Fluence Energy: Powering the Grid Storage Revolution

I. Introduction: The Unlikely Champion

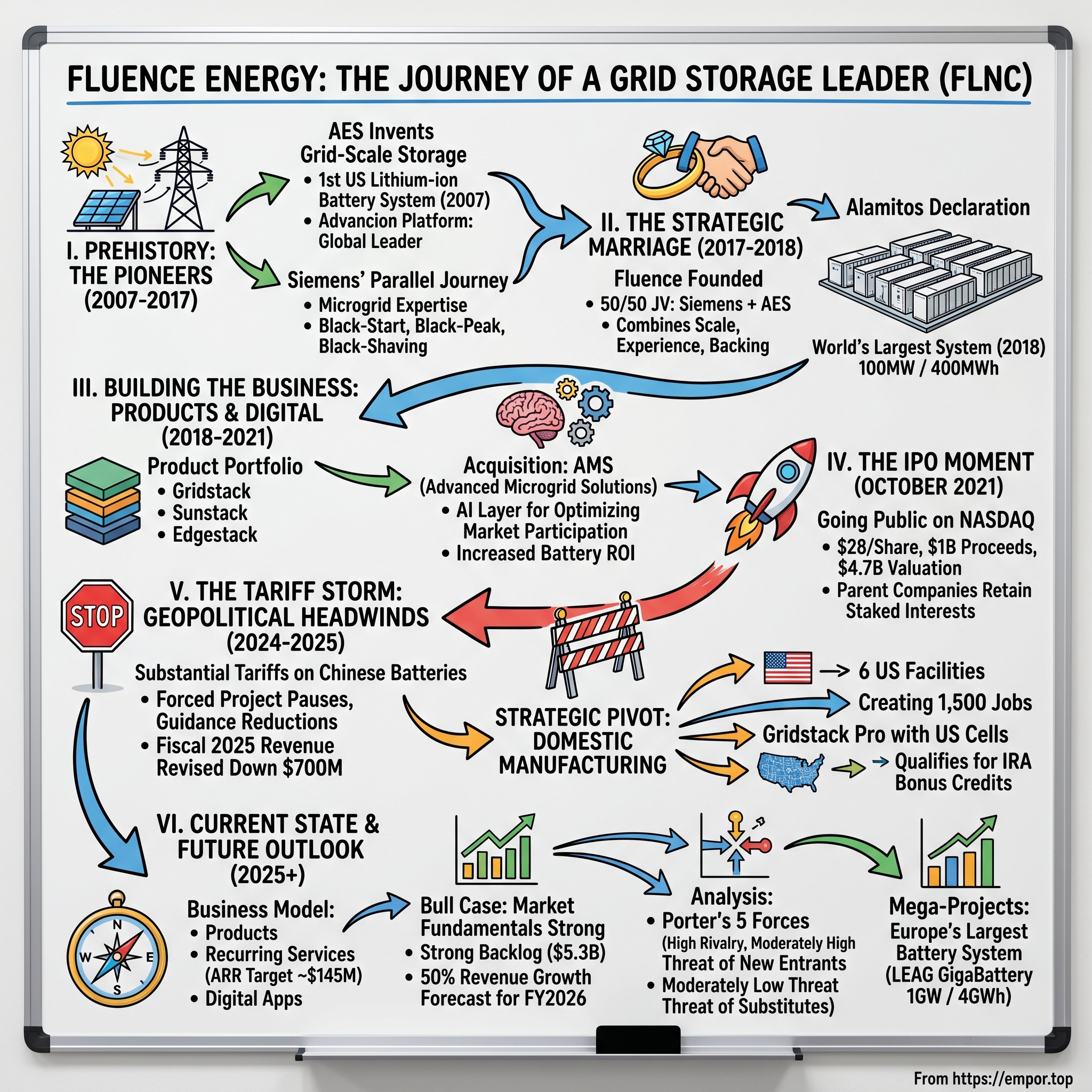

On a humid summer afternoon in Long Beach, California, the hum of the world's largest lithium-ion battery system filled the air. Nestled within AES's Alamitos power center, 400 megawatt-hours of stored electricity stood ready to dispatch power to Southern California's grid at a moment's notice—no fossil fuels, no emissions, just electrons flowing from chemistry to copper. This 100 MW/400 MWh installation, deployed in 2018, was then the largest lithium-ion battery-based energy storage system in North America. It was also a declaration of intent from a fledgling company born of an unusual corporate marriage.

Fluence Energy is the result of two industry powerhouses and pioneers in energy storage joining together to form a new company dedicated to innovating modern electric infrastructure. In January 2018, Siemens and AES launched Fluence, uniting the scale, experience, breadth, and financial backing of the two most experienced icons in energy storage.

The question that would define Fluence's trajectory: How did a joint venture between two legacy energy giants—one a German industrial conglomerate with roots stretching back to the age of telegraphs, the other an American power producer born in the Reagan era—become a pure-play bet on the grid storage revolution?

The answer emerges in Fluence's fiscal year 2025 financial results. Revenue reached $2.3 billion for fiscal year 2025 and $1.0 billion for the fourth quarter, with GAAP gross profit margin improving to approximately 13.1% for fiscal year 2025 and approximately 13.7% for the fourth quarter. The market strength is evidenced by the total backlog increasing 18% year-over-year to a record $5.3 billion, driven by $1.4 billion in Q4 order intake.

Fluence operates as a global market leader delivering intelligent energy storage and optimization software for renewables and storage. With gigawatts of projects successfully contracted, deployed, and under management across nearly 50 markets, the company is transforming the way we power our world for a more sustainable future.

Yet the path has been anything but smooth. The company faces formidable headwinds—substantial tariffs on Chinese batteries, which are expected to reach 155.9% in calendar year 2025 and 173.4% in 2026. This has forced project pauses, guidance reductions, and strategic pivots that would test the resolve of even the most seasoned management teams.

This is the story of Fluence Energy—a company that didn't just ride the energy storage wave but helped create it. It's a tale of corporate strategy, technological evolution, and the high-stakes gamble that domestic manufacturing might prove to be the ultimate competitive moat in an industry increasingly shaped by geopolitical forces.

II. The Prehistory: AES Invents Grid-Scale Storage (2007-2017)

Before there was Fluence, there was a bet placed in the desert.

In 2007, when the iPhone was still a novelty and Tesla was selling sports cars to Silicon Valley elites, engineers at AES Corporation were working on something that seemed equally improbable: connecting lithium-ion batteries to an electric grid. Fluence originated from AES' work to conceive and test the world's first lithium-ion energy storage system connected to an electric grid in 2007.

Prior to the formation of Fluence, AES had been pioneering grid-scale energy storage since 2007, when it installed the first grid-scale lithium-ion battery energy storage system in the United States. This wasn't a publicity stunt or a research project buried in some corporate R&D division. AES, a Fortune 500 power producer with operations spanning continents, was making a calculated bet that batteries would eventually compete with natural gas turbines.

The logic was elegant in its simplicity: solar panels produce power when the sun shines, wind turbines spin when the breeze blows, but consumers flip light switches according to their schedules, not nature's. The grid needed a buffer—a giant shock absorber that could soak up renewable energy during periods of abundance and release it during periods of scarcity.

The Advancion Platform Emerges

AES branded its storage technology "Advancion," and over the next decade, the company accumulated experience that no competitor could match. "Over the past ten years, AES has become a global leader in utility-scale, battery-based energy storage. Today AES' Advancion platform is present in seven countries with more than 200 MW of energy storage deployed, including the largest installed system of its kind in the world," said Andrés Gluski, AES President and CEO.

Two hundred megawatts might seem modest by today's standards, where gigawatt-scale projects are announced quarterly. But in the early 2010s, this represented the frontier of what was technologically and economically feasible. Each installation taught AES lessons that couldn't be learned in a laboratory: how batteries degrade in desert heat, how to manage thermal runaway risks, how to integrate storage systems with legacy grid infrastructure, and how to extract maximum revenue from volatile wholesale electricity markets.

Siemens' Parallel Journey

While AES was pioneering utility-scale deployments, Siemens—the German engineering behemoth—was approaching energy storage from a different angle. Siemens brings its experience in microgrid and islanding applications, renewable hybrid technology, black-start capability, and consumer peak shaving, building on its intimate knowledge of customer power needs as a leading global original equipment manufacturer.

Where AES knew how to operate storage assets and extract value from electricity markets, Siemens understood the hardware—power electronics, thermal management, safety systems—and commanded a global sales force with relationships spanning more than 160 countries. The two companies were mirror images: operationally rich but geographically limited versus technically sophisticated but operationally inexperienced.

AES brings its deep expertise in utility-scale battery-based energy storage solutions for flexible peaking capacity, ancillary services such as frequency regulation, transmission and distribution reliability, and renewable integration applications dating back a decade and representing several of the largest energy storage installations in the world.

Why Storage Mattered

The strategic insight driving both companies was the same: the energy transition wasn't just about building more solar panels and wind farms. It was about fundamentally rewiring how electricity flows from generators to consumers. In a world powered predominantly by renewables, energy storage would become the backbone of the grid—the technology that makes everything else work.

"Almost 15 years ago, AES started working on developing lithium-ion battery systems to improve the efficiency and flexibility of the grid and enable the broader expansion of renewables," said Andrés Gluski, AES President and CEO. "In 2018, we joined together with Siemens to create Fluence to drive global adoption of energy storage systems."

By 2017, both companies recognized that going it alone would mean slower growth and missed opportunities. The question became: what if they combined forces?

For investors, the prehistory matters because it established the operational DNA that Fluence inherited. This wasn't a startup pivoting toward energy storage based on market trends. It was a company built on fifteen years of accumulated know-how, failure analysis, and customer relationships—assets that don't show up on balance sheets but prove decisive in a capital-intensive, relationship-driven industry.

III. The Strategic Marriage: Birth of Fluence (2017-2018)

The announcement came in September 2017, packaged in the carefully crafted language of corporate press releases. But beneath the boilerplate lay a transaction with genuinely transformative potential.

Siemens AG and The AES Corporation announced their agreement to form a new global energy storage technology and services company under the name Fluence. The joint venture would bring together AES' ten years of industry-defining experience deploying energy storage in seven countries with over a century of Siemens' energy technology leadership and its global sales presence in more than 160 countries.

The Architecture of a Joint Venture

Siemens and AES would have joint control of the company with each holding a 50 percent stake. Fluence's global headquarters would be located in the Washington, DC area with additional offices located in Erlangen, Germany and select cities worldwide.

The 50-50 structure was no accident. It signaled that this wasn't an acquisition with a dominant parent and a subordinate target. Both companies were committing capital, intellectual property, and personnel as equal partners—a governance arrangement that would create its own challenges but also its own advantages.

The company name "Fluence" was chosen to represent the confluence of forces that are transforming the global electricity sector. The branding team had earned their fees: "fluence" evoked both influence and confluence, suggesting a company positioned at the intersection of multiple powerful trends.

What Each Partner Contributed

AES and Siemens were currently ranked among the leading energy storage integrators worldwide by Navigant Research. Together, the two companies had deployed or been awarded 48 projects totaling 463 MW of battery-based energy storage across 13 countries, including the world's largest lithium-ion battery-based energy storage project near San Diego, California.

The asset inventory told only part of the story. AES contributed something harder to quantify but potentially more valuable: operational data from years of running storage systems in real-world conditions. This data—recording how batteries performed across thousands of charge-discharge cycles, how ambient temperatures affected degradation rates, how software configurations influenced revenue capture—would become the foundation for Fluence's AI-powered optimization platform.

Siemens contributed the Siestorage platform and, perhaps more importantly, customer relationships. Utilities and independent power producers around the world already bought turbines, transformers, and grid equipment from Siemens. Adding energy storage to that relationship was a natural extension.

The Alamitos Declaration

The joint venture announced its intentions with characteristic ambition. At launch, Fluence deployed the then-largest lithium-ion battery-based energy storage system in North America—the 100 MW/400 MWh installation in Long Beach, California at AES' Alamitos power center.

Alamitos wasn't just a commercial project; it was a statement piece. At 400 megawatt-hours, the installation could power roughly 120,000 homes for several hours—enough capacity to demonstrate that batteries could compete with natural gas "peaker" plants that utilities traditionally relied upon to meet surging afternoon demand.

The Logic of Combination

"As the energy storage market expands, customers face the challenge of finding a trusted technology partner with an appropriate portfolio and a profound knowledge of the power sector. Fluence will fill this major gap in the market. With the global reach of an experienced international sales force as well as Siemens' leading technology platform Siestorage at its disposal, Fluence will be perfectly equipped to serve this very interesting market," said Ralf Christian, CEO of Siemens' Energy Management Division.

The strategic logic was compelling: AES knew how to make money from storage; Siemens knew how to sell complex infrastructure globally. Together, they could offer customers something no competitor could match—a proven technology stack backed by a century of combined energy experience and the financial heft of two investment-grade corporations.

Fluence operates backed by its parent companies, industry giants Siemens and AES, to deliver the scale and staying power customers can rely on. In an industry where projects span decades and customers need confidence that their technology partner will still exist when warranties expire, this backing proved to be a decisive competitive advantage.

For investors evaluating Fluence today, the JV origins matter because they explain the company's unusual DNA. Fluence isn't a Silicon Valley startup with venture capital DNA and a move-fast-break-things culture. Nor is it a sleepy utility subsidiary. It's a hybrid—nimble enough to innovate rapidly but backed by institutional credibility that opens doors with the most conservative utility customers.

IV. Building the Business: Products, Acquisitions & Digital Strategy (2018-2021)

The years between Fluence's formation and its IPO were a period of rapid evolution. The company wasn't content to simply integrate its inherited product lines; it systematically built capabilities across hardware, software, and services—creating an ecosystem designed to capture value at every stage of a storage project's lifecycle.

The Product Portfolio Takes Shape

Fluence designs, deploys, and provides ongoing services for utility-scale energy storage systems, including their flagship Gridstack™, Sunstack™, and Edgestack™ product lines.

The product naming conventions reflected a deliberate segmentation strategy. Gridstack targeted the front-of-the-meter utility market—the mega-projects that grab headlines. Sunstack was designed for solar-plus-storage installations, where batteries are paired directly with photovoltaic arrays. Edgestack addressed smaller commercial and industrial applications.

This portfolio approach allowed Fluence to serve the full spectrum of storage use cases while maintaining standardized component architectures that drove manufacturing efficiencies.

The Advanced Microgrid Solutions Acquisition: Building the AI Layer

In October 2020, Fluence made a move that would prove prescient: acquiring Advanced Microgrid Solutions (AMS), a California company known for its artificial intelligence-driven optimization software.

AMS' technology uses artificial intelligence, advanced price forecasting, portfolio optimization and market bidding to ensure energy storage and flexible generation assets are responding optimally to price signals sent by the market. AMS' and Fluence's technologies together will act as a force multiplier, maximizing asset value by combining Fluence's deep experience operating batteries in the field with AMS' ability to optimize market participation.

"AMS has developed one of the most powerful AI-enabled software engines available in the industry," said Brett Galura, chief technology officer at Fluence.

The acquisition economics were compelling. The combination of Fluence's sixth generation tech stack, which can reduce balance of system costs for energy storage by up to 25 percent, with AI-enabled software that can increase revenue from battery energy storage by more than 100 percent, maximizes the ROI of energy storage.

The market bidding software was currently available in the U.S. in the California ISO (CAISO) and in Australia's National Electricity Market (NEM), where it optimized over 15 percent of Australia's wind and solar resources, with plans to expand to additional markets.

The Strategic Logic of Software

"Fluence's announcement that it has acquired AMS illustrates how system integrators are diversifying through a clear digital strategy and advanced software capabilities," Julian Jansen, research manager for energy storage at IHS Markit, said. "Investors are pouring into the energy storage space, but as projects rely on volatile merchant revenue stream, creating a digital proposition that centres around asset optimisation will help differentiate in a crowded, cost sensitive market."

The AMS acquisition signaled Fluence's understanding of a crucial dynamic: as battery hardware commoditizes, the margins would shift to software. A storage system that simply sits there storing and dispatching energy is valuable. A storage system that uses machine learning to anticipate wholesale electricity price spikes, optimize bidding strategies, and maximize revenue capture is exponentially more valuable.

The acquisition formed the foundation of Fluence's digital business, which has since developed the Fluence IQ Platform. In 2021, Fluence further expanded its digital capabilities with the acquisition of Nispera AG, a provider of AI-enabled renewable energy management software, which was integrated into the Fluence Mosaic offering.

The Qatar Investment Authority Investment

In December 2020, Fluence secured validation from one of the world's most sophisticated institutional investors.

Fluence announced that it had entered into a definitive agreement with the Qatar Investment Authority (QIA) pursuant to which QIA would commit to invest $125 million in Fluence through a private placement transaction.

The $125 million, in exchange for a 12 percent stake, valued Fluence at more than $1 billion, a rare achievement for the energy storage sector.

Fluence intended to use the net proceeds from the private placement to further accelerate development of its product offerings, particularly digital products, and deployment of existing products in more markets globally.

Fluence does not manufacture batteries; rather, it packages them into complete power plants with power electronics, safety equipment, energy management systems and digital controls.

This last point deserves emphasis. Fluence deliberately chose not to compete in cell manufacturing—a brutally competitive market dominated by Asian giants like CATL and LG. Instead, it positioned itself as a system integrator, sourcing cells from multiple suppliers and adding value through engineering, software, and services. This asset-light model preserved capital for growth while avoiding direct competition with vertically integrated battery manufacturers.

For investors, the pre-IPO period established the strategic architecture that defines Fluence today: a hardware-agnostic integrator with a growing software moat and a recurring revenue model built on long-term service contracts. The acquisitions weren't random bolt-ons; they were deliberate capability buildouts designed to create defensible competitive advantages.

V. The IPO Moment: Going Public (October 2021)

By late 2021, the energy storage market was entering what would become its breakout period. Battery costs had fallen roughly 90% over the preceding decade. The Biden administration had just taken office with ambitious climate commitments. Utilities across the developed world were announcing net-zero targets that would require massive storage deployments.

Fluence chose this moment to go public.

On October 27, 2021, Fluence announced the pricing of its initial public offering of 31,000,000 shares of its Class A common stock at a price to the public of $28.00 per share.

Fluence closed its initial public offering of 35,650,000 shares of its Class A common stock, including the exercise in full of the underwriters' option to purchase additional shares, at an initial public offering price of $28.00 per share. Proceeds from the initial public offering were $998.2 million, before deducting underwriting discounts and commissions and other offering expenses.

The pricing valued Fluence at approximately $4.7 billion.

The IPO Context

Since launching in 2018, Fluence had made waves on the energy storage market, especially with its digital platform designed to maximize bidding on the wholesale markets so providers can take full advantage of renewable and storage assets. In 2020, Fluence acquired AI firm Advanced Microgrid Solutions (AMS) to boost its management platform.

At IPO, Fluence had more than 3.4 GW of energy storage deployed or contracted in 29 markets globally, and more than 4.5 GW of wind, solar and storage assets optimized or contracted in Australia and California.

The IPO syndicate reflected the deal's importance: J.P. Morgan Securities LLC, Morgan Stanley, Barclays Capital Inc., and BofA Securities acted as joint lead book-running managers for the offering.

The Parent Company Dynamic

One unusual aspect of the IPO was the continued presence of the parent companies. Upon completion of Fluence's offering, AES would have an indirect economic interest in Fluence of approximately 35% (or approximately 34% if the underwriters exercised their option to purchase additional Class A shares). Fluence would be a "controlled company" within the meaning of the Nasdaq rules, and AES would have approximately 46% of the voting power in Fluence.

This structure gave Fluence the benefits of public market access—capital, liquidity, currency for acquisitions—while retaining the strategic alignment and financial backing of its parent companies. For risk-averse utility customers, the continued involvement of Siemens and AES provided reassurance that Fluence wasn't just another venture-backed startup that might disappear.

Market Reception and Early Performance

The IPO occurred during a period of intense investor enthusiasm for clean energy stocks. ESG mandates were driving institutional capital toward companies with sustainability credentials. The energy storage sector, in particular, was attracting attention as a pure-play bet on grid decarbonization.

The company was formed by two industry giants and pioneers in the field of energy storage—German engineering company Siemens and American power company AES—and combines the scale, experience, breadth and financial support of two of the most experienced leaders in the field of energy storage. The team has over 13 years of experience deploying and operating energy storage.

Fluence intended to use the net proceeds from the offering to repay debts and for general corporate purposes.

For long-term investors, the IPO moment established important baseline metrics. The $4.7 billion valuation at $28 per share represented a bet on rapid growth in a nascent market. Whether that valuation proves justified depends on Fluence's ability to convert its technological and operational advantages into sustainable profitability—a challenge that would prove more complex than the IPO euphoria suggested.

VI. The Business Model Deep Dive

Understanding how Fluence actually makes money requires peeling back layers of complexity. The company operates at the intersection of hardware manufacturing, software development, and industrial services—a combination that creates both opportunities and challenges.

Revenue Streams: The Three-Legged Stool

Fluence does not manufacture batteries; rather, it packages them into complete power plants with power electronics, safety equipment, energy management systems and digital controls.

The business model rests on three interconnected revenue streams:

1. Energy Storage Products and Solutions — The largest revenue contributor involves designing, engineering, and delivering complete battery energy storage systems. Fluence procures battery cells from suppliers (primarily CATL and AESC), integrates them with power electronics and thermal management systems, and delivers turnkey solutions to utility and commercial customers.

2. Recurring Services — Once systems are deployed, Fluence offers ongoing operational and maintenance services. These contracts typically span multiple years and provide predictable recurring revenue with attractive margins. The service relationship also creates switching costs—once a customer relies on Fluence for system monitoring and maintenance, transitioning to a competitor becomes operationally disruptive.

3. Digital Applications — The company offers the Fluence IQ™ digital platform, which includes Bidding Application and Fluence Mosaic™ for optimizing renewable energy assets. These software products generate subscription revenue independent of hardware sales and can be sold to customers who don't use Fluence storage systems.

The Digital Moat

The Fluence IQ platform uses machine learning to optimize system decision-making, manage battery degradation, and maximize dispatch revenue in volatile electricity markets—a critical edge over hardware-only competitors.

The digital layer deserves particular attention because it represents Fluence's most defensible competitive advantage. Every storage system Fluence deploys generates operational data—millions of data points capturing how batteries perform under real-world conditions. This data feeds machine learning models that improve bidding algorithms, predict degradation patterns, and optimize dispatch decisions.

The more systems Fluence deploys, the more data it collects. The more data it collects, the smarter its algorithms become. The smarter its algorithms become, the more value it delivers to customers. This creates a virtuous cycle that's difficult for competitors to replicate without comparable operational scale.

The Integration Model: Why Fluence Doesn't Make Cells

A strategic choice that defines Fluence's business model is the decision to remain a system integrator rather than backward-integrating into cell manufacturing.

Fluence has secured multi-year agreements with AESC, which is ramping up domestically manufactured cells for Fluence now. Moreover, the company is actively broadening its supply base beyond China.

This choice reflects cold economic logic. Cell manufacturing is a scale-intensive, capital-hungry business where Chinese manufacturers like CATL have established overwhelming cost advantages. By remaining supplier-agnostic, Fluence can source cells from whichever manufacturer offers the best combination of price, quality, and supply security—including domestic U.S. suppliers when tariff economics favor them.

Annual Recurring Revenue: The Key Metric

The Company reaffirmed its fiscal year 2025 annual recurring revenue ("ARR") guidance of approximately $145 million.

ARR has become a crucial metric for evaluating Fluence's business quality. Unlike one-time hardware sales, recurring revenue from services and software creates predictable cash flows and higher margins. The growth of ARR relative to total revenue indicates the company's success in building a more durable business model.

Product Evolution: From Gridstack to Smartstack

Fluence continues to invest heavily in product development, with the February 2025 launch of Smartstack representing the latest generation.

Fluence announced Smartstack™, a high-density, AC-based energy storage platform, now commercially available for grid-scale applications worldwide with customer deliveries scheduled to begin in the last quarter of 2025.

The platform is designed to maximize project site density and deliver approximately 30% higher energy density than other leading AC-based solutions.

Smartstack's patent-pending design strategically splits battery storage systems into units with easily transportable weight and dimensions, reducing shipping constraints and installation complexity.

For investors, the business model creates a complex picture. The hardware business drives revenue but faces margin pressure as the market matures and competitors intensify. The services and software businesses offer better unit economics but require continued investment to maintain technological leadership. The key question is whether Fluence can grow recurring revenue fast enough to offset inevitable margin compression in hardware.

VII. The Competitive Landscape: Giants & Challengers

Fluence operates in one of the most intensely competitive markets in the energy sector. The prize—becoming the dominant supplier of grid-scale energy storage—has attracted some of the world's largest and most sophisticated companies.

The Global Leaderboard

Tesla retained its top spot for the second year in a row as lead producer in the battery energy storage system (BESS) integrator market with a 15% market share in 2024, according to Wood Mackenzie's Global battery energy storage system integrator ranking 2025 report. While Tesla maintained its crown, Chinese competitor Sungrow significantly narrowed the gap, holding onto second place with 14% market share—reducing Tesla's lead from 4 percentage points in 2023 to just 1 percentage point in 2024.

CRRC rounded out the top three with 8% market share, maintaining the same podium positions for the second straight year.

Seven of the global top 10 BESS integrators are now headquartered in China, reflecting the country's growing influence in the sector.

The Tesla Factor

Tesla remains Fluence's most formidable competitor, particularly in the North American market. Tesla remained the largest player in North America with a 39% market share.

Tesla's advantages are significant: vertical integration (it manufactures its own cells at Gigafactory Nevada), brand recognition, and the ability to leverage manufacturing scale across automotive and energy divisions. Tesla's Megapack product has become the default choice for many large-scale projects, particularly those seeking to capitalize on the brand's consumer recognition.

Chinese Competition: The Rising Tide

Intense domestic competition and oversupply have forced Chinese companies to expand aggressively into overseas markets, particularly Europe and the Middle East.

The growth in China-headquartered companies was particularly seen in Europe, where they increased their market share by 67% year-on-year and now make up four out of the ten largest suppliers. Sungrow led this charge, doubling its market share from 10% in 2023 to 21% in 2024 to become the largest supplier in Europe.

Chinese manufacturers like Sungrow, BYD, and CATL benefit from massive domestic market scale, integrated supply chains, and government support. Their cost advantages are substantial—often 15-30% below Western competitors on comparable systems.

Fluence's Position

In North America, Tesla, Sungrow and Fluence remained market leaders in 2023. The three vendors captured 72% of the region's market share for BESS shipments in 2023, growing 20% YoY in the percentage.

In Europe, the top five are Sungrow, Fluence, Nidec ASI, Tesla, SMA Altenso.

Market Dynamics: Fragmentation vs. Consolidation

In 2024, the energy storage market was rapidly restructuring. Leading companies increased their market share through cost control and strong distribution, while smaller players struggled with price competition and limited funding, leading to industry consolidation.

Chinese firms saw opposite fortunes in North America, where their market share fell from 23% to 16%, mainly due to escalating US-China geopolitical tensions and trade barriers.

The Competitive Moat Analysis

Fluence's competitive position rests on several factors:

-

Operational Track Record: With 15+ years of deployment experience inherited from AES, Fluence can credibly claim more operational data than any competitor except Tesla.

-

Software Differentiation: The Fluence IQ platform provides optimization capabilities that hardware-only competitors cannot match.

-

Parent Company Backing: As a joint venture between Siemens and AES, Fluence benefits from established industry connections, financial stability, and a global presence in nearly 50 markets.

-

Domestic Content Strategy: Fluence's early investments in U.S. manufacturing position it favorably as tariffs reshape competitive dynamics.

Myth vs. Reality: Is Energy Storage a Commodity?

A common misconception is that battery storage systems are increasingly commoditized, with competition primarily on price. Reality is more nuanced.

While battery cells themselves have become more commodity-like, complete systems involve significant engineering complexity. Integration with grid infrastructure, compliance with local regulations, thermal management design, and software optimization all create meaningful differentiation opportunities.

"Energy storage capacity prices are currently approximately $9 per kilowatt a month, which is about half the price of a gas fired plant," noted Fluence CEO Julian Nebreda.

The pricing comparison to gas plants—not to competing battery systems—suggests that storage economics are increasingly competitive with traditional generation, expanding the total addressable market even as supplier competition intensifies.

VIII. The Tariff Storm: Navigating Geopolitical Headwinds (2024-2025)

In the spring of 2025, Fluence faced its most severe test since going public. The culprit wasn't technological failure or competitive pressure—it was the Trump administration's trade policy.

The Challenge Emerges

The most significant factor affecting Fluence's outlook is the substantial tariffs on Chinese batteries, which are expected to reach 155.9% in calendar year 2025 and 173.4% in 2026.

"The evolving trade and tariff landscape has created significant uncertainty in the U.S. market, which has led us to agree with our customers during the second quarter to pause certain contracts both under execution and those we expected to sign until we have better visibility," said Fluence CEO Julian Nebreda.

The tariff escalation represented a fundamental disruption to Fluence's business model. The company had historically sourced a significant portion of its battery cells from Chinese manufacturers like CATL, leveraging their cost advantages to deliver competitive pricing to customers. With tariffs approaching 156%, that calculus became untenable.

The Financial Impact

Total fiscal year 2025 revenue was revised to be in the range of $2.6 billion to $2.8 billion (midpoint $2.7 billion), down from the previous range of $3.1 billion to $3.7 billion (midpoint $3.4 billion). This $700 million reduction at the midpoint was primarily attributable to mutual decisions made during the second quarter by the Company and its customers to pause U.S. projects under existing contracts.

The company reported a 31% decline in revenue for the quarter ending March 2025 compared with 2024, receiving approximately $431.6 million, down from $623.1 million. Fluence reported a net loss of approximately $41.9 million, a significant increase compared to its $12.9 million loss in the same period last year.

The Company lowered its fiscal year 2025 Adjusted EBITDA guidance to a range of $0 to $20 million (midpoint $10 million), from the prior range of $70 million to $100 million (midpoint $85 million). This reduction was primarily driven by the anticipated impact on Adjusted EBITDA from the $700 million reduced revenue outlook as well as an approximate $20 million anticipated incremental impact from the recently enacted U.S. tariffs.

The Domestic Content Response

Rather than simply absorbing tariff-related losses, Fluence accelerated a strategic pivot that management had been planning for years.

The company has established six production facilities across the United States, creating over 1,500 jobs. This integrated supply chain includes manufacturing operations for enclosures, modules, chillers, cells, inverters, and communication equipment.

Gridstack Pro is available with US-manufactured 305Ah LFP cells produced in an existing factory in Tennessee—enabling Fluence to bring domestic content systems to market in early 2025. First, Fluence has already been proactive in securing domestically manufactured cells that align with current Inflation Reduction Act (IRA) domestic content requirements.

The Strategic Positioning

From a competitive standpoint, Fluence believes these changes could ultimately strengthen the company's market position. The company's early investments in domestic supply chains and its ability to provide products meeting IRA domestic content requirements may give it a distinct advantage over competitors more heavily reliant on Chinese imports.

The domestic content strategy serves multiple purposes. First, it insulates Fluence from tariff exposure—systems assembled with U.S.-manufactured cells and modules aren't subject to Chinese tariffs. Second, it qualifies projects for the Inflation Reduction Act's domestic content bonus, which can add 10 percentage points to the base 30% investment tax credit. Third, it positions Fluence ahead of potential further trade restrictions.

The 90-Day Pause

Taking into account battery-specific tariffs, the move temporarily reduced the combined duty on Chinese battery energy storage systems (BESS) or batteries for BESS from 155.9% to 40.9% right now, rising to 58.4% on January 1, 2026 when a higher Section 301 tariff kicks in. At 155.9%, the US BESS market was essentially 'frozen', sources told Energy-Storage.news.

The tariff pause provided temporary relief but didn't eliminate underlying uncertainty. Customers remained hesitant to commit to long-term projects without clarity on final tariff levels.

Navigating Through the Storm

As of March 31, 2025, the company had total liquidity of $1,142 million, including $610 million in cash and $532 million in availability under working capital facilities.

The Company reaffirmed its fiscal year 2025 revenue guidance range of $2.6 billion to $2.8 billion, but expected to be at the lower end of the range due to a slower than expected production ramp up at its recently commissioned U.S. manufacturing facilities. This delay shifted some anticipated revenue to fiscal year 2026. These facilities were expected to reach targeted capacity by calendar year-end, ensuring on-time customer deliveries and strengthening Fluence's domestic content position.

For investors, the tariff crisis reveals both the vulnerability and the resilience of Fluence's business model. The vulnerability is clear: geopolitical forces beyond management's control can dramatically impact near-term results. The resilience lies in management's response—pivoting to domestic manufacturing faster than competitors, maintaining strong liquidity, and positioning for potential long-term advantages from the very policy that created short-term pain.

IX. Playbook: Business & Strategic Lessons

The Fluence story offers several lessons for investors analyzing capital-intensive technology businesses in politically sensitive industries.

Lesson 1: The Joint Venture Playbook

Fluence demonstrates that joint ventures between corporate giants can create genuinely innovative entities, not just bureaucratic hybrids. The keys to success:

- Clear complementary capabilities (AES's operational experience + Siemens' technology and sales reach)

- Equal governance preventing one partner from dominating

- Independent operational structure allowing startup-like agility

- Continued parent company support without micromanagement

Backed by parent companies, industry giants Siemens and AES, Fluence can deliver the scale and staying power customers can rely on.

Lesson 2: Vertical Integration vs. Specialization

Fluence's choice to be an integrator rather than a cell manufacturer reflects a deliberate strategic calculus. In an industry where battery cell manufacturing is dominated by Asian giants with massive scale advantages, attempting to compete on cells would have required billions in capital expenditure with uncertain returns.

Instead, Fluence focuses on higher-value activities: system design, software optimization, and operational services. This preserves capital while targeting segments where differentiation is more sustainable.

Lesson 3: Software as a Moat

The acquisitions of Advanced Microgrid Solutions and Nispera weren't random bolt-ons—they were deliberate investments in defensible competitive advantages. As hardware commoditizes, software becomes the primary source of differentiation and margin.

AI-enabled software can increase revenue from battery energy storage by more than 100 percent—a capability that hardware-only competitors cannot match.

Lesson 4: Domestic Content as Competitive Advantage

Fluence's early investments in U.S. manufacturing, which may have seemed financially suboptimal when Chinese imports were cheap, now look prescient. Management's willingness to sacrifice near-term margins for supply chain resilience has positioned the company advantageously as tariff dynamics reshape the competitive landscape.

Lesson 5: Capital Discipline Under Pressure

Maintaining total liquidity of $1,142 million, including $610 million in cash, despite challenging conditions demonstrates management's understanding that surviving industry disruptions requires financial flexibility. Companies that lever up during good times often find themselves unable to weather storms.

X. Analysis: Porter's Five Forces & Hamilton's Seven Powers

Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-HIGH

The energy storage market has moderate barriers to entry. High capital requirements and technical complexity create meaningful hurdles, but they're not insurmountable. In 2024, the energy storage market was rapidly restructuring. Leading companies increased their market share through cost control and strong distribution, while smaller players struggled with price competition and limited funding, leading to industry consolidation.

Chinese manufacturers have demonstrated that scale economics and aggressive pricing can rapidly gain market share. New entrants with deep pockets (automotive OEMs, major utilities, sovereign-backed companies) pose ongoing threats.

2. Bargaining Power of Suppliers: HIGH

Fluence's dependence on battery cell manufacturers creates meaningful supplier power. CATL and EVE Energy remained the top two energy storage cell makers with orders from major customers like Tesla and Fluence.

With a handful of manufacturers controlling the majority of global cell production, and with cells representing the largest cost component of storage systems, supplier dynamics significantly influence Fluence's margins and supply security.

Mitigation: Fluence has diversified its supplier base and established domestic sourcing partnerships, but supplier concentration remains a structural challenge.

3. Bargaining Power of Buyers: MODERATE

Fluence's customers are large, sophisticated utilities and developers with significant negotiating leverage. However, the limited number of Tier 1 suppliers with proven track records provides some balance. Switching costs exist due to integration complexity and the importance of long-term service relationships.

4. Threat of Substitutes: LOW-MODERATE

Alternative storage technologies (pumped hydro, compressed air, hydrogen, flow batteries) exist but face limitations that make lithium-ion the preferred choice for most grid applications. Record lows of $115/kWh in 2024 firmly repositioned LFP as the anchor chemistry for long-duration BESS.

Over longer time horizons, emerging technologies could disrupt lithium-ion dominance, but near-term substitution risk appears limited.

5. Competitive Rivalry: HIGH

Competition is intense and intensifying. Tesla's scale, Chinese manufacturers' cost advantages, and the entry of new players create sustained pricing pressure. Market share battles across regions suggest that no competitor has yet established dominance.

Hamilton's Seven Powers Analysis

1. Scale Economies: EMERGING

As of 2023, Fluence employs approximately 1,595 people across more than 40 countries and has deployed or contracted over 20 GW of energy storage and energy optimization projects globally.

Scale provides procurement advantages and operational leverage, but Fluence hasn't yet achieved the dominant scale position that would create a durable moat. Tesla and Chinese competitors possess comparable or greater scale in relevant segments.

2. Network Effects: LIMITED

Fluence's software platform generates more value as it collects more operational data, creating a form of data network effect. However, this isn't a true network effect in the Facebook/Uber sense—the value to one customer doesn't directly increase because other customers use the platform.

3. Counter-Positioning: MODERATE

Fluence's early focus on domestic sourcing positions the company favorably. As one of the first movers in establishing significant domestic production capacity, Fluence stands to benefit.

Fluence is counter-positioned against Chinese competitors on domestic content. Competitors heavily reliant on Chinese supply chains would face significant costs and delays to match Fluence's U.S. manufacturing footprint.

4. Switching Costs: MODERATE

Long-term service contracts, software integration, and operational familiarity create meaningful switching costs. Once a utility standardizes on Fluence systems and software, transitioning to a competitor involves real costs and risks.

5. Branding: MODERATE

The Siemens and AES parentage provides credibility. In an industry where customers need confidence that suppliers will honor long-term warranties and support commitments, the parent company backing enhances Fluence's brand relative to smaller competitors.

6. Cornered Resource: LIMITED

Fluence doesn't possess proprietary technology or exclusive access to critical resources. Its advantages derive from accumulated know-how and relationships rather than protected resources.

7. Process Power: EMERGING

Fifteen years of operational experience have created process advantages that competitors cannot easily replicate. Knowledge accumulated from thousands of battery cycles across diverse climatic conditions feeds into design improvements and operational optimizations.

XI. Bull vs. Bear Case

Bull Case

1. Market Fundamentals Remain Strong

The United States Energy Storage Market size in terms of installed base is expected to grow from 49.52 gigawatt in 2025 to 131.75 gigawatt by 2030, at a CAGR of 21.62% during the forecast period.

Energy storage installations around the world are projected to reach a cumulative 411 gigawatts (or 1,194 gigawatt-hours) by the end of 2030. That is 15 times the 27GW/56GWh of storage that was online at the end of 2021.

The underlying demand drivers—renewable energy integration, grid reliability needs, AI data center power requirements—remain intact regardless of near-term tariff disruptions.

2. Domestic Content Advantage

Fluence's domestic manufacturing investments position it to capture market share as tariffs reshape competitive dynamics. Customers seeking IRA domestic content bonuses and tariff-insulated supply chains have limited alternatives.

3. Strong Backlog Provides Visibility

The total backlog increased 18% year-over-year to a record $5.3 billion, driven by $1.4 billion in Q4 order intake. This substantial order book provides unprecedented revenue predictability, covering 85% of the midpoint of the projected $3.4 billion to $3.6 billion revenue guidance for fiscal year 2026.

4. Software/Services Growth

Recurring revenue from services and digital applications is growing faster than hardware revenue and carries superior margins. As this segment scales, overall profitability should improve.

5. Fiscal 2026 Guidance

"With approximately 85% of our revenue forecast already secured in our backlog and a record liquidity position, we are confident in our ability to deliver 50% revenue growth for fiscal year 2026."

Bear Case

1. Profitability Concerns

Total Revenue was $2,262.8 million for fiscal year 2025, a decrease of 16.1% from the previous year, primarily due to lower average prices and project delays. Gross Profit was $295.8 million, a decrease of 13.3% from the previous year. Net Loss was $67.989 million, compared to net income of $30.367 million in the previous year.

Despite growing revenue, Fluence has struggled to generate consistent profits. Hardware margins face ongoing pressure from competition.

2. Tariff Uncertainty Persists

The 90-day tariff pause doesn't eliminate structural uncertainty. Policy could swing dramatically depending on U.S.-China relations and election outcomes, making long-term planning difficult.

3. Chinese Competition Intensifies

Intense domestic competition and oversupply have forced Chinese companies to expand aggressively into overseas markets.

Chinese manufacturers continue to gain share in Europe and other non-U.S. markets. Their cost advantages remain substantial, and potential easing of U.S.-China tensions could reignite price competition in the U.S.

4. Cash Flow Challenges

Fiscal year 2025 was marked by a 16% revenue decline to $2.3 billion, a shift to a $68.0 million net loss, and a significant use of $145.5 million in operating cash flow. Strong top-line successes were overshadowed by operational failures that saw Adjusted EBITDA plunge 75% and operating cash flow swing negatively by $225 million due to a massive inventory build.

5. Manufacturing Execution Risk

Ramping domestic manufacturing capacity involves execution risk. Delays in scaling new manufacturing facilities in the U.S. resulted in lower-than-expected revenue for the quarter.

Key Metrics to Watch

For investors monitoring Fluence, the following KPIs are most critical:

1. Order Backlog and Conversion Rates The ~$5 billion backlog provides visibility, but what matters is conversion velocity. Watch quarterly order intake and backlog-to-revenue conversion rates. Stagnant or declining backlogs would signal demand problems; accelerating conversion rates would indicate improving execution.

2. Adjusted Gross Margin Trend Current guidance targets mid-teens adjusted gross margins. Margin expansion would validate the software/services strategy and pricing power. Margin compression would signal commoditization pressures.

3. Domestic Content Mix as Percentage of U.S. Revenue As domestic manufacturing scales, the proportion of U.S. revenue from domestic content products should increase. This metric indicates progress in insulating the business from tariff exposure.

XII. Recent Developments & Future Outlook

As 2025 draws to a close, Fluence has secured what may be the most significant contract in its history.

The LEAG Mega-Project

LEAG Clean Power GmbH and Fluence Energy GmbH will build Europe's largest battery energy storage system, a 1 GW / 4 GWh system in Jänschwalde, Germany, underlining their role as energy technology leaders in Europe. The GigaBattery Jänschwalde 1000 project will be powered by Smartstack™, Fluence's advanced energy storage solution.

The 1 GW / 4 GWh battery energy storage system will be Fluence's largest single storage project globally to date.

According to information provided by LEAG, the GigaBattery project is expected to break ground after the completion of the approval process in the second quarter of next year (May/June). Commissioning is tentatively planned for late 2027 or early 2028.

The LEAG project validates several aspects of Fluence's strategy. First, it demonstrates the competitiveness of Smartstack, the company's latest platform, against global alternatives. Second, it shows Fluence's strong position in Europe, where it has established leadership outside the tariff-affected U.S. market. Third, the scale—4 GWh of storage capacity—represents the kind of mega-project that only Tier 1 integrators can execute.

Smartstack: The Next Generation

Smartstack's innovative architecture strategically splits systems into easily transportable units, reducing shipping constraints and installation complexity. The platform is designed to maximize project site density and deliver approximately 30% higher energy density than other leading AC-based solutions.

The new partner manufacturing facility in Vietnam is a significant component of Fluence's strategy to expand production capability and uphold quality assurance. With a projected annual manufacturing capacity of 35 GWh, the facility features a fully automated production process designed to enhance productivity and safety while delivering world-class product quality.

Customer deliveries for Smartstack are scheduled to begin in the last quarter of calendar year 2025.

Market Growth Trajectory

The broader energy storage market continues its rapid expansion. BloombergNEF expects additions to grow 35% this year, setting a record for annual additions, at 94 gigawatts (247 gigawatt-hours), excluding pumped hydro. The bumper year will be followed by a compound annual growth rate of 14.7% through to 2035.

AI Data Center Demand

A potentially transformative demand driver is the buildout of AI infrastructure. Data centers powering large language models and other AI applications require enormous, reliable power supplies. Energy storage provides both backup power and the ability to smooth demand spikes—making storage increasingly attractive to hyperscale data center operators.

European Market Expansion

The growth in China-headquartered companies was particularly seen in Europe, where they increased their market share by 67% year-on-year. Sungrow led this charge.

Despite Chinese competition, Fluence maintains a strong position in Europe. In Europe, the top five are Sungrow, Fluence, Nidec ASI, Tesla, SMA Altenso.

The LEAG project reinforces Fluence's European leadership and provides a reference installation for future mega-scale opportunities.

Fiscal 2026 Outlook

Management has expressed confidence in the year ahead. "With approximately 85% of our revenue forecast already secured in our backlog and a record liquidity position, we are confident in our ability to deliver 50% revenue growth for fiscal year 2026."

The combination of backlog coverage, improving domestic manufacturing capabilities, and stabilizing (though still uncertain) tariff dynamics suggests fiscal 2026 could mark a return to growth. Whether that growth translates to profitability depends on execution—particularly the successful ramp of domestic production and the continued growth of higher-margin services revenue.

Conclusion: The Energy Storage Inflection Point

Fluence Energy stands at a critical inflection point—both for the company and for the industry it helped create. Fifteen years after AES engineers connected the first lithium-ion battery to an electric grid, energy storage has moved from experimental technology to essential infrastructure. The question is no longer whether batteries will transform the grid, but which companies will dominate the transformation.

Fluence enters this phase with significant advantages: decades of operational experience, a growing software moat, strategic parent company backing, and first-mover positioning in domestic U.S. manufacturing. It also faces substantial challenges: intense competition from Tesla and Chinese manufacturers, margin pressure in hardware, and geopolitical uncertainty that could swing tariff policy unpredictably.

For long-term investors, the core thesis centers on whether Fluence can execute the transition from a hardware-centric to a software-and-services business while navigating near-term disruptions. The backlog provides visibility, the domestic content strategy provides protection, and the market growth provides opportunity. Whether management can convert these advantages into sustainable profitability will determine whether Fluence becomes a defining company of the energy transition or another casualty of the industry's brutal competitive dynamics.

The grid storage revolution is real. Fluence's role in that revolution remains to be fully written.

Material Regulatory and Accounting Considerations

Tariff Exposure: Fluence has material exposure to U.S. trade policy regarding Chinese batteries. Changes to Section 301 tariffs, AD/CVD determinations, and IRA domestic content rules could significantly impact margins and competitive positioning.

Revenue Recognition: Large-scale storage projects involve complex revenue recognition across design, manufacturing, delivery, installation, and commissioning phases. Investors should monitor changes in revenue recognition patterns and deferred revenue balances.

Warranty Obligations: Long-term performance guarantees create potential liability. The company provides warranties on system performance extending up to 25 years for certain products.

Related Party Transactions: As a controlled company with significant parent company involvement, investors should monitor related party transactions with AES and Siemens.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube