AGNC Investment Corp: The Mortgage REIT That Bet on the American Dream

I. Introduction & Episode Roadmap

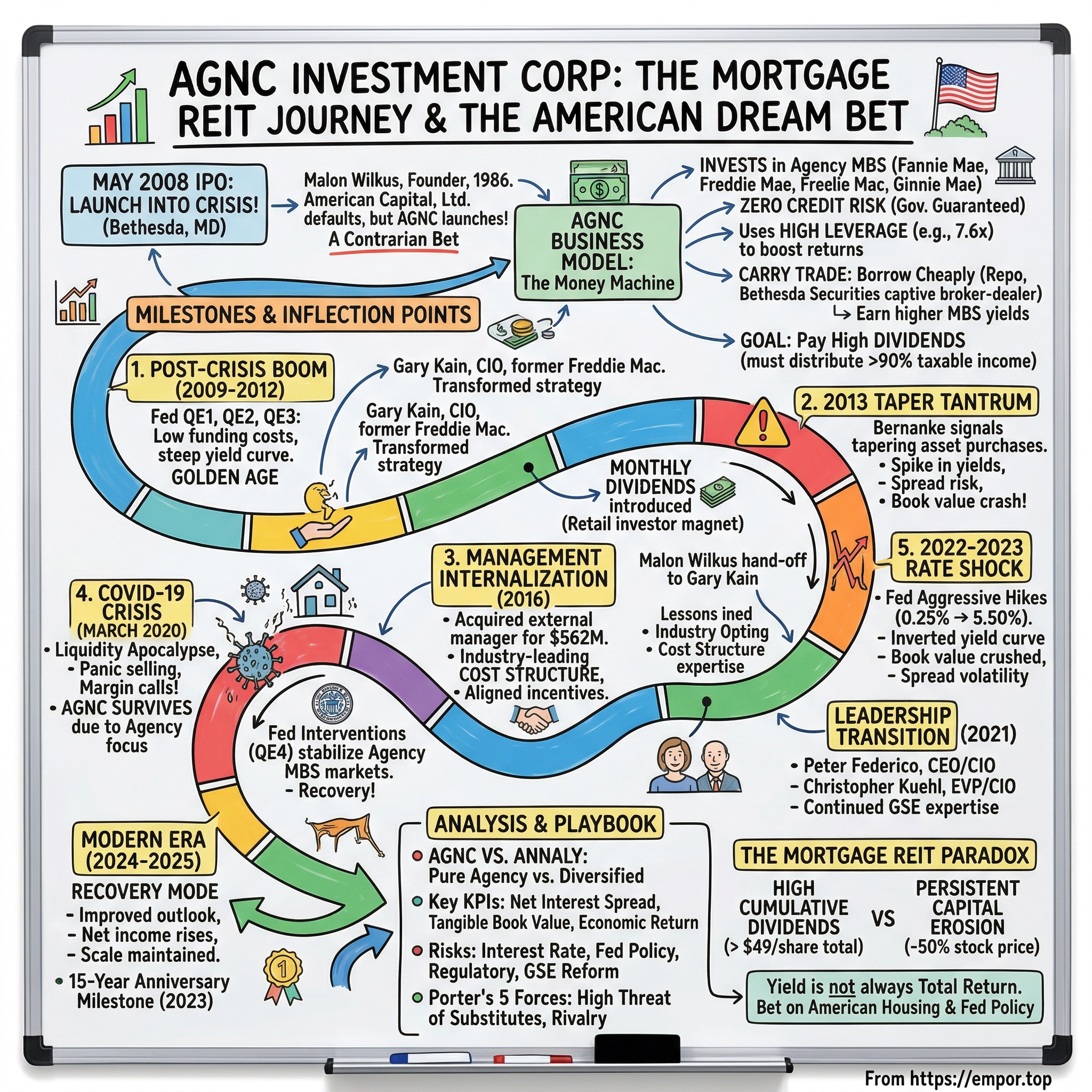

Picture this: May 2008. Bear Stearns has just collapsed into the arms of JPMorgan Chase. Lehman Brothers is six months from its date with oblivion. The entire U.S. housing market—once the foundation of the American Dream—has become a radioactive wasteland that sophisticated investors are fleeing in droves.

And yet, in Bethesda, Maryland, a team of financial engineers is doing the unthinkable: launching a mortgage-focused investment company into the teeth of the greatest housing crisis in American history.

This is the story of AGNC Investment Corp., a leading investor in Agency residential mortgage-backed securities (Agency MBS), which benefit from a guarantee against credit losses by Fannie Mae, Freddie Mac, or Ginnie Mae. It's a story about understanding the difference between credit risk and interest rate risk, about riding the Federal Reserve's coattails through three rounds of quantitative easing, about surviving margin calls and market panics, and about the eternal investor debate between yield and total return.

The numbers are staggering. From its May 2008 initial public offering through the third quarter of 2025, the Company has declared a total of $49.72 per common share in dividends. To put that in perspective: the stock currently trades around $10. AGNC has returned more than five times its current share price in cumulative dividends alone—an almost unimaginable cash distribution machine.

But here's the uncomfortable truth that makes AGNC so intellectually fascinating: despite those massive dividend payments, the stock has lost roughly half its value since its IPO. AGNC annual dividend per share is now -74.29% below its all-time high of $5.60, reached on December 31, 2010. This tension—enormous income generation alongside persistent capital erosion—lies at the heart of the mortgage REIT paradox.

Why does this matter beyond the trading screens of yield-hungry investors? Because AGNC represents something larger: the "shadow banking system" that emerged after the 2008 crisis, the complex dance between the Federal Reserve and private capital in mortgage markets, and the fundamental question of how the U.S. housing market gets funded.

Today, we're going to unpack how the money machine actually works, navigate the key inflection points that shaped AGNC's trajectory, examine the management team that has steered this ship through multiple market cycles, and extract the playbook lessons that apply far beyond mortgage REITs. This is the Acquired deep dive on AGNC Investment Corp.

II. The Origin Story: Birth in Crisis (2008)

The Perfect Storm

To understand AGNC's genesis, you need to understand the man behind it. Malon Wilkus was the Founder, Chairperson and CEO of American Capital Agency Corp., now named AGNC Investment Corp., from its founding in 2008 to 2016. AGNC trades on NASDAQ and is a real estate investment trust (REIT).

But Wilkus wasn't some Wall Street newcomer. American Capital was founded by Malon Wilkus in 1986, who served as Chairperson and Chief Executive Officer until the time of the sale of American Capital in 2017. The company was headquartered in Bethesda, Maryland. By 2008, Wilkus had built American Capital, Ltd. into a publicly traded private equity powerhouse that had been a component of the S&P 500 from 2007 to 2009.

The timing of AGNC's birth seems almost suicidal in retrospect. In 2008, American Capital launched and took public American Capital Agency (NASDAQ: AGNC). This was the same year that due to the dramatic depreciation of its assets, American Capital defaulted on its debt and began negotiations with its creditors.

Think about that for a moment. The parent company was defaulting on its debt, negotiating with creditors, and about to be ejected from the S&P 500—yet simultaneously launching a new mortgage-focused investment vehicle into the worst housing market since the Great Depression.

The company went public through an Initial Public Offering (IPO) on the NASDAQ stock exchange in May 2008, trading under the ticker AGNC. The IPO raised significant capital, providing the foundation for its investment activities in agency mortgage-backed securities (MBS).

The Contrarian Bet

So why do it? Why launch a mortgage REIT when mortgage securities were the financial equivalent of plutonium?

The answer lies in understanding a crucial distinction that most panicking investors missed in 2008: the difference between credit risk and interest rate risk.

The subprime mortgage crisis was fundamentally a credit crisis. Millions of borrowers couldn't repay their loans, causing massive losses for anyone holding non-agency mortgage securities. But Agency MBS—securities backed by Fannie Mae, Freddie Mac, or Ginnie Mae—carried an implicit (and later explicit) government guarantee against credit losses.

Launching publicly amidst the global financial crisis was a bold move. It established AGNC early on, allowing it to capitalize on market dislocations in the agency MBS sector and build scale quickly.

The genius insight was this: in the panic of 2008, investors were selling everything mortgage-related, regardless of credit quality. This pushed the yields on Agency MBS to extraordinary levels—even though these securities had essentially zero credit risk thanks to government backing. The spread between what AGNC could earn on Agency MBS and what it cost to fund those positions was historically wide.

Wilkus and his team saw what others couldn't: an asymmetric opportunity. They could buy government-guaranteed securities at panic prices, finance them cheaply, and pocket the spread—all without taking meaningful credit risk. The only real risks were interest rate movements and prepayment behavior, both of which were manageable with proper hedging.

Understanding the Business Model

Before we proceed further, we need to establish exactly how mortgage REITs make money. This is crucial because the model is often misunderstood, even by sophisticated investors.

The interest rates on agency MBS tend to be low because the bonds are guaranteed by government agencies. Consequently, to pay out a high dividend, mortgage REITs use leverage by taking out debt and investing the proceeds in mortgage-backed securities. Borrowing money to invest in an income-generating asset is known as a carry trade. The carry trade will be profitable as long as the interest rate on the debt is lower than the MBS yield and nothing happens that adversely impacts mortgage-backed security prices. The difference between the funding cost on the debt and the MBS yield is known as the net interest spread or net interest margin.

The primary funding mechanism is repurchase agreements, or "repos." Repurchase agreements are short-term collateralized loans. In a repo agreement, the mortgage-REIT sells its MBS holdings to a lender for cash and then promises to buy back the MBS later at a higher price. The MBS buyer earns interest, which is effectively the difference between the prices that the MBS was sold for and bought back. Essentially, the mortgage REIT borrows money to buy MBS and in turn, those securities serve as collateral for additional debt financing.

Mortgage REITs are highly leveraged in that the total debt can be ten times book value. Because leverage is so great, mortgage REITs will usually enter into hedging contracts in order to lock in the cost of their debt financing. Hedging debt costs helps mortgage REITs have greater confidence that the net interest spread will be positive so that they can fund dividend payments to shareholders.

And here's the tax angle that makes the structure work: It qualifies as a real estate investment trust for federal income tax purposes. The company generally would not be subject to federal or state corporate income taxes if it distributes at least 90% of its taxable income to its stockholders.

This is why mortgage REITs pay such high dividends—they're legally required to distribute nearly all their income to maintain their tax-advantaged status. The high yield isn't generosity; it's structural necessity.

III. The Mortgage REIT Deep Dive: How the Money Machine Works

Understanding Agency MBS

Let's go deeper into the asset side of the balance sheet. What exactly is AGNC buying?

Agency mortgage-backed securities are pools of residential mortgages that have been securitized and guaranteed by government-sponsored enterprises (Fannie Mae, Freddie Mac) or a government agency (Ginnie Mae). When homeowners make their monthly mortgage payments, those cash flows get passed through to MBS holders.

The guarantee is the crucial feature. If a homeowner defaults on their mortgage, the agency steps in and makes the investor whole. Given that agency backed mortgage securities are backed by government agencies, investments in agency MBS carry limited credit risk, since these investments are backstopped by the government. Over 88% of Annaly's portfolio and 97% of AGNC's portfolio are in agency backed MBS.

This near-elimination of credit risk is what allows AGNC to use significant leverage. If you're holding assets that can't default in the traditional sense, you can borrow more against them than you could against riskier assets.

The Spread Game & Leverage

The mechanics are deceptively simple in concept but diabolically complex in execution. AGNC borrows at short-term rates (usually overnight to one-year maturities) and invests in longer-duration mortgage securities. The difference—the "spread"—is profit.

The difference between the interest earned on assets and the cost of borrowing and hedging determines the net interest spread, a key profitability driver. For Q3 2024, the average net interest spread was reported around 2.84%, excluding certain amortization impacts.

But here's where leverage enters the picture. A 2.84% spread sounds modest until you apply 7-8x leverage. 7.6x tangible net book value "at risk" leverage as of September 30, 2025. Suddenly that modest spread becomes a double-digit return on equity.

The use of leverage allows mortgage REITs to magnify the yield on MBS and maintain dividend yields of over 10%.

The funding mechanism deserves special attention. AGNC created a structural advantage that most competitors lack: Bethesda Securities, a member of the Fixed Income Clearing Corporation (FICC) and the Financial Industry Regulatory Authority (FINRA), enables access to lower wholesale funding rates, reduces collateral requirements, and limits our counterparty risk.

A key operational enhancement was the formation of Bethesda Securities, its captive FINRA member broker-dealer. This move provided direct access to the Fixed Income Clearing Corporation (FICC), boosting AGNC's competitive funding advantages by streamlining repurchase agreement financing.

This captive broker-dealer is one of AGNC's genuine competitive moats. Most mortgage REITs must work through third-party dealers, which means higher funding costs and larger haircuts on collateral. AGNC's direct FICC access means cheaper money and more efficient capital utilization.

Risk Management: The Hidden Art

If the spread game is the engine, risk management is the steering wheel. And in mortgage REITs, small steering errors can be fatal.

The primary risks mortgage REITs face are:

Interest Rate Risk: Since mortgages are fixed income investments, they carry interest rate risk. As with any type of bond, when interest rates go up, the price of the bond, or in this case MBS, goes down. Because if newly issued MBS is yielding a higher rate, the value of older MBS needs to go down to match the current rate.

Prepayment Risk: When interest rates fall, homeowners refinance. This accelerates the return of principal to MBS holders, who then must reinvest at lower rates. This shortens the effective duration of the asset just when you don't want it shortened.

Extension Risk: The flip side—when rates rise, prepayments slow. Mortgages you expected to get paid off quickly now extend into a longer-duration instrument, just as rising rates are killing mark-to-market values.

Spread Risk: Even if interest rates don't move, the spread between MBS yields and Treasury yields can widen, causing price declines in MBS that are not offset by hedges designed for parallel rate movements.

AGNC's approach to managing these risks involves sophisticated hedging using interest rate swaps, swaptions, and Treasury positions. The company uses TBA securities and U.S. Treasury futures as part of its hedging strategy. These instruments help manage exposure to interest rate changes and are accounted for as derivative transactions.

The key insight here is that mortgage REITs are essentially spread-trading and interest rate arbitrage vehicles wrapped in REIT tax structure. The management team's ability to navigate duration, convexity, and spread risks is what separates survivors from casualties.

IV. Key Inflection Point #1: The Post-Crisis Boom & Fed's QE (2009-2012)

The Golden Era of Mortgage REITs

The Federal Reserve's response to the 2008 crisis created what can only be described as a golden age for mortgage REITs. In late November 2008, the Federal Reserve started buying $600 billion in mortgage-backed securities. By March 2009, it held $1.75 trillion of bank debt, mortgage-backed securities, and Treasury notes; this amount reached a peak of $2.1 trillion in June 2010.

This first round of quantitative easing (QE1) was followed by QE2 in November 2010. In November 2010, the Fed announced a second round of quantitative easing, buying $600 billion of Treasury securities by the end of the second quarter of 2011.

For mortgage REITs, quantitative easing created a near-perfect operating environment:

-

Lower funding costs: The Fed pushed short-term rates to essentially zero, making repo financing extremely cheap.

-

Compressed volatility: Fed purchases suppressed volatility in the MBS market, making hedging more predictable and less costly.

-

Steeper yield curve: The spread between short-term funding rates and long-term mortgage yields widened, increasing the net interest margin.

-

Implicit price support: With the Fed buying hundreds of billions in MBS, there was a natural floor under prices.

During the period from late 2008 through late 2014, the FOMC provided further monetary policy easing by authorizing three rounds of large-scale asset purchase programs–often referred to as quantitative easing–and a maturity extension program. The FOMC directed the New York Fed's Open Market Trading Desk to purchase longer-term securities, with the goal of putting downward pressure on longer-term interest rates, supporting mortgage markets, and making broader financial market conditions more accommodative. The longer-term securities purchased during these programs included agency MBS.

AGNC rode this wave brilliantly. The company rapidly scaled its portfolio, raising equity capital and deploying it into Agency MBS at attractive spreads. AGNC annual dividend per share reached its all-time high of $5.60 on December 31, 2010—a quarterly dividend of $1.40 that annualized to double-digit yields even on the stock's higher prices at the time.

The Architecture of Success: Gary Kain

The man who would become the architect of AGNC's investment strategy joined in early 2009. On January 12, 2009, American Capital Agency Corp. announced that its Board of Directors had appointed Gary Kain as the Company's Senior Vice President and Chief Investment Officer. Mr. Kain most recently served as Senior Vice President of Investments and Capital Markets of Freddie Mac. He also served as Senior Vice President of Mortgage Investments & Structuring of Freddie Mac from February 2005 to April 2008. Mr. Kain's group was responsible for managing all of Freddie Mac's mortgage investment activities for the company's $700 billion retained portfolio.

This hire was transformational. Gary Kain wasn't just another portfolio manager—he had been responsible for managing one of the largest mortgage portfolios on Earth. At Freddie Mac, he had overseen investment strategy, liability management, hedging, and interest rate risk management for a $700 billion book. There was perhaps no one in America better qualified to run an Agency MBS portfolio.

Gary D. Kain, born in 1966, has a solid background that supports his role, including an MBA from The Wharton School at the University of Pennsylvania. Kain's journey isn't just about titles; his track record at Freddie Mac, where he managed a $700 billion portfolio, speaks volumes about his expertise.

Kain brought two critical elements to AGNC: deep technical expertise in MBS dynamics and a genuine understanding of how the GSEs (Fannie and Freddie) operated. This insider knowledge proved invaluable in predicting prepayment behavior, understanding repo market mechanics, and anticipating Fed policy impacts.

Monthly Dividends: The Retail Investor Magnet

Between 2012 and 2015, AGNC transitioned from quarterly to monthly common stock dividends, aiming to provide investors with a more consistent income stream.

This seemingly minor operational change had significant implications for AGNC's investor base. Monthly dividends appeal particularly to retail investors seeking regular income, such as retirees. By converting to monthly payments, AGNC positioned itself as an income vehicle that could replace or supplement Social Security or pension checks.

The psychological impact of receiving twelve dividend payments per year rather than four shouldn't be underestimated. For yield-focused investors, that monthly check creates an emotional attachment to the stock that quarterly payers can't match.

Combined with yields often exceeding 10%, AGNC became a magnet for income-seeking investors. This retail following would prove both a blessing—providing a stable shareholder base—and a complication when managing expectations during difficult periods.

V. Key Inflection Point #2: The 2013 Taper Tantrum

The Shock Heard Round the Mortgage World

If the post-crisis QE era was AGNC's honeymoon, May 22, 2013 was the day the music stopped.

While then-Chairman Bernanke had attempted some earlier signals, on May 22, 2013 he announced that the Fed would begin tapering its asset purchases at some future date. The suggestion that they were considering ending those purchases sent Treasury markets into the so-called "taper tantrum". On that day, the yield on 10-year Treasury constant-maturity bonds began to rise, ultimately increasing by more than one percentage point over the next seven months. That was the "tantrum": At the announcement of what seemed a relatively uncontroversial and gradual adjustment to monetary policy, markets both immediately and over the ensuing months priced in considerably higher interest rates.

On May 22, 2013, Federal Reserve Chairman Ben Bernanke suggested in a testimony before Congress that the Fed could start tapering its bond purchases if the economy showed signs of sustained improvement. This announcement caught investors off guard, leading to a significant spike in Treasury yields as markets anticipated a tightening of monetary policy.

For mortgage REITs, this was a worst-case scenario unfolding in real time. Rising rates meant:

- Mark-to-market losses: MBS prices fell as rates rose, crushing book values.

- Duration extension: Prepayments slowed as refinancing activity collapsed, extending the duration of portfolios just as rates were rising.

- Wider spreads: MBS underperformed Treasuries, compounding losses.

- Hedge losses: Duration hedges helped but couldn't fully protect against spread widening.

REITs had a total return of negative 16 percent over the two months following their peak just prior to then-Chairman Bernanke's speech when he announced the Fed would soon taper off its purchases of Treasury and Agency securities. There was a similar initial negative reaction by REIT shares to the Taper Tantrum in 2013, which was also followed by a strong recovery. The downturn was short-lived, however.

After the taper tantrum of 2013, where rates shot up ahead of the Fed's move to end quantitative easing, mortgage REIT investors finally got a taste of interest rate risk.

This is a big event for REIT investors and those who've been watching them for signs of another crash in their prices, as occurred in 2013 when mortgage long-end Treasury yields and mortgage rates rose at the fastest rate in history. One of the reasons for the lack of a negative reaction by the REITs to today's data is that they never recovered from the crash in prices in 2013.

Lessons Learned

The taper tantrum taught the entire mortgage REIT industry several crucial lessons:

Communication is everything: Markets don't respond just to policy changes—they respond to expectations of policy changes. The Fed's communication strategy (or lack thereof) in 2013 created chaos that more transparent guidance might have avoided.

Duration management is survival: Mortgage REITs that had let their duration exposure drift too long suffered disproportionate losses. Those with tighter hedging and more active management fared better.

Spread risk is real: Most hedging strategies protect against parallel rate movements, not against MBS underperforming Treasuries. The taper tantrum showed that spread widening can be just as damaging as rate increases.

For AGNC specifically, 2013 was painful but not fatal. The company's disciplined hedging approach and pure Agency focus meant it weathered the storm better than many peers with mixed portfolios. But the experience shaped AGNC's future risk management—making the team even more attentive to duration exposure and Fed policy signals.

VI. Key Inflection Point #3: Management Internalization (2016)

The $562 Million Transformation

In July 2016, AGNC executed one of the most consequential transactions in its history—and one that most casual observers probably missed entirely.

From its founding through 2016, AGNC had been externally managed by American Capital Mortgage Management, LLC, a subsidiary of American Capital, Ltd. This was a common structure for REITs: an external manager provides investment advisory services in exchange for management fees.

But external management creates an inherent conflict of interest. The external manager gets paid based on assets under management, which can incentivize growing the portfolio even when that's not in shareholders' best interests. The manager also captures a significant portion of the economics, diluting returns to shareholders.

AGNC's board decided to change this dynamic permanently by internalizing management—essentially buying out the external manager and bringing all operations in-house.

AGNC internalizes our management structure through the acquisition of our external manager, establishing an industry-leading cost structure. As an internally managed company, AGNC adopts a stockholder-aligned incentive compensation program.

The company was formerly known as American Capital Agency Corp. and changed its name to AGNC Investment Corp. in September 2016.

Why Internalization Mattered

The internalization had three major benefits:

1. Cost savings: Without paying management fees to an external party, AGNC's operating costs dropped significantly. Those savings flowed directly to shareholders through either higher dividends or better returns.

2. Alignment of interests: With management now employed directly by AGNC and compensated through shareholder-aligned incentive programs, the conflict of interest inherent in external management structures disappeared. Management's success became directly tied to shareholder success.

3. Strategic flexibility: As an internally managed company, AGNC could make decisions based purely on what was best for shareholders, without having to consider the interests of an external manager.

AGNC internalized its management structure, leading to an industry-leading cost structure.

The internalization also coincided with Gary Kain's formal elevation to CEO. Malon Wilkus said: "Now it's come time for me to hand over the CEO position to Gary Kain. Gary has headed the company's operations and outstanding investing activities since 2009 and there is nobody better qualified than Gary to lead the company into the future and to contribute to the company's Board."

This leadership transition marked the full transfer of AGNC from its founding parent to its operational management team. Wilkus stepped back, and Kain—who had been running day-to-day investment operations since 2009—took the helm of a now-independent, internally managed company.

VII. Key Inflection Point #4: COVID-19 Crisis (March 2020)

The Liquidity Apocalypse

March 2020 tested AGNC—and the entire financial system—in ways that even the 2008 crisis hadn't. The COVID-19 pandemic triggered what can only be described as a liquidity apocalypse in fixed income markets.

As you know, conditions were extremely challenging in March as the market reacted to the COVID-19 pandemic. The dislocations witnessed during mid-March were unprecedented in terms of both magnitude and speed, resulting in a significant decline in the valuation of Agency MBS and other fixed income products. AGNC's financial performance like almost all financial companies were severely impacted by the market volatility with AGNC posting an economic return for the quarter of negative 20%.

There is considerable variation across firms, with leverage multiples ranging from 1.7 to 10.6. Amid the liquidity crunch and resulting dash for cash in mid-March, the mREIT equity price index fell more than 60% as spreads across many types of structured credit widened to levels last seen in the global financial crisis. Agency MBS spreads increased from 40 bps to 132 bps at peak.

The mechanics of what happened were terrifying in their speed. As the pandemic's severity became clear:

- Institutional investors panicked: Everyone wanted cash simultaneously.

- MBS prices collapsed: Even government-guaranteed securities fell sharply as forced sellers flooded the market.

- Repo markets seized: Lenders became nervous about taking MBS as collateral.

- Margin calls cascaded: As MBS prices fell, leveraged investors faced margin calls, forcing them to sell into a falling market.

For mortgage REITs with non-Agency exposure, this proved fatal. Several well-known names failed to meet margin calls and entered distress. For most of 2020, the mortgage real estate investment trust (REIT) sector followed the arc of a turnaround story. These stocks were beaten up badly in the early days of the novel coronavirus pandemic, and many became insolvent. AGNC Investment navigated the crisis better than most of its peers.

AGNC's Survival: Agency Focus Vindicated

AGNC's pure Agency focus proved its worth during the COVID crisis. While non-Agency mortgage REITs faced credit concerns on top of liquidity pressures, AGNC's government-guaranteed portfolio meant the company only had to manage market risk—not credit risk.

Fortunately, our portfolio is comprised almost entirely of Agency MBS, which enjoy the guarantee of timely interest and principal from the GSEs. As a result, we have very little credit exposure in our portfolio, which is where the bulk of the future uncertainty lies.

The company's strong liquidity position entering the crisis also proved crucial. The total of the $3.5 billion that we had on March 31st plus the $1.2 billion at Bethesda, which is all cash in from Agency MBS and then the $300 million non-agencies totaled $5 billion and that was 54% of our capital. So we actually had—at the end of March, we ended the crisis period on a percentage basis with more cash in unencumbered equity.

AGNC Investment ended 2019 with a tangible book value per share of $17.66. By the end of the first quarter of 2020 (March 31), it had fallen to $13.62. Since then, however, AGNC has been able to rebuild it, reaching $17.22 in tangible book value per share at the end of this year's first quarter. On this basis, AGNC has fully recovered from the damage the COVID-19 crisis did to its balance sheet. AGNC was able to do that via a combination of asset price recovery, income on investments, and stock buybacks. The company purchased around $650 million (or 7.5% of shares outstanding) at a discount to book value.

Despite surviving, the COVID crisis did force painful decisions. During 2020, AGNC cut its monthly dividend from $0.15 to $0.12 per share. This 20% dividend cut was the company's way of preserving capital and flexibility during extraordinary uncertainty.

The Fed's Massive Intervention

The Federal Reserve's response to the COVID crisis dwarfed even the post-2008 interventions. The Federal Reserve began conducting its fourth quantitative easing operation since the 2008 financial crisis; on March 15, 2020, it announced approximately $700 billion in new quantitative easing via asset purchases to support US liquidity in response to the COVID-19 pandemic. As of mid-summer 2022 this resulted in an additional $2 trillion in assets on the books of the Federal Reserve.

According to the latest data, the Fed increased its MBS holdings by more than $178 billion from May 6 to May 13 of 2020. The Federal Reserve purchased nearly $180 billion in Mortgage-Backed Securities last week, more than any week in history—including during the housing crisis.

This unprecedented intervention stabilized Agency MBS markets rapidly. On March 23, the Federal Reserve announced the FOMC would purchase agency MBS "in the amounts needed to support smooth market functioning." The Fed's action tightened agency MBS spreads to nearly pre-crisis levels. We find that the Fed's actions helped stabilize the agency mREIT industry.

For AGNC, the Fed's intervention was salvation. Spreads normalized, repo markets reopened, and the company's book value began recovering almost immediately. By Q1 2021, AGNC had fully recovered from the COVID damage—a remarkable turnaround that validated both the Agency-focused strategy and the company's liquidity management.

VIII. Key Inflection Point #5: The 2022-2023 Rate Shock

The Most Aggressive Rate Hiking Cycle in Decades

Just as AGNC recovered from COVID, the Federal Reserve embarked on the most aggressive rate-hiking cycle in four decades to combat inflation.

In March 2022, the Federal Reserve started to aggressively increase interest rates from a range of 0.25-0.50% to 5.25-5.50% by the summer of 2023.

For mortgage REITs, this was another worst-case scenario. Rising rates meant:

- Mark-to-market carnage: MBS prices fell dramatically as rates surged.

- Inverted yield curve: Short-term funding costs actually exceeded long-term MBS yields for extended periods.

- Spread widening: MBS underperformed Treasuries again.

- Volatility surge: Rate volatility made hedging more expensive and less precise.

Mortgage REITs, meanwhile, saw the value of their portfolios, as reflected in their book value, crushed during this period. For example, AGNC saw its book value decline by nearly -50% from the start of 2022 until the end of 2023.

The chart shows a history of the spread between the MBS yield and the Treasury yield. The wider the yield, the lower AGNC's book value. At present, a wider spread than during The Financial Crisis and COVID! Yet, AGNC is still upright. Bloodied and bruised, yes, but alive.

Dividend History: The Uncomfortable Truth

The 2022-2023 rate shock brought into sharp relief the fundamental tension in AGNC's investment proposition: phenomenal income generation alongside persistent capital erosion.

As of today, AGNC annual dividend per share is $1.44, unchanged on December 31, 2024. During the last 3 years, AGNC annual dividend per share has risen by $0.00 (0.00%). AGNC annual dividend per share is now -74.29% below its all-time high of $5.60, reached on December 31, 2010.

Consider the math: at the 2010 peak, AGNC was paying $5.60 in annual dividends per share. Today, it pays $1.44—a 74% reduction over 15 years. Yet the company has distributed more than $49 per share in cumulative dividends since inception, against a current stock price around $10.

This creates what some call the "dividend trap" narrative. High yields attract income investors, but if book value and stock price decline over time, investors who spend their dividends (rather than reinvesting) end up with less capital and less income.

From a total return perspective—reinvesting dividends—AGNC has performed reasonably well over its history. But from a pure income perspective—spending dividends as received—the story is more complicated. The monthly check keeps shrinking as the company reduces dividends to match its reduced earning power.

Leadership Transition

In July 2021, amidst these challenging conditions, AGNC completed a planned leadership transition. Peter Federico has served as our Chief Investment Officer since March 2025, as a Director and our Chief Executive Officer since July 2021, and as our President since March 2018. He previously served as our Chief Operating Officer from March 2018 until July 2021, as Executive Vice President and Chief Financial Officer from July 2016 until March 2018.

The AGNC management team is led by Peter Federico, our President and Chief Executive Officer, and Christopher Kuehl, our Executive Vice President and Chief Investment Officer. Following our successful leadership transition in July 2021, Gary Kain, previously our Chief Executive Officer and Chief Investment Officer, now serves as Executive Chair of our Board of Directors. Messrs. Federico, Kuehl, and Kain collectively have over 90 years of experience investing in MBS and have worked together at AGNC for the last 12 years.

Like Gary Kain before him, Peter Federico brought deep GSE experience to AGNC. Prior to joining AGNC Investment Corp., Mr. Federico served as Executive Vice President and Treasurer of Freddie Mac from October 2010 through May 2011, where he was primarily responsible for managing the company's investment activities for its retained portfolio and developing, implementing and managing risk mitigation strategies. He was also responsible for managing Freddie Mac's $1.2 trillion interest rate derivative portfolio and short- and long-term debt issuance programs. Mr. Federico also served in a number of other capacities at Freddie Mac, including as Senior Vice President, Asset & Liability Management, during his tenure with the company, which began in 1988.

This represented remarkable continuity—a 23-year Freddie Mac veteran taking over from a former Freddie Mac Senior VP. The Freddie Mac DNA runs deep at AGNC.

IX. Modern Era & Current State (2024-2025)

Recovery Mode

By 2024, conditions began improving for AGNC. The Fed's rate-hiking cycle ended, and expectations shifted toward rate cuts. Spread volatility declined. The yield curve began normalizing.

Against this improved investment backdrop, AGNC generated a positive economic return of 13.2% in 2024, driven by our compelling monthly dividend. Our 2024 performance provides investors a good example of AGNC's ability to generate strong investment returns in environments in which Agency MBS spreads are wide and stable. Moreover, AGNC provides investors with access to this unique and attractively valued fixed income asset class on a levered basis through an investment vehicle that has produced best-in-class returns since inception.

Management stated: "Entering 2025, we continue to have a very positive outlook for Agency MBS, supported by the increasingly favorable environment that emerged in 2024. The Federal Reserve finally shifted its restrictive monetary policy stance and began the process of returning short term rates to a neutral level. With declining inflationary pressures and accommodative monetary policy, interest rate volatility eased during the year, and the yield curve steepened after being inverted for the second longest episode on record. In addition, with primary mortgages rates again near 7%, the supply of Agency MBS should continue to be limited and reasonably well-aligned with investor demand. Lastly, and perhaps most importantly to our business, Agency MBS spreads to benchmark rates remain in a well-defined range and offer levered and unlevered investors very attractive return opportunities."

The most recent quarterly results reflect this improved environment. AGNC reported $764 million in net income available to common stockholders for the three months ended September 30, 2025, up from $313 million in the same period in 2024, highlighting increased profitability. The net income per common share (basic) was $0.73 for the three months ended September 30, 2025, compared to $0.39 for the same period in 2024. The net income per common share (diluted) was $0.72 for the three months ended September 30, 2025, compared to $0.39 for the same period in 2024.

In 2024, AGNC Investment's revenue was $973.00 million, an increase of 287.65% compared to the previous year's $251.00 million. Earnings were $731.00 million, an increase of 2184.38%.

15-Year Anniversary Milestone

In 2023, AGNC marked a significant milestone—15 years as a publicly traded company.

We had the honor of ringing the Nasdaq opening bell to commemorate AGNC's 15-year listing anniversary. Since AGNC's IPO in 2008, we have successfully navigated a range of market cycles while producing exceptional long-term total returns for our stockholders, significantly outperforming the Bloomberg Mortgage REIT Index, the S&P 500 Financials Index, and the S&P 500 Real Estate Index.

That 15-year track record encompasses the 2008 financial crisis aftermath, three rounds of quantitative easing, the 2013 taper tantrum, the COVID-19 liquidity crisis, and the 2022-2023 rate shock. Not many financial entities can claim survival—let alone relative outperformance—across such a gauntlet of challenges.

Current Portfolio Positioning

As of the most recent reporting, AGNC's portfolio remains heavily weighted toward Agency MBS. As of December 31, 2024, the portfolio reached $73.3 billion, primarily in Agency RMBS. By March 31, 2025, the portfolio further increased to $78.9 billion.

The company continues to maintain substantial liquidity. With leverage around 7.5x and a captive broker-dealer providing advantaged funding, AGNC is positioned to navigate continued market volatility while generating income for shareholders.

X. Playbook: Business & Investing Lessons

The Mortgage REIT Playbook

Lesson 1: Crisis Creates Opportunity

AGNC's founding during the 2008 crisis demonstrates how distressed markets can offer asymmetric returns. The key insight was distinguishing credit risk from interest rate risk: Agency MBS offered crisis-level spreads without actual credit risk. Investors who recognized this difference could profit from panic sellers who were treating all mortgage products as radioactive.

The broader lesson: in panic-driven selloffs, assets are often mispriced relative to their fundamental risk. Those who understand the nuances can find opportunity where others see only danger.

Lesson 2: Structural Advantages Matter

AGNC's two main structural advantages—pure Agency focus eliminating credit risk, and captive broker-dealer reducing funding costs—aren't easily replicable by competitors. AGNC is one of a handful of mREITs that has an exclusive "captive" broker-dealer. It holds that deal with Bethesda Securities—a member of FICC and FINRA—to gain access to lower wholesale funding rates and lower collateral requirements than other mREITs that have non-captive deals.

These may seem like small operational details, but in a spread business where margins are measured in tens of basis points, a funding cost advantage of 10-15 basis points can mean meaningfully higher returns over time.

Lesson 3: Yield ≠ Return

This is perhaps the most important lesson for income investors. High dividend yield does not guarantee positive total return. AGNC has paid enormous cumulative dividends, but its stock price has declined significantly over time.

For investors who reinvest dividends, AGNC's total return has been competitive with benchmarks. For investors who spend dividends, the experience has been more mixed—gradually declining income on gradually declining capital.

The lesson isn't that AGNC is a bad investment—it's that investors must be clear about their investment thesis. Is this a total return vehicle or an income vehicle? The answer dramatically affects how you should think about the stock.

Lesson 4: Fed Policy is Everything

Mortgage REITs are, at their core, Fed policy trades wrapped in REIT tax structure. When the Fed is buying MBS and suppressing rate volatility (QE1-3, COVID response), mortgage REITs flourish. When the Fed is hiking rates and shrinking its balance sheet (2013 taper, 2022-2023 tightening), mortgage REITs suffer.

This doesn't make mortgage REITs "bad"—but it does mean investors must have a view on Fed policy direction to form a view on mortgage REIT prospects.

Competitive Analysis: AGNC vs. Annaly

AGNC Investment Corp. and Annaly Capital Management are two of the biggest names within the mortgage real estate investment trusts industry. Both offer favorable long-term returns to stockholders, along with a substantial dividend yield, but differ in their portfolio strategies and risk profiles.

AGNC Investment is the purest agency mortgage REIT out there. It invests almost exclusively in government-guaranteed mortgage-backed securities. This means AGNC takes almost no credit risk. If the borrower on one of the underlying mortgages stops paying, the government will ensure that AGNC gets all of its scheduled principal and interest payments.

Annaly has positioned itself to better withstand interest rate volatility through its diversified portfolio, particularly with its investments in MSR, and residential and commercial credit assets. Given this, the increase in NLY's borrowing costs was lower than that of AGNC.

The choice between AGNC and Annaly essentially comes down to purity vs. diversification:

- AGNC: Pure Agency focus means no credit risk but full exposure to interest rate and spread dynamics.

- Annaly: Diversified portfolio including mortgage servicing rights (which gain value when rates rise) provides natural hedging but introduces credit risk.

Neither approach is objectively "better"—they represent different risk/return tradeoffs suited to different investor preferences and market views.

Porter's Five Forces Analysis

Threat of New Entrants: Low-Moderate Entry barriers include regulatory requirements, capital intensity, and the need for sophisticated risk management capabilities. However, anyone with sufficient capital can enter—the "moat" is operational rather than structural.

Buyer Power: Low AGNC buys Agency MBS in deep, liquid markets. No single seller has pricing power.

Supplier Power: Moderate Funding through repo markets involves relationships with major banks and dealers. While funding is generally available, terms can tighten dramatically during crises (as seen in March 2020).

Threat of Substitutes: High Investors seeking yield have many alternatives: traditional REITs, high-dividend stocks, bonds, CDs. When CD rates approach mortgage REIT yields (as occurred in 2023), capital can flow elsewhere.

Industry Rivalry: High Mortgage REITs compete primarily on yield and perceived safety. There's limited ability to differentiate on the asset side—Agency MBS is Agency MBS. Competition focuses on funding costs, hedging efficiency, and track record.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Moderate. Larger portfolios may provide slightly better funding terms and operational efficiency, but the benefits are limited.

Network Effects: None. This is not a network business.

Counter-Positioning: AGNC's pure Agency focus could be considered counter-positioning vs. diversified competitors—but it's more strategic choice than sustainable advantage.

Switching Costs: None. Investors can switch between mortgage REITs with no friction.

Branding: Limited. AGNC has brand recognition among income investors, but brand doesn't command premium pricing.

Cornered Resource: Bethesda Securities (the captive broker-dealer) is a genuine cornered resource providing funding advantages. Management expertise from former Freddie Mac executives is another.

Process Power: AGNC's risk management processes have been proven through multiple crises. This institutional knowledge is a genuine advantage but could be replicated by competitors over time.

Assessment: AGNC has limited durable competitive advantages in the Helmer framework. Its primary moats are operational (captive broker-dealer, management expertise) rather than structural. This is consistent with the commodity-like nature of Agency MBS investing.

Key Performance Indicators to Track

For investors monitoring AGNC's ongoing performance, three KPIs stand out as most critical:

1. Net Interest Spread (excluding premium amortization) This measures the core profitability of the spread trade. Watch for trends in funding costs vs. asset yields. Compression suggests earnings pressure; expansion suggests improving conditions.

2. Tangible Book Value Per Share This is the most important balance sheet metric. Mortgage REITs typically trade around book value, so changes in book value directly impact stock price potential. Persistent book value declines signal capital destruction.

3. Economic Return on Tangible Common Equity This combines dividend payments with book value changes to show total shareholder return. A positive economic return means shareholders are getting paid even if book value is flat or slightly declining; a negative economic return means capital destruction is exceeding dividend income.

Material Risks and Regulatory Considerations

Interest Rate Risk: AGNC is fundamentally an interest rate play. Material rate movements—especially rapid ones—can significantly impact book value regardless of hedging.

Fed Policy Risk: Changes in Fed MBS holdings or purchase policies directly affect Agency MBS valuations and spreads.

Regulatory Risk: Mortgage REITs operate under complex regulations governing REITs, leverage, and financial counterparties. Changes to these rules could impact operations.

GSE Reform Risk: Any changes to Fannie Mae, Freddie Mac, or their guarantee structures could fundamentally alter the Agency MBS market. While reform has been discussed for over a decade without action, it remains a tail risk.

Liquidity Risk: During market stress, repo funding can become unavailable or prohibitively expensive. March 2020 demonstrated this risk clearly.

Myth vs. Reality

| Common Narrative | Reality Check |

|---|---|

| "AGNC is a bond fund in REIT clothing" | Partially true. AGNC invests in fixed income (MBS) but uses leverage and hedging strategies that make it behave very differently from a bond fund. The REIT structure provides tax efficiency but creates 90% distribution requirements that limit capital retention. |

| "High yield means high risk" | Nuanced. AGNC's yield is high partly due to leverage and partly due to its required REIT distributions. The credit risk on Agency MBS is near-zero due to government guarantees—but interest rate and spread risks are very real. |

| "Mortgage REITs failed in 2020" | Some did, many didn't. Non-Agency focused REITs faced margin calls they couldn't meet. Agency-focused REITs like AGNC survived. The asset quality distinction matters enormously. |

| "Declining dividend means the company is failing" | Incomplete. AGNC's dividend has declined from $5.60 annually (2010) to $1.44 today. But this reflects changed market conditions (lower spreads, higher funding costs) rather than operational failure. The company has survived every major crisis since 2008. |

Final Thoughts

AGNC Investment Corp. stands as one of the financial sector's most fascinating case studies. Born into crisis, surviving through multiple market catastrophes, and distributing nearly $50 per share in dividends over 17 years—all while its stock price declined by roughly half.

Is that success or failure? The answer depends entirely on why you own it.

For total return investors who reinvested dividends, AGNC has provided competitive returns through a remarkably volatile period. For income investors who spent dividends on living expenses, the experience has been more challenging—gradually declining income on gradually declining capital.

The company's pure Agency focus remains both its greatest strength and its defining constraint. By eliminating credit risk, AGNC achieves a kind of operational purity that few financial entities can match. But that same purity means no escape from interest rate and spread dynamics—when Agency MBS struggles, AGNC struggles, regardless of management quality.

Looking forward, AGNC's prospects depend heavily on Fed policy, yield curve shape, and MBS spread dynamics. In an environment of stable or declining rates, moderate volatility, and wide spreads, AGNC can generate attractive income. In an environment of rising rates, elevated volatility, and compressing spreads, AGNC will face headwinds.

The management team—with combined experience exceeding 90 years in MBS markets—has navigated every conceivable challenge. The captive broker-dealer provides genuine funding advantages. The track record of crisis survival speaks for itself.

But ultimately, AGNC is a bet on the American mortgage market wrapped in a tax-efficient structure and amplified by leverage. For investors comfortable with that proposition—and clear-eyed about the income vs. total return distinction—it remains one of the most accessible ways to express a view on Agency MBS.

For everyone else, there's always Realty Income.

XI. The Total Return vs. Income Debate Revisited

Understanding the Paradox

The tension between AGNC's extraordinary dividend history and its declining share price deserves deeper examination. This paradox sits at the heart of how investors should think about mortgage REITs—and indeed, about income investing more broadly. The distinction between total return and income investing proves critical to understanding AGNC's value proposition. On a stock price-only basis, AGNC Investment's price is down about 50% from its IPO. Total return, which assumes dividend reinvestment, is hugely positive at a gain of over 400%.

This divergence illuminates one of the most important—and often misunderstood—dynamics in income investing. The mortgage REIT isn't designed to generate income so much as to provide a strong total return. The dividend is just a part of the total return equation.

The company's management has been transparent about this distinction. Since its inception through the end of 2024, its total return averaged about 10% a year. It's hard to complain about that, given that 10% is the return that most investors expect from the broader stock market.

The Income Investor's Dilemma

Given that most dividend investors are likely trying to live off of the dividends they collect, which effectively means they are being spent, AGNC Investment would have left dividend investors with less income and a smaller nest egg. That is not a good outcome.

This observation cuts to the heart of the yield trap. Retirees attracted by double-digit yields who spend those dividends rather than reinvesting them face a compounding problem: as book value erodes and dividends get cut, both their income stream and their remaining capital shrink over time.

If you are a long-term dividend investor seeking reliable income, it's hard to imagine how AGNC Investment would fit well in your portfolio for any extended length of time. It isn't a bad company, but it isn't a long-term income stock, and AGNC management is very open about that fact.

The Sector-Wide Challenge

On average mortgage REIT prices have fallen 4.4% annually. For the ten years ending May 31, 2024, the FTSE Nareit All Mortgage REIT Index, a measure of mortgage REIT performance, returned 2.1% annualized. That is much lower than the 7.5% 10-year annualized return through December 31, 2021.

This broader industry context is essential. AGNC's challenges aren't unique—they reflect the fundamental economics of the mortgage REIT business model. They are highly leveraged, and that leverage has led to volatility in the dividend, which has impacted mortgage REIT returns. While a double-digit dividend is attractive, the total returns for mortgage REITS have fallen short of the dividend yield with long-term annualized returns of 6%.

mREITs had a dividend yield of 12.65% at the end of 2024 compared to 3.96% for equity REITs. mREITs paid a cumulative $5.9 billion in dividends by the third quarter of 2024. mREITs struggled in 2024 from a total return perspective, finishing the year with an annual return of 0.36% as interest rates remained high and property market transactions were low.

XII. Most Recent Performance and Forward Outlook

Q2 and Q3 2025 Results

The most recent financial results provide a snapshot of AGNC's current operating environment. On July 21, 2025, AGNC Investment Corp. reported its financial results for the second quarter of 2025. AGNC Investment Corp. reported a comprehensive loss of $0.13 per common share for Q2 2025, comprising a net loss of $0.17 per share and $0.05 other comprehensive income. Net spread and dollar roll income was $0.38 per common share, excluding a $0.01 catch-up premium amortization benefit.

Tangible net book value per common share decreased 5.3% to $7.81 from $8.25, yielding a -1.0% economic return, driven by $0.36 dividends and a $0.44 decline in book value. The investment portfolio totaled $82.3 billion, including $73.3 billion in Agency MBS and $8.3 billion in TBA securities, with leverage at 7.6x tangible net book value.

The Q1 2025 results showed improvement from a challenging Q4 2024. The company reported comprehensive income per share of $0.12, economic return of 2.4%, and net spread and dollar roll income of $0.44 per share. These figures represent a positive turnaround from Q4 2024, when the company experienced a comprehensive loss and negative economic return.

Average asset yield increased to 4.87% from 4.80% in the previous quarter, while average repo cost decreased significantly from 4.86% to 4.45%. The average cost of funds also declined from 2.89% to 2.75%, contributing to improved net interest margins.

Scale and Capital Position

AGNC continues to operate at significant scale. The company maintained its attractive 15.0% dividend yield while growing its asset base to $78.9 billion, up from $73.3 billion at the end of 2024.

AGNC has maintained a strong market position with $9.1 billion in market capitalization and has paid $14.3 billion in total dividends since its IPO in May 2008.

The dividend has remained stable. The dividend has been held at the same level since a cut in 2020. At $0.12 per month, or $1.44 annually, the dividend represents management's judgment about sustainable distributions given the current operating environment.

XIII. The Broader Significance: AGNC and the American Housing System

The Shadow Banking Narrative

AGNC represents more than just an investment vehicle—it embodies a fundamental shift in how American housing gets financed. Before 2008, banks originated mortgages and often held them on their balance sheets. The financial crisis accelerated a transformation where mortgages increasingly move from origination into securitized pools, with entities like AGNC serving as permanent capital pools absorbing this supply.

mREITs help provide essential liquidity for the real estate market. mREITs invest in residential and commercial mortgages, as well as residential mortgage-backed securities (RMBS) and commercial mortgage-backed securities (CMBS). mREITs typically focus on either the residential or commercial mortgage markets, although some invest in both RMBS and CMBS.

mREITs play an important role in single family home financing. Nareit estimated that mREITs helped finance 1 million homes in the U.S.

This creates an interesting dynamic: every time an American takes out a mortgage, there's a reasonable probability that AGNC ends up owning a slice of that debt. The company provides private capital to support homeownership—a function that might otherwise fall more heavily on government balance sheets or bank portfolios.

The Fed's Dance Partner

AGNC's trajectory has been inextricably linked to Federal Reserve policy. During QE, the Fed and mortgage REITs were essentially buying the same assets—Agency MBS. The Fed's massive purchases supported prices, compressed volatility, and created a favorable operating environment. When the Fed shifts to quantitative tightening, the dynamic reverses.

This creates a peculiar relationship. AGNC profits when the Fed is actively intervening in mortgage markets, yet that intervention is typically triggered by crisis conditions that threaten financial stability. The golden ages for mortgage REITs (2009-2012, post-COVID) corresponded to periods of economic distress that prompted extraordinary monetary policy.

Conversely, periods of "normal" monetary policy—positive short-term rates, modest balance sheet, limited intervention—tend to compress mortgage REIT spreads and returns. The sector thrives in abnormal times.

XIV. Conclusion: The AGNC Investment Paradox

AGNC Investment Corp. embodies a fascinating paradox of modern finance: extraordinary income generation alongside persistent capital erosion, crisis survival alongside peacetime challenges, phenomenal dividend track record alongside a declining share price.

The numbers tell the story in stark relief. Since May 2008, the company has distributed nearly $50 per share in cumulative dividends—more than five times the current stock price. For total return investors who reinvested those distributions, the result has been competitive with broader market indices. For income investors who spent those distributions, the experience has been one of gradually declining income on gradually declining capital.

Neither narrative is wrong—they simply reflect different investment objectives and approaches to the same underlying business.

The management team, with combined experience exceeding 90 years in MBS markets, has navigated every conceivable challenge: the aftermath of the 2008 financial crisis, three rounds of quantitative easing, the 2013 taper tantrum, the COVID-19 liquidity crisis, and the 2022-2023 rate shock. The pure Agency focus has proven its value in crisis after crisis, eliminating credit risk and ensuring survival when non-Agency competitors faced existential threats.

The captive broker-dealer provides genuine funding advantages. The internalized management structure aligns incentives with shareholders. The operational infrastructure has been stress-tested through multiple market cycles.

But fundamentally, AGNC remains a leveraged bet on Agency MBS spreads, which in turn depends heavily on Federal Reserve policy, yield curve dynamics, and interest rate volatility. The company cannot escape these fundamental exposures—it can only manage them with varying degrees of skill.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube