Mueller Water Products: The Hidden Infrastructure Giant Behind Every Fire Hydrant

I. Introduction & Episode Roadmap

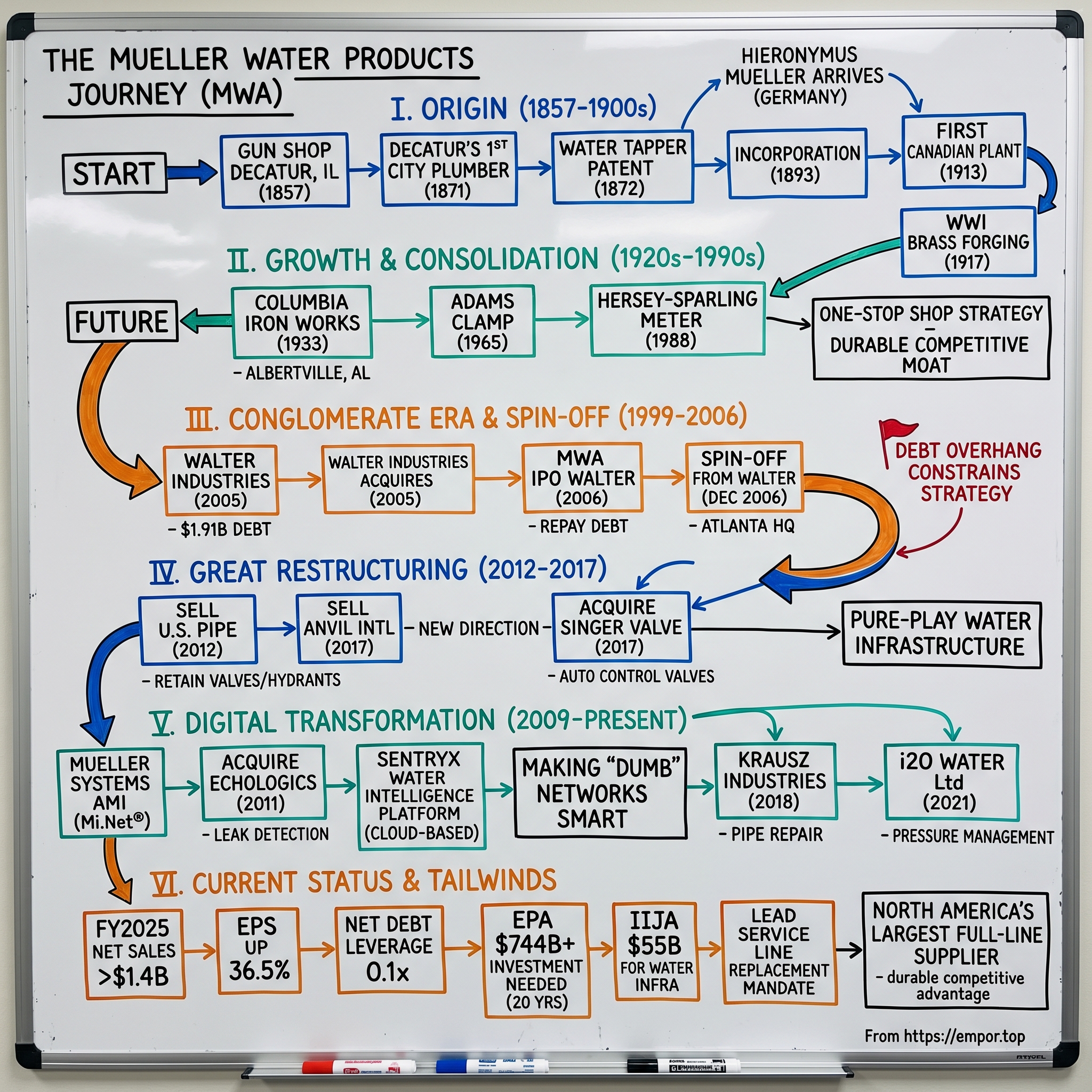

Picture the classic American streetscape: a red fire hydrant standing sentinel on the corner, so ubiquitous it becomes invisible. That hydrant—there's roughly a one-in-three chance it was made by a company most people have never heard of, yet one whose products touch virtually every glass of water poured from a tap in the United States. Mueller Water Products, Inc. (MWP) is a publicly traded company headquartered in Atlanta, Georgia. It is one of the largest manufacturers and distributors of fire hydrants, gate valves, and other water infrastructure products in North America.

This is the story of how a German immigrant's gun shop in small-town Illinois became the backbone of America's water infrastructure—a $1.4 billion enterprise that traces its lineage through Civil War-era invention, industrial consolidation, conglomerate roller coasters, and a digital transformation that's still unfolding today.

The hook that first drew us to Mueller is a piece of trivia that borders on the surreal. United States Patent #251726A was issued to Hieronymus Mueller in 1892 for a water pressure regulator. In 1913, modified versions of this valve were deployed for an engineering challenge of global significance. Today, as many as 95 valves based on Mueller's original design are still used to protect the canal's system of locks—specifically, the Panama Canal. Think about that: technology invented by a German-American tinkerer in Decatur, Illinois, still protects ships from accidentally crashing into lock gates more than a century later.

In the decades since Hieronymus Mueller created his eponymous water products company, Mueller Water Products has grown to serve some of North America's largest utilities, with its products being specified by the United States' 100 largest metropolitan areas. When city engineers write specifications for new water infrastructure projects, Mueller products are often named explicitly. That kind of specification power—where your brand becomes part of the official playbook—represents one of the most durable competitive advantages in industrial manufacturing.

What makes Mueller particularly fascinating right now is the confluence of three powerful forces. First, there's the macro tailwind: The Environmental Protection Agency (EPA) estimates that the country will need to spend more than $744 billion over the next two decades on water infrastructure. America's water pipes are aging, breaking, and leaking at alarming rates. Second, there's a regulatory catalyst: The EPA mandates full replacement of all lead service lines across the country within 10 years, with some limited exceptions. And third, there's Mueller's own evolution from a pure-play manufacturer into a technology-enabled infrastructure company, building a digital platform called Sentryx that aims to make "dumb" water networks smart.

Mueller Water Products reported record Q4 and FY2025 results, with Q4 net sales up 9.4% YoY and adjusted EBITDA margin exceeding 24%. FY2025 net sales rose 8.7% to over $1.4B, with adjusted EPS up 36.5% to $1.31.

In this episode, we'll trace the full arc: from gun shop to water empire, through the conglomerate era and spin-off, the great restructuring that transformed Mueller into a focused pure-play, the digital bet that's reshaping the company's future, and finally, why America's crumbling water infrastructure might represent the company's biggest opportunity in its 167-year history.

II. The Origin Story: From Gun Shop to Water Innovation (1857-1900s)

Hieronymus Mueller arrived in America the way so many immigrants did in the mid-nineteenth century: fleeing upheaval, carrying skills, and harboring ambition. Hieronymus Mueller was born in Wertheim, Germany in 1832. He was trained and apprenticed as a machinist but became caught up in the widespread economic and political upheaval engulfing Germany in the 1840's. This unrest culminated in the revolutions of 1848 which attempted to consolidate the several German states into a more democratic nation and to increase economic opportunity. The movement failed and was followed by greater repression as the old power structure reasserted itself and repealed reforms of the past decade. Hieronymus was involved in some degree with the reformist movement—family lore tells that he was charged with a conspiracy in a failed plot to blow up a bridge with other revolutionaries. We have no record that would confirm this, but we do know that Hieronymus did decide to flee Germany in 1850 and that he soon made his way to the United States.

Whether or not the bridge-bombing story is apocryphal, what we know for certain is that Hieronymus was a trained machinist with an inventor's restlessness. By 1857, he had made his way to Decatur, Illinois, a growing town in the heart of the prairie, and opened 'H. Mueller, Gun Shop' in Decatur, Illinois.

What happened next reveals the opportunistic pragmatism that would characterize the Mueller family for generations. Mueller closed the business briefly in 1858 to prospect for gold in Colorado, but returned to his business not long after, expanding it to include sewing machine and clock repairs and the sale of hunting and fishing equipment in addition to gunsmithing. The gold rush didn't pan out—literally—but Mueller's willingness to chase opportunity while maintaining his core competency would prove prescient.

Hieronymus Mueller was good with his hands—he had been trained as a machinist in his native Germany. But, he was also good with his mind—an apparently natural talent. He started his business with a small gunsmithing shop but soon added locksmithing and sewing machine repairs. He had a knack for understanding mechanical devices. This led to his appointment as Decatur's first "city plumber" in 1871 to oversee the installation of a water distribution system.

That appointment was the pivot point. As America's cities expanded explosively in the post-Civil War era, the need for clean water distribution became urgent. Cholera outbreaks, typhoid epidemics, and devastating fires all pointed to the same infrastructure gap. Hieronymus Mueller, already tinkering with metalwork and repairs, saw the opportunity.

The breakthrough came in 1872. The following year he patented his first major invention, the Mueller Water Tapper—which is, with minor modifications, still the standard for the industry. This invention was revolutionary: Hieronymus Mueller's patent for an improved water tapping machine marked a significant advancement, allowing connections to pressurized water mains without disruption.

Think about the engineering challenge here. Water mains in the 1870s were pressurized systems—you couldn't simply drill into them without causing geysers of water to erupt. Mueller's tapping machine allowed utility workers to drill into a live main and connect service lines without shutting off service or depressurizing the system. In an era when shutting off water service meant fire risk and public health hazards, this was transformative. And here's the remarkable part: the basic principle Mueller invented in 1872 remains the industry standard today.

By 1880, the focus of Mueller's business shifted from manufacturing guns to manufacturing plumbing goods, and in 1885, Mueller changed the name of his business to "H. Mueller Manufacturing Co." and he moved the gun and sporting goods division of his company to a separate location.

By 1896, it focused exclusively on plumbing goods after selling its gun and sporting goods business. The transition was complete: Mueller was now entirely focused on water infrastructure.

What set Mueller apart wasn't just one invention—it was sustained innovation across decades. He and his sons went on to obtain 501 patents including water pressure regulators, faucet designs, the first sanitary drinking fountain, a roller skate design, and a bicycle kick-stand. The sanitary drinking fountain invention is particularly notable: in an era when shared drinking cups spread disease, Mueller's fountain allowed people to drink directly from a jet of water without touching anything. It was a public health innovation disguised as a plumbing product.

This period of prosperous growth culminated in the formal incorporation of the business in Michigan in 1893 with $68,000 in capital.

The company's growth extended internationally early on. The company's growth extended internationally with its first Canadian plant opening in 1913. A significant step was the 1917 reincorporation as Mueller Metals Company, coinciding with the opening of the U.S.'s first commercial brass forging facility to support World War I efforts.

The World War I brass foundry represented both patriotic contribution and strategic diversification—Mueller was now vertically integrated, controlling its raw material supply while serving the war effort. This pattern of building internal capabilities rather than relying on suppliers would characterize Mueller for the next century.

What does this origin story tell us about the company's DNA? Three things stand out. First, Mueller was founded by an engineer-entrepreneur who understood that practical invention drives industrial success. Second, the company pivoted decisively when opportunity presented itself—from guns to plumbing, from local to national to international. Third, innovation became embedded in the culture: 501 patents from a family of tinkerers over a few decades established a tradition of continuous improvement that persists today.

III. Growth & Consolidation: Building an Empire (1920s-1990s)

The interwar period and post-World War II decades saw Mueller transform from a large regional manufacturer into a diversified national powerhouse through systematic acquisition. This era established the strategic logic that still shapes the company: become the full-line supplier, own the customer relationship across multiple product categories, and make switching costs prohibitively high.

After World War I, Mueller continued its technological advancements, introducing copper plumbing and flare connections for domestic use in 1923. The acquisition of Columbia Iron Works in 1933 expanded its manufacturing of hydrants and gate valves, marking key milestones in the Brief History of Mueller Water Products.

The Columbia Iron Works acquisition deserves particular attention. Chattanooga, Tennessee-based Columbia was a manufacturer of fire hydrants and gate valves—products complementary to Mueller's existing brass and valve lines. By acquiring Columbia during the depths of the Great Depression, Mueller demonstrated both financial resilience and opportunistic M&A acumen. The brand name was later changed to Mueller in 1955, fully integrating the acquisition.

The fire hydrant manufacturing operations from this acquisition eventually moved to Albertville, Alabama, in 1975, a decision that would earn that small town a peculiar distinction: Mueller still manufactures gate valves at this location, but the fire hydrant manufacturing operation was moved to Albertville, Alabama in 1975, earning the town the moniker "Fire Hydrant Capital of the World" in 1991.

By 1963, the scale of Mueller's growth was evident: Mueller reported profits of $2.35 million on sales of $80.8 million, demonstrating substantial growth. Adjusted for inflation, that's roughly $800 million in today's dollars—a substantial mid-century industrial enterprise.

The acquisition pace continued. In 1965, Mueller acquired the Los Angeles-based Adams Clamp Company, expanding its product line. In 1988 came a more transformative deal: Further expansion occurred through acquisitions like Bay Engineering Company in 1964 and Hersey-Sparling Meter Company in 1988. The Hersey-Sparling acquisition marked Mueller's entry into the water metering business—a product category that would become increasingly important as utilities moved toward digital monitoring.

In 1996, Mueller added two more businesses: Henry Pratt Company, a manufacturer of butterfly and specialty valves, and James Jones Company. Each acquisition added product categories and customer relationships, building toward Mueller's ultimate strategic goal of becoming the one-stop shop for water utilities.

The logic of full-line supply is powerful in infrastructure businesses. Municipal purchasing officers prefer dealing with fewer vendors. Contractors appreciate simplified logistics. And once a municipality standardizes on Mueller products—fire hydrants, gate valves, service brass, meters—switching to competitors becomes enormously complicated. You'd need to retrain maintenance crews, renegotiate specifications, and manage compatibility issues across decades of installed infrastructure. This installed base becomes a moat that deepens with every year of operation.

Over the course of its more than 160-year history, Mueller Water Products has balanced steady, expansive growth with its roots as an innovative, family-owned business originating in Decatur, Illinois.

IV. The Walter Industries Era & The IPO (1999-2006)

The most dramatic chapter in Mueller's corporate history began in October 2005, when Walter Industries, Inc. entered the picture. Walter Industries, Inc. acquires Mueller Water Products, Inc. formerly a privately held leading supplier of flow control products, for an aggregated value of approximately $1.91 billion, and combines with U.S. Pipe and Foundry.

To understand this transaction, you need to understand Walter Industries. Founded in 1946 by Tampa entrepreneur James W. Walter Sr. as a builder of affordable homes, Walter Industries had evolved into a sprawling conglomerate with operations in homebuilding, mortgage financing, coal mining, and industrial products. Walter Energy, Inc. was a publicly traded "pure play" metallurgical coal producer for the global steel industry. The company also produced natural gas, steam coal and industrial coal, anthracite, metallurgical coke, and coal bed methane gas.

The deal structure was complex. The initial prospectus for Mueller Water Products is very complex, because of the convoluted history of the company. Basically Walter Industries took on a lot of debt to buy "Old Mueller" and then merged it with the existing U.S Pipe and Foundry Company owned by Walter.

The combined entity now operated three distinct business units: Mueller Co. (valves, hydrants, brass products), Anvil International (pipe fittings for construction), and U.S. Pipe (ductile iron pipe manufacturing). The company's Water Products business unit includes the Mueller, Anvil, and U.S. Pipe organizations, and Walter recently filed a registration with the Securities and Exchange Commission for an initial public offering.

Walter says it intends to spin off the Water Products Business approximately six months after the IPO by distributing the new stock to the company's shareholders. Walter is also studying spin-offs of its other business units, Homebuilding and Financing, to its shareholders.

In June 2006, Mueller Water completed its initial public offering (IPO) of 28.8 million shares of Series A common stock, at $16 per share (NYSE: MWA). The net proceeds of $428.9 million were used to repay a portion of Mueller Water's existing debt.

The spin-off followed in December 2006. Mueller Water Products spun off from Walter Industries in December 2006. The company is headquartered in Atlanta, Ga.

The combined entity was then spun off as the publicly held Mueller Water Products, Inc. in 2006, moving its headquarters from the company's birthplace of Decatur, Illinois, to Atlanta, Georgia.

For investors, the spin-off created something novel: a pure-play water infrastructure company. But the newly public Mueller carried significant baggage. The $1.91 billion acquisition price, financed largely with debt, meant the newly independent company faced substantial interest payments and limited financial flexibility. This debt overhang would constrain Mueller's strategic options for years.

In connection with the spin-off of Mueller Water on December 14, 2006, we entered into certain agreements with Mueller Water, including an income tax allocation agreement and a joint litigation agreement. Under the terms of those agreements, we and Mueller Water agreed to indemnify each other with respect to the indebtedness, liabilities and obligations that will be retained by our respective companies, including certain tax and litigation liabilities. These indemnification obligations could be significant.

The Walter Industries chapter illustrates both the opportunities and risks of conglomerate ownership. On the positive side, the combination with U.S. Pipe and Anvil created a larger, more diversified entity with broader product coverage. On the negative side, the debt-fueled acquisition left Mueller financially constrained, and the three business units had limited operational synergy. Walter Industries itself would eventually file for bankruptcy in 2015, years after spinning off Mueller.

V. The Great Restructuring (2012-2017)

The post-spin-off Mueller faced a strategic dilemma. The three-segment structure made theoretical sense—cover the full water infrastructure value chain from pipes to valves to fittings—but the businesses had fundamentally different economics. U.S. Pipe manufactured ductile iron pipes, a capital-intensive commodity business with thin margins and cyclical demand. Anvil International made pipe fittings for construction, a business with different customers and distribution channels than municipal water infrastructure. Mueller Co. produced the valves, hydrants, and brass products that were the company's historical core.

The restructuring began in 2012. In 2012 Mueller Water Products divested U.S. Pipe to Wynnchurch Capital, Ltd., retaining only the valve and hydrant division, which now operates under the Mueller Co. business unit.

The U.S. Pipe divestiture was a recognition of commodity economics. Ductile iron pipe manufacturing requires massive capital investment in foundries, faces intense price competition, and offers limited differentiation. The business was solid but didn't fit the higher-margin, more differentiated profile Mueller wanted to build.

Five years later came the second major portfolio move. Early in 2017 Mueller Water Products sold its Anvil International division to One Equity Partners and also completed the acquisition of Singer Valve, a manufacturer of automatic control valves.

The Anvil sale completed the transformation. Mueller was now a focused water infrastructure company—no more pipe manufacturing, no more construction fittings. But the same announcement included an acquisition that signaled the company's new strategic direction: Singer Valve, which manufactured automatic control valves. Mueller Water came out of a protracted quiet period on the M&A front when it picked up Singer Valve in 2017. Despite the Krausz deal following relatively quickly, Hall maintains that the company is unlikely to accelerate its M&A activity.

The Singer acquisition hinted at Mueller's evolving thesis: the future wasn't just about making valves and hydrants, but about making them smart. Automatic control valves respond to pressure changes and flow conditions in real-time—a first step toward the intelligent water networks Mueller would increasingly pursue.

MWP is made up of two business units—Mueller Co. and Mueller Technologies—that oversee more than a dozen brands and affiliates, including Echologics and Mueller Systems.

The restructuring created a leaner, more focused enterprise, but it also exposed a challenge: organic growth in the core valve and hydrant business was modest, tied to municipal budgets and new construction. The technology pivot represented Mueller's answer to the growth question.

VI. The Digital Transformation & Technology Bet (2009-Present)

Mueller's digital transformation didn't begin with a sudden revelation—it evolved through a series of acquisitions and organic investments that collectively repositioned the company from pure-play manufacturer to technology-enabled infrastructure provider.

Mueller Water Products created Mueller Systems by combining Arkion Systems and Hersey Meters. Mueller expands its advanced metering infrastructure (AMI) offerings to help municipalities improve conservation and operational efficiencies with the introduction of Mi.Net® Mueller infrastructure for Utilities.

The Mi.Net system represented Mueller's first major foray into connected infrastructure. Traditional water meters were "dumb" devices—they measured consumption, but someone had to physically read them. AMI systems allowed remote, wireless meter reading, eliminating truck rolls and enabling near-real-time consumption data.

Mueller Water Products expands its leak detection and pipe condition assessment capabilities with the acquisition of Echologics Holdings, the parent company of Echologics Engineering Inc.

The Echologics acquisition, completed in 2011, added a critical capability: acoustic-based leak detection. That's why Echologics, a Mueller brand, created EchoShore®-DX and DXe technologies—permanent acoustic-based leak detection systems deployed on existing fittings within a distribution system of small diameter pipes. The technology regularly monitors leaks within a pipe infrastructure network. Sensors are deployed throughout the distribution network (fire hydrants or valves) and record acoustic data daily—in the early morning hours when it's the quietest.

The technology works by detecting the subtle acoustic signatures that leaks create. Water escaping through even small cracks generates sound waves that travel through pipes and can be detected by sensitive sensors. By analyzing these acoustic signals, utilities can identify and locate leaks before they become catastrophic failures.

Echologics was acquired by Mueller more than 15 years ago because Mueller saw the need and opportunity to bridge technology with infrastructure for network and asset management, as a whole. Echologics has integrated solutions as a standalone and working with other groups to collaborate on products and technology to support an overall holistic solution for utilities and network managers.

The culmination of these efforts was Sentryx, Mueller's digital services platform. Sentryx Water Intelligence is a digital services platform for water utilities to monitor, operate and monetize water distribution networks. Easy: All your water network data integrated into one secure platform with intuitive dashboards.

To make intelligent decisions on your water infrastructure, you need data intelligence. The Sentryx™ Water Intelligence platform provides utilities with unique insights into the health of the distribution system.

Sentryx represents Mueller's answer to a fundamental question: in a world of IoT and cloud computing, how does a 167-year-old valve manufacturer remain relevant? The answer is by making physical infrastructure intelligent—embedding sensors in hydrants, connecting meters to networks, and building software that turns data into actionable insights.

One hydrant with new digital capabilities—whether retrofitting an existing Mueller hydrant or installing a new one—is known as the Sentryx software enabled Super Centurion hydrant. Mueller introduces Sentryx-enabled Super Centurion hydrant. The hydrant acts as a communications hub, housing state-of-the-art sensors that communicate data to the scalable, fully cloud-based Sentryx platform. This solution is designed for any size water distribution network.

The 2018 Krausz acquisition added another dimension to Mueller's strategy. Mueller Water Products, Inc. has announced it has signed a definitive agreement to acquire Krausz Industries, Ltd., a manufacturer of pipe couplings, grips and clamps, for $140 million in cash. Krausz Industries provides a full suite of innovative and proprietary pipe couplings, grips and clamps under the HYMAX brand for the global water and wastewater industries.

Mueller Water Products is looking to leverage its $140 million acquisition of Krausz Industries as a growth platform in the North American water network repair market, serving to offset tepid investment in new infrastructure and headwinds in residential construction.

The Krausz deal positioned Mueller in the pipe repair market—a segment that grows regardless of new construction, because aging infrastructure inevitably needs fixing.

In 2021, Mueller completed another technology-focused acquisition. Mueller Water Products, Inc. today announced that it has acquired i2O Water Ltd ("i2O Water"), a provider of pressure management solutions for approximately $20 million in cash. i2O Water delivers intelligent water networks to more than 100 water companies in over 45 countries around the world to reduce water loss by providing solutions that enable clients to instrument, analyze and control water networks to reduce leakage, lower energy consumption and improve supply. Founded in 2005, i2O Water is headquartered in Southampton, UK, with operations in Malaysia and Colombia.

The acquisition of i2O Water enhances Mueller's ability to accelerate its software offerings. i20's intelligent network solutions are complementary to both Sentryx™, Mueller's digital services platform, and existing Mueller technology-enabled products used for metering, leak detection, pipe condition assessment and water quality. Additionally, Mueller plans to introduce i20's products and solutions in North America, where i20 currently has no presence.

The i2O deal was modest in size but strategically significant. It added advanced pressure management capabilities—the ability to dynamically adjust water pressure throughout a network to reduce leaks and extend pipe life. More importantly, it gave Mueller technology that was already proven in international markets, ready for introduction to North American utilities.

VII. Understanding the Business Model

Mueller today operates through two segments that reflect its strategic evolution. It operates in two segments, Water Flow Solutions and Water Management Solutions. The Water Flow Solutions segment provides valves for water systems, such as iron gate, butterfly, tapping, check, knife, plug, and ball valves, which are used to control distribution and transmission of potable water and non-potable water, as well as in water transmission or distribution, water treatment facilities, or industrial applications. It also offers service brass products.

The Water Management Solutions segment offers dry-barrel and wet-barrel fire hydrants for water infrastructure development; fire protection systems, and water infrastructure repair and replacement projects; pipe repair products, such as couplings, grips, and clamps used to repair leaks; residential, fire protection, and commercial water metering products and systems; water leak detection and pipe condition assessment products and services; machines and tools for tapping, drilling, extracting, installing, and stopping-off; gas valve products for use in gas distribution systems; and intelligent water solutions, including pressure control valves, advanced pressure management, network analytics, event management, and date logging.

The Water Flow Solutions segment represents Mueller's historical core—the iron gate valves, specialty valves, and service brass products that trace directly back to Hieronymus Mueller's nineteenth-century inventions. This segment is characterized by installed base advantages, specification-driven sales, and replacement cycles measured in decades.

The Water Management Solutions segment reflects Mueller's strategic evolution, combining traditional products (hydrants, repair clamps) with technology-enabled offerings (leak detection, smart meters, pressure management). This segment offers both higher growth potential and greater investment requirements.

Mueller's manufacturing moat deserves particular attention. MWP is the only manufacturer of valves and hydrants that utilizes the lost-foam casting process, which reduces the amount of required materials for casting and reduces the amount of waste and emissions generated by the casting process.

Lost-foam casting is a manufacturing technique where a foam pattern is coated with refractory material and then vaporized when molten metal is poured into the mold. The result is a near-net-shape casting that requires less machining and generates less waste than traditional sand casting. Mueller's investment in this technology creates both cost advantages and environmental benefits—an increasingly important differentiator as utilities face pressure to reduce their carbon footprints.

This evolution led to becoming North America's largest full-line supplier of potable water distribution products, offering everything from fire hydrants to advanced leak detection.

The geographic concentration of Mueller's business is notable. All of Mueller's current manufacturing facilities are located in the US, Canada, and Mexico, and while the firm has sales offices in the UK and the Netherlands, less than 10% of its revenues are derived from outside North America.

This North American focus is both a strength and a limitation. On the positive side, it insulates Mueller from international currency volatility and political risk. On the negative side, it concentrates the company's fortunes in a single geographic market, limiting diversification benefits.

VIII. The Macro Tailwind: America's Water Infrastructure Crisis

The case for Mueller ultimately rests on a simple premise: America's water infrastructure is crumbling, and someone has to fix it. The numbers paint a stark picture.

The Environmental Protection Agency (EPA) estimates that the country will need to spend more than $744 billion over the next two decades on water infrastructure, including pipes, treatment plants, and wastewater management facilities. However, private industry groups including the American Water Works Association say the costs will top $1 trillion.

Approximately 250,000 water main breaks occur each year in the United States, according to the American Water Works Association (AWWA). These breaks lead not only to wasted water but also to significant economic costs, including emergency repairs and disruptions in service.

The American Society of Civil Engineers' U.S. Infrastructure Report Card in 2021 estimated that a water main breaks every two minutes somewhere in the U.S., losing 6 billion gallons of treated water a day.

Despite a recent infusion of federal dollars, the health of the country's aging water infrastructure has plateaued amid burgeoning environmental stressors and new cleanup demands, according to the American Society of Civil Engineers' 2025 Infrastructure Report Card released last week. Drinking water infrastructure notched a "C-" while wastewater got a "D+" and stormwater tied with transit for the category with the lowest grade of "D."

The Infrastructure Investment and Jobs Act (IIJA), passed in 2021, represents the largest federal investment in water infrastructure in American history. In November 2021, Biden signed the bipartisan Infrastructure Investment and Jobs Act (IIJA), a $1 trillion infrastructure spending bill that earmarked $55 billion for water infrastructure. Most of those appropriations will go toward protecting environmental resources and upgrading and repairing aging systems; at least $15 billion will be used to replace lead pipes in existing water infrastructure.

Currently, private and public water and wastewater utilities are all underfunded, according to a March 11 report from New York-based consulting firm McKinsey & Co. The U.S. water utility sector faced an estimated $110 billion funding gap in 2024, which is nearly 60% of utilities' overall spending. By 2030, this gap could increase to approximately $194 billion.

Beyond the general infrastructure crisis, there's a specific regulatory catalyst: the EPA's new Lead and Copper Rule Improvements (LCRI). The U.S. Environmental Protection Agency (EPA) issued its final Lead and Copper Rule Improvements (LCRI), marking a pivotal change in the regulation of lead in drinking water. This updated rule mandates full replacement of all lead service lines across the country within 10 years, with some limited exceptions, among other significant requirements. Notably, when a water system has access—whether legal or physical—to conduct a full replacement of lead or galvanized requiring replacement (GRR) service lines, it is considered to have control over the service line and must replace it under the LCRI.

Funding: The Bipartisan Infrastructure Law provides $50 billion to support upgrades to the nation's drinking water and wastewater infrastructure. This includes $15 billion over five years dedicated to lead service line replacement and $11.7 billion of general Drinking Water State Revolving Funds that can also be used for lead service line replacement.

For Mueller, the lead service line replacement mandate is particularly significant because of the company's brass products business. Every lead service line that gets replaced requires new brass fittings, valves, and connections. Mueller's lead-free brass products are positioned to capture this regulatory-driven demand.

Mueller Co. offers all of its waterworks brass products in low-lead varieties.

IX. Current Financial Performance & Recent Developments

Mueller's fiscal 2025 results (year ending September 30, 2025) demonstrated the company's operational momentum. Increased net sales 9.4% to $380.8 million as compared with $348.2 million in the prior year quarter. Mueller Water Products, Inc. (NYSE: MWA), a leading manufacturer and marketer of products and solutions used in the transmission, distribution and measurement of water in North America, announced financial results for its fourth quarter and fiscal year ended September 30, 2025.

Increased net sales 9.4% to $380.8 million as compared with $348.2 million in the prior year quarter. Reported operating income of $69.6 million as compared with $28.4 million in the prior year quarter, and increased adjusted operating income 39.6% to $78.9 million as compared with $56.5 million in the prior year quarter. Reported operating margin of 18.3% as compared with 8.2% in the prior year quarter, and increased adjusted operating margin to 20.7% as compared with 16.2% in the prior year quarter. Generated net income of $52.6 million as compared with $10.0 million in the prior year quarter, with net income margin of 13.8% as compared with 2.9% in the prior year quarter.

For the full year, gross margin was 36.1%, an increase of 120 basis points compared with the prior year, which is a record level for Mueller. The improvement was driven by manufacturing efficiencies and increased volumes, which more than offset the impact from higher tariffs.

The balance sheet has strengthened materially. As of September 30, 2025, Mueller Water Products had $451.6 million of total debt outstanding and $431.5 million of cash and cash equivalents, resulting in a debt leverage ratio of 1.4x and net debt leverage ratio of 0.1x. We did not have any borrowings under our ABL Agreement at the end of the fourth quarter, nor did we borrow any amounts under our ABL during the year. There are no maturities on the Company's debt financings until June 2029 and its 4.0% Senior Notes have no financial maintenance covenants.

That 0.1x net debt leverage ratio is remarkable for a company that emerged from the Walter Industries acquisition laden with debt. Over 15 years, Mueller has systematically deleveraged while maintaining investment in growth initiatives.

Looking forward, management provided guidance for fiscal 2026. The Company is introducing its fiscal 2026 consolidated net sales guidance to be between $1,450 million and $1,470 million, or an increase of 1.4% to 2.8% compared with the prior year.

As it relates to our 2026 sales guidance, we have contemplated slightly positive volumes, and that's predicated on expecting a slowdown that we started to see in the fourth quarter with residential construction. We're contemplating that residential construction will be down in the high single-digit range, and Muni repair and replacement growth will be in the low single-digit to mid-single-digit range, and project-based specialty valves will be in the mid-single-digit to high single-digit range. We're expecting that both the Muni repair and replacement and the specialty valves will more than offset the slowdown that will be seen in the residential construction.

The CEO transition announced in November 2025 represents an important leadership moment. Mueller Water Products (NYSE: MWA) announced a planned CEO succession: President and COO Paul McAndrew will become President and Chief Executive Officer effective at the annual shareholders meeting on February 9, 2026. He has been nominated to join the Board. Martie Edmunds Zakas will retire as CEO and as a Board member on that date after a 19-year career and will serve as a Senior Advisor through December 31, 2026 to support transition.

Paul McAndrew has been the Company's Chief Operating Officer since August 2023 and was also named President in May 2024. He is a seasoned global operating executive with strong leadership experience in operations, engineering and sales. Prior to joining Mueller in 2022, Mr. McAndrew worked at Emerson as a Vice President and General Manager of Professional Tools where he held full P&L responsibility and leadership across all functions, including sales and marketing, product management and engineering, operations and supply chain and human resources. Mr. McAndrew also played a pivotal role in Emerson's successful acquisition of Textron's Tools and Test business, Greenlee, in 2018.

The transition is effective on February 9, 2026, when Paul McAndrew becomes President and Chief Executive Officer. Paul McAndrew will receive a $915,000 base salary, a target bonus equal to 100% of salary for FY2026, and a target LTI equal to 370% of salary, split 25% options, 25% RSUs, 50% PRSUs.

InvestingPro data shows Mueller has raised its dividend for 11 consecutive years and maintained dividend payments for 20 consecutive years, with a current yield of 1.07%.

X. Competitive Landscape & Strategic Analysis

Porter's Five Forces Analysis

Threat of New Entrants: LOW

MWP is the only manufacturer of valves and hydrants that utilizes the lost-foam casting process. This manufacturing capability, combined with 167 years of accumulated know-how in foundry operations, creates significant barriers. New entrants would need to invest hundreds of millions in manufacturing facilities, develop relationships with thousands of municipalities, achieve the certifications required for municipal water products, and overcome the specification advantage that incumbents enjoy.

The certification requirements alone are formidable. Municipal water products must meet stringent testing and approval standards before utilities will specify them. These certifications take years to achieve and represent significant R&D investment.

In the decades since Hieronymus Mueller created his eponymous water products company, Mueller Water Products has grown to serve some of North America's largest utilities, with its products being specified by the United States' 100 largest metropolitan areas.

Bargaining Power of Suppliers: MODERATE

Mueller's raw materials—brass, iron, steel—are commoditized inputs subject to price fluctuations. The company has demonstrated ability to manage these costs through recycled material usage (the company reports using approximately 95% recycled metal in production) and strategic sourcing. However, specialty inputs and electronic components for smart products can create constraints.

Bargaining Power of Buyers: MODERATE-LOW

Mueller's customers are primarily municipalities and water utilities with inelastic demand—water is essential, and infrastructure must be maintained. Products are often specified in infrastructure projects; once specified, alternatives are limited. Long replacement cycles (measured in decades) create loyalty and lock-in.

Price sensitivity exists but is balanced by quality and reliability requirements. A failed valve or hydrant in a municipal water system creates public safety hazards and political embarrassment—factors that reduce price sensitivity.

Threat of Substitutes: VERY LOW

There is no substitute for fire hydrants, gate valves, or water distribution infrastructure. Cities need these products, full stop. Technology upgrades (smart meters, sensors, pressure management systems) represent evolution rather than substitution—and Mueller is positioned to capture that evolution through its Sentryx platform.

Competitive Rivalry: MODERATE

In North America, significant direct competitors for utility water meters and radio products include Sensus, a Xylem company, Neptune Technology Group Inc., Master Meter, Inc., and Mueller Water Products, Inc.

Market concentration is moderate, with a handful of global manufacturers, Badger Meter, Kamstrup, Neptune, Diehl, and Xylem, controlling most large tenders. Competitive differentiation hinges on analytics depth, cybersecurity credentials, and service models rather than meter hardware alone.

Badger Meter, Gorman Rupp, Franklin Electric Co, RWC Global, and Trane Technologies are some of the 40 competitors of Mueller Water Products.

The competitive landscape varies by product category. In fire hydrants and gate valves, Mueller faces limited direct competition and enjoys strong market share. In metering and technology, competition is more intense, with Badger Meter and Xylem's Sensus brand as significant players.

Hamilton Helmer's 7 Powers Framework

Mueller's strategic position can be analyzed through Helmer's framework:

Process Power: Mueller's lost-foam casting expertise and integrated manufacturing capabilities create cost advantages that competitors cannot easily replicate. The company's 167-year manufacturing heritage represents embedded learning that would take decades to reproduce.

Scale Economies: As the largest manufacturer of fire hydrants in North America, Mueller achieves scale efficiencies in production, distribution, and R&D that smaller competitors cannot match.

Switching Costs: Once a municipality standardizes on Mueller products, switching involves retraining maintenance crews, renegotiating specifications, and managing compatibility issues across decades of installed infrastructure. These switching costs deepen over time as more Mueller products enter the installed base.

Network Effects: Mueller's Sentryx platform creates potential network effects—as more utilities adopt the platform and share data, the analytics capabilities improve, making the platform more valuable for all participants. This is nascent but represents strategic optionality.

Cornered Resource: Mueller's specification acceptance with the 100 largest U.S. metropolitan areas represents a form of cornered resource. These specifications, built over decades of performance and relationship-building, cannot be easily duplicated.

Branding: In municipal water infrastructure, the Mueller brand carries significant weight. Utility engineers know the name, trust the quality, and often default to Mueller when writing specifications.

Counter-Positioning: Mueller's digital transformation represents a potential counter-positioning move—investing in capabilities that traditional pure-play manufacturers cannot easily replicate.

XI. Key KPIs and Investment Considerations

For investors monitoring Mueller's ongoing performance, three metrics stand out as most critical:

1. Municipal Repair & Replacement Growth Rate This metric captures the core demand driver for Mueller's products—municipal spending on water infrastructure maintenance. Unlike residential construction (which is cyclical) or new infrastructure (which depends on federal funding timing), municipal repair and replacement represents steady, recurring demand that tracks the aging of America's installed water base. Management's guidance suggests low-to-mid single-digit growth in this category for FY2026.

2. Adjusted EBITDA Margin Mueller's margin expansion over the past several years reflects operational improvements, pricing power, and manufacturing efficiencies. For the full year, gross margin was 36.1%, an increase of 120 basis points compared with the prior year, which is a record level for Mueller. Continued margin expansion would validate the company's strategic positioning and operational execution.

3. Technology Segment Revenue and Profitability Mueller's digital transformation thesis depends on the technology business scaling profitably. Historically, this segment has required significant investment and operated at losses. Investors should track whether technology revenue growth translates into improved segment profitability over time.

Bull Case

The bull case rests on several pillars: America's $1+ trillion water infrastructure crisis creates decades of demand; EPA's lead service line replacement mandate creates immediate regulatory-driven demand for Mueller's brass products; the Sentryx platform positions Mueller to capture the smart water opportunity; the company's near-zero net leverage provides M&A and investment firepower; and the transition to Paul McAndrew as CEO brings operational expertise at a time when manufacturing execution matters.

This evolution led to becoming North America's largest full-line supplier of potable water distribution products, offering everything from fire hydrants to advanced leak detection. The full-line supplier position creates switching costs and customer stickiness that should endure.

Bear Case

The bear case centers on execution risks and competitive dynamics. The technology transformation requires investments that may not generate returns for years. Competition in smart water from well-funded players like Badger Meter and Xylem could pressure margins. Federal infrastructure funding, while substantial, may take years to fully deploy. We're contemplating that residential construction will be down in the high single-digit range—and residential construction weakness could pressure near-term results.

The CEO transition, while orderly, introduces leadership uncertainty at a time when strategic execution matters. And tariff impacts on specialty products represent an ongoing headwind that management has had to manage.

Myth vs. Reality

Myth: Mueller is just a boring old manufacturing company. Reality: Mueller is transforming into a technology-enabled infrastructure provider. The Sentryx platform, acoustic leak detection, and smart hydrants represent genuine digital capabilities.

Myth: The federal infrastructure bill will immediately boost Mueller's results. Reality: Federal funding flows through multiple layers of government administration and takes years to deploy. The benefits are real but will phase in gradually.

Myth: Water infrastructure is a sleepy industry resistant to change. Reality: The industry is undergoing rapid technological transformation, with smart meters, IoT sensors, and cloud analytics reshaping how utilities operate.

XII. Conclusion: The Long View

Mueller Water Products stands at the intersection of durable competitive advantages and powerful secular tailwinds. The company's 167-year history has created manufacturing capabilities, customer relationships, and specification acceptance that would take decades to replicate. America's trillion-dollar water infrastructure crisis and EPA's lead service line mandate create decades of demand growth. And Mueller's digital transformation, while still evolving, positions the company to capture the smart water opportunity.

The numbers tell a compelling story: FY2025 net sales rose 8.7% to over $1.4B, with adjusted EPS up 36.5% to $1.31. The balance sheet is the strongest in the company's public history, with near-zero net leverage and no debt maturities until 2029.

"Paul has been a key member of the management team for the last three years, including as President and COO. He has played a central role in improving our organization, its operations and our financial success. Paul has a deep understanding of our industry and culture, and he has developed strong employee and customer relationships."

The leadership transition to Paul McAndrew introduces execution risk but also brings operational expertise from Emerson's industrial equipment businesses—experience that could accelerate Mueller's manufacturing and supply chain improvements.

The company was founded in 1857 by Hieronymus Mueller, a German immigrant who evolved to a career as an inventor and entrepreneur. Creating new and innovative products from faucets to sporting goods, Mr. Mueller and his sons obtained over 500 patents for various inventions. Over time, Hieronymus settled on water distribution products, having invented water pressure regulators, the first sanitary drinking fountain, and a method to "hot tap" pressurized water and gas lines using a machine that remains the industry standard to this day with only slight modifications.

Hieronymus Mueller fled revolutionary Germany with nothing but his skills as a machinist and his inventor's restlessness. Over the next 167 years, his successors built his small-town gun shop into North America's leading water infrastructure company—a business that literally touches every glass of water Americans drink.

The fire hydrant standing sentinel on your street corner? There's a good chance it was made in Albertville, Alabama, by a company whose innovations still protect the Panama Canal. That's the kind of legacy—and the kind of competitive moat—that endures across generations.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube