions in the capital market as an investment banker.

This pedigree matters. Gabay didn't come from property development or construction. He came from capital markets—from understanding how securities are structured, how prospectuses are written, how institutional money flows. Among other things, he was CEO of the investment banking division of Bank Leumi, one of Israel's largest banks. He also served as chairman of Gmul Investments (Israel), which managed pension fund, real estate and securities investments totaling $30 billion.

The family background is equally remarkable. Gabay is the son of Meir Gabay, a former Director-General of the Israeli Ministry of Justice who also served as the Civil Service Commissioner of Israel, in addition to being elected the President of the United Nations Administrative Tribunal. Yemima Gabay, his mother, was a senior at the Israeli State Attorney's Office and Director of the Pardons Department in the State of Israel's Ministry of Justice. A family steeped in public service and institutional rigor—not exactly the profile one associates with speculative real estate plays.

But it was precisely this institutional mindset that gave Gabay an edge. By the early 2000s, he had witnessed how international capital was flowing into assets across Europe, seeking yield in an increasingly low-rate environment. He understood that real estate wasn't just about bricks and mortar—it was about financial engineering, capital structure optimization, and arbitraging the spread between borrowing costs and asset yields.

CEO of the investment banking division of Bank Leumi, then partner and chairman of Gmul Investments which back then managed investments for pension funds, in real estate and securities totaling $30 Billions. In 2004, Mr. Yakir Gabay established real estate investment activity in Berlin and Amsterdam and expanded to other large cities in Germany and the Netherlands in the residential, hotel and office markets.

The timing of 2004 wasn't accidental. Germany—and Berlin in particular—was emerging from a decade-long real estate depression that had created one of the most asymmetric risk/reward opportunities in global property markets. Understanding why requires a brief detour into German reunification history.

Yakir Gabay's fortune is estimated at $3.4 billion and he is the number 766 of the billionaires on the Forbes 2023 list. That wealth didn't materialize from thin air—it was built on a very specific historical moment and a very specific thesis about how capital markets would evolve.

III. The Genesis: Post-Reunification Berlin's Hidden Opportunity (2004-2010)

Picture Berlin in 2004. Fifteen years after the Wall fell, the city remained an economic basket case—a capital with world-class architecture and culture, yet property prices that defied logic. Unification brings change From 1990 to 2005, Berlin faced the problematic issue of reunification – in the context of a stagnating economy – with a 20 percent unemployment rate and GDP growth close to zero. Public deficits combined with an enormous stock of property inherited from the German Democratic Republic of East Berlin resulted in a constant inflow of properties into the market through the government and public housing corporation auctions.

By that time, oversupply matched by weak demand – as a result of the poor economy – put enormous pressure on property prices, bringing them down to a level without comparison in the whole of Europe and other developed countries. Furthermore, before 1990 Berlin was managed by a vast amount of state subsidies that included the residential rental market, creating a legacy of low rental costs. This encouraged people to rent as opposed to buy, and led to one of the lowest homeownership rates in the whole EU area.

The reunification process was a fiscal disaster for Germany overall and Berlin in particular. But time and growth are allowing the economy to regain its health. Germany's unemployment rate recently dropped below 10 percent for the first time in 10 years.

This was the landscape when Gabay made his first moves. In 2004, Gabay established real estate investment activity in Berlin and expanded to other large cities in Germany, UK and the Netherlands in the residential, hotel and office markets.

Early investments between 2004 and 2006 involved small-scale purchases of underutilized assets in Berlin's urban core, capitalizing on market opportunities in post-reunification properties to generate income through modernization and leasing. This approach allowed for steady portfolio expansion during the initial years as a privately held entity.

The initial business model was elegantly simple. Gabay and his team would identify underperforming properties—buildings with high vacancy rates, deferred maintenance, or absentee landlords who had inherited assets they didn't care to manage. They'd acquire these properties at distressed valuations, execute operational improvements (renovations, better tenant management, repositioning), and harvest the resulting value through either refinancing or sales.

After the burst of the dot.com-bubble in 2001, international capital sought less volatile investments in the housing market to diversify their portfolio. While in many European countries, house prices increased rapidly until 2007, the value of German residential properties increased only slightly. Hence, the German housing market was widely considered to be under-valued and high yields were expected.

Then came the 2008-2009 global financial crisis—and what could have been a disaster became an accelerant. While distressed property owners across Germany rushed to liquidate, Gabay and his team were buyers. By 2009–2010, Aroundtown had evolved from ad hoc private investments into a more formalized structure, broadening its scope beyond Berlin to include other major German cities while laying groundwork for future capital market access. This period marked a shift toward scalable operations, setting the stage for subsequent growth in the commercial real estate sector.

The neighborhoods that Gabay initially focused on—Mitte and Charlottenburg in central Berlin—would become some of the most valuable real estate in Germany over the following decade. But in 2004, they were simply undervalued urban core assets in a city struggling to find its post-Cold War identity. The key insight wasn't just about buying cheap property. It was recognizing that Berlin's fundamentals—its status as Germany's capital, its cultural magnetism, its untapped potential—would eventually close the gap with other European capitals where comparable properties traded at multiples higher.

IV. The Grand City Playbook: First Public Vehicle (2012-2014)

Before Aroundtown itself went public, Gabay tested the capital markets through a residential-focused vehicle that would prove the concept. In mid-2012, Gabay issued Grand City Properties SA, a residential company, at a company value of €150 million and price share of €2.7. The issue is considered most successful on the Frankfurt Stock Exchange. The company is traded on prime standard segment of the Frankfurt stock exchange, with total assets over €10 billion and at a market cap of €3.6 billion with price share of €20 (as of December 2020), and is included in the major stock indices such as MDAX.

Grand City Properties represented more than just another listing—it was a proof of concept for a capital-light, value-add strategy that could be scaled through public market access. The company targeted a specific niche: affordable rental housing in German secondary cities, acquiring properties that had been "sub-optimally managed" and systematically improving returns.

The value-add playbook was methodical. Acquire underperforming buildings. Reduce vacancy through better property management. Execute modest capital improvements—upgrading apartments, installing playgrounds, improving access with elevators. Optimize rent rolls. The result: rental income improvements of 20% or more across the portfolio, with corresponding asset value appreciation.

But the real innovation was on the capital side. Grand City obtained something that would become Aroundtown's most valuable competitive advantage: one of the first investment-grade credit ratings for a German real estate company from S&P. This wasn't just a badge of honor—it was a structural advantage that enabled access to debt capital markets at rates unavailable to competitors.

In the zero-interest-rate environment of 2012-2015, the difference between borrowing at 2% versus 4% was enormous when applied to billions of euros of acquisitions. The spread business—borrow cheap, buy assets yielding more than your cost of capital, pocket the difference—worked spectacularly when money was nearly free.

Grand City Properties, a residential owner, was listed on the Frankfurt Stock Exchange (MDAX) in mid-2012 with a company value of €150 million, reaching a market cap of €4 billion. Aroundtown SA, a commercial real estate owner, was listed on Euronext Paris and the Frankfurt Stock Exchange in mid-2015, with a value of €1.5 billion and reached a market cap of €10 billion.

Grand City Properties' trajectory—from €150 million at listing to €4 billion market cap—validated the thesis that institutional investors were hungry for German real estate exposure, particularly when packaged with professional management and investment-grade credit metrics. The playbook was proven. Now it was time to apply it to commercial real estate on a grander scale.

V. Going Public & Hypergrowth (2015-2019)

In mid-2015, Gabay listed the shares of Aroundtown SA in both Euronext Paris and the Frankfurt Stock Exchange, at a company value of €1.5 billion and share price of €3.2. The listing was successful with more than doubling of the share price to 6.2 in December 2020.

The commercial real estate strategy differed from Grand City's residential focus. Aroundtown targeted a different asset mix—offices, hotels, retail—in top-tier European cities, with Germany as the core market. In 2014, the company acquired 22 hotels across major German cities including Berlin, North Rhine-Westphalia (NRW), Leipzig, and Baden-Baden, valued at €200 million, contributing to a commercial portfolio expansion to 301,000 square meters with hotel properties reaching a fair value of €405 million by year-end.

By 2015, Aroundtown acquired €1.3 billion in commercial properties mainly in Germany—such as Berlin, Munich, NRW, and Hamburg—with allocations of approximately 40% to offices, 25% to retail, and 20% to hotels, significantly boosting its portfolio fair value from €426 million at the end of 2014 to €2.43 billion.

What followed was one of the most aggressive growth stories in European real estate. The company promptly obtained an investment-grade rating and through 2020, successfully raised consecutive rounds of funding. The growth metrics were staggering:

| Metric | 2014 | 2019 | Growth |

|---|---|---|---|

| Revenue | €257 million | €895 million | 3.5x |

| EPRA NAV | €1,274 million | €10.6 billion | 8.3x |

| Adjusted EBITDA | €60 million | €773 million | 12.9x |

Aroundtown which is the largest listed commercial real estate company in Germany, merged in February 2020 with TLG Immobilien AG which was traded on the Frankfurt Stock Exchange with market cap of over €3 billion. By 2019, it had become the largest publicly traded real estate company in Germany.

The geographic distribution reflected a focused strategy on prime locations. Berlin represented 25% of the portfolio, with Frankfurt, Munich, Cologne, Hamburg, Amsterdam, and London comprising the remainder. Aroundtown is the largest commercial real estate company in Germany and 4th largest in Europe. The Company invests in top tier cities and metropolitans of Germany, Netherlands and London. The focus of Aroundtown's business model is buying, repositioning and optimizing office, hotel and residential properties.

The European zero-interest-rate environment served as the ultimate tailwind. With the ECB's main refinancing rate at or below zero for most of this period, the spread between Aroundtown's cost of debt and the yields on acquired properties created an almost mechanical profit engine. Borrow at sub-2%, buy assets yielding 4-6%, leverage 50-60%, and the equity returns compound rapidly.

Aroundtown SA and Grand City Properties are both ranked by Standard & Poor's Global Ratings BBB +. The investment-grade rating wasn't just prestige—it enabled access to the European bond market, where Aroundtown could tap institutional capital at rates that smaller, unrated competitors couldn't match.

The virtuous cycle seemed unstoppable: lower financing costs enabled more acquisitions, which generated more rental income, which supported higher property valuations, which improved credit metrics, which enabled even cheaper financing. What could possibly go wrong?

VI. The TLG Immobilien Mega-Merger (2019-2020)

By late 2019, Aroundtown and TLG Immobilien had grown into complementary juggernauts. Both focused on German commercial real estate, but with different historical roots and portfolio compositions. A combination seemed logical—scale benefits, operational synergies, and an even stronger platform for capital markets access.

Germany's Aroundtown and TLG Immobilien are examining a merger to create a pan-European commercial real estate market leader worth 25 billion euros ($28 billion). As a booming market encourages expansion, TLG Immobilien on Sunday said it bought a 9.99% stake in rival Aroundtown from its largest shareholder, Avisco Group for about 1.02 billion euros, adding the deal would immediately add to its funds from operations per share.

In September 2019, TLG Immobilien AG acquired a 9.99% stake in Aroundtown SA from entities controlled by Yakir Gabay for approximately €1.02 billion ($1.14 billion), marking a partial exit for Gabay ahead of the subsequent combination. This transaction provided TLG with a foothold in Aroundtown while allowing Gabay, as Aroundtown's largest shareholder and deputy chairman of its advisory board, to realize gains from his holdings without fully divesting. On November 18, 2019, Aroundtown SA and TLG Immobilien signed a binding business combination agreement, under which Aroundtown launched a voluntary public takeover offer for all outstanding shares of TLG not already held by Aroundtown.

TLG Immobilien, which has its roots in eastern Germany but has been spreading its investment wings recently, has a property portfolio valued at €4.6bn (end-June 2019). This consists mainly of offices, particularly in Berlin, Dresden, Leipzig, Rostock, and Frankfurt am Main, and a regionally-diversified portfolio of retail properties, mainly grocery-anchored retail parks, together with seven good quality hotels.

TLG's history was distinctly German. Das Unternehmen wurde 1991 als Tochtergesellschaft der Treuhandanstalt gegründet. Der Treuhand Liegenschaftsgesellschaft mbH (TLG) oblag die Verwaltung, Verwertung und Entwicklung der sonstigen Immobilienbestände in den neuen Bundesländern im Besitz der Treuhandanstalt. (The company was founded in 1991 as a subsidiary of the Treuhandanstalt, the agency responsible for privatizing East German state assets after reunification.)

As part of the agreed transaction, TLG shareholders will receive 3.6 new Aroundtown shares in exchange for each share held in the targeted company. The public offer translates to €27.655 per TLG share. Major shareholders and the board of TLG support the proposal, with approximately 28% of the company's total share capital already committed to the tender that is expected to result in annual FFO growth of between €110 million and €139 million within five years following the merger.

Durch die Fusion entsteht laut Analysten ein möglicher Kandidat für den Dax. Bislang ist der Gewerbeimmobilienkonzern Aroundtown im MDax und TLG Immobilien im Nebenwerteindex SDax gelistet. Nach Abschluss der Übernahme würde ein europäisches "Schwergewicht" mit einem geschätzt 25 Milliarden Euro schweren Büro- und Hotelimmobilienportfolio entstehen. (Through the merger, analysts expected a possible DAX candidate. At the time, Aroundtown was listed in the MDAX and TLG in the SDAX index.)

Am 13. Februar 2020 meldet Aroundtown eine Annahmequote für das Angebot an die Aktionäre der TLG Immobilien von 77.8 %, womit die Fusion auch formal eingeleitet wurde. (On February 13, 2020, Aroundtown announced an acceptance rate of 77.8% for the offer to TLG shareholders, formally initiating the merger.)

The timing irony was brutal. The merger closed in February 2020—just weeks before COVID-19 would send hotels globally into unprecedented distress, and less than two years before the ECB would begin its most aggressive rate-hiking cycle in history.

VII. COVID-19 Impact & Hotel Portfolio Stress (2020-2021)

The pandemic struck Aroundtown at its most vulnerable point: the hotel portfolio. Almost 30% of Aroundtown's hotels by rent remain closed due to the impact of the pandemic. Any potential conversions of hotel assets to residential units would build on Aroundtown's already substantial residential portfolio, which comprises about 13% of the group's assets by value.

Hotels represented approximately 20% of Aroundtown's commercial portfolio—a significant exposure to an asset class that went to near-zero occupancy overnight. Conference travel evaporated. Business travel collapsed. Tourism stopped entirely. During the first quarter of 2021, the Company posted an FFO I of €87 million, including extraordinary provisions for uncollected rent related to the hotel portfolio. Excluding these expenses, FFO I for the reporting period stood at €125 million, as compared to €127 million in the first quarter of 2020, slightly lower as a result of the strong disposal activity between the periods.

The COVID-19 pandemic introduced challenges, particularly in the hotel sector, where collection rates fell to 60% and like-for-like net rental income declined by 1.8%. Despite these pressures, including €120 million in extraordinary expenses for uncollected rents, the company's diversified portfolio provided resilience.

The company pivoted to accelerate refurbishment programs during the lockdowns—executing renovations more quickly and with less disruption while properties sat empty. One standout example: the €7 million refurbishment of an iconic water tower in Cologne, once the largest of its kind in Europe, which was repositioned as part of Hilton's Curio Collection with a rooftop bar offering 360-degree views.

GCP, a publicly listed entity on the Frankfurt Stock Exchange, was fully consolidated into Aroundtown's financial statements starting July 1, 2021, following Aroundtown's acquisition of a controlling stake, now at 62% as of June 2025, enabling integrated reporting of its residential assets primarily located in Germany and the United Kingdom.

The consolidation of Grand City Properties added significant residential exposure, which proved more resilient during the pandemic than commercial assets. But a new threat was already gathering—one that would prove far more damaging than COVID-19 to Aroundtown's business model.

VIII. The Interest Rate Reckoning (2022-2023) — KEY INFLECTION POINT

The ECB Pivot

For over a decade, European real estate had been powered by one overwhelming tailwind: near-zero or negative interest rates. That era ended abruptly in 2022.

In response to rising inflation, the European Central Bank (ECB) changed its interest policy and raised rates significantly. The ECB's main refinancing rate, for example, increased from 0% in June 2022 to 4.5% in September 2023. The result, however, threw the German real estate market into profound uncertainty.

The speed of the rate increases was unprecedented. The European Central Bank on Thursday announced a 10th consecutive hike in its main interest rate, as the fight against inflation took precedence over a weakening economy. Rate rises have now hauled the central bank's main deposit facility from -0.5% in June 2022 to a record 4%.

For mortgage rates, the impact was even more dramatic. In January 2022, German mortgage rates stood at approximately 1.4%. By November 2023, the average interest rate for a housing loan in Germany reached 4.3%—the highest level since 2009. Financing costs had more than tripled in under two years.

The German Real Estate Crash

Nominal house prices fell by 3.94% in 2022 and by a further 7.11% in 2023, translating into real declines of 11.53% and 10.30%, respectively. The contraction was most pronounced in previously overheated city markets, where years of rapid appreciation had stretched affordability to record levels.

The result, however, threw the German real estate market into profound uncertainty. For example, the House Price Index (HPI)—a key market indicator that previously had climbed steadily for years—recorded a decline of around 9% from the second quarter of 2022 to the first quarter of 2023.

Transaction volumes collapsed. The real estate transaction market in Germany ended 2022 with approximately €65 billion in volume, down from €110 billion in 2021—a 41% decline. In some segments, activity came to a virtual standstill as buyers and sellers couldn't agree on prices.

Aroundtown's Stock Collapse

Shares in German real estate firm Aroundtown SA slumped 13% to an all-time low, dragging down the entire European property sector, after BNP Paribas Exane slashed its price target on the stock to one euro and predicted earnings would tank by over a third. Aroundtown, which invests in commercial as well as residential real estate, is already this year's worst European equity performer after Credit Suisse AG, having shed more than half its value since mid-January.

On the other end, Luxembourg-registered Aroundtown Property fell 11% after its subsidiary Grand City Properties said Thursday that it would not pay a dividend for the past fiscal year.

LUXEMBOURG (dpa-AFX) - Aroundtown subsidiary Grand City Properties surprisingly does not plan to pay a dividend for the past fiscal year. In a statement published in Luxembourg on Thursday, the company justified this by citing uncertainty with regard to valuations, rising financing costs and limited access to capital markets.

The dividend suspension was a watershed moment. Real estate companies are supposed to be dividend machines—steady income generators that distribute cash flows to shareholders. When Grand City suspended its dividend, citing "limited access to capital markets," it signaled that the model built on cheap debt was broken.

The Debt Refinancing Challenge

The math had flipped brutally. When Aroundtown could borrow at 1-2%, acquiring assets yielding 4-5% generated attractive spreads. When borrowing costs rose to 4-5%, that spread compressed to zero or went negative. Worse, debt taken on during the low-rate years was now approaching maturity and would need to be refinanced at dramatically higher costs.

The company's debt levels remained relatively high compared to property values, and the impact on refinancing costs was substantial. For a company that had built its entire model on the spread between cost of capital and asset yields, rising rates weren't just a headwind—they were an existential challenge to the business model itself.

IX. Restructuring & Deleveraging (2023-2025)

The response to the crisis was predictable: dispose assets, reduce debt, and survive until rates normalized.

TLG Immobilien, integrated as a subsidiary after the 2020 merger and subsequent delisting tender offer in 2024 following the successful completion of the delisting in late 2024, supports Aroundtown's commercial property strategy.

Like many competitors, Aroundtown had struggled for some time with higher interest rates following years of a real estate boom, responding in part by selling properties. In the first half of 2025, properties worth around €400 million changed hands, roughly at book value, according to the company.

During the first nine months of 2025, Aroundtown completed €460 million in asset disposals at a slight premium to book value. This represents a significant slowdown from the €630 million in disposals signed in the same period of 2024, which had previously prompted S&P to downgrade the company's credit rating to BBB in April.

The third quarter 2025 results painted a picture of a company in transition. Aroundtown ('the Company' or 'AT') announces results for the first nine months of 2025, with net rental income amounting to €886 million, stable compared to €883 million in 9M 2024, as the impact from net disposals was offset by operational improvements.

Adjusted EBITDA slightly decreased to €750 million, down 1% from €758 million in the same period of 2024, while FFO I (funds from operations) amounted to €221 million or €0.20 per share. The company's loan-to-value ratio improved to 41% as of September 2025, down from 42% at the end of 2024.

Despite the FFO decline, Aroundtown confirmed its full-year 2025 guidance, maintaining expectations for FFO I to range between €280 million and €310 million, or €0.26-€0.28 per share.

There were signs of financial engineering acumen even in crisis mode. The proceeds of the issuance have been utilized to buy back perpetual notes in total aggregate amount of €1.2 billion, including through a tender offer launched in parallel to the issuance, as well as subsequent redemption call options. The perpetual notes bought back carried higher average coupons of 7%, while the total perpetual notes balance was reduced by approximately €510 million. As a result, the transaction is expected to reduce coupon payments in the amount of approx. €50 million on an annualized basis, supporting FFO as well as credit rating metrics under S&P's methodology.

In September 2025, Aroundtown issued a new €850 million bond at a coupon of 3.25%, which had a settlement date in October 2025, further decreasing compared to the 3.5% and 4.8% coupon rates of the bonds issued in May 2025 and July 2024, respectively.

The path to normalization has been aided by the broader German housing market beginning its recovery. According to preliminary results by the Federal Statistical Office (Destatis), the House Price Index rose by 3.18% year-on-year in the second quarter of 2025, marking the third consecutive quarter of positive annual growth since Q4 2024.

After years of balance sheet consolidation, the real estate group now aims to return to growth. Internally, Aroundtown can expand by repositioning hotels and redeveloping office spaces. In addition, its strong liquidity position and reduced debt level provide leeway to consider acquisition opportunities.

X. Porter's Five Forces Analysis

| Force | Assessment |

|---|---|

| Threat of New Entrants | LOW-MEDIUM: High capital requirements create barriers, and established relationships with municipalities matter. However, when cheap capital is abundant, barriers lower significantly—as the 2010s demonstrated. |

| Bargaining Power of Suppliers | LOW-MEDIUM: Construction costs matter, but diverse contractor base exists. The key "supplier" is capital—and here, power shifted dramatically when the ECB raised rates. |

| Bargaining Power of Buyers (Tenants) | MEDIUM: Prime locations give landlord leverage, but remote work trends have shifted office tenant power. Hotel guests have alternatives. Residential tenants in supply-constrained German cities have limited options. |

| Threat of Substitutes | MEDIUM: For offices, remote work is a major substitute. For hotels, Airbnb competition exists. For residential, limited substitutes in supply-constrained German cities. |

| Industry Rivalry | HIGH: Intense competition among listed German landlords (Vonovia, Deutsche Wohnen, LEG Immobilien) and private equity players hunting for yield in the same markets. |

The Porter's analysis reveals a fundamental vulnerability: Aroundtown's business model was exquisitely sensitive to one input—the cost of capital. When money was cheap, the model generated extraordinary returns. When money became expensive, competitive advantages evaporated.

XI. Hamilton's Seven Powers Analysis

| Power | Assessment |

|---|---|

| Scale Economies | MODERATE: Property management at scale creates cost advantages, but real estate is fundamentally local—Berlin expertise doesn't automatically transfer to Munich or Amsterdam. |

| Network Effects | WEAK: Real estate has limited network effects. Tenant relationships don't create winner-take-all dynamics. |

| Counter-Positioning | PARTIAL: Good relationships with brokers, ready supply of capital, and established deal-sourcing networks presented numerous attractive opportunities. Property deals sourced from banks, distressed owners, private investors, and court auctions. This off-market deal flow represented counter-positioning—but competitors have since replicated it. |

| Switching Costs | MODERATE: Long-term commercial leases (5-10 years) create tenant lock-in. But tenants eventually do move, limiting stickiness. |

| Branding | WEAK: Real estate is not a brand-driven business. Tenants care about location, amenities, and price—not landlord reputation. |

| Cornered Resource | PARTIAL: Prime locations in Berlin (25%), Frankfurt, Munich are scarce. But Aroundtown doesn't "corner" these markets—it's one of many significant owners. |

| Process Power | MODERATE: Operating with a fully integrated real estate value chain Aroundtown targets value creation opportunities from repositioning properties. Aroundtown picks quality cash generating properties with upside potential in rent and/or occupancy increase and consequential value. This represents real process expertise, but it's replicable by well-capitalized competitors. |

Overall Assessment: Aroundtown possesses moderate competitive advantages primarily from scale and process expertise in value-add investing, but lacks the durable moats (network effects, high switching costs, strong branding) that would protect against interest rate normalization. The business proved highly sensitive to the cost of capital—a factor entirely outside management's control.

XII. Business Model Deep Dive

It operates through Commercial Portfolio and GCP Portfolio segments. The company invests in commercial real estate properties, including hotel, office, retail, logistics, and other properties, as well as in residential real estate properties.

Aroundtown invests in commercial and residential real estate which benefits from strong fundamentals and growth prospects. Aroundtown invests in residential real estate through its subsidiary Grand City Properties S.A. ("GCP"), a publicly traded real estate company that focuses on investing in value-add opportunities predominantly in the German residential real estate market.

The business model can be distilled to three components:

1. The Spread Business: Borrow at investment-grade rates, acquire assets yielding more than the cost of capital, capture the spread. This works spectacularly in falling rate environments and fails in rising ones.

2. Value-Add Operations: Acquire underperforming properties, execute operational improvements, harvest appreciation through refinancing or sales.

3. Geographic Concentration: Focus on prime locations in top-tier European cities—Berlin (25% of portfolio), Frankfurt, Munich, Amsterdam, London—where supply constraints support long-term value.

Why the Model Works in Falling Rate Environments

When rates fall, real estate benefits from multiple tailwinds: - Existing debt becomes more valuable (locked in at higher rates) - Refinancing unlocks immediate savings - Asset values appreciate as cap rates compress - Acquisition multiples expand, enabling profitable exits

Why the Model Fails in Rising Rate Environments

When rates rise, the dynamics reverse: - Existing debt advantages erode at refinancing - New acquisitions require higher yields to generate returns - Cap rate expansion compresses asset values - The spread between borrowing costs and asset yields shrinks or inverts

The fundamental insight is that Aroundtown was running what's essentially a financial arbitrage wrapped in real estate operations. The real estate was high quality; the operations were professional. But the returns were primarily driven by the gap between financing costs and asset yields—a gap that depends entirely on macroeconomic conditions outside management's control.

XIII. Current Competitive Position & Industry Context

Myth vs. Reality

| Consensus Narrative | Reality Check |

|---|---|

| "Aroundtown was destroyed by COVID" | COVID hurt the hotel portfolio, but the real damage came from ECB rate hikes. Hotels have largely recovered; the equity hasn't. |

| "German real estate is permanently impaired" | All in all, we expect the housing market to continue its modest recovery. Elevated uncertainty, weak consumer sentiment, and affordability constraints will likely keep momentum in check. The mismatch between supply and demand, high rents and low homeownership ratios, however, will be clear drivers of continued growth. |

| "The business model is broken" | The spread model is impaired in current rate environment, but value-add operations and prime locations retain fundamental value. |

| "Management failed" | Management successfully navigated capital markets through crisis—reduced debt, extended maturities, maintained investment-grade rating. The model failure was structural, not operational. |

The Bull Case

-

Valuation discount to NAV: The company's EPRA NTA per share increased by 9.2% YoY to €7.78. Trading at roughly €3, the stock reflects a massive discount to net tangible assets—potentially pricing in more downside than warranted.

-

Rate environment normalizing: The ECB has begun cutting rates. If borrowing costs decline materially, the spread model could work again.

-

German housing fundamentals: Supply-demand imbalance remains acute. The Federal Institute for Research on Building, Urban Affairs and Spatial Development (BBSR) estimates the country will need 2.56 million new units by 2030—around 320,000 annually. Berlin, Munich, Hamburg, and Frankfurt top the list of cities with the largest shortages.

-

Operating improvements: Management has demonstrated capital markets acumen, reducing perpetual note coupons and extending maturities at progressively lower rates.

The Bear Case

-

Interest rates may stay elevated: If inflation proves sticky, the "higher for longer" narrative could persist, keeping financing costs elevated.

-

Office sector structural challenges: Remote work has permanently reduced demand for office space in ways that haven't fully repriced.

-

Hotel exposure volatility: While recovering, hotels remain cyclically exposed to economic downturns.

-

Leverage still elevated: LTV of 41% is manageable but leaves limited margin for error.

-

Founder dilution: Gabay held 36% of the shares of Aroundtown SA. In September 2019 Gabay sold €1.5 worth of Aroundtown shares which reduced his holdings in Aroundtown to 10% as of December 2020. Significant insider selling at higher prices.

XIV. Key Performance Indicators for Monitoring

For investors following this story, three KPIs matter above all else:

1. Loan-to-Value (LTV) Ratio

The company's leverage level determines its vulnerability to further asset value declines and ability to refinance maturing debt. Current: 41%. Watch for movement toward 40% or below as a positive signal; movement toward 45%+ would raise concerns.

2. Funds From Operations (FFO I) per Share

The core cash generation metric for real estate companies, adjusting for non-cash items. FFO I is expected to range between €280 million and €310 million for full-year 2025, or €0.26-€0.28 per share. Year-over-year trajectory indicates operational health and ability to service debt/pay dividends.

3. Like-for-Like Rental Growth

The organic growth rate in rental income from existing properties, excluding acquisitions and disposals. Like-for-like net rental growth was 3.1% YoY, with the hotel segment leading at 4.2%, followed by residential at 3.9% and offices at 1.5%. This metric indicates underlying demand for Aroundtown's properties and ability to raise rents.

XV. Investment Implications

The Aroundtown story offers several lessons for fundamental investors:

Lesson 1: Understand the Business Model's Dependencies Aroundtown appeared to be a diversified real estate company with operational expertise. In reality, it was a spread trade—highly dependent on the gap between borrowing costs and asset yields. When that gap compressed, no amount of operational excellence could save the equity.

Lesson 2: Beware "Sustainable" Dividends Funded by Cheap Debt Real estate companies that increase dividends during falling rate environments may be capitalizing temporary conditions. Grand City's dividend suspension revealed the fragility underneath.

Lesson 3: Investment-Grade Ratings Aren't Moats Aroundtown's investment-grade rating enabled cheap borrowing—but it didn't prevent the stock from falling 70%+. The rating facilitated the business model; it didn't protect shareholders from model failure.

Lesson 4: Look for True Competitive Advantages In the Seven Powers framework, Aroundtown had partial advantages in several categories but dominant positions in none. The absence of true moats left the business exposed when macroeconomic conditions shifted.

Lesson 5: Timing Matters—Sometimes Permanently The TLG merger closed in February 2020, just before COVID and two years before rate hikes. The strategic logic may have been sound, but the timing destroyed enormous value. In M&A, buying at cycle peaks with cycle-peak stock amplifies downside risk.

XVI. Conclusion: What Recovery Looks Like

As 2025 draws to a close, Aroundtown stands at an inflection point. The worst of the crisis appears over. German property prices have stabilized and begun recovering. The company has executed debt restructuring, reduced perpetual note coupons, and maintained its investment-grade rating. Management speaks of returning to growth.

But the questions facing long-term investors remain fundamental:

Is this a structurally impaired business or a cyclical recovery story?

The answer depends entirely on whether you believe: 1. Interest rates will normalize to levels that restore the spread model 2. German real estate fundamentals (supply scarcity, demographic demand) will drive continued value appreciation 3. Management's operational expertise in value-add investing creates genuine alpha

At the bottom line, Aroundtown posted a profit of €578 million, primarily due to positive valuation effects. In the same period last year, the company had recorded a loss of nearly €330 million as a result of a devaluation of its property portfolio.

The stock trades at roughly 40% of net tangible asset value—a valuation that implies either permanent value destruction or substantial upside if fundamentals normalize. Whether that discount represents opportunity or warning depends on your view of European rates, German property markets, and the sustainability of the company's competitive position.

What's clear is that Aroundtown's story—from post-reunification Berlin opportunity to Germany's largest commercial landlord to rate-hike victim—represents one of the most dramatic arcs in modern European real estate. The playbook that generated extraordinary returns for fifteen years proved exquisitely fragile when the monetary environment shifted.

For investors, the lesson transcends this specific company: understand what really drives the returns you're buying. Sometimes the business is the sizzle; the steak is the macro.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube