DT Midstream: The Pure-Play Pipeline Story

I. Introduction: From Detroit's Basements to America's Pipelines

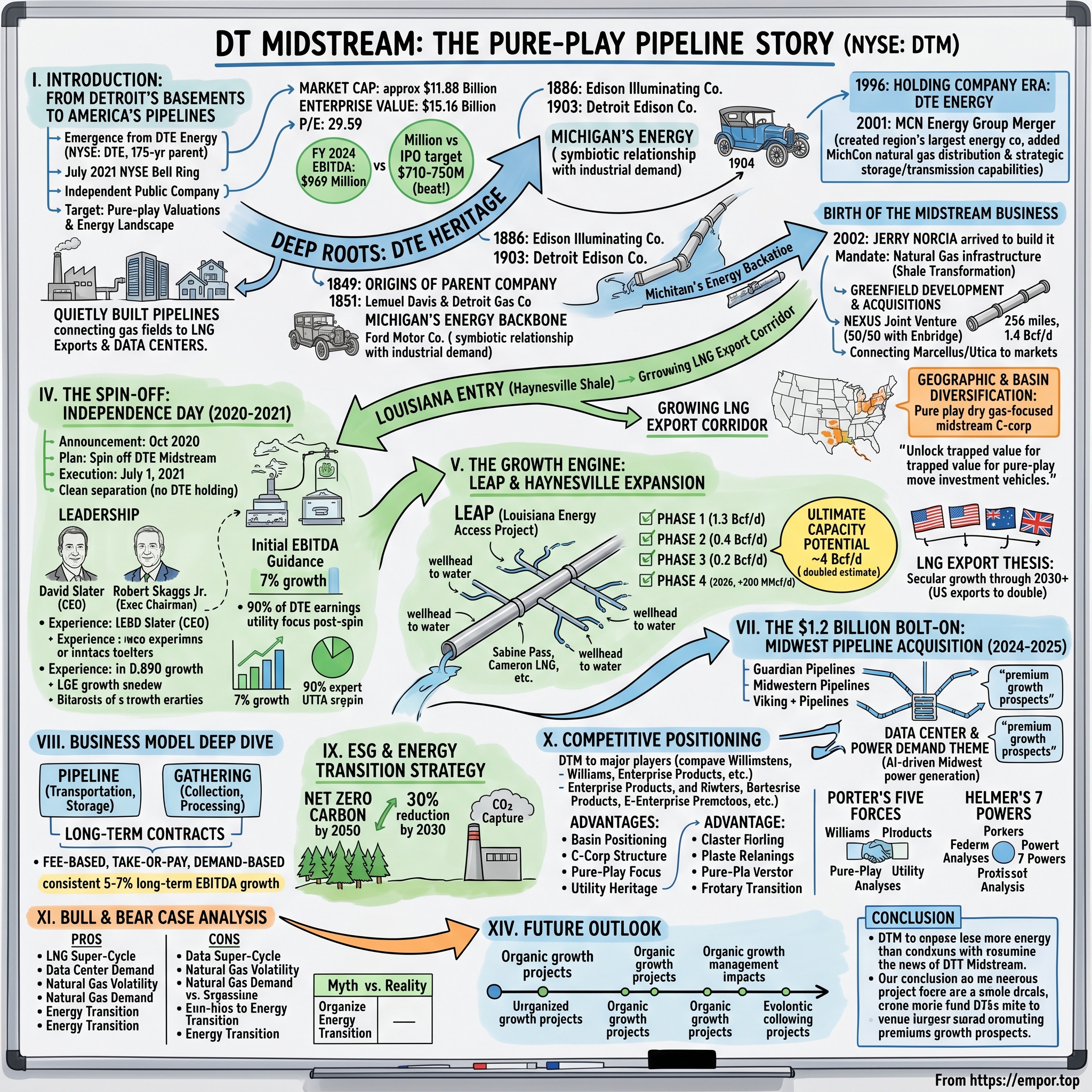

On a crisp July morning in 2021, the New York Stock Exchange bell rang for a company that most Americans had never heard of—yet one that quietly underpinned their ability to heat their homes, power their factories, and increasingly, run the data centers storing their photos, emails, and everything else digital. DT Midstream (NYSE: DTM) emerged from the shadow of its 175-year-old parent, DTE Energy, to begin life as an independent publicly traded company.

DT Midstream, Inc., a premier natural gas pipeline, storage and gathering provider, debuted as an independent, publicly traded company after successfully completing its separation from DTE Energy. The spin-off marked more than a corporate restructuring—it represented the culmination of nearly two decades of patient infrastructure building, the pursuit of pure-play valuations, and a strategic bet on America's evolving energy landscape.

Today, DT Midstream trades with a market capitalization of approximately $11.88 billion, an enterprise value of $15.16 billion, and a trailing P/E ratio of 29.59. For context, when the company went public, it targeted adjusted EBITDA of $710-750 million. By full year 2024, the company achieved adjusted EBITDA of $969 million, raised its dividend by 12%, and increased its 2025 adjusted EBITDA guidance.

But the DT Midstream story is about more than financial metrics. It's about how a regulated utility in Detroit—a city synonymous with automotive manufacturing rather than energy infrastructure—quietly built a portfolio of pipelines stretching from the Appalachian shale fields to the Louisiana bayous, connecting some of America's most prolific natural gas basins to the insatiable demand of LNG export terminals and, increasingly, power-hungry data centers.

DT Midstream owns and operates a diverse, integrated portfolio of midstream pipeline, storage and gathering assets. The company is a pure play natural gas-focused midstream C-corp with assets linking major demand markets to supply from the Marcellus/Utica and Haynesville shale basins.

This article traces that journey—from the gas lamps illuminating Detroit's streets in 1849, through the holding company restructuring of the 1990s, the methodical infrastructure buildout of the 2000s and 2010s, and the strategic spin-off that created today's DTM. Along the way, we'll examine what makes midstream infrastructure such a compelling—and misunderstood—business model, how DTM has positioned itself to ride the twin secular waves of LNG exports and data center demand, and what investors should consider when evaluating this pure-play pipeline story.

II. The Deep Roots: DTE Energy & Detroit's Energy Heritage (1849–2001)

Origins of the Parent Company

Long before anyone imagined natural gas flowing through steel pipes across Louisiana swampland to fuel LNG tankers bound for Asia, the story of DT Midstream begins with a Philadelphia engineer named Lemuel Davis and his vision for illuminating a young frontier city.

DTE's gas operations trace their roots to 1849, when the City of Detroit Gas Company began operation with Philadelphia engineer Lemuel Davis as its first president. Davis arrived in Detroit at a time when the city's streets were dark after sunset, lit only by oil lamps and candles. Gas lighting—already transforming European and East Coast American cities—represented the cutting edge of urban technology.

In June of 1851, 53 gas street lamps were erected on Woodward, Woodbridge and Jefferson Avenues to light Detroit for the first time. Those 53 flickering lamps marked the beginning of an energy enterprise that would evolve over the next 175 years into what we know today as DTE Energy—and ultimately spin off the midstream division that became DTM.

The electricity side of the business arrived later. DTE's earliest direct corporate ancestor, the Edison Illuminating Company of Detroit, was founded in 1886. By the turn of the century, it split responsibility for commercial electric power in the fast-growing city of Detroit with the Peninsular Electric Light Company. In 1903, the two companies merged as the Detroit Edison Company, which began trading on January 17.

Building Michigan's Energy Backbone

The timing of Detroit Edison's formation proved fortuitous. That same year, construction began on the Delray 1 Power Plant, and Henry Ford, who had left Edison Illuminating four years earlier, founded Ford Motor Company. Detroit was about to become the Motor City, and Detroit Edison would power its transformation.

In 1904, Detroit Edison signed its first power contract with an automobile company—the Cadillac Motor Car Co. This began a symbiotic relationship between utility and industry that would define both for the next century. As automobile factories proliferated across southeastern Michigan, Detroit Edison expanded its generation capacity and distribution network to meet demand.

DTE Energy serves roughly 2 million electrical customers in southeastern Michigan. While the company's market territory only covers 13 percent of Michigan's total area, it accounts for half of Michigan's total population, energy consumption, and industrial capacity.

This concentration of industrial demand created both opportunities and challenges. Detroit Edison became expert at managing large, sophisticated load profiles—a capability that would later prove relevant as the company expanded into midstream operations serving industrial customers, power generators, and other large energy consumers.

The Holding Company Era

By the 1990s, utility industry dynamics were shifting. Deregulation loomed, and management recognized the need for structural flexibility to pursue growth opportunities beyond the regulated utility model.

In response to industry-wide changes, Detroit Edison was reorganized in late 1995. On January 1, 1996, DTE Energy Company became the holding company for subsidiaries that included Detroit Edison and several non-utility assets, among them Biomass Energy Systems, Edison Energy Services, and Midwest Energy Resources. The new structure allowed the company greater financial flexibility in creating new energy-related businesses and separated regulated subsidiaries from those not under state or federal regulations.

"DTE" was selected because it was the existing stock ticker symbol for Detroit Edison. The ticker persists today, though the company it represents has evolved dramatically.

The pivotal moment came in 2001. On May 31, 2001, DTE Energy and MCN Energy Group completed a merger which created Michigan's largest energy company and a premier regional energy provider. MichCon became an operating company of DTE Energy.

The MichCon acquisition fundamentally reshaped DTE's business. MichCon brought natural gas distribution infrastructure serving 1.3 million Michigan customers—but also something more strategically significant for the future DTM story: expertise in natural gas operations, storage, and transmission. This capabilities foundation would prove essential for what came next.

The investor implication from this era is clear: DTE Energy's corporate DNA included both regulated utility discipline and entrepreneurial appetite for non-utility growth. When Jerry Norcia arrived in 2002 to build the midstream business, he was joining an organization that understood both sides of the energy equation.

III. Birth of the Midstream Business (2002–2020)

Jerry Norcia's Pipeline Vision

The year 2002 marked an inflection point that few observers recognized at the time. While most attention focused on DTE Energy's core utility operations, a new executive arrived in Detroit with a mandate to build something different.

Jerry Norcia joined the company in 2002 as President of the Gas Storage and Pipelines business. Prior to joining DTE, Norcia was Vice President of Business Development for Union Gas.

Norcia, a chemical engineer by training with deep experience in Canadian gas markets, understood something that would take years to fully manifest: America's natural gas landscape was about to undergo a revolutionary transformation. The hydraulic fracturing techniques being refined in Texas would soon unlock vast shale reserves across the country, fundamentally reshaping gas supply—and creating enormous demand for new pipeline infrastructure.

During his tenure, Norcia has grown DTE's midstream business from a small business to one that is projected to earn $170 million by 2020. That projection, made in 2016, would prove conservative. By the time of the 2021 spin-off, the midstream division had grown into a substantial enterprise with assets spanning multiple states and serving major shale basins.

Norcia joined DTE in 2002 and held leadership roles throughout the company before being promoted to President and COO in 2017, CEO in 2019 and Board Chairman in 2022. In his 22 years with DTE, Norcia shaped a culture grounded in performance, integrity and impact.

Building Key Infrastructure Assets

The midstream business grew through a combination of greenfield development and strategic acquisitions, with DTE methodically building positions in what would prove to be the country's most prolific dry gas basins.

The NEXUS Joint Venture: Perhaps no asset better exemplifies DTE's strategic approach than the NEXUS Gas Transmission Pipeline. The NEXUS Gas Transmission Pipeline system consists of a 256-mile interstate pipeline with current capacity of approximately 1.4 Bcf per day, and three compression facilities, with 99,100 HP installed. It provides transport for natural gas from the Marcellus/Utica shale formations in Pennsylvania, Ohio and West Virginia to markets, directly and indirectly, in Ohio, Michigan, Illinois and Ontario, Canada.

NEXUS Gas Transmission is a 50/50 partnership between DT Midstream and Enbridge, Inc. NEXUS transports much needed, cleaner-burning and affordable natural gas to Ohio, Michigan and Ontario.

The NEXUS pipeline, which entered service in October 2018, transports emerging Appalachian shale gas supplies directly to consumers in northern Ohio and southeastern Michigan. NEXUS diversifies the region's energy sources, and provides energy security and reliability in the region, by delivering natural gas to consumers in northern Ohio, southeastern Michigan and the Dawn Hub in Ontario, Canada.

The Dawn Hub connection deserves emphasis—it's one of North America's most important natural gas trading points, providing access to storage and market liquidity that enhances the commercial value of the pipeline.

The construction phase of NEXUS was estimated to have created about 6,800 jobs and $660 million in wages. In its first five years of operation, it's estimated that NEXUS will generate $412 million in local tax revenue, of which $125 million will go directly to local school districts in Ohio and Michigan.

Louisiana Entry and the Haynesville: While the Appalachian assets addressed demand in the Midwest and Canada, DTE also recognized the strategic importance of Louisiana—home to the rapidly growing LNG export corridor along the Gulf Coast. The company built gathering and lateral pipeline infrastructure in the Haynesville Shale, positioning itself at the nexus of supply and export demand.

Geographic & Basin Diversification

By the time the spin-off was announced, DT Midstream had assembled a portfolio spanning multiple geographies:

The Company has a portfolio of integrated assets strategically located in the premier Marcellus, Utica, and Haynesville dry gas basins serving key growing markets; a strong balance sheet with low leverage; predictable and robust contracted cash flows; and a mature environmental, social, and governance (ESG) commitment.

The emphasis on "dry gas" basins is strategically significant. Unlike "wet gas" basins that produce significant natural gas liquids alongside methane, dry gas basins produce primarily methane. This simplifies operations (no need for processing plants to strip liquids) and aligns perfectly with LNG export demand, which requires pipeline-quality dry gas.

The Pure-Play Utility Trend

By the late 2010s, a pattern had emerged across the utility sector: conglomerates were spinning off non-utility businesses to create pure-play investment vehicles. The logic was straightforward—different investor bases preferred different risk-return profiles.

Slater explained the spinoff rationale: "We embarked upon this, thinking about how to maximize the value to DTE shareholders over a year ago after sensing a desire by a shareholder base for more pure-play investment vehicles. So we really wanted to take DTE and separate these two operating divisions so you have a pure-play utility...and a pure-play pipeline company, which is what DTM is. We really felt that would suit the needs of the investors better and unlock some trapped value that we thought was inside the DTE share."

Asked if this was an industry trend, Slater confirmed: "Yes, there have been a number of other transactions that had the same strategic intent. And really, you want to have each respective management team very focused on its lane, so to speak, its area of focus. And I believe there will be higher value creation as a result of that, where you don't have that diversified company, where you have investors who need to understand three or four industries to really understand the investment thesis for that company."

This insight proved prescient. Post-spin-off, DTM attracted infrastructure-focused investors comfortable with long-duration contracted cash flows, while DTE Energy attracted utility-focused investors seeking regulated returns. Both groups got what they wanted.

IV. The Spin-Off: Independence Day (2020–2021)

Announcement & Rationale

On October 27, 2020, DTE announced its plan to spin off DTE Midstream into an independent, publicly traded business called DT Midstream.

DTE Energy reported it had made significant progress on its plan to spin off its non-utility natural gas pipeline, storage and gathering business into a new stand-alone independent, publicly traded company, to be named DT Midstream and headquartered in Detroit, Michigan. The separation was expected to benefit both DTE Energy and DT Midstream, including by unlocking significant shareholder value and positioning each business to best serve the interests of their respective stakeholders.

The timing was notable—announcing a major corporate restructuring during a global pandemic demonstrated confidence in the fundamental value proposition. Management clearly believed the midstream business had grown substantial enough to stand independently and that separation would benefit both entities.

Execution & Structure

DT Midstream debuted as an independent, publicly traded company after successfully completing its separation from DTE Energy. Shares of DT Midstream began trading on the New York Stock Exchange under the symbol "DTM."

At 12:01 a.m. ET on July 1, 2021, DTE shareholders received a distribution of one share of DT Midstream common stock for every two shares of DTE common stock owned as of the close of business on June 18, 2021, the record date.

DTE Energy did not retain any of the outstanding common stock of DT Midstream. This clean separation ensured DTM would operate without conflicts or entanglements with its former parent—a complete corporate divorce rather than a partial divestiture.

Initial Financials & Guidance

At launch, management set expectations that would prove conservative:

For 2021, DT Midstream expected operating earnings of $296 million to $312 million or $3.06 to $3.22 per share. The company expected an adjusted EBITDA of $710 million to $750 million in 2021, delivering 7% growth compared to 2020.

DTM's integrated asset portfolio included 900 miles of Federal Energy Regulatory Commission (FERC) regulated interstate gas pipelines, 290 miles of intrastate lateral pipelines, and over 1,000 miles of gathering lines. It also owned and operated 94 Bcf of regulated gas storage capacity in Michigan.

Leadership Team

The leadership team was carefully assembled with deep midstream experience:

David Slater is the president and chief executive officer of DT Midstream, Inc. He previously served as president and chief operating officer of DTE Gas Storage and Pipelines, a wholly-owned midstream subsidiary of DTE Energy. David has more than 30 years of executive experience in the energy industry and has served in multi-national, investment banking and operational roles.

Slater joined DTE Energy in 2011 as senior vice president of DTE Gas Storage & Pipelines Company and DTE Pipeline Company and was promoted to executive vice president of DTE Midstream / GS&P in 2014. Prior to joining DTE Energy, Slater held various senior management positions at Goldman Sachs, Nexen Marketing USA Inc., a top 10 North American energy merchant, Engage Energy US, L.P., an energy merchant, and Union Gas Ltd., a gas utility in Ontario.

Slater's Goldman Sachs experience provides notable color—he understands both operational realities and capital markets expectations, a useful combination for running a newly public company.

Robert Skaggs, Jr., who served as executive chairman, has over 35 years of experience in the energy industry, including leading companies in the midstream, pipeline and regulated utility sectors. He served as president and CEO of NiSource, Inc. from 2005 to 2015 and executed its successful spin-off of Columbia Pipeline Group, Inc. in mid-2015.

Skaggs' presence on the board was particularly significant—he had literally written the playbook on midstream spin-offs with Columbia Pipeline Group, giving DTM leadership with direct M&A and spin-off experience.

Impact on Both Companies

Jerry Norcia, DTE Energy president and CEO, stated: "The separation of DT Midstream builds on our long track record of delivering value to our shareholders. With the completion of this transaction, approximately 90% of DTE Energy's operating earnings and investments will now be focused on our utility operations."

The 2021 spin-off of DTE Midstream marked a strategic refocusing. By separating the non-utility midstream assets, DTE Energy sharpened its concentration on its core regulated electric and gas utility businesses in Michigan, aiming for more predictable earnings and aligning closer with clean energy transition goals.

For DTM, independence meant freedom to pursue midstream-specific capital allocation—higher growth capital expenditures, accretive acquisitions, and expansion projects that might not have fit within a regulated utility's capital allocation framework.

V. The Growth Engine: LEAP & Haynesville Expansion (2022–2025)

LEAP: Louisiana Energy Access Project

If there's a single asset that defines DTM's growth thesis, it's LEAP—the Louisiana Energy Access Project. This 155-mile high-pressure lateral pipeline has become the company's primary growth engine, with capacity expanding dramatically to meet booming LNG export demand.

The LEAP Gathering Lateral Pipeline is a 155-mile high-pressure lateral pipeline that gathers gas along a spine-like system from Haynesville shale area producers and redelivers gas to interstate pipelines that provide access to petrochemical and refining facilities, power plants and LNG export facilities.

Today, customers on LEAP have access to multiple existing or under construction LNG terminals including, Sabine Pass, Cameron, Calcasieu Pass, Plaquemines, and Golden Pass via interconnects with Creole Trail, Cameron Interstate Pipeline, Texas Eastern, and Transco.

This is the "wellhead to water" value proposition in action—DTM connects Haynesville producers directly to export markets, earning transportation fees on every molecule that flows.

Multi-Phase Expansion Story

LEAP's capacity has grown through a systematic multi-phase expansion program:

Phase 1 (2023): DT Midstream announced the early commissioning of its LEAP phase 1 expansion, increasing its capacity from 1.0 Bcf/d to 1.3 Bcf/d, ahead of its planned Q4 2023 in service date and on budget.

Phase 2 (2024): DT Midstream announced the early mechanical completion of its Phase 2 LEAP expansion. The 400 MMcf/d expansion became available for firm service on January 1, 2024.

Phase 3 (2024): DT Midstream's LEAP Phase 3 project expanded the existing LEAP pipeline by 0.2 Bcf/d. As of June 2024, LEAP can transport 1.9 Bcf/d of natural gas from the Haynesville region to Gulf Coast markets via interconnections with other pipelines at the Gillis Hub near Ragley, Louisiana.

Phase 4 (2026): The 200 MMcf/d expansion would bring LEAP's total capacity to 2.1 Bcf/d. The project is underpinned by long-term, demand-based contracts with two LEAP customers and is expected to enter service in the first half of 2026.

Ultimate Capacity Potential

The expansion story doesn't end at 2.1 Bcf/d. DT Midstream has boosted the top end capacity estimate for its Louisiana Energy Access Project, or LEAP, to 4 Bcf/d, roughly double the amount of natural gas it could be transporting by 2026.

Based on the work to expand LEAP, CEO David Slater noted: "it's become clear to us that we actually can expand this beyond 3 Bcf/d up to the 4 Bcf/d neighborhood."

A new 1 Bcf/d interconnect between LEAP and TC Energy's Gillis Access project will expand LEAP's market connectivity to 3.6 Bcf/d along the Louisiana LNG corridor, with optionality to supply various LNG projects in the region.

LNG Export Thesis

The LNG export theme deserves emphasis because it represents a secular, multi-decade growth driver for LEAP:

These domestic industrial and international LNG markets are expected to grow by over 8 Bcf/d by 2030.

U.S. LNG exports are projected to nearly double to 21.5 Bcf/d by 2030, boosting shale gas output in the Haynesville, Permian, and Appalachia. Analysts say new pipelines and terminals will be key to meeting surging global demand.

According to EIA projections, natural gas converted to LNG for export will increase to 9.8 trillion cubic feet (Tcf), or almost 27 billion cubic feet per day, in 2037 in the Reference case compared with 4.4 Tcf in 2024.

DTM's positioning in the Haynesville, proximate to the Gulf Coast LNG corridor, places it squarely in the path of this demand wave. The company doesn't face the same permitting challenges as new greenfield pipelines—LEAP is an existing system that can be expanded incrementally to meet demand.

VI. Appalachian Expansion & Gathering Systems

Marcellus & Utica Shale Presence

While LEAP captures headlines for LNG-driven growth, DTM's Appalachian assets serve different but equally important markets—utility demand in the Midwest and Northeast, power generation, and Canadian market access via the Dawn Hub.

Phase two of an expansion for the Appalachia Gathering System was completed, which added 150 MMcf/d of mainline capacity.

In Ohio, an initial trunkline for a Utica Shale gathering project was also completed.

The gathering business operates under different economics than long-haul transmission. Gathering systems connect wellheads to mainline pipelines, typically serving a concentrated geographic area. These assets benefit from acreage dedication agreements where producers commit all production from defined acreage to the gathering system—providing volume visibility that supports project financing.

Infrastructure Footprint

DTM delivers to high-quality markets via approximately 2,900 miles of transportation and lateral pipelines and more than 800 miles of gathering lines. The company also owns and operates 94 Bcf of natural gas storage capacity in Michigan, serving local distribution companies, power generators and other customers in regions across the Midwest, the Northeast and Canada.

The Michigan storage capacity deserves attention. Natural gas storage provides multiple value streams: seasonal arbitrage (storing cheap summer gas for winter sales), system balancing, and reliability services. DTM's 94 Bcf represents significant capacity that serves regional utilities and can command premium pricing during peak demand periods.

Blue Union System

In the fourth quarter, an expansion was completed for the Blue Union gathering system and treating system in Louisiana.

Blue Union represents DTM's Haynesville gathering footprint, complementing LEAP's transmission capabilities. This vertical integration—from wellhead gathering through transmission to market—allows DTM to capture margin across multiple value chain segments while providing customers integrated "wellhead to water" solutions.

VII. The $1.2 Billion Bolt-On: Midwest Pipeline Acquisition (2024–2025)

Deal Announcement & Rationale

DTM's largest acquisition to date closed on December 31, 2024, dramatically expanding the company's Midwest footprint:

DT Midstream completed its acquisition of three natural gas transmission pipelines from ONEOK, Inc. for $1.2 billion, effective December 31, 2024. This deal is part of DT Midstream's strategy to enhance its natural gas portfolio and increase revenue from its pipeline segment, which is backed by strong contracts with reliable utility customers. The acquisition includes 100% ownership of Guardian Pipeline, Midwestern Gas Transmission, and Viking Gas Transmission, totaling over 3.7 Bcf/d of capacity across approximately 1,300 miles in the Midwest.

The acquisition price represents an approximately 10.5x 2025 EBITDA multiple.

A 10.5x EBITDA multiple for FERC-regulated pipelines with investment-grade utility customers is reasonable in the current environment—neither cheap nor expensive, but fairly valued for quality assets.

Acquired Assets

Guardian Pipeline: The 260-mile Guardian Pipeline interconnects with several pipelines near Joliet, Illinois, and serves Wisconsin.

Midwestern Gas Transmission: Midwestern Gas Transmission is a 400-mile bi-directional interstate pipeline connecting Tennessee to the Chicago Hub.

Viking Gas Transmission: Viking Gas Transmission links Minnesota, Wisconsin and North Dakota to Canadian supply. The system provides access to Canadian gas supplies at Emerson, Manitoba.

Strategic Fit & Synergies

David Slater stated: "The bolt-on acquisition of these premier pipelines is fully aligned with our pure play natural gas strategy."

"This acquisition also increases the revenue contribution from our pipeline segment, supported by take-or-pay contracts with strong credit quality utility customers."

This strategic move is expected to elevate DTM's pipeline segment to account for 70% of its Adjusted EBITDA by 2025, providing immediate accretion to Distributable Cash Flow.

The shift toward pipeline segment weighting (70% vs. 30% gathering) de-risks the company's cash flow profile. Transmission pipelines typically operate under FERC-regulated cost-of-service or negotiated rate structures with creditworthy utility customers, while gathering assets face more volume risk from producer activity levels.

Data Center & Power Demand Theme

Perhaps the most intriguing aspect of the acquisition is its positioning for data center-driven power demand:

DT Midstream is expanding its Guardian Pipeline project and considering a new Vector system buildout as surging Midwest power generation and data center load drive stronger natural gas demand across the region.

Guardian capacity is set to increase by 537 MMcf/d, and an open season for Vector could add 400 MMcf/d. Data centers and utilities are driving Midwest growth.

Jefferies highlighted DTM's "premium growth prospects in key Midwest data center markets" that support a 9% EBITDA CAGR from 2025-2030, exceeding the company's long-term guidance of 5-7% growth on $3.9 billion of capital expenditures.

The convergence of AI-driven data center expansion with natural gas infrastructure creates a secular demand tailwind that DTM is uniquely positioned to capture given its Midwest footprint.

VIII. Business Model Deep Dive

Revenue Segments

The company operates in two segments, Pipeline and Gathering. The Pipeline segment owns and operates interstate and intrastate natural gas pipelines, storage systems, and natural gas gathering lateral pipelines. This segment also engages in the transportation and storage of natural gas for intermediate and end-user customers. The Gathering segment owns and operates gas gathering systems. This segment is involved in the collection of natural gas for delivery to plants for treating, to gathering pipelines for further gathering, or to pipelines for transportation; and provision of associated ancillary services, including compression, dehydration, gas treatment, water impoundment, water transportation, water disposal, and sand mining.

DTM serves natural gas producers, local distribution companies, electric power generators, industrials, and national marketers.

Customer Base & Contract Structure

The quality of DTM's customer base and contract structure warrants emphasis:

The results for the fourth quarter and the full year reflect DT Midstream's ongoing efforts to deliver distinctive and predictable growth while maintaining a resilient cash flow profile supported by long-term contractual arrangements.

Most midstream companies operate under long-term contracts with fee-based structures that provide cash flow visibility. DTM's mix includes:

- Take-or-pay contracts: Shippers pay regardless of whether they actually use capacity

- Demand-based contracts: Fees based on reserved capacity rather than actual volumes

- Fixed-fee arrangements: Predictable revenue streams insulated from commodity price volatility

These initiatives are projected to drive a consistent 5-7% long-term EBITDA growth.

Financial Performance

On February 26, 2025, DT Midstream reported record financial results for 2024, with a full-year adjusted EBITDA of $969 million and net income of $354 million.

The company provided 2026 Adjusted EBITDA early outlook range of $1.155 to $1.225 billion, representing 6% annual growth from 2025.

DT Midstream's Board of Directors declared a quarterly cash dividend of $0.82 per share of common stock. At current share prices around $116, this translates to an approximate 2.8% dividend yield.

DTM has a backlog of $1.3 billion in growth projects through 2027.

IX. ESG & Energy Transition Strategy

Net Zero Commitment

DTM was among the first midstream companies to establish comprehensive decarbonization targets:

DTM is one of the first midstream companies to begin implementing plans to achieve net zero carbon and greenhouse gas emissions by 2050 with an interim reduction target of 30% by 2030.

DTE Midstream announced its goal to achieve net zero greenhouse gas emissions by 2050, estimating greenhouse gas emissions reduction of 3.5 million metric tons in its operations annually by 2050. The company is among the first in its sector to establish a 2050 net zero carbon emissions goal.

Carbon Capture Opportunity

CEO Slater discussed the decarbonization approach: "I'd say there is a whole series of actions we are taking, but probably one of the most interesting ones—and the one that is percolating to the surface—is carbon capture and sequestration. We see that as very applicable to our Haynesville assets, and it is somewhat of a two-for-one for us where it would significantly move us to that carbon reduction goal that we have and also create an incremental investment opportunity for shareholders. We haven't quite gotten to the point of commercializing it yet, but it feels very viable right now."

The Haynesville's proximity to industrial CO2 emitters and suitable geology for sequestration makes carbon capture a potential growth avenue that could transform an environmental obligation into a revenue opportunity.

DTM has gone above and beyond existing regulations on methane emissions and was among the first of its peers to commit to achieving net zero greenhouse gas emissions by 2050. The company expects to achieve a 30% reduction by 2030.

X. Competitive Positioning & Industry Dynamics

The Midstream Landscape

The U.S. midstream sector is fragmented yet dominated by several major players:

The largest U.S. midstream companies by market capitalization include The Williams Companies, Inc. at $72.21 billion, Enterprise Products Partners L.P. at $68.34 billion, Kinder Morgan, Inc. at $63.35 billion, and Energy Transfer LP at $61.67 billion.

DTM, with its approximately $12 billion market cap, occupies a middle tier—large enough for index inclusion and institutional ownership, but small enough to pursue accretive bolt-on acquisitions without integration headaches.

DT Midstream is one of 39 publicly-traded companies in the "Natural gas transmission" industry, competing based on the strength of its earnings, risk, analyst recommendations, dividends, institutional ownership, valuation and profitability.

81.5% of DT Midstream shares are held by institutional investors. High institutional ownership typically indicates sophisticated investors comfortable with the business model and growth prospects.

DTM's Competitive Advantages

Basin Positioning: DTM's focus on the Marcellus/Utica and Haynesville—America's two most prolific dry gas basins—provides structural advantages. These basins have the lowest-cost production in North America and serve the highest-growth demand centers (LNG export terminals and Midwest/Northeast utilities).

C-Corp Structure: Unlike many midstream peers structured as MLPs, DTM operates as a C-corporation. This simplifies tax reporting for investors, enables index inclusion, and provides structural flexibility for capital allocation.

Pure-Play Focus: While diversified midstream companies may offer more services, DTM's pure-play natural gas focus provides clarity for investors and management. No distractions from crude oil, NGL, or other commodities.

Utility Heritage: DTM's DNA traces to DTE Energy's utility culture—emphasizing reliability, safety, and long-term customer relationships over short-term profit maximization.

Porter's Five Forces Analysis

Threat of New Entrants: LOW - Significant capital requirements ($2-3 billion+ for major pipeline projects) - Lengthy permitting processes (FERC approval, state permits, environmental reviews) - Established right-of-way and customer relationships create barriers - Economies of scale favor incumbents

Bargaining Power of Suppliers: LOW-MODERATE - Steel pipe and equipment are commodity inputs - Labor markets can tighten during construction cycles - Compressor equipment from limited manufacturers (Caterpillar, Solar Turbines)

Bargaining Power of Buyers: MODERATE - Large utility and producer customers have negotiating power - Long-term contracts limit annual repricing - Switching costs are high once connected to infrastructure - Multiple pipeline options in some markets create competition

Threat of Substitutes: LOW (Near-term), MODERATE (Long-term) - No near-term substitute for natural gas pipeline transportation - Electrification poses long-term displacement risk for some gas demand - LNG export demand provides sustained near-term growth - Data center demand creates new secular driver

Competitive Rivalry: MODERATE - Fragmented industry with many regional players - Competition primarily for new project development - Existing infrastructure enjoys protected market positions - Rate regulation limits aggressive pricing competition

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Moderate. Pipeline economics improve with volume throughput over fixed infrastructure costs.

Network Effects: Weak. Unlike digital platforms, adding users doesn't inherently improve value for other users.

Counter-Positioning: Strong. DTM's pure-play natural gas strategy positions it as focused specialist versus diversified competitors. Established players may be hesitant to spin off similar divisions.

Switching Costs: Strong. Once producers and utilities connect to infrastructure, switching requires physical disconnection and reconnection—expensive and disruptive.

Branding: Weak. Commoditized service where reliability and price matter more than brand.

Cornered Resource: Moderate to Strong. Rights-of-way, permits, and geographic positioning near producing basins and demand centers are difficult to replicate.

Process Power: Moderate. Operational excellence and safety track records differentiate operators, but core processes are similar across industry.

XI. Bull & Bear Case Analysis

The Bull Case

LNG Export Super-Cycle: U.S. LNG exports are projected to roughly double by 2030. LNG gross exports are expected to increase by 19% to 14.2 billion cubic feet per day (Bcf/d) in 2025 and by 15% to 16.4 Bcf/d in 2026. DTM's Haynesville infrastructure sits directly in the path of this demand wave.

Data Center Demand: The potential impact on natural gas demand is significant. While estimates vary, an average of four analyst forecasts suggests AI data centers in the U.S. could require an incremental 8.0 billion cubic feet per day (Bcf/d) of natural gas by 2030. This directly benefits midstream companies, which will operate the pipeline infrastructure needed to deliver natural gas to data centers or the utilities supporting them.

Acquisition Integration: The ONEOK acquisition provides immediate EBITDA accretion and positions DTM for Midwest power demand growth tied to data centers.

Execution Track Record: LEAP expansions have consistently delivered ahead of schedule and on budget—a rare combination in large infrastructure projects.

Conservative Financial Profile: With a robust financial health, evidenced by an investment-grade credit rating from all three major agencies in July 2025, DT Midstream is well-positioned to largely self-fund its growth.

Dividend Growth: The company has increased dividends consistently since the spin-off, with the latest 12% increase demonstrating cash flow durability.

The Bear Case

Natural Gas Price Volatility: While DTM's contracts provide volume insulation, producer curtailments during price downturns can impact gathering volumes. As a dry gas play, the Haynesville is more vulnerable to natural gas price slumps than liquids-rich basins where operators can earn revenue from multiple products. After averaging 16.5 Bcf/d in 2023, the U.S. Energy Information Administration expects Haynesville supply to drop to 14.9 Bcf/d in 2024 before rebounding to 15.1 Bcf/d in 2025.

Long-Term Energy Transition: Decades-long decarbonization trends pose structural headwinds for natural gas infrastructure. While near-term demand is robust, 2040s and 2050s outlook is uncertain.

Regulatory Risk: FERC regulation, state permitting, and environmental reviews can delay or cancel projects. Political shifts could affect permitting timelines and regulatory treatment.

Concentration Risk: Significant exposure to specific basins (Haynesville, Marcellus/Utica) and customers. Producer consolidation could increase customer bargaining power.

Valuation Premium: At a trailing P/E ratio of 29.59, DTM trades at a premium to many midstream peers. Growth expectations are embedded in the price, leaving less margin of safety if execution disappoints.

Integration Risk: The ONEOK acquisition is DTM's largest to date. Integration challenges could distract management and delay synergy realization.

Myth vs. Reality

| Consensus View | Reality Check |

|---|---|

| "Natural gas is a bridge fuel that will decline rapidly" | Near-term demand growth from LNG exports and data centers contradicts this narrative; EIA projections show gas production growing through 2030+ |

| "Midstream is a yield play for income investors only" | DTM's 5-7% EBITDA growth target plus dividend growth provides total return opportunity beyond yield |

| "Pipeline stocks are energy price plays" | Fee-based, take-or-pay contracts provide substantial insulation from commodity price volatility |

| "ESG pressures will destroy midstream valuations" | Early mover advantage on net zero commitments and carbon capture could differentiate DTM |

XII. Key Metrics to Watch

For ongoing monitoring of DTM's performance, investors should focus on:

1. LEAP Utilization Rate

The ratio of actual throughput to capacity on the LEAP system indicates how effectively the company is monetizing its flagship growth asset. High utilization (>80%) suggests strong demand and validates expansion investments.

2. Adjusted EBITDA Growth Rate

Management guides to 5-7% long-term EBITDA growth. Consistent achievement of the high end of this range would indicate successful execution on organic projects and acquisition integration.

3. Dividend Coverage / Distributable Cash Flow

The ratio of distributable cash flow to dividends paid indicates sustainability of the dividend and capacity for future increases. Coverage above 1.3x provides comfortable margin.

XIII. Valuation Framework

DTM currently trades at approximately: - EV/EBITDA: ~15.5x (based on 2024 EBITDA) - P/E: ~29x trailing - Dividend Yield: ~2.8%

These multiples reflect growth expectations embedded in the stock price. For context, large-cap midstream peers (Williams, Kinder Morgan, Enterprise Products) trade at lower multiples but also have lower growth profiles.

The valuation question centers on whether DTM can deliver on its growth projections—particularly capturing LNG export demand through LEAP expansions and data center-driven power demand through the acquired Midwest assets.

XIV. Future Outlook

CEO Slater articulated the long-term vision: "Longer term, we expect natural gas demand to continue to grow, driven by the expanding LNG export market, increased power and data center demand, and from industrial and commercial onshoring, all of which will support high utilization and further development of natural gas infrastructure."

The company is aggressively pursuing a $2.3 billion portfolio of organic growth projects, including the LEAP Phase 4 expansion in Haynesville, the Stonewall Expansion, and various gathering expansions.

Management provided 2026 Adjusted EBITDA early outlook range of $1.155 to $1.225 billion, representing 6% annual growth from 2025.

The near-term visibility is strong—contracted projects, regulatory approvals in place, construction timelines established. The medium-term outlook depends on continued LNG export capacity additions and data center construction. The long-term outlook hinges on broader energy transition dynamics and whether natural gas maintains its role in the U.S. energy mix.

XV. Conclusion

DT Midstream represents a compelling case study in corporate evolution—from the gas lamps of 1849 Detroit to the LNG export terminals of 2025 Louisiana, from a division of a Midwestern utility to an independent pure-play infrastructure company.

The company benefits from secular demand tailwinds (LNG exports, data center power demand), a high-quality asset base positioned in premium basins, and a management team with deep operational and capital markets experience. The conservative balance sheet and investment-grade credit ratings provide financial flexibility for growth.

Risks include energy transition uncertainty, commodity price impacts on producer activity, and execution challenges on the substantial growth backlog. The premium valuation leaves limited margin of safety if growth disappoints.

For investors seeking exposure to natural gas infrastructure with growth characteristics, DTM offers a differentiated proposition: a pure-play, C-corp structure focused on the highest-quality dry gas basins with direct exposure to the LNG export theme. Whether that justifies the current valuation premium requires individual assessment of growth expectations and risk tolerance.

The company's heritage—stretching back 175 years through Detroit Edison and DTE Energy—provides institutional depth and operational discipline. Yet DTM's future lies not in Michigan basements but in Louisiana bayous and Ohio shale fields, connecting American natural gas to global markets one molecule at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube